CHAPTER 7 SALES AND COLLECTION CYCLE

Timing of Revenue Recognition

Revenue Recognition: Some Examples (pp. 258-9)

Using the example in the text, if the Atlanta Braves collected $450,000 in advance ticket sales in March of 2001 and 10% of the games the tickets were sold for were played in April, the journal entries to record the transactions would be as follows:

Date Transaction Debit Credit 3/2001 Cash $450,000

Unearned ticket revenue $450,000

To record collection for advance ticket sales

4/2001 Unearned revenue $45,000 Ticket revenue earned . $45,000

To recognize revenue earned from advance ticket sales The FSU ticket office has sold $100,000 worth of tickets for the upcoming football season. There are six home games. Prepare the journal entry to record the sale, assuming the tickets were sold several months before the football season starts. Prepare the journal entries to record the revenue recognition in September (half the games were played) and October (one-third of the games were played).

STUDY BREAK 7-1 (p. 259) SEE HOW YOU’RE DOING

Sales Discounts (pp. 259-60) Suppose you sold $1,000 worth of merchandise to a customer with the terms 2/10, n/30, and the customer paid within the discount period. The journal entries are as follows:

Date Transaction Debit Credit Accounts receivable $1,000

Sales $1,000

To record the sale of inventory, terms 2/10, n/30

39

Date Transaction Debit Credit

Cash $980 Sales discounts 20 Accounts receivable $1,000

To record accounts receivable collections

In March, Good Buy Company sold merchandise for $3,500 with the terms 3/10, n/30. Customers always take advantage of cash discount offers. Prepare the journal entries to record Good Buy Company's March sales and accounts receivable collections.

STUDY BREAK 7-2 (p. 260) SEE HOW YOU’RE DOING

Sales Returns (pp. 260-61) If $10,000 worth of merchandise was sold and $2,000 was returned, the entries would be as follows:

Date Transaction Debit Credit Cash or Accounts receivable $10,000

Sales $10,000

To record merchandise sales

Sales returns $2,000 Cash or Accounts receivable $2,000

To record the return of merchandise

Accounting for Cash (pp. 261 - 64)

When doing a bank reconciliation, every adjustment to the balance per books requires a journal entry to update the cash account, as well as adjust other accounts as needed. Based upon the Low Company example, the following journal entries are required:

Date Transaction Debit Credit 5/31/2002 Cash $1,030

Notes receivable $1,000 Interest revenue 30

To record collection of a notes receivable by the bank (assuming $1,000 principal and $30 interest)

40

Date Transaction Debit Credit 5/31/2001 Operating expense $ 10 Accounts receivable 100 Accounts payable 18

Cash $128

To record bank service charges and necessary account balance corrections

ABC Company’s unadjusted book balance for cash amounted to $2,400. The company’s bank statement included a debit memo for bank service charges of $100. There were two credit memos. One was for $300, which represented a collection that the bank made for ABC. The second credit memo was for $100, which represented the amount of interest that ABC had earned on its bank accounts during the period. Outstanding checks amounted to $250 and there were no deposits in transit. Prepare the journal entries that would be required to adjust ABC Company's cash account.

STUDY BREAK 7-3 (p. 264) SEE HOW YOU’RE DOING

Accounts Receivable: Collecting Payment for Sales Made on Account

Direct Write-Off Method (pp. 264-5) If you use the direct write-off method, no bad debt expense is recorded until a specific debt is determined to be uncollectible. For example, if you determine that a $150 account is uncollectible, the journal entry is as follows:

Date Transaction Debit Credit Bad debt expense $150

Accounts receivable $150

To record the write-off of an uncollectible account.

Gloria’s Glassware uses the direct write-off method to account for bad debts. In 2005, Gloria sold $20,000 on account. She estimated that between $100 and $150 would eventually go uncollected. No specific accounts were identified as uncollectible during 2005. In 2006, a credit customer who owed Gloria $35 filed for bankruptcy. Gloria wants to remove that customer’s account from her outstanding Accounts receivable. Prepare the journal entries to account for Gloria’s bad debt expense that are required in 2005 and 2006.

STUDY BREAK 7-4 (p. 265) SEE HOW YOU’RE DOING

41

Allowance Method (pp. 265-69)

Sales. Under the sales method, the bad debt expense estimate is based upon a percentage of sales. If sales for the year total $100,000 and you estimate that 5% are uncollectible, the journal entry is:

Date Transaction Debit Credit Bad debt expense $5,000

Allowance for uncollectible accounts $5,000

To record the estimate for bad debts based on the sales method

When using the allowance method and an actual $150 account is determined to be uncollectible, the journal entry reduces the Allowance account and Accounts receivable. No bad debt expense is recorded at the time of an actual writeoff.

Date Transaction Debit Credit Allowance for uncollectible accounts $150

Accounts receivable $150

To record the write-off of an uncollectible account

Accounts Receivable. Following the Good Guys Company example in the text, the journal entries relating to bad debt expense and the allowance for doubtful accounts for the first two years are as follows:

Date Transaction Debit Credit 12/31/2003 Bad debt expense $2,078

Allowance for uncollectible accounts $2,078

To record the estimate for bad debts based on the accounts receivable aging method

Date Transaction Debit Credit

Allowance for uncollectible accounts $600 Accounts receivable (Dibbs) $600

To record the write-off of M. Dibb’s account

1/1 – 12/31 2004 Allowance for uncollectible accounts $1,400 Accounts receivable (various) $1,400

To record the write-off of other uncollectible accounts.

12/31/2004 Bad debt expense $2,422 Allowance for uncollectible accounts $2,422

To record the estimate for bad debts based on the accounts receivable aging method ($2,500 estimated uncollectible amount - $78 overestimated amount from 2003)

42

Suppose at the end of the year, Pendleton Corp. records showed the following: Allowance for uncollectible accounts 0 (excess from prior year) 100 Bad debt expensea 0 Accounts receivable 10,000 a Bad debt expense has a zero balance because no adjustments have been made. Pendleton estimated the end-of-year uncollectible accounts receivable to be $500, based on an aging schedule of current accounts receivable. Prepare the journal entry to record bad debt expense for the year.

STUDY BREAK 7-5 (p. 269) SEE HOW YOU’RE DOING

Credit Card Sales (pp. 269 - 70)

If Wally Tire Company makes $1,000 of MasterCard sales and the MasterCard fee is 5%, the journal entry to record the day’s sales is as follows: Date Transaction Debit Credit Accounts receivable (MasterCard) $ 950 Credit card expense 50

Sales revenue $1,000 To record the day’s credit card sales

During December, Magic Cow Company made a $5,000 MasterCard sale to a customer. MasterCard charges Magic Cow a fee of 3% of sales for its services. Prepare the journal entry to record this transaction.

STUDY BREAK 7-6 (p. 270) SEE HOW YOU’RE DOING

Warranties (pp. 270 - 1) If Brooke’s Bike Company sold 100 bikes in the month of June with a 1-year warranty and the accountant estimated that each bike will require $30 worth of warranty repairs, the journal entry to record the warranty expense and related liability is as follows:

43

Date Transaction Debit Credit 6/30 Warranty expense $3,000

Estimated warranty liability $3,000 To record the estimated warranty expense/liability for June sales

In July, Brooke’s didn’t make any sales, but they did incur $250 of repair costs related to June sales. The journal entry to record the repair costs is as follows:

Date Transaction Debit Credit 7/1 – 7/31 Estimated warranty liability $250

Cash $250 To record the warranty repairs made in July

August was another slow month for bicycle sales (none were made), but Brooke’s Bike Company did some warranty repairs on previous sales. The total spent was $500. Prepare the journal entry to record the repairs.

STUDY BREAK 7-7 (p. 271) SEE HOW YOU’RE DOING

Summary Problem: Tom's Wear Increases Sales in June Transaction 1 Pays cash of $2,400 for 2 months of rent on the warehouse beginning June 15th.

Date Transaction Debit Credit 6/1/2001 Prepaid rent $2,400

Cash $2,400 To record the prepayment of 2 month’s rent Transaction 2

Pays Sam Cubby's salary for May; gross pay $1,000; also makes the payroll tax deposit, including the employer's matching payroll taxes.

Date Transaction Debit Credit 6/5/2001 Salaries payable $723

PayOth

roll taxes withheld 277 er payables 77 Cash $1,077 To record payment of salary and taxes Transaction 3

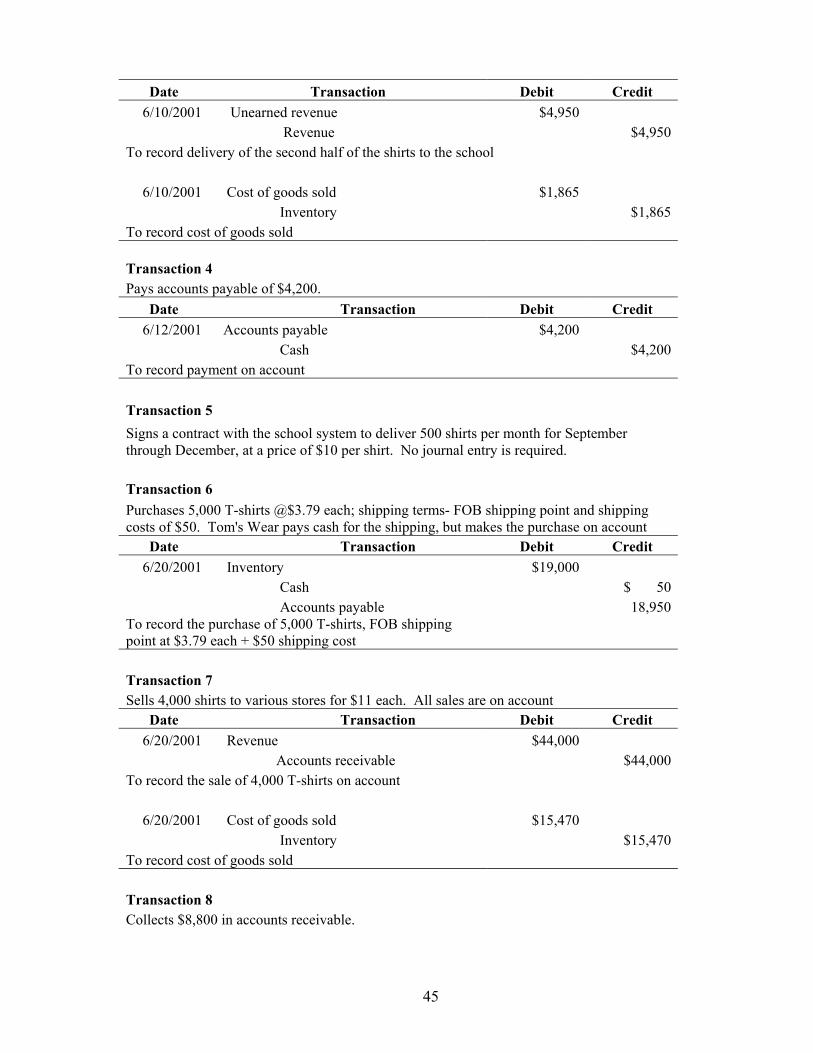

Delivers the second half of the shirts to the school system - 450 shirts - and recognizes revenue of $4,950.

44

Date Transaction Debit Credit 6/10/2001 Unearned revenue $4,950

Cos

Revenue $4,950 To record delivery of the second half of the shirts to the school

6/10/2001 t of goods sold $1,865

Inventory $1,865 To record cost of goods sold Transaction 4 Pays accounts payable of $4,200.

Date Transaction Debit Credit 6/12/2001 Accounts payable $4,200

Cash $4,200 To record payment on account

Transaction 5

Signs a contract with the school system to deliver 500 shirts per month for September through December, at a price of $10 per shirt. No journal entry is required. Transaction 6 Purchases 5,000 T-shirts @$3.79 each; shipping terms- FOB shipping point and shipping costs of $50. Tom's Wear pays cash for the shipping, but makes the purchase on account

Date Transaction Debit Credit 6/20/2001 Inventory $19,000

Cash $ 50 Accounts payable 18,950

To record the purchase of 5,000 T-shirts, FOB shipping point at $3.79 each + $50 shipping cost Transaction 7 Sells 4,000 shirts to various stores for $11 each. All sales are on account

Date Transaction Debit Credit 6/20/2001 Revenue $44,000

Accounts receivable $44,000 To record the sale of 4,000 T-shirts on account

Cos

6/20/2001 t of goods sold $15,470

Inventory $15,470 To record cost of goods sold Transaction 8 Collects $8,800 in accounts receivable.

45

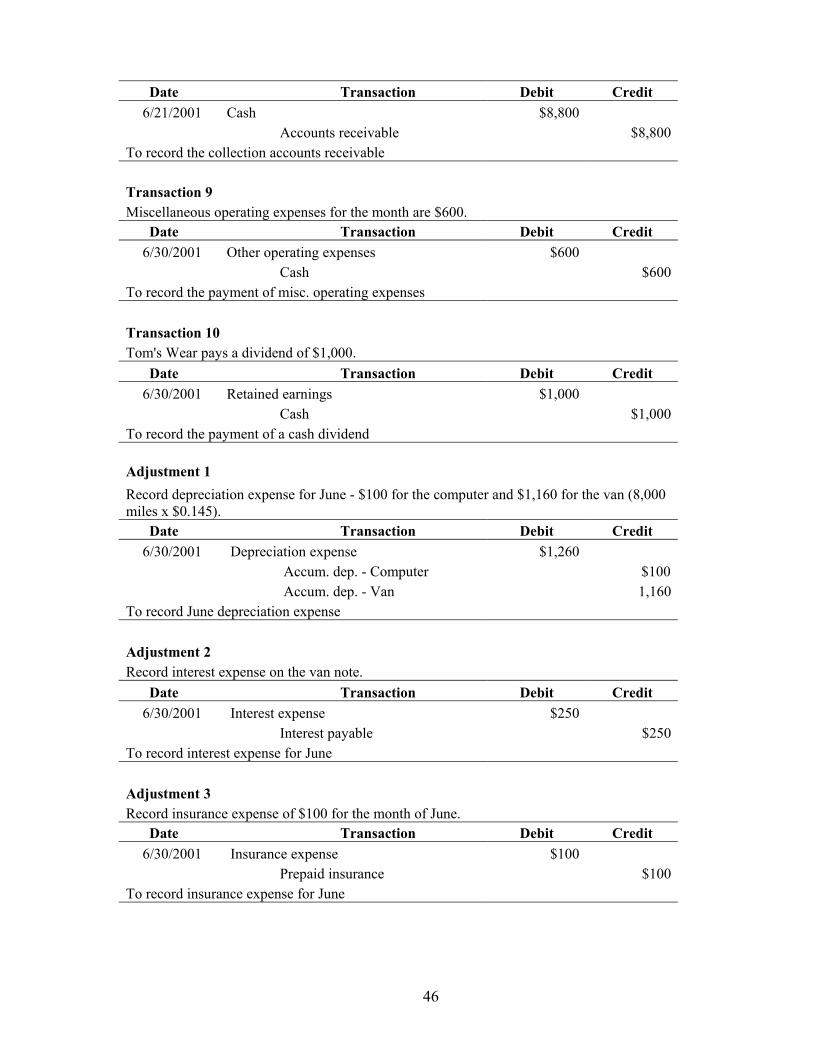

Date Transaction Debit Credit 6/21/2001 Cash $8,800

Accounts receivable $8,800 To record the collection accounts receivable Transaction 9 Miscellaneous operating expenses for the month are $600.

Date Transaction Debit Credit 6/30/2001 Other operating expenses $600

Cash $600 To record the payment of misc. operating expenses Transaction 10 Tom's Wear pays a dividend of $1,000.

Date Transaction Debit Credit 6/30/2001 Retained earnings $1,000

Cash $1,000 To record the payment of a cash dividend Adjustment 1 Record depreciation expense for June - $100 for the computer and $1,160 for the van (8,000 miles x $0.145).

Date Transaction Debit Credit 6/30/2001 Depreciation expense $1,260

Accum. dep. - Computer $100 Accum. dep. - Van 1,160 To record June depreciation expense Adjustment 2 Record interest expense on the van note.

Date Transaction Debit Credit 6/30/2001 Interest expense $250

Interest payable $250 To record interest expense for June Adjustment 3 Record insurance expense of $100 for the month of June.

Date Transaction Debit Credit 6/30/2001 Insurance expense $100

Prepaid insurance $100 To record insurance expense for June

46

Adjustment 4 Record rent expense of $1,200 for the month of June.

Date Transaction Debit Credit 6/30/2001 Rent expense $1,200

Prepaid rent $1,200 To record rent expense for June Adjustment 5 Record Web costs of $50 for June.

Date Transaction Debit Credit 6/30/2001 Other operating expenses $50

Prepaid Web service $50 To record web maintenance services for June

Adjustment 6

Accrue Sam Cubbie's salary for June, including the employer portion of payroll taxes. Date Transaction Debit Credit

6/30/2001 Salary expense $1,000 Employer's payroll tax expense 77 Payroll taxes withheld $277 Other payables 77 Salaries payable 723 To record the accrual of Sam Cubbie's salary, withholding and payroll taxes

Adjustment 7 Bad debt estimate = 3% of credit sales.

Date Transaction Debit Credit 6/30/2001 Bad debt expense $1,320

Allowance for bad debts $1,320 To record the bad debt estimate for June Adjustment 8 Warranty liability estimate = 2% of total sales.

Date Transaction Debit Credit 6/30/2001 Warranty expense $979

Warranties payable $979 To record the estimated warranty liability for June

47

BB $8,8 8,

$8,

BB $250

2

A

Pre

48

805 $2,400 1 BB $8,900 $8,800 8 $1,320 Adj-7 BB $4,700 $1,865 3 BB $250 $100 Adj-3800 1,077 2 7 44,000 0 0 6 19,000 15,470 7

4,200 4 1,320 15050 6 44,100 6,365

600 9

1,000 10278

$50 Adj-5 BB $600 $1,200 Adj-4 BB $4,000 $300 BB BB $30,000 1 2,400 100 Adj-1

200 4,000 30,0001,800 400

$1,595 BB 4 $4,200 $4,200 BB $500 BB 3 $4,950 $4,950 BB 2 277 $277 Adj-61,160 Adj-1 18,950 6 250 Adj-2 277

02,755 18,950 750 277

77 $77 BB 2 723 $723 BB $979 Adj-8 $30,000 BB $5,000 BB77 Adj-6 723 Adj-6

979 30,000 5,00077 723

Interest payableAccounts payable

Equipment - Van

Warranties payable Notes payable Common stockSalaries payable

Unearned revenuePayroll taxes

withheldcc dep - Van

paid Web service

Other payables

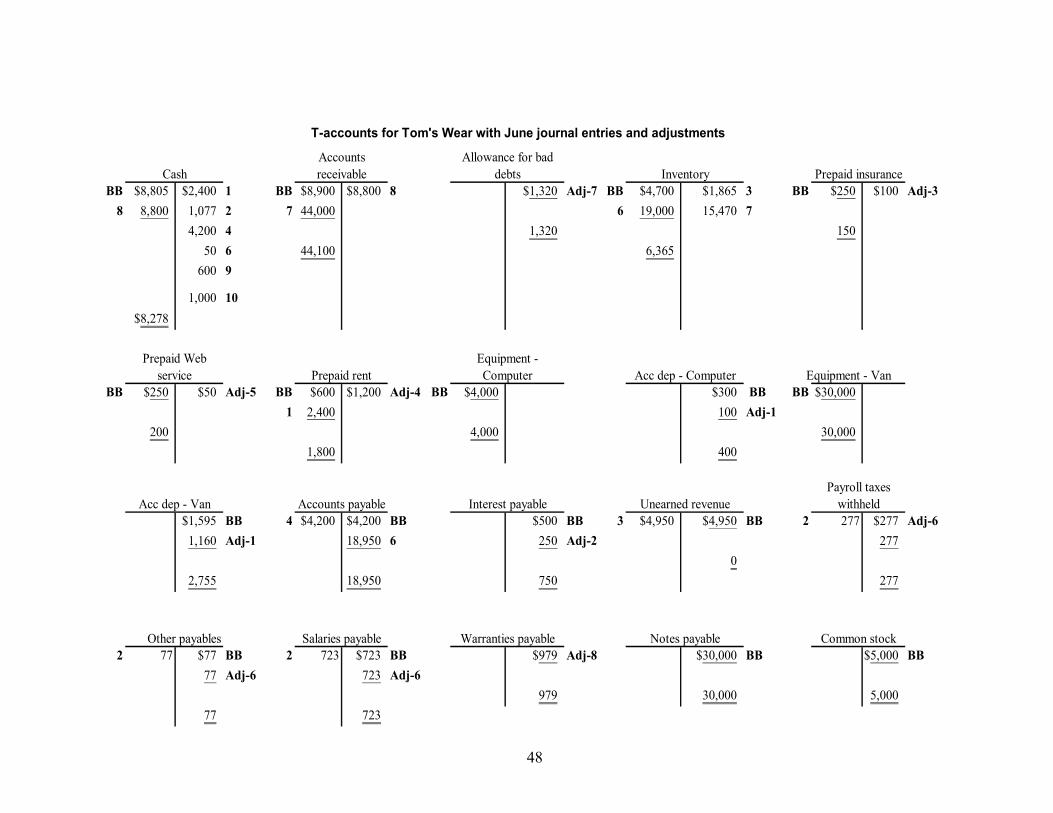

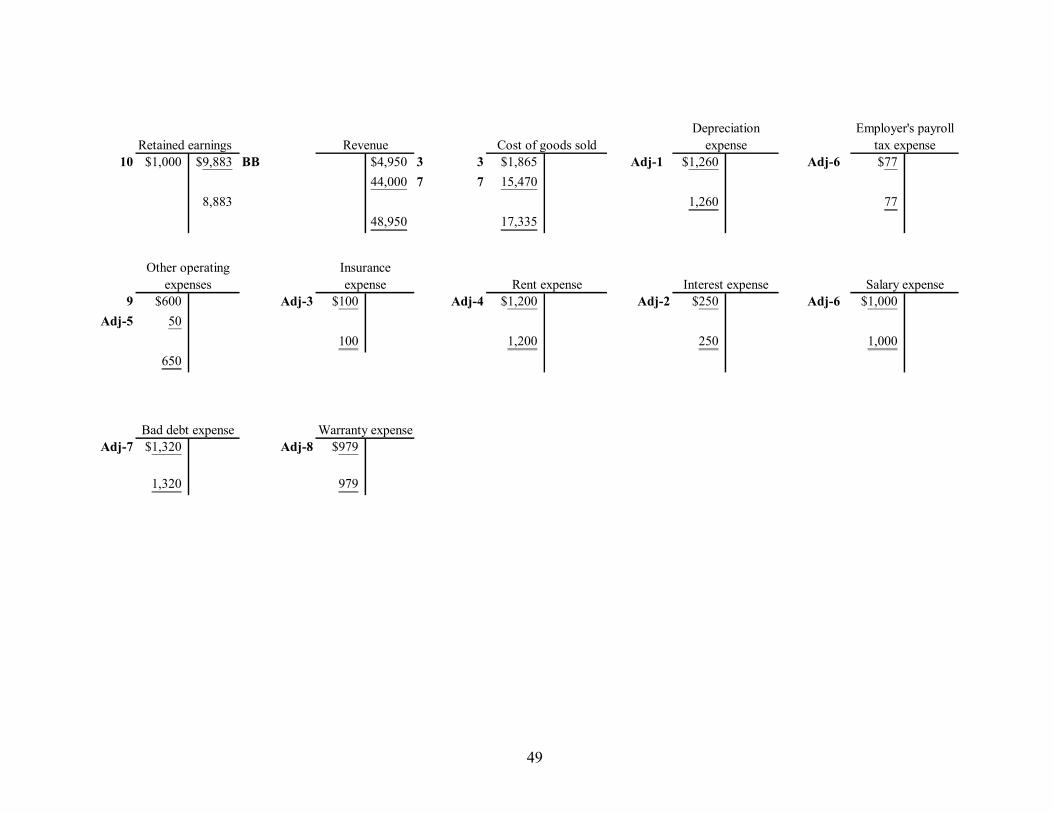

T-accounts for Tom's Wear with June journal entries and adjustments

Prepaid insurance

Equipment - Computer Acc dep - Computer

Accounts receivableCash Inventory

Allowance for bad debts

Prepaid rent

49

Retained earnings10 $1,000 $9,883 BB $4,950 3 3 $1,865 Adj-1 $1,260 Adj-6 $77

44,000 7 7 15,470 8,883 1,260 77

48,950 17,335

9 $600 Adj-3 $100 Adj-4 $1,200 Adj-2 $250 Adj-6 $1,000Adj-5 50

100 1,200 250 1,000650

Adj-7 $1,320 Adj-8 $979

1,320 979

Employer's payrotax expense

Salary expenseInsurance expense

Depreciation expense

Interest expenseRent expense

Cost of goods sold

Bad debt expense Warranty expense

Revenue

Other operating expenses

ll

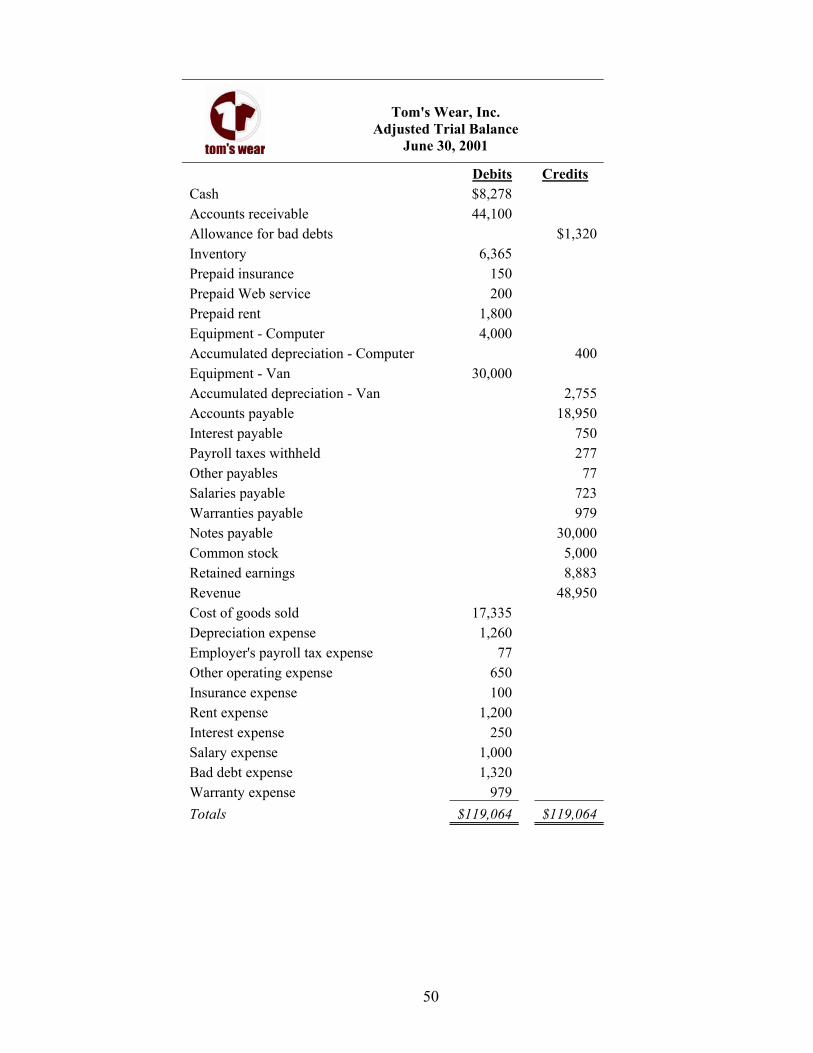

Tom's Wear, Inc. Adjusted Trial Balance

June 30, 2001

Debits Credits Cash $8,278 Accounts receivable 44,100 Allowance for bad debts $1,320 Inventory 6,365 Prepaid insurance 150 Prepaid Web service 200 Prepaid rent 1,800 Equipment - Computer 4,000 Accumulated depreciation - Computer 400 Equipment - Van 30,000 Accumulated depreciation - Van 2,755 Accounts payable 18,950 Interest payable 750 Payroll taxes withheld 277 Other payables 77 Salaries payable 723 Warranties payable 979 Notes payable 30,000 Common stock 5,000 Retained earnings 8,883 Revenue 48,950 Cost of goods sold 17,335 Depreciation expense 1,260 Employer's payroll tax expense 77 Other operating expense 650 Insurance expense 100 Rent expense 1,200 Interest expense 250 Salary expense 1,000 Bad debt expense 1,320 Warranty expense 979 Totals $119,064 $119,064

50

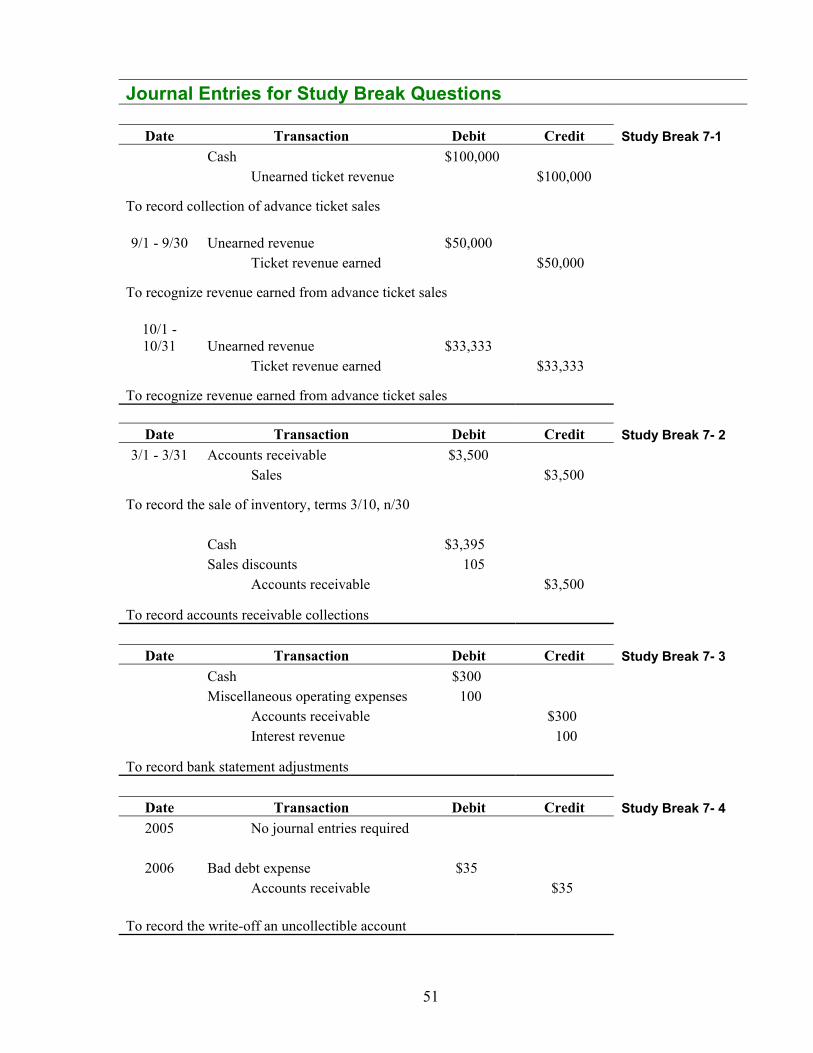

Journal Entries for Study Break Questions

Date Transaction Debit Credit Study Break 7-1 Cash $100,000 Unearned ticket revenue $100,000

To record collection of advance ticket sales 9/1 - 9/30 Unearned revenue $50,000

Ticket revenue earned $50,000

To recognize revenue earned from advance ticket sales

10/1 - 10/31 Unearned revenue $33,333

Ticket revenue earned $33,333

To recognize revenue earned from advance ticket sales

Date Transaction Debit Credit Study Break 7- 2 3/1 - 3/31 Accounts receivable $3,500

Sales $3,500

To record the sale of inventory, terms 3/10, n/30

Cash $3,395 Sales discounts 105

Accounts receivable $3,500

To record accounts receivable collections

Date Transaction Debit Credit Study Break 7- 3 Cash $300 Miscellaneous operating expenses 100 Accounts receivable $300

Interest revenue 100

To record bank statement adjustments

Date Transaction Debit Credit Study Break 7- 4 2005 No journal entries required

2006 Bad debt expense $35

Accounts receivable $35 To record the write-off an uncollectible account

51

Date Transaction Debit Credit Study Break 7- 5 12/31 Bad debt expense $400

Allowance for uncollectible accounts $400

To record bad debt expense

Date Transaction Debit Credit Study Break 7- 6 Dec. Accounts receivable (MasterCard) $4,850

Credit card expense 150 Sales revenue $5,000

To record bad debt expense

Date Transaction Debit Credit Study Break 7- 7 8/1 - 8/31 Estimated warranty liability $500

Cash $500

To record August warranty repairs

Short Exercises

SE7-41Datatech's accountant wrote a check to a supplier for $1,050, but erroneously recorded it on the company's books as $1,500. She discovered this when she saw the monthly bank statement and noticed that the check had cleared the bank for $1,050. Give the journal entry Datatech needs to make to its accounting records to correct this error.

Date Account Debit Credit

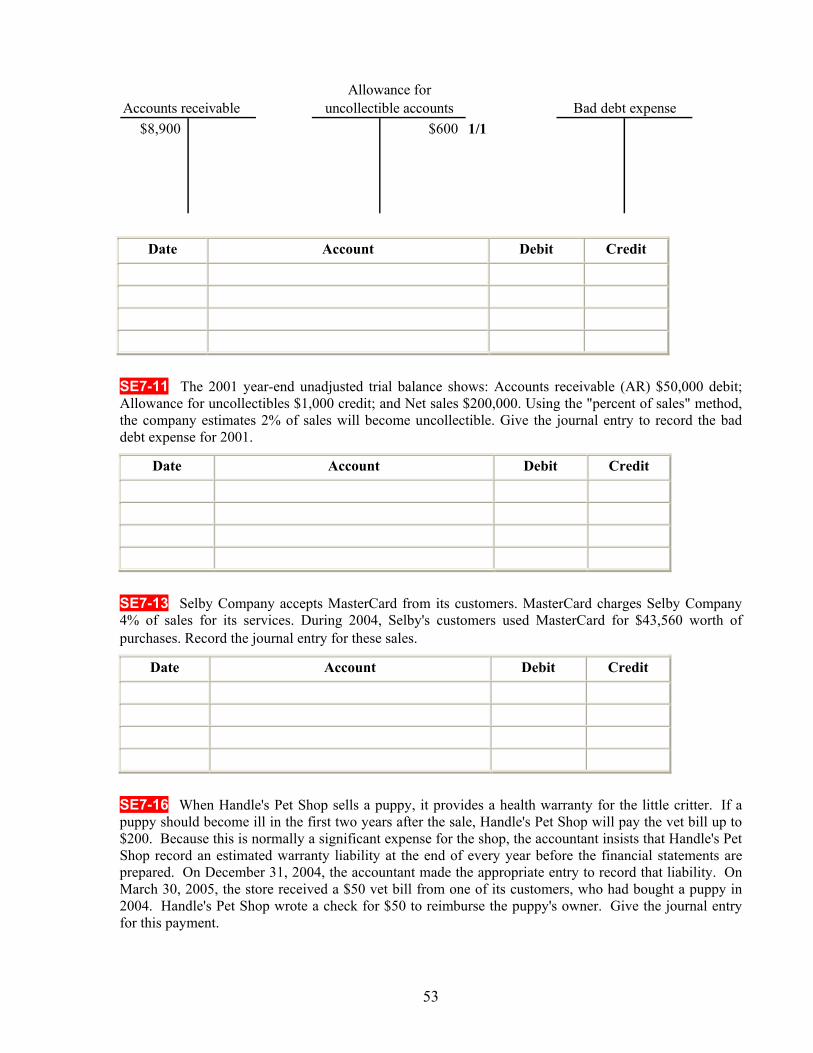

SE7-8 On January 1, 2002, a company's accounts receivable balance was $8,900 and the allowance for doubtful accounts balance was $600. This information came from the December 31, 2001 balance sheet. During 2002, the company reported $77,000 of credit sales; $400 of specific receivables were written off as uncollectible during 2002. Cash collections of receivables were $69,000 for the year. The company estimates that 3% of the year-end accounts receivable will be uncollectible. Use T-accounts to analyze the problem, and then make the journal entry to record the bad debt expense for the year ended December 31, 2002.

52

Accounts receivable$8,900 $600 1/1

Allowance for uncollectible accounts Bad debt expense

Date Account Debit Credit

SE7-11 The 2001 year-end unadjusted trial balance shows: Accounts receivable (AR) $50,000 debit; Allowance for uncollectibles $1,000 credit; and Net sales $200,000. Using the "percent of sales" method, the company estimates 2% of sales will become uncollectible. Give the journal entry to record the bad debt expense for 2001.

Date Account Debit Credit

SE7-13 Selby Company accepts MasterCard from its customers. MasterCard charges Selby Company 4% of sales for its services. During 2004, Selby's customers used MasterCard for $43,560 worth of purchases. Record the journal entry for these sales.

Date Account Debit Credit

SE7-16 When Handle's Pet Shop sells a puppy, it provides a health warranty for the little critter. If a puppy should become ill in the first two years after the sale, Handle's Pet Shop will pay the vet bill up to $200. Because this is normally a significant expense for the shop, the accountant insists that Handle's Pet Shop record an estimated warranty liability at the end of every year before the financial statements are prepared. On December 31, 2004, the accountant made the appropriate entry to record that liability. On March 30, 2005, the store received a $50 vet bill from one of its customers, who had bought a puppy in 2004. Handle's Pet Shop wrote a check for $50 to reimburse the puppy's owner. Give the journal entry for this payment.

53

54

Date Account Debit Credit

Exercises

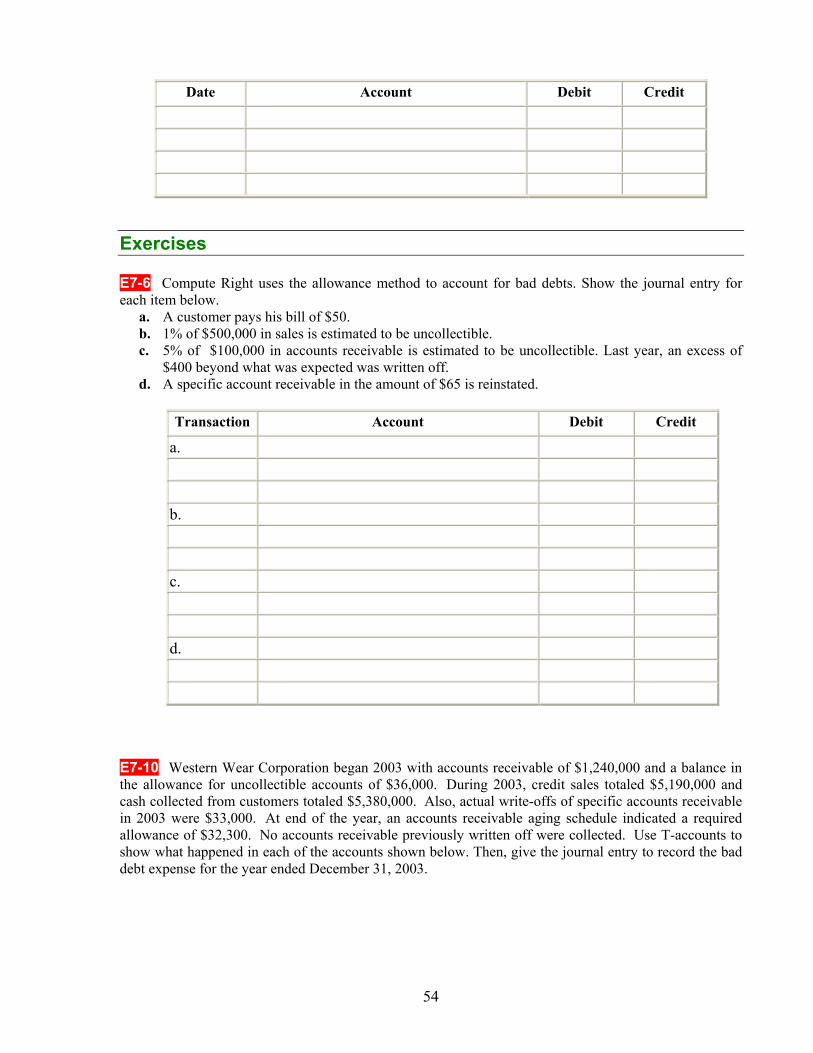

E7-6 Compute Right uses the allowance method to account for bad debts. Show the journal entry for each item below.

a. A customer pays his bill of $50. b. 1% of $500,000 in sales is estimated to be uncollectible. c. 5% of $100,000 in accounts receivable is estimated to be uncollectible. Last year, an excess of

$400 beyond what was expected was written off. d. A specific account receivable in the amount of $65 is reinstated.

Transaction Account Debit Credit

a. b. c. d.

E7-10 Western Wear Corporation began 2003 with accounts receivable of $1,240,000 and a balance in the allowance for uncollectible accounts of $36,000. During 2003, credit sales totaled $5,190,000 and cash collected from customers totaled $5,380,000. Also, actual write-offs of specific accounts receivable in 2003 were $33,000. At end of the year, an accounts receivable aging schedule indicated a required allowance of $32,300. No accounts receivable previously written off were collected. Use T-accounts to show what happened in each of the accounts shown below. Then, give the journal entry to record the bad debt expense for the year ended December 31, 2003.

Accounts receivable1/1 $1,240,000 1/1 $36,000

uncollectible accounts Bad debt expenseAllowance for

Date Account Debit Credit

E7-13 Trane Air Company accepts cash or credit card payment from customers. During July, Trane sold $100,000 worth of merchandise to customers who used VISA to pay for their purchases. VISA charges Trane 4% of sales for their services. Give the journal entry to record this transaction in Trane's financial records.

Date Account Debit Credit

Problems – Set A

P7-3A Given the following errors:

a. The bank recorded a deposit of $200 as $2,000. b. The company's bookkeeper mistakenly recorded a deposit of $530 as $350. c. The company's bookkeeper mistakenly recorded a payment of $250 received from a customer

as $25 on the bank deposit slip. The bank caught the error and made the deposit for the correct amount.

d. The bank statement shows that check that was written by the company for $255 was erroneously paid (cleared the account) as $225. This was the bank's error.

e. The bookkeeper wrote a check for $369 but erroneously wrote down $396 as the cash disbursement in the company's records.

Required:

Determine which of the errors would require the company to record a journal entry. Then, record the journal entry.

55

Transaction Account Debit Credit

P7-4A Consider the following:

a. At year-end, Vio Company has accounts receivable of $14,000. The allowance for uncollectible accounts has a credit balance prior to adjustment of $300. (Last year, uncollectible accounts were overestimated by $300.) An aging schedule prepared on December 31 indicates that $1,100 of Vio's accounts receivable are uncollectible accounts.

b. At year-end, Demato Company has accounts receivable of $25,700. The allowance for uncollectible accounts has a debit balance prior to adjustment of $400. (Last year, uncollectible accounts were underestimated by $400.) An aging schedule prepared on December 31 indicates that $2,300 of Demato's accounts receivable are uncollectible accounts.

Required: For each situation described above, give the journal entry to record bad debt expense. In both cases, the company uses the accounts receivable balance as the basis for estimating bad debts.

Transaction Account Debit Credit

a.

b.

56

57

P7-5A Consider the following situations: a. At year-end, Nash Company has accounts receivable of $84,000. The allowance for uncollectible

accounts has a credit balance prior to adjustment of $300. (Last year, uncollectible accounts were overestimated by $300.) Net credit sales for the year were $250,000 and 3% is estimated to be uncollectible.

b. At year-end, Bridges Company has accounts receivable of $83,000. The allowance for uncollectible accounts has a debit balance prior to adjustment of $400. (Last year, uncollectible accounts were underestimated by $400.) Net credit sales for the year were $250,000 and 3% is estimated to be uncollectible.

Required: For each situation described above, give the journal entry to record bad debt expense. In both cases, the company uses net credit sales as the basis for estimating bad debts.

Transaction Account Debit Credit

a.

b.

Recommended