Standard and Itemized Deductions

1

1040 Page 2

2

Standard Deduction• A set dollar amount based on filing status that is

subtracted from taxpayers income.o Lowers tax liabilityo Important to choose the correct filing status

3

Filing Status Standard Deduction 2014

Single $6,200

Married Filing Separately $6,200

Head of Household $9,100

Married Filing Jointly $12,400

Qualified Widow(er) $12,400

Itemized Deduction• A taxpayer may use eligible expenses in place of

the standard deduction to lower their taxable income and possibly their tax liability.

• Taxpayers will take the greater of their itemized expenses or the standard deduction

• State and local tax refunds become taxable income for the following tax year.

• If MFS, both parties must agree to both take the standard deduction or both take itemized deductions

4

Intake and Interview Form

5

6

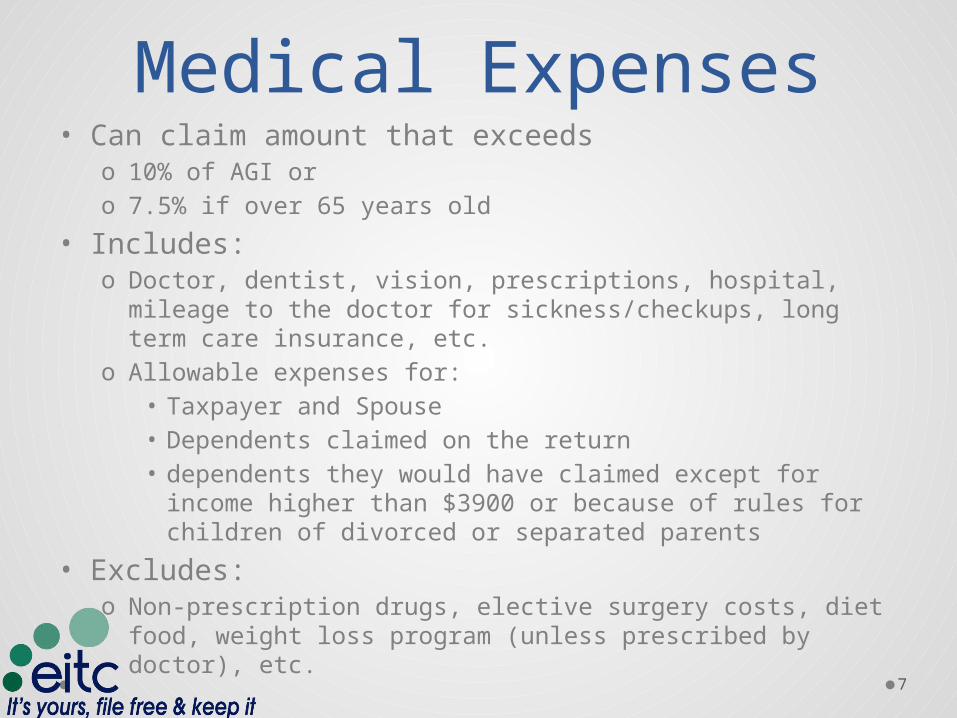

Medical Expenses• Can claim amount that exceeds

o 10% of AGI or o 7.5% if over 65 years old

• Includes: o Doctor, dentist, vision, prescriptions, hospital, mileage to

the doctor for sickness/checkups, long term care insurance, etc.

o Allowable expenses for:• Taxpayer and Spouse• Dependents claimed on the return• dependents they would have claimed except for

income higher than $3900 or because of rules for children of divorced or separated parents

• Excludes: o Non-prescription drugs, elective surgery costs, diet food,

weight loss program (unless prescribed by doctor), etc. 7

Schedule A Detail

8

Taxes• Includes:

o State and Local Taxes, Real estate taxes paid, personal property tax

• Excludes: o License fees for cars, Services that are included in Real

estate taxes paid (i.e. sewer, trash pickup)

• Tip: o Any local and state tax refunds received when a person

itemizes, must be claimed as income in the following tax year since it was taken as a deduction.

9

Interest Paid• Includes:

o Mortgage Interest on 1st and 2nd home, Points paid when mortgage taken out, mortgage insurance premiums - all will be shown on 1099 statement from bank

• Excludes: o credit card, pay day loan interest paid

10

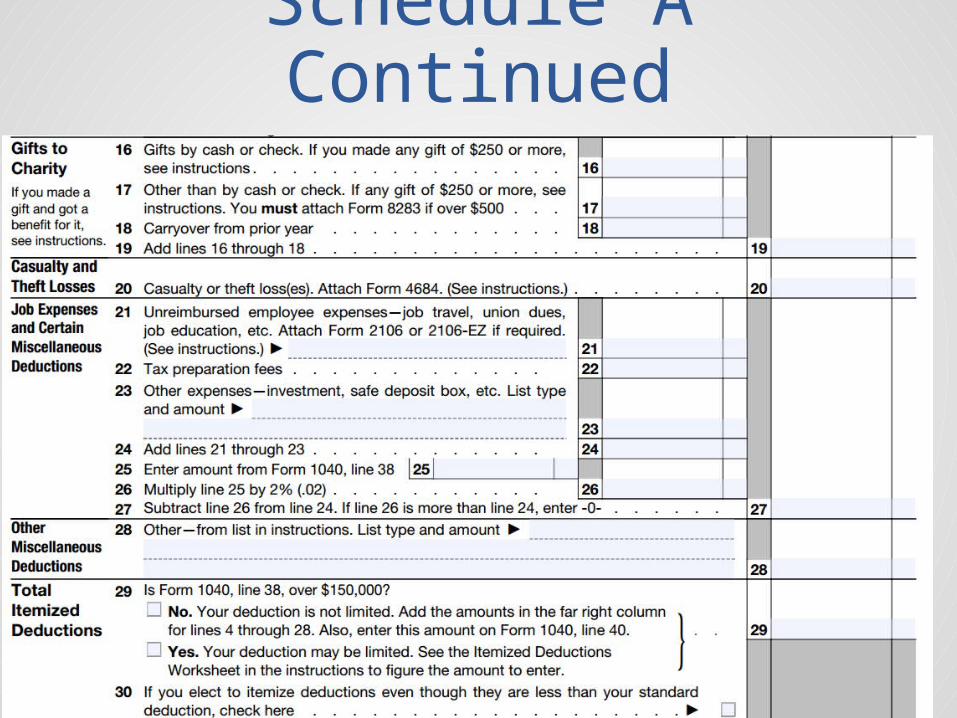

Schedule A Continued

11

Gifts to Charity• Includes:

o Cash, Non-Cash donations (up to $500)o Volunteer mileage or gas, parking, tolls, required uniform

expenses (need receipts)

• Need receipts to show donations• Non-cash donations of $500 or higher are out of

scopeo Refer to a professional

12

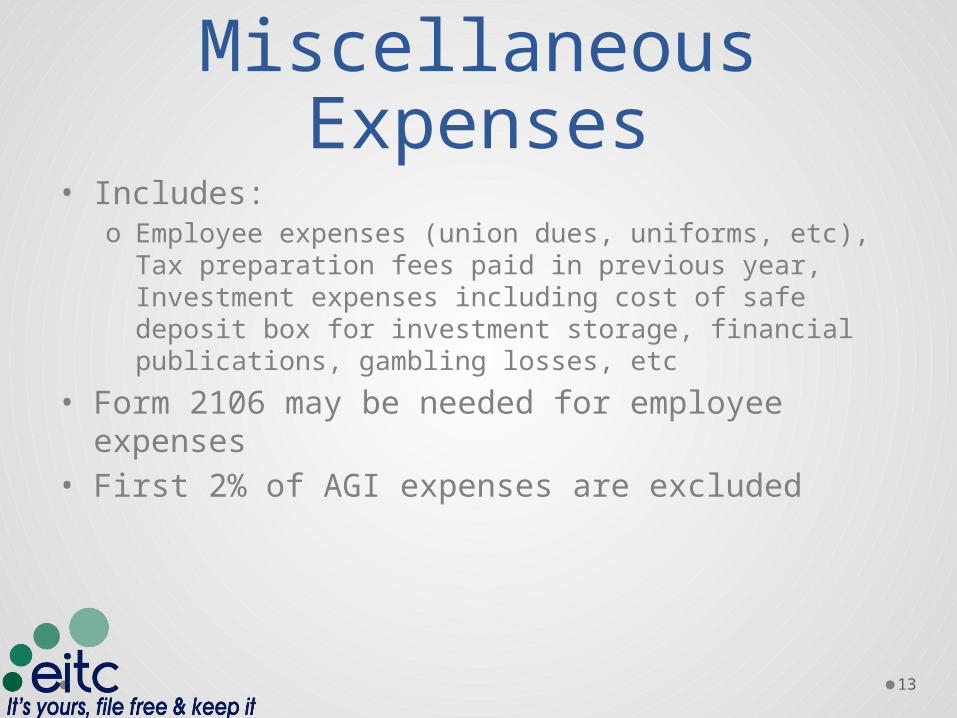

Miscellaneous Expenses

• Includes: o Employee expenses (union dues, uniforms, etc), Tax

preparation fees paid in previous year, Investment expenses including cost of safe deposit box for investment storage, financial publications, gambling losses, etc

• Form 2106 may be needed for employee expenses

• First 2% of AGI expenses are excluded

13

Exercise• $1,259 in out of pocket medical paid• $1,120 in real estate taxes• $2,003 in mortgage interest paid• $1,800 paid to their church• $200 in gambling losses• $178 local tax paid• $535.50 state tax paid

• The taxpayer will file single and has an AGI of $17,850. $850 of that is gambling winnings. Should they itemize or take the standard deduction?

14

Tips for Itemizing• Walk through the exercise if client has several of

the eligible expenses o sometimes some expenses like local taxes and state

taxes paid are overlooked to push the taxpayer over standard amount

• Some medical expenses carry over to the state return to benefit the taxpayero Include all medical even if it doesn’t meet the 10% or

7.5% rules.

• Publication 4012 has detailed charts for walking through itemizing as a helpful reminder

15

Recommended