Law 316: Secured Transactions G. Morgan (Waldron, Fall 2012) | Page 1

Secured Transactions Outline(Waldron, Fall 2012)

Road MapPPSA, Bank Act or Bills of Exchange Act?

PPSA: any creditor Bank Act: creditor must be a bank Bills of Exchange Act: negotiation on bill of exchange, promissory note, cheque, consumer bill or note

Personal Property Security ActDo you have a secured interest?

What is your collateral? goods consumer goods inventory equipment other stuff: instruments, money, licenses, etc.

Is the transaction covered by the PPSA? is the transaction named in PPSA s. 4 (major exclusions)?

yes no PPSA if no, does the transaction secure payment or performance of an obligation?

yes all PPSA applies if no, is the transaction named in PPSA s. 3 (transfer of an account or chattel paper, a commercial consignment or a

lease > 1 year)?yes deemed security interest = PPSA Parts I-IV apply (not Part V – Realisation)

n.b. PPSA s. 1(3): lease must be > 1 year AND the lease has run past 1 year to be a deemed security interestno no PPSA

Did the security interest attach? PPSA s. 12: attachment = a) value; b) rights in the collateral; and c) except for the purpose of enforcing rights between

parties, s/i enforceable under PPSA s. 10 (formality requirement) [generally, signed and written security agreement] PPSA s. 13: attachment steamroller (exceptions: crops and generally consumer goods unless replacement of original

collateral)Is there a signed and written security agreement? If no, do you need one?

PPSA s. 10: formal requirements for a security agreement to be enforceable against third partiesDid the creditor make a subsequent advance on the same collateral?

PPSA s. 14: tacking

Law 316: Secured Transactions G. Morgan (Waldron, Fall 2012) | Page 2

Do you have a perfected secured interest?Is the security interest perfected?

PPSA s. 19: perfection = (a) attachment + (b) all steps for perfection under PPSA completed

Three ways to fulfill PPSA s. 19(b) : PPSA s. 24: possession (but not seizure) PPSA s.25: registration of a financing statement temporary perfection provisions (period of time to either possess or (re)register the collateral)

PPSA ss. 26, 28(3),Did the creditor extend the money to purchase the collateral?

PPSA s. 22: perfection of PMSIsDid you register your secured interest properly?

Is the security interest perfected? PPSA s. 19: perfection = (a) attachment + (b) all steps for perfection under PPSA completed

Three ways to fulfill PPSA s. 19(b) : PPSA s. 24: possession (but not seizure) PPSA s.25: registration of a financing statement temporary perfection provisions (period of time to either possess or (re)register the collateral)

PPSA s. 26, 28(3), etc.Did something happen to your secured interest?

Was the collateral sold? cut-off rules(see below) PPSA s. 28: proceeds

n.b. requires a proper collateral description for the s/a to cover the proceeds tracing rules: lowest intermediate balance; tracing by subrogation

n.b. PPSA s. 1(5): equitable tracing rules can be applied to secured relationships that are not trustsDid the debtor change names or transfer the collateral to someone else?

PPSA s. 51: re-registration requirementsDid you accidentally discharge your financing statement?

PPSA s. 35(7): re-registration no more than 30 days to retain original priority (w/ exceptions)Did you make a mistake in your registration?

PPSA s. 43: seriously misleading objective test (Coates)

Who gets the stuff?Is the security interest cut-off?

PPSA s. 20(c): bona fide purchaser for value gets the collateral subject to an unperfected security interest PPSA s. 28(1): authorized dealing (express or implicit authorization) PPSA s. 30(2): OCB sale PPSA s. 30(3)(4): bona fide purchaser for value of consumer goods provided not fixtures nor purchase price/market value >

$1000 PPSA s. 30(5): cuts off grace period (15 day windows) for innocent third party buyers in PPSA s. 28(3) [proceeds]; s. 29(4)

[returned goods]; s. 51 [transfer of collateral to new debtor OR change in debtor name] PPSA s.30(6)(7): un-perfects serial numbered goods not registered by serial number for innocent third party buyers PPSA s. 51: transfer of collateral to new debtor OR change in debtor name

n.b. the specific priority rule always applies before the residual priority rules in s. 35(1)Does a specific priority rule apply?

PPSA s. 20(a)(b) notice provisionsn.b. grace period in PPSA s. 22 (15 days for PMSI holder to protect itself)

PPSA s. 28 proceedsn.b. requires a proper collateral description to cover proceeds

PPSA s. 35(4) failure to register serial number goods by serial number makes one unperfected for PPSA s. 35(1), lapsed registration rule in s. 35(7) and transfer in provision in s. 35(8)

PPSA s. 35(5)(6) future advance rules (creditor can tack future advances to priority position until the creditor has knowledge of a judgement creditor’s interest [n.b. can still tack some advances after knowledge

PPSA s. 35(7) 30 days from an inadvertent lapse or discharge of registration to re-register and retain priority (provided no one else has registered a s/i in the meantime notice principle)

PPSA s. 35(8) transfer in rule

Law 316: Secured Transactions G. Morgan (Waldron, Fall 2012) | Page 3

n.b. can apply to priority between s/i given to 2 different debtors PPSA s. 34(1)(2) PMSI

n.b. the priority rules in s. 34 only apply to S/I’s given by the same debtor PPSA s. 34(4): PMSI vendor > PMSI lender PPSA s. 34(5): priority for accounts financers PPSA s. 34(6): PMSI in original collateral > PMSI in collateral as proceeds PPSA s. 34(8)(9): PMSI in crops and livestock

If no specific priority rule apples, apply the residual priority rule PPSA s. 35(1) residual priority rule = perfected s/i generally take priority by the date of registration of f/s (or possession if

perfected by possession); perfected > unperfected; unperfected s/i generally take priority by date of attachmento n.b. only applies if a specific priority rule DOES NOT apply including other sub-rules in s. 35 that must be

considered before s. 35(1) appliesIs the stuff an instrument or another special circumstance?

Is the collateral / proceeds a negotiable or quasi-negotiable instrument? PPSA s. 31(1): cash $ PPSA s. 31(2): instrument drawn by debtor and delivered in payment of a debt owing to the recipient (w/ or w/o knowledge) PPSA s. 31(3): purchaser of an instrument has priority over an instrument perfected under PPSA s. 25 or temporarily

perfected under PPSA s. 26 or 28(3) if a) gave value; b) acquired w/o knowledge; and c) took possession PPSA s. 31(6): priority for chattel paper purchaser for new value

Is the property a returned or repossessed good? PPSA s. 29(1)(2): reattached and new security interests in returned or reposed goods

n.b. last priority to the account holder and first priority to holder of chattel paper who has a right to the chattel papern.b. see the Moodle handout on s. 29

Is the property a fixture? PPSA s. 36: fixtures

n.b. not priority between two secured parties but between a secured party and the land holder PPSA s. 49: registration in Land Title Office

Is the property crops? PPSA s. 37: crops

n.b. not priority between two secured parties but between a secured party and the land holderIs the property an accession?

PPSA s. 38: accessionsIs the property a co-mingled good?

PPSA s. 39: co-mingled goods n.b. no overlap with s. 38 therefore determine whether accession first

Is the property subject to a repairers’ lien? PPSA s. 32: repairer liens

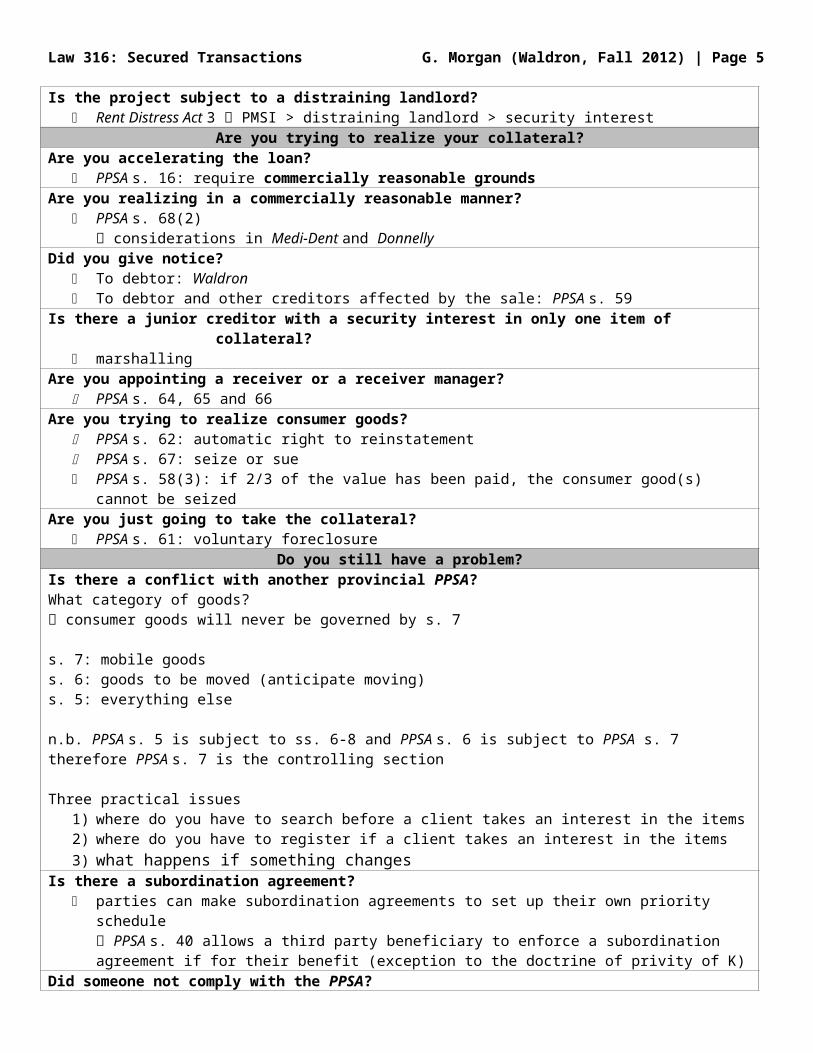

Is the project subject to a distraining landlord? Rent Distress Act 3 PMSI > distraining landlord > security interest

Are you trying to realize your collateral?Are you accelerating the loan?

PPSA s. 16: require commercially reasonable groundsAre you realizing in a commercially reasonable manner?

PPSA s. 68(2) considerations in Medi-Dent and Donnelly

Did you give notice? To debtor: Waldron To debtor and other creditors affected by the sale: PPSA s. 59

Is there a junior creditor with a security interest in only one item of collateral? marshalling

Are you appointing a receiver or a receiver manager? PPSA s. 64, 65 and 66

Are you trying to realize consumer goods? PPSA s. 62: automatic right to reinstatement PPSA s. 67: seize or sue PPSA s. 58(3): if 2/3 of the value has been paid, the consumer good(s) cannot be seized

Are you just going to take the collateral?

Law 316: Secured Transactions G. Morgan (Waldron, Fall 2012) | Page 4

PPSA s. 61: voluntary foreclosureDo you still have a problem?

Is there a conflict with another provincial PPSA?What category of goods? consumer goods will never be governed by s. 7

s. 7: mobile goodss. 6: goods to be moved (anticipate moving)s. 5: everything else

n.b. PPSA s. 5 is subject to ss. 6-8 and PPSA s. 6 is subject to PPSA s. 7 therefore PPSA s. 7 is the controlling section

Three practical issues1) where do you have to search before a client takes an interest in the items2) where do you have to register if a client takes an interest in the items3) what happens if something changes

Is there a subordination agreement? parties can make subordination agreements to set up their own priority schedule

PPSA s. 40 allows a third party beneficiary to enforce a subordination agreement if for their benefit (exception to the doctrine of privity of K)

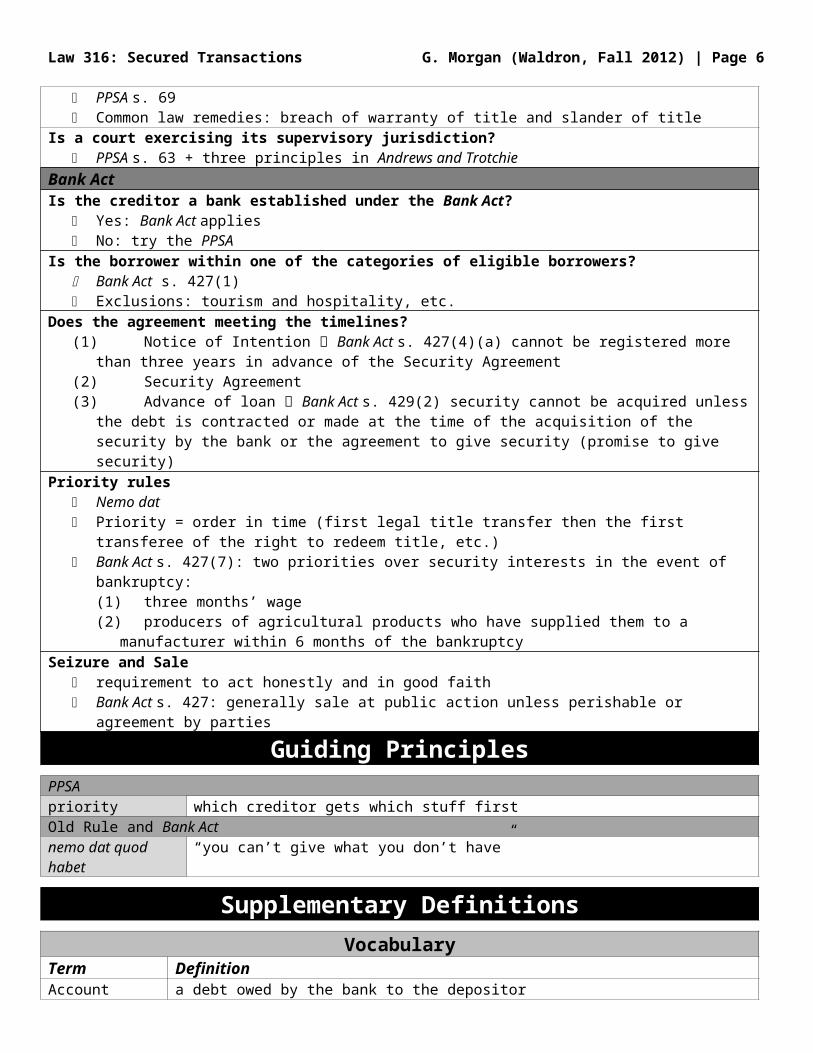

Did someone not comply with the PPSA? PPSA s. 69 Common law remedies: breach of warranty of title and slander of title

Is a court exercising its supervisory jurisdiction? PPSA s. 63 + three principles in Andrews and Trotchie

Bank ActIs the creditor a bank established under the Bank Act?

Yes: Bank Act applies No: try the PPSA

Is the borrower within one of the categories of eligible borrowers? Bank Act s. 427(1) Exclusions: tourism and hospitality, etc.

Does the agreement meeting the timelines?(1) Notice of Intention Bank Act s. 427(4)(a) cannot be registered more than three years in advance of the Security

Agreement(2) Security Agreement(3) Advance of loan Bank Act s. 429(2) security cannot be acquired unless the debt is contracted or made at the time of the

acquisition of the security by the bank or the agreement to give security (promise to give security)Priority rules

Nemo dat Priority = order in time (first legal title transfer then the first transferee of the right to redeem title, etc.) Bank Act s. 427(7): two priorities over security interests in the event of bankruptcy:

(1) three months’ wage(2) producers of agricultural products who have supplied them to a manufacturer within 6 months of the bankruptcy

Seizure and Sale requirement to act honestly and in good faith Bank Act s. 427: generally sale at public action unless perishable or agreement by parties

Guiding PrinciplesPPSApriority which creditor gets which stuff firstOld Rule and Bank Actnemo dat quod habet “you can’t give what you don’t have”

Supplementary DefinitionsVocabulary

Law 316: Secured Transactions G. Morgan (Waldron, Fall 2012) | Page 5

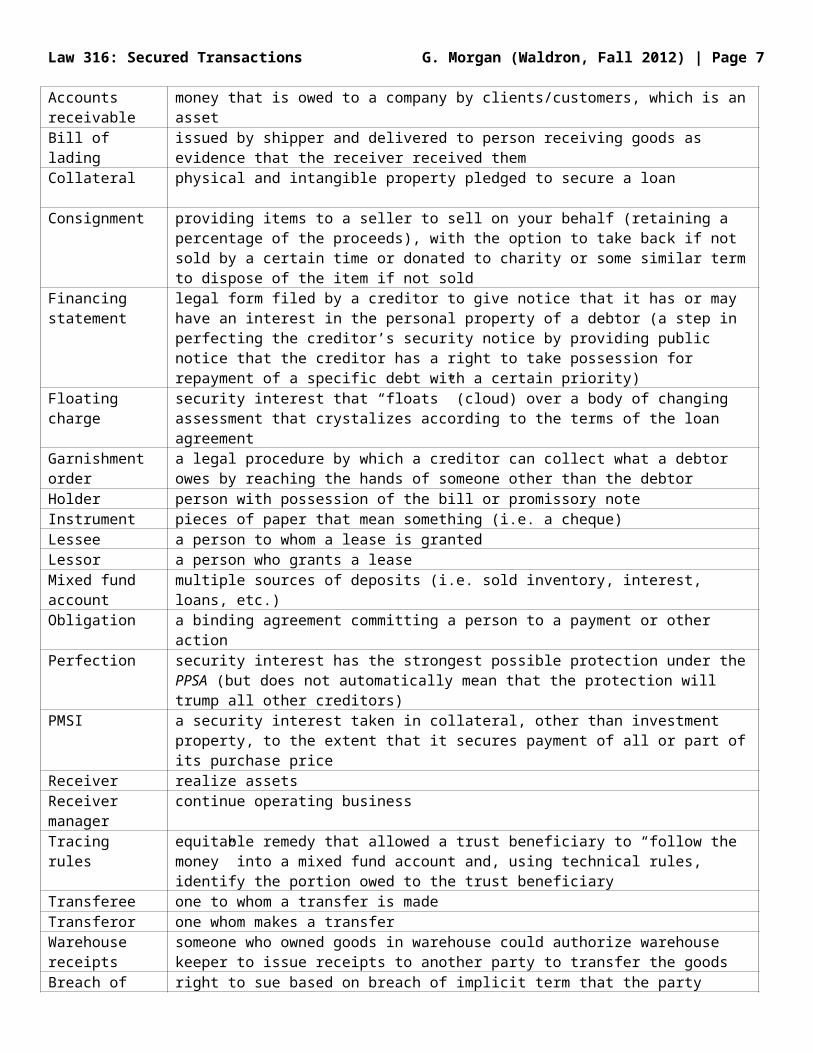

Term DefinitionAccount a debt owed by the bank to the depositorAccounts receivable money that is owed to a company by clients/customers, which is an assetBill of lading issued by shipper and delivered to person receiving goods as evidence that the receiver received themCollateral physical and intangible property pledged to secure a loan

Consignment providing items to a seller to sell on your behalf (retaining a percentage of the proceeds), with the option to take back if not sold by a certain time or donated to charity or some similar term to dispose of the item if not sold

Financing statement legal form filed by a creditor to give notice that it has or may have an interest in the personal property of a debtor (a step in perfecting the creditor’s security notice by providing public notice that the creditor has a right to take possession for repayment of a specific debt with a certain priority)

Floating charge security interest that “floats” (cloud) over a body of changing assessment that crystalizes according to the terms of the loan agreement

Garnishment order a legal procedure by which a creditor can collect what a debtor owes by reaching the hands of someone other than the debtor

Holder person with possession of the bill or promissory noteInstrument pieces of paper that mean something (i.e. a cheque)Lessee a person to whom a lease is grantedLessor a person who grants a leaseMixed fund account multiple sources of deposits (i.e. sold inventory, interest, loans, etc.)Obligation a binding agreement committing a person to a payment or other actionPerfection security interest has the strongest possible protection under the PPSA (but does not automatically mean that

the protection will trump all other creditors)PMSI a security interest taken in collateral, other than investment property, to the extent that it secures payment of

all or part of its purchase priceReceiver realize assetsReceiver manager continue operating businessTracing rules equitable remedy that allowed a trust beneficiary to “follow the money” into a mixed fund account and, using

technical rules, identify the portion owed to the trust beneficiaryTransferee one to whom a transfer is madeTransferor one whom makes a transferWarehouse receipts someone who owned goods in warehouse could authorize warehouse keeper to issue receipts to another

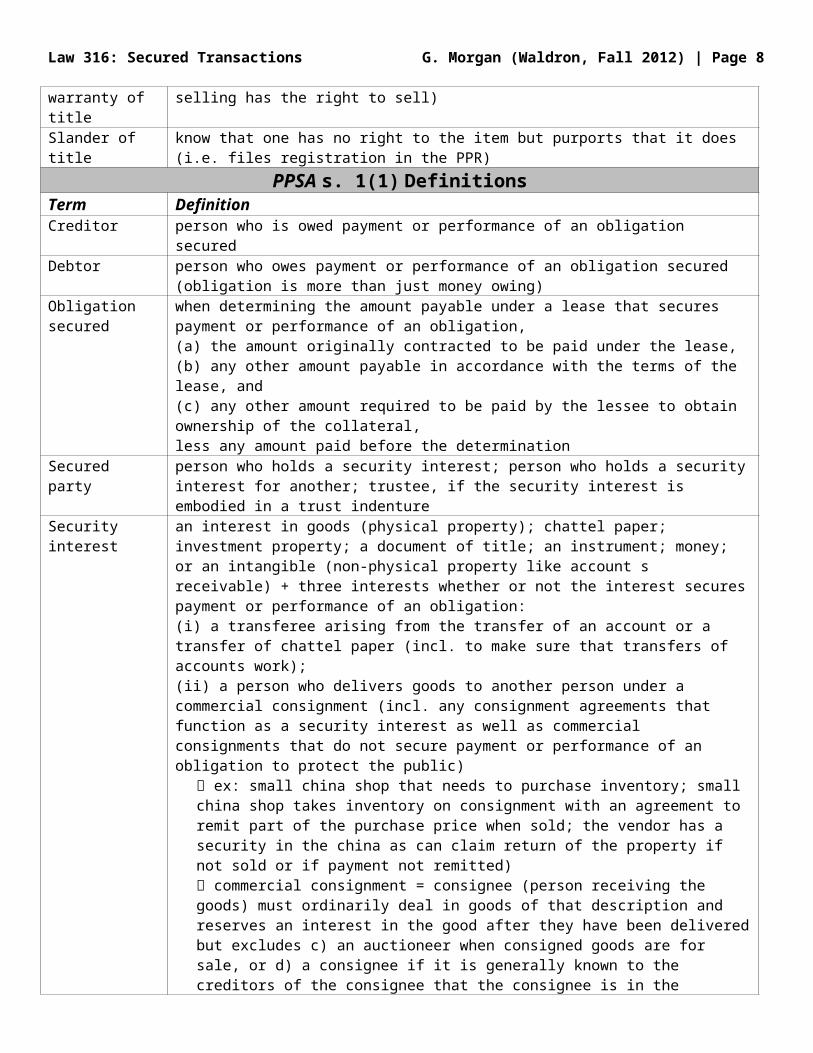

party to transfer the goodsBreach of warranty of title

right to sue based on breach of implicit term that the party selling has the right to sell)

Slander of title know that one has no right to the item but purports that it does (i.e. files registration in the PPR)PPSA s. 1(1) Definitions

Term DefinitionCreditor person who is owed payment or performance of an obligation securedDebtor person who owes payment or performance of an obligation secured (obligation is more than just money

owing)Obligation secured when determining the amount payable under a lease that secures payment or performance of an obligation,

(a) the amount originally contracted to be paid under the lease,(b) any other amount payable in accordance with the terms of the lease, and(c) any other amount required to be paid by the lessee to obtain ownership of the collateral,less any amount paid before the determination

Secured party person who holds a security interest; person who holds a security interest for another; trustee, if the security interest is embodied in a trust indenture

Security interest an interest in goods (physical property); chattel paper; investment property; a document of title; an instrument; money; or an intangible (non-physical property like account s receivable) + three interests whether or not the interest secures payment or performance of an obligation:(i) a transferee arising from the transfer of an account or a transfer of chattel paper (incl. to make sure that transfers of accounts work);(ii) a person who delivers goods to another person under a commercial consignment (incl. any consignment agreements that function as a security interest as well as commercial consignments that do not secure payment or performance of an obligation to protect the public)

Law 316: Secured Transactions G. Morgan (Waldron, Fall 2012) | Page 6

ex: small china shop that needs to purchase inventory; small china shop takes inventory on consignment with an agreement to remit part of the purchase price when sold; the vendor has a security in the china as can claim return of the property if not sold or if payment not remitted) commercial consignment = consignee (person receiving the goods) must ordinarily deal in goods of that description and reserves an interest in the good after they have been delivered but excludes c) an auctioneer when consigned goods are for sale, or d) a consignee if it is generally known to the creditors of the consignee that the consignee is in the business of selling or leasing goods of others

(iii) lease greater than 1 year including an indefinite term or a renewable lease with the total potential terms greater than 1 year but excludes a lease with a lessor who is not typically in the business of leasing goods or the lease of goods as part of a property lease, such as a furnished apartment (catch both the times where it is a security interest and the times where it it appear as if the lessee has ownership, so registration protects the public by providing notice that the lessee is not the owner)

Value any consideration sufficient to support a simple contract, and includes an antecedent debt or liability

New value = value other than antecedent debt or liabilityBills of Exchange Definitions

Term DefinitionBill of exchange “an unconditional order in writing, addressed by one person to another, signed by the person giving it,

requiring the person to whom it is addressed to pay, on demand or at a fixed or determinable future time, a sum certain in money to or to the order of a specified person or to bearer” (Bills of Exchange Act s. 16)

Cheque “cheque is a bill drawn on a bank, payable on demand” (Bills of Exchange s. 165)Promissory note “A promissory note is an unconditional promise in writing made by one person to another person, signed by

the maker, engaging to pay, on demand or at a fixed or determinable future time, a sum certain in money to, or to the order of, a specified person or to bearer” (Bills of Exchange Act s. 176)

Holder in due course person who has a bill that appears complete and regular provided a) became a holder before it was overdue and without notice that it has been dishonoured, and b) acquired in good faith and for value, and at time of negotiation no notice of defect in title of the person who negotiated it (Bills of Exchange Act s.55)

Policy ArgumentsPolicy Considerations in Secured Transactions

Policy Consideration Detailsfacilitate borrowing need capital to grow business, manage risk (permit business to save some capital in bankruptcy, spread

loss to others incl. vendor), make more money (leverage: capital of $100 plus loan of $1000 at 5% = investment of $1,100 with 10% interest = $110 profit - $50 interest = $60 gain = 60% rate of return on $100)

provide security way to ensure return of a loan (if you pay, you keep your property but if you don’t pay, you lose your property) more favourable interest rate with better security (i.e. interest rates are tailored to the risk of the loan, among other things, with a lower risk with a better security)

economic efficiency justification for the priority of secured debt: willing to lend money b/c there is assurance that the loan will be repaid need loans to promote commercial efficiency and productivity

Historical Framework for Secured TransactionsTerm Details Key ConceptsThree types of historical security arrangements

(1) Conditional sales agreement = vendor provides financing to a purchaser by accepting payments over a defined period of time (purchaser took possession from outset but the vendor retained title until the financing was paid in full)

(2) Chattel mortgage = purchaser borrows financing from a third party to make an expenditure from a vendor who is unable or unwilling to provide term financing under a CSA. As security, the purchaser will transfer some aspect of the title of an asset to the third party.

(3) Other legal arrangements that mimic the above transactions (i.e. a chattel lease, which mimics a CSA lease payments made over time with possession of the property, which the right to purchase outright at the end of the pre-defined lease term)

CSA = vendor financing

CM = third party financing

Historical context 16th century: pledge (similar to a contemporary pawn shop) unpaid vendor

Law 316: Secured Transactions G. Morgan (Waldron, Fall 2012) | Page 7

give up a possession in exchange for $; pay back $ + interest = return of possession)

However, what happens if you need to retain possession of the valuable item?Ownership of property = bundle of rights (possession and title are independent)Therefore the seller could retain the legal title while passing possession (and transferring title when the full amount is paid); failure to pay = right to possession ends and seller exercises legal right as the title-holder Conditional sales agreements (“CSA”)

But if the vendor is not in a position to lend the money, the purchaser may arrange a loan from a third-party (i.e. a bank) purchaser gets full title and possession as vendor is completely paid third-party lender gets security by taking the title for the purchased item (similar set up to CSAs) Chattel mortgage (“CM”)

What happens if there is already an existing CSA but the business owner needs an additional loan? can’t transfer title as security because the title is still with the vendor in the CSA (“nemo dat quod non habet”) vendor has title = problem: innocent party can lose out (i.e. if the purchaser sold the property under the CSA to a third party)

Registry system document of CSA filed in a central public registry so third parties can check the registry (public notice that a creditor has an interest in the property of a debitor) carrot = business efficacy but very big stick = significant consequences if the creditor does not register the CSA (non-enforcement against certain groups of people; typically bona fide purchasers for value without notice, other secured creditors, judgement creditors, trustee in bankruptcy)

Other arrangements then arose to avoid the registry systemExamples:

(1) Lease for defined period + final payment = transfer of ownership (similar arrangement to CSA but long-term lease with either an option or obligation to purchase at the end of the lease term)

(2) Consignments(3) Transfers of Accounts Receivable

However, the same problems arise out of these arrangements in that there is the potential to defraud third parties by appearing to have ownership even though the title remained with a different person/business

= money lender

Legislative response

Multiple statutes (i.e. Conditional Sales Acts, Chattel Acts, etc.) governing these types of lending arrangements with multiple processes for registration and multiple consequences for failure to register

Modernization started with Ontario in the 1970s: rational, unified and orderly system to facilitate business borrowing while protecting creditors and innocent third party purchasers adapted Article 9 of the Uniform Commercial Code followed by BC in 1980 and virtually every other jurisdiction in Canada

Law 316: Secured Transactions G. Morgan (Waldron, Fall 2012) | Page 8

Personal Property Security ActIntroduction

Term Details Key ConceptsFunctions of the PPSA

(1) regulates the creation and effectiveness of any instrument or document that creates a “security interest” (i.e. CSA, CMs, the “skirting” vehicles like long term leases

(2) pulls in some transactions that aren’t security interests but have the same capacity to deceive others about ownership (“deemed security interests”)

(3) registration or other public notice of these interests created in a debitor’s property (PPR registry)

(4) allows creditor to select the duration of registration (1 year to infinity)(5) consequences for non-registration (same as previous consequences)(6) rationalization of priorities(7) code for the realization of security interests (problem under the old law, which

said nothing about what happens when the debitor defaults on a loan)Relationships to other acts

s. 73 generally, the PPSA trumps other acts unless a specific provision that the other act applies despite the PPSAs. 74 two exceptions:

the Business Practices and Consumer Protection Act (or a provision for the protection of consumers in any other Act)

the Land Title Act

s. 75(1) references to Book Accounts Assignment Act, Chattel Mortgage Act, Company Act, Manufactured Home Act or the Sale of Goods on Condition Act that relates to a security interest = reference to the PPSA

s. 75(2) references to a chattel mortgage, conditional sales contract, floating charge, pledge, assignment of book accounts or other similar agreements = reference to the corresponding kind of security agreement in the PPSA

Marine Building Holdings Ltd. (BCSC 1993)

Facts: Δ makes a security agreement with the bank conveying a security interest in a number of items of Δ’s property (incl. Δ’s accounts receivable). Bank registers a financing statement, which achieved perfection of their security interest. Δ also became indebted to the Π. As Δ did not pay, Π sued Δ and got a legal judgement for the debt. Π began enforcement . Π serves garnishment orders to the Bank, Moli Energy and Westcoast Energy. Moli and Westcoast Energy paid their accounts receivable to the court. The bank argues that it is entitled to the money under the PPSA. The Π argues that it is entitled to the money under the judgement order.

Decision: PPSA trumps the other legislation therefore the bank gets the garnished funds as the Π was essentially an unsecured creditor

PPSA s. 20: groups that will win against an unperfected security interest (1) trustee in bankruptcy; (2) judgement creditor in the process of executing the order; (3) purchaser for value without notice

Justification for the priority of secured debt: economic efficiency (willing to lend money b/c there is assurance that the loan will be repaid)

Canamsucco Road House Food Co. (ONCtJ 1991)

Π owns a restaurant and is indebted to CIBC for a significant loan. CIBC has a registered GSA (General Security Agreement (GSA) = bank has security over absolutely everything). Π wants to sell the restaurant to Δ but Δ has to pay over time. Π agrees but takes out a GSA for the restaurant equipment to ensure Δ’s payment. If the Π fails to pay the money owed to CIBC, the agreement has a condition to allow the Δ to take over the CIBC payments (but taking that amount off the money owed to the Π). As Π is not paying the bank, the Δ starts making the payments directly to CIBC (and deducting from what is owed the Π). The Δ has an affiliated company, 936, provide the money to pay off CIBC in full, and CIBC assigns its GSA to 936 (936 essentially jumps into the shoes

Law 316: Secured Transactions G. Morgan (Waldron, Fall 2012) | Page 9

of the bank with the first security interest). There is also a third GSA taken out in favour of 936 for some additional funds owing. Δ argues that this third GSA is tacked onto the first GSA (CIBC 936) and therefore has priority.Decision: cannot tack in this situation (assigned priority does not get tacked with future advances) however, the PPSA may permit this type of tacking; open to interpretation

Significance of case: limit on tacking ability; structure of sale transaction (common mechanism by which to sell a business)

TackingTerm Details Key ConceptsStatutory Authorization

PPSA s. 14 provides that future advances and tacking can be included (CP 7)

Definition T1: S/I for Creditor AT2: S/I for Creditor BT3: further advance by Creditor A

Generally, Creditor A can “tack” the further advance at T3 to the obligation secured at T1 (typically securing priority over Creditor B) however, not always applicable (c.f. Canamsucco where tacking was not permitted as it would defeat the purpose of the PPSA)

Example Ex: T0 = security interest registered; T1 = $50,000; T1A = new security interest registered + loan of $100,000; T2 = loan $100,000; T3 = loan $50,000 the security interest registered at T0 includes the loans made at T2 and T3 in advance of T1A (provided perfected) tacking = add later advances to priority position created earlier

Hypothetical:X owns a car valued at $20,000X still owes the bank $10,000 on the loan borrowed to purchase the carBank holds a security interest in the car.X decided to sell the car to Y.

(1) Y assumes the $10,000 loan and pays X $10,000(2) Y pays X $20,000 and X promises Y that $10,000 will be paid to the bank to

resolve the loan problem: what happens if X doesn’t pay off the bank? write one cheque for $10,000 to X and one cheque for $10,000 to X and the bank (forcing X to pay the loan by making the bank party to that payment)

Debt AccelerationTerm Details Key ConceptsDefinition If the debtor defaults, it accelerates the debt (i.e. it’s all due after defaulting instead of

the balance over the pre-scheduled payment periods)Limitation under PPSA

Acceleration limited under PPSA PPSA s. 16: acceleration only when there are commercially reasonable grounds to believe that payment or performance is (or is about to be) impaired, or that the collateral is (or is about to be) placed in jeopardy however, the limitation does not apply to default situations but rather only when the secured party believes itself to be insured or that the collateral is in jeopardy

Policy considerations

Why the limitation? most corporations do not have the funds on hand to accelerate repayment, which results in the company losing all assets

Formal RequirementsTerm Details Key ConceptsRiepe v. Stingray Holdings Ltd. (BCSC 2002)

Facts: Riepe Sr. leased a pick-up truck with a lease agreement (“true lease”). Written agreement but business conducted without regard for the terms of the written agreement. At the end of lease, Riepe Sr. wants to purchase but he has defaulted on some payments. However, some agreement that they would continue with the

Law 316: Secured Transactions G. Morgan (Waldron, Fall 2012) | Page 10

purchase. Riepe Sr. sells truck to son, Riepe Jr. (not quite a bona fide purchaser for value without notice although it’s unclear what he knew). Payments not concluded. Stingray attempts to re-possess truck. However, was there a written security agreement to enforce rights against third party?

Decision: no written security agreement (however, no written agreement as there was only a verbal agreement to continue with the purchase. Waldron: unlikely that there was actually a security agreement after the lease agreement lapsed as no clear terms that the truck would be re-possessed)

Policy considerations: secured parties have an extraordinarily privileged position, which means that they must comply with the formalities of the PPSA to maintain that privileged position

674921 BC Ltd. v. New Solutions Financial Corp. (BCCA 2006)

Facts: two creditors of the same debtor. T1: Creditor A (674921) makes loan agreement with term that security would be given. T2: Creditor B (New Solutions) loaned the debtor money. T3: Debtor delivers GSA to Creditor A. New Solutions argues that at T2, there was no written agreement per the PPSA.

Decision: no security agreement at T1; further, no sufficient description for s. 10 – “assets” is not sufficiently precise

Waldron: it doesn’t take much to meet the requirements of the PPSA but they must be present to be enforceable

Inclusions / ExclusionsTerm Details Key ConceptsCommercial consignment

Commercial consignment (defined term) = goods delivered for sale, lease or other disposition (yes) to a consignee who, in the ordinary course of the consignee’s business, deals in goods of that description, by a consignor who,

(a) in the ordinary course of the consignor’s business, deals in goods of that description, and

(b) reserves an interest in the goods after they have been delivered (yes),but does not include an agreement under which goods are delivered(c) to an auctioneer for sale,(d) to a consignee other than an auctioneer for sale, lease or other disposition

if it is generally known to the creditors of the consignee that the consignee is in the business of selling or leasing goods of others why significant? protecting innocent third party rights but not extended to creditors when it is likely obvious that the goods in the warehouse would not be owned by the debtor

Re Toyerama (OSCB 1980)

* ON case, and ON law differs from BC law (add’l factor that would be significant in BC)

Facts: in 1979, toy manufacturer (Regal) was not moving “Willi Walker” and “Laffy Cathy.” To dispose of excess inventory, entered K with Toyerama to consign these toys to Toyerama. Toyerama declares bankrupty. Trustee who represents unsecured creditors wants to sell the toys to divide proceeds to the unsecured creditors. Regal objects as the toys were provided under consignment, which means that Regal retained title. Trustee argues that the consignment was a disguised security interest. If security interest, it is covered by PPSA, which is problematic as Regal did not register a financing statement with respect to the toys (failure to perfect = losses to certain groups of people, including trustees in bankruptcy PPSA s. 20(b)). Regal objects that it was a true consignment (not intended as a security interest). n.b. Ontario PPSA does not automatically include commercial consignments.

Waldron: the agreement omits an important part what happens if Toyerama does not sell the items consigned to it? (hallmark of a true consignment is that the items are returned or disposed of according to the terms of the agreement no obligation to pay for the item if not sold)

Re Stephanian’s Persian Carpets (ON 1980): if there was no obligation to pay for the

commercial consignment?

Law 316: Secured Transactions G. Morgan (Waldron, Fall 2012) | Page 11

items unless sold, there was no security agreement as there was not automatic debt

Decision: Regal retains ownership of items where there was no obligation to pay for; however, the trustee got ownership of items where there was an obligation to pay (i.e. returned items or items shipped to the retail locations)

BC is it a security interest? maybe/maybe not is it a commercial consignment under PPSA s. 3?

(a) in the ordinary course of the consignor’s business, deals in goods of that description (yes), and

(b) reserves an interest in the goods after they have been delivered (yes),but does not include an agreement under which goods are delivered(c) to an auctioneer for sale (no),(d) to a consignee other than an auctioneer for sale, lease or other disposition

if it is generally known to the creditors of the consignee that the consignee is in the business of selling or leasing goods of others (problem) why significant? protecting innocent third party rights but not extended to creditors when it is likely obvious that the goods in the warehouse would not be owned by the debtor in this case, unlikely that there are sufficient facts to make an adequate determination

however, some indication that this would be a ‘yes’ in this case (which would exclude the agreement from the automatic inclusion of a commercial consignment)

Leases Whether or not a lease falls under part 5 of the PPSA (i.e. true security lease or incl. simply b/c the lease term is more than 1 year) is important for personal leases (less relevant with commercial leases, when the terms of part 5 closely parallel the commercial reality) why? consumer protection vs. seize/sue provision of part 5 of the PPSA

Large body of literature distinguishing a true lease from a lease disguising a security interest list of factors (CP 35-6) that are considered but problematically they are ambiguous (i.e. insurance provisions likely applicable to both situations

Key factors: substantial security deposit req’d (i.e does it look like a partial down payment

on the purchase price?) what happens at the end of the lease term?

no option to purchase = true lease unless all the lease payments add up to the purchase price and the item will be worthless at the end of the lease period option to purchase: does the purchase price reasonably reflect the value of the item at the end of the lease period? this likely indicates a true lease. however, a nominal price would perhaps indicate a disguised security lease

Considered factors ( Daimler Chrysler ) :1) whether there was an option to purchase for a nominal sum2) whether there was a provision in the lease granting the lessee an equity or

property interest in the equipment3) whether the nature of the lessor’s business was to act as a financing agency4) whether the lessee paid a sales tax incident to acquisition of the equipment5) whether the lessee paid all other taxes incident to ownership of the equipment6) whether the lessee was responsible for comprehensive insurance on the

equipment7) whether the lessee was required to pay any and all licence fees for operation of

the equipment and to maintain the equipment at his expense8) whether the agreement placed the entire risk of loss upon the lessee9) whether the agreement included a clause permitting the lessor to accelerate the

payment of rent upon default of the lessee and granted remedies similar to

Law 316: Secured Transactions G. Morgan (Waldron, Fall 2012) | Page 12

those of a mortgagee10) whether the equipment subject to the agreement was selected by the lessee

and purchased by the lessor for this specific leaseDaimlerChrysler Services Canada Inc v Cameron (BCCA 2007)

@ trial: emphasis on the damages if the lessee failed to make lease payments (agreement provided that all monthly payments@ CA: term was a normal breach for a chattel sale agreementTwo options: (1) true lease (some PPSA would apply as the term was > 1 year but the realisation provisions would not apply); (2) lease intended as a security agreement (all PPSA applies incl. realisation provisions)

Debtor wants the lease to be considered (2) as the realization provisions incl. protection for consumer property (either repossess or sue for damages but not both)

@ trial focus on the default provision (¶18), which was inconsistent with the lease of property where taking the property back ended further damages (however, BCCA notes that this position was reversed by the SCC proper measure of damages is expectation damages, which is the measure described in ¶18) @BCCA factors considered in characterization of lease (¶22)

Big question: what happens at the end of the defined lease term? If there is no option to purchase, is there any value left in the item after the

defined lease term? (no value = intended as security agreement b/c it is like purchasing the item; some value = true lease)

If there is an option to purchase, is the option a nominal sum or is it set to reflect the real value of the item anticipated at the end of the lease period? (real value of item = true lease; nominal value = intended as security agreement)

lease

Newcourt Financial Ltd. v. Frizzell (BCSC 2000)

Facts: lease agreement for vehicle; debtor defaulted one payment, made two payments and then defaulted two payments; creditor attempted to speak to debtor ; creditor went to repossess the vehicle

Acceleration clause limited by PPSA commercially reasonable grounds to accelerate the owning balance if the creditor thinks that the debtor may default

The opposite of an acceleration clause is the right to re-instate payments after default under the PPSA, a consumer has a right to re-instate two payments per calendar year (in Part V of the PPSA)

Typically the re-instatement is acceptable to the creditor (given the limited options to realise consumer goods under the PPSA)

In this case, the creditor wanted to continue the acceleration the ability to seek this provision hinges on whether the lease is a true lease or a lease intended as a security agreement

Application: clearly a lease > 1 year but option price = “genuine pre-estimate of the vehicle’s fair market value on that date [end of the term]” accordingly, true lease

Trusts How could a trust be set up to provide security? (Waldron: used to be a common structure but no longer)

Ex: Retailer (“R”) who sells various items of inventory. R cannot afford to pay for inventory before it is sold (i.e. financing their inventory). R makes arrangement with Wholesaler (“W”). W can send inventory to R under a trust arrangement (trustee has possession and trust beneficiary has title with trustee obliged to act in the interests of the trust beneficiary incl. the money produced by the sale of goods). Trust arrangement meant that R held profits in trust for W. If R defaulted, W would have a right for the unsold inventory as well as a right to the proceeds (“trust funds.”) This model provided W with a very secure position.

Benefits:

Inventory supplier common actor in PPSA

Law 316: Secured Transactions G. Morgan (Waldron, Fall 2012) | Page 13

In bankruptcy, the trustee in bankruptcy generally cannot touch trust funds W has equitable tracing rules

Skybridge Holidays Inc. (Trustee of) v. British Columbia (Registrar of Travel Services) (BCCA 1999)

Facts: Skybridge had money given by travellers purchasing travel packages with Skybridge (i.e. Customer X gives Skybridge $$$ to purchase tickets). Before the tickets are purchased, the money is placed in Skybridge’s account (with the money of different travellers.) At any given time, Skybridge’s account has money from multiple travellers.

Skybridge declares bankruptcy. The trustee in bankruptcy swoops in to get $ for unsecured bankruptcy. However, money owed to secured creditors and property not owned by Skybridge is not available to the trustee.

Skybridge was regulated by statute. The provincial statue required that Skybridge hold money received by travellers be held in trust. However, the Bankruptcy and Insolvency Act (federal legislation) did not recognized provincially created trusts and (through paramountcy) therefore the travellers become 1 of however many unsecured creditors.

@ trial, the travellers argue that there was a genuine trustProblem: each traveller will have to prove on the facts that the funds were provided to Skybridge in a trustee relationship trustee in bankrupty argues that the trusts were security interests (unregistered) therefore not perfected b/c not registered (PPSA s. 20 = failure to register means that the trustee in bankruptcy has priority) PPSA creates an exemption to the rule that trustees in bankruptcy cannot take property not owned by the bankrupt (if you are considered to have created a security interest in an item but fail to fulfill PPSA requirements, the trustee in bankruptcy can take the property)

Problem: is the trust a security interest? (i.e. is it securing payment or performance of an obligation? (analysis: what is the obligation and what happens if the obligation is unfulfilled)

in this case, customer X has no security for the transferred funds therefore not a security interest

accordingly, the case will proceed as an analysis of each individual’s trust relationship (if any) to Skybridge

Moral of the story: a trust can be a security interest but not always there needs to be an obligation secured by the right of the creditor to use some of the debtor’s property to fulfill the obligation if the debtor fails to repay the credit

Furmanek v. Community Futures Development Corp. of Howe Sound (BCSC 2000)

Facts: Spargo enters agreement to purchase Furmanek’s jewellery business. Spargo

borrows money from Community Futures to partially pay Furmanek, and Furmanek accepts the balance on a payment plan (i.e. as a creditor). Both Community Futures and Furmanek take security interests. Furmanek agrees that Community Futures should have first priority (only way to get a third party lender). However, in registration, Furmanek perfects first b/c Community Futures made a mistake in registration. However, the Court gave Community Futures priority as that was the agreement between the two creditors.

Spargo entered consignment agreement with Seca Gems (genuine consignment). Seca sends jewellery to Spargo.

Spargo defaults on loans from Furmanek and Community Futures, and Community Futures appoints receiver to engage in orderly realization of business property

Seca’s jewellery is still in Spargo’s inventory

Is Seca’s jewellery a commercial consignment (and therefore covered by the PPSA as an unperfected security interest)?

commercial consignment = goods deliver for sale, lease or other disposition (yes) to a consignee who, in the ordinary course of the consignee’s business,

commercial consignment?

Law 316: Secured Transactions G. Morgan (Waldron, Fall 2012) | Page 14

deals in goods of that description (yes), by a consignor who,(e) in the ordinary course of the consignor’s business, deals in goods of that

description (yes), and(f) reserves an interest in the goods after they have been delivered (yes),but does not include an agreement under which goods are delivered(g) to an auctioneer for sale (no),(h) to a consignee other than an auctioneer for sale, lease or other disposition

if it is generally known to the creditors of the consignee that the consignee is in the business of selling or leasing goods of others (problem) Furmanek was aware b/c it was how Furmanek did business as the past owner however, Community Futures was not aware court: test is whether creditors generally now (not whether the specific creditors knee) in this case, creditors did not generally know that Spargo was in the business of selling or leasing goods of others

Accordingly, Seca was deemed to be a commercial consignment and therefore lost priority to the perfected secured creditors

However, Seca took back some of the property and the security interests of Furmanek and Community Futures specified inventory, which the property was no longer when Seca regained possession

Court not quite as the receiver was appointed by the property was regained (which defeats the purpose of the PPSA to orderly distribute assets)

CollateralTerm Details Key ConceptsCollateral Definition: personal property that is subject to a security interest

in PPSA, the categories under personal property are almost always mutually exclusive (i.e. if it falls into one category, it won’t all in the other)

two major divisions: (1) goods; (2) other stuff

Goods (defined term) = tangible personal property (stuff you can touch) plus fixtures, crops, unborn young of animals but does not include chattel paper, documents of title, money, trees other than crops, minerals and hydrocarbon prior to being extractedThree categories of goods:

(1) consumer goods(2) inventory(3) equipment

Other stuff = instruments (defined term includes cheques, letters of credit); accounts (defined term monetary obligation that cannot be touched; excludes chattel paper and instruments); chattel paper (defined term one or more writings that evidence both a monetary obligation and a security interest in goods; e.g. lease agreements in DaimlerChrysler and Newcourt Financial); intangible property; licenses (defined term right that entitles the holder to do some things); money (defined term medium of exchange)

debate over fishing licences: right issued by the government at the discretion of the minister (and which can be revoked); traditionally b/c of reliance on ministerial discretion it was not considered property; however, it is a very valuable item (essential to secure loans for holders as often most valuable property) therefore broader definition than common law (Saulnier)

ProceedsTerm Details Key ConceptsDefinition Definition of “proceeds” (defined term)

Law 316: Secured Transactions G. Morgan (Waldron, Fall 2012) | Page 15

(a) identifiable or traceable personal property, fixtures and cropsi) derived directly or indirectly from any dealing with collateral or the

proceeds of collateral, andii) in which the debtor acquires an interest

(b) a right to an insurance payment or any other payment as indemnity or compensation for loss of, or damage to, the collateral or proceeds of the collateral

(c) a payment made in total or partial discharge or redemption of an intangible, an instrument, investment property or chattel paper, and

(d) rights arising out of, or property collected on, or distributed on account of, collateral that is investment property

(b) to (d) are additional inclusions that may not be evidenceExamples Ex: Vendor sells boat to debtor on a condition sales agreement. Debtor sells boat to X

duplicitously. If vendor registered, the vendor could follow and reclaim the boat from X as notice given. However, this could be complicated if the debtor is in the business of selling boats, etc. The vendor might actually want the proceeds from the sale to X (i.e. $1000 + smaller boat).

The old law did not give a right to the proceeds. However, the PPSA gives a right to the proceeds from the sale of collateral (PPSA s. 28).

Revised example:D receives $1000 and a blue boat for the sale of the collateral to X derived from the sale of the collateral.

identifiable personal property = blue boat + $1000 in cash traceable personal property = $1000 after deposit in mixed funds bank account

Hypothetical #1:A buys a red boat and gives the bank a security interest in the red boat to finance the purchase price. A sells the red boat to B in exchange for a blue boat plus $1000 in cash. B sells the red boat to C in exchange for a green boat.

Proceeds from red boat blue boat + $1000 cash Proceeds does not include the green boat (while the green boat is derived from

a dealing in the collateral, the debtor – A – did not acquire an interest in it)

The bank registers a financing statement reading “a security interest in A’s red boat.”S. 28(3) gives 15 days to amend the f/s otherwise the perfected status of the security interest is lost (hence subject to lesser priority under s. 20.)

Limitations Limitations to proceeds: PPSA s. 28(1): secured party expressly or impliedly authorizes the dealing

with the collateral what about inventory held for sale? likely implied authorization but also PPSA s. 30(2): a sale in the ordinary course of business of the seller (def’d s. 30(1))

* key to public notice: registration of a financing statement in the PPR

n.b. the PPSA includes proceeds of proceeds (i.e. exchanging the blue boat for a refrigerator.) This extends indefinitely.

Re CIBC & Marathon Realty Co. Ltd. (SKCA 1987)

Facts: Kiddies has loan to purchase inventory and also defaults on rent. Right to distraint: commercial landlords seize goods to sell off to pay for defaulted rent. However, right to distraint subject to certain types of security interests (Rent Distress Act).

Decision: CIBC had a properly perfected interest in the inventory (even though it was proceeds of proceeds) that the landlord could have found by searching the registry

Additional note: not commercial reasonable for third parties to expect secured parties’ to

Law 316: Secured Transactions G. Morgan (Waldron, Fall 2012) | Page 16

enforce rights unilaterally

Tracing ProceedsTerm Details Key ConceptsTracing rules Customer uses a $20 bill to purchase an item of inventory. The bill goes in the cash

register and this money is then deposited in a bank account where it is credited to the vendor’s account. An account is a debt (i.e. the bank owes you the amount of money in the account.) The account will have different sources of money (i.e. funds from different items of inventory sold, some interest on investments, etc.) a mixed fund account.

Equitable tracing rules allow a trust beneficiary to follow funds into a mixed fund account and to claim a portion under technical rules that identified what portion belonged to the trust beneficiary.

Identifiable Proceeds

at common law, funds from a trust could not be followed once they were converted to a different form but equitable tracing rules allowed the trust beneficiary to follow the funds so long as the funds were identifiable the PPSA gives the tracing rules to secured parties (even outside the context of a trust) (see PPSA s. 1(5))Hypothetical:

T1: A gives bank security interest in “all freezers” and bank registers f/s to that effectT2: A sellers a freezer to B. B gives A a cheque for $6,000 assume that the sale is not in the course of ordinary business (i.e. A owns a restaurant) cheque = instrument = proceeds under s. 28(2) [perfected security interest]T3: A deposits cheque into an account at a credit union. account = proceeds of proceeds (i.e. B sells credit union the cheque for an account) cheques = bills of exchange under federal act (negotiable intstruments are an occupied field per s. 28(2), the bank has a security interest in the accountT4: A withdraws $2,000 cash, A used $1,000 to pay MasterCard bill and A gives $1,000 cash to niece as birthday gift. proceeds of proceeds (balance of account) + proceeds of proceeds of proceeds ($2,000 cash) money is a continuously perfected security interest per s.28(2) money is governed by the federal government and is the easiest security interest to lose (b/c it must be freely transferrable)

What if the account was a mixed fund account? turn to equitable tracing rules: lowest intermediate balance rule

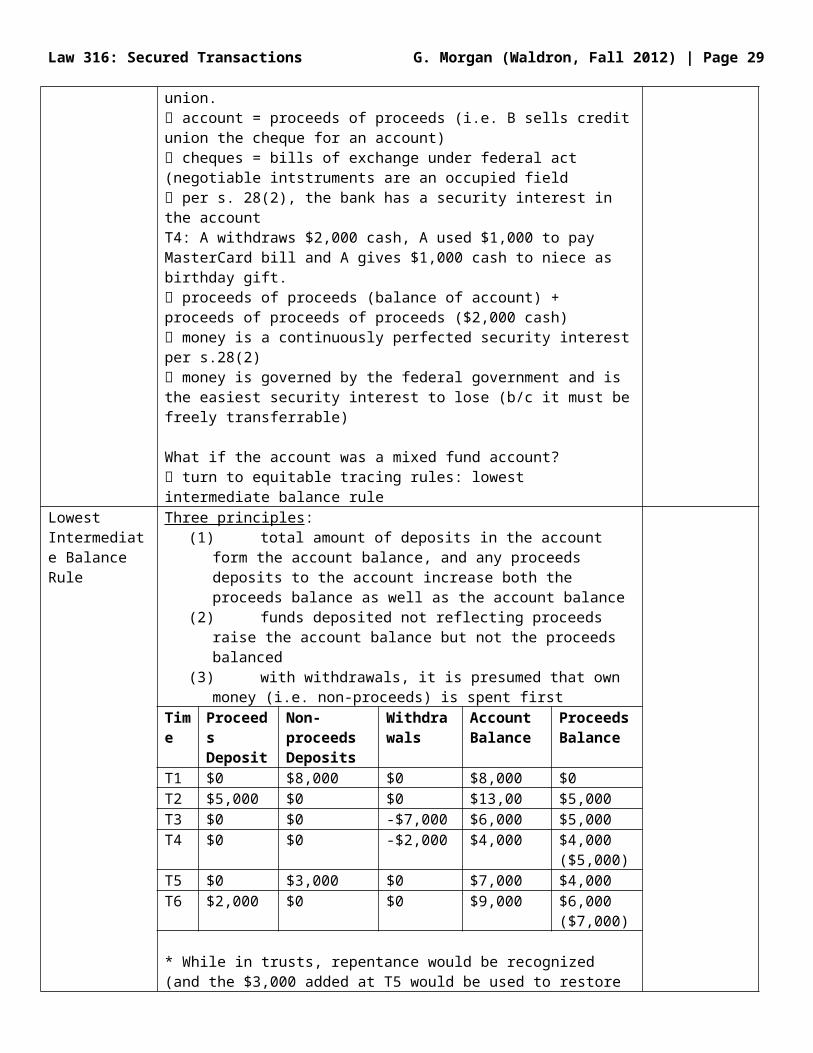

Lowest Intermediate Balance Rule

Three principles:(1) total amount of deposits in the account form the account balance, and any

proceeds deposits to the account increase both the proceeds balance as well as the account balance

(2) funds deposited not reflecting proceeds raise the account balance but not the proceeds balanced

(3) with withdrawals, it is presumed that own money (i.e. non-proceeds) is spent first

Time

Proceeds Deposit

Non-proceeds Deposits

Withdrawals

Account Balance

Proceeds Balance

T1 $0 $8,000 $0 $8,000 $0T2 $5,000 $0 $0 $13,00 $5,000T3 $0 $0 -$7,000 $6,000 $5,000T4 $0 $0 -$2,000 $4,000 $4,000

($5,000)T5 $0 $3,000 $0 $7,000 $4,000T6 $2,000 $0 $0 $9,000 $6,000

Law 316: Secured Transactions G. Morgan (Waldron, Fall 2012) | Page 17

($7,000)

* While in trusts, repentance would be recognized (and the $3,000 added at T5 would be used to restore the proceeds balance to $5,000), it is not recognized in PPSA as the remainder of the account goes to other creditors (less secured or unsecured creditors) policy benefit: balance secured creditors with other creditors

* Rule must be applied mechanically (no preference for specific creditors, etc.)Universal C.I.T. Credit Corporation v. Farmers Bank of Portageville (USDC 1973)

Facts: Ryan sells cars on a financing agreement for the Π. Π had financing statements filed reflecting security interest in the proceeds from the sale of the cars. Ryan deposits the funds in an account with the Δ. Ryan also owes money to the Δ on a promissory note. Π indicates that it will be cancelling the financing agreement. Ryan had written cheques to Π but they had not been deposited. Ryan tells the bank to withdraw the money owed on the promissory note (instead of letting the money go to the Π). The cheques bounced (NSF). Π sues the Δ for the withdrawn funds.

Application of lowest intermediary balance rule on CB 91

However, a slight tweak to the fact pattern may have resulted in a different outcome if the bank was not aware that proceeds were held in the account [innocent party] the withdrawal was irregular (after the close of business), which suggested a fraudulent practice to defraud the secured party [different if Ryan had withdrawn the money himself and then given it to the bank]

Tracing by subrogation

Broader understanding of tracing rules than strict “follow the money” (i.e. in situations where the accounts are more complex, or perhaps multiple accounts)

considers the commercial realities what is the original collateral, what role did it have in the debtor’s life/business, what interest does

is there a connection between the end going into the ball of yarn and the end going out? how much is the secured party entitled to?

Agricultural Credit Corp. of Sask. v. Pettyjohn (SKCA 1991)

Facts: the Pettyjohns took out money from ACCS to purchase cows. ACCS had a purchase money security interest in 47% of the cows as well as a general security interest in all cows (type of interest important as garden-variety security interest does not permit seizure of farm equipment.) The Pettyjohns started to sell herd to replace them with Watusi cattle. Given the complicated and often undocumented nature of the transactions, it was very difficult to trace the original cattle to the Watusi cattle (smaller herd).

the Pettyjohns argued that since ACCS could not trace (per trust law), ACCS could not

However, the court noted that the PPSA is not a trust therefore the strict trust rules do not apply replacement collateral (i.e. follow the string in and out)

the Watusi cattle perform the same function as the PMSI cattle clear that the funds from the PMSI cattle were used to purchase “replacement”

property

Dissent: security interest over all Watusi cattle to the total of the PPSIMajority: the dissent’s reasoning would be unfair to unsecured creditors therefore ACCS is entitled to a security

The dissent noted that the Pettyjohns would benefit (not unsecured creditors) and the mess was in part due to their mismanagement. The majority, however, was of the opinion that the outcome was specific to the particulars of this case (as opposed to a different situation with unsecured creditors)

Tracing by subrogation rule

look at the original collateral if the middle is too confusing, look to the end to see if there is replacement collateral that performs the same function in the debtor’s economic situation if there is replacement collateral, the creditor will get the same proportion of this

Law 316: Secured Transactions G. Morgan (Waldron, Fall 2012) | Page 18

collateral in security interest as it had in the original collateral

* no requirement that the middle is too confusing because of a particular reason (i.e. poor bookkeeping in Pettyjohn) but it likely would be advantageous to be able to argue that there are reasons that tracing rules are not functioning (i.e. poor bookkeeping ;-) )

Re River Industries Ltd. (BCSC 1992)

BC example of application of tracing by subrogation rule

Facts: Acklands Ltd. had a security interest in some of the inventory of the debtor. The debtor sold everything in bulk.

Neither cut-off rule applied no consent to deal (sale in bulk different from individual inventory sale) and not a OCB sale

Accordingly, Acklands Ltd. was allowed to retrieve the inventory that it had supplied on credit. However, it did not account for proceeds (i.e. additional inventory purchased from the proceeds of the sale of other Acklands inventory and other inventory in general.)

Application of tracing by subrogation rule Beginning: Acklands Ltd. had a security interest in X% of the inventory End: inventory that likely included proceeds Acklands granted X% of the end inventoryCreating the Security Interest: Perfection and Attachment

Term Details Key ConceptsPerfection PPSA s. 19 a security interest is perfected when

a) is has attached, andb) all steps required for perfection under this Act have been completed,regardless of the order of occurrence

Three ways to fulfill s.19(b):(1) PPSA s. 24 subject to s. 19 (i.e. must attach as well), possession of

collateral perfects a s/I in chattel paper, goods, an instrument, a negotiable document of title and money unless the possession is a result of seizure or repossession perfection = attachment + possession (but not seizure)

(2) PPSA s. 25 subject to s. 19, registration of a financing statement perfects a s/I in collateral perfection = attachment + registration of a financing statement

(3) provisions for temporary perfection such as PPSA s. 28(3) temporary perfection = attachment + a period of time to either possess or register the collateral

What do these methods achieve? notice to third party (either by possessing the collateral or by registering the

collateral)Attachment PPSA s. 12

(1) A security interest attaches whena) value is given,

valueb) the debtor has rights in the collateral or power to transfer rights in the

collateral to a secured party, and rights in the collateral

c) except for the purpose of enforcing rights between the parties to the security agreement, the security interest becomes enforceable under s. 10 (formality requirement either possession or a security agreement in writing signed by the debtor that properly described the collateral) generally, a signed written security agreement

Law 316: Secured Transactions G. Morgan (Waldron, Fall 2012) | Page 19

PPSA s. 13(1) automatic attachment when the security agreement covers after acquired

property and the debtor purchases further assets (“attachment steamroller”)(2) exceptions:

a) crops that start to grow after a yearb) generally excludes consumer goods unless the newly acquired item is a

replacement for the original collateralTiming of Attachment and Perfection

Scenario 1:

T1: debtor buys collateralT2: creditor lends $ and a general security agreement is signedT3: creditor registers financing statement

Attachment = T2Perfection = T3

Scenario 2:

T1: creditor lends $ and a general security agreement is signedT2: creditor registers financing statementT3: debtor buys collateral

Attachment = T3Perfection = T3

significant to PPSA s. 35

Scenario 3:

T1: creditor registers a financing statementT2: creditor lends $ and a general security agreement is signedT3: debtor buys collateral

Attachment = T3Perfection = T3

Scenario 4:

T1: creditor registers a financing statementT2: debtor buys collateralT3: creditor lends $ and a general security agreement is signed

Attachment = T3Perfection = T3

Components of AttachmentValue (defined term) any consideration sufficient to support a simple contract, and includes an

antecedent debt or liability the PPSA may specify new value but attachment only needs value

TD Bank v. Nova Entertainment (ABQB 1992)

Facts: parent company makes loans to subsidiary company at T1; parent company takes security interest/registers interest at T2

Another creditor argues that the parent company did not get value (i.e. was not perfected) however, as value includes an antecedent debt, the security interest was perfected

Rights in the Collateral

PPSA s. 12(2) a debtor has rights to leased goods or consigned goods when the debtor obtains possession of them in accordance with the lease or consignmentHowever, the secured party can only acquire the rights that the debtor has under the lease or consignment

PPSA s. 12(3)A debtor does not have rights in any of the following:

a) crops until they become growing cropsb) the young of animals until they are conceivedc) minerals or hydrocarbons until they are extractedd) tress, other than crops, until they are severed

* mere possession is (i.e. insufficient to be a gratuitous bailee or a bailee for hire)Kinetics Technology International Corp. v. The Fourth National Bank of Tulsa (US CA 10th circ. 1983)

Facts: Oklahoma Heat Transfer (OHT) indebted to the bank: took out loan and granted

security interest in inventory OHT entered K with KTI to produce furnace economizers KTI sent goods to OHT, who installed the goods in constructed items KTI would also send progress payments to OHT OHT was in financial difficulties so bank directed KTI to pay progress payments

directly to OHT

Law 316: Secured Transactions G. Morgan (Waldron, Fall 2012) | Page 20

Bank goes to realise on debt KTI items are in OHT’s possession KTI claims ownership of items

Issue: does the bank have a perfected security interest in the items? did the bank’s security interest attach to the items sent by KTI? did OHT have sufficient rights in the items from KTI to allow the bank’s security interest to attach?

Decision: OHT had some rights to the property mere possession, however, is insufficient (i.e. borrowing grandma’s car)

need sufficient rights in the item for attachment in this case, OHT had more than a possessory right right to hold and use in manufacturing process = sufficient for attachment however, KTI was making partial payments to sale of the completed economizers accordingly, ordinary course of business sale, which the bank accepted as it took

the $ from KTI

Waldron: unsatisfactory solution although fair result(hard to see OCB sale for items that had not been installed into the completed units)

Alternative solution: in addition to attachment, there are other factors that must be considered in

determining who gets the other considerations: (1) rules provided by the Act; and (2) PPSA s. 68 in default,

the common law and the law of merchant applies

Example for (1) rules provided by the Act:

T1: A borrows from Bank 1 and gives Bank 1 a security interest in all present and after acquired property. Bank 1 registers a financing statement.T2: A borrows from Bank 2 and gives Bank 2 a security interest in all present and after acquired property. Bank 2 does not register a financing statement.

In this example, both banks have an attached security interests. However, this does not tell us who gets the assets. We have to turn to the Act and the priority rules to see that Bank 1, with its perfected security interest, has priority over Bank 2.

Accordingly, attachment is not determinative of which creditor gets the property.

Application to KTI: what is the nature of KTI’s interests in the goods? no security interest; not

transfer of account or chattel paper; not a lease of > 1 year; not a commercial consignment

given KTI’s interest (which is not that of a secured prarty), what part of the PPSA sorts out priority? no part of the PPSA governs

therefore consider the common law KTI has title (ownership) in the goods nothing in the common law gives the bank a right to items owned by KTI b/c it has a

security interest w/ OHTHaibeck v. No. 40 Taurus Ventures Ltd. (BCSC 1991)

Pre-PPSA security properly registered under the previous law was treated as perfected in the PPSA during the transition period if it came into competition with a PPSA perfected security interest, the PPSA governed

Facts: debenture (security interest) issued to RoyNat by No 40 and registered (i.e.

completed legal formalities under pre-PPSA law perfected security interest when PPSA came into effect)

Law 316: Secured Transactions G. Morgan (Waldron, Fall 2012) | Page 21

Builders sold appliances to No. 40 on a condition sales contract Builders perfects security interest in appliances No. 40 defaults on CSC

Issue: RoyNat had security interest Builders had security interest Is there a rule in the act that covers this conflict? yes priority between competing

perfected security interests = registration date

Decision: RoyNat’s security interest was perfected before Builders accordingly it has priority in realization (i.e. gets to take its security interest out of No. 40 and any leftover would go to Builders)

Unfair? No, Builders could have obtained priority if it had registered quicker (rule within the Act that would have given priority provided registration was completed).

Purchase Money Security InterestsTopic Notes Key ConceptsDefinition (a) a security interest taken in collateral, other than investment property, to the extent

that it secures payment of all or part of its purchase price, vendor financing (security interest = likely the car)

(b) a security interest taken in collateral, other than investment property, by a person who gives value for the purpose of enabling the debtor to acquire rights in the collateral, to the extent that the value is applied to acquire the rights, third party financing (security interest = likely the car = PMSI)

(c) the interest of a lessor of goods under a lease for a term of more than one year, and long term lease equivalent to vendor financing

(d) the interest of a person who delivers goods to another person under a commercial consignment consignment equivalent to vendor financingbut does not include a transaction of sale by and lease back to the seller and, for the purposes of this definition, "purchase price" and "value" include credit charges or interest payable for the purchase or loan credit;

Example A takes out an $80,000 loan from the bank to purchase a computer system. The bank takes a security interest in the computer system.

However, A finds a cheaper version of the computer system for $60,000. A then uses the excess $20,000 on a cruise.

What happens to the PMSI? PMSI in computer system to $60,000 qualification in (b) of “to the extent that the value is applied to acquire the rights”

Modified example:

A takes out an $80,000 loan from the bank to purchase a computer system. The bank takes a security interest in the computer system and all present and after acquired property. A finds a cheaper version of the computer system for $60,000. A then uses the excess $20,000 on a cruise.

security interest in the computer system and all business property to $80,000 PMSI in the computer system to $60,000

Priority rules for PMSIs

PPSA s. 34(1) subject to s. 28, a PMSI in (a) collateral or its proceeds that is perfected not later than 15 days after the day the debtor obtains possession of the collateral, or (b) an intangible or its proceeds that is perfected not later than 15 days after the day the security interest in the intangible attaches, has priority over any other security interest in the same collateral given by the same debtor hence the problem in Haibeck

Law 316: Secured Transactions G. Morgan (Waldron, Fall 2012) | Page 22

Policy consideration: allows businesses to expand business base on security (as otherwise creditors would not extend financing)

Major exception to 34(1) inventory (items purchased to re-sell)

PPSA s. 34(2) = inventory provision PMSI in inventory or its proceeds has priority if

a) the PMSI is perfected at the time of possession (i.e. financing statement registered)b) the secured party gives notice to any other secured party that has before the time

registered a financing statement that includes the same type of collaterald) formal requirements for noticee) notice is given before possession

Example:

T1 = credit union has perfected security interest in all present and after acquired propertyT2 = inventory supplier provides inventory with a security interest in all inventory and proceeds (PMSI)

Did the inventory supplier meet the requirements in PPSA s. 34(2)? registration notice

Policy consideration: up to creditors to protect their interests in the PPSA

n.b. a reason why perfection is not always sufficient (i.e. can be subordinate to a PMSI)Impact on existing creditors

Generally, it is to the advantage of existing creditors for the debtor to be able to give PMSIs allows debtor expand asset base, build business

However, in some cases, the creditor has restricted the debtor’s ability to seek other credit (typically in situations with higher asset to debt ratios).

PMSI Priority PPSA s. 22 priority for a PMSI that is perfected no later than 15 days after the debtor obtains possession of a collateral / an intangible attaches

T1 bank loans debtor $ to purchase boiler, debtor takes possession of boilerT2 debtor defaults and trustee in bankruptcy is appointedT3 bank registers financing statement

If the bank is not providing a PMSI, the trustee in bankruptcy will get the boiler per PPSA .s. 20. However, if it is a PMSI, the bank has priority provided there is no more than 15 days between T1 and T3 per PPSA s. 21.

* most grace periods in the PPSA are 15 daysAgricultural Credit Corp. of Sask. v. Pettyjohn (SKCA 1991)

Facts: see earlier discussion in Proceeds

Did ACCS give value to the Pettyjohns to purchase the cows? YesMore difficult question: was the value used to acquire the cows? Pettyjohns argued that the funds were not used to buy the cows (rather, the funds were used to pay off the interim lender who financed the purchase of the cows.)

Court: commercially unreasonable to divide the transaction so minutely value from ACCS was used to pay off interim financing, but the interim financing was always based on the Pettyjohns’ acquiring financing accordingly, all part of the same transactional scheme

Unisource Canada Inc. v.

Facts:T1 = bank loans debtor $ for purchase of a printing press and registers a financing statement

Law 316: Secured Transactions G. Morgan (Waldron, Fall 2012) | Page 23

Laurentian Bank (ONCA 2000)

but not a PMSI (why? transaction was a sale and lease back arrangement)T2 = debtor gives GSA to Unisource who registers a financing statementT3: debtor reorganizes finances, Laurentian loans money to debtor and debtor uses $ to pay off loan from bank. Laurentian registers a financing statement for the security interest in the printing press.*T4: debtor defaults

* mistake on the part of Laurentian should have taken an assignment of the bank’s security interest to maintain the bank’s priority

However, Laurentian had to argue that there was a PMSI in the printing press. As bank had the title (given the sale and lease back), discharging the debt met that the debtor now acquired title in the printing press and then provided a security interest to Laurentian

Waldron: technical argument as the debtor’s position didn’t really change (i.e. just swapped one creditor for another)

Prof. Cumming correct solution but not as a PMSI (rather, when the bank’s financing was paid off, Laurentian was subrogated to the position of the bank)

Inventory financing

Pre-PPSA: (1) floating charge that hovered over inventory until event of default when default occurred, the charge crystallized over the inventory at the time; or (2) specific charge on each item of inventory (most useful with big-ticket items like cars)

Post-PPSA: security interest in all inventory (PMSI entitled to super priority under s. 34(2))Chrysler Credit Canada v. Royal Bank of Canada (SKCA 1986)

Facts: financing arrangement was set up pre-PPSA and therefore continued to structure financing in the old way post-PPSA the structure was not consistent with the principles of the PPSA.

T1: dealer acquires car and gives chattel mortgage to CCCT2: dealer sells car and repays CCCRepeat giving specific charges to CCC as a separate transaction to be discharged when the car was sold

When the debtor defaults, CCC gets the new cars with registered chattel mortgages. With respect to used cars, CCC argues that they are proceeds of the sold cars. Receiver

Three groups(1) trade-ins on the sale of new cars where the loans to CCC had not been repaid

CCC had a S/I in the sold car (cut-off in OCB sale) but S/I in trade-in car that retains the PMSI priority

(2) 31 used cars traceable to the sale of new cars where the loans had been repaid(3) nine used cars of unknown origin CCC not entitled to PMSI priority as unable to

demonstrate that they are proceeds

Problem: group (2)

Security agreement provided expressly that the security interest secured any and all present and future obligations (including proceeds), and indebtedness that is from time to time reduced and thereafter increased or entirely extinguished and thereafter re-incurred (CB 122) indicated that CCC intended to have a security interest even after the loan was repaid

Waldron: conclusion based on private contract (not PPSA) further problem: not a PMSI as once the debt is discharged there is no value that secures payment

T1: loan of $25,000 to purchase boiler perfected PMSIT2: loan of $50,000 to purchase backhoe perfected PMSIT3: debtor starts making loan payments

Law 316: Secured Transactions G. Morgan (Waldron, Fall 2012) | Page 24

The creditor may structure repayments to all pro rata across the collateral (i.e. each payment in the above scenario applied in a 1:2 ratio) ensures that the creditor retains a PMSI in both for the duration of the loan period

Perfection by RegistrationTopic Notes Key ConceptsRegistration of financing statement

PPSA s. 43 register with office of the registry (online submission), registration effective from time assigned (typically based on registration #), must pay fees, may be registered before attachment,

PPSA s. 18 gives right to a debtor, creditor, sheriff, person interested in the personal property of the debtor or an authorized individual of the above to make a request to the creditor to provide information including a copy of any security agreement, statement in writing of the amount of the indebtedness and terms of payment, a written approval or correction of an itemized list of personal property, written approval or correction of the amount of indebtedness and the terms of payment, and sufficient information as to the location of the security agreement to enable a person entitled to receive a copy to inspect it at that location however, excludes potential creditors (work around: have the debtor authorize the potential creditor to obtain it as a condition of the credit arrangement)

Error in Financing Statement

PPSA s. 43(6) defect does not affect validity unless “seriously misleading”(8) no requirement to prove, however, that someone was misled protection for the trustee in bankruptcy, judgement creditor, bona fide purchaser for value, etc.

Requirements for registration

PPSA Regulations Part 2 Division 1 (4) what type of registration length of registration (1-25 years or infinity) secured party’s name and mailing address name of each debtor must register second name if there is one description of collateral

PPSA Regulations Part 2 Division 1 (10)Serial number goods Schedule 2 must be described by serial number or in accordance with (11) however, non-registration by serial number for equipment leaves the collateral vulnerable in certain situations

PPSA Regulations Part 2 Division 1 (11)Non-serial number goods must describe collateral by item or kind OR statement of APAAP OR statement of APAAP exception certain specifies items or kinds OR inventory similar to requirements for security agreements in PPSA s. 10 (but not identical)

Seriously Misleading “Seriously misleading”