Ali MADANIPhone: + 33 1 47 78 46 [email protected]

2

TUTORIAL Orthopaedics Market

June 2016

Table of contents

Worldwide orthopaedic market: dynamics, competition, drivers, limiters, … Worldwide orthopaedic markets in 2015: hip, knee, trauma, spine, others…Worldwide orthopaedic Market: products, innovations, growth, competition & trendsMarket drivers, market limitersForecasts by 2020

European orthopaedic market: market share, new products in details, heavy trends, …

European orthopaedic markets in 2015: market share for hip, knee & shoulderEuropean orthopaedic Market: new products, trends…Forecasts by 2020

Summaries

I

II

III

http://www.implants-event.com/program/presentations-2016/

Password: biarritz_2016

To download the presentations:

Ali MADANIPhone: + 33 1 47 78 46 [email protected]

3

TUTORIAL Orthopaedics Market

June 2016

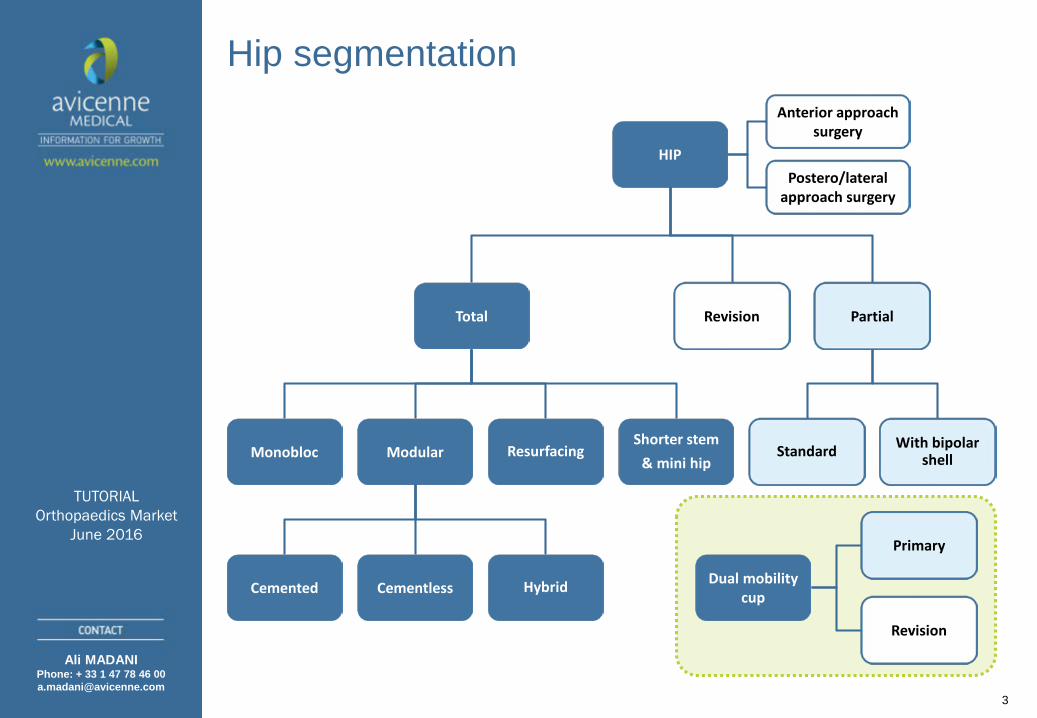

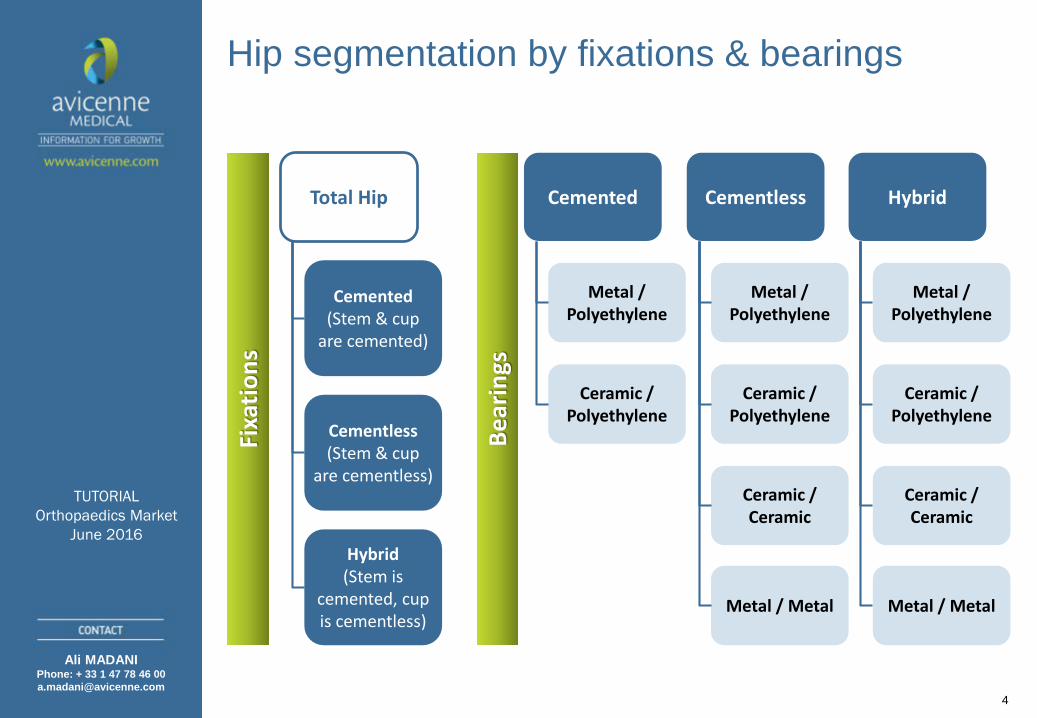

Hip segmentation

Cemented Cementless Hybrid

Monobloc Modular ResurfacingShorter stem

& mini hipStandard With bipolar

shell

Total PartialRevision

Dual mobilitycup

Primary

Revision

HIP

Anterior approachsurgery

Postero/lateralapproach surgery

Ali MADANIPhone: + 33 1 47 78 46 [email protected]

4

TUTORIAL Orthopaedics Market

June 2016

Bear

ings

Fixa

tions

Total Hip

Cemented(Stem & cup

are cemented)

Cementless(Stem & cup

are cementless)

Hybrid(Stem is

cemented, cup is cementless)

Cemented

Metal / Polyethylene

Ceramic / Polyethylene

Cementless

Metal / Polyethylene

Ceramic / Polyethylene

Ceramic / Ceramic

Hybrid

Metal / Polyethylene

Ceramic / Polyethylene

Metal / Metal

Hip segmentation by fixations & bearings

Ceramic / Ceramic

Metal / Metal

Ali MADANIPhone: + 33 1 47 78 46 [email protected]

5

TUTORIAL Orthopaedics Market

June 2016

Knee segmentation

KNEE

FIXED MOBILE UNICONDYLAR FEMORO PATELAR

TOTAL Partial Revision

Ali MADANIPhone: + 33 1 47 78 46 [email protected]

6

TUTORIAL Orthopaedics Market

June 2016

Fixe

d Vs

. Mob

ile k

nee

bear

ings

& F

ixat

ions

Post

erio

r sta

biliz

ed V

s. C

ruci

ate

Reta

inin

g To

tal k

nee

TOTAL

Posterior stabilized

Cruciateretaining

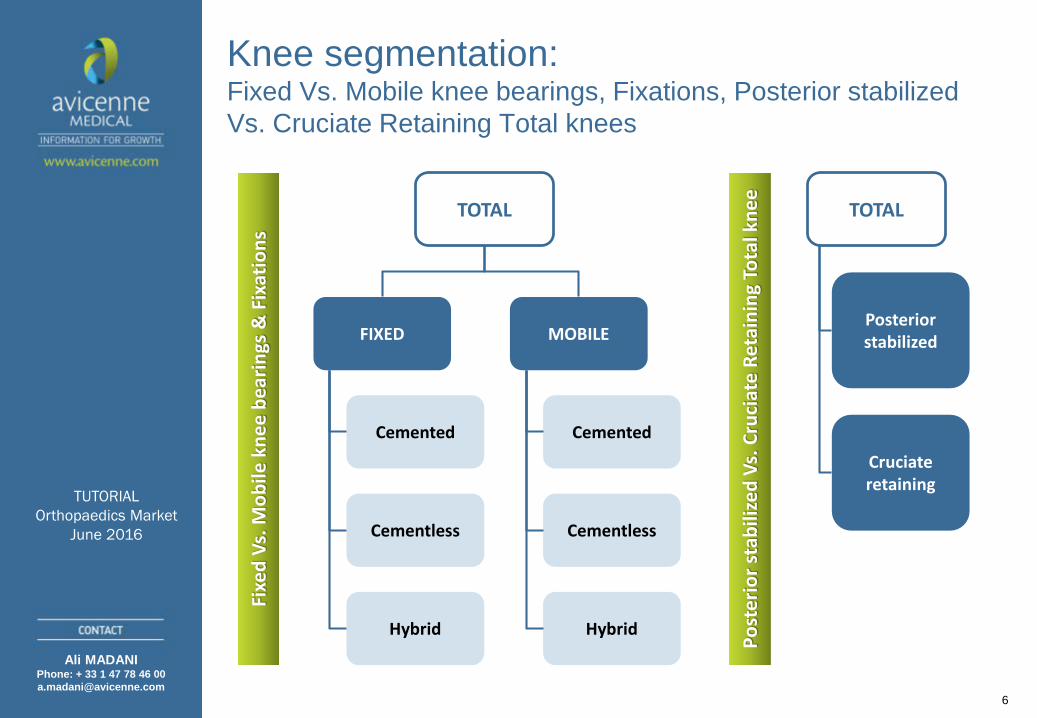

Knee segmentation: Fixed Vs. Mobile knee bearings, Fixations, Posterior stabilized Vs. Cruciate Retaining Total knees

FIXED MOBILE

Cemented

Cementless

Hybrid

Cemented

Cementless

Hybrid

TOTAL

Ali MADANIPhone: + 33 1 47 78 46 [email protected]

7

TUTORIAL Orthopaedics Market

June 2016

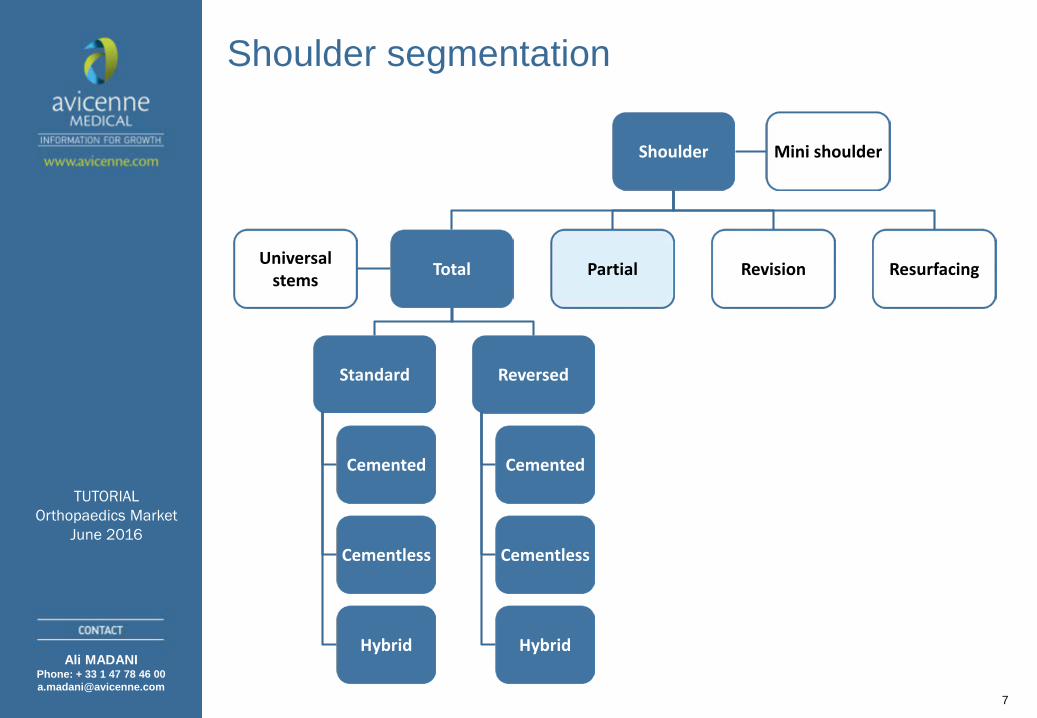

Shoulder segmentation

Shoulder

Total Partial Revision Resurfacing

Standard Reversed

Cemented Cemented

Cementless Cementless

Hybrid Hybrid

Mini shoulder

Universal stems

Ali MADANIPhone: + 33 1 47 78 46 [email protected]

8

TUTORIAL Orthopaedics Market

June 2016

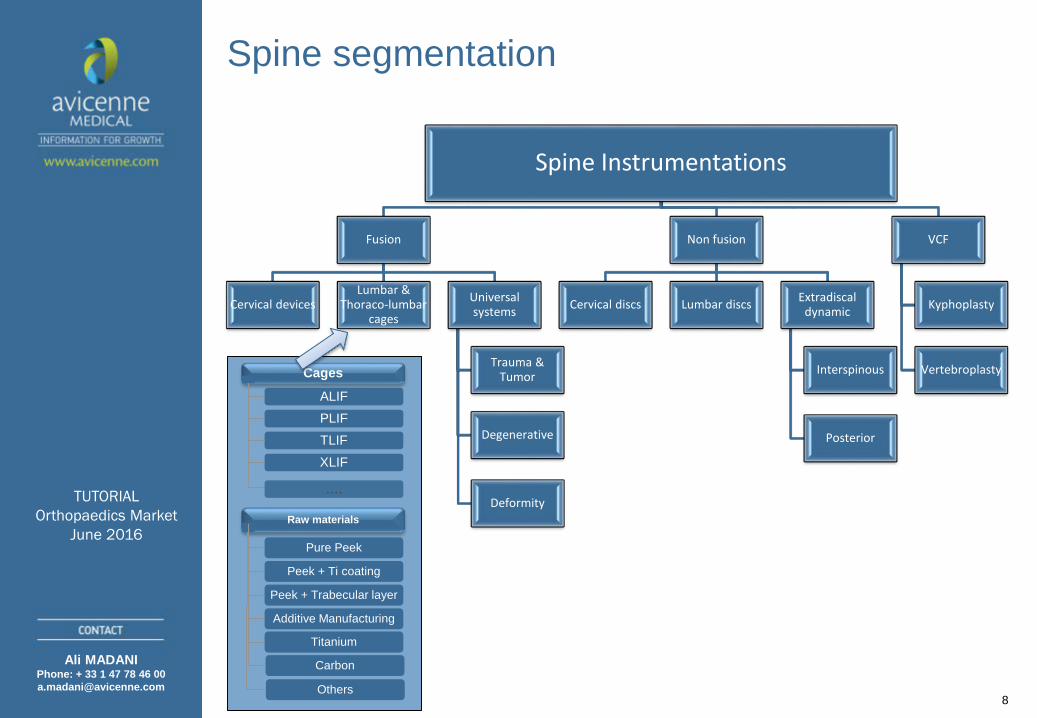

Spine segmentation

Spine Instrumentations

Fusion

Cervical devicesLumbar &

Thoraco-lumbarcages

Universalsystems

Trauma & Tumor

Degenerative

Deformity

Non fusion

Cervical discs Lumbar discs Extradiscaldynamic

Interspinous

Posterior

VCF

Kyphoplasty

VertebroplastyCages

ALIFPLIF TLIFXLIF

Raw materials

Pure Peek

Peek + Ti coating

Peek + Trabecular layer

Additive Manufacturing

Titanium

Carbon

Others

….

Ali MADANIPhone: + 33 1 47 78 46 [email protected]

9

TUTORIAL Orthopaedics Market

June 2016

19%

5%2%

17%23%

13%

21%

Worldwide orthopaedic* markets in 2015:~39 BUS$ (+4.3%)

Source: Avicenne research & analysis 2016

HIPKNEE

EXTREMITIES

SPINE

TRAUMA

ORTHO-BIOLOGICS

OTHERS

KNEE8.9 B$

+4.5%

Hip6.5 B$

+2.1%

SPINE8.3 B$

+2.9%

• Extremities: Shoulder, Elbow, Ankle, Foot, hand,… (excluding trauma)• Orthobiologics: Allograft, Xenograft, Synthetic Bone, Cement, BMP, others, Cell based Product, Auto repair product, Anti Adhesion product, Hyaluronic Acid,…• Other: Navigation, ortho. Equipment, etc..

• * Not included : Power tools, Arthroscopy & soft tissue repair, sport Medicine, Neuro-stimulation

Ali MADANIPhone: + 33 1 47 78 46 [email protected]

10

TUTORIAL Orthopaedics Market

June 2016

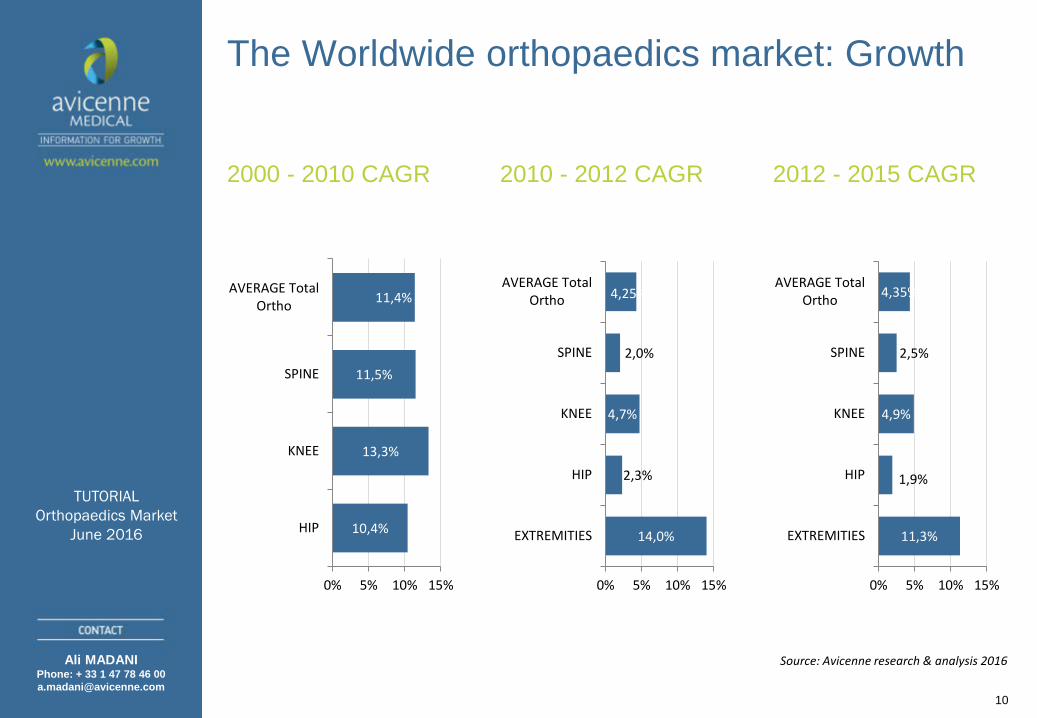

The Worldwide orthopaedics market: Growth

2000 - 2010 CAGR

Source: Avicenne research & analysis 2016

2010 - 2012 CAGR 2012 - 2015 CAGR

11,3%

1,9%

4,9%

2,5%

4,35%

0% 5% 10% 15%

EXTREMITIES

HIP

KNEE

SPINE

AVERAGE TotalOrtho

14,0%

2,3%

4,7%

2,0%

4,25%

0% 5% 10% 15%

EXTREMITIES

HIP

KNEE

SPINE

AVERAGE TotalOrtho

10,4%

13,3%

11,5%

11,4%

0% 5% 10% 15%

HIP

KNEE

SPINE

AVERAGE TotalOrtho

Ali MADANIPhone: + 33 1 47 78 46 [email protected]

11

TUTORIAL Orthopaedics Market

June 2016

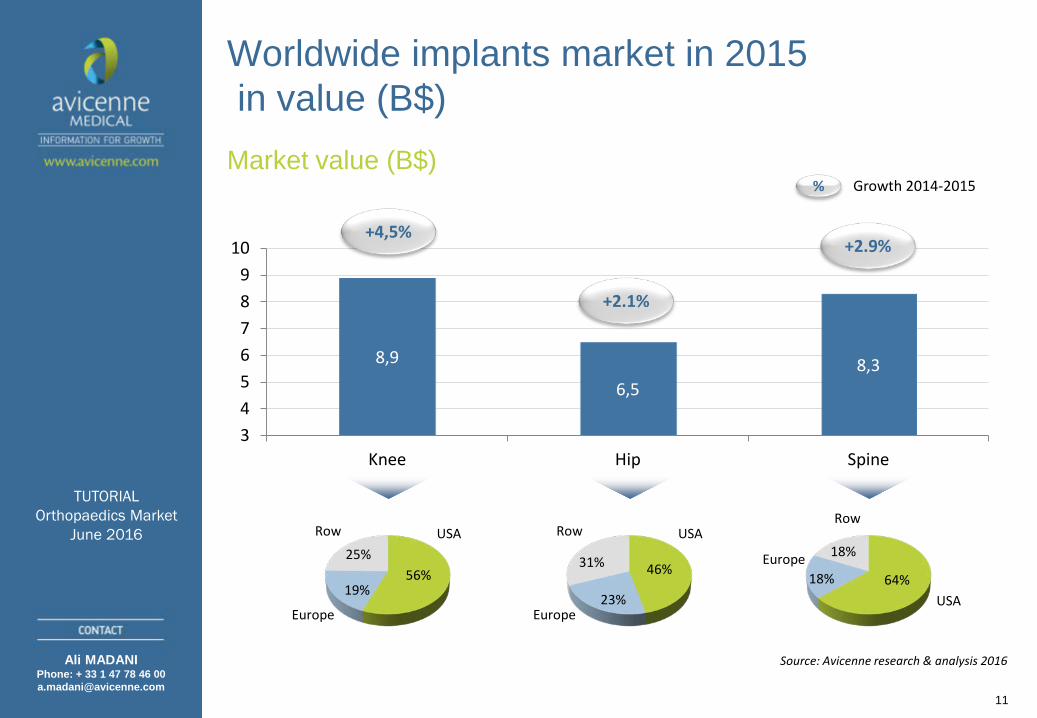

Worldwide implants market in 2015 in value (B$)

Market value (B$)

Source: Avicenne research & analysis 2016

8,9

6,58,3

3456789

10

Knee Hip Spine

56%19%

25%

Row USA

Europe

46%

23%

31%

Row USA

Europe

64%18%

18%

Row

USA

Europe

+4,5%

+2.1%

+2.9%

% Growth 2014-2015

Ali MADANIPhone: + 33 1 47 78 46 [email protected]

12

TUTORIAL Orthopaedics Market

June 2016

Worldwide implants & Orthobiologics marketin 2015 in value (B$)Market value (B$)

Source: Avicenne research & analysis 2016

7,35,3

2,00

2

4

6

8

Trauma & CMF Orthobiologics Extremities

45%

25%

30%

Row USA

Europe

70%21%

9%Row

USA

Europe 60%24%

16%

RowUSA

Europe

+5.2%

+5.4%

+10.5%

% Growth 2014-2015

Ali MADANIPhone: + 33 1 47 78 46 [email protected]

13

TUTORIAL Orthopaedics Market

June 2016

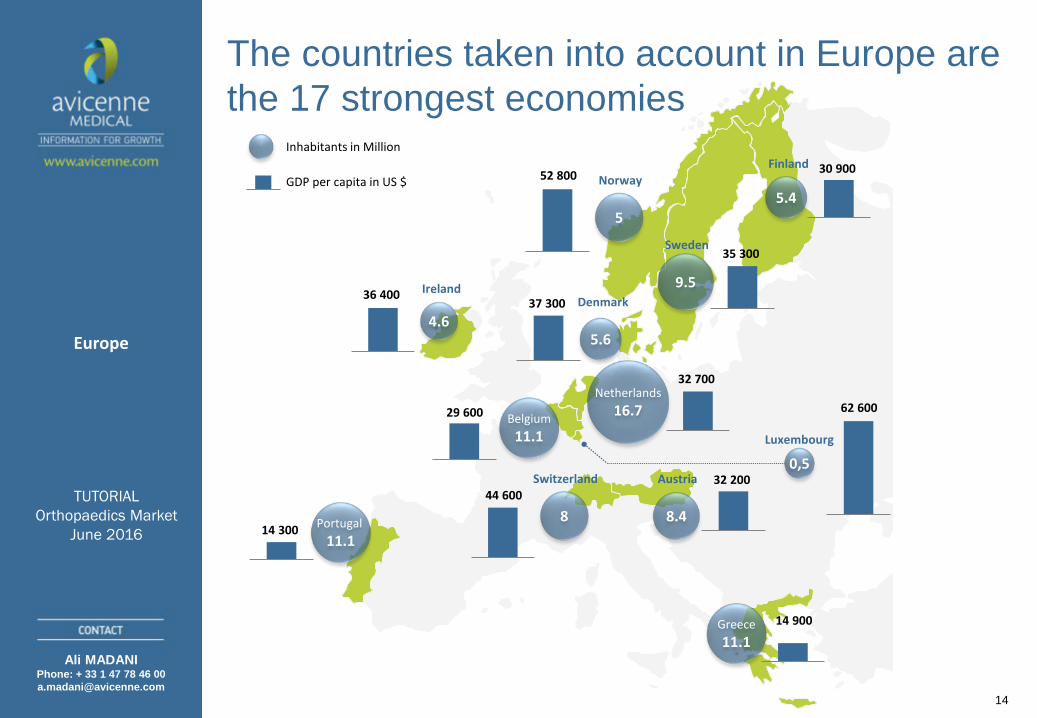

The countries taken into account in Europe are the 17 strongest economies

France65

Germany82

Italy61

UK64

Spain47

27 600

30 400

30 200

22 80020 200

Inhabitants in Million

GDP per capita in US $

Europe

Ali MADANIPhone: + 33 1 47 78 46 [email protected]

14

TUTORIAL Orthopaedics Market

June 2016

The countries taken into account in Europe are the 17 strongest economies

Belgium11.1

29 600

5.6

37 300 Denmark

5.4

30 900Finland

9.5

Sweden35 300

4.6

Ireland36 400

Netherlands16.7

32 700

8.4

Austria 32 2000,5

Luxembourg

Greece11.1

62 600

14 900

Portugal 11.1

14 3008

Switzerland44 600

5

Norway52 800

Inhabitants in Million

GDP per capita in US $

Europe

Ali MADANIPhone: + 33 1 47 78 46 [email protected]

15

TUTORIAL Orthopaedics Market

June 2016

Worldwide orthopaedic market in 2015: competition2015 Worldwide Orthopaedic Market

Source: Avicenne research & analysis 2016

2015 revenues of the Major Orthopaedic Companies (B$)

Depuy-Synthes

20%

Zimmer Biomet

16%Stryker

13%Medtronic

8%

Smith & Nephew

5%

Other38%

2,0

3

5

6,3

8

0 10 20 30

Smith & Nephew

Medtronic

Stryker

Zimmer Biomet

Depuy-Synthes

Ortho products

Other Medical devices

2015: Zimmer acquired Biomet for 13.4 B USD

2012: Depuyacquired Synthes

for 21.3 B USD

33,3%

34,8%

37,9%

30% 35% 40%

2013

2014

2015

OtherMarket share

2015: Medtronic acquired Covidien for

50 B USD

Ali MADANIPhone: + 33 1 47 78 46 [email protected]

16

TUTORIAL Orthopaedics Market

June 2016

Worldwide competition by product in 2015: Market share

Source: Avicenne research & analysis 2016

Others

HipTop 5: 75%

KneeTop 5: 84%

SpineTop 5: 71%

Trauma & CMF

Top 5: 67%

Total Ortho

Top 6: 65%

20%

17%

22%

35%

21%

19%

16%

9%

13%

13%

30%

32%

5%

8%

16%

0%

0%

30%

0%

8%

9%

10%

0%

7%

5%

21%

25%

35%

38%

35%

Worldwide

=100%

=100%

=100%

=100%

=100%

Ali MADANIPhone: + 33 1 47 78 46 [email protected]

17

TUTORIAL Orthopaedics Market

June 2016

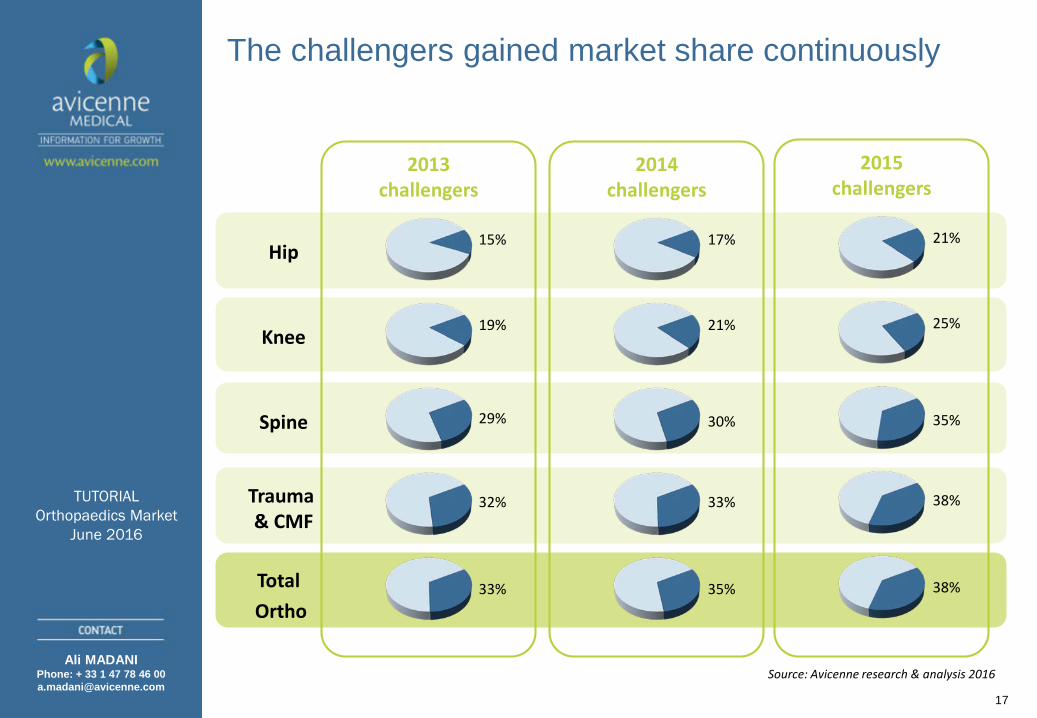

The challengers gained market share continuously

Source: Avicenne research & analysis 2016

2013challengers

2014challengers

Hip

Knee

Spine

Trauma & CMF

Total Ortho

15%

19%

29%

32%

33% 35%

17%

21%

30%

33%

2015challengers

38%

21%

25%

35%

38%

Ali MADANIPhone: + 33 1 47 78 46 [email protected]

18

TUTORIAL Orthopaedics Market

June 2016

26% 21%

19%

26%

15% 13%

12%12%13%

10%

8% 8%9%

9% 8% 8%

5,6% 7,7%

32%

39%

46% 47%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

2008 2012 2014 2015

Zimmer Depuy Stryker Smith & Nephew Biomet Challengers

Challengers

Hip Europe market share 2008-2015

Hip Europe market share

Source: Avicenne analysis 2016

Ali MADANIPhone: + 33 1 47 78 46 [email protected]

19

TUTORIAL Orthopaedics Market

June 2016

Knee Europe market share 2008-2015

Knee Europe market share

24%20%

19%

28%

20% 17%

19%18%

12%

11% 10% 10%11%

14%

12%12%

8%

12%

11%

25%

27% 30%32%

0%

5%

10%

15%

20%

25%

30%

35%

2008 2012 2014 2015

Zimmer Depuy Stryker Smith & Nephew Biomet Challengers

Challengers

Source: Avicenne analysis 2016

Ali MADANIPhone: + 33 1 47 78 46 [email protected]

Worldwide orthopaedic Contract Manufacturing

market report 2015-2020

&Top 100 player profiles

Majors Vs Challengers: Majors saved their margins & Challengers got the growth!

0%

5%

10%

15%

20%

25%

30%

35%

-10% -5% 0% 5% 10% 15% 20% 25%

WW

Ort

ho 2

014

mar

kets

hare

(%)

Revenues CAGR 2011-2014 (%)

20

Source: Avicenne , annual reports and companies June 2015

ChallengersLegende

Market share

Revenues growth

1 BUS$

Challengers

CAGR 2011-2014 Ortho revenues

Company CAGR Main drivers

LDR 24,5% Spine/USA

Wright 18% Extremities

LIMA 11,8% Hip/ export*Shoulder/USA

Amplitude 11% Knee, hip/export

Mathys 8,6% Hip, knee/export

* export: apart from their home country

Challengers CAGR average 16,2%

Ali MADANIPhone: + 33 1 47 78 46 [email protected]

21

TUTORIAL Orthopaedics Market

June 2016

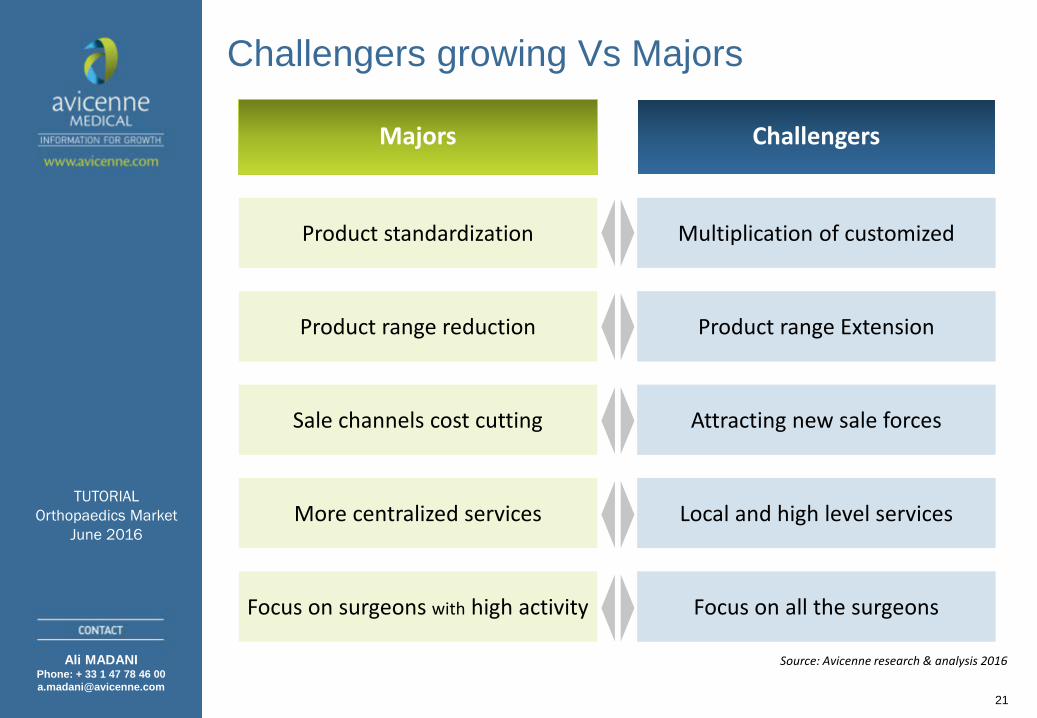

Challengers growing Vs Majors

Source: Avicenne research & analysis 2016

Majors Challengers

Product standardization Multiplication of customized

Product range reduction Product range Extension

Sale channels cost cutting Attracting new sale forces

More centralized services Local and high level services

Focus on surgeons with high activity Focus on all the surgeons

Ali MADANIPhone: + 33 1 47 78 46 [email protected]

22

TUTORIAL Orthopaedics Market

June 2016

Market Drivers

Source: Avicenne research & analysis 2016

Demographic& Economic

Impact 1: Population

Impact 2: Inhabitants 65+ years

Impact 3: Health expenses

Impact 4: Obesity

New products& innovationand revision

Impact 1: Product mix impact

Ali MADANIPhone: + 33 1 47 78 46 [email protected]

23

TUTORIAL Orthopaedics Market

June 2016

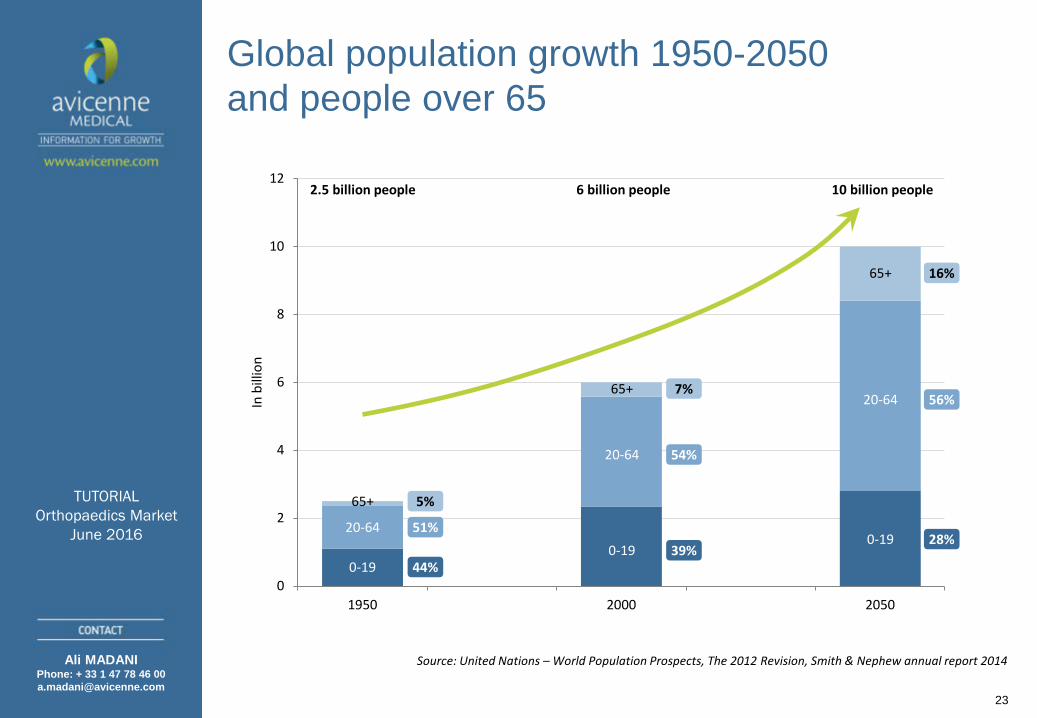

Global population growth 1950-2050and people over 65

Source: United Nations – World Population Prospects, The 2012 Revision, Smith & Nephew annual report 2014

0

2

4

6

8

10

12

1950 2000 2050

In b

illio

n

5%

51%

44%

2.5 billion people 6 billion people 10 billion people

0-19

20-64

65+

0-19

20-64

65+ 7%

54%

39%0-19

20-64

65+ 16%

56%

28%

Ali MADANIPhone: + 33 1 47 78 46 [email protected]

24

TUTORIAL Orthopaedics Market

June 2016

The market drivers: Demographic & Economic

Obesity in developed countries % of inhabitants

Health expenses % of GDP

15%

23%

31%34% 37%

4% 6%9%

13%17%

7%

14%

23%26% 28%

0%

10%

20%

30%

40%

1980 1990 2000 2010 2020

USA France UK

Source : OCDE

6%8%

10%

13%

15%

5%6%

8%10%

11%

4%

6%

6%7%

8%

0%

10%

20%

1980 1990 2000 2010 2020

USA France UK

Source : OCDE

Ali MADANIPhone: + 33 1 47 78 46 [email protected]

Worldwide orthopaedic Contract Manufacturing

market report 2015-2020

&Top 100 player profiles

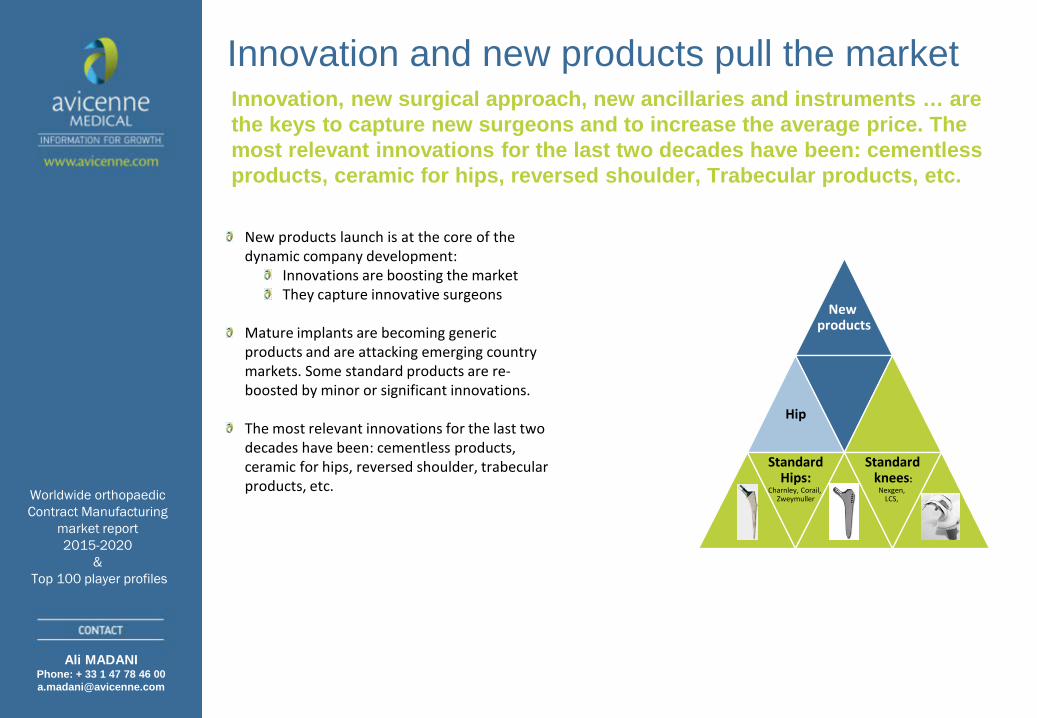

Innovation and new products pull the market

New products launch is at the core of the dynamic company development:

Innovations are boosting the marketThey capture innovative surgeons

Mature implants are becoming generic products and are attacking emerging country markets. Some standard products are re-boosted by minor or significant innovations.

The most relevant innovations for the last two decades have been: cementless products, ceramic for hips, reversed shoulder, trabecular products, etc.

Innovation, new surgical approach, new ancillaries and instruments … are the keys to capture new surgeons and to increase the average price. The most relevant innovations for the last two decades have been: cementlessproducts, ceramic for hips, reversed shoulder, Trabecular products, etc.

New products

Hip

StandardHips:

Charnley, Corail, Zweymuller

Standardknees:

Nexgen, LCS,

Ali MADANIPhone: + 33 1 47 78 46 [email protected]

Innovative surgeons are looking for new products. They are lured by new orthopaedic projects. Conservative surgeons mainly use standard products with decades of clinical evidences

25%40%

40%

40%

35%20%

Latin countries Evidence basedcountries

Conservatives Followers Innovatives

% of the surgeons by category in each type of country

26

Sources: AVICENNE analysis

Conservativesurgeons

Innovativesurgeons

Followersurgeons

New products

Hip

StandardHips:

Charnley, Corail, Zweymuller

Standardknees:

Nexgen, LCS, TUTORIAL

Orthopaedics MarketJune 2015

Ali MADANIPhone: + 33 1 47 78 46 [email protected]

27

TUTORIAL Orthopaedics Market

June 2016

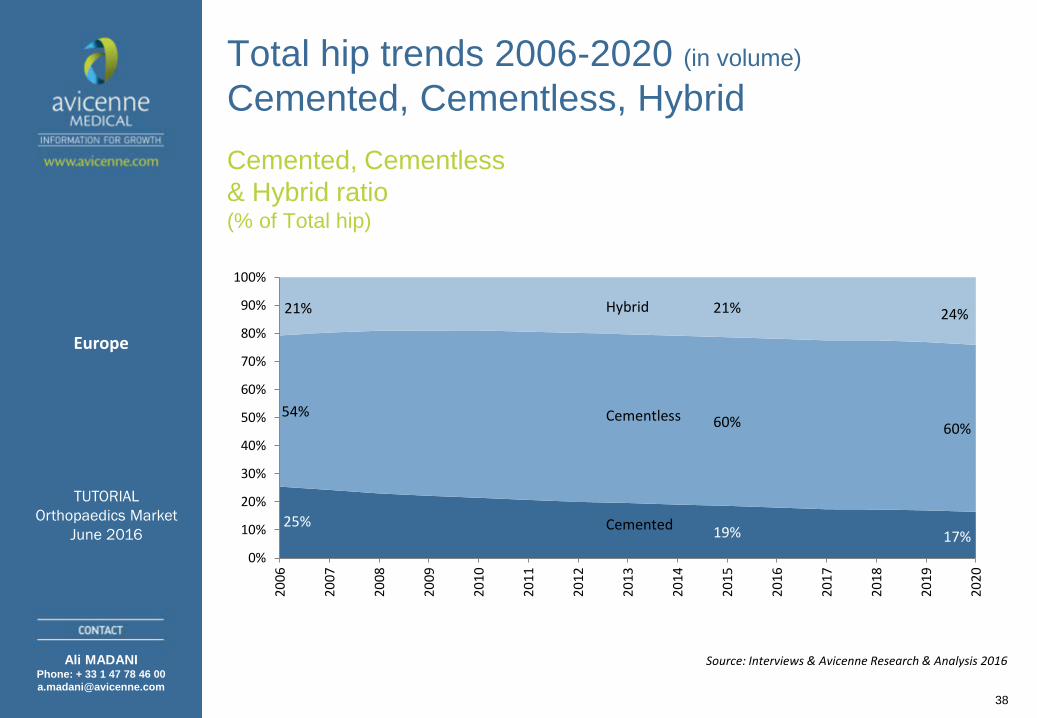

Product Mix pulls the marketTotal hip trends 2006-2020 (in volume)

Cemented, Cementless, Hybrid

Cemented, Cementless & Hybrid ratio(% of Total hip)

Source: Interviews & Avicenne Research & Analysis 2016

25%19% 17%

54%60% 60%

21% 21% 24%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%20

06

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

Hybrid

Cementless

Cemented

Europe

Ali MADANIPhone: + 33 1 47 78 46 [email protected]

28

TUTORIAL Orthopaedics Market

June 2016

The revision driver: more and more people have more than one implant in their lifeHip implant trends 2006-2020 (in volume)

Total, Partial & Revision hip, mini hip Ratio (% of the global market)

Source: Interviews & Avicenne Research & Analysis 2016

66%60% 56%

18%15%

14%

12%16%

18%

4%1%

1%

8% 12%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

Mini hip

Resurfacing

Revision

Partial

Total

Europe

Ali MADANIPhone: + 33 1 47 78 46 [email protected]

29

TUTORIAL Orthopaedics Market

June 2016

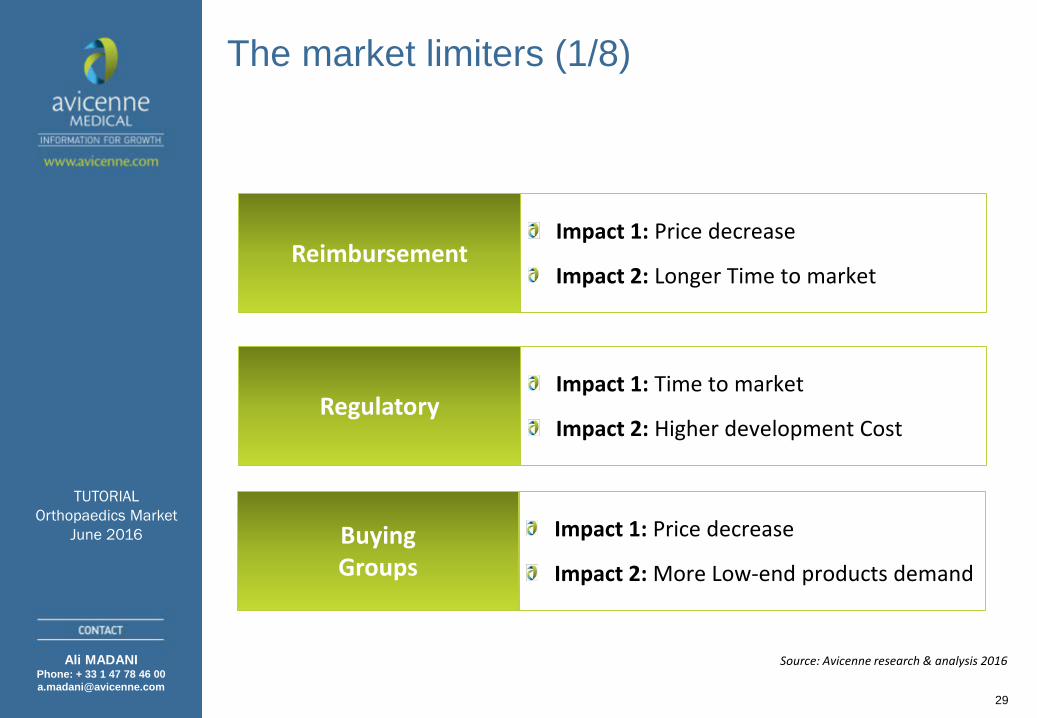

The market limiters (1/8)

Source: Avicenne research & analysis 2016

ReimbursementImpact 1: Price decrease

Impact 2: Longer Time to market

Buying Groups

Impact 1: Price decrease

Impact 2: More Low-end products demand

RegulatoryImpact 1: Time to market

Impact 2: Higher development Cost

Ali MADANIPhone: + 33 1 47 78 46 [email protected]

30

TUTORIAL Orthopaedics Market

June 2016

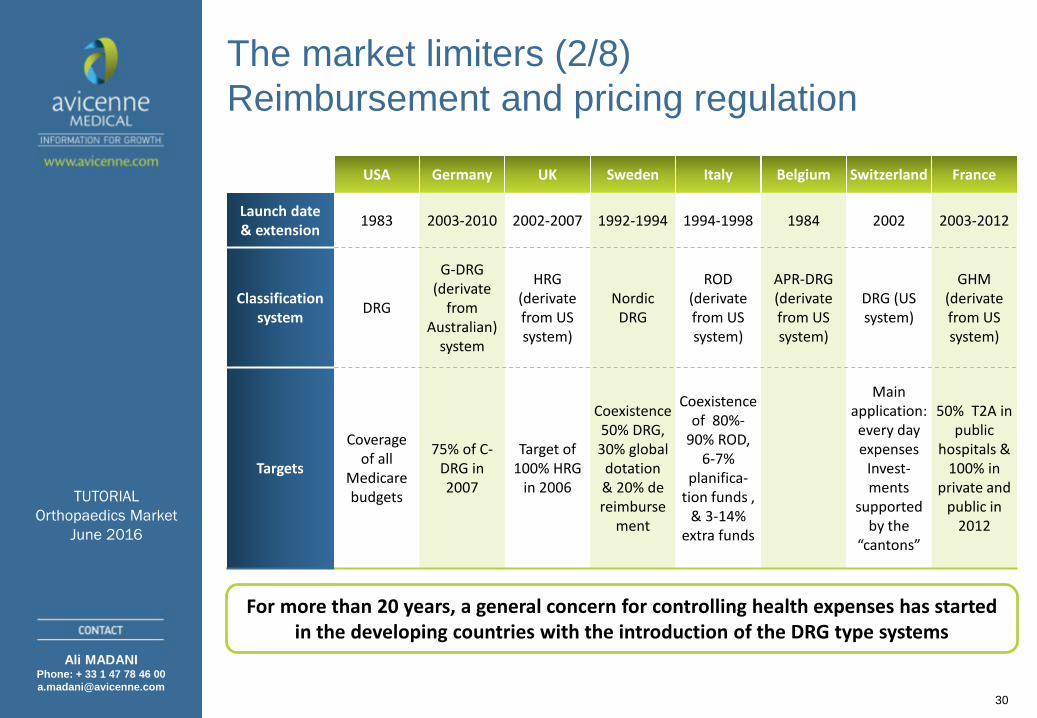

The market limiters (2/8)Reimbursement and pricing regulation

USA Germany UK Sweden Italy Belgium Switzerland France

Launch date & extension 1983 2003-2010 2002-2007 1992-1994 1994-1998 1984 2002 2003-2012

Classification system DRG

G-DRG (derivate

from Australian)

system

HRG (derivate from US system)

NordicDRG

ROD (derivate from US system)

APR-DRG (derivate from US system)

DRG (US system)

GHM (derivate from US system)

Targets

Coverage of all

Medicare budgets

75% of C-DRG in 2007

Target of 100% HRG

in 2006

Coexistence 50% DRG, 30% global

dotation& 20% de reimburse

ment

Coexistenceof 80%-

90% ROD, 6-7%

planifica-tion funds ,

& 3-14% extra funds

Main application: every day expenses

Invest-ments

supported by the

“cantons”

50% T2A in public

hospitals & 100% in

private and public in

2012

For more than 20 years, a general concern for controlling health expenses has started in the developing countries with the introduction of the DRG type systems

Ali MADANIPhone: + 33 1 47 78 46 [email protected]

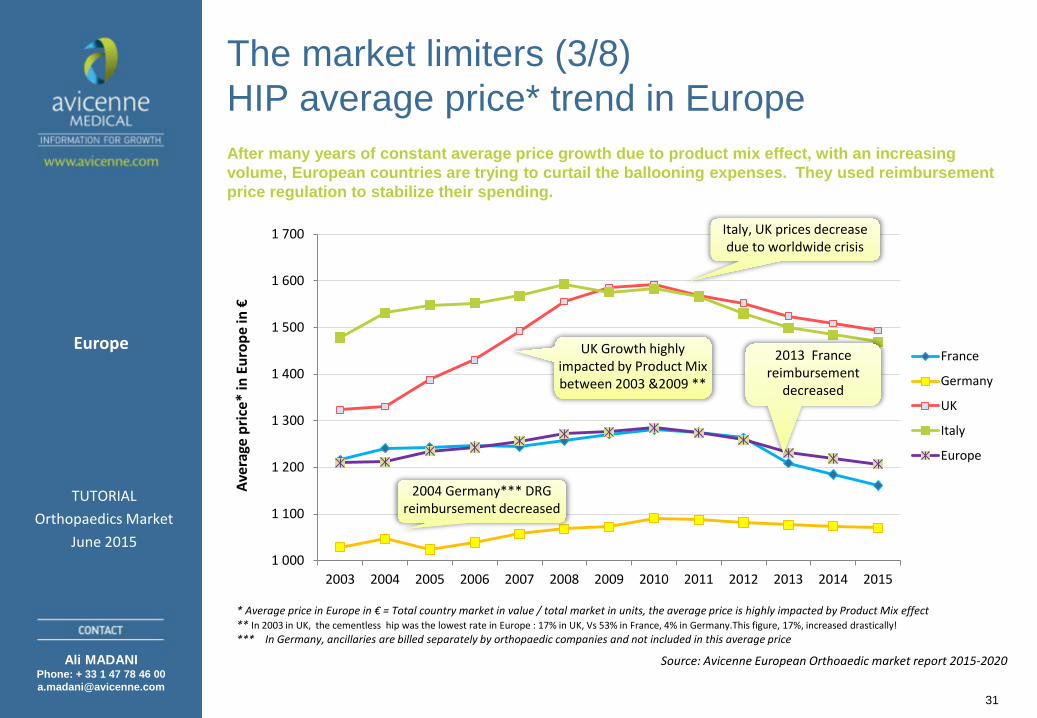

The market limiters (3/8)HIP average price* trend in Europe

1 000

1 100

1 200

1 300

1 400

1 500

1 600

1 700

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Aver

age

pric

e* in

Eur

ope

in €

France

Germany

UK

Italy

Europe

After many years of constant average price growth due to product mix effect, with an increasing volume, European countries are trying to curtail the ballooning expenses. They used reimbursement price regulation to stabilize their spending.

31

Source: Avicenne European Orthoaedic market report 2015-2020

2004 Germany*** DRG reimbursement decreased

Italy, UK prices decrease due to worldwide crisis

UK Growth highly impacted by Product Mix between 2003 &2009 **

2013 France reimbursement

decreased

* Average price in Europe in € = Total country market in value / total market in units, the average price is highly impacted by Product Mix effect** In 2003 in UK, the cementless hip was the lowest rate in Europe : 17% in UK, Vs 53% in France, 4% in Germany.This figure, 17%, increased drastically!*** In Germany, ancillaries are billed separately by orthopaedic companies and not included in this average price

TUTORIALOrthopaedics Market

June 2015

Europe

Ali MADANIPhone: + 33 1 47 78 46 [email protected]

32

TUTORIAL Orthopaedics Market

June 20160,2%

0,6%0,8%

-0,1%0,5%

-0,8%-1,1%-2,1%

-1,8%-1,1%-1,1%-1,1%

-1,5%-1,5%-1,5%

-3,0% -2,0% -1,0% 0,0% 1,0%

200620072008200920102011201220132014201520162017201820192020

Price trends (4/8)

Average sales price trendper year for hips

Source: Interviews & Avicenne Research & Analysis 2016

Example of price decrease for each product (Euros)Average forecasted price decrease/year from 2013 to 2020: -1.3 %

664 €

899 €

1 642 €

298 €

661 €

0

500

1 000

1 500

2 000

2 500

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

M/PE cemented

Ce/PE cemented

Ce/Ce cementless

Partial standard

Partial with Bipolar shell

Europe

Ali MADANIPhone: + 33 1 47 78 46 [email protected]

33

TUTORIAL Orthopaedics Market

June 2016

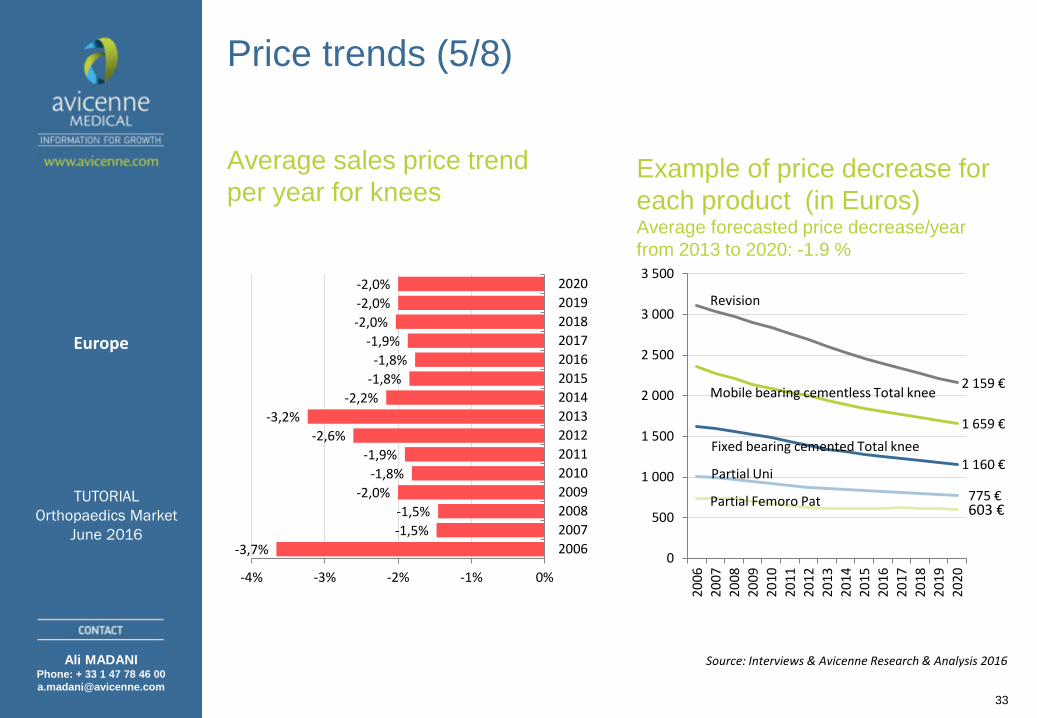

Price trends (5/8)

Average sales price trendper year for knees

Source: Interviews & Avicenne Research & Analysis 2016

Example of price decrease for each product (in Euros)Average forecasted price decrease/year from 2013 to 2020: -1.9 %

-3,7%-1,5%-1,5%

-2,0%-1,8%

-1,9%-2,6%

-3,2%-2,2%

-1,8%-1,8%

-1,9%-2,0%-2,0%-2,0%

-4% -3% -2% -1% 0%

200620072008200920102011201220132014201520162017201820192020

1 160 €

1 659 €

775 €603 €

2 159 €

0

500

1 000

1 500

2 000

2 500

3 000

3 500

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

Revision

Mobile bearing cementless Total knee

Partial Uni

Fixed bearing cemented Total knee

Partial Femoro Pat

Europe

Ali MADANIPhone: + 33 1 47 78 46 [email protected]

34

TUTORIAL Orthopaedics Market

June 2016

Price trends (6/8)

Average sales price trendper year for shoulders

Example of price decrease for each product Average forecasted price decrease/year from 2013 to 2020: -1.5 %

-0,6%-0,8%

-1,0%-1,1%

-1,8%-2,3%

-0,9%-2,1%

-2,4%-1,4%

-1,1%-1,0%

-1,5%-1,5%-1,5%

-3% -2% -1% 0%

200620072008200920102011201220132014201520162017201820192020

1 439 €

2 000 €1 781 €

1 294 €

623 €

2 178 €

0

500

1 000

1 500

2 000

2 500

3 000

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

Source: Interviews & Avicenne Research & Analysis 2016

Total standard cemented shoulder

Total reversed cementless shoulderTotal reversed hybrid shoulder

Partial

Resurfacing

RevisionEurope

Ali MADANIPhone: + 33 1 47 78 46 [email protected]

35

TUTORIAL Orthopaedics Market

June 2016

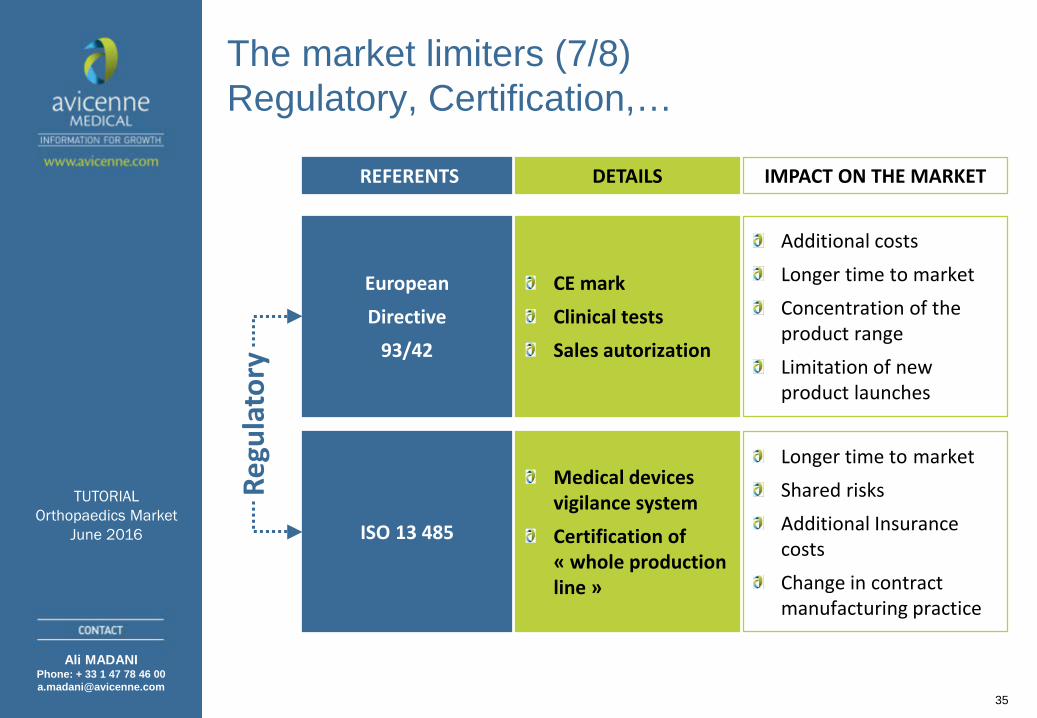

The market limiters (7/8)Regulatory, Certification,…

Regu

lato

ry

REFERENTS DETAILS IMPACT ON THE MARKET

EuropeanDirective

93/42

ISO 13 485

CE markClinical testsSales autorization

Medical devicesvigilance systemCertification of « whole production line »

Additional costsLonger time to marketConcentration of the product rangeLimitation of new product launches

Longer time to marketShared risksAdditional InsurancecostsChange in contractmanufacturing practice

Ali MADANIPhone: + 33 1 47 78 46 [email protected]

36

TUTORIAL Orthopaedics Market

June 2016

The market limiters (8/8)

Group purchasing developments in Germany drove the implant prices down… It now serves as a model in lot of other European countries

Source: Avicenne research & analysis 2016

Group purchasing was a success in

Germany…

For example the basic knee (fixed tibial plate - cemented) is priced at 1 350 €, for some tenders a Major proposed 900 € for this basic product.Another Major had in his customer portfolio the “Endoclinic and DAM Group” for 4 hospitals, with 10,000 knee and hip sales per year! Average price for the knee for this customer is much less than 1 000 €.

…it was much less successful in France and Italy

Some private hospital groups in France like “Vitalia or Générale de Santé” have tried to centralize their implant purchasing, but it is only the beginning. The discounted price was only a few % lower and those hospitals have to share these savings with the “French Caissed’Assurance Maladie”. The surgeon name reputation is considered as product marketing showcase of the private hospitals, which are making what is necessary to keep their surgeons. Hence they are not focusing on implants price reduction.In Italy, purchasing groups make less than 10% of the total orthopaedicmarket value per year and growing slowly.

Ali MADANIPhone: + 33 1 47 78 46 [email protected]

37

TUTORIAL Orthopaedics Market

June 2016

The revision driver: more and more people have more than one implant in their lifeHip implant trends 2006-2020 (in volume)

Total, Partial & Revision hip Ratio (% of the global market)

Source: Interviews & Avicenne Research & Analysis 2016

66%60% 56%

18%15%

14%

12%16%

18%

4%1%

1%

8% 12%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

Mini hip

Resurfacing

Revision

Partial

Total

Europe

Ali MADANIPhone: + 33 1 47 78 46 [email protected]

38

TUTORIAL Orthopaedics Market

June 2016

Total hip trends 2006-2020 (in volume)

Cemented, Cementless, HybridCemented, Cementless & Hybrid ratio(% of Total hip)

Source: Interviews & Avicenne Research & Analysis 2016

25%19% 17%

54%60% 60%

21% 21% 24%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%20

06

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

Hybrid

Cementless

Cemented

Europe

Ali MADANIPhone: + 33 1 47 78 46 [email protected]

39

TUTORIAL Orthopaedics Market

June 2016

Cementless trends 2006 – 2020M/Pe, Ce/Pe, Ce/Ce, M/M

Source: Interviews & Avicenne Research & Analysis 2016

M/Pe, Ce/Pe, Ce/Ce & M/M ratio(% of Cementless & Hybrid Total hip)

43% 39% 37%

29% 34% 36%

21% 27% 27%

7% 1% 1%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

M/M

Ce/Ce

Ce/Pe

M/Pe

Ce/Pe is continuing slightly to grow

Europe

Ali MADANIPhone: + 33 1 47 78 46 [email protected]

40

TUTORIAL Orthopaedics Market

June 2016

Ceramic, Metal & PE trends for Heads and Cups 2006-2020% of Metal & CeramicHEAD

Source: Interviews & Avicenne Research & Analysis 2016

% of Metal, Ceramic & PE CUP

80% 77% 77%

15% 21% 22%

5% 1% 1%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2006

2008

2010

2012

2014

2016

2018

2020

Metal

Ceramic

PE

45%55%

57%

55%45% 43%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%20

0620

0720

0820

0920

1020

1120

1220

1320

1420

1520

1620

1720

1820

1920

20

Ceramic for heads is still growing in Europe

Europe

Ali MADANIPhone: + 33 1 47 78 46 [email protected]

41

TUTORIAL Orthopaedics Market

June 2016

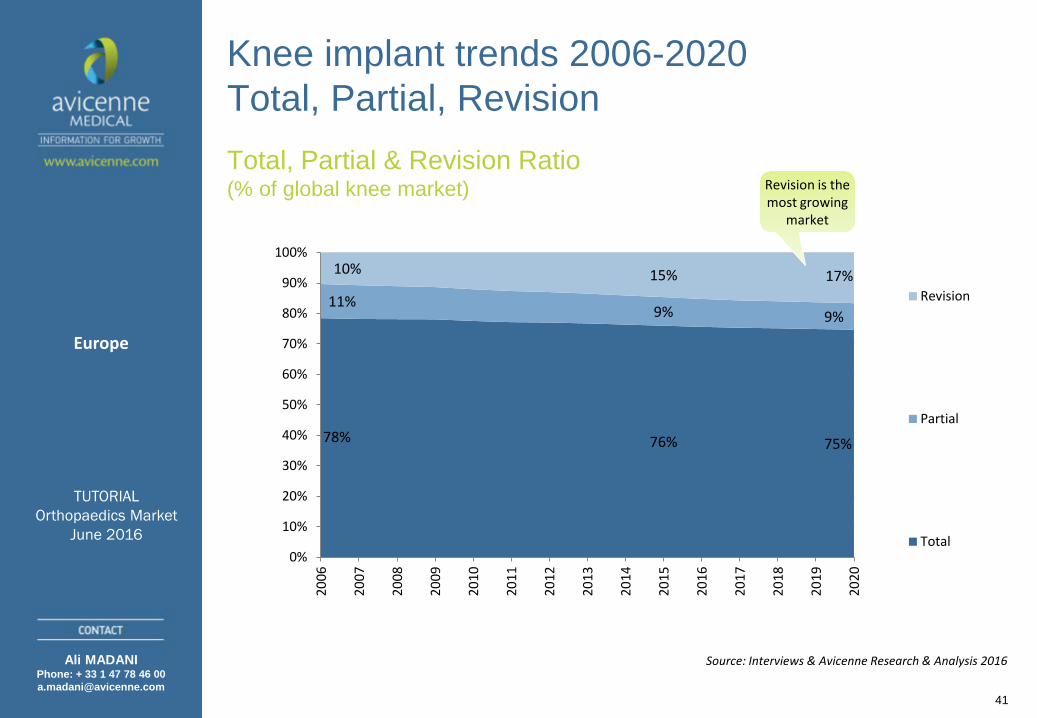

Knee implant trends 2006-2020Total, Partial, RevisionTotal, Partial & Revision Ratio(% of global knee market)

Source: Interviews & Avicenne Research & Analysis 2016

78% 76% 75%

11%9% 9%

10% 15% 17%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

Revision

Partial

Total

Europe

Revision is the most growing

market

Ali MADANIPhone: + 33 1 47 78 46 [email protected]

42

TUTORIAL Orthopaedics Market

June 2016

Total knee trends 2006-2020 (in volume)

Fixed bearing Vs. Mobile bearingFixed VS Mobile bearing Ratio (% of Total knees)

Source: Interviews & Avicenne Research & Analysis 2016

61% 60% 67%77%

39% 40% 33%23%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%20

06

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

Mobile bearing

Fixed bearing

Mobile bearing rate is decreasing

Europe

Ali MADANIPhone: + 33 1 47 78 46 [email protected]

43

TUTORIAL Orthopaedics Market

June 2016

Fixed bearing knee trends 2006-2020Cemented, Cementless, HybridCemented, cementless & hybrid ratio (% of fixed bearing Total knees)

Source: Interviews & Avicenne Research & Analysis 2016

66%56% 51%

15%23%

25%

19% 22% 25%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

Hybrid

Cementless

Cemented

Europe

Ali MADANIPhone: + 33 1 47 78 46 [email protected]

44

TUTORIAL Orthopaedics Market

June 2016

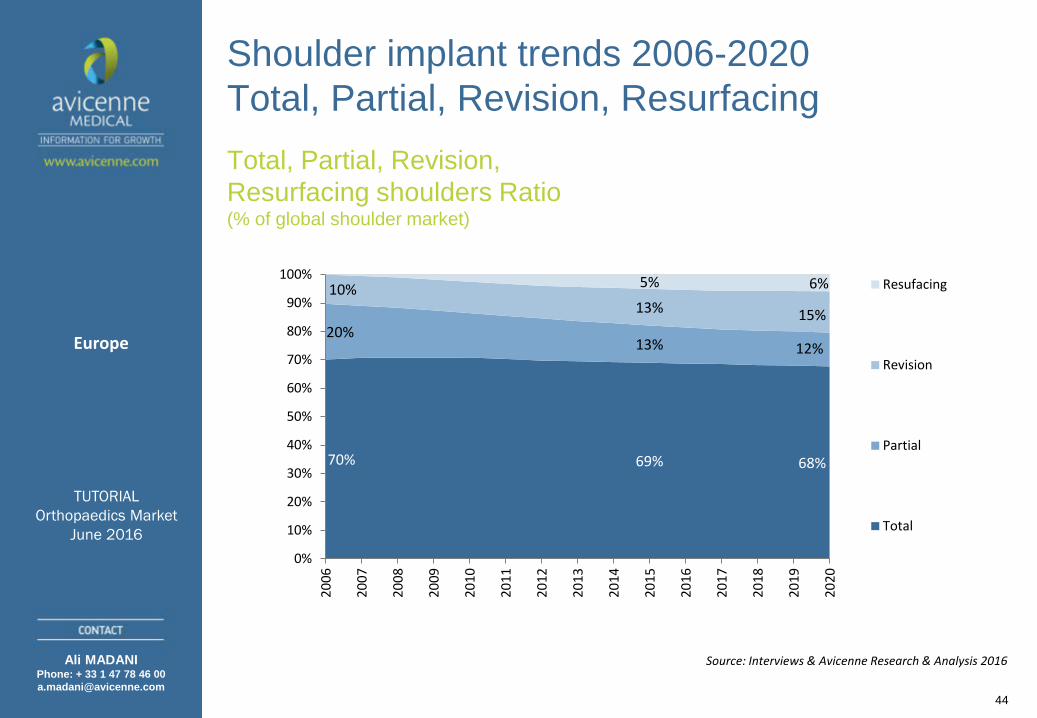

Shoulder implant trends 2006-2020Total, Partial, Revision, ResurfacingTotal, Partial, Revision, Resurfacing shoulders Ratio(% of global shoulder market)

Source: Interviews & Avicenne Research & Analysis 2016

70% 69% 68%

20%13% 12%

10%13% 15%

5% 6%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

Resufacing

Revision

Partial

Total

Europe

Ali MADANIPhone: + 33 1 47 78 46 [email protected]

45

TUTORIAL Orthopaedics Market

June 2016

Shoulder implant trends 2006-2020Standard Vs. ReversedTotal modular Shoulder implants Standard Vs Reversed(% of global shoulder market)

Source: Interviews & Avicenne Research & Analysis 2016

57%

35%28%

43%

65%72%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

Reversed

Standard

Reversed shoulder is a growing market

Europe

Ali MADANIPhone: + 33 1 47 78 46 [email protected]

46

TUTORIAL Orthopaedics Market

June 2016

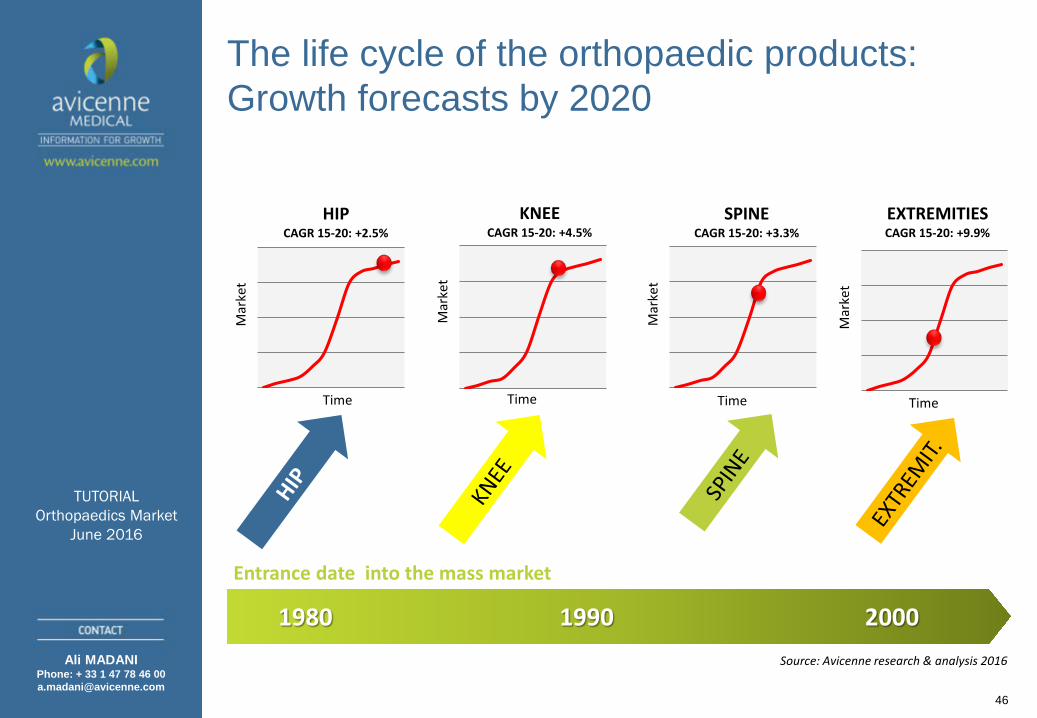

The life cycle of the orthopaedic products: Growth forecasts by 2020

Source: Avicenne research & analysis 2016

1980 1990 2000

Mar

ket

Time

HIP CAGR 15-20: +2.5%

Mar

ket

Time

KNEECAGR 15-20: +4.5%

Mar

ket

Time

SPINECAGR 15-20: +3.3%

Entrance date into the mass market

Mar

ket

Time

EXTREMITIESCAGR 15-20: +9.9%

Ali MADANIPhone: + 33 1 47 78 46 [email protected]

47

TUTORIAL Orthopaedics Market

June 2016

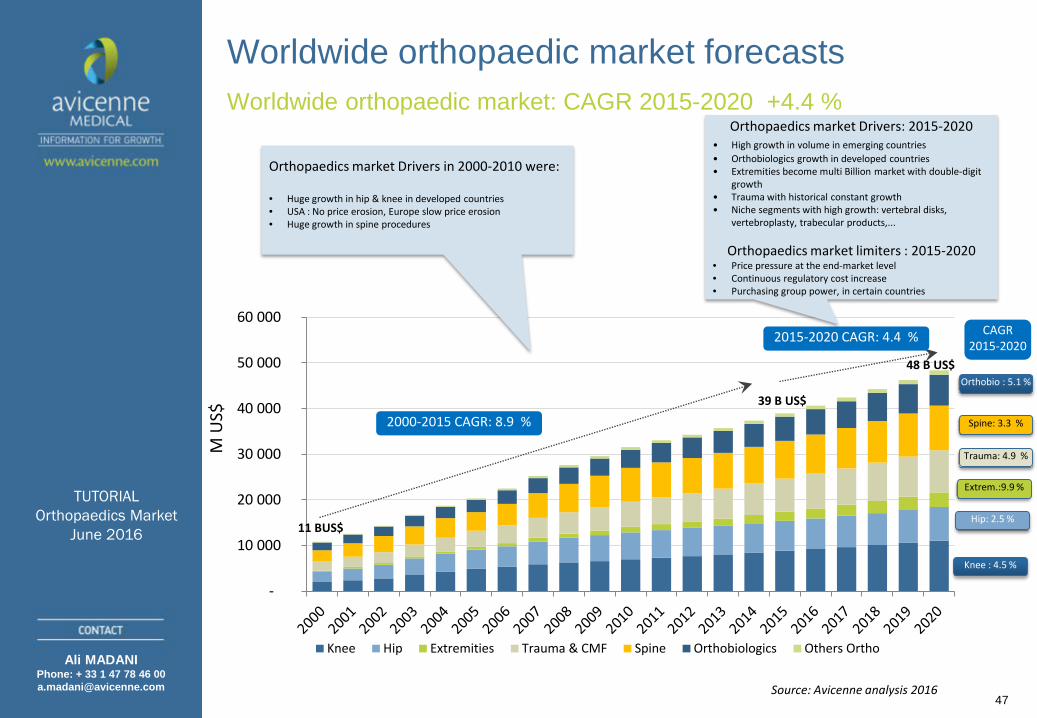

Worldwide orthopaedic market forecastsWorldwide orthopaedic market: CAGR 2015-2020 +4.4 %

11 BUS$

39 B US$

48 B US$

-

10 000

20 000

30 000

40 000

50 000

60 000

Knee Hip Extremities Trauma & CMF Spine Orthobiologics Others Ortho

2015-2020 CAGR: 4.4 %

Hip: 2.5 %

Knee : 4.5 %

M U

S$

CAGR 2015-2020

Extrem.:9.9 %

Trauma: 4.9 %

Source: Avicenne analysis 2016

Orthopaedics market Drivers in 2000-2010 were:

• Huge growth in hip & knee in developed countries• USA : No price erosion, Europe slow price erosion• Huge growth in spine procedures

Spine: 3.3 %

Orthobio : 5.1 %

2000-2015 CAGR: 8.9 %

Orthopaedics market Drivers: 2015-2020• High growth in volume in emerging countries • Orthobiologics growth in developed countries• Extremities become multi Billion market with double-digit

growth• Trauma with historical constant growth• Niche segments with high growth: vertebral disks,

vertebroplasty, trabecular products,...

Orthopaedics market limiters : 2015-2020• Price pressure at the end-market level • Continuous regulatory cost increase • Purchasing group power, in certain countries

Ali MADANIPhone: + 33 1 47 78 46 [email protected]

48

TUTORIAL Orthopaedics Market

June 2016

SummaryThe orthopaedics market, including hip, knee, spine, trauma, extremities and Orthobiologics accounted for more than US$39B in 2015, with 4.3% growth.The United States remains the largest market due to historical trends & higher sale prices. In Europe, Germany is by far the biggest market for all segments. Followed by the UK, France & Italy.Even the 5 major companies, controlling more than 60% of the worldwide orthopaedics market, have continuously loose market share to the challengers. The challengers have gained 1 to 2% market share per year (US$400 to 800 additional revenue), achieving US$15B in revenue in 2015 (13 US$15B in 2014!) .The only way for the Majors to have two-digit growth is by acquiring rivals (Depuy & Synthes, Zimmer & Biomet, Medtronic & Covidien ).A huge gap remains between the size of the Majors and that of the Challengers. The revenues of the Majors are 10 to 50 times bigger of the Challengers. But the Challengers are growing more rapidly, on average by 15%, due to their wider range of products, their local, high level services. They are also attracting new sales forces.The main drivers of the orthopaedics market remain demographic & economic parameters. Product innovation, resulting in a better (or higher) Product Mix, is boosting the market.The reimbursement trend results in price pressure. This is the main limiter of the orthopaedic market. Price erosion of mature products in orthopaedics has been a constant over the past 20 years. We do not expect a major shift, but some countries will suffer a more significant price decrease than others.

Ali MADANIPhone: + 33 1 47 78 46 [email protected]

49

TUTORIAL Orthopaedics Market

June 2016

SummaryRegulatory issues are becoming heavier and resulting in a longer time to market for new product launches, additional costs and a more limited range of products.Competition is fierce. In each country, the local challengers have a robust market share: Aesculap & Link for example in Germany, Lima & Adler in Italy, Amplitude in France, etc.Revision Implants are growing for all types of implants, cementless & Hybrid products continue to gain market share. Reversed shoulder, mini hip, Trabecular for hips and cages are examples of growing segments.In spite of regulatory issues & reimbursement trends, the orthopaedics market must continue to introduce innovations & new products and instruments to improve the new, less invasive and much more reliable surgical techniques.In 2000, this market was US$11 B It grew to US$39B in 2015, and it will achieve around US$48 B in 2020.That represents an average of 4.4% growth in the coming years.

THANK YOU

Recommended