WHEN CONTRACTS GO SOUR:Drafting and Due Diligence Lessons Learned From Litigation

Washington Metropolitan Area Corporate Counsel AssociationApril 8, 2008

Jerome L. Epstein, Partner Jenner & Block LLPTel: 202 639-6062

E-mail: [email protected]

Tobias L. Knapp, Partner Jenner & Block LLPTel: 212 891-1655

E-mail: [email protected]

2

AGENDA

Drafting, Litigation, and Due Diligence Tips

Relating to Frequently Litigated Contractual Clauses• The Intersection of Fraud and Contract: Integration Clauses,

Disclaimers, and other Tools to Ward Off Fraud Claims

• Lessons from Recent Decisions Concerning Specific Performance/Material Adverse Change

• Best Efforts

• Arbitration Clauses

• Indemnification Clauses and Limitations of Liability

3

Fraud Claims Arising Out of “Contractual” Disputes

• Essential Elements of a Common Law Fraud Claim Determining Justifiable Reliance

• Why do We Care if a Seeming “Breach” is Presented as an Intentional Tort?

• When a Buyer Sues in Tort – Fraudulent Inducement

4

Tips for Avoiding Fraudulent Inducement Claims

• Merger/integration clauses are usually necessary but not sufficient.

• Protection from a Disclaimer? General vs. Specific

5

Tips for Avoiding Fraudulent Inducement Claims Continued

• “As is” clause • Buyer’s access to information• Indemnification as buyer’s exclusive remedy • Anti-sandbagging clause• Caveats in offering memorandum or other pre-contract

formal descriptions

• Other contractual clauses that help defeat fraud claims, even if insufficient standing alone:

6

Tips for Avoiding Fraudulent Inducement Claims Continued

• Due Diligence Tips Records of documents produced

Attendance at all interviews conducted by buyer

Requirement that buyer seek updated diligence

Buyers, in turn, must be careful to follow up on key items on their own diligence lists

Establish clear record that the other party was asked if it required more information

7

Litigation Tips for Defending Fraud Claims Between Parties to a Contract

• Don’t rule out motion to dismiss

• Was missing information in the Seller’s “exclusive knowledge,” or should it have been discovered through reasonable due diligence?

• Was alleged misrepresentation a statement of opinion, or mere puffery?

• Reliance, reliance, reliance!

8

Pre-Closing Disputes: MAC Clauses and Specific Performance

MAC Clauses

Specific Performance / Reverse Termination Fee

URI v. Cerberus: The “Forthright Negotiator”

9

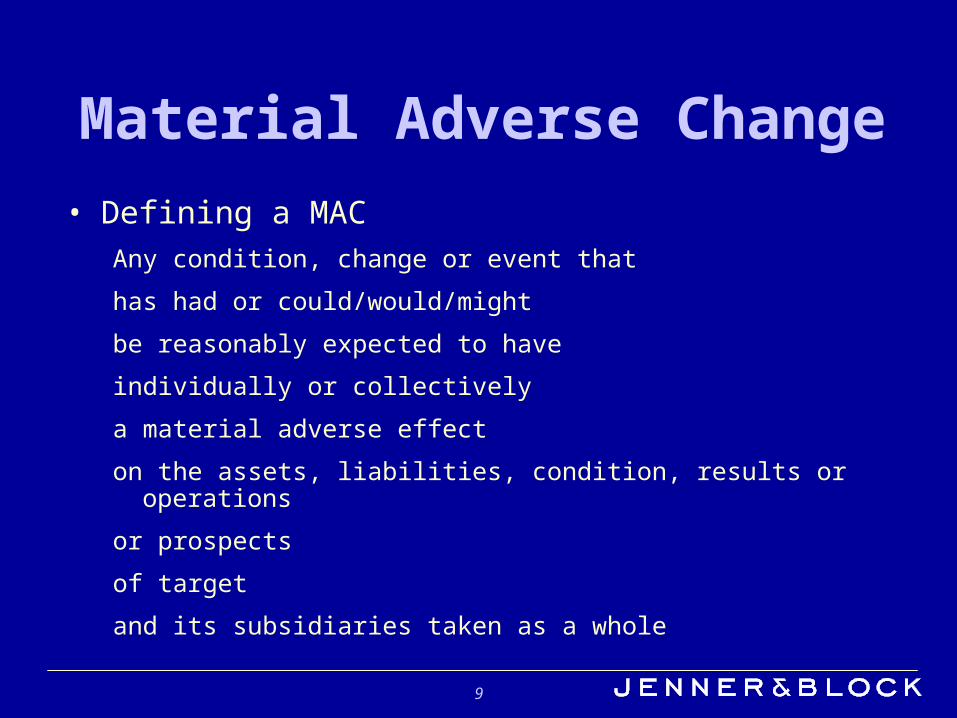

Material Adverse Change• Defining a MAC

Any condition, change or event that

has had or could/would/might

be reasonably expected to have

individually or collectively

a material adverse effect

on the assets, liabilities, condition, results or operations

or prospects

of target

and its subsidiaries taken as a whole

10

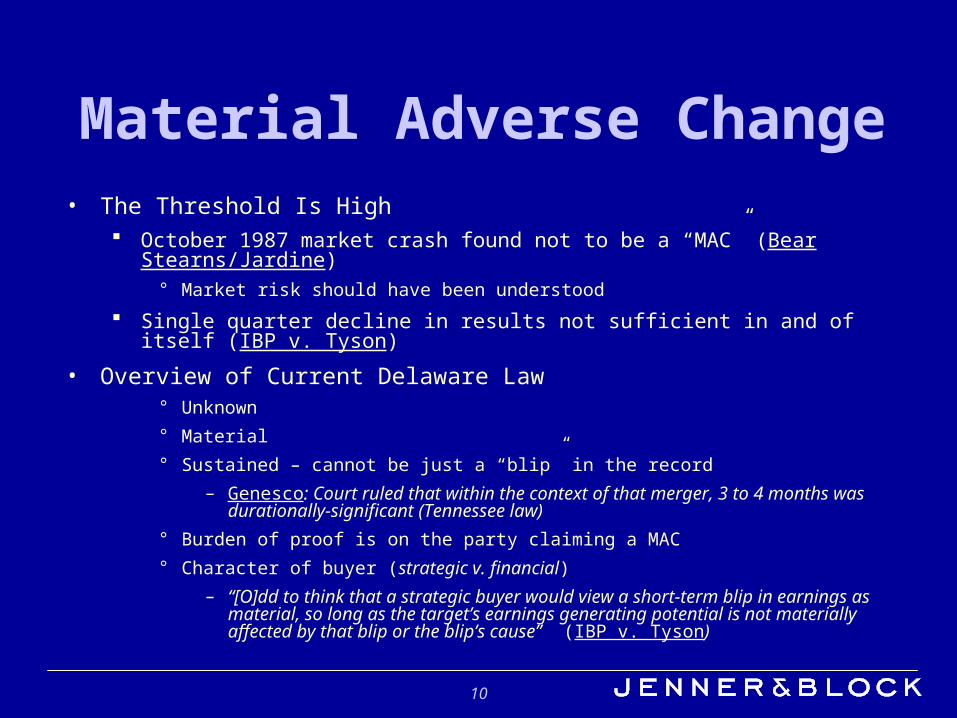

Material Adverse Change• The Threshold Is High

October 1987 market crash found not to be a “MAC” (Bear Stearns/Jardine)° Market risk should have been understood

Single quarter decline in results not sufficient in and of itself (IBP v. Tyson)

• Overview of Current Delaware Law° Unknown° Material° Sustained – cannot be just a “blip” in the record

– Genesco: Court ruled that within the context of that merger, 3 to 4 months was durationally-significant (Tennessee law)

° Burden of proof is on the party claiming a MAC° Character of buyer (strategic v. financial)

– “[O]dd to think that a strategic buyer would view a short-term blip in earnings as material, so long as the target’s earnings generating potential is not materially affected by that blip or the blip’s cause” (IBP v. Tyson)

11

Material Adverse Change

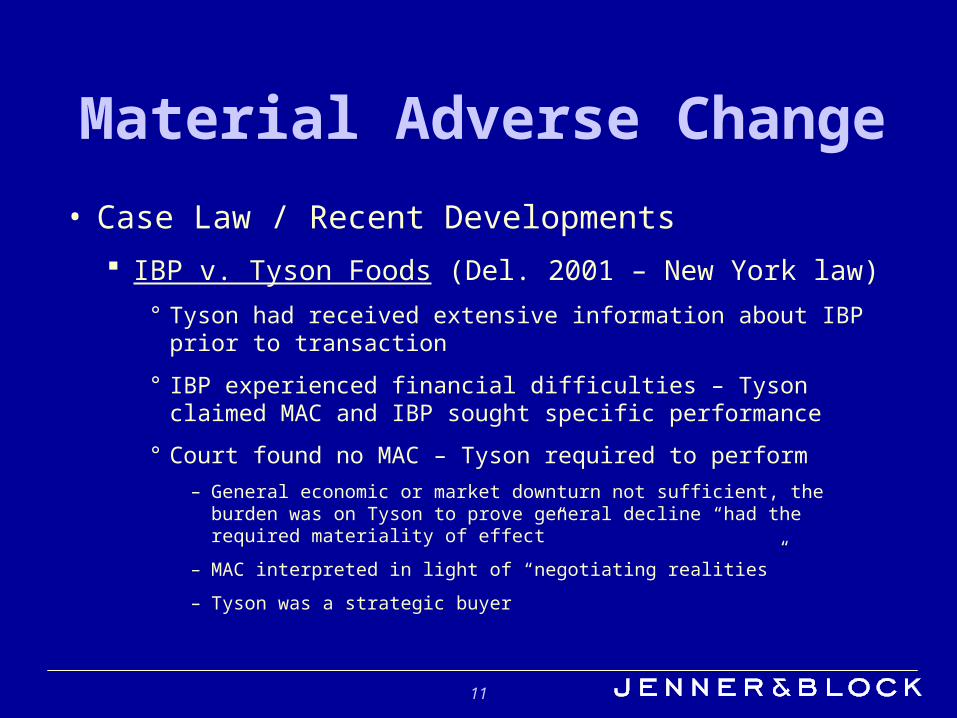

• Case Law / Recent Developments IBP v. Tyson Foods (Del. 2001 – New York law)

° Tyson had received extensive information about IBP prior to transaction

° IBP experienced financial difficulties – Tyson claimed MAC and IBP sought specific performance

° Court found no MAC – Tyson required to perform– General economic or market downturn not sufficient, the burden was on Tyson to

prove general decline “had the required materiality of effect”

– MAC interpreted in light of “negotiating realities”

– Tyson was a strategic buyer

12

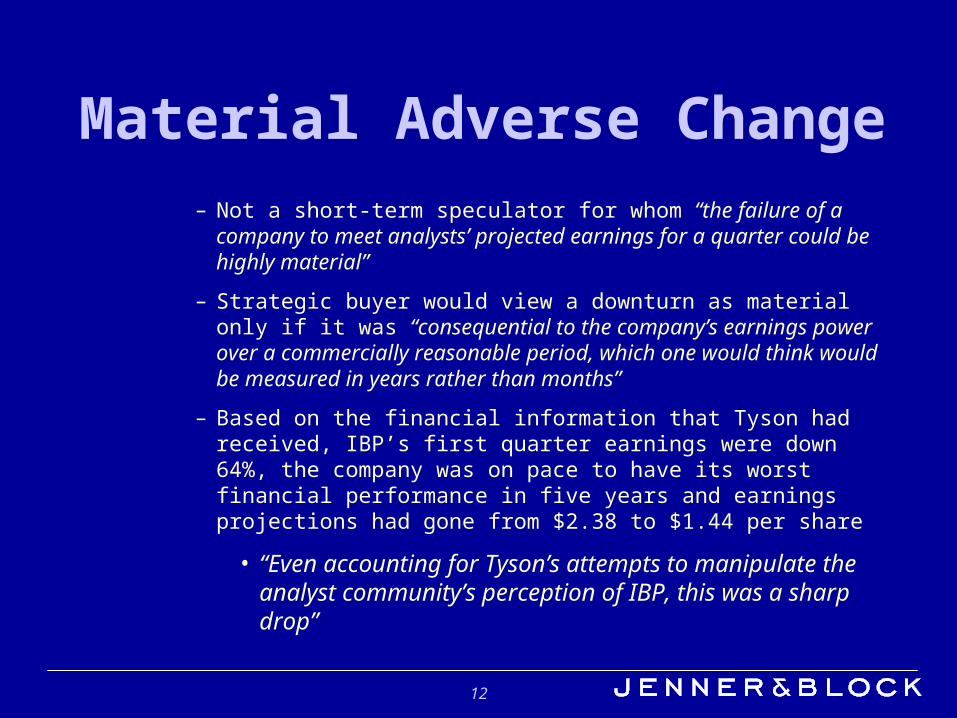

Material Adverse Change– Not a short-term speculator for whom “the failure of a company to meet

analysts’ projected earnings for a quarter could be highly material”

– Strategic buyer would view a downturn as material only if it was “consequential to the company’s earnings power over a commercially reasonable period, which one would think would be measured in years rather than months”

– Based on the financial information that Tyson had received, IBP’s first quarter earnings were down 64%, the company was on pace to have its worst financial performance in five years and earnings projections had gone from $2.38 to $1.44 per share

• “Even accounting for Tyson’s attempts to manipulate the analyst community’s perception of IBP, this was a sharp drop”

13

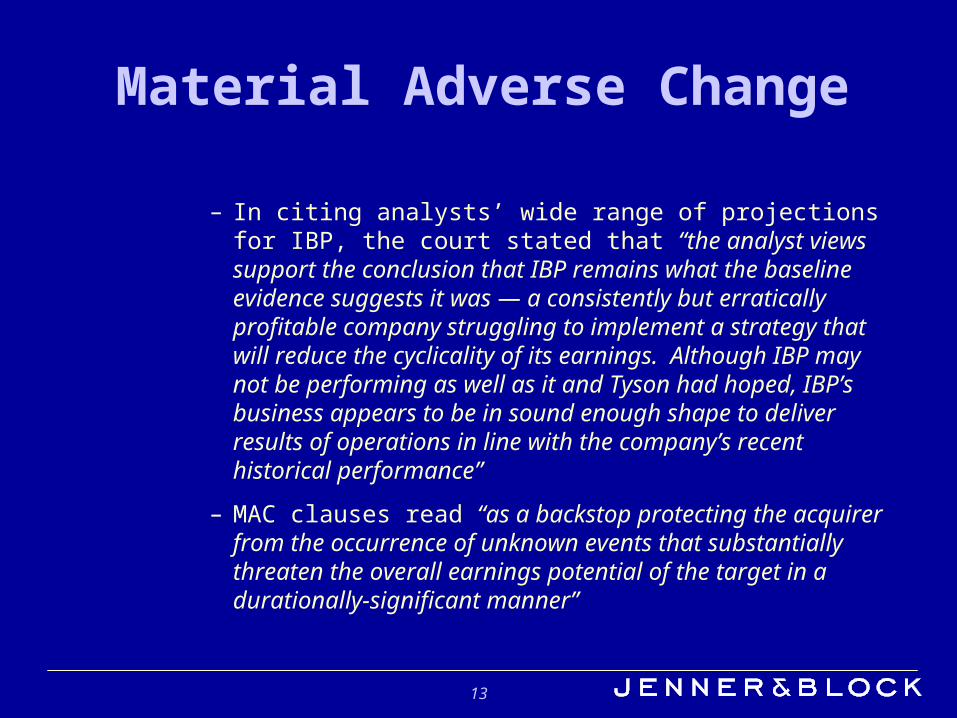

Material Adverse Change

– In citing analysts’ wide range of projections for IBP, the court stated that “the analyst views support the conclusion that IBP remains what the baseline evidence suggests it was — a consistently but erratically profitable company struggling to implement a strategy that will reduce the cyclicality of its earnings. Although IBP may not be performing as well as it and Tyson had hoped, IBP’s business appears to be in sound enough shape to deliver results of operations in line with the company’s recent historical performance”

– MAC clauses read “as a backstop protecting the acquirer from the occurrence of unknown events that substantially threaten the overall earnings potential of the target in a durationally-significant manner”

14

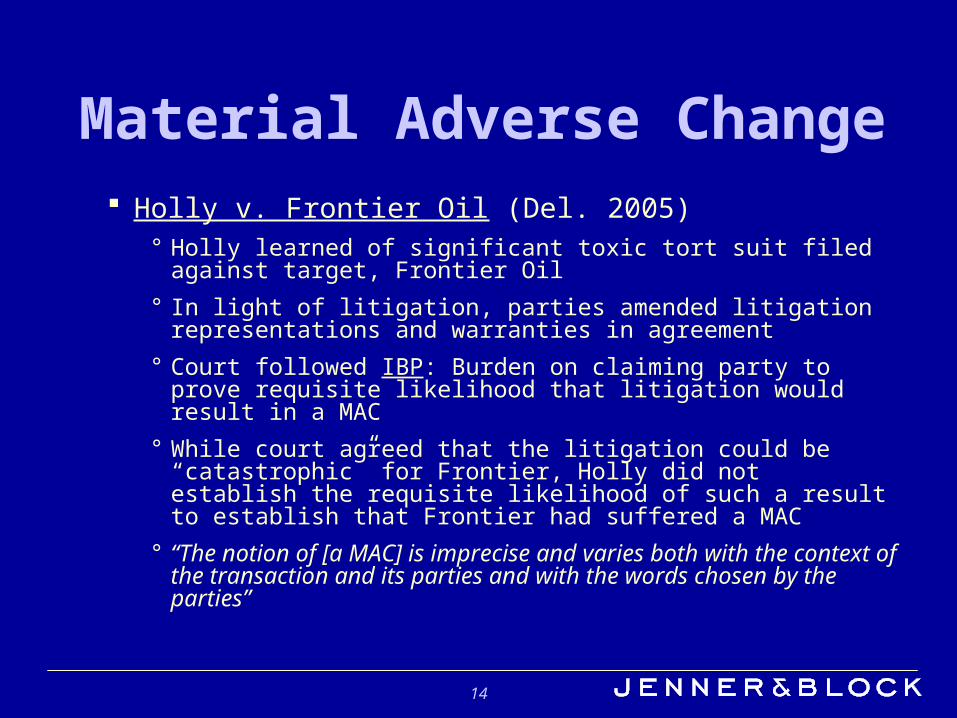

Material Adverse Change Holly v. Frontier Oil (Del. 2005)

° Holly learned of significant toxic tort suit filed against target, Frontier Oil° In light of litigation, parties amended litigation representations and

warranties in agreement° Court followed IBP: Burden on claiming party to prove requisite likelihood

that litigation would result in a MAC° While court agreed that the litigation could be “catastrophic” for Frontier,

Holly did not establish the requisite likelihood of such a result to establish that Frontier had suffered a MAC

° “The notion of [a MAC] is imprecise and varies both with the context of the transaction and its parties and with the words chosen by the parties”

15

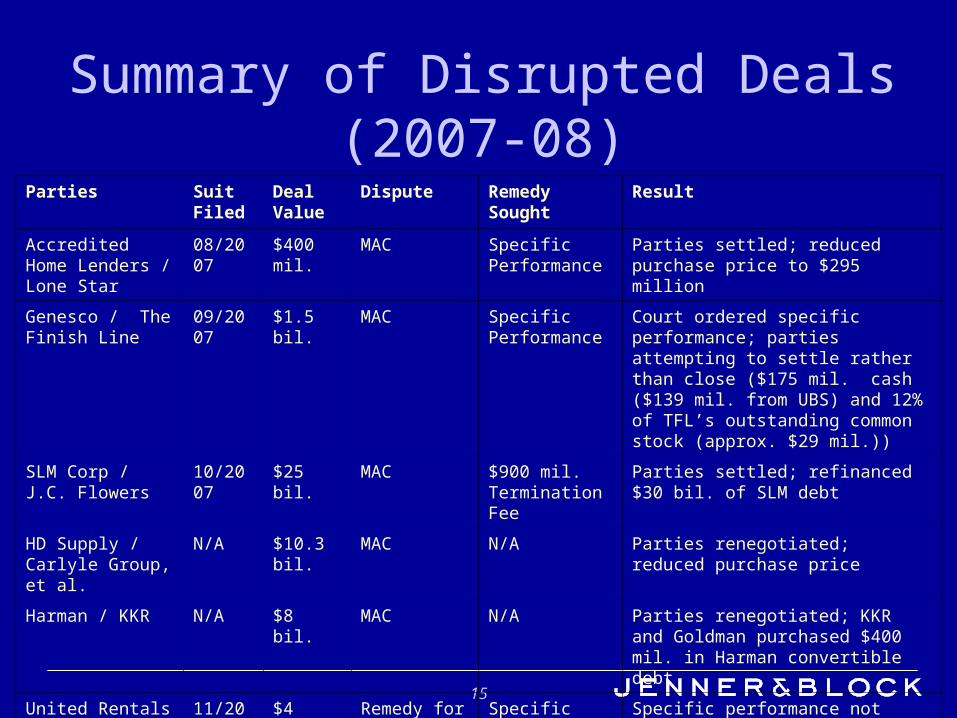

Summary of Disrupted Deals (2007-08)Parties Suit

FiledDeal Value

Dispute Remedy Sought Result

Accredited Home Lenders / Lone Star

08/2007 $400 mil. MAC Specific Performance

Parties settled; reduced purchase price to $295 million

Genesco / The Finish Line

09/2007 $1.5 bil. MAC Specific Performance

Court ordered specific performance; parties attempting to settle rather than close ($175 mil. cash ($139 mil. from UBS) and 12% of TFL’s outstanding common stock (approx. $29 mil.))

SLM Corp / J.C. Flowers

10/2007 $25 bil. MAC $900 mil. Termination Fee

Parties settled; refinanced $30 bil. of SLM debt

HD Supply / Carlyle Group, et al.

N/A $10.3 bil. MAC N/A Parties renegotiated; reduced purchase price

Harman / KKR N/A $8 bil. MAC N/A Parties renegotiated; KKR and Goldman purchased $400 mil. in Harman convertible debt

United Rentals / Cerberus

11/2007 $4 bil. Remedy for breach

Specific Performance

Specific performance not available; $100 mil. termination fee

3Com / Bain Capital N/A $2.2 bil. Termination Fee N/A Pending

16

Material Adverse Change

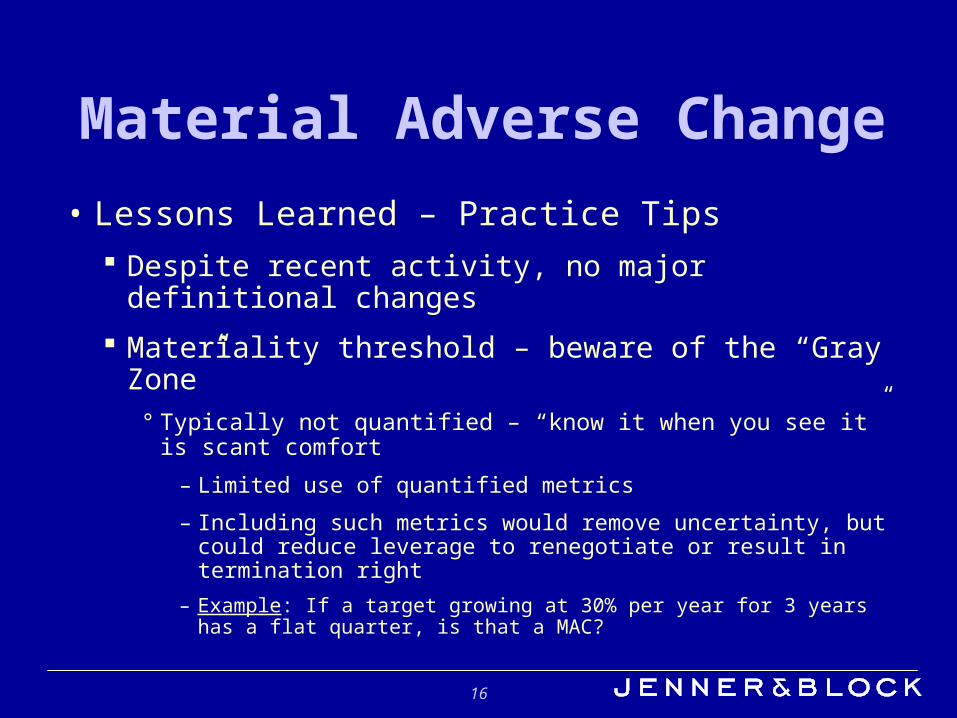

• Lessons Learned – Practice Tips Despite recent activity, no major definitional changes

Materiality threshold – beware of the “Gray Zone”° Typically not quantified – “know it when you see it” is scant comfort

– Limited use of quantified metrics

– Including such metrics would remove uncertainty, but could reduce leverage to renegotiate or result in termination right

– Example: If a target growing at 30% per year for 3 years has a flat quarter, is that a MAC?

17

Material Adverse Change• Rely on the MAC for the truly unknown facts, but use

specific additional conditions/requirements to address the known risks

– e.g., Consider requirement to satisfy certain hurdles/conditions– Use MAC out as a backstop rather than the primary line of defense

Facts and circumstances analysis– Interpret MAC in light of “negotiating realities”

Anticipate the introduction of extrinsic evidence to interpret an ambiguous MAC clause

– Be careful what you ask for and do not get

Additional contract provisions will also be considered– e.g., Genesco duration of cure period

18

Specific Performance• Other Drafting Considerations

Reverse termination fees began as private equity buyers began to eliminate financing contingencies (which many strategic buyers don’t need)

° Reverse termination fees were payable to target/seller if deal didn’t close because financing wasn’t available

Quickly evolved into broader limitation on private equity buyers’ liability if transaction didn’t close for any reason

Exclusivity became important because private equity buyers would not put “full, faith and credit” up to support a deal unless burn was capped

Led to questions about circumstances under which a private equity buyer could walk from deal for any reason

Practices/drafting varied° Some made it clear contract was essentially an option

19

Specific Performance° Others were less clear – included payment as exclusive remedy but then

also included specific performance as well – inconsistent

° Others indicated target could specifically enforce obligations to draw financing and close but that the fee capped damages of sponsor if deal didn’t otherwise close

Specific Performance° MAC Cases (IBP, Frontier Oil, Genesco, etc.)

° Reverse Termination Fees - United Rentals v. RAM Holdings (Del. 2007)

– RAM (Cerberus subsidiary) sought to terminate transaction and pay break-up fee

20

URI v Cerberus: Forthright Negotiator

– Conflict based on provision which offered URI the “sole and exclusive remedy” of enforcing break-up fee

– Because the court held that (i) the language of the merger agreement presented a direct conflict between provisions relating to remedies and (ii) the evidence of negotiations was too muddled to clearly support URI’s interpretation of the relevant provisions, the court applied the so-called “forthright negotiator” principle to the two key provisions at issue

21

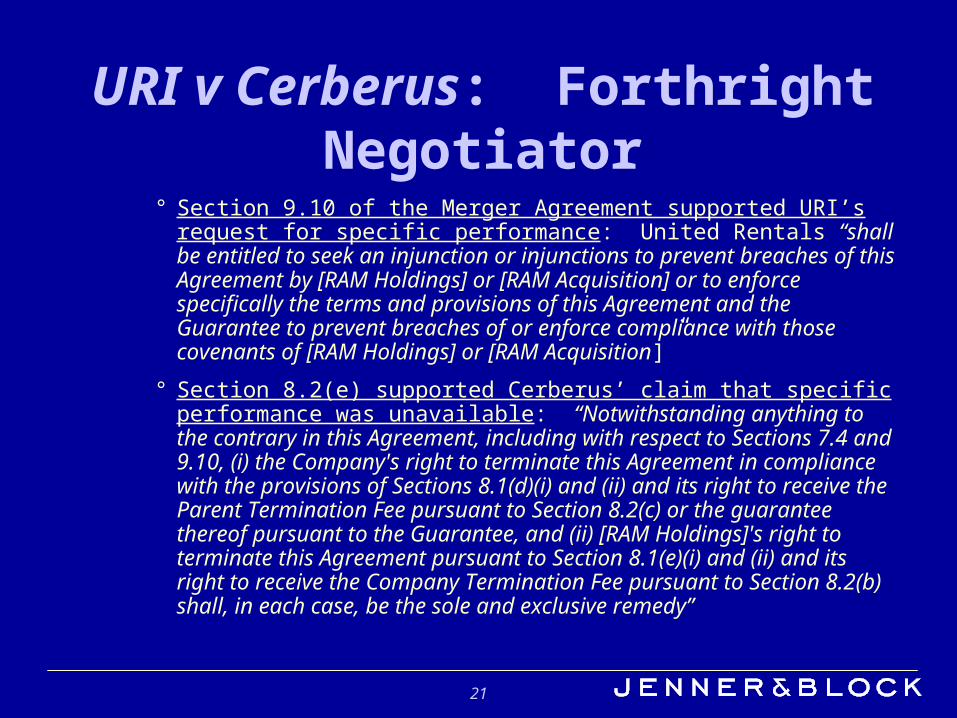

URI v Cerberus: Forthright Negotiator

° Section 9.10 of the Merger Agreement supported URI’s request for specific performance: United Rentals “shall be entitled to seek an injunction or injunctions to prevent breaches of this Agreement by [RAM Holdings] or [RAM Acquisition] or to enforce specifically the terms and provisions of this Agreement and the Guarantee to prevent breaches of or enforce compliance with those covenants of [RAM Holdings] or [RAM Acquisition]”

° Section 8.2(e) supported Cerberus’ claim that specific performance was unavailable: “Notwithstanding anything to the contrary in this Agreement, including with respect to Sections 7.4 and 9.10, (i) the Company's right to terminate this Agreement in compliance with the provisions of Sections 8.1(d)(i) and (ii) and its right to receive the Parent Termination Fee pursuant to Section 8.2(c) or the guarantee thereof pursuant to the Guarantee, and (ii) [RAM Holdings]'s right to terminate this Agreement pursuant to Section 8.1(e)(i) and (ii) and its right to receive the Company Termination Fee pursuant to Section 8.2(b) shall, in each case, be the sole and exclusive remedy”

22

URI v Cerberus: Forthright Negotiator

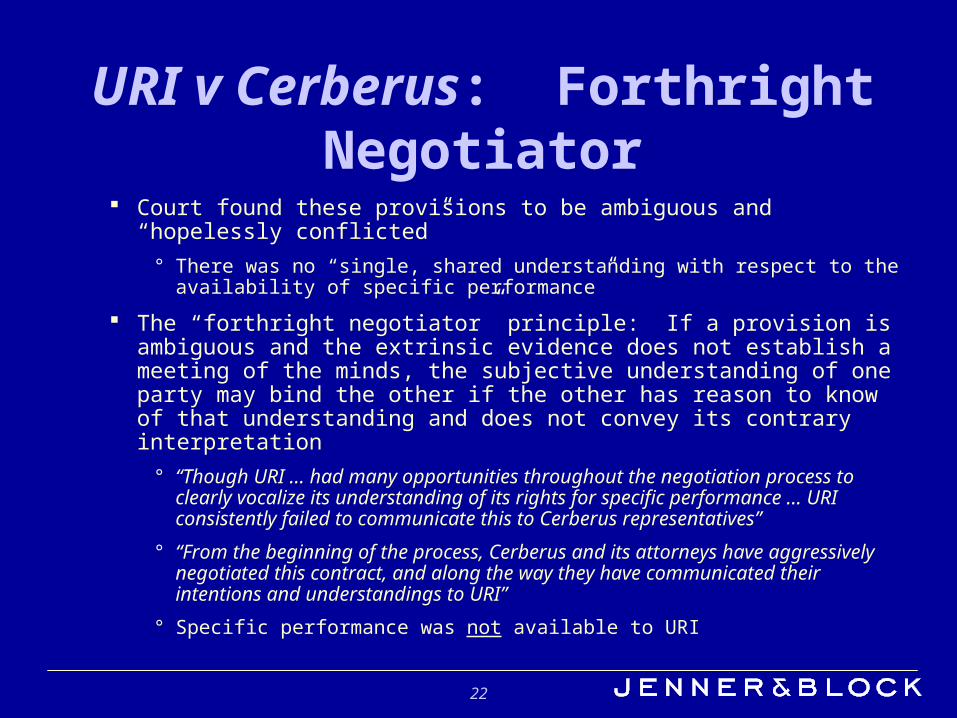

Court found these provisions to be ambiguous and “hopelessly conflicted”° There was no “single, shared understanding with respect to the availability of specific

performance”

The “forthright negotiator” principle: If a provision is ambiguous and the extrinsic evidence does not establish a meeting of the minds, the subjective understanding of one party may bind the other if the other has reason to know of that understanding and does not convey its contrary interpretation

° “Though URI … had many opportunities throughout the negotiation process to clearly vocalize its understanding of its rights for specific performance … URI consistently failed to communicate this to Cerberus representatives”

° “From the beginning of the process, Cerberus and its attorneys have aggressively negotiated this contract, and along the way they have communicated their intentions and understandings to URI”

° Specific performance was not available to URI

23

Best Efforts

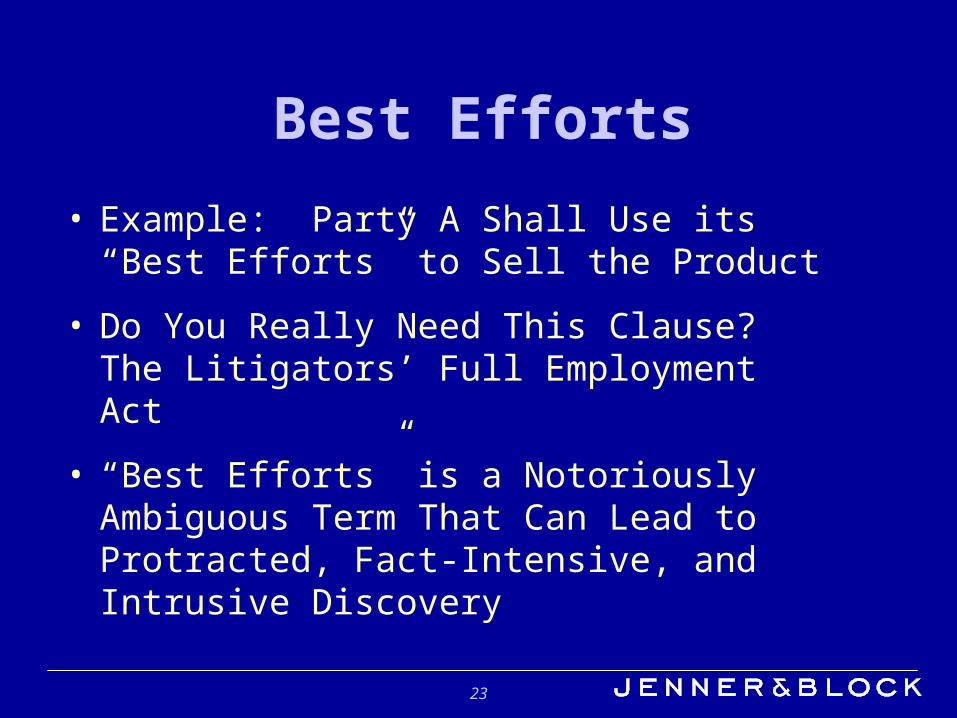

• Example: Party A Shall Use its “Best Efforts” to Sell the Product

• Do You Really Need This Clause? The Litigators’ Full Employment Act

• “Best Efforts” is a Notoriously Ambiguous Term That Can Lead to Protracted, Fact-Intensive, and Intrusive Discovery

24

Best Efforts Continued

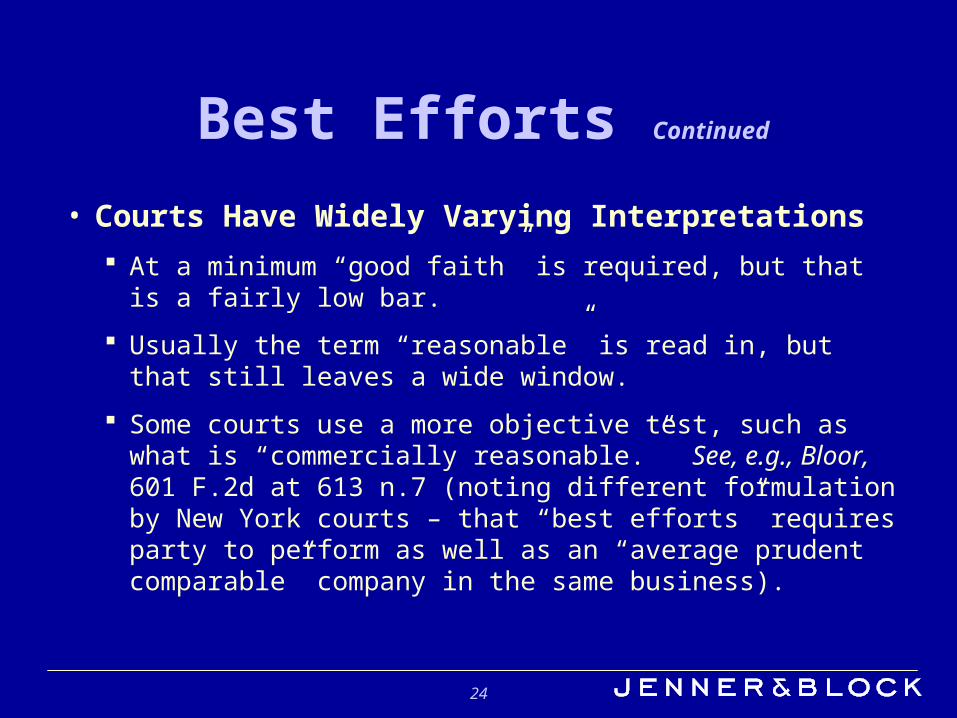

• Courts Have Widely Varying Interpretations

At a minimum “good faith” is required, but that is a fairly low bar.

Usually the term “reasonable” is read in, but that still leaves a wide window.

Some courts use a more objective test, such as what is “commercially reasonable.” See, e.g., Bloor, 601 F.2d at 613 n.7 (noting different formulation by New York courts – that “best efforts” requires party to perform as well as an “average prudent comparable” company in the same business).

25

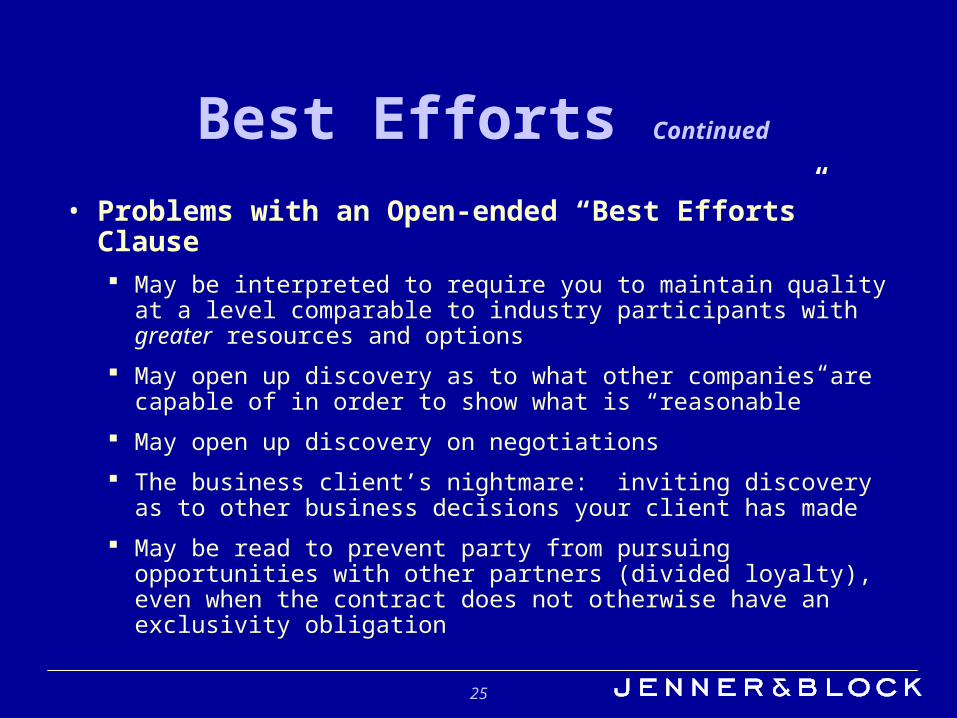

Best Efforts Continued

• Problems with an Open-ended “Best Efforts” Clause May be interpreted to require you to maintain quality at a level comparable to

industry participants with greater resources and options

May open up discovery as to what other companies are capable of in order to show what is “reasonable”

May open up discovery on negotiations

The business client’s nightmare: inviting discovery as to other business decisions your client has made

May be read to prevent party from pursuing opportunities with other partners (divided loyalty), even when the contract does not otherwise have an exclusivity obligation

26

Best Efforts Continued

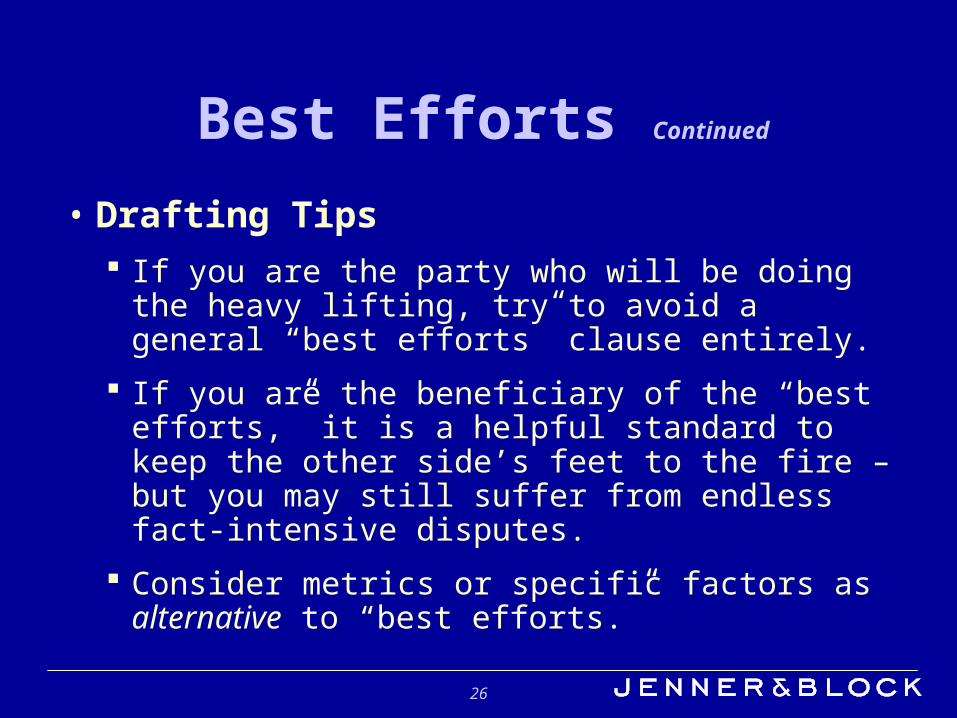

• Drafting Tips If you are the party who will be doing the heavy lifting,

try to avoid a general “best efforts” clause entirely.

If you are the beneficiary of the “best efforts,” it is a helpful standard to keep the other side’s feet to the fire – but you may still suffer from endless fact-intensive disputes.

Consider metrics or specific factors as alternative to “best efforts.”

27

Best Efforts Continued

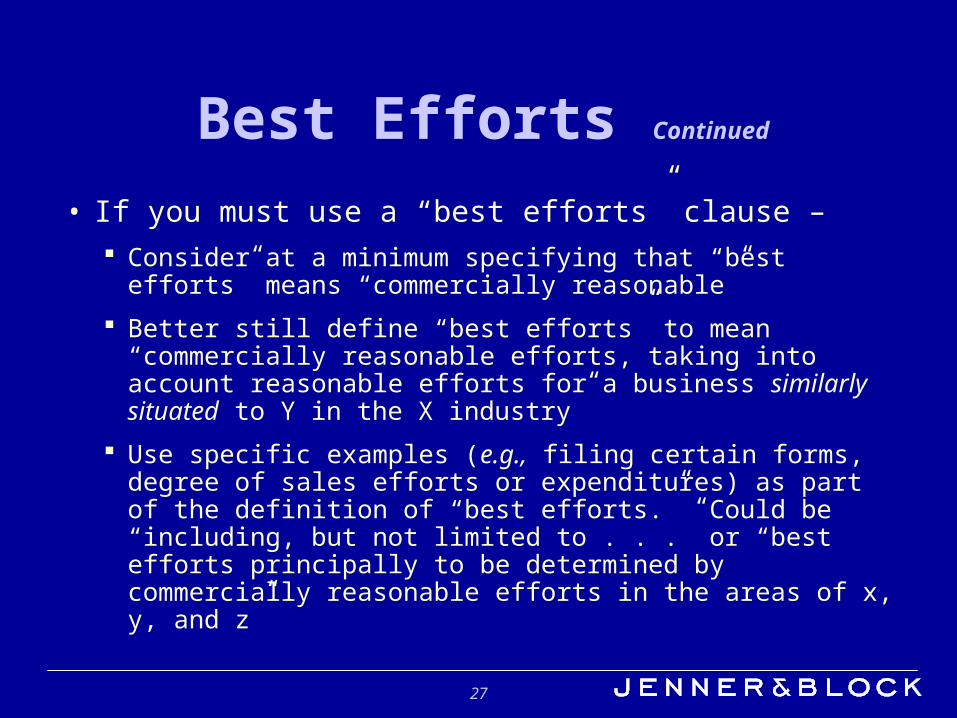

• If you must use a “best efforts” clause – Consider at a minimum specifying that “best efforts” means

“commercially reasonable”

Better still define “best efforts” to mean “commercially reasonable efforts, taking into account reasonable efforts for a business similarly situated to Y in the X industry”

Use specific examples (e.g., filing certain forms, degree of sales efforts or expenditures) as part of the definition of “best efforts.” Could be “including, but not limited to . . .” or “best efforts principally to be determined by commercially reasonable efforts in the areas of x, y, and z”

28

Best Efforts Continued

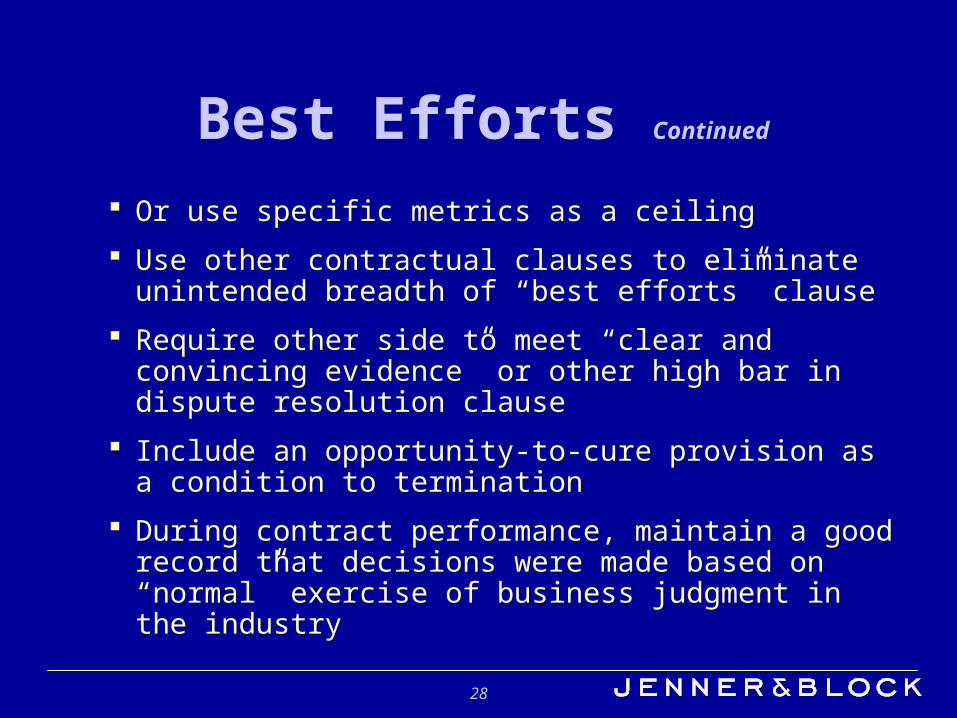

Or use specific metrics as a ceiling

Use other contractual clauses to eliminate unintended breadth of “best efforts” clause

Require other side to meet “clear and convincing evidence” or other high bar in dispute resolution clause

Include an opportunity-to-cure provision as a condition to termination

During contract performance, maintain a good record that decisions were made based on “normal” exercise of business judgment in the industry

29

Arbitration

• Pros and Cons of Arbitration Clauses

• Don’t Reinvent the Wheel for a Standard Clause

• Additional Drafting Details to Consider Mandatory Mediation

Mandatory Expertise/Background of Panelists

Confidentiality

Specifying Scope of Discovery

30

Arbitration Continued

Time Limits/Schedule

Place of Arbitration

Allocation of Costs and Fees

Limitations on Damages

Form of Award/Decision

Limitations on Types of Claims

31

Indemnification and Limitationsof Liability

• Tips from a Litigator’s Perspective

• Don’t assume you cannot get a limitation on consequentials, incidentals, etc.

• Beware of “form” contracts or lopsided negotiations with one-sided indemnification clauses. Courts can enforce agreements where you have agreed to indemnify the other side for losses, even when the other side is negligent.

• Specify who is being indemnified (e.g., in addition to contracting party, its officers, directors, employees, agents)

32

Indemnification and Limitationsof Liability Continued

• Specify the conduct triggering indemnification; e.g., any act or omission arising out of seller’s performance, including its subcontractors? Only for breach of contract?

• Watch for ambiguity as to the type of indemnification or types of losses to which indemnification applies – e.g., for personal injury, property damage, attorneys’ fees and duty to defend/costs of defense, economic loss?

• Watch for damages you thought were excluded coming in through the back door – e.g., in a termination clause, or an additional form contract incorporated by reference.

• Consider caps – applying a specific cap to a set of specific indemnifiable events.

Recommended