The Balance Sheet

The balance sheet, together with the income statement and cash flow statement, make up the cornerstone of any company’s financial statements.

The Balance Sheet

• Also known as a “statement of financial position”

• Reveals a company’s assets, liabilities and owners’ equity

• A snapshot of the company’s financial position at a single point in time

• Divided into two parts that must equal, or balance each other…

The Balance Sheet

The balance sheet equation:

Assets = Liabilities + Shareholders’ Equity

The Balance Sheet

• Assets are equal to the sum of the company’s equity investment or capitalization, plus retained earnings, minus any current financial obligations or debt.

• Assets are what a company uses to operate its business, while its liabilities and equity are two sources that support these assets.

• Owner or shareholder equity is the amount of money initially invested into the company plus any retained earnings and it represents a source of funding for the business.

Ratios

Debt-to-Equity Ratio

• A measure of a company’s financial leverage

• Calculated by dividing total liabilities by shareholders’ equity

• Indicates what proportion of equity and debt the company is using to finance its assets.

Debt-to-Equity Ratio

Debt-to-Equity equation:

Total liabilities ÷ Shareholder equity

• Sometimes only interest-bearing, long-term debt is used instead of total liabilities in the calculation

• This ratio can be applied to personal financial statements as well as corporate ones

Debt-to-Equity Ratio

• A measure of a company’s financial leverage

• Calculated by dividing total liabilities by shareholders’ equity

• Indicates what proportion of equity and debt the company is using to finance its assets.

Quick Ratio

• An indicator of a company’s short-term liquidity

• Shows the dollar amount of liquid assets available for each dollar of current liabilities

• Measures a company’s ability to meet its short-term obligations with its most liquid assets

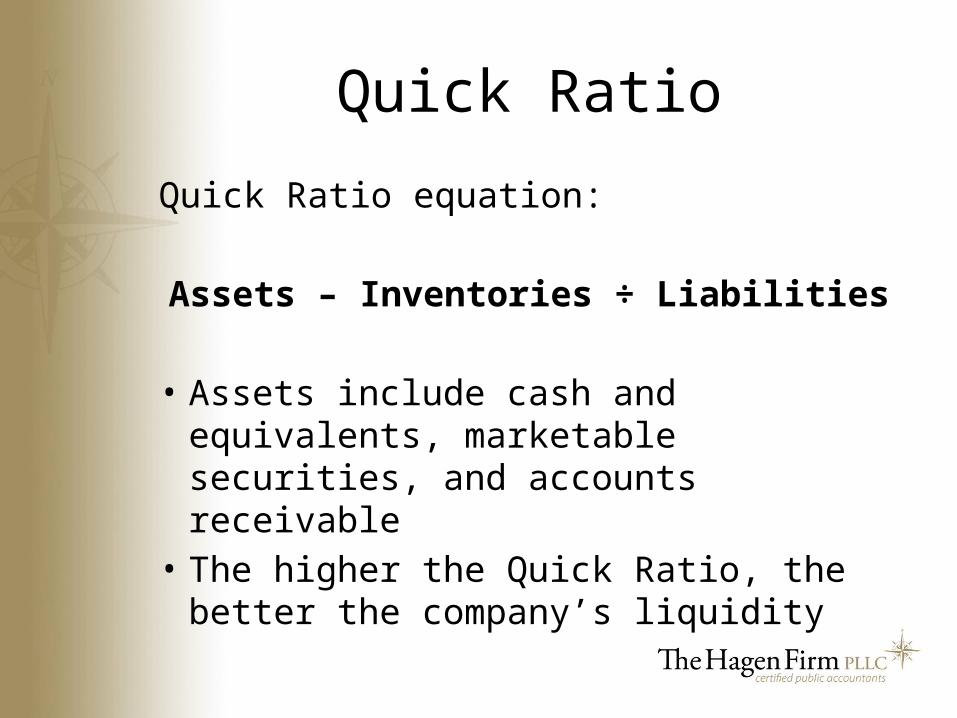

Quick Ratio

Quick Ratio equation:

Assets – Inventories ÷ Liabilities

• Assets include cash and equivalents, marketable securities, and accounts receivable

• The higher the Quick Ratio, the better the company’s liquidity

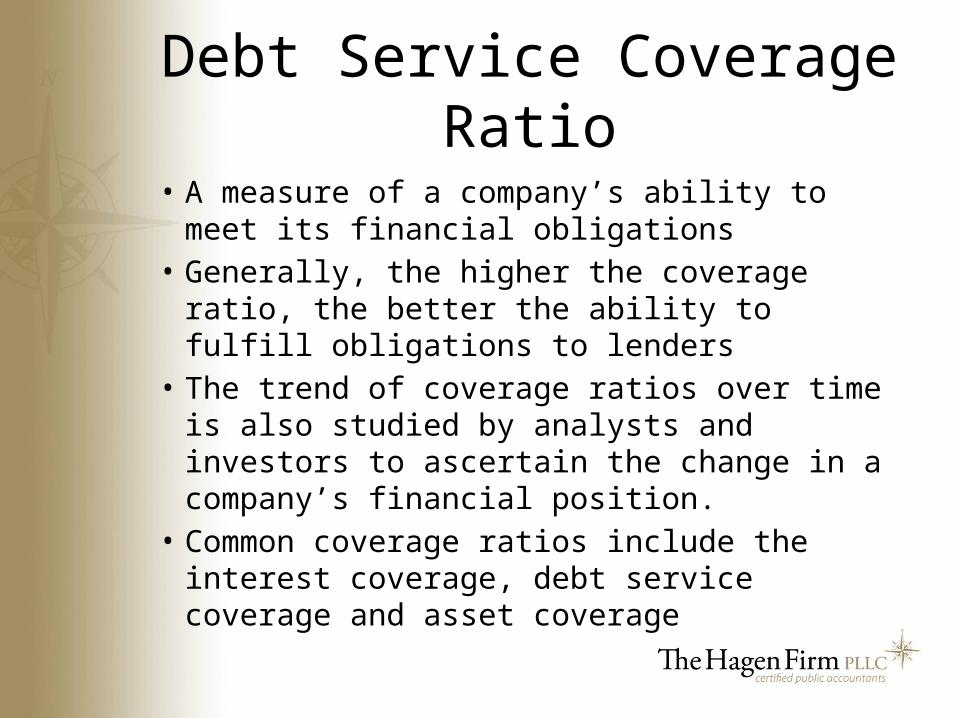

Debt Service Coverage Ratio

• A measure of a company’s ability to meet its financial obligations

• Generally, the higher the coverage ratio, the better the ability to fulfill obligations to lenders

• The trend of coverage ratios over time is also studied by analysts and investors to ascertain the change in a company’s financial position.

• Common coverage ratios include the interest coverage, debt service coverage and asset coverage

Inventory and Sales

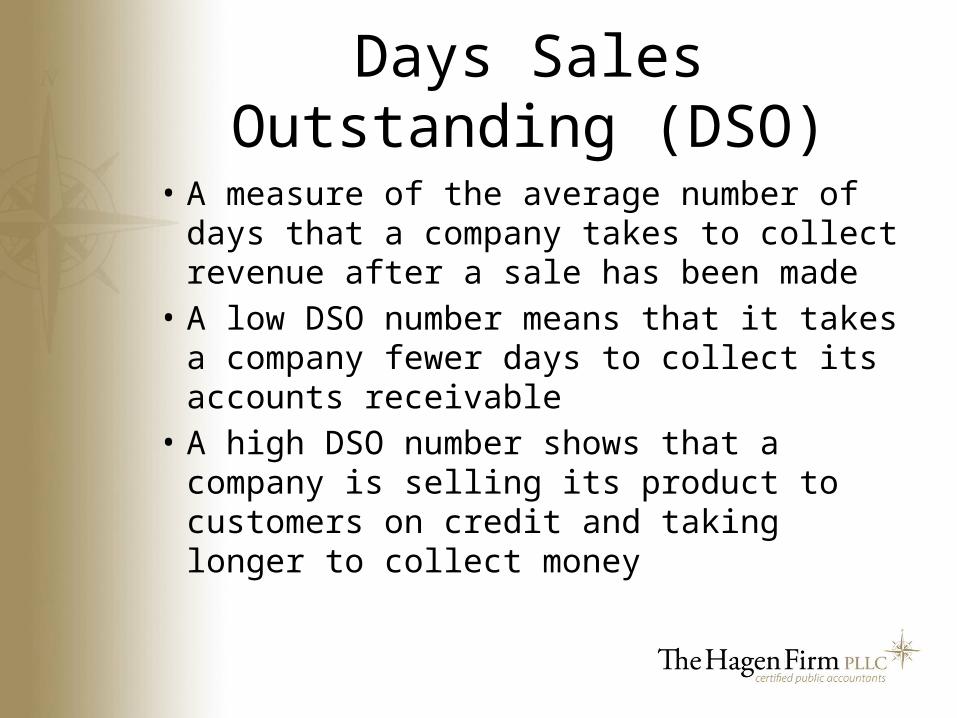

Days Sales Outstanding (DSO)

• A measure of the average number of days that a company takes to collect revenue after a sale has been made

• A low DSO number means that it takes a company fewer days to collect its accounts receivable

• A high DSO number shows that a company is selling its product to customers on credit and taking longer to collect money

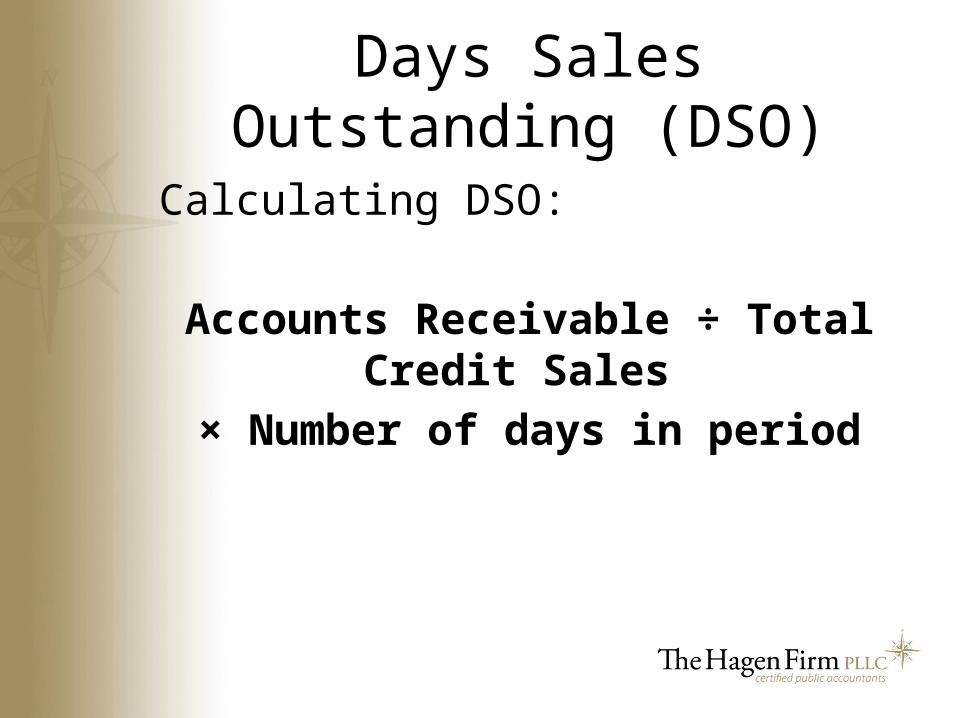

Days Sales Outstanding (DSO)

Calculating DSO:

Accounts Receivable ÷ Total Credit Sales × Number of days in period

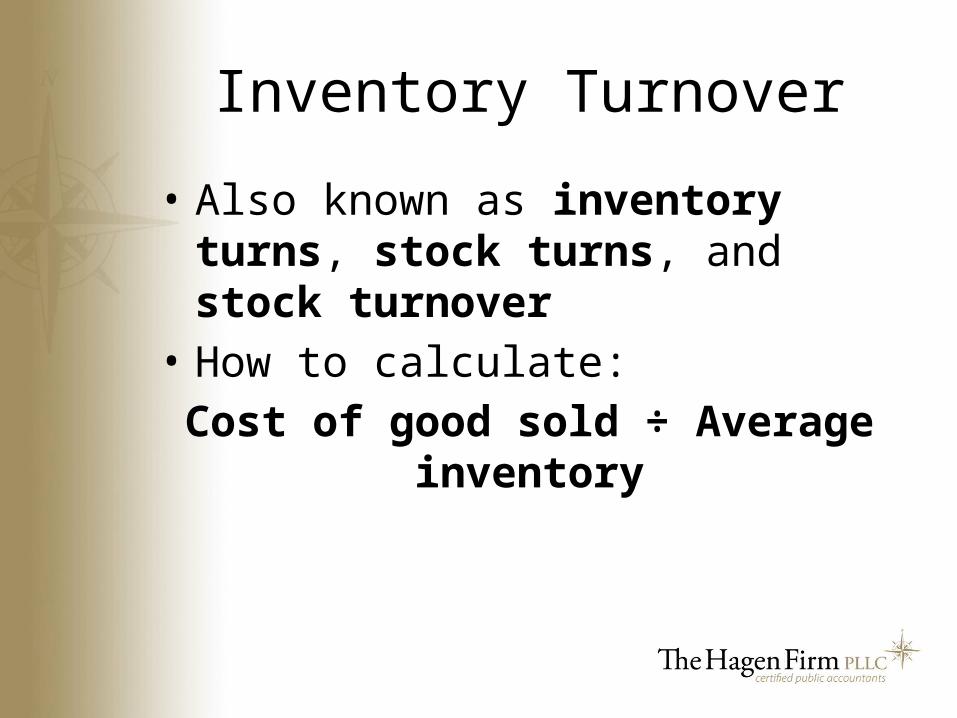

Inventory Turnover

• Also known as inventory turns, stock turns, and stock turnover

• How to calculate:Cost of good sold ÷ Average inventory

Inventory Turnover

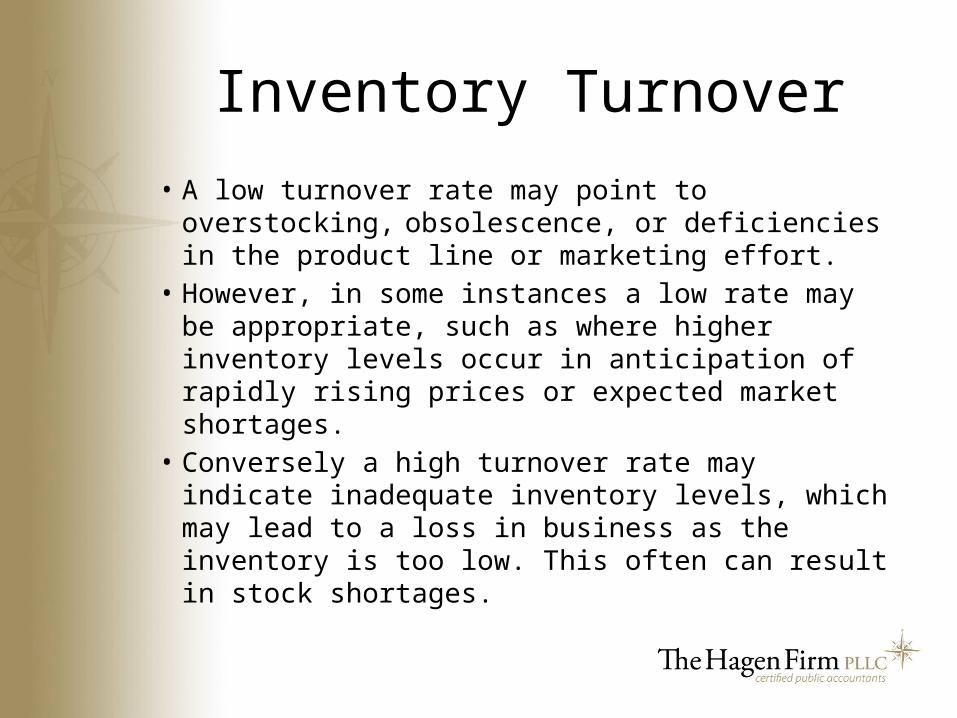

• A low turnover rate may point to overstocking,

obsolescence, or deficiencies in the product line or marketing effort.

• However, in some instances a low rate may be appropriate, such as where higher inventory levels occur in anticipation of rapidly rising prices or expected market shortages.

• Conversely a high turnover rate may indicate inadequate inventory levels, which may lead to a loss in business as the inventory is too low. This often can result in stock shortages.

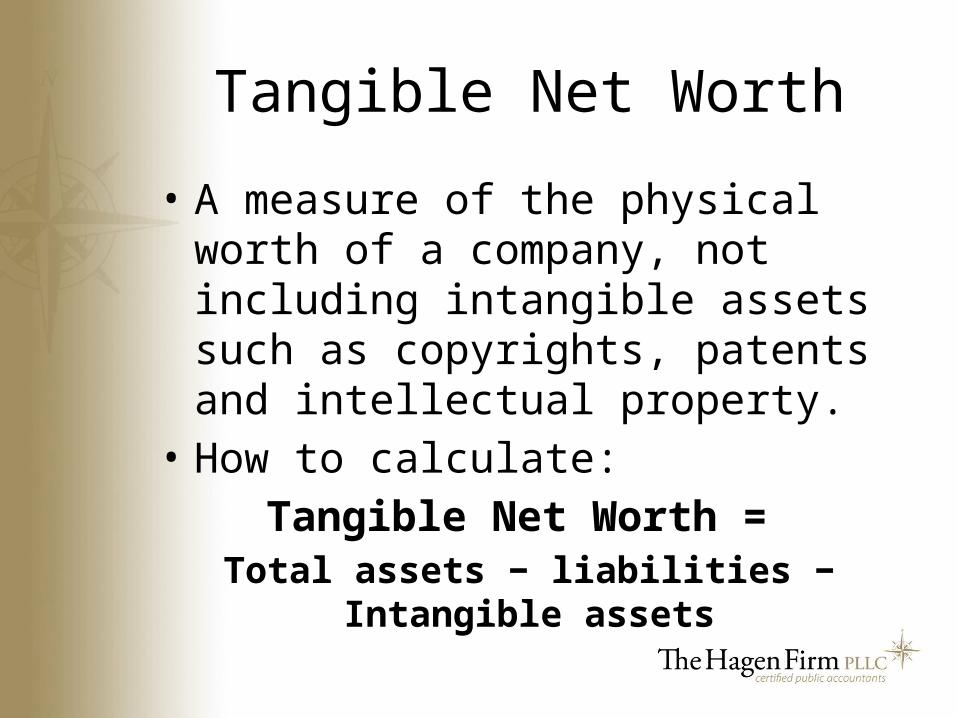

Tangible Net Worth

• A measure of the physical worth of a company, not including intangible assets such as copyrights, patents and intellectual property.

• How to calculate:Tangible Net Worth =

Total assets − liabilities − Intangible assets

Gross Margins

• [Add your content here…]

Contribution Margins

• [Add your content here…]

Subtopics…

• [Add your content here…]

Subtopics…

Subtopics…

Recommended