Opportunity Day

FY2017 Result

WHA Corporation PCL

Your Ultimate Solution Partner

Disclaimers WHA Group

The information contained in this presentation is for information purposes only and does not constitute an offer or invitation to sell or the solicitation of an offer or invitation to purchase or subscribe for share in WHA Corporation Public Company Limited (“WHA” and shares in WHA, “shares”) in any jurisdiction nor should it or any part of it form the basis of, or be relied upon in any connection with, any contract or commitment whatsoever. In addition, this presentation contains projections and forward-looking statements that reflect the Company's current views with respect to future events and financial performance. These views are based on a number of estimates and current assumptions which are subject to business, economic and competitive uncertainties and contingencies as well as various risks and these may change over time and in many cases are outside the control of the Company and its directors. You are cautioned not to place undue reliance on these forward looking statements, which are based on the current view of the management of the Company on future events. No assurance can be given that future events will occur, that projections will be achieved, or that the Company's assumptions are correct. The Company does not assume any responsibility to amend, modify or revise any forward-looking statements, on the basis of any subsequent developments, information or events, or otherwise. These statements can be recognized by the use of words such as “expects,” “plans,” “will,” “estimates,” “projects,” or words of similar meaning. Such forward-looking statements are not guarantees of future performance and actual results may differ from those forecast and projected or in the forward-looking statements as a result of various factors and assumptions.

2

Agenda

II. Summary of Operating Performance - 2017

IV. Financial Performance - 2017

Appendix

3

I. WHA Group Overview

III. Business and Financing Plan - 2018

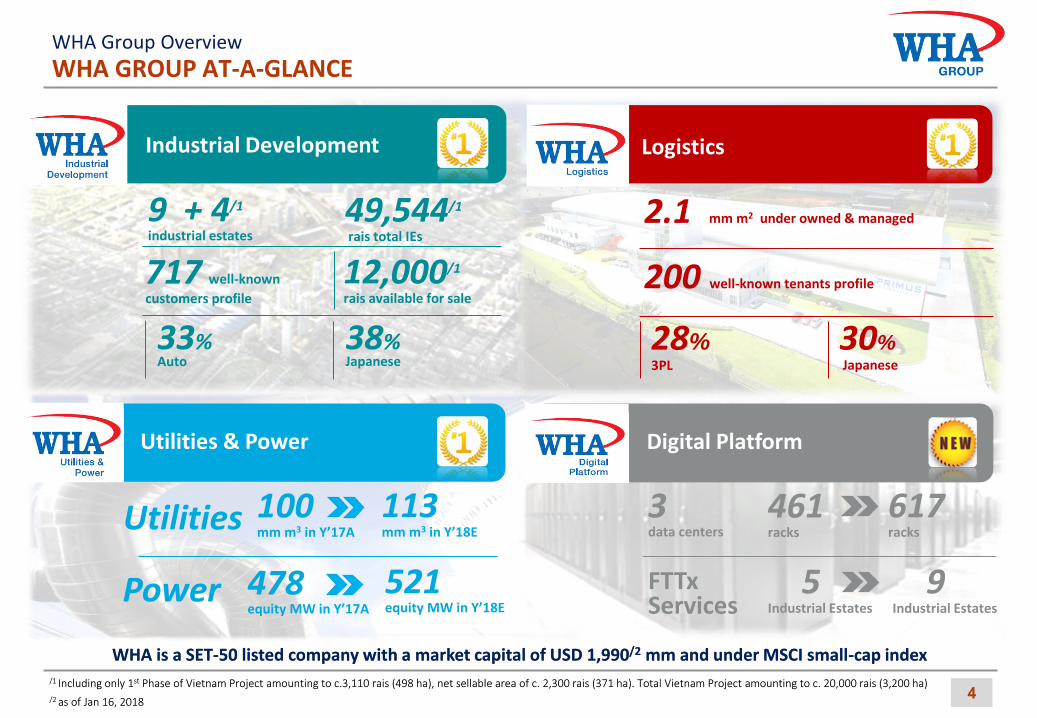

WHA GROUP AT-A-GLANCE WHA Group Overview

/1 Including only 1st Phase of Vietnam Project amounting to c.3,110 rais (498 ha), net sellable area of c. 2,300 rais (371 ha). Total Vietnam Project amounting to c. 20,000 rais (3,200 ha)

/2 as of Jan 16, 2018

WHA is a SET-50 listed company with a market capital of USD 1,990/2 mm and under MSCI small-cap index

4

2.1 mm m2 under owned & managed

200 well‐known tenants profile

28% 3PL

30% Japanese

Logistics

9 + 4/1 industrial estates

717 well‐known

customers profile

33% Auto

38% Japanese

12,000/1

rais available for sale

49,544/1

rais total IEs

Industrial Development

100 mm m3 in Y’17A

478 equity MW in Y’17A

113 mm m3 in Y’18E

521 equity MW in Y’18E

Utilities & Power

3 data centers

FTTx Services

Digital Platform

Utilities

Power

Remark: /1The Utilities & Power business’s operating matrix under WHA level may differ from one shown in WHAUP level as a result of Pre-IPO restructuring, resulting in partial recognition in FY2016 under WHAUP.

461 racks

617 racks

5 Industrial Estates

9 Industrial Estates

5

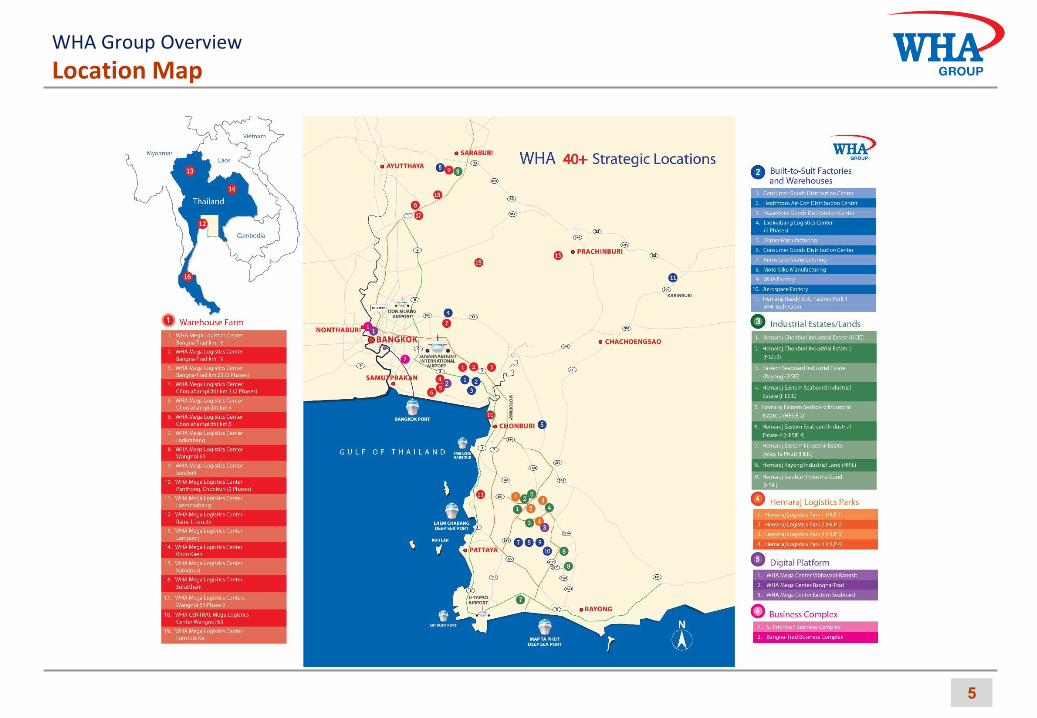

Location Map WHA Group Overview

Group Structure – Operating Companies WHA Group Overview

Warehouse

Asia Alliance Registered and

Paid-up

Capital – THB 310

mm

WHA

Alliance Registered and

Paid-up

Capital – THB 260

mm

WHA KPN Alliance

Central WHA

Alliance

PT WHA

International

Indonesia/1

Registered and Paid-up

Capital – US 2.0

mm

WHART

NAV per unit –THB 9.80/1

Paid-Up Capital–THB 18,237.7 mm/2

Total Asset–THB 27,479 mm/7

WHABT

NAV per unit –THB 10.07/1

Paid-Up Capital–THB 1,966.7 mm/4

Total Asset–THB 2,581.7 mm/1

99.9% 99.9% 99.9% 99.9%

15.00%

15.00%

Remarks: /1 NAV per unit as of Jan 9, 2018 /2 Information as of Jan 9, 2018 /3 Held by Hemaraj Land and Development PCL.

WHA Daiwa

Logistics Property

WHA Infonite

Registered – THB 185 mm

Paid-up – THB 185 mm/2

Hemaraj Land and

Development PCL.

Registered – THB 6,000 mm

paid-up Cap – THB 3,882 mm

98.54%

94.97%

Core Business

WHA Corporation PCL

Registered – THB 1,567.8 mm

paid-up Cap – THB 1,432.6 mm

WHAUP/3

Registered – THB 3,825 mm

paid-up Cap – THB 3,825 mm

70.00%/4

Property Funds and REITs

HPF/3

NAV per unit –THB 9.811

Paid-Up Capital–THB 4,629.5 mm/6

Total Asset–THB 4,693.5 mm/2

22.95%

HREIT/3

NAV per unit – THB 8.69/1

Paid-Up Capital–THB 6,693.8 mm/5

Total Asset–THB 9,064.3 mm/8

15.00%

JV Collaborations

Gheco-One

Glow IPP

Houy Ho Power

GJP NLL

Gulf Solar

WHA Gunkul

BPWHA1

JV Collaborations – Utilities & Power/3

65.00% 50.00%

51.00%

35.00%

5.00%

12.75%

25.01%

25.01%

75.00%

25.01%

Chonburi

Clean Energy

33.33%

WHA Hemaraj Nghe An

JSC/3

99.00%

/4 Including the 8th capital reduction

/5 Including the 1st capital increase

/6 Including the 1st capital reduction

6

Total Fund Raised c. THB 39,138 mm

Gulf VTP Gulf TS1-4 Gulf WHA MT

25.01% 25.01% 51.00%

/7 Interpolate conversion of WHAPF and new fund raising

/8 Interpolate new fund raising

7

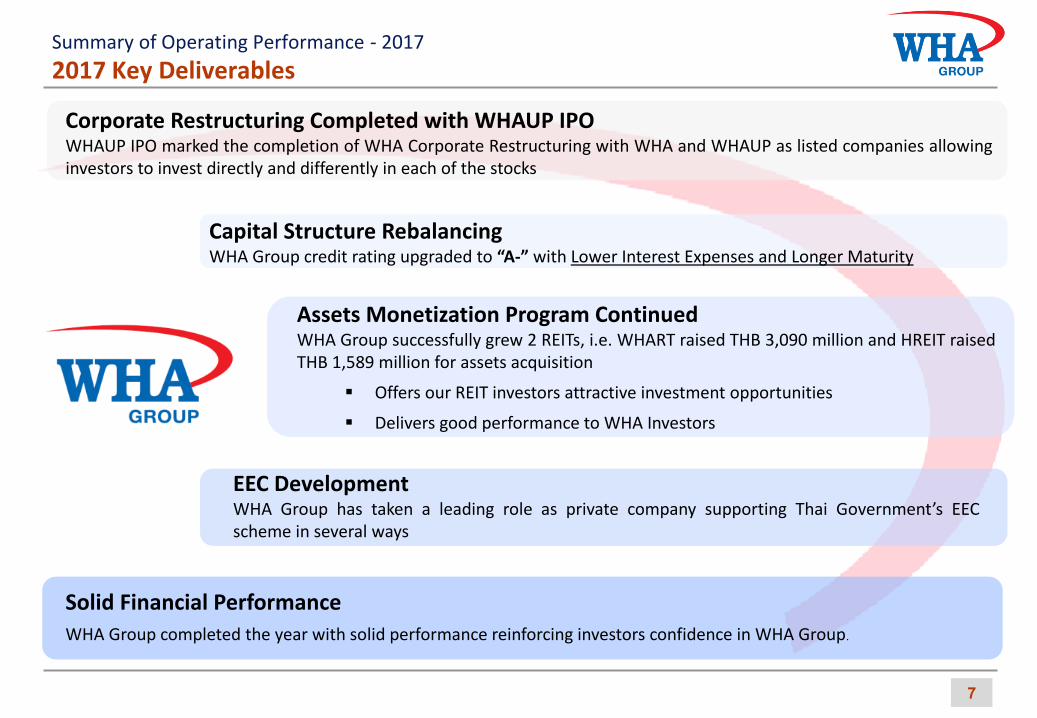

2017 Key Deliverables Summary of Operating Performance - 2017

Corporate Restructuring Completed with WHAUP IPO WHAUP IPO marked the completion of WHA Corporate Restructuring with WHA and WHAUP as listed companies allowing investors to invest directly and differently in each of the stocks

Capital Structure Rebalancing WHA Group credit rating upgraded to “A-” with Lower Interest Expenses and Longer Maturity

Assets Monetization Program Continued WHA Group successfully grew 2 REITs, i.e. WHART raised THB 3,090 million and HREIT raised THB 1,589 million for assets acquisition

Offers our REIT investors attractive investment opportunities

Delivers good performance to WHA Investors

EEC Development WHA Group has taken a leading role as private company supporting Thai Government’s EEC scheme in several ways

Solid Financial Performance

WHA Group completed the year with solid performance reinforcing investors confidence in WHA Group.

8

2017 Key Achievements

K E Y A C H I E V E M E N T S

POWER CAPACITY INCREASED TO

478 Equity MW

3 DATA CENTERS COMMENCED OPERATION

(461 RACKS) 161,588 SECURED PRE-LEASED AREAS

sqm

2.1 MILLION sqm

UNDER OWNERSHIP &

MANAGEMENT

5 COMMENCED OPERATION

FTTx in

20 THB BILLIONS MARKET CAPITAL

SUCCESSFULLY LISTED

3,110 IRC APPROVED

FOR NGHE AN

PROJECT (VIETNAM)

RAI

HESIE4

SPECIAL PROMOTION ZONE

EEC 100

MILLION M3 OF

UTILITIES AND SALES MANAGEMENT VOLUME

L O G I S T I C S I N D U S T R I A L D E V E L O P M E N T

U T I L I T I E S & P O W E R

D I G I T A L P L A T F O R M

START PROVIDING

MANAGED SERVICES

75% 1,000 RAI LAND SALES

INCLUDING CONTINENTAL

MARKET SHARE

WHART

SUCCESSFULLY

CONVERTED WHAPF

INTO

2017 Industrial Estate

Summary of Operating Performance - 2017

Revenue from Sales of Industrial Estate (Industrial Development Business)

THB 3,211 mm 32% • Mainly from higher the number of land transferred in 2017 compared to 2016

Revenue from Sale of Investment Properties (Logistics Properties Business)

THB 3,079 mm 74%

• Mainly from large asset monetization to WHART and HREIT in 2016 which was 420,455 sq.m. compared with those in 2017 which was 85,867 sq.m.

Rental, Service Revenue and Other Incomes (Logistics Properties Business)

THB 1,148 mm 31% • Mainly from large asset monetization to HREIT and WHART in 2016.

Revenue from Sales and Service (Utilities Business)

THB 2,075 mm 4% • If excluding the one-time excessive charge, utilities income grew c. 8% due to completion of COD of 5 SPPs since 4Q’2016

Share of Profit from Joint Ventures THB 1,963 mm 95% • Mainly due to additional 5 SPPs which commenced its operation from Nov 16 onwards resulting in 478 Equity MW as of 2017.

Interest Expenses THB 1,617 mm 34% • Substantially decrease in interest expense from 1. Hemaraj acquisition loan repayment of THB 20,955 mm during

2016 2. Loan and Bond repayment of THB 8,300 mm during 2017 3. Loan refinancing by bond issuance of THB 4,000 mm under

WHAUP having lower cost of fund from 4.20% to 3.33% in Sep 17

Net Profit Attribute to Owners of the Parents

THB 3,266 mm

13% • Good performance year due to 1. Higher share of profit from strong performance of power

business. 2. Higher profitability from industrial estates business. 3. Higher profitability from asset monetization to WHART 4. Lower interest expense.

Financial Highlights 2017 Financial Performance

Remark: Power & Utility Businesses were full year performance comparing to WHAUP, which was partial consolidation 9

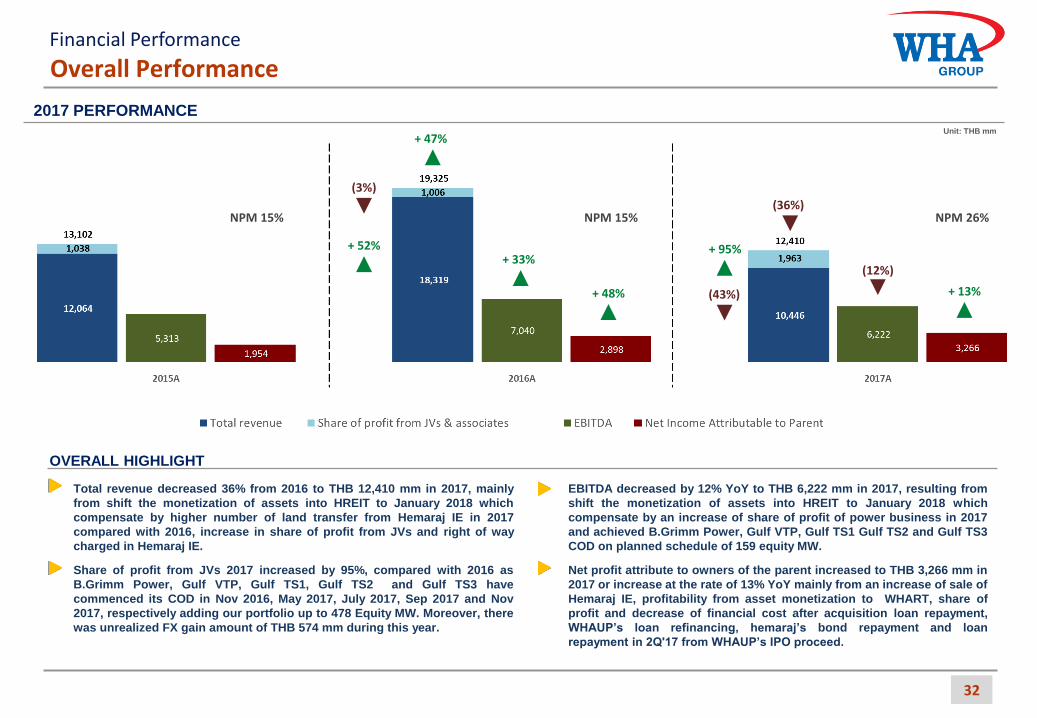

Total Revenue and Share of Profit : THB 12,410 mm 36% YoY

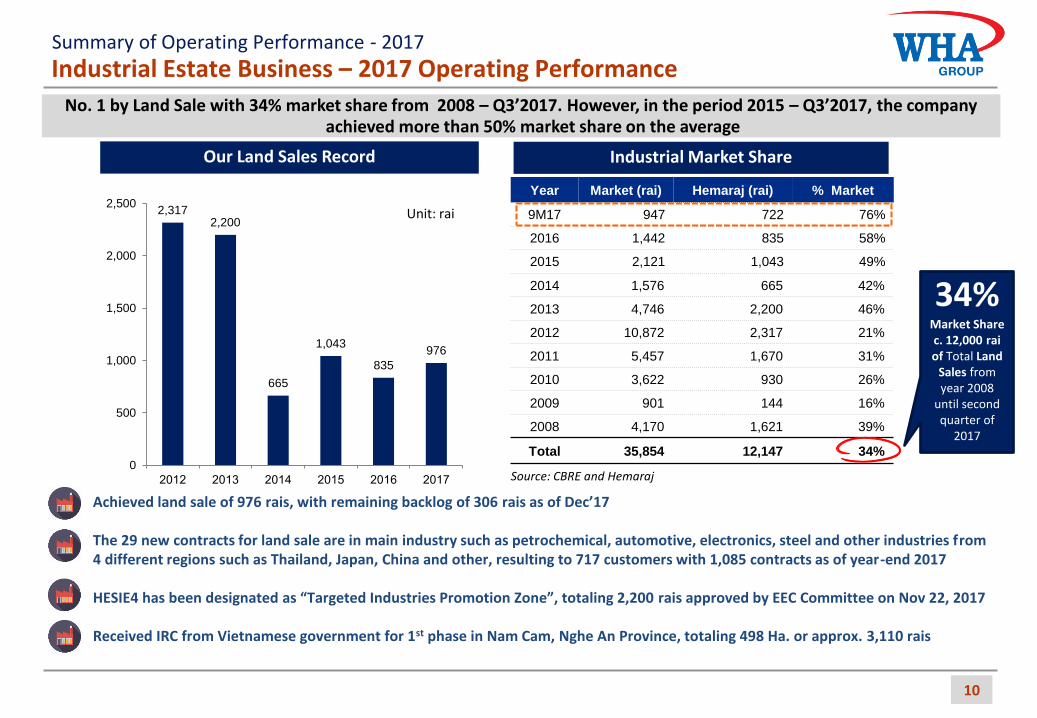

Year Market (rai) Hemaraj (rai) % Market

9M17 947 722 76%

2016 1,442 835 58%

2015 2,121 1,043 49%

2014 1,576 665 42%

2013 4,746 2,200 46%

2012 10,872 2,317 21%

2011 5,457 1,670 31%

2010 3,622 930 26%

2009 901 144 16%

2008 4,170 1,621 39%

Total 35,854 12,147 34%

10

Industrial Estate Business – 2017 Operating Performance No. 1 by Land Sale with 34% market share from 2008 – Q3’2017. However, in the period 2015 – Q3’2017, the company

achieved more than 50% market share on the average

Source: CBRE and Hemaraj

Our Land Sales Record

Unit: rai

Industrial Market Share

34% Market Share c. 12,000 rai of Total Land

Sales from year 2008

until second quarter of

2017

Achieved land sale of 976 rais, with remaining backlog of 306 rais as of Dec’17 The 29 new contracts for land sale are in main industry such as petrochemical, automotive, electronics, steel and other industries from

4 different regions such as Thailand, Japan, China and other, resulting to 717 customers with 1,085 contracts as of year-end 2017

HESIE4 has been designated as “Targeted Industries Promotion Zone”, totaling 2,200 rais approved by EEC Committee on Nov 22, 2017

Received IRC from Vietnamese government for 1st phase in Nam Cam, Nghe An Province, totaling 498 Ha. or approx. 3,110 rais

2,317 2,200

665

1,043

835

976

0

500

1,000

1,500

2,000

2,500

2012 2013 2014 2015 2016 2017

Summary of Operating Performance - 2017

Japan 38%

Thailand 19%

Europe 11%

USA 9%

Australia 5%

Taiwan 3%

India 2%

China 3%

Korea 2%

Others 8%

11

Industrial Estate Business – Customer Profile

Customer by Industry

Customer by Nationality

Our Customers and Contracts

2012

717 Customers

Q4’17

832 Contracts

2012

1,085 Contracts

Q4’17

555 Customers

9 Operating

Industrial Estates

4

New Industrial Estates

Auto 33%

Consumer 13%

Petrochemical 9%

Steel/Metal 9%

Electronics 8%

Building Material

7%

Logistics 5%

Others 16%

Summary of Operating Performance - 2017

Logistics & Industrial Properties Business – 2017 Operating Performance • Built-to-Suit distribution center and warehouse in prime location to help

customers optimize long-term logistics cost

• Built-to-Suit factory with cross referral of customers from HEMRAJ esp. those in high value sectors e.g. automotive

• Sophisticated Built-to-Suit product e.g. cold storage, multi-temp DC, and E-Commerce DC

• Ready-Built factory and warehouse in IEs and logistic parks

• Geographical expansion e.g. Indonesia and Vietnam

Group-Owned assets and preleased Asset Under Management

12

Area owned by Hemaraj and its subsidiaries

Area sold to HPF and HREIT

Industrial Properties

Area owned by WHA and its subsidiaries

Area sold to WHART and WHABT

Logistics Properties

701,677

235,115

466,562

701,677

1,449,163

1,006,362

442,802

1,449,163

Location • Bangna-Trad

km 18-23 • Ladkrabang • Rama II • Laem Chabang • Lum Luk Ka • Wangnoi

Location • Chonburi • Rayong • Saraburi • Prachin Buri

Area: 2,144 rais Area: 979 rais

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

88,913 141,619 141,619 169,433

891,286

298,139 192,341

505,051

1,108,740

Total 2,150,840

1,975,792 2,115,723

Unit : sq.m.

CAGR 33.59% (2006A – 2017A)

CAGR 33.28% (2012A – 2017A)

Remark: Figures as of 4 Jan 2018

Summary of Operating Performance - 2017

29%

27% 20%

15%

8%

1% Thai

Japan

Europe

Asia(Exclu.Japan, Thai)USA

Other

29%

40%

25%

6% 3PL

FMCG&Healthcare

Manufacturer

Other

38%

27%

9%

9%

13%

2% 2% Japan

Europe

Asia(Exclu.Japan, China)USA

Australia

China

39%

19% 10%

12%

5% 15%

Auto&Parts

Logistic

Electronic

Consumer

IndustrialServiceOther

Industrial Properties Business Logistics Properties Business

Customer by Nationality Customer by Industry

Industrial Properties Business Logistics Properties Business

386,234

179,582 203,028

105,986 109,565

35,595 52,023

-

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

450,000

2013 2014 2015 2016 2017

RBF/RBW BTS/Warehouse farm

Logistics & Industrial Properties Business - Performance

13

Unit: Sq.m.

141,581

Pre-Leased / New Contracts

161,588

Remark: Pre-leased/New contracts performance based on gross basis

WHA has secured pre-leased area/new contracts for Built-to-Suit, warehouse farm and RBF/RBW totals 161,588 sq.m.

- 109,565 sq.m. for Built-to-Suit and warehouse farm which mostly located in Bangna-Trad zone

- 52,023 sq.m. for RBF and RBW

Asset monetization to WHART of 84,967 sq.m. in tandem with WHAPF conversion to WHART on Nov 29, 2017

Asset monetization to HREIT of 55,131 sq.m. on Jan 4, 2018

Summary of Operating Performance - 2017

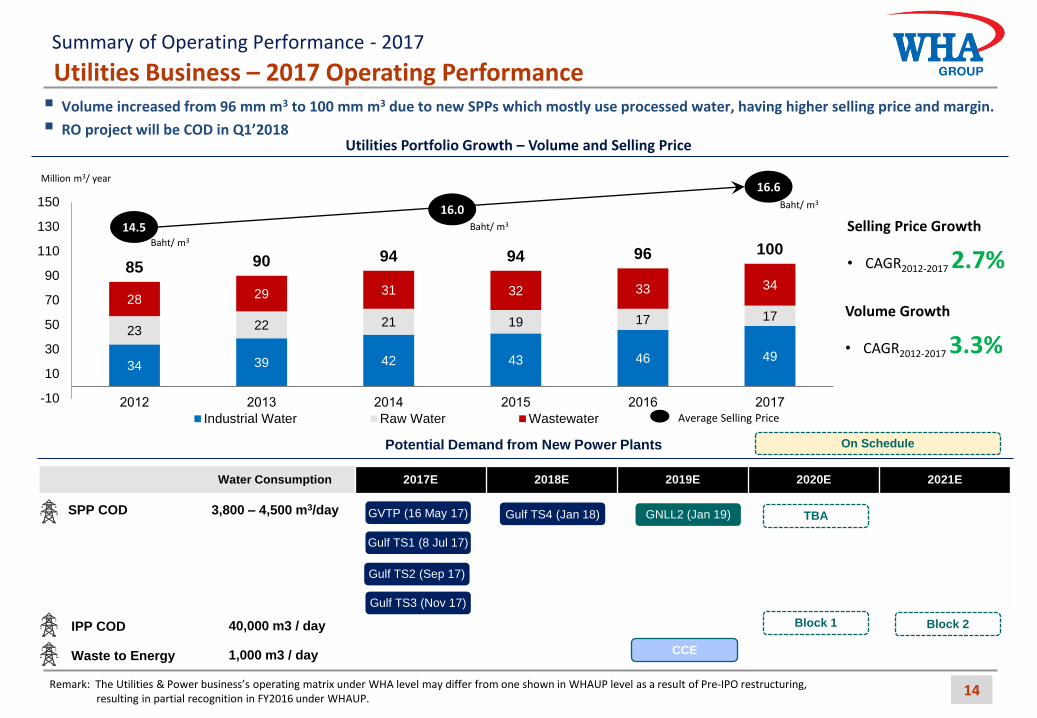

34 39 42 43 46 49

23 22 21 19 17 17

28 29 31 32 33 34

85 90 94 94 96 100

-10

10

30

50

70

90

110

130

150

2012 2013 2014 2015 2016 2017

Industrial Water Raw Water Wastewater

Volume increased from 96 mm m3 to 100 mm m3 due to new SPPs which mostly use processed water, having higher selling price and margin.

RO project will be COD in Q1’2018

Utilities Business – 2017 Operating Performance

14

Utilities Portfolio Growth – Volume and Selling Price

Million m3/ year

14.5

16.6

16.0

Average Selling Price

Baht/ m3

Baht/ m3

Baht/ m3

Selling Price Growth

• CAGR2012-2017 2.7%

Volume Growth

• CAGR2012-2017 3.3%

Remark: The Utilities & Power business’s operating matrix under WHA level may differ from one shown in WHAUP level as a result of Pre-IPO restructuring, resulting in partial recognition in FY2016 under WHAUP.

Potential Demand from New Power Plants

Water Consumption 2017E 2018E 2019E 2020E 2021E

SPP COD 3,800 – 4,500 m3/day

GVTP (16 May 17)

Gulf TS1 (8 Jul 17)

Gulf TS2 (Sep 17)

Gulf TS3 (Nov 17)

Gulf TS4 (Jan 18) GNLL2 (Jan 19) TBA

Block 1 Block 2

On Schedule

CCE Waste to Energy 1,000 m3 / day

IPP COD 40,000 m3 / day

Summary of Operating Performance - 2017

Completion on COD of 4 SPPs, which increase Equity MW from 350 MW in 2016 to 478 MW in 2017

Commencement of construction on Natural Gas Distribution Projects in 2 IEs i.e. HESIE2 and HESIE4

Po

rtfo

lio A

nal

ysis

Power Business – Well-Balanced Portfolio with Strategic Location

15

Po

rtfo

lio A

nal

ysis

IPP 53%

SPP 47%

By Type of Power Plant By Type of Sourcing

Coal 43%

Gas 53%

Hydro 4%

By Type of Power Plant By Type of Sourcing

VSPP 100% Solar 60%

WTE 40%

Conventional

Power: 537.0

Equity MW

Secured

Alternative

Power: 5.8

Equity MW

Secured

Highly reliable off-taker (EGAT)

Client Profile

Long-maturity Portfolio

Po

rtfo

lio S

um

mar

y

Project Name Type JV Partner Location Contracted Capacities

(MW)

WHAUP

Portion Equity MW COD

Operating Phase

Gheco-I IPP Coal Glow Map Ta Phut IE 660.0 35.00% 231.0 Q3’12

Glow IPP IPP Gas Combined Cycle Glow HCIE 713.0 5.00% 35.7 Jan-03

Houay Ho Power IPP Hydro Glow Lao PDR 152.0 12.75% 19.4 Sep-99

GJP NLL SPP Gas Co-gen Gulf JP HRIL 122.5 25.01% 30.6 May-13

Gulf Solar VSPP Solar Gulf HLP1, HCIE, HESIE, ESIE 0.6 25.01% 0.2 Jun-14 – Jan-15

WHA Gunkul VSPP Solar Gunkul Bangna and Ayudthaya 3.3 74.99% 2.5 Apr – Jul-14

BGWHA-1 SPP Gas Co-gen B Grimm HCIE 121.0 25.01% 30.3 Nov-16

GVTP SPP Gas Co-gen Gulf MP ESIE 130.0 25.01% 32.5 May-17

GTS1 SPP Gas Co-gen Gulf MP ESIE 130.0 25.01% 32.5 Jul-17

GTS2 SPP Gas Co-gen Gulf MP ESIE 130.0 25.01% 32.5 Sep-17

GTS3 SPP Gas Co-gen Gulf MP HESIE 125.0 25.01% 31.3 Nov-17

GTS4 SPP Gas Co-gen Gulf MP HESIE 125.0 25.01% 31.3 Jan-18

WHA KM.3 Solar VSPP Solar - Samutprakan 0.9 100.0% 0.9 Feb-18

Total 2,413.3 510.5

Construction Phase

GNLL2 SPP Gas Co-gen Gulf MP HRIL 120.0 25.01% 30.0 Jan-19

CCE VSPP Waste-to-energy Glow& Suez HCIE 6.9 33.33% 2.3 2019

Total 126.9 32.3

EGAT/ PEA/ MEA, 92%

Industrial

Users, 8%

Maturity < 20 Years, 20%

Maturity ≥ 20 Years, 80%

Maturity ≥ 20

Years,

100%

Additional Incoming

Project in 2018-2019 2017

Summary of Operating Performance - 2017

Po

rtfo

lio A

nal

ysis

Digital Platform Business

16

4 Data Center & 2 Cloud Solutions

Establish 4 Data Centers and 2 Cloud Computing as a managed service (IaaS, PaaS, SaaS)

# Data Centers 3 1

# Cloud Solutions 2 -

Location Zone Vibhavadi Bangna-Trad Eastern Seaboard

Bangna-Trad

Shareholding 100% by WHA Join Ventures

Start operation May 2017

Local Loop in 6 Industrial Estates (FTTx)

Implementing Local Loop as a managed service in 6 IEs

# Local Loop 3 New IEs 3 Existing IEs

Rental/Leasing Equipment

Procuring, implementing, maintaining all IT equipment and facilities, i.e. hardware, software, accessories, linkage etc., and Rent/Lease the equipment out to our clients

System Integrators and Data Mining (Big Data)

Designing, training, implementing, bringing together IT component subsystem in providing a comprehensive IT solution for our clients

IT Outsourcing/Business Process Outsourcing (BPO)

A service provider to deliver IT-enabled business process, IT human resources, applications and infrastructure solutions to enhance our clients’ business outcomes.

Comprehensive IT solution provider leveraging on WHA Group Customers Base

3 Established Data Centers with 461 Racks in operation, covering Vibhavadi and Bangna- Trad area. Built and operated according to

“Best Practices” and in conformity with Tier III compliance

5 Industrial Estates Linkage Fiber Optic Internet (FTTx Service)

Initial Complimentary Services Offerings

IT Outsourcing Service

CRM (call center)

Rental/Leasing Equipment and Software Service

System Integrator Service

Well-known Customers Reference

3 data centers with 450 racks

3 FTTx Services

new Digital Platform

Business Collaboration with Reputable Partners

Summary of Operating Performance - 2017

Logistics Business

17

Business and Financing Plan - 2018

200,000 – 250,000 sq.m. Pre-Leased and New Contract Area

160,000 – 170,000 sq.m. Leasable Area Monetized to REITs Expected 50% of the new Pre-Leased/Contract will be from High-Value and Overseas Properties

Diversify the Rental Properties to E-Commerce and Automated Warehouse/Distribution Center Leverage on premium brand and track record of BTS concept

for high-value properties Strengthen our footprint in serving global E-Commerce

giants

Capitalize on Government Policy on High-Value Industry Clusters Reap the benefit of U-Tapao’s multi-purpose usage Expect more automation warehouse/distribution center

supported by tax benefit

Expand to ASEAN Countries including Indonesia, Vietnam and Myanmar Start 2nd phase Indonesia project More proactive in CLMV countries

Assets Monetization to REITs Monetize rental properties to WHART and HREIT as part of

prudent capital management

Initiatives Key Deliverables

Logistics Business - Market Outlook

18

Business and Financing Plan - 2018

Thailand E-Commerce Growing Market with Favorable Environment Digital outlook in 2017

Total Population

Internet Users Active Social Media Users

Mobile Subscription

Active Mobile Social Users

644.1 339.2 305.9 854.0 272.6

vs. Population 53% 47% 133% 42%

Since Jan 2016 +31% +31% +8% +36%

68.2 46.0 46.0 90.9 42.0

vs. Population 67% 67% 133% 62%

Since Jan 2016 +21% +21% +10% +24%

126.2 117.8 64.0 185.3 64.0

vs. Population 93% 51% 147% 51%

Since Jan 2016 +2.4% +20.8% +6.9% +20.8%

50.6 45.5 41.9 58.2 41.9

vs. Population 90% 83% 115% 83%

Since Jan 2016 +0.4% +9.2% +2.0% +9.2%

(Unit: million)

YOY

YOY

YOY

YOY

Southeast Asia

• Thailand e-commerce market is expected to grow exponentially in the next 7 years, in line with the regional e-commerce market growth, which has a CAGR of 32%.

• Continuous growth of mobile device users combined with

increased number of internet users will support the growth of e-commerce market as well as act as the leading indicator for the e-commerce market overall.

Logistics Business - Market Outlook

19

Business and Financing Plan - 2018

Air Cargo

MRO

EEC Initiative on MRO & Air Cargo implementation in U-Tapao airport

• The government will prioritize the development of U-Tapao airport as the cornerstone of the EEC. • Thai airways international has announced its intention to build the region’s finest aircraft maintenance, repair and overhaul facility at U-Tapao. • To improve connectivity by air with the opening of the U-Tapao airport’s second passenger terminal and runway, the U-Tapao airport’s passenger

capacity will increase from its current 800,000 people to 3 million, as well as to cope with the increase in air cargo transportation. • WHA is in collaboration with the government on the development of the MRO facility as well as air cargo located in the free trade zone,

combining the strength in order to create world-class facilities.

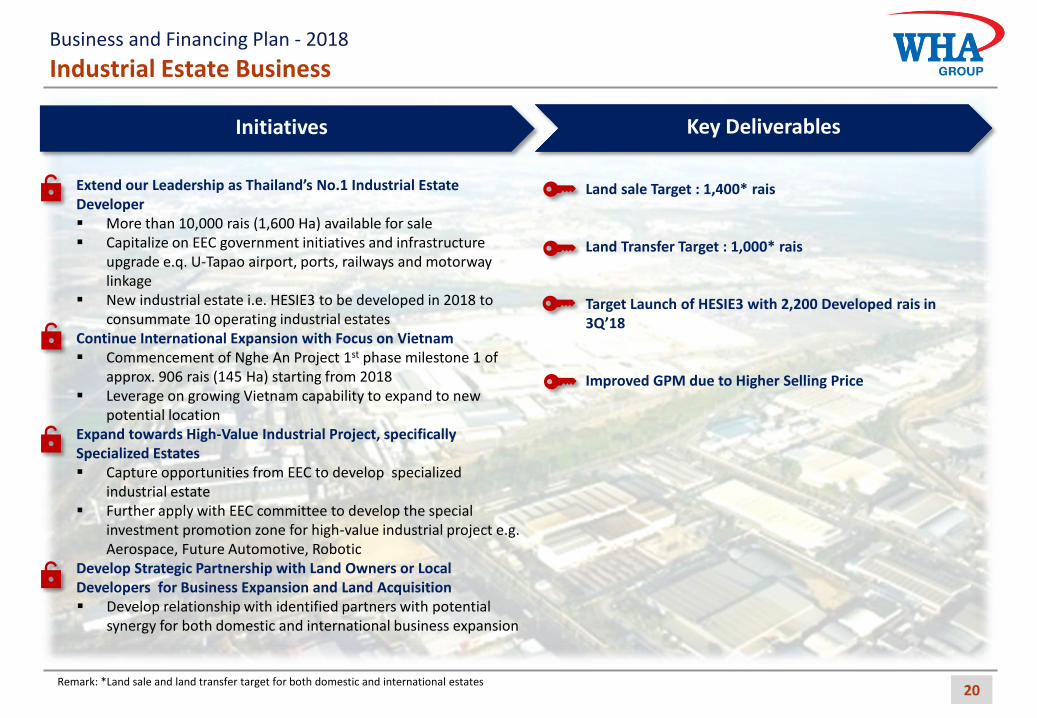

Industrial Estate Business

20

Business and Financing Plan - 2018

Land sale Target : 1,400* rais Land Transfer Target : 1,000* rais Target Launch of HESIE3 with 2,200 Developed rais in 3Q’18 Improved GPM due to Higher Selling Price

Extend our Leadership as Thailand’s No.1 Industrial Estate Developer More than 10,000 rais (1,600 Ha) available for sale Capitalize on EEC government initiatives and infrastructure

upgrade e.q. U-Tapao airport, ports, railways and motorway linkage

New industrial estate i.e. HESIE3 to be developed in 2018 to consummate 10 operating industrial estates

Continue International Expansion with Focus on Vietnam Commencement of Nghe An Project 1st phase milestone 1 of

approx. 906 rais (145 Ha) starting from 2018 Leverage on growing Vietnam capability to expand to new

potential location Expand towards High-Value Industrial Project, specifically Specialized Estates Capture opportunities from EEC to develop specialized

industrial estate Further apply with EEC committee to develop the special

investment promotion zone for high-value industrial project e.g. Aerospace, Future Automotive, Robotic

Develop Strategic Partnership with Land Owners or Local Developers for Business Expansion and Land Acquisition Develop relationship with identified partners with potential

synergy for both domestic and international business expansion

Initiatives Key Deliverables

Remark: *Land sale and land transfer target for both domestic and international estates

21

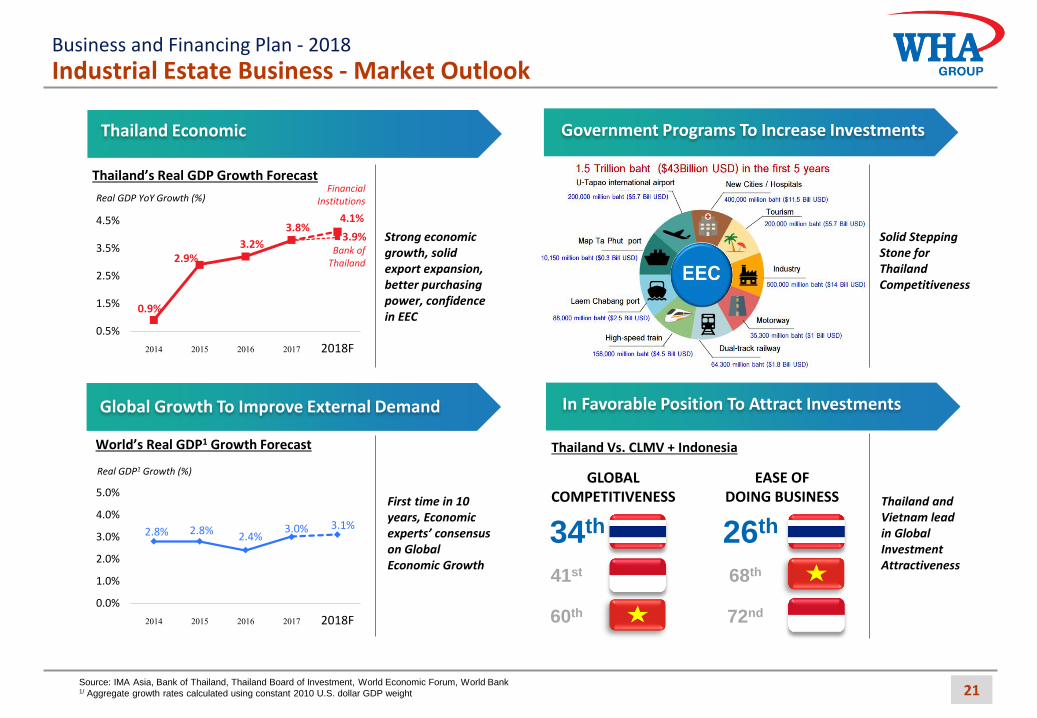

Industrial Estate Business - Market Outlook Business and Financing Plan - 2018

Source: IMA Asia, Bank of Thailand, Thailand Board of Investment, World Economic Forum, World Bank 1/ Aggregate growth rates calculated using constant 2010 U.S. dollar GDP weight

0.9%

2.9% 3.2%

3.8% 3.9%

4.1%

0.5%

1.5%

2.5%

3.5%

4.5%

2014 2015 2016 2017 2018F

Real GDP YoY Growth (%)

In Favorable Position To Attract Investments

2.8% 2.8% 2.4%

3.0% 3.1%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

2014 2015 2016 2017 2018F

Global Growth To Improve External Demand

Real GDP1 Growth (%)

World’s Real GDP1 Growth Forecast

Thailand’s Real GDP Growth Forecast

GLOBAL COMPETITIVENESS

EASE OF DOING BUSINESS

Thailand Vs. CLMV + Indonesia

34th

41st

60th

26th

68th

72nd

Thailand Economic Government Programs To Increase Investments

Strong economic growth, solid export expansion, better purchasing power, confidence in EEC

Thailand and Vietnam lead in Global Investment Attractiveness

Solid Stepping Stone for Thailand Competitiveness

Bank of Thailand

Financial Institutions

First time in 10 years, Economic experts’ consensus on Global Economic Growth

High Speed Train (BKK-Rayong)

Investment: USD 4,471 mm Chachoengsao

Bangkok

Chonburi

Rayong

Double Track Railway

(Map Ta Phut Port)

Investment: USD 1,822

mm

U-Tapao International Airport

Capacity: 3 Million Passenger /

Year

Motorway (Map Ta Phut)

Investment: USD 580 mm

Map Ta Phut Industrial

Port Expansion

Investment: USD 290 mm

Laem Chabang Sea Port Expansion

Investment: USD 1,000 mm

22

Industrial Estate Business - Market Outlook Business and Financing Plan - 2018

“EEC, the First Area-based Development, to Transform the Country into an Innovation-driven Economy, a New Economic Model of Thailand 4.0”

Source: Thailand’s Eastern Seaboard by BOI, Opportunity Thailand Innovation-Driven Economy by BOI, Logistic2day

STRATEGIC LOCATION INFRASTRUCTURE LINKAGE EXCELLENT ATMOSPHERE

Infrastructure Development 10 Targeted Industries Development 1 2 Moving Toward New Technology with Industry Inclusive

U-Tapao International Airport

Laem Chabang Deep Sea Port

Map Ta Phut Phase 3 Port

Double-Track Railway

BKK-Rayong High-Speed Rail Link

1

2

Pattaya-Map Ta Phut Motorway 3

4

5

Sattahip Commercial Port

6

7

EECi Innovation Hub 8

EECd Digital Hub 9

City Development 3 CHACHOENGSAO

CHON BURI

SRI RACHA-LAEM CHABANG

New Bangkok Urban

Educational and Human Resource Development center

Incentive Enhancement 4 Investment Facilitation 5

PATTAYA-SATTAHIP

U-TAPAO

RAYONG

Center of Work-Life Harmony

World-famous Tourist Destination

Home of Future ASEAN’s Aviation & Marine Service Center

Home of Petrochemicals and Energy Industries

• Exemption from corporate income tax for up to 15 Years

• 17% personal income tax rate for management, investor, experts

• Exemption of import duties on machinery/raw materials

• Matching Grants for Investment/ R&D/ Innovation for Targeted Industries

• Permission to own land for BOI promoted projects

• Rights to state’s land lease for 50 + 49 years

• Five-year work visa issuance to attract investors, experts and scientists from around the world

• One-stop service centre to facilitate foreign investors and issue permits for trading, export and import all in one location

• EEC Fast-track designed to speed up launch of investment projects, will shorten the time frame to 8-10 months from the current average of 40 months

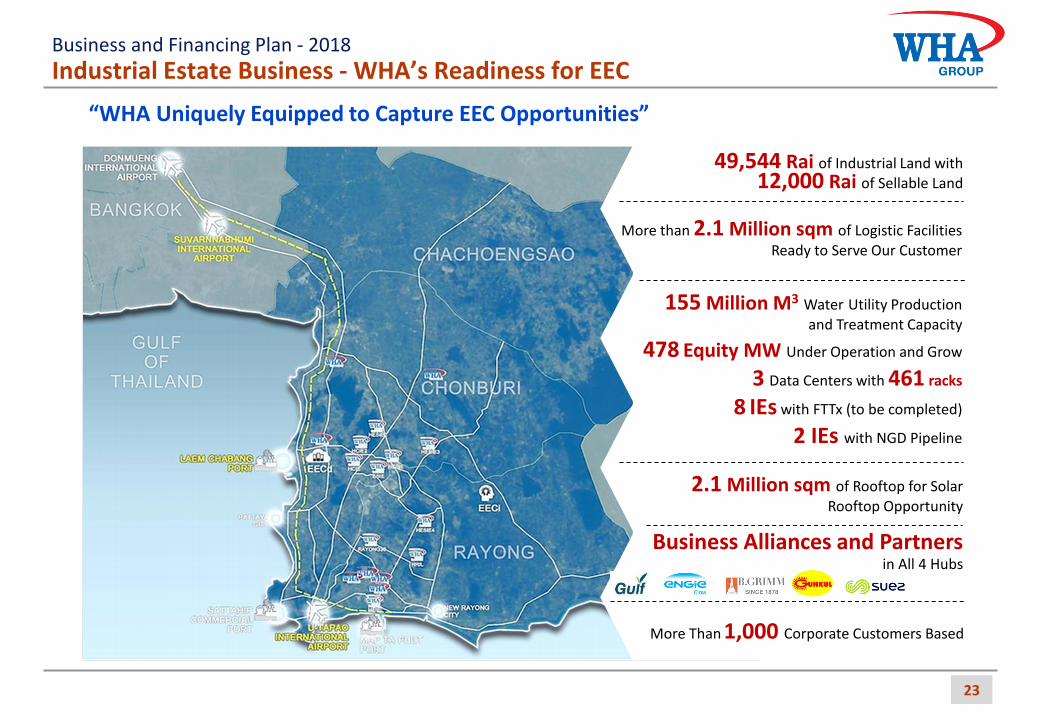

More Than 1,000 Corporate Customers Based

49,544 Rai of Industrial Land with 12,000 Rai of Sellable Land

155 Million M3 Water Utility Production and Treatment Capacity

478 Equity MW Under Operation and Grow

3 Data Centers with 461 racks

8 IEs with FTTx (to be completed)

2 IEs with NGD Pipeline

2.1 Million sqm of Rooftop for Solar Rooftop Opportunity

Business Alliances and Partners in All 4 Hubs

More than 2.1 Million sqm of Logistic Facilities Ready to Serve Our Customer

23

Industrial Estate Business - WHA’s Readiness for EEC Business and Financing Plan - 2018

“WHA Uniquely Equipped to Capture EEC Opportunities”

Industrial Estate Business – More Favorable Tax Incentive for EEC Area

24 Source: European Chamber Luncheon BOI Policy Update, March 2017

B O I – A c t i v i t y / S e c t o r B a s e d S8 = Technology based activities, giving incentive to

development of Biotechnology, Nanotechnology, Advanced Material Technology and Digital Technology

A1 = Knowledge-based activities, focusing on R&D and design to enhance the country’s competitiveness

A2 = Activities in infrastructure for the country’s development, activities using advanced technology to create value added, with none or very few existing investments in Thailand

A3 = High technology activities which are important to the country’s development, with a few investments already existing in Thailand

A4 = Activities with lower technology than A1-A3 but add value to domestic resources and strengthen supply chain

B1-B2 = Supporting industries that do not use high technology but are important to value chain

The EEC will receive a super incentive promotion package which goes far beyond the current regulations of the BOI-Act as followings: The exemption for corporate income

taxation (CIT) will be granted up to 15 years instead of the current maximal tax holidays of eight years.

A maximum personal income tax rate of 17% for management, investor, experts.

A five-year business visa, A land lease for 50+49 years, Trade using foreign currencies directly

without having to exchange it into Thai baht,

B O I – A r e a B a s e d

• R&D

• Support academic/research institutes, or technology and human resource development funds

• IP licensing fee

• Advanced Technology Training

• Development of local suppliers

• Product and packaging design

Merit on Competitiveness

Enhancement

Merit on Decentralization

Merit on

Industrial Area

Development

B O I – M e r i t B a s e d

• SEZ (10 Provinces)

• Southern Border (4 Provinces, 4 Districts)

• 20 Provinces with the Lowest per Capita Income

• Industrial Estates/Zones

• Science and Technology Parks

B O I - E E C P a c k a g e

Promote investments in the targeted industries located in EEC provinces

Special Investment Promotion Zone • Additional Corporate Income Tax holiday for 2 years

(maximum tax holiday up to 10 years) • Additional 50% reduction on Corporate Income Tax for 5

years

Industrial Promotion Zone to support targeted industry • Additional 50% reduction on Corporate Income Tax for 5

years

Industrial Estates or Industrial Parks located in 3 EEC provinces • Additional 50% reduction on Corporate Income Tax for 3

years

(As of 22nd November 2017)

E E C A c t

(Expected to become effective in Q12018) Area-based Promote investment that is 3 provinces – Rayong, Chonburi, and Chachoengsao

• Exemption from corporate income tax for up to 15 years (subject to further announcement on required qualifications)

• Exemption of import duties on machinery/raw or essential materials imported for use in production for export/ goods for R&D

• Matching Grants for Investment/ R&D/ Innovation/ Human Resources Development for Targeted Industries

• Permission to own land for BOI promoted projects

• Rights to state’s land lease for 50 years, renewable upon approval for a further 49 years

• 17% personal income tax rate for foreign executives working for regional headquarters or international trading companies, treasury centres, along with regional R&D centres

• One-stop service centre to facilitate foreign investors, provide useful information, and issue permits for trading, export and import all in one location

• Five-year work visa issuance to attract investors, experts and scientists from around the world

Exemption of CIT Exemption of Import Duty on

Machinery

Exemption of Import

Duty on Raw Material

Non-Tax

S8 10 Years (No Cap) + Merit

A1 8 Years (No Cap) + Merit

A2 8 Years + Merit

A3 5 Years + Merit

A4 3 Years + Merit

B1 0 Years + Merit (for some activities)

B2 - -

S8

Business and Financing Plan - 2018 St

and

ard

BO

I In

vest

me

nt

Pri

vile

ge

Spe

cial

Ince

nti

ve fo

r EE

C A

rea

Special Investment Promotion Zone (EECa, EECd, EECi)

• Additional Corporate Income Tax holiday for 2 years (maximum tax holiday up to 10 years)

• Additional 50% reduction on Corporate Income Tax for 5 years

• Applicants are required to provide training in science and technology for at least 10% of employees or a minimum 50 people a year

Industrial Promotion Zone for the targeted industries (IEs which has been promoted/qualified as industrial promotion zone e.g. HESIE4)

• Additional 50% reduction on Corporate Income Tax for 5 years

• Applicants are required to provide training in science and technology for at least 10% of employees or a minimum 50 people a year

Industrial Estates or Industrial Park located in EEC provinces (General IPs not qualified as industrial promotion zone)

• Additional 50% reduction on Corporate Income Tax for 3 years

• Applicants are required to provide training in science and technology for at least 5% of employees or a minimum 25 people a year

State Owned

Enterprises

Private Companies

Private Companies

Corporate

Personal

Others

• Maximum personal income tax of 17% for management, Investors and experts

• Five-year work permit

• Land lease up to 99 years (For State-owned Enterprise Land)

• Freehold land (For industrial estate developed in private operator) • Fast-track EIA

Utilities Business

25

Business and Financing Plan - 2018

Target Sale Volume of Utilities : 113 mm m3 per year Improving GPM by change in product mix and initiative of RO technology to supplant the processed water

Extend our Leadership in Industrial Estate Utilities Business To continuously build up reputation and trust by

improving service quality and enhancing R&D

Continue Expanding Markets To grow with new WHA-Hemaraj’s Industrial Estates

- HESIE3 to be launched in 2018 - Nghe An Vietnam Phase 1 to commence in2018 - Exploring opportunities in Vietnam

To serve on-premise demand (in WHA-Hemaraj IEs and outside) - Under negotiation process with customers

To tap non-industrial market (Municipal, commercial buildings) - Capturing the opportunities from specialized estates

To enter into other CLMV - Feasibility Study on the water supply projects in

Myanmar and Vietnam

Continue Adding More Products/Services To expand products mix to cover recycled water,

demineralized water, desalination, RO water, etc.

Initiatives Key Deliverables

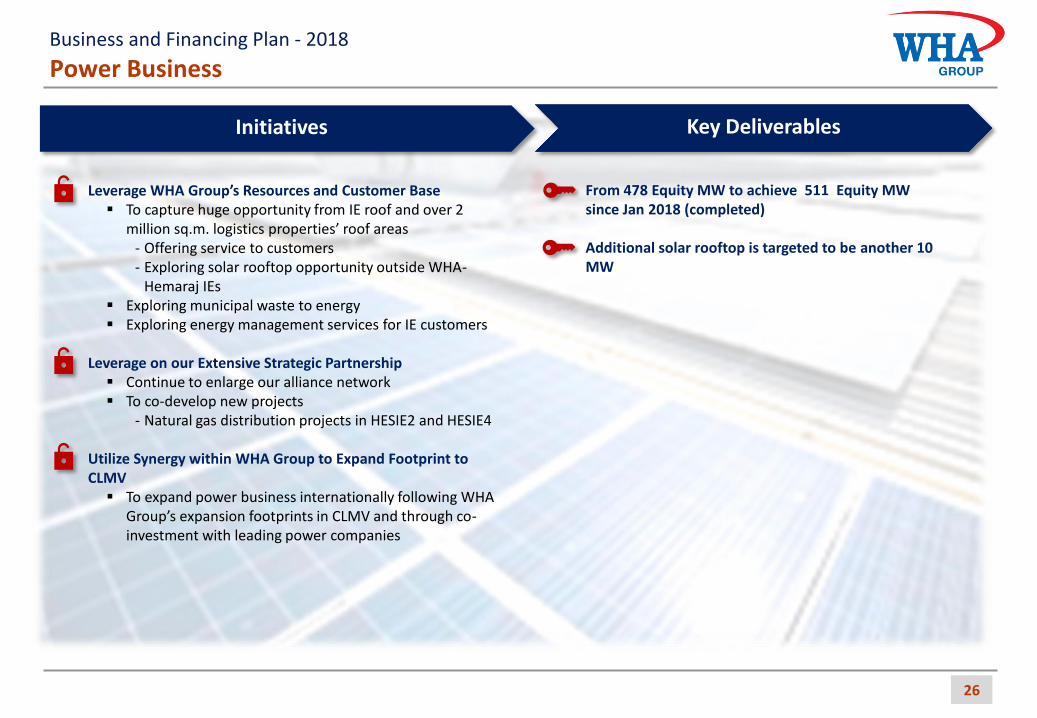

Power Business

26

Business and Financing Plan - 2018

From 478 Equity MW to achieve 511 Equity MW since Jan 2018 (completed) Additional solar rooftop is targeted to be another 10 MW

Leverage WHA Group’s Resources and Customer Base To capture huge opportunity from IE roof and over 2

million sq.m. logistics properties’ roof areas - Offering service to customers - Exploring solar rooftop opportunity outside WHA-

Hemaraj IEs Exploring municipal waste to energy Exploring energy management services for IE customers

Leverage on our Extensive Strategic Partnership Continue to enlarge our alliance network To co-develop new projects

- Natural gas distribution projects in HESIE2 and HESIE4

Utilize Synergy within WHA Group to Expand Footprint to CLMV To expand power business internationally following WHA

Group’s expansion footprints in CLMV and through co-investment with leading power companies

Initiatives Key Deliverables

Digital Platform Business

27

Business and Financing Plan - 2018

80% year-end Occupancy Rate of Data Center 9 FTTx in all WHA Hemaraj Industrial Estates 50% of Revenue in Managed Services which is Complementary to Data Center Rental Business

Completion of Data Center Roll-out in 3 Strategic Location Leveraging on WHA Group Customer Base • Establish 3 tier-3 data center with 617 racks by year-end

2018 • Commence operation of all FTTx in all WHA Hemaraj

industrial estates Gradually move up the Value Chain to Platform as a Service (PAAS) from Existing Infrastructure as a Service (IAAS)

Initiatives Key Deliverables

Big-Data + Data Analytics

Cloud computing + Wholesaler-Retailer Model

Co-location (DR+DC)/ FTTx/Networking/CCTV/Conference call

Platform as a Service

Infrastructure as a Service

Solution as a Service

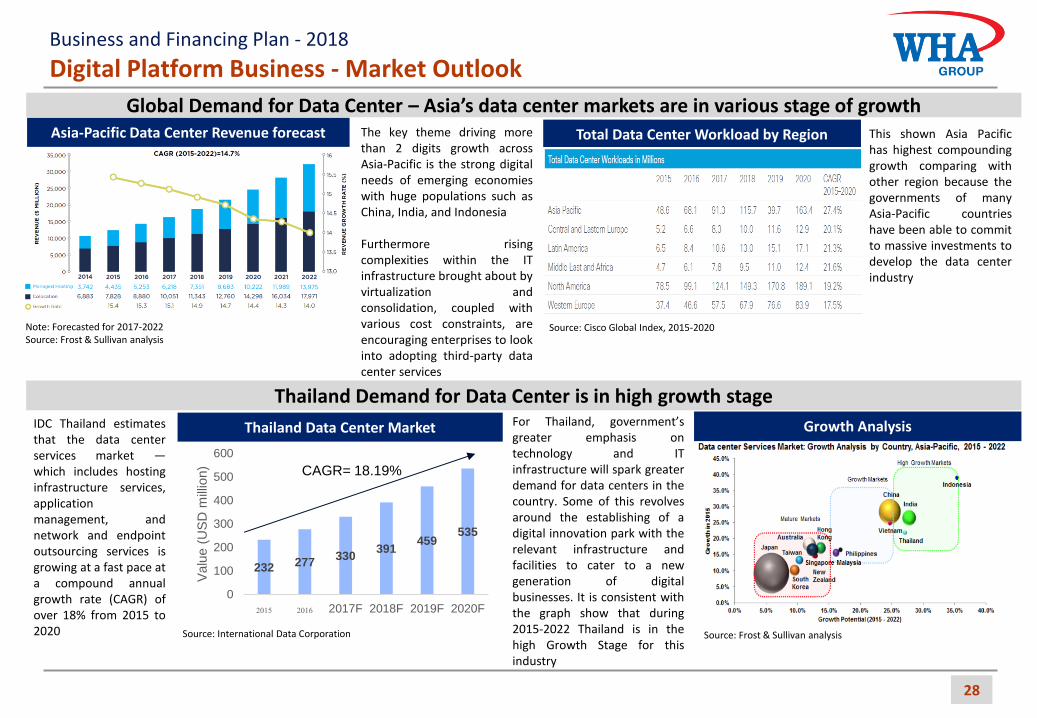

Digital Platform Business - Market Outlook

28

Asia-Pacific Data Center Revenue forecast

Note: Forecasted for 2017-2022 Source: Frost & Sullivan analysis

The key theme driving more than 2 digits growth across Asia-Pacific is the strong digital needs of emerging economies with huge populations such as China, India, and Indonesia

Furthermore rising complexities within the IT infrastructure brought about by virtualization and consolidation, coupled with various cost constraints, are encouraging enterprises to look into adopting third-party data center services

Total Data Center Workload by Region This shown Asia Pacific has highest compounding growth comparing with other region because the governments of many Asia-Pacific countries have been able to commit to massive investments to develop the data center industry

Source: Cisco Global Index, 2015-2020

Global Demand for Data Center – Asia’s data center markets are in various stage of growth

Thailand Data Center Market

232 277 330

391 459

535

0

100

200

300

400

500

600

2015 2016 2017F 2018F 2019F 2020F

Valu

e (

US

D m

illio

n) CAGR= 18.19%

Source: International Data Corporation

IDC Thailand estimates that the data center services market — which includes hosting infrastructure services, application management, and network and endpoint outsourcing services is growing at a fast pace at a compound annual growth rate (CAGR) of over 18% from 2015 to 2020

Growth Analysis For Thailand, government’s greater emphasis on technology and IT infrastructure will spark greater demand for data centers in the country. Some of this revolves around the establishing of a digital innovation park with the relevant infrastructure and facilities to cater to a new generation of digital businesses. It is consistent with the graph show that during 2015-2022 Thailand is in the high Growth Stage for this industry

Source: Frost & Sullivan analysis

Thailand Demand for Data Center is in high growth stage

Business and Financing Plan - 2018

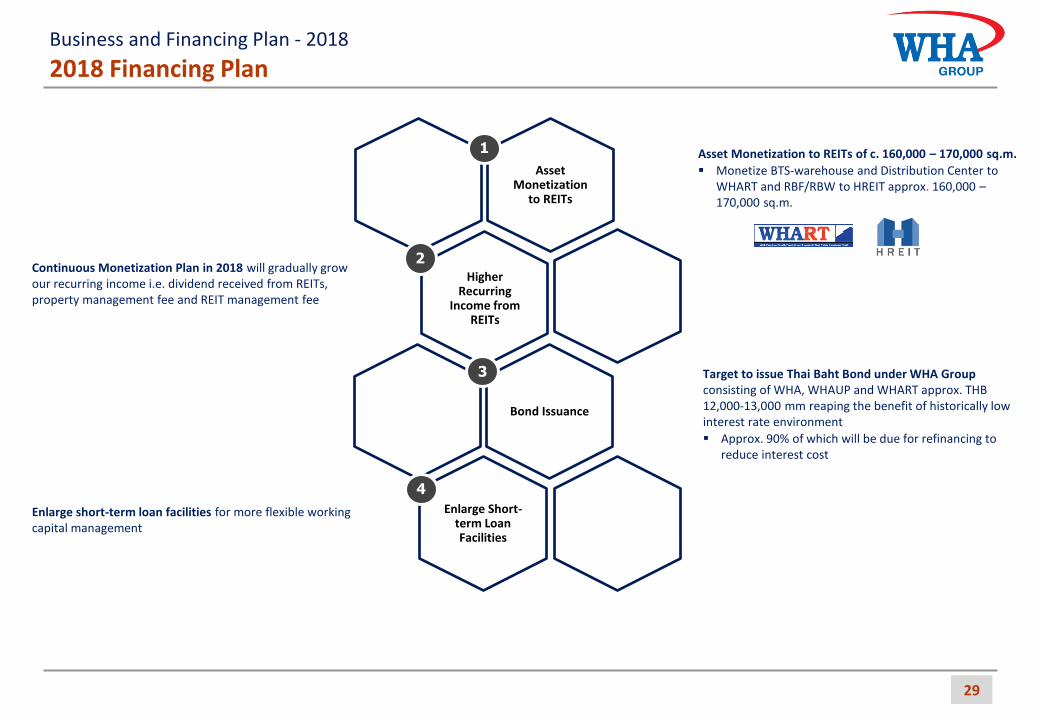

2018 Financing Plan

Enlarge short-term loan facilities for more flexible working capital management

Asset Monetization to REITs of c. 160,000 – 170,000 sq.m.

Monetize BTS-warehouse and Distribution Center to WHART and RBF/RBW to HREIT approx. 160,000 – 170,000 sq.m.

Continuous Monetization Plan in 2018 will gradually grow our recurring income i.e. dividend received from REITs, property management fee and REIT management fee

Target to issue Thai Baht Bond under WHA Group consisting of WHA, WHAUP and WHART approx. THB 12,000-13,000 mm reaping the benefit of historically low interest rate environment

Approx. 90% of which will be due for refinancing to reduce interest cost

29

Higher Recurring

Income from REITs

Bond Issuance

Enlarge Short-term Loan Facilities

Asset Monetization

to REITs

1

2

3

4

Business and Financing Plan - 2018

2017A 2018F

12,410 14,700

44%

28%

25%

3%

Logistics & REITs Industrial Development

Utilities and Power Digital Platform

2018 Revenue and Share of Profits

30

61%

39%

Sales Recurring Income

Sales VS Recurring Income

2018F

Revenue* by Hub

2018F

Solid Revenue and Share of Profits Prospect

Better Earnings Visibility

Strengthen all Business Platforms

Well-diversified Revenue

Healthy Sales and Recurring Income Mix

Expected 19% GROWTH

Business and Financing Plan - 2018

Remark: *Revenue include share of profit from power business

2018 Investment Plan and Leverage Level

31

2016A 2017A 2018F 2019F 2020F

Investment Plan

5Y Total Investment Plan

THB 43,000 mm

In 2018, investment in 4 businesses is expected at THB 6,600 mm

The estimated group-wide investment for 5 years of THB 43,000 mm is align with 5Y strategy

The distribution of CAPEX by hub is well structured

Estimated Leverage

38%

31%

28%

3%

Logistics

Industrial Development

Utilities and Power

Digital Platform

CAPEX 2018F

6,600

9,900

MB 1.9x

1.2x 1.1x 1.1x 0.9x

2016A 2017A 2018F 2019F 2020F

Interest-bearing Debt/Equity Target < 1.0x

Target Interest-bearing Debt/Equity < 1.0X

Target Interest-bearing Debt/EBITDA < 4.5X

Target

Given stronger profitability and lower financial loan, the group will have healthier financial position with decreasing trend of the leverage ratio

6,100 4,900

Unit : THB mm

Business and Financing Plan - 2018

Overall Performance Financial Performance

2017 PERFORMANCE Unit: THB mm

32

Total revenue decreased 36% from 2016 to THB 12,410 mm in 2017, mainly

from shift the monetization of assets into HREIT to January 2018 which

compensate by higher number of land transfer from Hemaraj IE in 2017

compared with 2016, increase in share of profit from JVs and right of way

charged in Hemaraj IE.

EBITDA decreased by 12% YoY to THB 6,222 mm in 2017, resulting from

shift the monetization of assets into HREIT to January 2018 which

compensate by an increase of share of profit of power business in 2017

and achieved B.Grimm Power, Gulf VTP, Gulf TS1 Gulf TS2 and Gulf TS3

COD on planned schedule of 159 equity MW.

Share of profit from JVs 2017 increased by 95%, compared with 2016 as

B.Grimm Power, Gulf VTP, Gulf TS1, Gulf TS2 and Gulf TS3 have

commenced its COD in Nov 2016, May 2017, July 2017, Sep 2017 and Nov

2017, respectively adding our portfolio up to 478 Equity MW. Moreover, there

was unrealized FX gain amount of THB 574 mm during this year.

Net profit attribute to owners of the parent increased to THB 3,266 mm in

2017 or increase at the rate of 13% YoY mainly from an increase of sale of

Hemaraj IE, profitability from asset monetization to WHART, share of

profit and decrease of financial cost after acquisition loan repayment,

WHAUP’s loan refinancing, hemaraj’s bond repayment and loan

repayment in 2Q'17 from WHAUP’s IPO proceed.

OVERALL HIGHLIGHT

+ 13%

(12%)

(36%)

(43%)

+ 95%

NPM 26% NPM 15% NPM 15%

+ 48%

+ 33%

+ 47%

(3%)

+ 52%

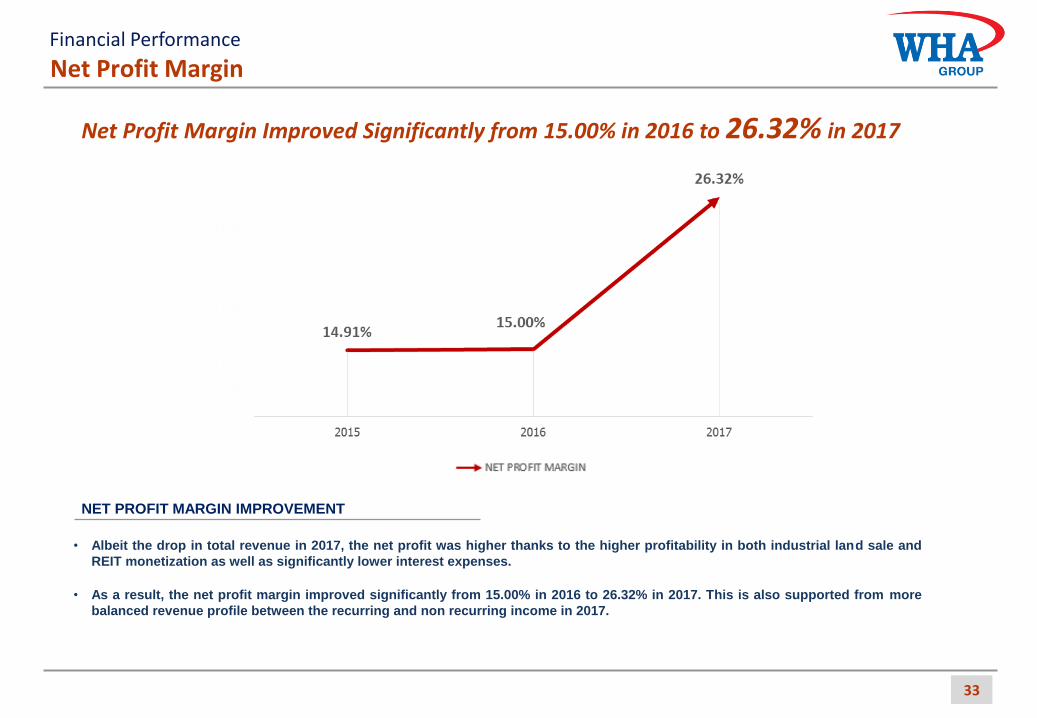

Net Profit Margin Financial Performance

33

• Albeit the drop in total revenue in 2017, the net profit was higher thanks to the higher profitability in both industrial land sale and

REIT monetization as well as significantly lower interest expenses.

• As a result, the net profit margin improved significantly from 15.00% in 2016 to 26.32% in 2017. This is also supported from more

balanced revenue profile between the recurring and non recurring income in 2017.

NET PROFIT MARGIN IMPROVEMENT

Net Profit Margin Improved Significantly from 15.00% in 2016 to 26.32% in 2017

Profitability by Business

RENTAL PROPERTY BUSINESS SALES OF PROPERTIES BUSINESS

Unit: THB mm

Financial Performance

OTHER REVENUES

The increase in other revenues in 2017 mainly

resulted from right of way charged in Hemaraj

IE amount to THB 209 mm and acquisition fee

from WHAPF conversion and new asset

acquisition in WHA logistic amounted to THB

121 mm

Hemaraj sold investment estates amounted to THB 3,343 mm in 2017, a margin

of 57% on genuine operation’s level and 51% on consolidated level after PPA.

The increase was mainly due to higher number of land transfer in 2017

WHA had revenue recognition mainly from assets monetization to WHART of

THB 2,875 mm , a margin of 45%.

Sale to HREIT

Sale of IEs

Rental and service income of WHA decreased by 22%, while RBF/RBW from

Hemaraj decreased by 39% in 2017 from 2016 as a result of large assets

monetization into HREIT amounted to 261,314 sqm in 4Q2016.

Remark: Other revenues consist of property and REIT management fee, acquisition fee, dividend income,

share of profit from property fund, and other income

34

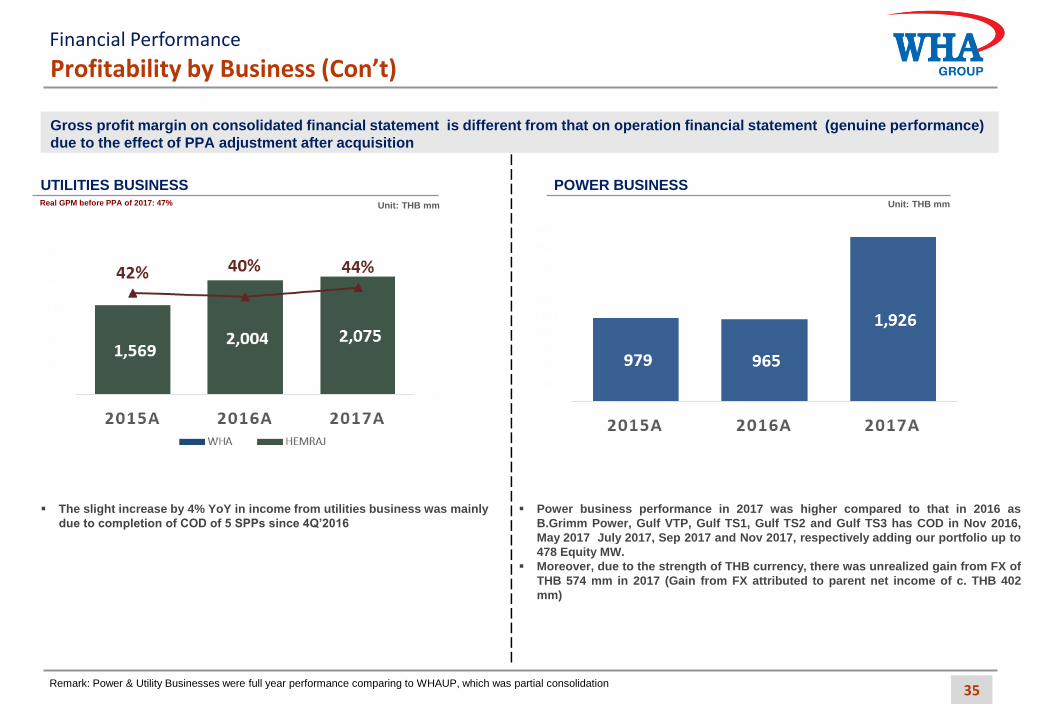

Real GPM before PPA of 2017: 58% Real GPM before PPA of 2017: 51%

Gross profit margin on consolidated financial statement is different from that on operation financial statement (genuine performance)

due to the effect of PPA adjustment after acquisition

Unit: THB mm

Unit: THB mm

Profitability by Business (Con’t)

UTILITIES BUSINESS POWER BUSINESS

Gross profit margin on consolidated financial statement is different from that on operation financial statement (genuine performance)

due to the effect of PPA adjustment after acquisition

Financial Performance

The slight increase by 4% YoY in income from utilities business was mainly

due to completion of COD of 5 SPPs since 4Q’2016

Power business performance in 2017 was higher compared to that in 2016 as

B.Grimm Power, Gulf VTP, Gulf TS1, Gulf TS2 and Gulf TS3 has COD in Nov 2016,

May 2017 July 2017, Sep 2017 and Nov 2017, respectively adding our portfolio up to

478 Equity MW.

Moreover, due to the strength of THB currency, there was unrealized gain from FX of

THB 574 mm in 2017 (Gain from FX attributed to parent net income of c. THB 402

mm)

Remark: Power & Utility Businesses were full year performance comparing to WHAUP, which was partial consolidation 35

Real GPM before PPA of 2017: 47% Unit: THB mm Unit: THB mm

Revenue and Gross Profit Breakdown

36

2017 GROSS PROFIT BREAKDOWN

2017 REVENUE BREAKDOWN

Unit: THB mm Unit: THB mm

TOTAL

THB 12,410 mm TOTAL

THB 7,408 mm

Remark: Share of profit from JV’s and Associates included Remark: Share of profit from JV’s and Associates included

Gross profits are based on consolidated financial statements and thus

affected by PPA adjustment

Recurring vs Non-Recurring = 49:51 Recurring vs Non-Recurring = 60:40

Financial Performance

Remark: Power & Utility Businesses were full-year performance, comparing to WHAUP, which was partial consolidation

Financial Position

37

Unit: THB mm

CAPITAL STRUCTURE ASSETS

Unit: THB mm

RETURN ON INVESTMENT

IP’s stood at THB 9,422 mm in 2017 due to reclassification to non- current assets held for sale.

Intangible assets & goodwill of THB 21,694 mm resulted from the PPA after the acquisition.

Hemaraj contributed Cost of Real Estate Developments after PPA of THB 13,740 mm and Investment in Associates after PPA of THB 12,339 mm to the consolidated balance sheet in 2017.

Financial Performance

Remark: ROE = Trailing 12 months net Income attributable to parent / Average total equity attributable to owners of the parent

ROA = Trailing 12 months net income / Average total asset ROIC = Trailing 12 months NOPAT / Average Invested Capital (IBD and Equity)

Others

Intangible Assets & Goodwill

Investment Properties

Investment in Associates

Non-Current Assets Held for Sale

Cost of Real Estate Development

Cash & ST Investments

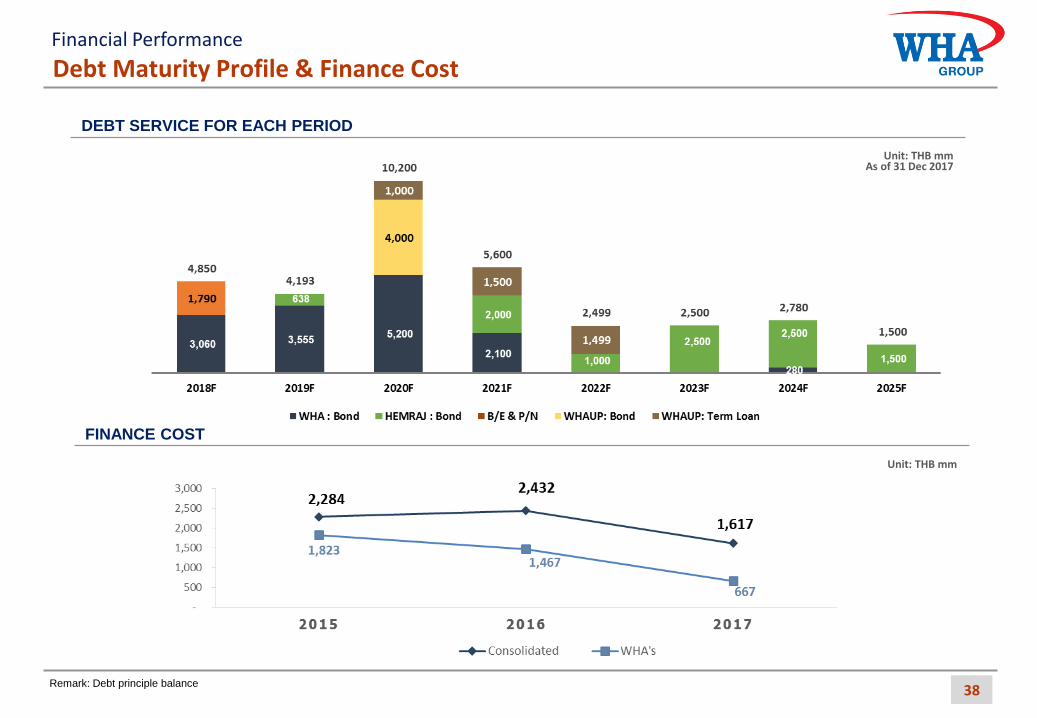

Debt Maturity Profile & Finance Cost

DEBT SERVICE FOR EACH PERIOD

Unit: THB mm

FINANCE COST

Financial Performance

Unit: THB mm As of 31 Dec 2017

38 Remark: Debt principle balance

Appendix

39

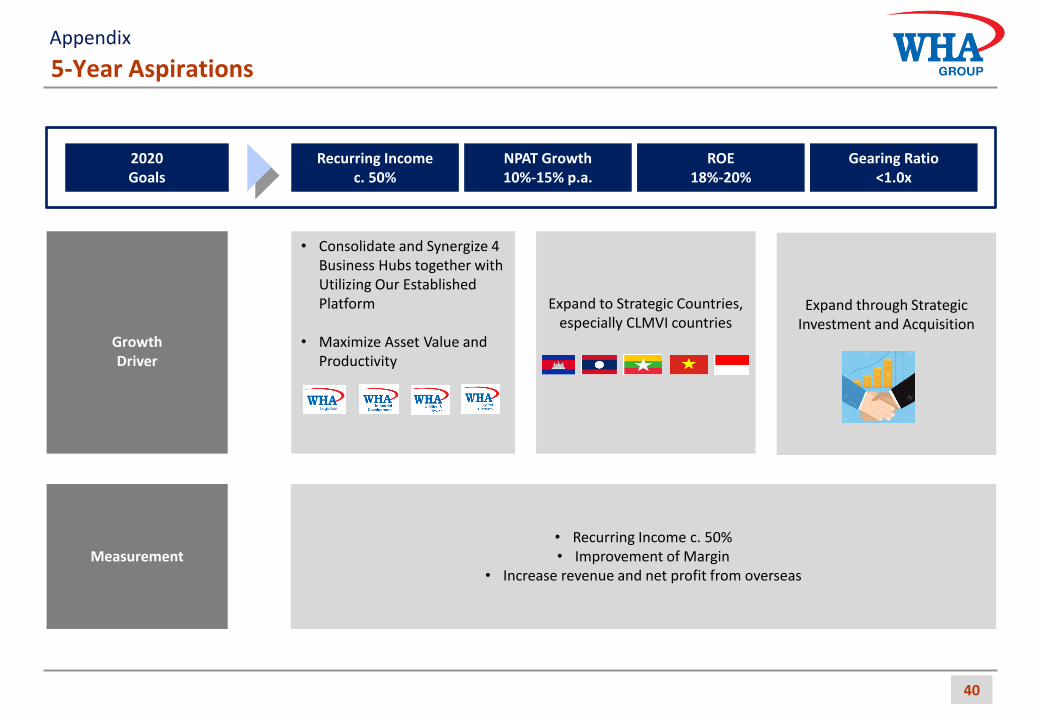

5-Year Aspirations

40

2020 Goals

Recurring Income c. 50%

NPAT Growth 10%-15% p.a.

ROE 18%-20%

Gearing Ratio <1.0x

Growth Driver

• Consolidate and Synergize 4 Business Hubs together with Utilizing Our Established Platform

• Maximize Asset Value and Productivity

Expand through Strategic Investment and Acquisition

Expand to Strategic Countries, especially CLMVI countries

Measurement

• Recurring Income c. 50% • Improvement of Margin

• Increase revenue and net profit from overseas

Appendix

41

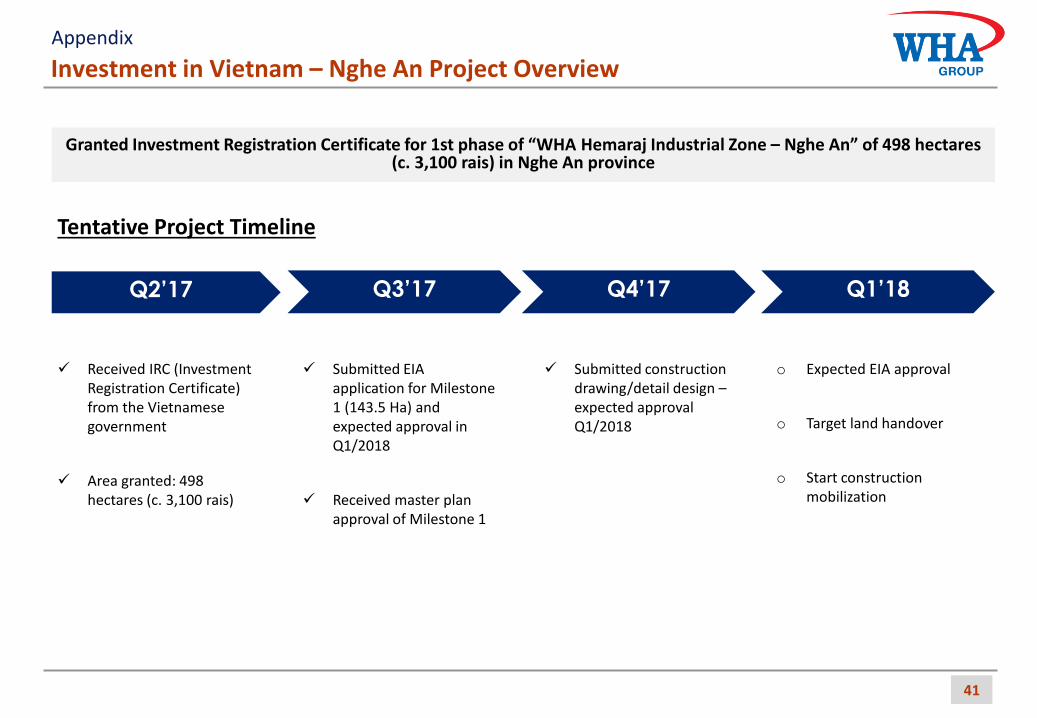

Investment in Vietnam – Nghe An Project Overview

Tentative Project Timeline

Received IRC (Investment Registration Certificate) from the Vietnamese government

Area granted: 498 hectares (c. 3,100 rais)

Submitted EIA application for Milestone 1 (143.5 Ha) and expected approval in Q1/2018

Received master plan approval of Milestone 1

Submitted construction drawing/detail design – expected approval Q1/2018

Q2’17 Q3’17

o Expected EIA approval

o Target land handover

o Start construction mobilization

Q4’17 Q1’18

Granted Investment Registration Certificate for 1st phase of “WHA Hemaraj Industrial Zone – Nghe An” of 498 hectares (c. 3,100 rais) in Nghe An province

Appendix

42

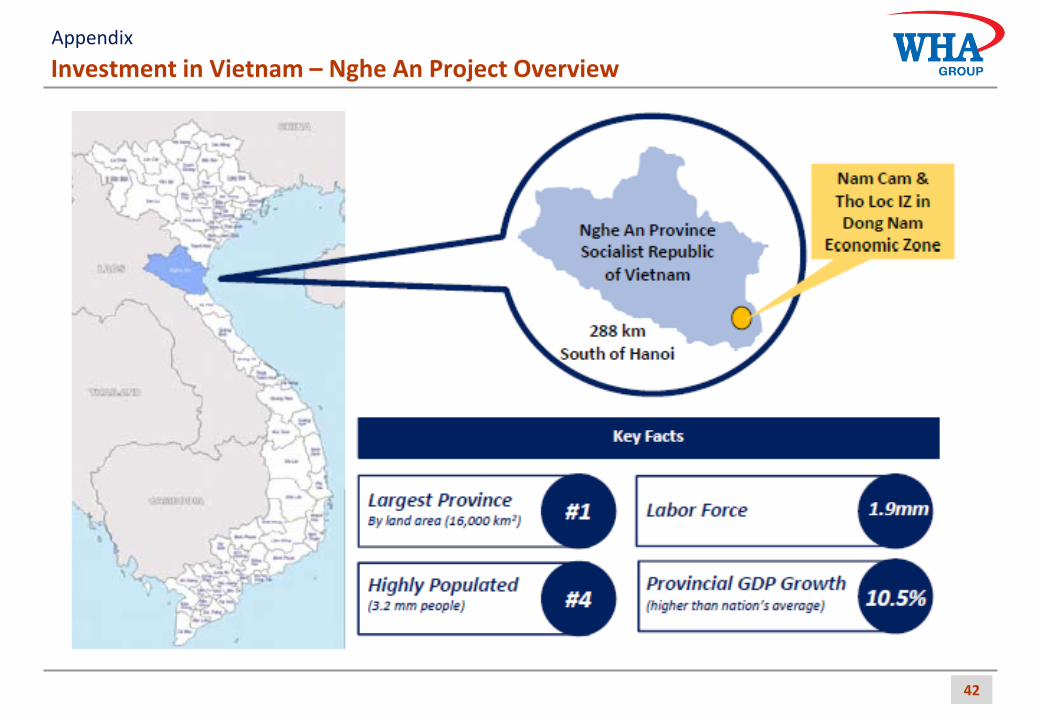

Investment in Vietnam – Nghe An Project Overview Appendix

43

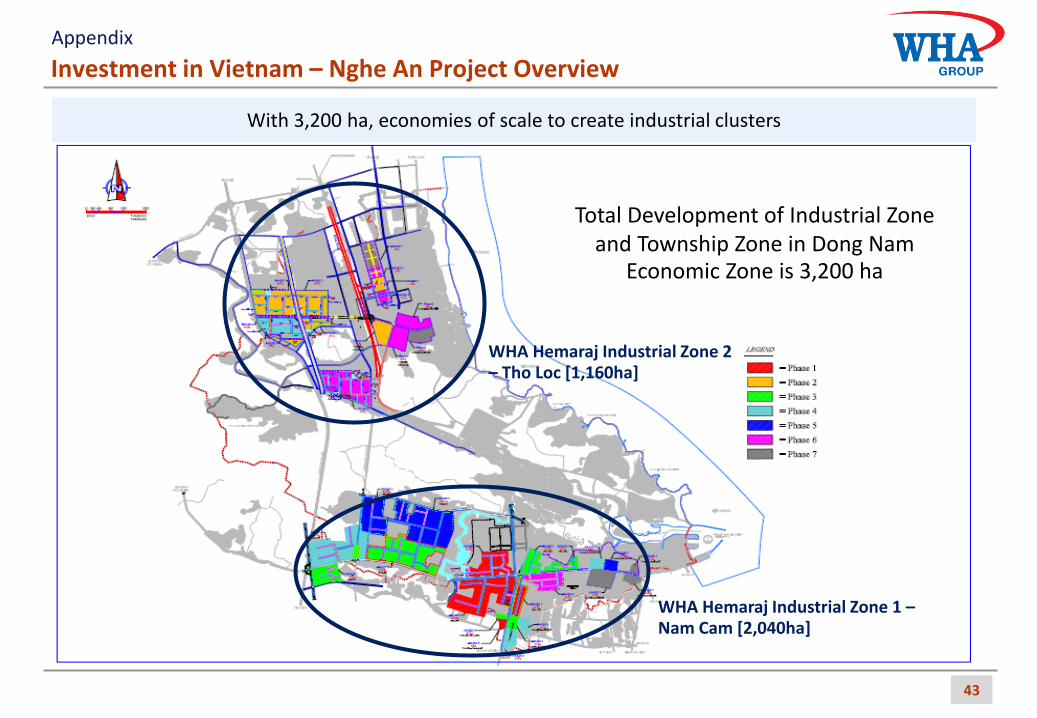

With 3,200 ha, economies of scale to create industrial clusters

WHA Hemaraj Industrial Zone 2 – Tho Loc [1,160ha]

WHA Hemaraj Industrial Zone 1 – Nam Cam [2,040ha]

Total Development of Industrial Zone and Township Zone in Dong Nam

Economic Zone is 3,200 ha

Investment in Vietnam – Nghe An Project Overview Appendix

44

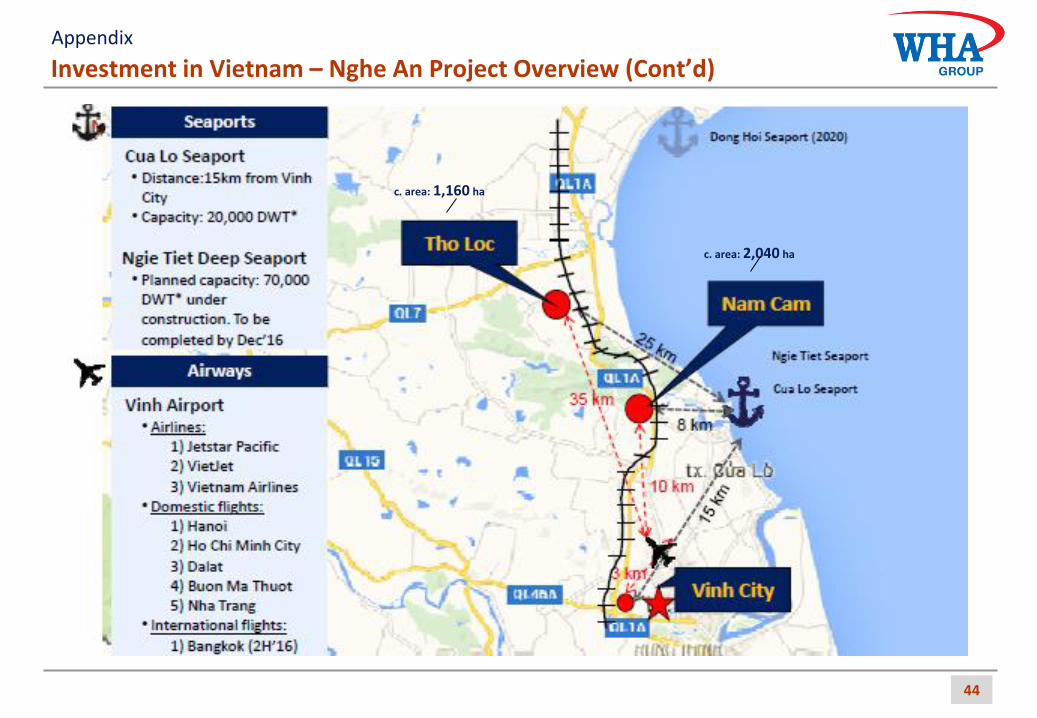

Investment in Vietnam – Nghe An Project Overview (Cont’d)

c. area: 2,040 ha

c. area: 1,160 ha

Appendix

45

Investment in Vietnam – Nghe An Project Overview (Cont’d)

c. area: 2,040 ha

c. area: 1,160 ha

Appendix

Shareholding Information / Board of Director

Shareholding Information/1

Top 10 Shareholder/1

Shareholder No. of Share/3 %

1) WHA Holding Co., Ltd. 3,629,083,491 25.3

2) Ms. Jareeporn Jarukornsakul 1,629,989,569 11.4

3) Mr. Somyos Anantaprayoon 1,090,894,523 7.6

4) UBS AG HONG KONG BRANCH 101,400,000 0.7

5) CREDIT SUISSE AG, SINGAPORE BRANCH 321,473,360 2.2

6) STATE STREET BANK EUROPE LIMITED 1,431,873,815 10.0

7) Thai NVDR Co., Ltd. 388,720,713 2.7

8) Mr. Sompong Chonkadeedumrongkul 247,160,300 1.7

9) N.C.B.TRUST LIMITED-NORGES BANK 11 217,217,300 1.5

10) Mr. Wut Jarukornsakul 158,500,000 1.1

• Major shareholder 47.3%

• Other pre-IPO shareholder /1 3.2%

• Post-IPO Investors 49.5%

Major Shareholder /2

Paid-up Capital

(THB 1,432.2 mm)

46

Board of Director and Management

Ms. Jareeporn Jarukornsakul

Chairman of Board of Directors

Group Chief Executive Officer

Mr. David Richard Nardone

Vice Chairman of Board of Directors

Chief Executive Officer- Industrial Business

Mr. Vivat Jiratikarnsakul

Director

Chief Operating Officer-Industrial business

Mr. Arttavit Chalermsaphayakorn

Director

Chief Financial Officer

Mr. Jakrit Chaisanit

Director

Chief Operating Officer-Logistics business

Mr. Narong Kritchanchai

Director

Chief Legal Officer

Mr. Krailuck Asawachatroj

Director

Chief Strategic Officer

Mr. Somsak Boonchoyreungchai

Director

Vice President of Accounting

Dr. Apichai Boontherawara

Independent Director

Chairman of the Audit Committee

Dr. Kritsana Sukboonyasatit

Independent Director

Member of the Audit Committee

Mr. Chanvit Amatamatucharti

Independent Director

Dr. Somsak Pratomsrimek

Independent Director

Member of the Audit Committee

Appendix

Remarks: /1 Shareholder information as of May 11, 2017 /2 Major shareholder holds 47.3% of the total outstanding shares while parts of major shareholders shares are hold via UBS AG Hong Kong Branch and Credit Suisse AG Singapore Branch.

47.3%

27.2%

8.5%

17.0%

Major Shareholders

Local Retail

Local Institution

Foreign Institution

CONSUMER GOODS

DANGEROUS GOODS

FOOD CHAIN AND PET FOOD

HEALTHCARE

AUTOMOTIVE

THIRD PARTY LOGISTICS (3PL)

AIRCRAFT MANUFACTURING

47

Selected Logistics Customers Appendix

48

Consumer Petrochemical Steel/Metal

Automotive

Selected Industrial Customers Appendix

Recommended