THE INFLUENCE OF ETHICAL WORK CLIMATE

(EWC) AND DEMOGRAPHIC VARIABLES ON

AUDITORS’ ETHICAL EVALUATION

SKRIPSI

By

Devi Selena

008201200053

presented to the

Faculty of Business President University

in partial fulfillment of the requirements for

Bachelor Degree in Economics Major in Accounting

President University

CikarangBaru – Bekasi

Indonesia

2016

iv

ABSTRACTS

Ethics are considered to be important in audit practice. The intensive

works lead ethical dilemma, especially when there is no exact rules exist.

Researchers have responded by attempting to investigate and analyze the ethical

behavior. While each ethical reasoning process is important, the ability of

auditors to evaluate ethical problems (second phase of Rest’s ethical reasoning

process) that may not be obvious should be studied and understood. This study

will indentify the influence of ethical work climate (EWC) and specified

demographic variables (age, gender, and length of experience) on ethical

evaluation. The climate of accounting public firm is examined based on Victor

and Cullen’s ethical work climate type.

Findings in this study are based on response to scenarios that is related to

cost and time pressures in the fieldwork such as underreporting of time (URT)

and quality threatening behavior (QTB). We targeted the respondents who work

as professional public auditors in Java Island, Indonesia. From 300 questionnaires

distributed, researcher got feedback from 283 auditors. The data is analyzed by

using structural equation model method. Structural equation method is used

because ethical evaluation and ethical work climate cannot be measured directly.

The finding revealed that ethical work climate has significant influence on

auditors’ ethical evaluation. Ethical work climate which exist in public

accounting firm in Java area is composed by six dimensions such as efficiency,

friendship, team interest, social responsibility/public interest, company rules and

procedures, and laws and professional codes climates. Specified demographic

variables are found to give insignificant influence on auditors’ ethical evaluation.

Implications of findings and areas for future research are discussed in the last

chapter.

KEY WORDS: auditors’ ethical evaluation, ethical work climate, age, gender,

length of experience, underreporting of time (URT), quality threatening behavior

(QTB).

v

ACKNOWLEDGMENT

This research is hardly to be done without the big supports from many

parties. Author would like to express my gratitude to:

1. Ida Sang Hyang Widhi Wasa for His favor and the wisdom that are given

during the thesis process.

2. Dr. Sumarno Zain, SE, Ak, M.B.A as advisor of my thesis for giving me

advice, guidance, and recommendation to collate and arrange the thesis

properly.

3. Drs. Gatot Imam Nugroho, Ak, MBA, CA and Drs. Asep Supriatna, MBA

as examiners during defense and comprehensive test for giving me

excellent experience.

4. Putu Purna Wirawan and Ni Nyoman Dwi Adnyani as my parents for their

loves and pray for my success. Nadia Indah Devianty and Made Sandika

D. as my sister and brother in law for giving inspiration during writing

thesis.

5. Ketut Dwi Adnyawati as my twin mother, Putu Venessa, and Made Wina

Sadina as my beloved cousins for helping me to correct my grammar.

6. Ongky Aristian for giving me spirit and love to finish my thesis.

7. Angelina Suryani and Geraldo Risa Maranatha for helping me in

distributing my questionnaires to public accounting firms.

8. Wratsari Windrawati W., Tasya Firsty Annissa, and Deviani Riasari

Nalurita as my roommates for encouraging me when I am feeling down.

9. Daisy Wijaya and Prasetio Nur as my best senior for giving guidance in

each obstacle that I have found in university life.

10. Febru Aulia Ramadhani and Nursa Sherli Yoanita as my beloved team in

competition for attending and support me during defense.

11. Natasya, Ariana, Adam Maulana Akbar, Merinda, Melisa Anggreni, and

Vania Marleen for attending my defense.

12. All members in Accounting Club for encourage me and becoming my

family.

vi

13. KAP Hendrawinata Eddy Siddharta & Tanzil, KAP Mulyamin Sensi

Suryanto & Lianny, KAP Joachim Poltak Lian Michell dan Rekan, KAP

Meidina Ratna, KAP Jansen & Ramdan, KAP Drs. Bernardi & Rekan,

KAP Jojo Sunarjo & Rekan, KAP Drs. Selamat, Ak., BAP, KAP Drs.

Bambang Mudjiono & Widiarto, KAP Maurice Ganda Nainggolan, KAP

Rama Wendra, KAP Aria Kanaka & Rekan, KAP Basyiruddin & Wildan,

KAP Abdul Aziz Fiby Ariza, KAP Warnoyo, S.E., M.Si., KAP Yuwono

H., KAP Drs. Bambang Sudaryono & Rekan, KAP Effendy & Rekan,

KAP Heliantono & Rekan (Cabang Bekasi), KAP Drs. Mohammad

Yoesoef dan Rekan, KAP Moh. Mahsun, Ak, M.Si, CPA, KAP Toton

Sucipto and all external auditors as respondents for giving feedback of my

questionnaires.

14. All accounting students batch 2012.

15. All related people that cannot be mentioned one by one.

Researcher needs critics and suggestions to get better knowledge about what parts

to be improved in this research. Researcher hopes that this thesis will be useful

for the reader. Thank you.

Cikarang, 1st February 2016

Devi Selena

vii

TABLE OF CONTENTS

THE ADVISER RECOMMENDATION LETTER .............................................. i

DECLARATION OF ORIGINALITY ................................................................ ii

PANELS OF EXAMINERS APPROVAL SHEET ............................................ iii

APPROVAL SHEET ......................................................................................... iii

ABSTRACTS .................................................................................................... iv

ACKNOWLEDGMENT ...................................................................................... v

LIST OF TABLES ............................................................................................... x

LIST OF FIGURES ........................................................................................... xi

LIST OF ACRONYMS .................................................................................... xii

CHAPTER I ........................................................................................................ 1

INTRODUCTION ............................................................................................... 1

1.1. Research Background ............................................................................ 1

1.2. Problem Identification ........................................................................... 2

1.3. Statement of the Problem ....................................................................... 3

1.4. Research Objective ................................................................................ 4

1.5. Significance of the Study ....................................................................... 4

1.6. Scope and Limitation of the Study Assumption...................................... 6

1.7. Definition of Terms ............................................................................... 6

CHAPTER II ....................................................................................................... 7

LITERATURE REVIEW .................................................................................... 7

2.1. Rest’s Ethical Reasoning Process ........................................................... 7

2.2. Kohlberg Theory of Cognitive Development ......................................... 8

2.3. Ethical Work Climate Theory .............................................................. 10

2.4. Ethical Behaviors Examined ................................................................ 12

viii

2.5. Relationship between Ethical Evaluation and Ethical Work Climate

(EWC) ........................................................................................................... 13

2.6. Relationship between Ethical Evaluation and Demographics Variables 15

2.7. Theoretical Framework ........................................................................ 18

2.8. Assumption and Hypothesis ................................................................. 21

Chapter III ......................................................................................................... 22

Data Processing Method .................................................................................... 22

3.1. Research Method ................................................................................. 22

3.2. Operational Variable Identification ...................................................... 23

3.3. Data Collection Method ....................................................................... 25

3.4. Sampling Design ................................................................................. 25

3.5. Data Analysis ...................................................................................... 26

Stage 1: Defining individual constructs (Pretesting questionnaire) .............. 28

Stage 2: Developing and specifying the measurement model ...................... 28

Stage 3: Designing a study to produce empirical results .............................. 29

Stage 4: Assessing measurement model validity ......................................... 29

Stage 5: Specifying the structural model ..................................................... 33

Stage 6: Assessing the structural model validity .......................................... 33

3.6. Refining measures model ..................................................................... 34

3.6.1. Model I ......................................................................................... 34

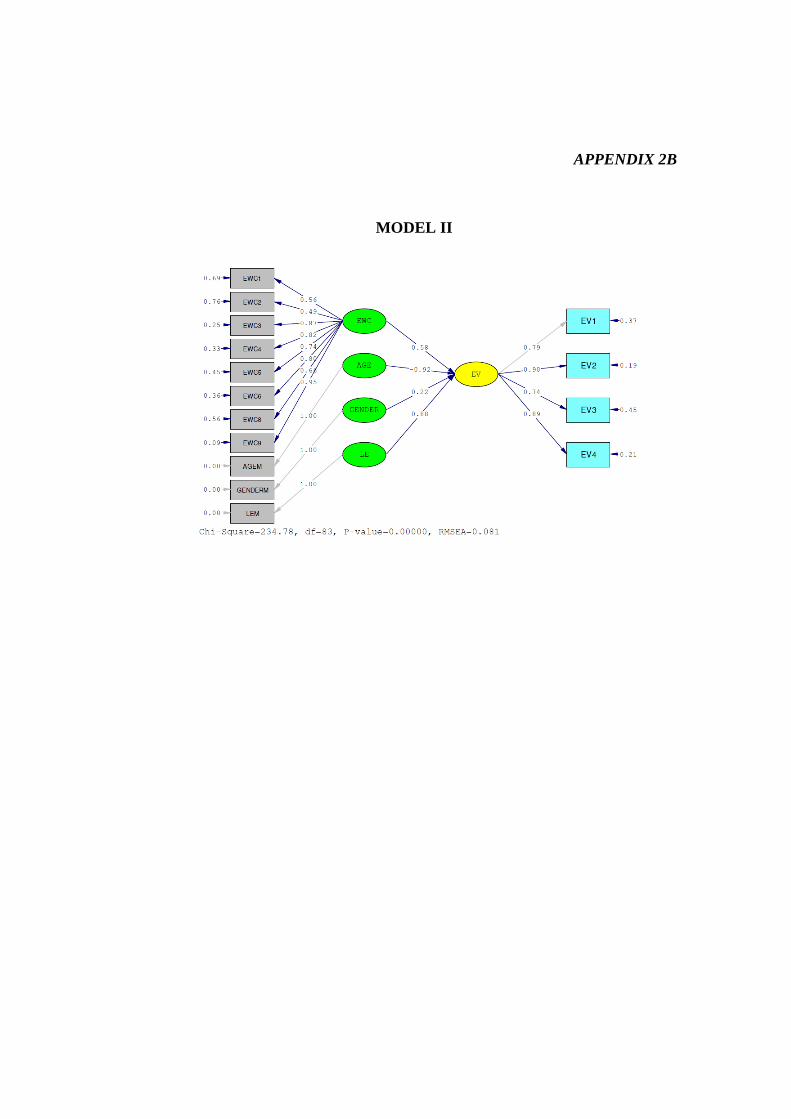

3.6.2. Model II ....................................................................................... 40

3.6.3. Model III ...................................................................................... 46

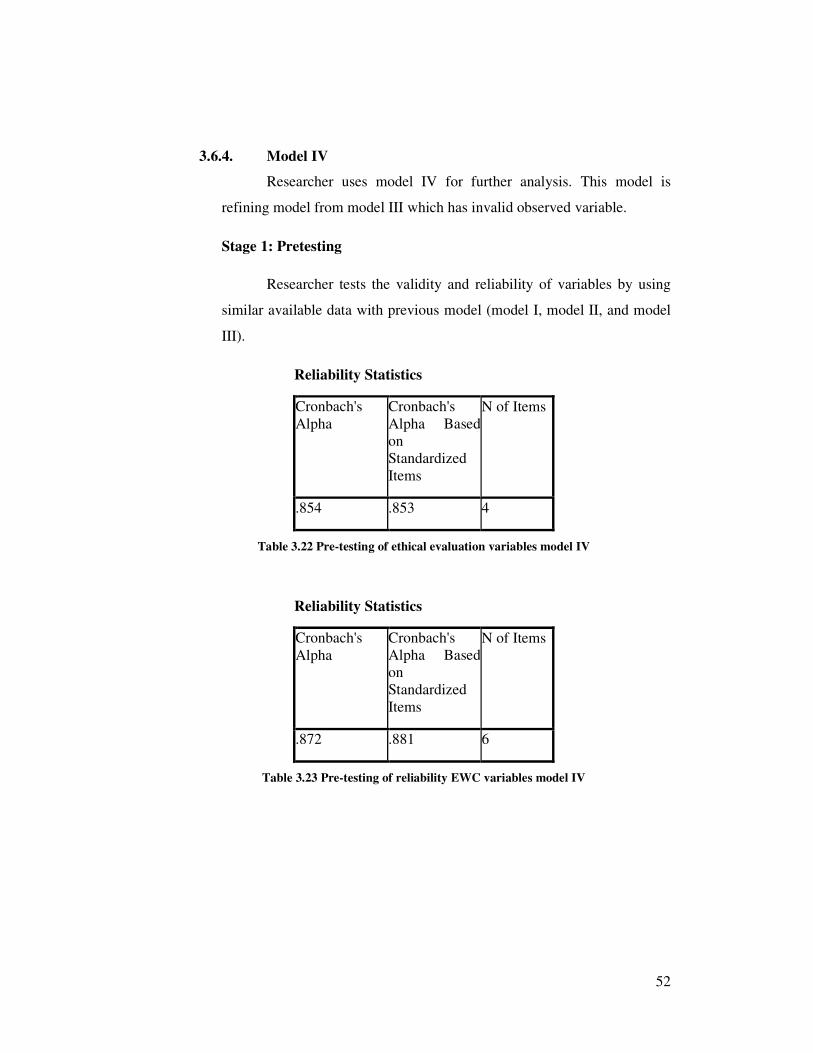

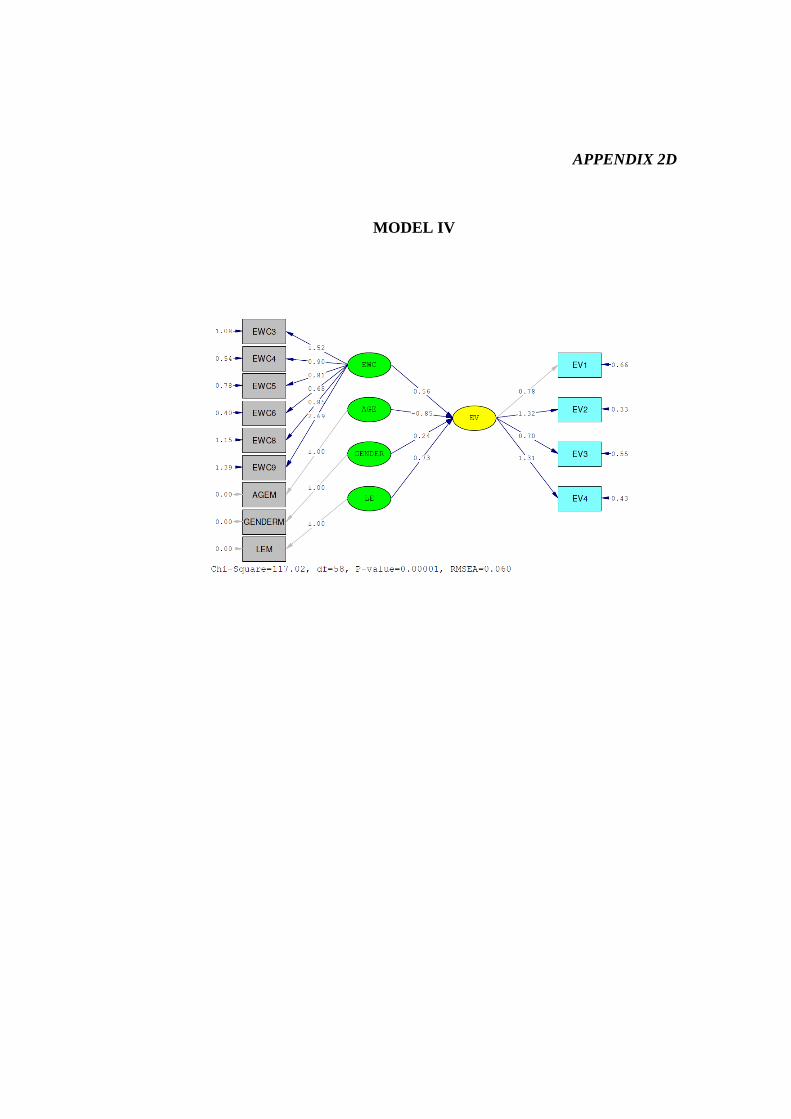

3.6.4. Model IV ...................................................................................... 52

3.7. Hypothesis Testing .............................................................................. 58

3.8. Limitations .......................................................................................... 58

CHAPTER IV.................................................................................................... 59

ix

ANALYSIS OF DATA AND INTERPRETATION OF RESULTS ................... 59

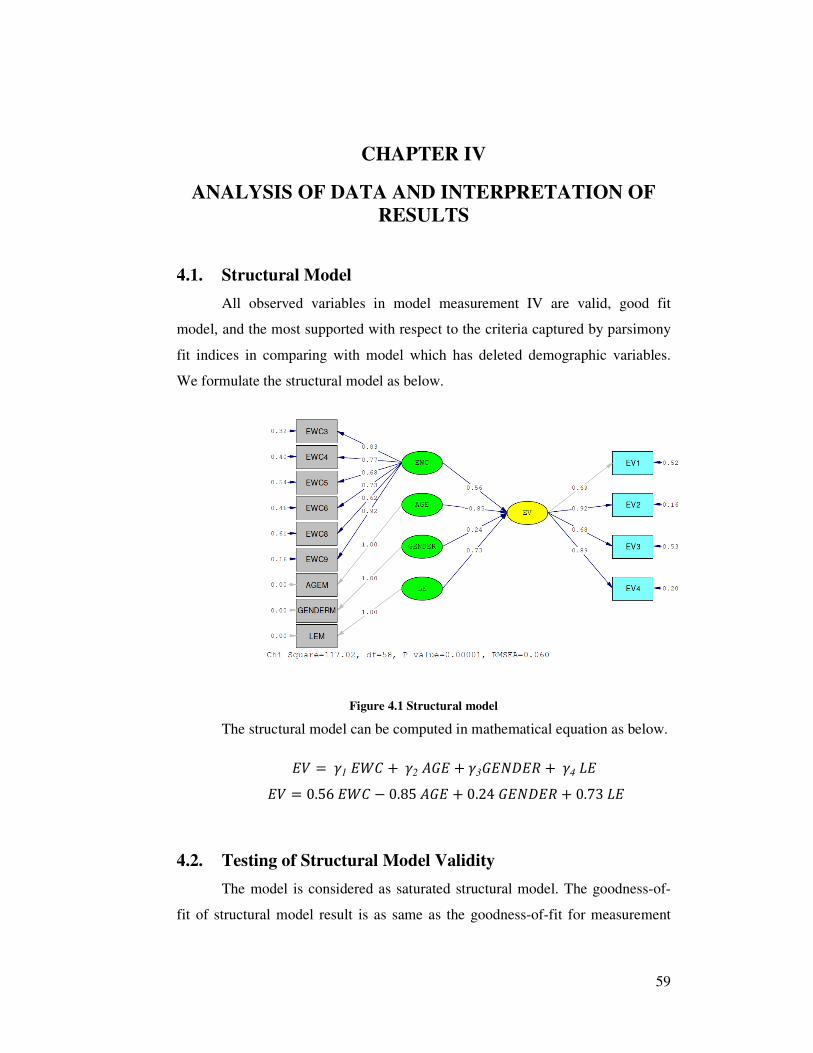

4.1. Structural Model .................................................................................. 59

4.2. Testing of Structural Model Validity.................................................... 59

4.3. Hypothesis Testing .............................................................................. 60

4.4. Data Interpretation ............................................................................... 62

4.4.1. The influence ethical work climate on ethical evaluation .............. 62

4.4.2. The influence specified demographic variables (age, gender, and

length of experience) on ethical evaluation ................................................. 63

CHAPTER V ..................................................................................................... 66

CONCLUSIONS AND RECOMMENDATIONS .............................................. 66

5.1. Conclusion .......................................................................................... 66

5.2. Recommendations ............................................................................... 66

REFERENCES

APPENDIX 1 - Definition of Terms

APPENDIX 2A - Model I

APPENDIX 2B - Model II

APPENDIX 2C - Model III

APPENDIX 2D - Model IV

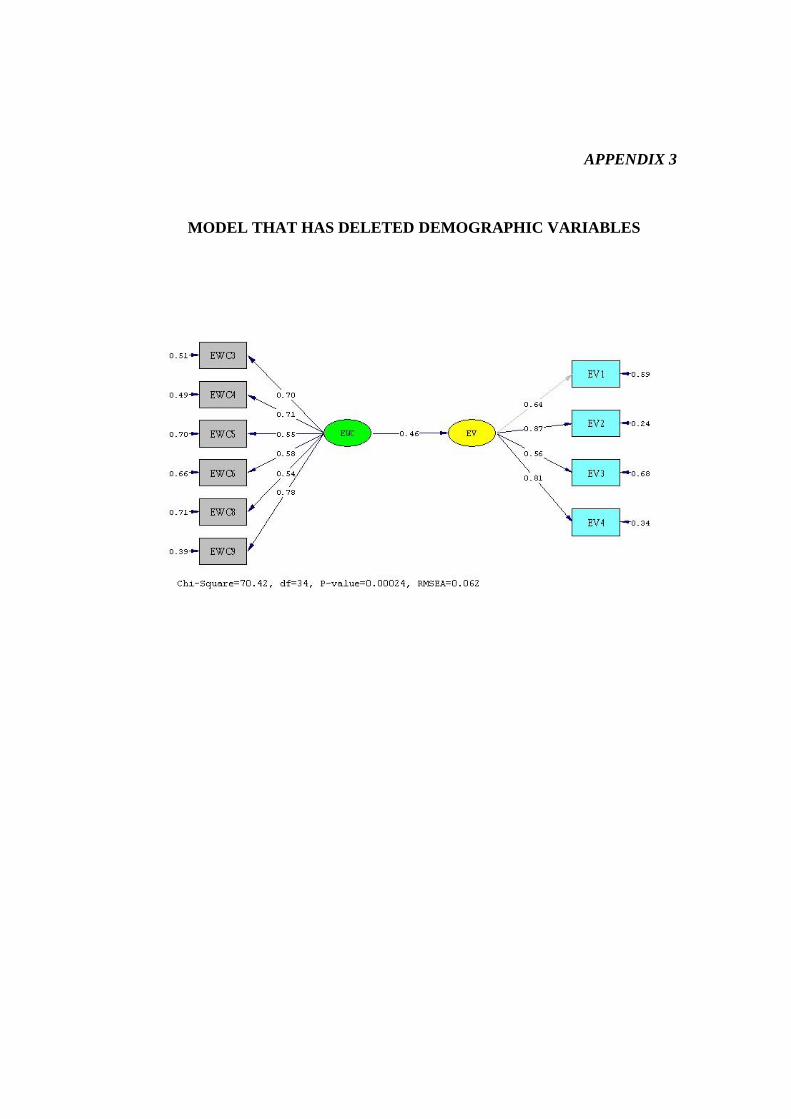

APPENDIX 3 - Model that has deleted demographic variables

APPENDIX 4 - Ethical evaluation: Means

APPENDIX 5 - Questionnaire

APPENDIX 6 - List of public accounting firms

x

LIST OF TABLES

Table 3.1 Operational variable identification ...................................................... 24

Table 3.2 Demographics details of the sample ................................................... 26

Table 3.3 Goodness-of-fit indices based on situational criterion (Hair, Black,

Babin, Anderson, & Tatham, 2006) ................................................................... 30

Table 3.4 Pre-testing of reliability ethical valuation variables model I ................ 34

Table 3.5 Pre-testing of reliability ethical work climate variables model I .......... 35

Table 3.6 Pre-testing of validity model I ............................................................ 35

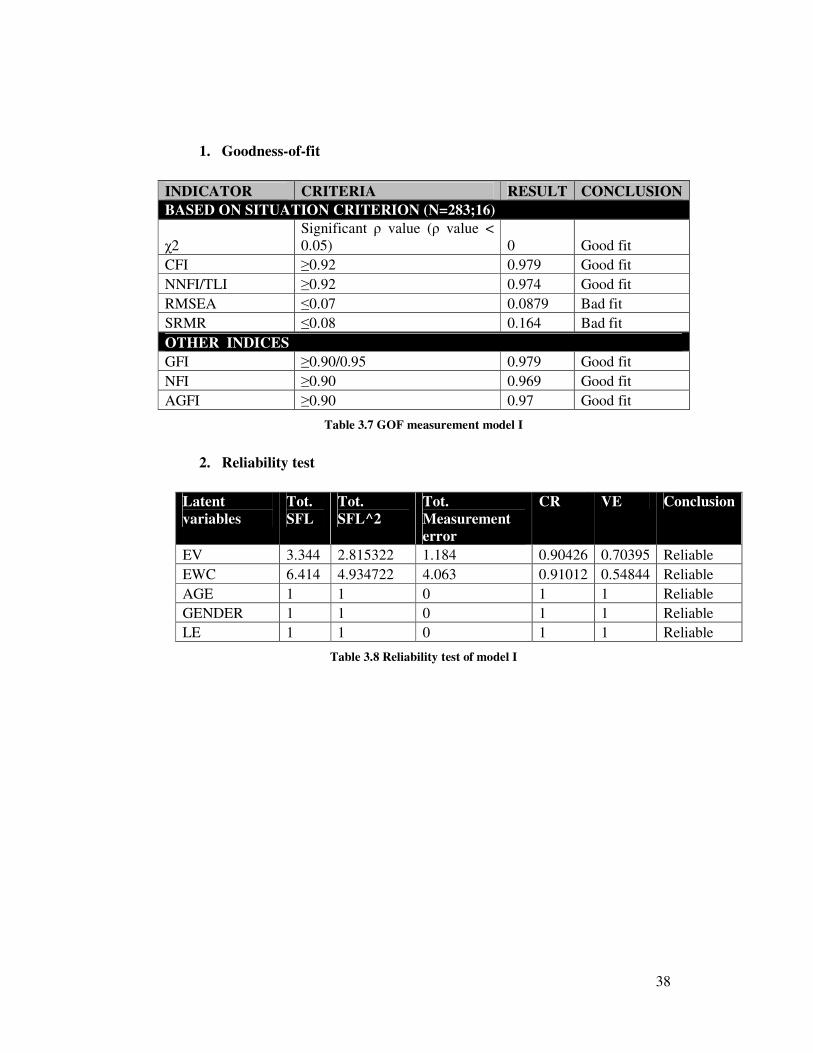

Table 3.7 GOF measurement model I ................................................................. 38

Table 3.8 Reliability test of model I ................................................................... 38

Table 3.9 Validity test of model I ....................................................................... 39

Table 3.10 Pre-testing of reliability ethical evaluation variables model II ........... 40

Table 3.11 Pre-testing of reliability ethical work climate variables model II ....... 40

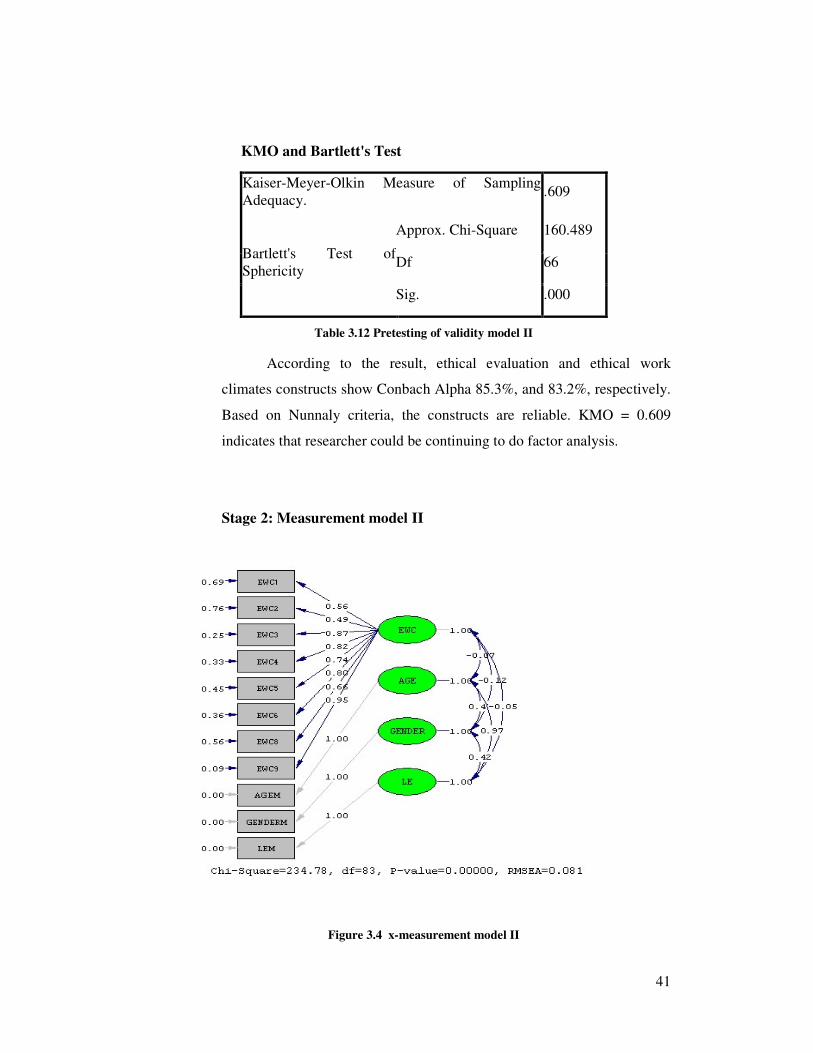

Table 3.12 Pretesting of validity model II .......................................................... 41

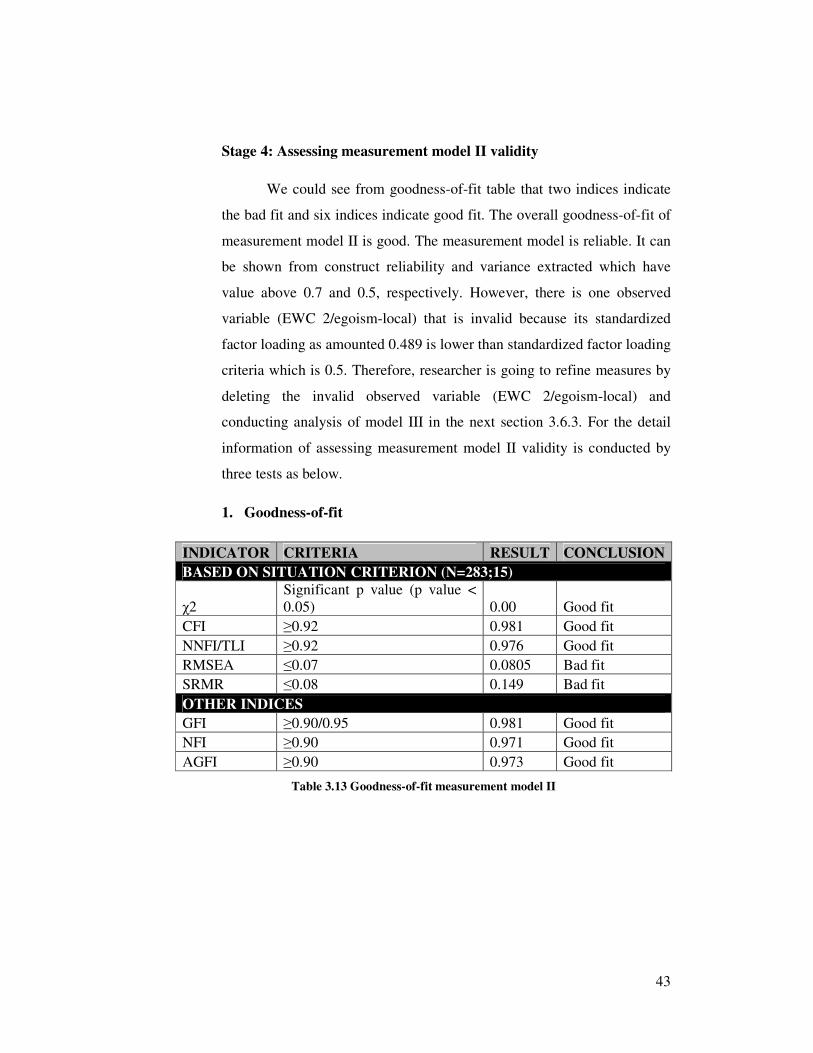

Table 3.13 Goodness-of-fit measurement model II ............................................. 43

Table 3.14 Reliability test of measurement model II .......................................... 44

Table 3.15 Validity test of model II ................................................................... 45

Table 3.16 Pre-testing of reliability ethical evaluation variables model III ......... 46

Table 3.17 Pre-testing of reliability ethical work climate variables model III ..... 46

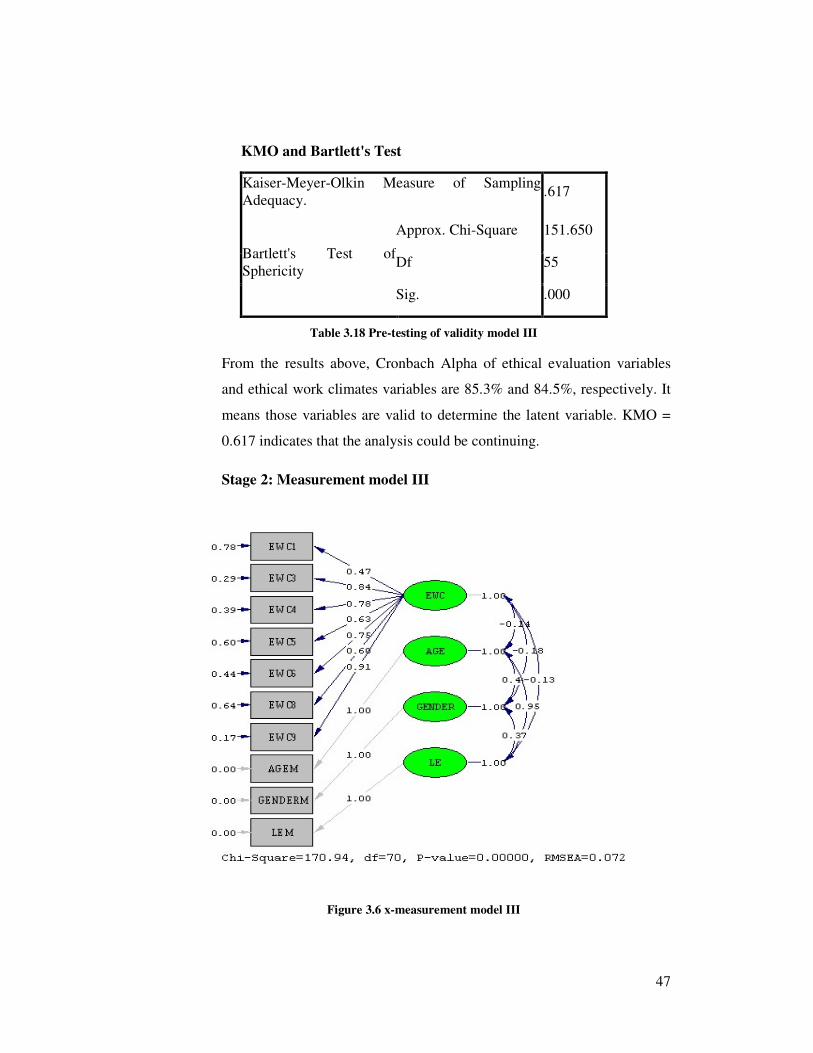

Table 3.18 Pre-testing of validity model III ........................................................ 47

Table 3.19 GOF measurement model III ............................................................ 49

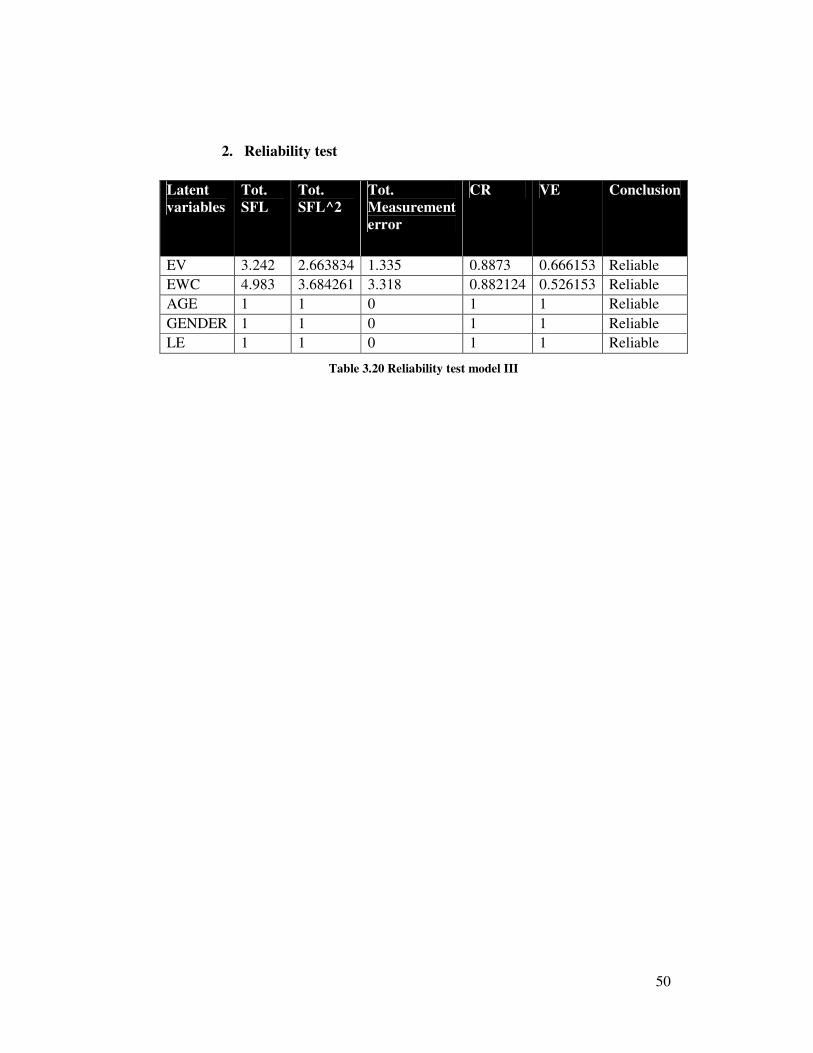

Table 3.20 Reliability test model III ................................................................... 50

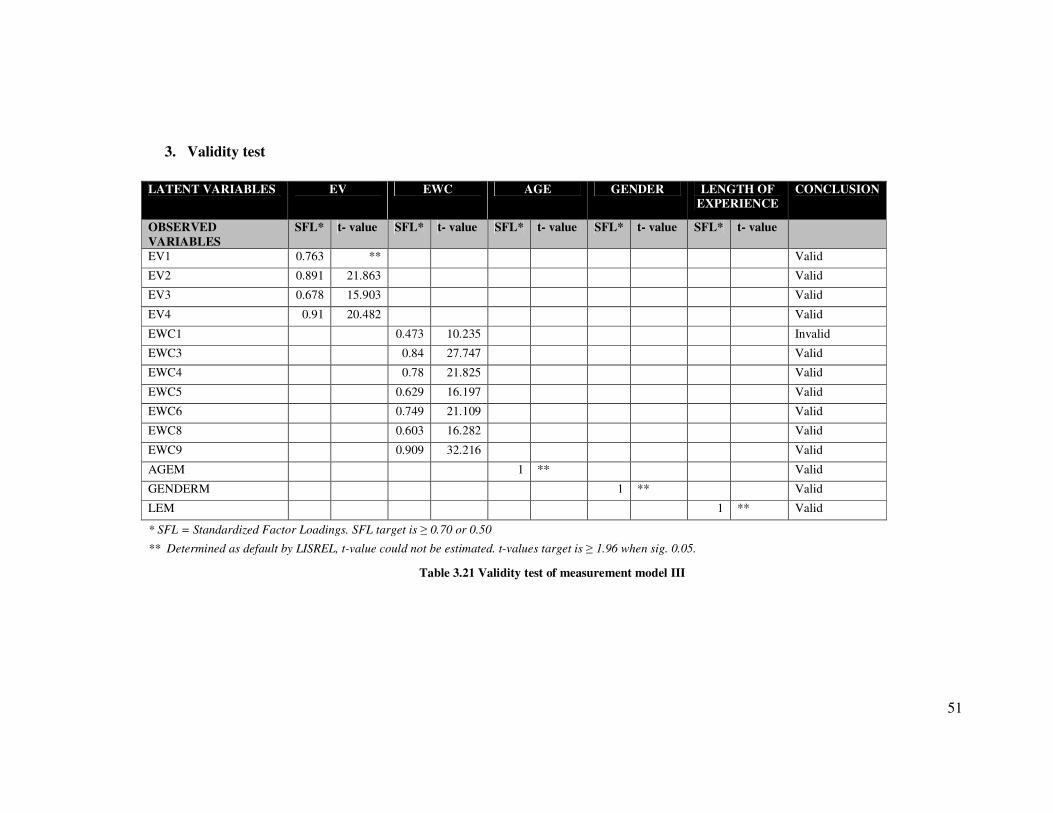

Table 3.21 Validity test of measurement model III ............................................. 51

Table 3.22 Pre-testing of ethical evaluation variables model IV ......................... 52

Table 3.23 Pre-testing of reliability EWC variables model IV ............................ 52

Table 3.24 Pre-testing validity model IV ............................................................ 53

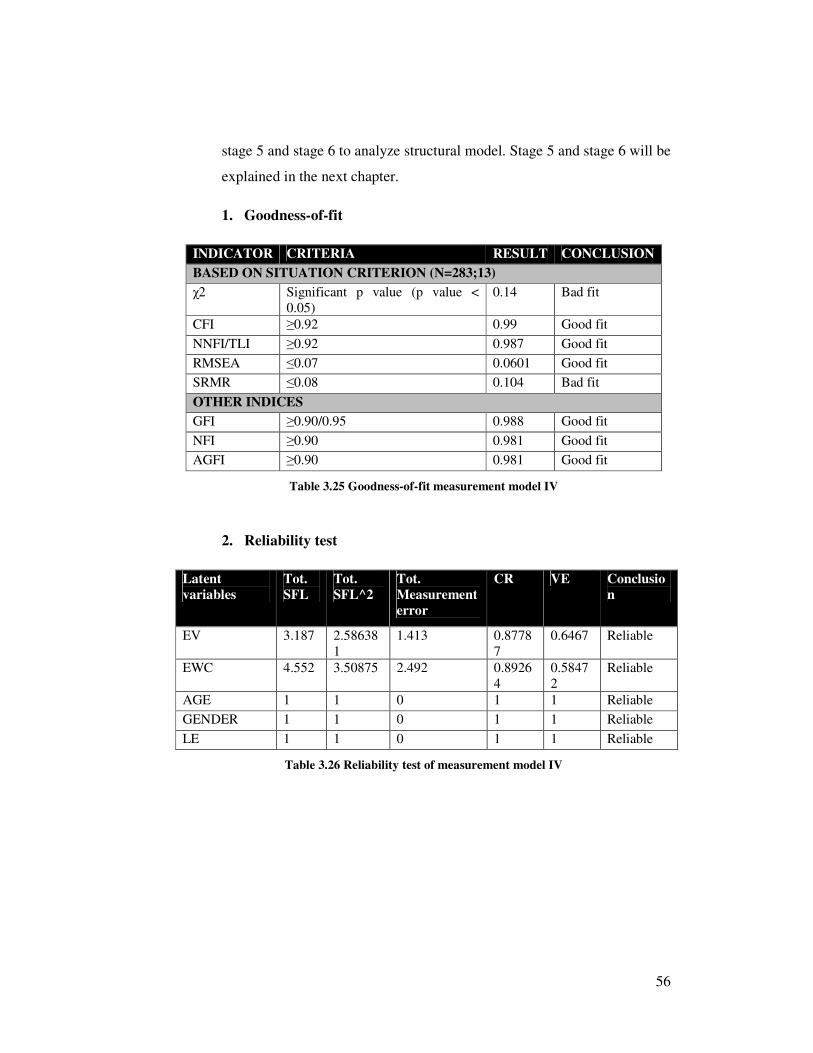

Table 3.25 Goodness-of-fit measurement model IV ........................................... 56

Table 3.26 Reliability test of measurement model IV ......................................... 56

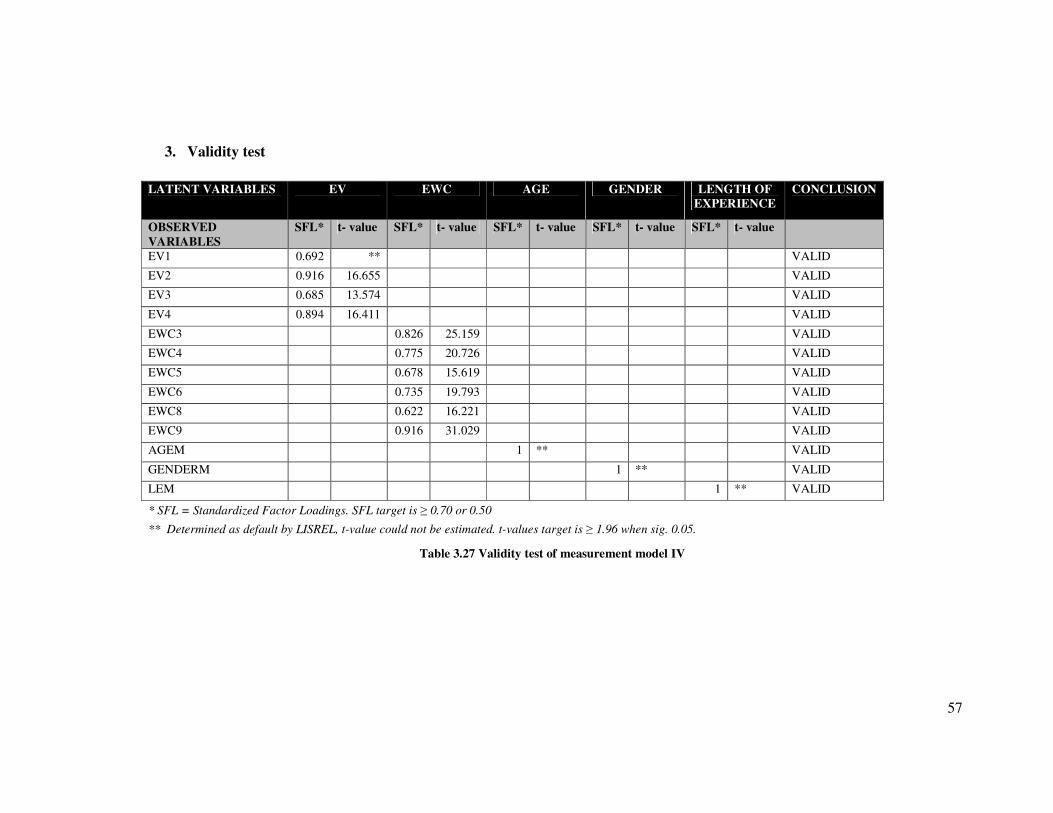

Table 3.27 Validity test of measurement model IV............................................. 57

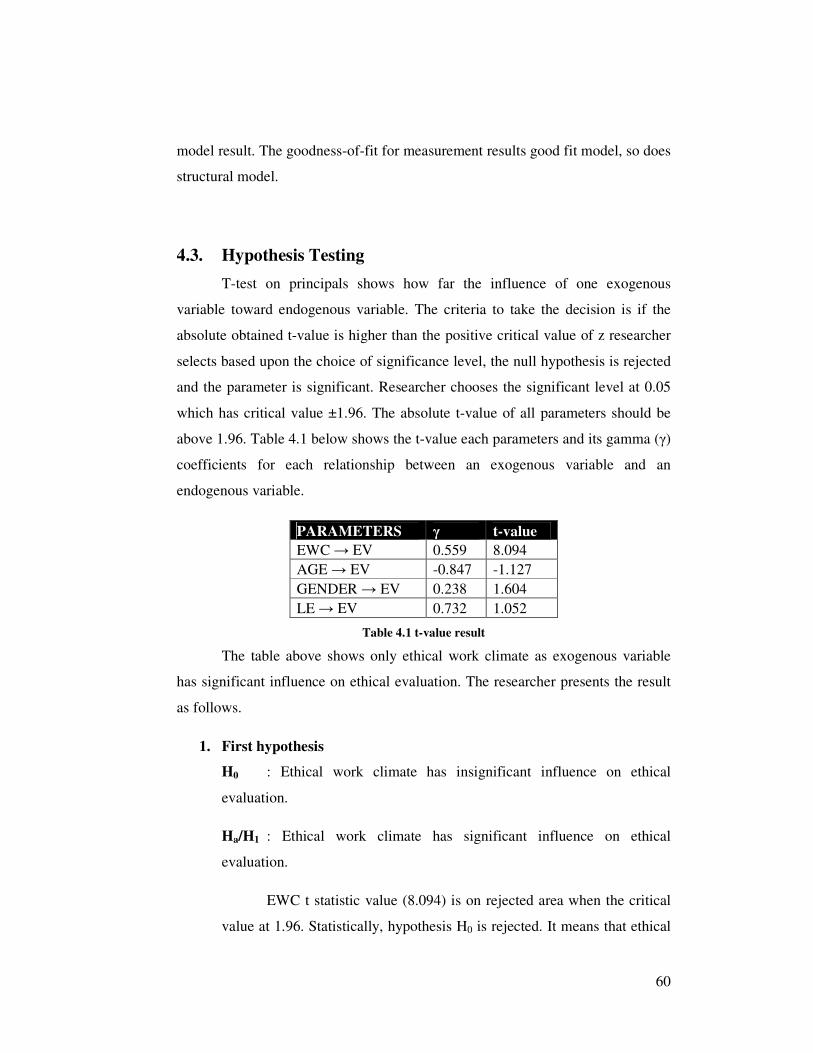

Table 4.1 t-value result ...................................................................................... 60

xi

LIST OF FIGURES

Figure 2.1 Rest's ethical reasoning process (Rest & Narvaez, Moral development

in the professions, 1994) ...................................................................................... 7

Figure 2.2 Teorectical ethical climate type (Victor & Cullen, A theory and

measure of ethical climate in organization, 1987) ............................................... 11

Figure 3.1 Six stages process of SEM (Hair, Black, Babin, Anderson, & Tatham,

2006) ................................................................................................................. 27

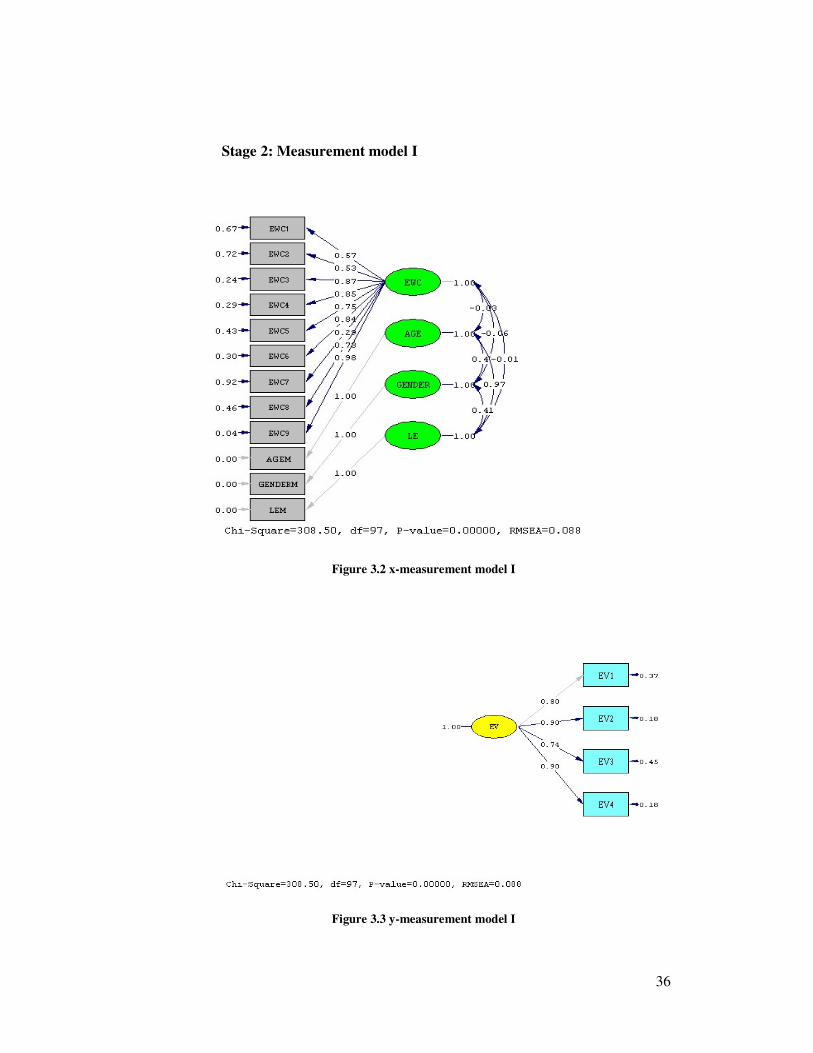

Figure 3.2 x-measurement model I ..................................................................... 36

Figure 3.3 y-measurement model I ..................................................................... 36

Figure 3.4 x-measurement model II................................................................... 41

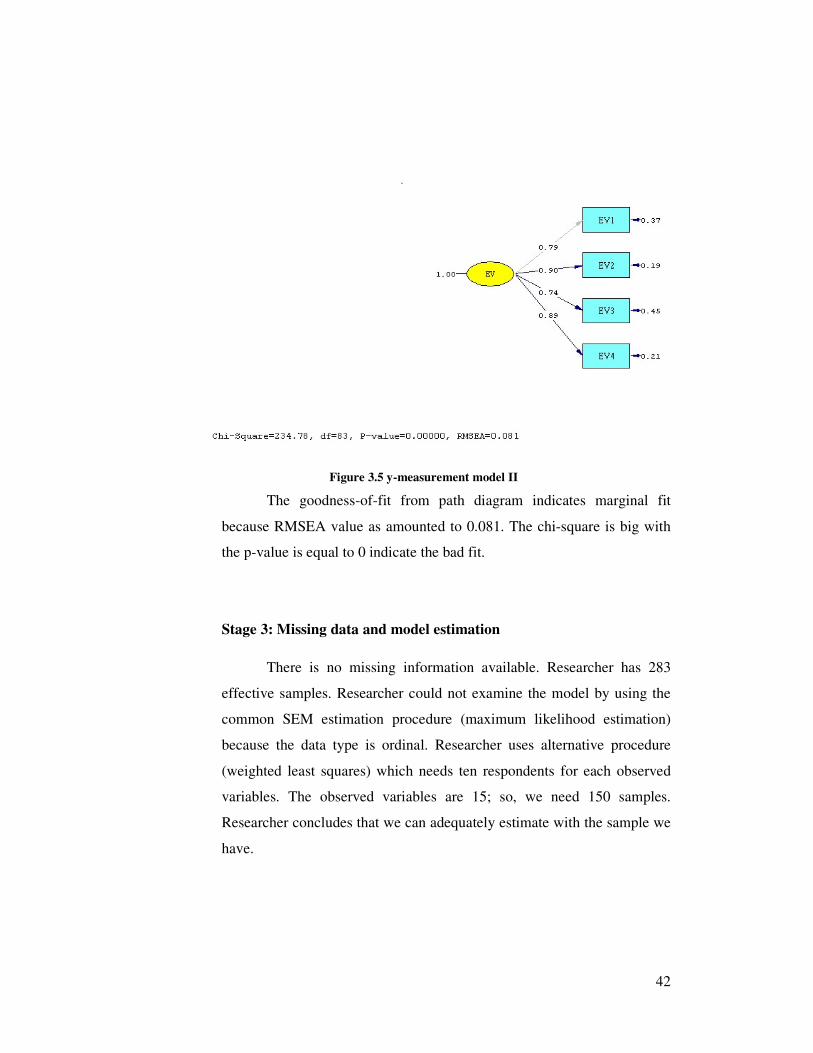

Figure 3.5 y-measurement model II ................................................................... 42

Figure 3.6 x-measurement model III .................................................................. 47

Figure 3.7 y-measurement model III .................................................................. 48

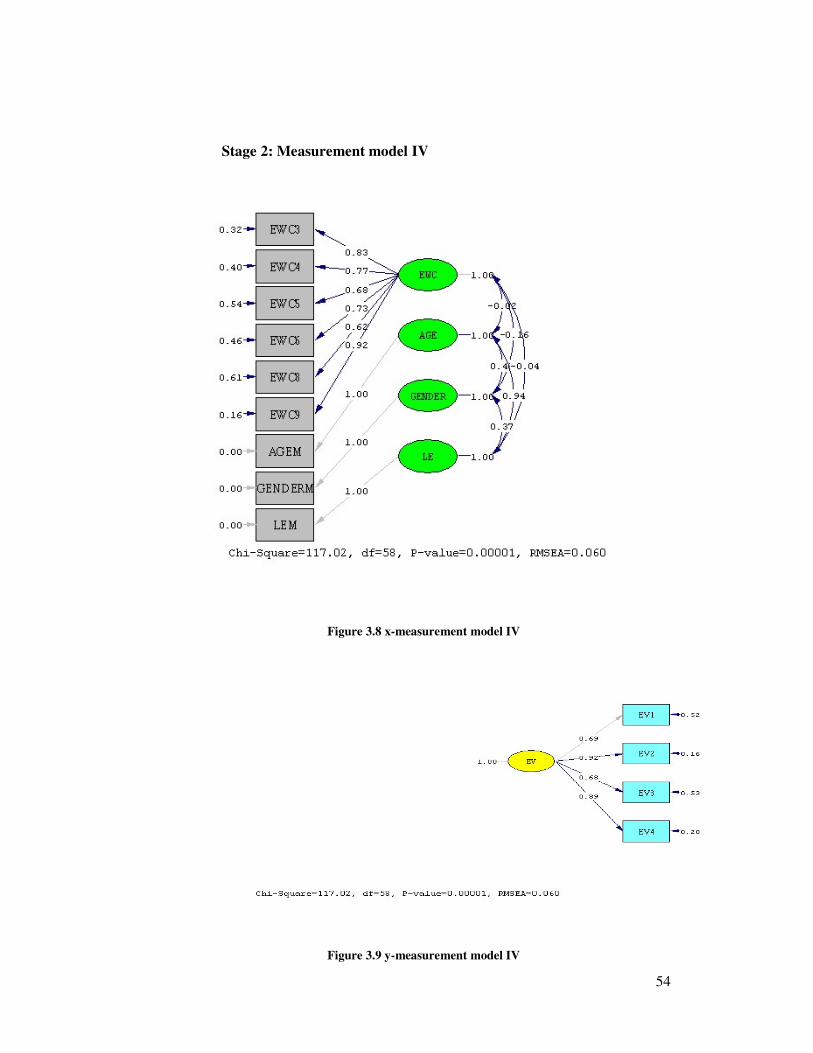

Figure 3.8 x-measurement model IV .................................................................. 54

Figure 3.9 y-measurement model IV .................................................................. 54

Figure 4.1 Structural model ................................................................................ 59

xii

LIST OF ACRONYMS

EWC : Ethical Work Climate

PSO : Premature Sign Off

QTB : Quality Threatening Behavior

URT : Underreporting of Time

SEM : Structural Equation Model

GAAP : Generally Accepted Accounting Principles

IFRS : International Financial Reporting Standards

GAAS : Generally Accepted Auditing Standard

1

CHAPTER I

INTRODUCTION

1.1. Research Background

The well-known accounting case, Enron, has raised question about the

auditors’ creditability as consequences of their external auditors’ role play in the

manipulation of financial statements. The implication of Enron’s external auditor,

Arthur Andersen, to engage with unethical action was suspended permanently,

although they have given assurance services for a long time. The Enron case also

initiated crisis facing the profession. The trust of auditors was wrecked. Auditors

suppose to have greater responsibility to the public rather than their client because

they have main responsibility to assure the financial statement that prepared by

management of company is reported fairly which will be used by external users.

The society expects auditors to have high standard of ethical behavior. Due to the

auditors’ ethical crisis, society doubt whether they could rely on to the

information given in audited financial statements. US Congress responded the

ethical crisis by issuing Sarbanes-Oxley Act in 2002 which legislates ethical

behavior for both public company and accounting public firms. Canary &

Jennings (2008) study found that corporation, particularly in the post-SOX time

frame, is at least attempting to make ethics a central concern of everyday

practices.

Ethics are considered to be important in every aspect, especially while

performing audit quality. But, auditors still engage in unethical behavior such as a

quality threatening behavior (QTB) and underreporting of time (URT) cause of

extremely time and cost pressure on audit. Being labor intensive, controlling cost

and time on an audit experience are high time and cost pressure on audit and put a

lot of stress on auditors. In the Janis and Mann’s decision model, stress is a key of

conflict model in ethical dilemmas (Janis & Mann, 1977). The auditors should

have technical and ethical experts in solving this dilemma (Gaa, 1994). Ethical

2

experts will determine the audit quality especially in the condition where there is

no exact rules existed.

A considerable amount of the research on ethics within auditing

profession has focused on the second elements of Rest’s ethical reasoning process

model, those being the individuals’ ethical evaluation of a relevant situation.

Previous researchers have elaborated the model by exploring the various

individual and contextual factors influence on ethical evaluation. Several studies

investigate the association between auditors’ ethical judgment and demographic

characteristics: age, gender, and length of experience. Researchers also

investigate the influence of ethical work climate that is already designed by

Victor and Cullen on auditors’ ethical evaluation.

Researcher initiates to examine the impact of ethical work climate and

demographic variables on the ethical evaluation element of the Rest’s model

within the context of certain time pressure-related dysfunctional auditor behaviors

– especially URT and QTB. Other main purpose is to fulfill the requirement for

graduating from President University. The researcher is seeking the data by

distributing questionnaire to a group of experience level auditors in Java Island.

The methodology that is used in the research is explanatory quantitative to

explain the influence of one variable to other variables.

1.2. Problem Identification

Unethical behavior is the most of unwilling act in the audit field work;

however, it often occurs in the real world. Some study found that when

accountability pressure exists, auditors tend to tailor their message to the audience

when the audience is known (Buchman, Tetlock, & Reed, 1996; Cuccia,

Hackenbrack, & Nelson, 1995; Hackenbrack & Nelson, 1996) and auditors’

judgment variability decreases (Ashton, 1992; DeZoort, Horrison, & Taylor,

2006). Increasing the quality of an audit involves investing more time in the audit

3

that leads of further costs and aggressive audit fee competition (Beattie &

Fearnley, 1998).

Based on Rest’s reasoning process, there is the phase of auditor to be

aware of the situation or dilemma that may affect the welfare of others, evaluate

their ethical, decide what they will do ethically, and actual behavior. Once an

ethical dilemma is identified, the auditor will frame an ethical strategy for

resolving ethical dilemma. At this point, auditor judges whose line of action is

ethically justifiable and then decides how the dilemma ought to be resolved. A

connection between organizational climate and demographic variables influences

and individual ethical judgment have long been assumed. The sub-organizational

climate that we will talk about is ethical work climate. The types of ethical work

climate use the theoretical designed by Victor-Cullen that has nine dimensions.

Demographic variables that will be examined are age, gender, and length of

experience.

1.3. Statement of the Problem

This research is about determining the influence of ethical work climate

on auditors’ ethical evaluation of ethical issues in the context of time and budget

pressure. Researcher wants to find out the correlation between ethical evaluation

and ethical work climate whether ethical work climate has a significant influence

on ethical evaluation or not. This study will add knowledge about the ethical

evaluation and the influence of ethical work climate into it, giving suggestion to

the public accountant firms in order to maintain the ethical work climate.

Statement of the problem 1: Does ethical work climate have significant

influence on ethical evaluation?

Researcher wants to determine the influence of specified demographic

variables (age, gender, and length of experience) on auditors’ ethical evaluation

of ethical issues in the context of time and budget pressure. Researcher is seeking

the impact of age, gender, and length of experience on ethical evaluation to enrich

4

literature in auditing field by giving empirical evidence about the impact of work

ethical climate and demographic variables on auditors’ ethical evaluation.

Statement of the problem 2: Does age have significant influence on ethical

evaluation?

Statement of the problem 3: Does gender have significant influence on ethical

evaluation?

Statement of the problem 2: Does length of experience have significant

influence on ethical evaluation?

1.4. Research Objective

The objectives to meet in this research which has a title “The Influence of Ethical

Work Climate and Demographic Variables on Auditors’ Ethical Evaluation” are

as follows:

1. To fulfill the requirement of graduating from President University

2. To examine the influence of ethical work climate on auditors’ ethical

evaluation.

3. To examine the influence of age on auditors’ ethical evaluation.

4. To examine the influence of gender on auditors’ ethical evaluation.

5. To examine the influence of experience on auditors’ ethical evaluation.

1.5. Significance of the Study

Research is a study and analysis of factors, subject, or problem to find the

solution, discover information, and reach an understanding. The result of this

research is expected to give benefit to several parties, they are:

1. External auditors

External auditors have responsibilities to serve public interest. They

should have great competence, integrity in the practice. This research will

5

help them to maintain their ethics that suppose to be important and

concerned of being professional auditor.

2. Public accounting firm

Public accounting firm has an employment level such as: partner, director,

manager auditor, senior auditor, associate level, and staff. Above level of

employment in public accounting firms need to monitor and supervise

their co-worker in the audit team. This research will help them to make

right decision regarding the ethical matter in work field and control the

behavior of senior associate level and associates level.

3. Accountant’s professional organizations

Accountant’s professional organization will be greatly benefited from the

finding of this study as consideration in order to improve code of conduct

or rules that give strict punishment to any auditors who do unethical act.

The rules exist to maintain the auditors’ responsibility to serve public

interest.

4. Academician

Researcher expects this study will give additional knowledge in context of

Accountant Professional Ethics about the factors influence toward

auditors’ ethical evaluation. The finding of this research will enrich

literature in ethical field by giving empirical evidence about the impact of

work ethical climate and demographic variables on auditors’ ethical

evaluation.

5. Researchers

This research could be a reference for future researchers who conduct

research regarding auditor ethics in context of pressure.

6

1.6. Scope and Limitation of the Study Assumption

There are some points that should be clarified for the equalization

perception among reader and researcher regarding the matter of the research. This

research examines the evaluation of ethical issues in the context of time and

budgeting pressure such as underreporting of time (URT) and quality threatening

behavior (QTB). Thus, only one step of Rest’s ethical reasoning process is

discussed in this research without examining other phases. The variables used in

this research to examine auditors’ ethical evaluation are ethical work climate,

gender, length of experience, and age. The climate of accounting public firm will

examine based on theoretical ethical work climate type that developed by Victor

and Cullen. Researcher examines the public firm in Java Island due to time and

cost barrier.

1.7. Definition of Terms

The definitions provide a common frame of reference to improve the

understanding and usefulness of this study. Please refer to APPENDIX 1 to see

the terms.

7

CHAPTER II

LITERATURE REVIEW

2.1. Rest’s Ethical Reasoning Process

Kohlberg (1969) theory of cognitive development has provided a

framework for the majority of studies on auditors’ ethical reasoning (Jones,

Massey, & Thorne, An experimental examination of the effects of individual and

situational factors on unethical behavioral intentions in the workplace, 1996).

Drawing upon the Kohlberg’s theory, Rest & Narvaez (1994) identified four

sequential components of the ethical reasoning process: sensitivity in identifying

the existence of a moral question, ethical evaluation, intention to act morally and

actual moral behavior (Figure 2.1). Moral reasoning is much more than moral

judgment in producing moral behavior which included, but is not limited to moral

sensitivity, judgment, motivation, and character which are all interrelated in the

moral development of individual (Rest & Narvaez, Moral development in the

professions, 1994).

Figure 2.1 Rest's ethical reasoning process (Rest & Narvaez, Moral development in the

professions, 1994)

The first component (ethical sensitivity) refers to the recognition of an issue as

having ethical implications. Failure of an individual to recognize that a situation

may or may not contain a moral element would impede that individual from going

any further in the moral analysis of the situation (Wortman, 2006). Jones T. M.

(1991) identified that there is two necessary components to recognize a moral

dilemma: the individual must understand that his/her actions will affect others and

Ethical

sensitivity

Ethical

evaluation

Intention

to act

Actual

Behavior

8

that she/he has a choice in a matter. When person is able to be aware, then that

person will continue to the next steps. The second involves making a judgment if

an action is ethically correct. Once an individual makes a judgment about a moral

dilemma, s/he still has the opportunity to decide what behavior to adopt

(Wortman, 2006). The third deals with intention to act which is determined by the

value of an individual places on the ethical course of action versus the value of

other courses of action. The fourth distinguishes the intention from the actual

action. An intention may not result in an action and, therefore, Rest sees this as a

separate and distinct component.

2.2. Kohlberg Theory of Cognitive Development

Kohlberg postulates that cognitive structures and interpretative processes

precipitate an individual’s ethical decision choices (Trevino, Experimental

approaches to studying ethical-unethical behavior in organization, 1992).

Kohlberg theory is developmental in focus and proposes three broad levels of

sophistication in ethical reasoning. At first level, the pre-conventional level, the

individual decides what is right or wrong based upon consequences. At the

second level, the conventional level, the individual is concerned about

expectations of significant others and relies upon rules and laws to determine

what is right or wrong. At the third level, the post-conventional level, the

individual decides what is right or wrong in using universal ethical principles

such as common good and justice (Kohlberg, Stage and sequences: The cognitive

development approach to socialization, 1969; Rest, Narvaez, Bebeau, & Thoma,

1999). In specific, the stages of cognitive moral development are as follows.

(Kohlberg, Continuities in childhood and adult moral development revisited,

1973; Kohlberg, The philosophy of moral development 1, 1981; Logsdon &

Yuthas, 1997)

Pre-convential level: Behavioral norms are viewed as being external to the

individual.

9

Stage 1: Punishment-obidience orientation.

Stage 2: Instrumental hedonism and concrete reciprocity.

Conventional level: Externally validated norms are internalized by the individual.

Stage 3: Orientation to interpersonnal relation of mutuality.

Stage 4: Maintenance of social order; fixed rules and authority.

Post-conventional level: Individual recognition that external norms may not fully

encompass ethical behavior.

Stage 5: Social contract, with conscience orientation.

Stage 6: Universal ethical principle orientation.

At the pre-conventional level, a person views rules as imposed and

external to himself/herself. Moral decisions are justified in terms of one’s own

hedonistic interests and in terms of rewards and punishment. Stage one of

individuals form moral judgments guided by obedience for its own sake and to

avoid punishment. Stage two moral judgments are guided by a “you scratch my

back, I will scratch yours” reciprocity. (Arnaud, 2006).

At level two, the conventional level, the individual internalizes the shared

moral norms of the society or a group of the society (e.g. family). What is

considered morally right is explained in terms of living up to roles and what is

expected of the individual by others, and fulfilling duties, rules and laws. Stage

three individuals find ethical behavior to be what pleases and help others. Stage

four individuals’ perspective broaden to consider the society of which they are

part. At this stage, moral judgments consider the riles and laws of social, legal, or

religious systems that are designed to promote the common good. (Arnaud, 2006)

At level three, the post-conventional level, the individual has gone beyond

identification with others’ expectation, rules and laws. Stage five individuals

recognize the relativism of personal values. They still emphasize laws and rules

because they represent the social contract, but they understand the laws can be

10

changed for socially useful purposed. Stage six individuals guided by self chosen

ethical principles of justice and human right. Kohlberg claimed that higher stage

moral judgments are better and more desirable (Arnaud, 2006).

2.3. Ethical Work Climate Theory

Victor & Cullen (1987) define ethical work climate (EWC) as the shared

perceptions of what is ethically correct behavior and how ethical issue should be

handled. They noted “organization are social actors responsible for the ethical or

unethical behaviors of their employees,” and there is “…increasing concern for

understanding and managing organzational normative systems that may guide the

ethical behavior of employees,” (Victor & Cullen, The organizational bases of

ethical work climates, 1988). Ethical work climate is environment of company

that support ethical behavior as guidance for their employees. In regard forming

possible ethical climate types, Victor & Cullen (1987) combine two dimensions:

the ethical criteria used for organizational decision making and the loci of anaysis

as referent in ethical decision making.

2.3.1. The ethical criteria dimension

This dimension of EWC is grounded in Kohlberg’s theory of

cognitive moral development (Arnaud, 2006). Victor & Cullen (1987)

draw three levels of cognitive moral reasoning to define ethical dimension

of their model. They termed these criteria egoism, benevolence, and

principle, corresponding to Kohlberg’s preconventional, conventional, and

postconventional moral reasoning, respectively. The egoistic criterionis

characterized by employees’ desires to maximise self interest. The

benevolence ethical criterion is characterised by employees’ desires to

maximise the collective interest of the organization. The principle ethical

criterion is characterised by employees’ adhrence to broader principles of

society and humanity. Egoistic climate tends to lead less ethical decision

rather than benevolent and principle climate (Shafer, Poon, & Tjosvold,

2013).

11

2.3.2. Loci of analysis

The second dimension of Victor & Cullen (1987) framework

borrows from Kohlberg’s theory who defines three loci of concern at

which three ethical criterias are to be considered. The first two of

Kohlberg’s stages, the locus of concern is individual; in the third and

fourth stages the individual’s referent group becomes a larger social

system; and in the highest stages consideration is given to humanity and

other consideration as a whole (VanSandt, Shepard, & Zappe, 2006).

The crossing of these dimensions produces the 3x3 matrix of climate type shown

as below.

Figure 2.2 Theoretical ethical climate type (Victor & Cullen, A theory and measure of

ethical climate in organization, 1987)

The self-interest climate is only care about what is best for them. Individual tends

to protect his/her own interest above others. People in company profit climate are

expected to do anything of further the company’s profit. Profit organization is

mainly goal to achieve higher profit over year to year. They expect their people to

work efficiently in the company (egoism/cosmopolitan). Organization with

benevolence/individual is care about each individual decision making. The

benevolence/local is essential climate. This climate concerns for the good of all

12

people in the company or placing other people’s interest first. Organization

concerned the effect of decision to public in benevolence/cosmopolitan climate.

In principle/individual climate, organization members are expected to follow their

own personal and moral beliefs to identify and make ethical decisions (Wortman,

2006). Organizational with principle/local climate is described in terms of “it is

important to follow strictly the company’s rules and procedures”. Most behaviors

in this climate are directed towards the enforcement of policies and procedure that

build in company. Within principle/cosmopolitan climate, members of company

are primarily concerned with conformity to and abiding by professional standards

and laws (e.g. GAAP, IFRS, GAAS).

2.4. Ethical Behaviors Examined

Ethics research in accounting has focused on a multitude of unethical

behaviors and research on ethical decision making suggests an adverse effect of

time pressure on ethical principles (Moberg, 2000). A stream of literature exists

since the 1970s on time pressure-induced auditor behaviors which are considered

dysfunctional for audit firms and potentially damaging for the profession (e.g.

Buchheit, Pasewark Jr., & Strawser, 2003; Kelley & Margheim, 1987; Rhode,

1978; Sweeney & Pierce, 2006). The range of the behaviors examined in previous

research includes URT and various QTB such as biasing of sample selection,

premature sign-off (PSO) (where auditors sign-off work as completed without

actually completing the work), unauthorized reduction of sample size, greater

than appropriate reliance on client work, acceptance of weak client explanations,

and failure to properly document work (Pierce & Sweeney, Auditor responses to

cost control, 2003).

QTB has been associated with both time deadline and time budget

pressures (Kelley & Margheim, 1999; Pierce & Sweeney, 2004), whereas URT is

only relevant in the context of time budget pressure (Sweeney & Pierce, 2006).

Regarding the ethicality of these behaviors, QTB has been described as an ethical

issue, as it ‘has consequences for others and involves choice or volition on the

13

part of the auditor’ (Coram, Glavovic, Ng, & Woodliff, 2008) and this also

applies to URT.

The type of QTB behavior was considered important by audit seniors in

determining the consequences, with premature sign-off being much more serious

than small reductions in sample size (Pierce & Sweeney, 2006). Perceived

consequences of URT were less severe and included positive consequences such

as improved performance evaluations, increased firm profitability and negative

consequences such as pressure on the individual to maintain image of efficiency

and reduction in the quality of management information (Sweeney & Pierce,

2006). While QTB and URT are not specifically referred to in ethical guidelines

of the profession, the behaviors can be considered contrary to the spirit of the

guidelines. It would be expected that the perceived magnitude of consequences

and perceived social consensus regarding the unacceptability of the behaviors

would be highest for PSO and lowest for URT.

Yet, Pierce & Sweeney (2006) found that audit seniors expressed a low

level of concern over the ethicality of QTB, while Sweeney & Pierce (2006)

found that audit seniors’ concern over the ethicality of URT was virtually non-

existent. Sweeney, Arnold, & Pierce (2010) found URT can be perceived as an

ethical act and PSO is more unacceptable behavior than some other types of QTB.

2.5. Relationship between Ethical Evaluation and Ethical Work

Climate (EWC)

In general, egoistic climates tend to lead to less ethical decisions, while

benevolent and principled climates lead to more ethical decisions (Shafer, Poon,

& Tjosvold, 2013). Indeed, with their explicit focus on the pursuit of self-interest

(egoistic/individual) and narrowly defined firm interests such as profitability

(egoistic/local), it seems logical that egoistic climates should be associated with

less ethical behavior (Shafer, Poon, & Tjosvold, 2013). In the case of benevolent

climates, the welfare of individuals, organizational groups or members of society

14

at large are a primary focus of concern (Shafer, Poon, & Tjosvold, 2013).

Members within benevolent/local organizational climate are concerned about

what is best for everyone in the company. Often this ethical climate is manifested

through communication, employee inclusiveness, valuing people, and

demonstration of concern (Whitener, Brodt, Korsgaard, & Werner, 1998). These

factors all make up a sense of trust which has been linked to decision making

process (Gao, Sirgy, & Bird, 2005).

In such climates, employees perceive that decisions are made based on an

overarching concern for the well-being of these parties (Martin & Cullen, 2006);

thus, such decisions should generally be viewed as ethical in nature. It is

somewhat more difficult to generalize regarding the effects of principled climates

on ethical behavior. As noted by Trevino, Butterfield, & McCabe (1998), this

difficulty arises primarily due to the uncertain effects of principled/individual

climates. When the organizational climate encourages individuals to follow their

own moral principles, it is difficult to predict behavior and whether such behavior

will be viewed by others as ethical. The principled/local and

principled/cosmopolitan climates, however, should clearly promote relatively

ethical behavior due to their emphasis on following prescribed organizational or

professional rules and codes of conduct (Shafer, Poon, & Tjosvold, 2013).

Significant variation exists in the specific ethical climates identified across

studies (Trevino, Butterfield, & McCabe, The ethical context in organizations:

influences on employee attitudes and behaviors, 1998; Martin & Cullen, 2006).

Indeed, the nine theoretical climate types were intended only as a general

framework for the conceptualization of ethical climates and thus inconsistencies

across organizational settings should be expected (Victor & Cullen, A theory and

measure of ethical climate in organization, 1987). Nonetheless, recent studies of

ethical climate in public accounting firms have consistently found support for the

existence of benevolent/cosmopolitan (public interest) and

principled/cosmopolitan climates, as well as egoistic/individual and/or

egoistic/local climates (Cullen, Parboteeah, & Victor, 2003; Parboteeah, Cullen,

Victor, & Sakano, 2005; Shafer W. , 2009). Due to the emphasis on serving the

15

public interest and following professional codes of conduct in public accounting

(AICPA, 2009), it is not surprising that benevolent/cosmopolitan and

principled/cosmopolitan climates have consistently emerged in this context.

Codes of conduct (principle climate dimension) have been a common proxy for

the ethical environment in accounting and auditing literature, because

organization, including accounting firms, and their employees consider them to

be relevant and important (Lamberton, Mihalek, & Smith, 2005) in making

explicit ethical values, putting employees on notice as to what is ethical, and

shifting accountability for actions from firms to individuals.

Egoistic/individual and egoistic/local climates also appear highly relevant

to the public accounting context, since the pursuit of self-interest and firm

profitability are arguably among the primary obstacles to serving the public

interest and following the spirit of professional codes of conduct (Shafer, Poon, &

Tjosvold, 2013). The ethical climate construct has been quite influential in the

business ethics literature and the weight of the evidence suggests that employees’

perceptions of the prevailing climates in their organization affect ethical

decisions, and are also associated with work outcomes such as organizational

commitment and job satisfaction (Martin & Cullen, 2006).

2.6. Relationship between Ethical Evaluation and Demographics

Variables

This research examines the impact of specified demographic variables:

age, gender, and the length of experience towards ethical evaluation.

2.6.1. Age

Mixed findings have been reported on the relationship between age

and ethical decision making (Ford & Richardson, Ethical decision

making: A review of the empirical literature, 1994). Clarke, Hill, &

Stevens (1996) found that age and moral development were significantly

negatively related for Big 6 practitioners, while Ruegger & King (1992)

16

found that age was positively correlated to ethical attitudes. Lane (1995),

Loe, Ferrel, & Mansfield (2000), Longeneeker, McKinney, & Moore

(1989), and Yoo & Donthu (2002) found a possitive correlation between

age and ethical decision making indicating that older students are more

likely to act ethically than the younger students. Early reviews (Ford &

Richardson, Ethical decision making: A review of the empirical literature,

1994; Loe, Ferrel, & Mansfield, 2000) found seven out of eight studies

indicating older people are more ethical than younger people. Age showed

a significant positive relationship with ethical evaluation (Sweeney,

Arnold, & Pierce, 2010). Ethical judgment was associated with increased

age (Valentine & Rittenburg, 2007). O'Fallon & Butterfield (2005) further

found mixed results with eight of their 21 findings not producing

significant results. Six studies found a positive relationship between age

and ethical decision making, while five studies indicated a negative

relationship. In Lehnert, Park, & Singh (2015) review four findings that

reported a significant effect of age. Three findings reported that older

people tend to behave more ethically than younger people. Mixed results

in previous studies indicate that the role of age in ethical decision making

is not clear; therefore, researcher concludes age may have a significant

influence on auditors’ ethical evaluation.

2.6.2. Gender

A number of studies has examined the impact of gender on ethical

decision making, with some findings that females have higher ethical

decision making ability than males (Barnett, Bass, & Brown, 1994;

Bernardi & Arnold, 1997; Cohen, Pant, & Sharp, 1998; Clarke, Hill, &

Stevens, 1996; Eynon, Hill, & Stevens, 1997; Sweeney, Arnold, & Pierce,

2010) and others showing no difference between males and females

(Dubinsky & Levy, 1985; Radtke, 2000; Ponemon, Ethical reasoning and

selection socialization in accounting., 1992; Armstrong, 1987). Sweeney,

Arnold, & Pierce (2010) study indicated females reported significantly

17

higher ethical evaluation than males. O'Fallon & Butterfield (2005) noted

49 studies in gender category, with the majority or tose studies (23

studies) not finding significant differences. In the 16 studies found

significant gender differences, females were found to be more ethical than

males. Glover, Bumpus, Logan, & Ciesla (1997) found a significant

correlation between gender and ethiccal decision making. They found that

women’s decision about moral issues were more ethical than men’s.

Female seems to be more aware of ethical issues and more likely to act

ethically than their male counterparts (Robin & Babin, 1997; Borkowski

& Ugras, 1998). In (Craft, 2013), discussion of the impact of various

gender-specific variable on ethical decision making highlights that

females are more ethical than males, however, males are more consistent

in their decision making. As general, researcher concludes that gender has

significant influence on auditors’ ethical sensitivity.

2.6.3. Length of experience

Glover, Bumpus, Sharp, & Munchus (2002) found a positive

relationship between years of management experience and ethical choice.

They argued that greater experience may be linked with greater awareness

of acceptable ethics and a greater experience of dealing with similar

situations (Sweeney, Arnold, & Pierce, 2010). Otherwise, Thorne,

Massey, & Magnan (2003) found that there is a significant negative

corelation between years experience and ethical judgment. Eweje &

Brunton (2010) found that more experienced students appeared to be more

ethically oriented. A study found a positive and significant relationship

between work experience and ethical decisoin making with the other two

reporting non significant results (Lehnert, Park, & Singh, 2015). Ethical

judgement was associated incrased experience (Valentine & Rittenburg,

2007).

18

General auditing experience has been found to be positively

related to auditors’ judgment performance when the audit task requires

exercise of individual judgment (Martinov-Bennie & Pflugrath, 2009). For

more complex tasks requiring greater exercise of judgment, general

auditing experience can improve performance by providing the necessary

skills and/or knowledge required to complete these tasks (Anderson,

Koonce, & Marchant, 1994; Anderson & Maletta, 1994). Task specific

experience has been shown to be able to provide additional improvement

in the quality of auditors’ judgments for semi-structured and unstructured

tasks (Bonner & Lewis, 1990; Libby & Tan, 1994; O’Reilly, Leitch, &

Wedell, 2004; Pincus, 1991; Wright, 2001). Martinov-Bennie & Pflugrath

(2009) found greater task-specific experience provide more significantly

higher quality technical judgments than those with lower levels of task-

specific experience.

According to previous studies, researcher concludes that length of

experience has significant influence on auditors’ ethical evaluation.

2.7. Theoretical Framework

Rest (1986) has suggested that one needs to perform four basic

psychological processes in order to behave ethically. The four basic psychological

processes are called as Rest’s ethical reasoning. In short, the process begins with

the awareness of moral problem exists, and then individual decides the correct

moral and has willingness to behave ethically. The last phase is actual behavior.

The evaluation of ethical issue is really important for the professionals to

decide what is right or wrong, ethical or unethical act while they have extremely

pressure on audit. Some study found that when accountability pressure exists,

auditors tend to tailor their message to the audience when the audience is known

(Buchman, Tetlock, & Reed, 1996; Cuccia, Hackenbrack, & Nelson, 1995;

Hackenbrack & Nelson, 1996) and auditors’ judgment variability decreases

19

(Ashton, 1992; DeZoort, Horrison, & Taylor, 2006). Cost and time pressures are

also caused in ethical dilemma of auditor. Bigger cost of audit is probably caused

of extended time on audit for increasing audit quality. Imbalance in audit work

and staffing, client induces pressure, and complexity of business environment will

increase time pressure on auditor. The un-behaved actions will be arisen from

cost and time pressures are quality threatening behaviors (QTB) and

underreporting of time (URT). In specific, dysfunctional responses caused of time

and budget pressure are biasing the sample selection, too much reliance on client

work, phantom ticking, and an overall lower standard of work.

Some previous literature already expanded the Rest’s model by

recognizing influence of multiple variables and their interactions. They have

developed the relationship between individual factors into Rest’s model such as

general demographics characteristics (e.g. gender (Gilligan, 1982; Barnett, Bass,

& Brown, 1994; Bernardi & Arnold, 1997; Clarke, Hill, & Stevens, 1996; Cohen,

Pant, & Sharp, 1998; Browning & B., 1983; Dubinsky & Levy, 1985; Radtke,

2000), political orientation (Elmer, Renwick, & Malone, 1983)), ethical

development (Trevino, 1986), etc. Prior researchers also identified the influence

of contextual factors into the Rest’s model which include the immediate job

context (time and budget pressure, role pressure, rewards and sactions, and the

influence of significant others) (Trevino & Weaver, Managing ethics in the

business organization: Social scientific perspectives, 2003), the external context

(professional environment, organizational environment), and issue specific

factors. The ethical climate construct has been quite influential in the business

ethics literature and the weight of the evidence suggests that employees’

perceptions of the prevailing climates in their organization affect ethical

decisions, and are also associated with work outcomes such as organizational

commitment and job satisfaction (Martin & Cullen, 2006).

Organizational climate is conceptualized as the way individuals perceive

personal impact of their environment (James, James, & Ashe, 1990). Thus,

climate encompasses the set of characteristics, which the members of the

organization perceive and come to describe in a shared way (Verbeke, Volgering,

20

& Hessels, 1998). Victor & Cullen (1987) develop theoretical ethical work

climate types by combining the locus of analysis and ethical criterion that adopted

from Kohlberg theory. Indeed, the nine theoretical climate types were intended

only as a general framework for the conceptualization of ethical climates and thus

inconsistencies across organizational settings should be expected (Victor &

Cullen, A theory and measure of ethical climate in organization, 1987).

Nonetheless, recent studies of ethical climate in public accounting firms have

consistently found support for the existence of benevolent/cosmopolitan (public

interest) and principled/cosmopolitan climates, as well as egoistic/individual

and/or egoistic/local climates (Cullen, Parboteeah, & Victor, 2003; Parboteeah,

Cullen, Victor, & Sakano, 2005; Shafer W. , 2009). The ethical climate construct

has been quite influential in the business ethics literature and the weight of the

evidence suggests that employees’ perceptions of the prevailing climates in their

organization affect ethical decisions (Martin & Cullen, 2006).

The influence of auditors’ ethical evaluation may also come from

demographic variable. According to Cambridge advanced learner's dictionary

third edition (2008), demographic is the quantity and characteristics of the people

who live in particular area, especially in relation to their age, how much money

they have and what they spend it on. Demographic variables are talking about

gender, age, and length of experience that will be discussed in this study. Mixed

findings have been reported on the relationship between specified demographic

variables (age, gender, and length of experience) and ethical decision making.

Researcher concludes that those demographic variables may have significant

influence on ethical evaluation.

21

2.8. Assumption and Hypothesis

According to explanation of theories above and formulation of problems

from previous chapter, several hypotheses suggest as follows.

H1: Ethical work climate has significant influence on ethical evaluation.

H2: Age has significant influence on ethical evaluation.

H3: Gender has significant influence on ethical evaluation.

H4: Length of experience has significant influence on ethical evaluation.

22

Chapter III

Data Processing Method

3.1. Research Method

The research employed a quantitative methodology that uses statistical

measurement to obtain the result. The quantitative methodology is best suited for

study due to concrete result as the basis to prove the hypothesis. The procedures

of quantitative methodology will form the scientific foundation to explain the

relationship between independent variables and dependent variables in targeted

population that is called as explanatory approach. In explanatory approach,

statistical techniques are used to test the significant relationship among variables.

The variables of this study are as follows.

3.1.1. Dependent variable

Dependent variable is the main variable that researcher wants to

investigate deeply. Researcher is interested in quantifying and measuring

dependent variable to get solution of the problem. The dependent variable

of this research is auditors’ ethical evaluation. Auditors’ ethical evaluation

is auditors’ ability to evaluate the action.

3.1.2. Independent variable

Independent variable causes the change in dependent variable in

either positive or negative way. The independent variables that may have

influenced on auditors’ ethical evaluation are ethical work climate and

demographic variable.

23

3.2. Operational Variable Identification

Operational variable identification is to determine how measurement of

variables will be made. Each variable will be defined operationally.

1. Auditors’ ethical evaluation

To identify auditors’ ability to evaluate the action, the researcher prepares

the cases related to certain time and cost pressure-related dysfunctional

auditor behaviors – especially URT and QTB. Auditors is requested to

give their preference in five point scale (1 = favor the action; 5 = oppose

the action). The higher score given reflects a higher ethical evaluation as it

indicates that the behaviors represented in the cases are considered

unethical.

2. Ethical work climate

The nine theoretical climate types were intended to be evaluated. The nine

questions of ethical work climate are adopted from Victor & Cullen

(1987, 1988). Each indicator is to be rated by the respondents based on

how they are perceived it really in their organization, not how they prefer

it to be, in a five point scale, ranging from “strongly disagree” to :strongly

agree”.

3. Specified demographic variables

The demographic variables that are willing to execute in this research are

age, gender, and length of experience. A question is prepared for each

variable to determine how long their experience in professional field, their

age, and their gender.

The indicators of each variable are elaborated on table 3.1 below.

24

VARIABLE INDICATOR SYMBOL* SCALE

MEASUREMENT

Auditors'

ethical

evaluation

a. Auditors evaluate behavior about biasing

sample selection. EV1 Ordinal

b. Auditors evaluate behavior about over-reliance

on client work. EV2 Ordinal

c. Auditors evaluate behavior about URT. EV3 Ordinal

d. Auditors evaluate behavior about PSO. EV4 Ordinal

Ethical work

climate a. People in this company are very concerned

about what is best for them (egoism-individual

climate)

EWC1 Ordinal

b. People are expected to do anything o further

the company’s interest (egoism-local climate). EWC2 Ordinal

c. In this company, each person is expected,

above all, to work efficiently (egoism-

cosmopolitan climate).

EWC3 Ordinal

d. It is expected that each individual is cared for

when making decisions here (benevolence-

individual climate).

EWC4 Ordinal

e. Our major consideration is what is best for

everyone in this company (benevolence-local

climate).

EWC5 Ordinal

f. The effect of decisions on the customer and the

public are primary concerned in this company

(benevolence-cosmopolitan climate).

EWC6 Ordinal

g. Each person in this company decides for

himself what is right and wrong (principle-

individual climate).

EWC7 Ordinal

h. It is important to follow strictly the company’s

rules and procedures (principle-local climate). EWC8 Ordinal

i. In this company, people are expected to strictly

follow legal or professional standards (principle-

cosmopolitan climate).

EWC9 Ordinal

Specified Demographic

variables (age, gender,

length of

experience)

a. Auditors give their personal information about

their age. AGEM Ordinal

b. Auditors give personal information about their

gender. GENDERM Ordinal

c. Auditors give personal information about how

long they have worked at professional accounting

firm.

LEM Ordinal

* symbol in path diagram

Table 3.1 Operational variable identification

25

3.3. Data Collection Method

Data collection methods are designed to maintain the integrity of the

study. In order to provide sufficient information for the study, the author uses the

qualitative data. The qualitative data is used as the data that presents related

literatures and concepts to support this study. To address the research questions,

researcher collected data from several sources as below:

1. Questionnaire is one of three main data collections in survey research.

Due to the limitation of researcher, the questionnaire will be manually and

electronically distributed. Questionnaires were distributed to professional

auditor at big four public accounting firms and non big four public

accounting firms in Java Island. To measure auditors’ ethical evaluation,

researcher distributed questionnaires with cases that adopted and explored

from previous study. The respondents will give their opinion of each

statement in the 5 point scale. The questionnaire includes 3 parts: 1)

unethical action cases to measure ethical evaluation variable 2) ethical

work climate 3) personal information in regards to demographic variables

(see APPENDIX 5).

2. Literature review is secondary data to gather the data from source that

already exist. Literature review is a method of collecting theoretical data

by reading and studying some books and other writing materials which are

relevant to the topic that the author has chosen. The materials will be used

as guidance to develop conceptual framework and supporting argument of

the finding.

3.4. Sampling Design

The sample must represent the population interest and must be adequate

for subsequent analysis. Some form of random sampling is used in probability

sample design to enable researcher in using probability theory to determine the

accuracy of results through the computation of standard error. Two types that are

explained in probability theory are probability sampling designs and non

26

probability sampling designs. The auditor uses the purposive sampling, one of

non probability sampling design types. Researcher received back 283

questionnaires from 300 questionnaires distributed. Researcher is also

compromising the data from the auditor into four types of demographic variables

which are age, gender, firm size, and length of experience in table 3.2.

Demographic details Total data

Non big four 205

Big four 78

Female 147

Male 136

Mean length experience 2.5231

Mean age 24.9965

Table 3.2 Demographics details of the sample

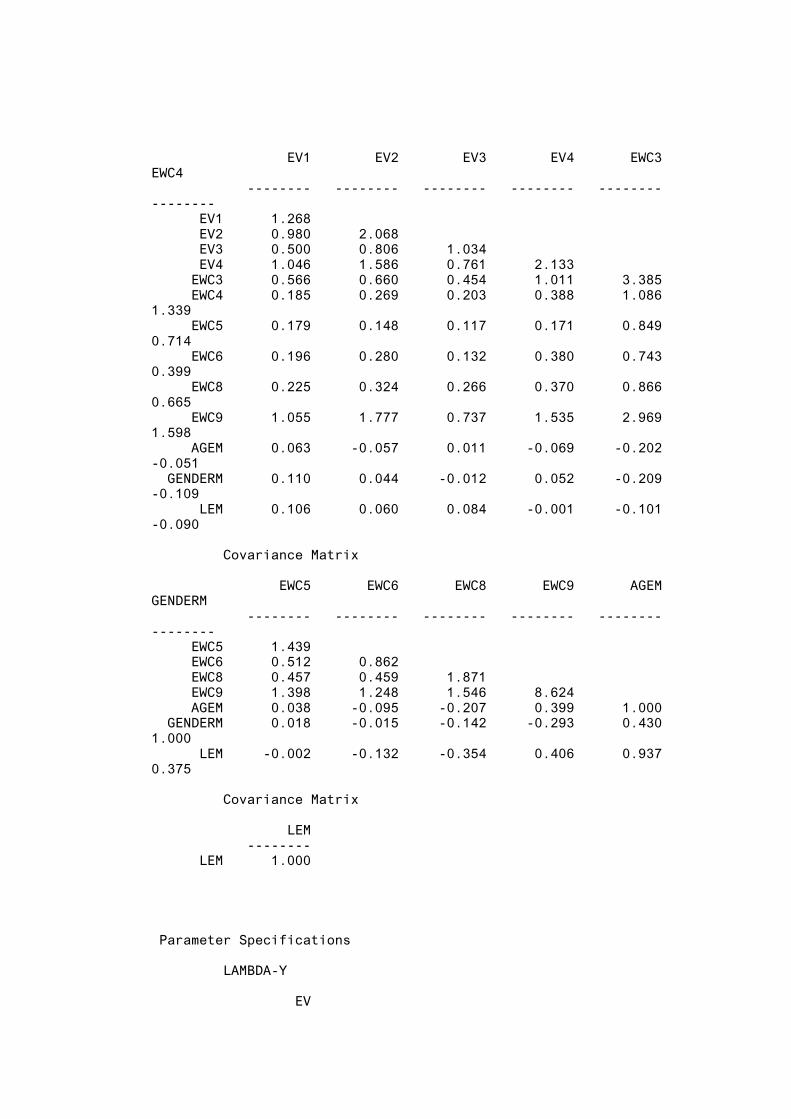

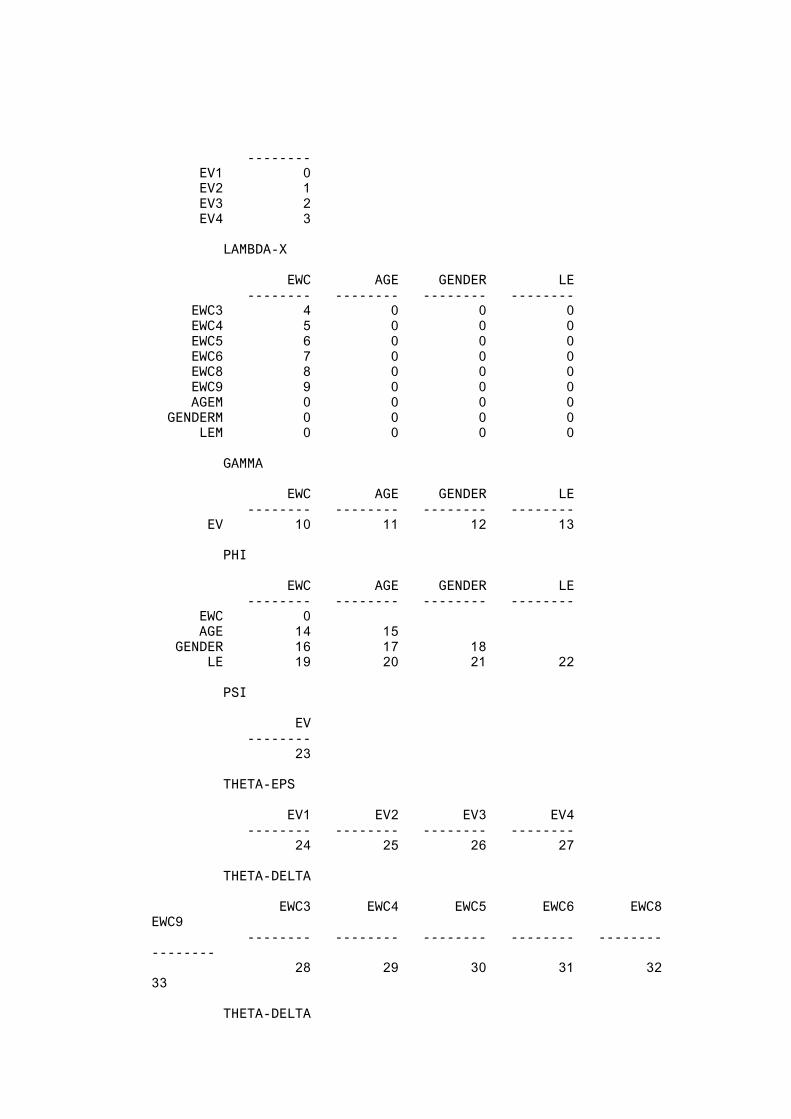

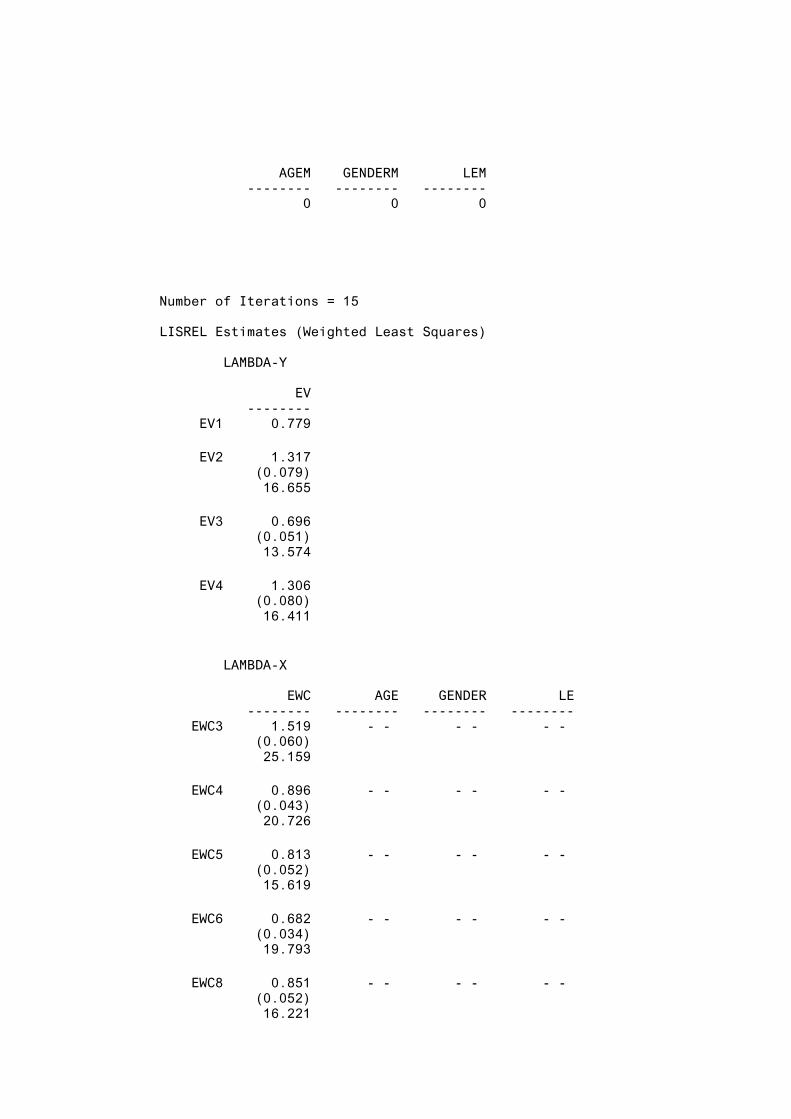

3.5. Data Analysis

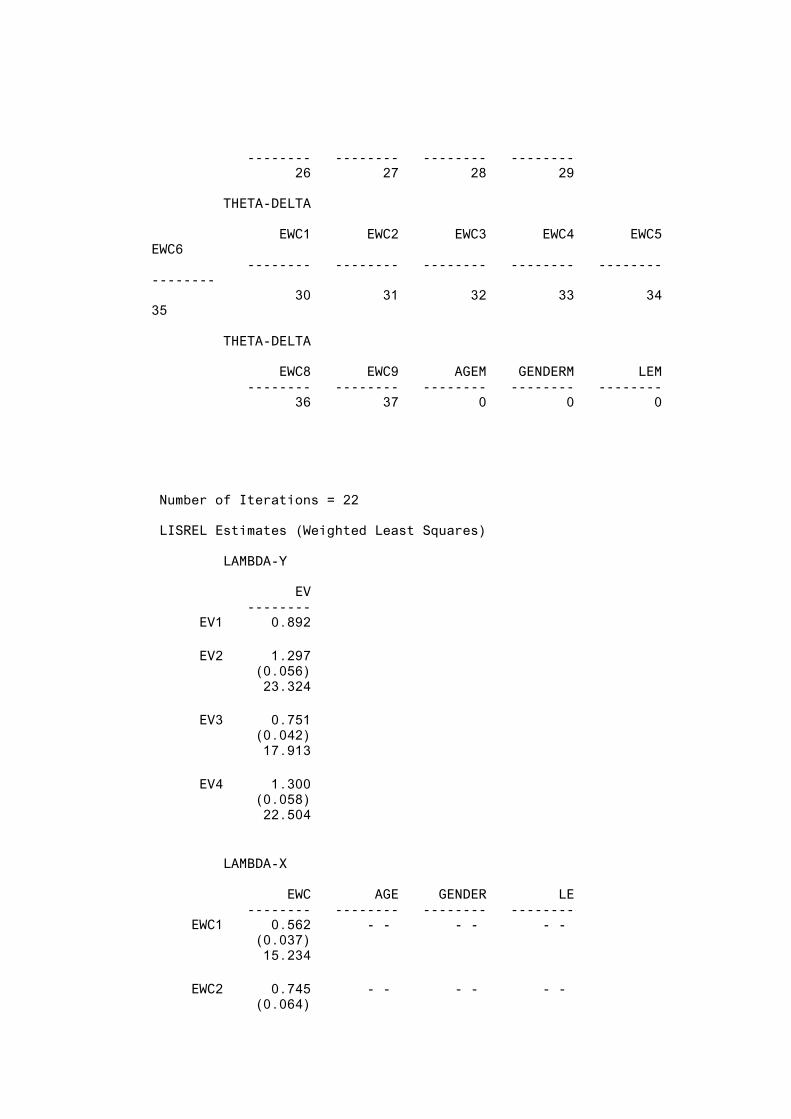

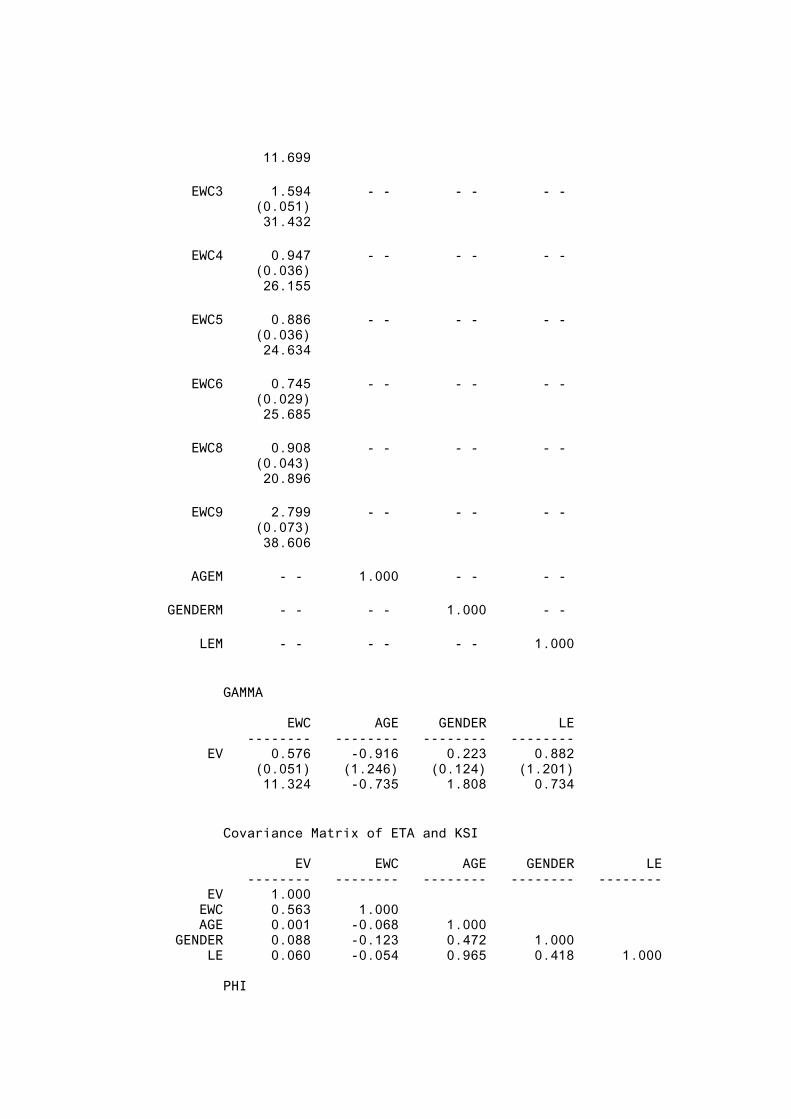

The research model is tested using structural equation modeling.

Structural equation modeling (SEM) is used to describe the causal relation among

the latent variables. The software for data processing is used LISREL. SEM is

also able to give information about factor loading and measurement errors of

variables. SEM is composed of two parts: measurement model and structural

model. Structural model describes relationship between latent variables.

Meanwhile, measurement model describes factor loading between observed

variables and latent variables.

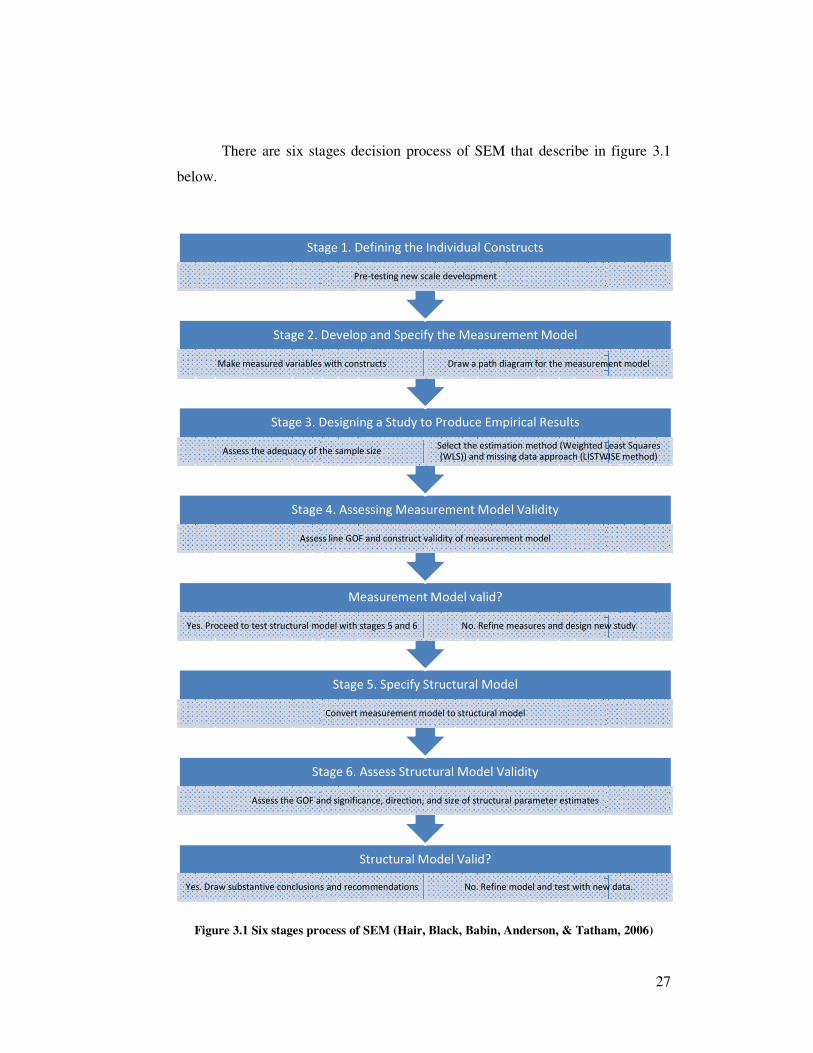

There are six stages decisi

below.

Figure 3.1 Six stages process of SEM

Yes. Draw substantive conclusions and recommendations

Stage 6. Assess Structural Model Validity

Assess the GOF and significance, direction, and size of structural parameter estimates

Yes. Proceed to test structural model with stages 5 and 6

Stage 4. Assessing Measurement Model Validity

Assess line GOF and construct validity of measurement model

Stage 3. Designing a Study to Produce Empirical Results

Assess the adequacy of the sample size

Stage 2. Develop and Specify the Measurement Model

Make measured variables with constructs

Stage 1. Defining the Individual Constructs

six stages decision process of SEM that describe in

Six stages process of SEM (Hair, Black, Babin, Anderson, & Tatham, 2006)

Structural Model Valid?

Yes. Draw substantive conclusions and recommendations No. Refine model and test with new data.

Stage 6. Assess Structural Model Validity

Assess the GOF and significance, direction, and size of structural parameter estimates

Stage 5. Specify Structural Model

Convert measurement model to structural model

Measurement Model valid?

Yes. Proceed to test structural model with stages 5 and 6 No. Refine measures and design new study

Stage 4. Assessing Measurement Model Validity

Assess line GOF and construct validity of measurement model

Stage 3. Designing a Study to Produce Empirical Results

Assess the adequacy of the sample sizeSelect the estimation method (Weighted Least Squares

(WLS)) and missing data approach (LISTWISE method)

Stage 2. Develop and Specify the Measurement Model

Make measured variables with constructs Draw a path diagram for the measurement model

Stage 1. Defining the Individual Constructs

Pre-testing new scale development

27

in figure 3.1

(Hair, Black, Babin, Anderson, & Tatham, 2006)

No. Refine model and test with new data.

No. Refine measures and design new study

Select the estimation method (Weighted Least Squares

(WLS)) and missing data approach (LISTWISE method)

Draw a path diagram for the measurement model

28

The six stages process is consistent with two-step SEM process. By two-

step, we test the fit and construct validity of the proposed measurement model.

Once a satisfactory measurement model is achieved, the second step is to test the

structural theory. Both of steps are assessing fit and the validity. Researcher

illustrates the six stages in detail as below.

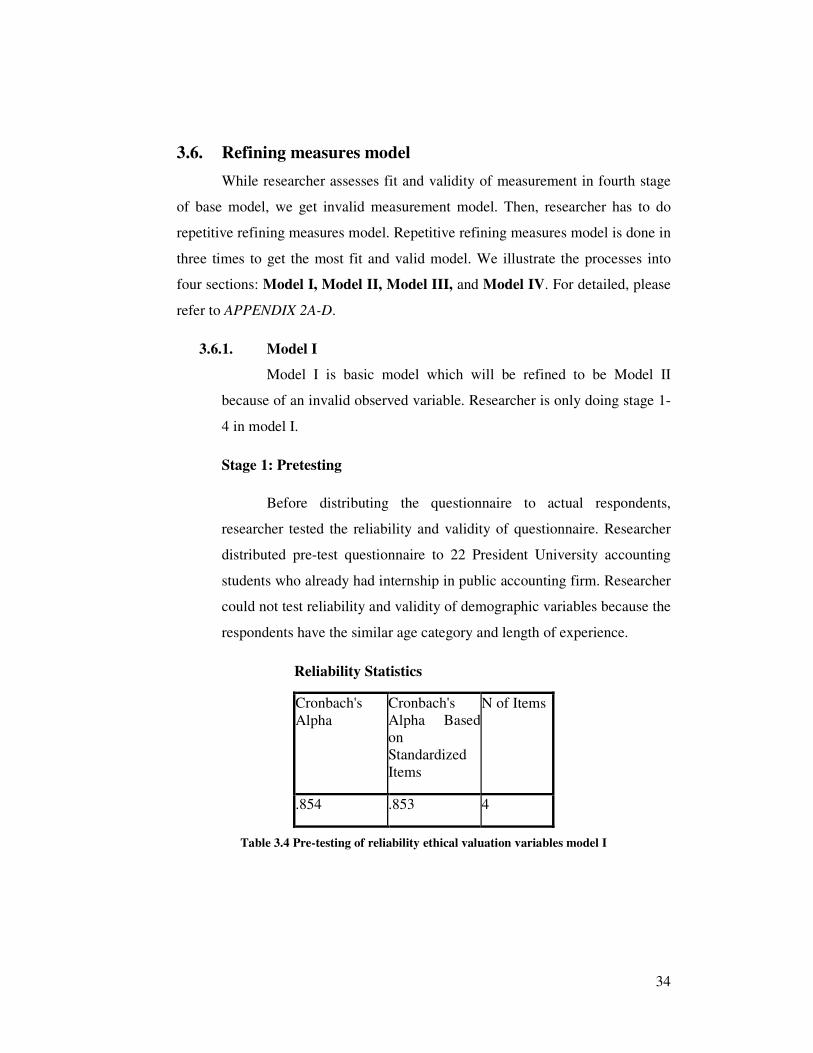

Stage 1: Defining individual constructs (Pretesting questionnaire)

The collected questionnaires are adopted and explored by researcher.

Cause of the new scale items, researcher should do pretesting questionnaire by

testing the reliability and validity among constructs. The reliability and validity

testing discussed as below.

1. Test reliability

Reliability testing is a measurement to test whether respondents could

answer the question consistently or not. There are two latent variables

such as ethical evaluation and ethical work climate. The measurement of

these variables is measured by statistics testing Cronbach Alpha (α).

Based on Nunnaly criterion, variables are reliable if their alpha is above

60% (Ghozali, 2006).

2. Test validity

Test validity is a measurement if the questions have already measured

what researcher wants to. Researcher uses Kaiser Meyer Oikin (KMO)

and Barlett’s Test to test validity among constructs. Based on the criteria

which is KMO should be more than 0.5 (Ghozali, 2006), the test factor

analysis could be done.

Stage 2: Developing and specifying the measurement model

In this stage, each latent construct to be included in the model is identified

and the measured indicator variables (items) are assigned to latent constructs.

This process will be represented with diagram in the next section.

29

Stage 3: Designing a study to produce empirical results

Designing a study to produce empirical results, we should concern about

two issues which are missing value method and estimation technique.

1. Weighted Least Square (WLS) Estimator

When assumption of multivariate normality is not met, researcher could

use alternative estimation technique which is Weighted Least Square

(WLS) (Hair, Black, Babin, Anderson, & Tatham, 2006). WLS is

estimation method that adapted from Asymptotically Distribution Free

(ADF). ADF is general estimation which does not depend on type of

distribution data. WLS needs ten respondents for each observed variable

(Wijayanto, 2008).

2. LISTWISE method

LISTWISE method or complete case approach is the simplest method for

dealing with missing data. Even though, it is easy for use, LISTWISE

method increases the likelihood of non-convergence (SEM program

cannot find any solution). But we can tackle this disadvantage because we

have large sample sizes (283 samples).

Stage 4: Assessing measurement model validity

Three measurements are using for assessing measurement model validity.

All the measurement should be valid to continue to the next stage.

1. Goodness-of-fit (GOF)

Hair, Black, Babin, Anderson, & Tatham (2006) categorize GOF indices

into three groups: absolute fit measures, incremental fit indices, and

parsimony fit indices. Absolute fit measures are direct measures of how

well the model specified the researcher reproduces the observed data.

Incremental fit indices assess how well a specified model fits relative to

some alternative baseline model. Parsimony fit indices are designed

30

specially to provide information about which model among sets if

competing models is the best, considering its fit relative to its complexity.

According to Hair, Black, Babin, Anderson, & Tatham (2006), using three

to four fit indices provides adequate evidence of model fit. The researcher

should report at least one incremental index and one absolute indices, in

addition to the χ2 and the associated degree of freedom. At least one of the

indices should be a badness of fit index. There are characteristics of

different fit indices used in demonstrating goodness of fit across different

model situation (Hair, Black, Babin, Anderson, & Tatham, 2006).

N<250 N>250

m≤12 12<m<30 m≥30 m≤12 12<m<30 m≥30

χ2 Insignificant

ρ-values

expected.

Significant

ρ-values

can result

even with

good fit.

Significant

ρ-values

expected.

Insignificant

ρ-values

expected.

Significant

ρ-values

expected.

Significant

ρ-values

expected.

CFI or

TLI

0.97 or

better.

0.95 or

better.

Above

0.92.

0.95 or

better.

Above

0.92.

Above

0.90.

SRMR Could be

biased

upward, use

other

indices.

0.80 or

less (with

CFI of

0.95 or

higher)..

Less than

0.09 (with

CFI above

0.92)

Could be

biased

upward, use

other

indices.

0.80 or

less (with

CFI of

0.92 or

higher).

0.80 or

less (with

CFI of

0.92 or

higher).

RMSEA Values <

0.08 with

CFI ≥ 0.97.

Values <

0.08 with

CFI ≥

0.95.

Values <

0.08 with

CFI ≥

0.92.

Values <

0.07 with

CFI ≥ 0.97.

Values <

0.07 with

CFI ≥

0.92.

Values <

0.07 with

CFI ≥

0.90.

Table 3.3 Goodness-of-fit indices based on situational criterion (Hair, Black, Babin,

Anderson, & Tatham, 2006)

31

Beside the above criteria, researcher could use indices below to

accept the overall fit.

a. Goodness-of-Fit Index (GFI) is less sensitive to sample size. Its

range value is 0 to 1 with higher values indicating better fit. In the

past, GFI values of greater than 0.90 typically were considered good.

Others argue 0.95 should be used (Hair, Black, Babin, Anderson, &

Tatham, 2006). Meanwhile, 0.80 ≤ GFI ≤ 0.90 is called marginal fit

(Wijayanto, 2008).

b. Normed Fit Index (NFI) is ratio of the difference in the χ2

value for

the fitted model and a null model divided by χ2

value for null model. A

model with perfect ft would produce an NFI of 1 (Hair, Black, Babin,

Anderson, & Tatham, 2006). NFI value ≥ 0.90 shows good fit and

0.80 ≤ NFI < 0.90 is referred to marginal fit (Wijayanto, 2008).

c. Adjusted Goodness of Fit Index (AGFI) is extended of GFI that

adjusted with ratio between degree of freedom of null or independence

or baseline model and degree of freedom of estimated model. Like as

GFI, AGFI value is around 0 to 1 and AGFI value that is higher than

or equal to 0.90 shows good fit. Meanwhile, 0.80 ≤ GFI < 0.90 is

usually called as marginal fit.

d. Parsimonious Normal Fit Index (PNFI) and Parsimony Goodness-

of-fit Index (PGFI) consider the number of degree of freedom to

achieve a good fit (Wijayanto, 2008). The values of the PNFI and

PGFI are meant to be used in comparing one model to another with the

highest PNFI and PGFI value being most supported with respect to the

criteria captured by these indices (Hair, Black, Babin, Anderson, &

Tatham, 2006).

2. Construct validity

To assess construct validity, researcher examines validity testing and

reliability testing as follows.

32

a. Validity testing of measurement model.

According to Ridgon & Ferguson (1991) and Doll, Xia, & Torkzadeh

(1994), a variable is valid if t-value of factor loading should be equal or

more than its critical value (or 1.96) and its standardized factor loading is

equal and higher than 0.70. Hair, Black, Babin, Anderson, & Tatham

(2006) state that standardized factor loading ≥ 0.50 is very significant.

b. Reliability testing of measurement model

Two measurements that could measure the reliability of measurement

model are:

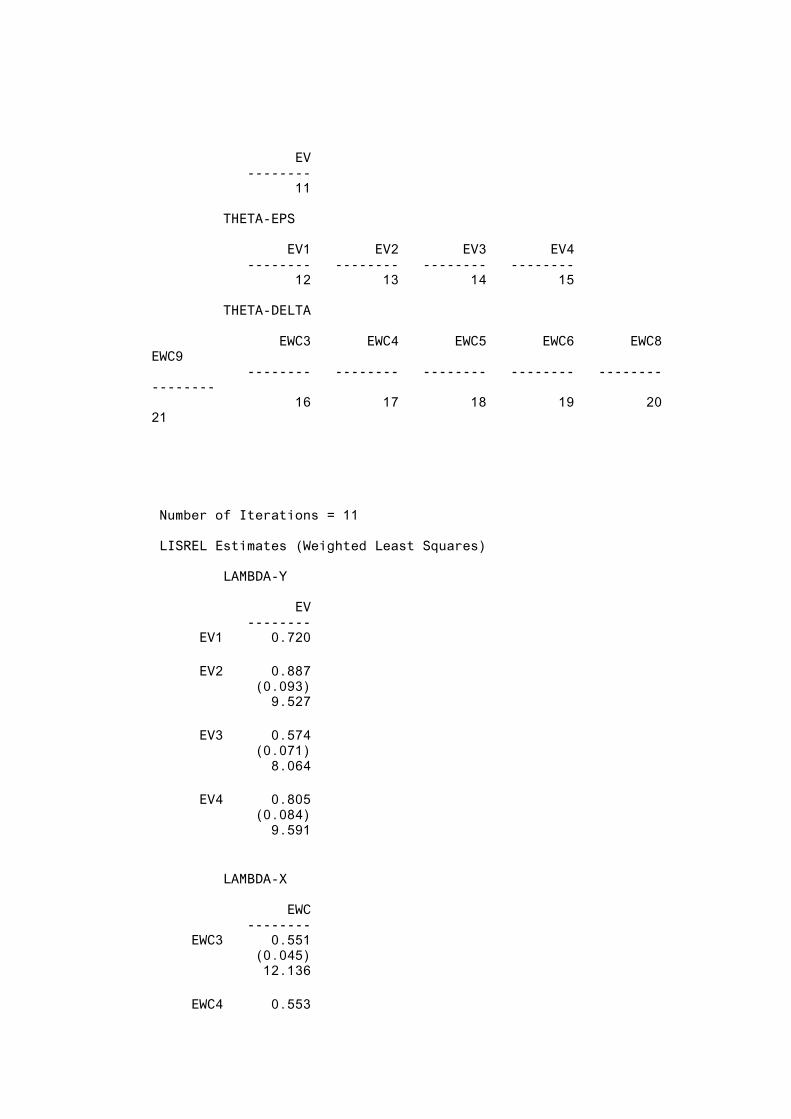

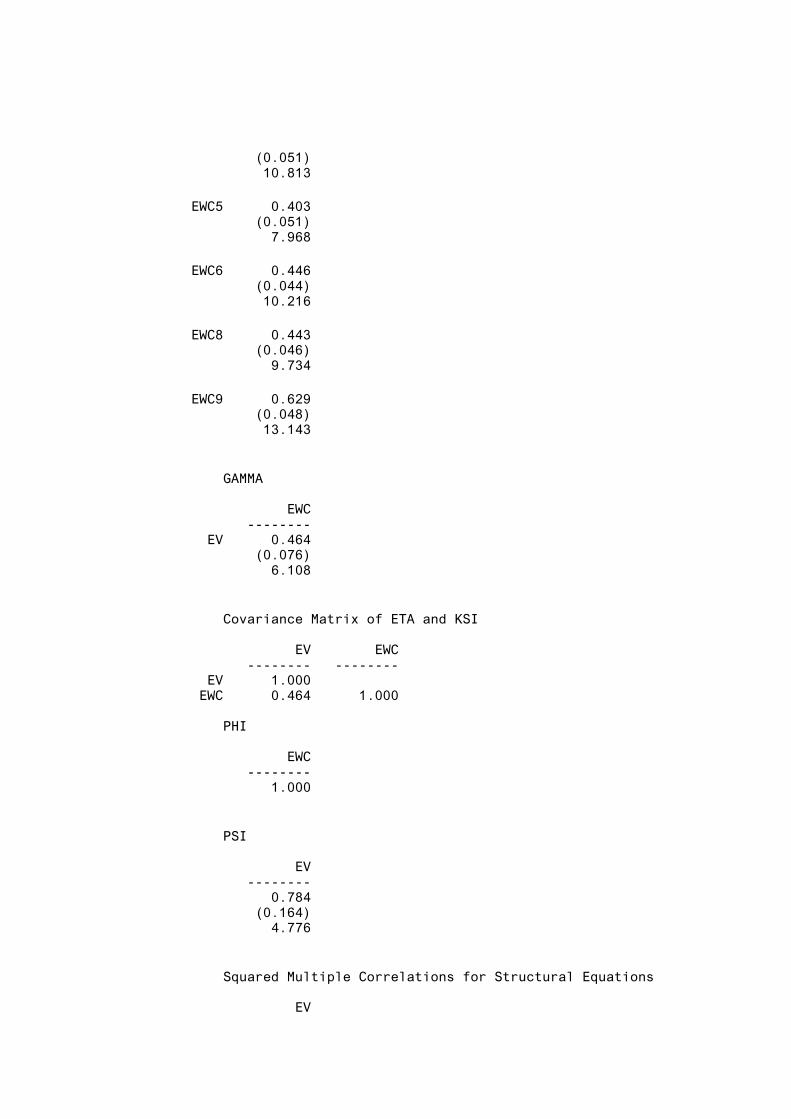

Construct reliability measure

��������� ��� ������ = �∑ ��� �� ���� ��

�∑ ��� �� ������

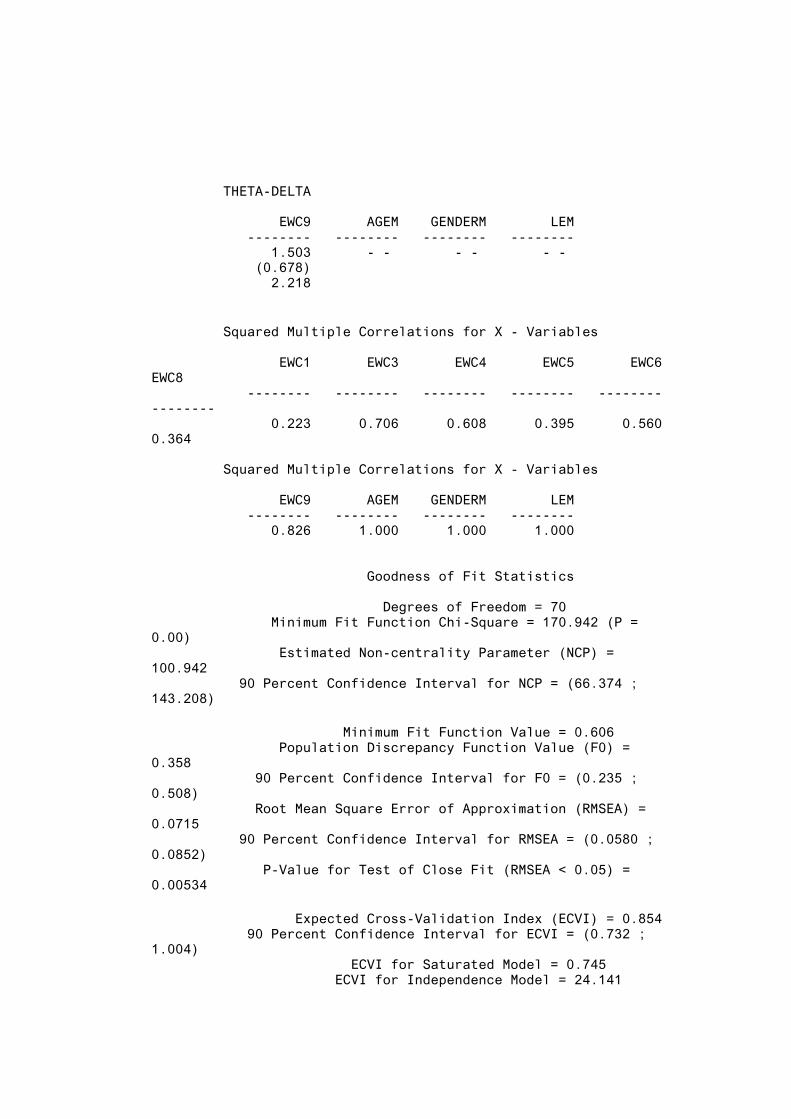

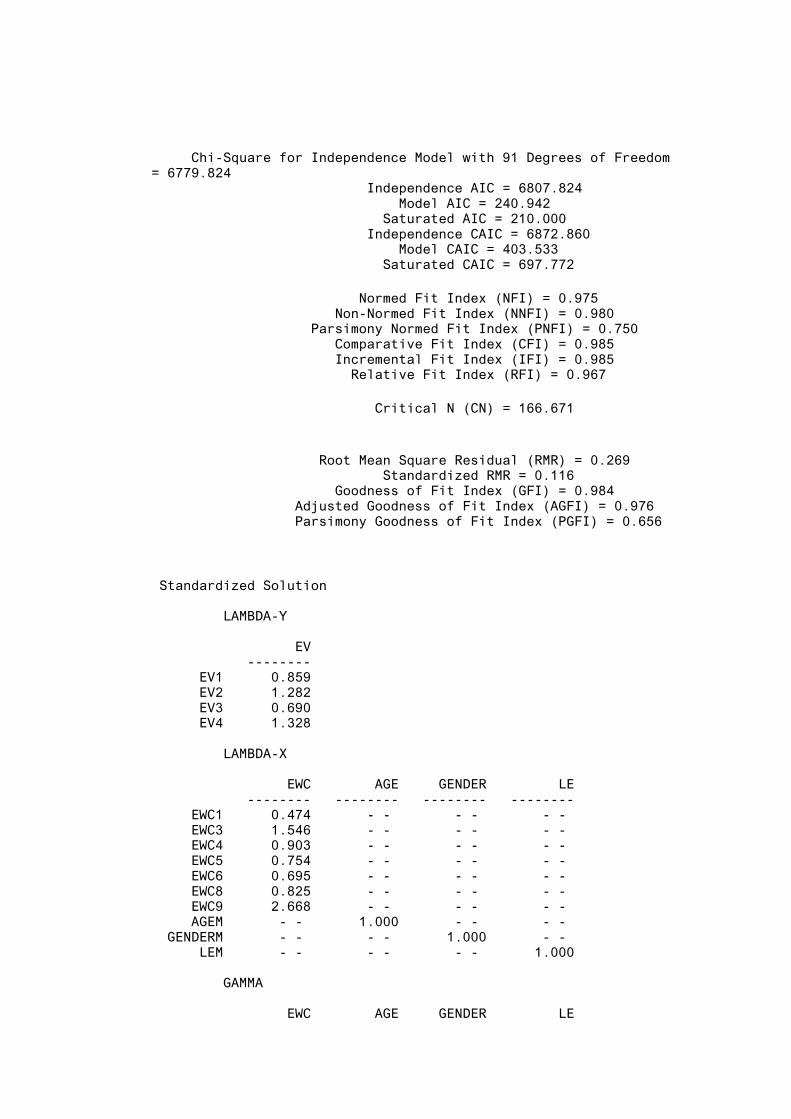

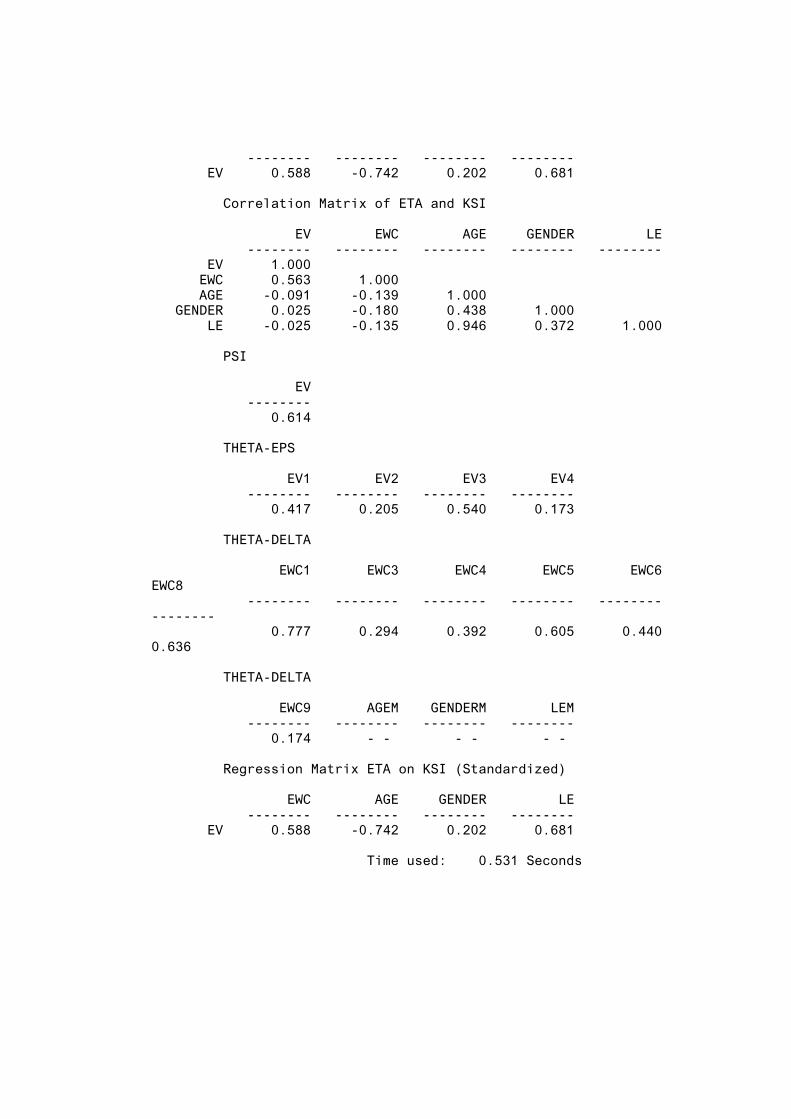

+ ∑ �

Note:

Std. loading = standardized loading

ej = measurement error.

Variance extracted measure

Variance extracted = ∑ ���. �� ����

�

∑ ���. �� �����

+ ∑ �

Note:

Std. loading = standardized loading

ej = measurement error.

Hair, Black, Babin, Anderson, & Tatham (2006) stated that a construct is

reliable if construct reliability (CR) ≥ 0.07 and variance extracted (VE) ≥

0.05.

33

Stage 5: Specifying the structural model

Stage 5 involves specifying the structural model by assigning relationships

from one construct to another based on the proposed theoretical model (Hair,

Black, Babin, Anderson, & Tatham, 2006). In detail, it will be illustrated in the

next chapter.

Stage 6: Assessing the structural model validity

The fit of structural model can be tested by structural model GOF. The

overall fit can be assessed using the same criteria as the measurement model:

using the χ2 value for structural model, one other absolute index, one incremental

index, one goodness-of-fit indicator, and badness-of-fit indicator (Hair, Black,

Babin, Anderson, & Tatham, 2006). The model of this researcher is considered as

saturated structural model then, the fit for saturated theoretical model should be

the same as those obtained for the CFA model. Researcher does not need to test

goodness-of-fit of structural model.

Good model fit alone is insufficient to support a proposed theory.

Researcher also examines the individual estimation to test specific hypothesis. A

theoretical model is considered valid to the extent that the parameter estimates are

statistically significant and in the predicted direction (Hair, Black, Babin,

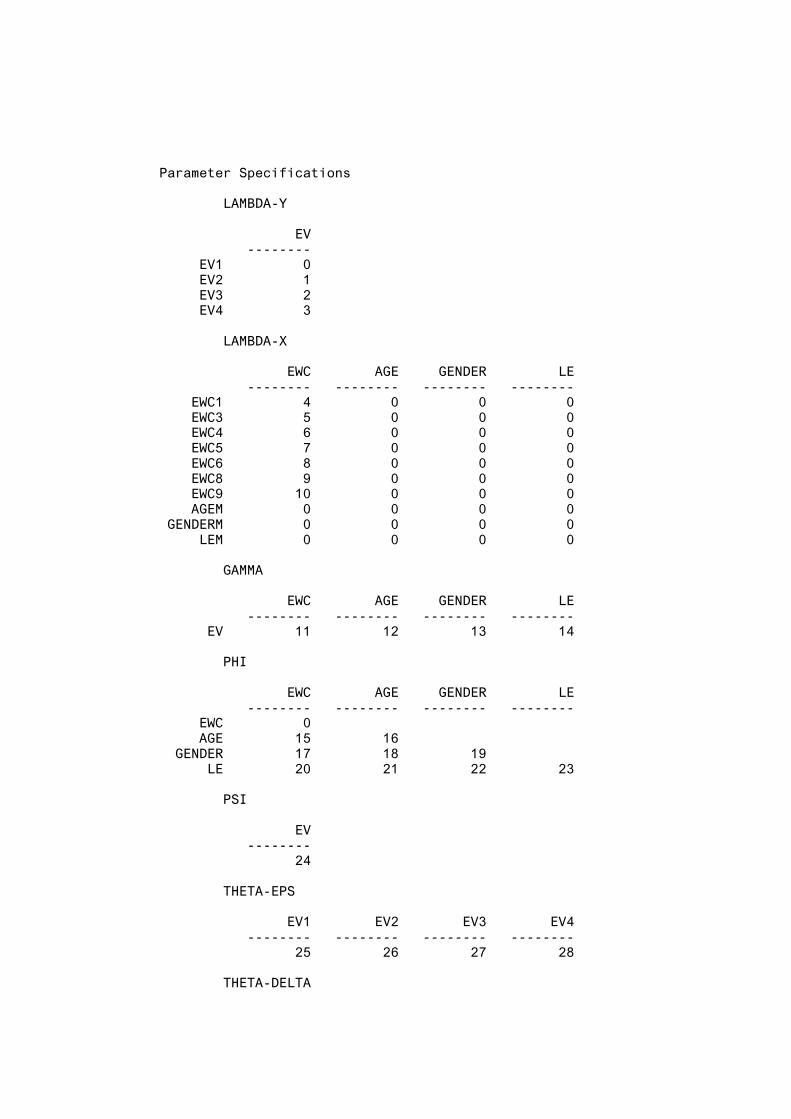

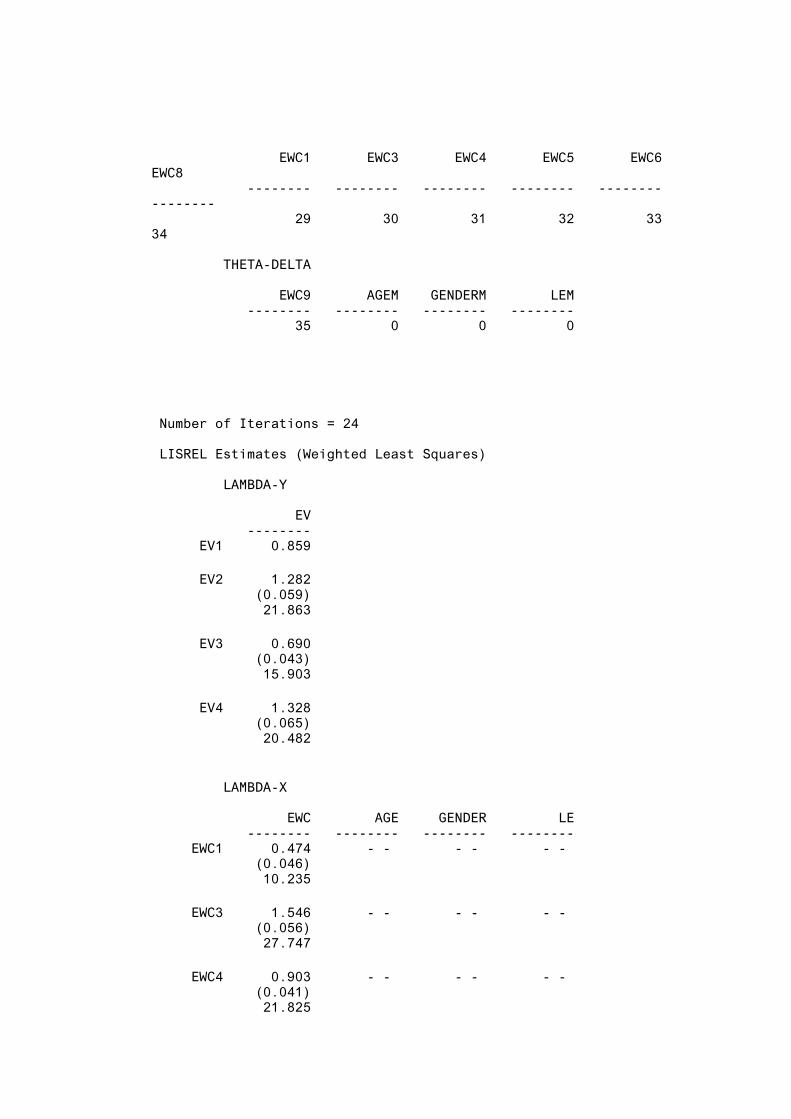

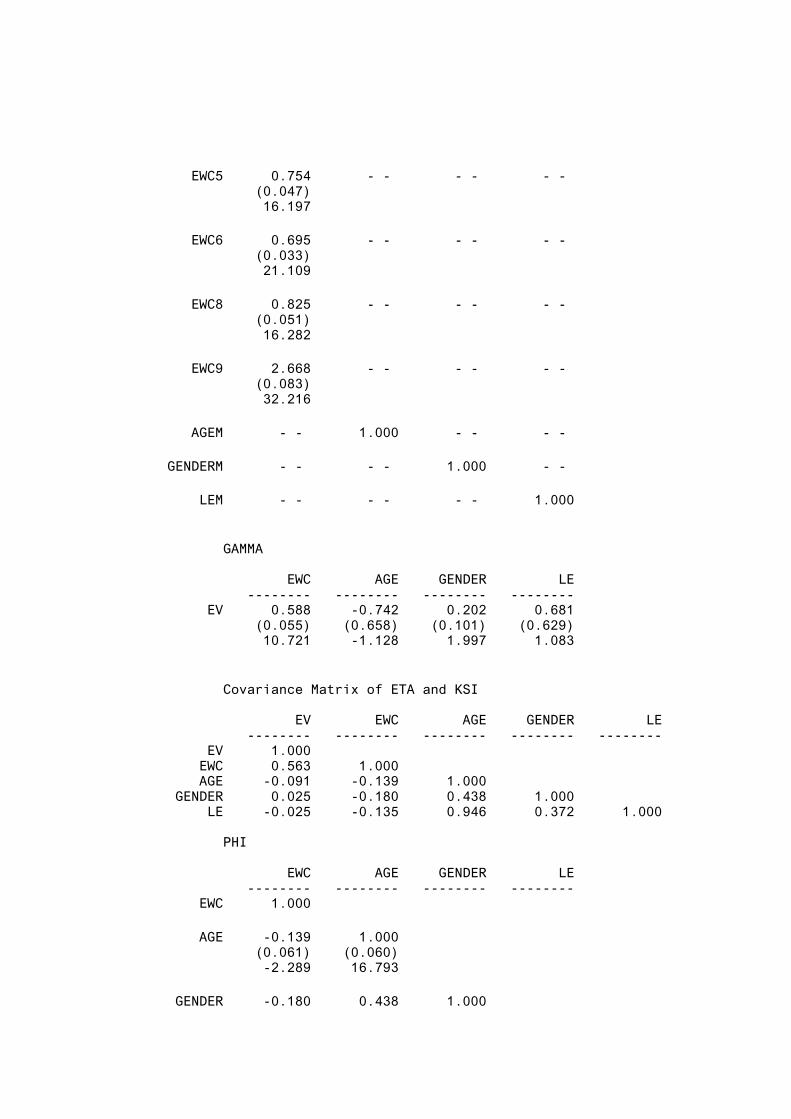

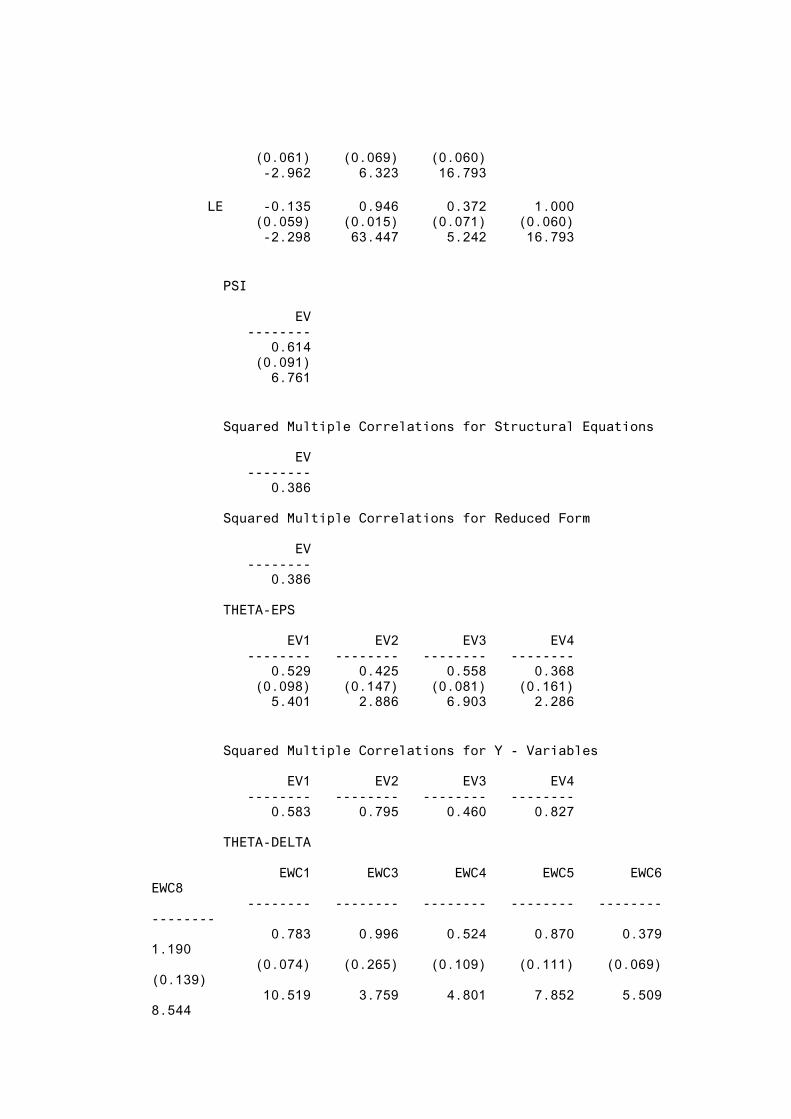

Anderson, & Tatham, 2006). As other multivariate techniques, the significant