© 2004 Hewlett-Packard Development Company, L.P. The information contained herein is subject to change without notice

Winning and growing

Peter BlackmoreExecutive Vice President Customer Solutions Group

Customer Solutions Group

Customer focus

Simplicity

Growth

• Aligned by customer segment

• One face to the customer

• Power of portfolio leveraged across region and country

• Growth plans by country, by segment, by account

• Managing Director role

• Greater share of wallet from accounts

• Volume direct growth, balanced with strong channel

IT partner for the next generation

CSG – structured for growth by…

Segment

Customer

Country/region

Partner

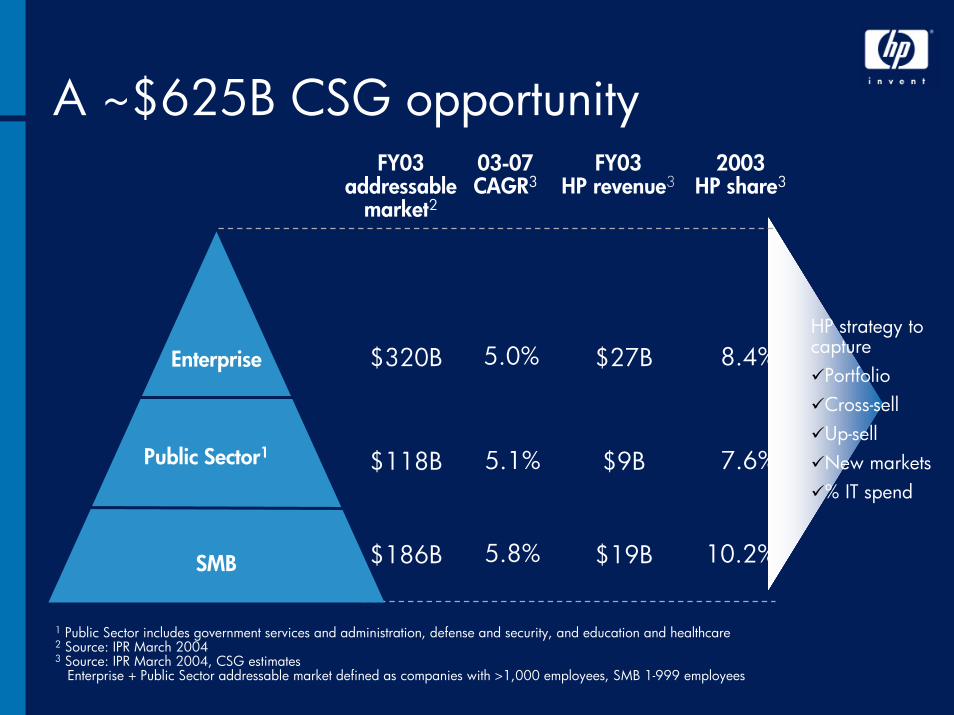

A ~$625B CSG opportunityFY03

HP revenue32003

HP share3

$27B

$9B

8.4%

7.6%

03-07CAGR3

10.2%

5.0%

5.1%

5.8% $19BSMB

Enterprise

Public Sector1

FY03addressable

market2

$320B

$118B

$186B

HP strategy tocapture

PortfolioCross-sellUp-sellNew markets% IT spend

1 Public Sector includes government services and administration, defense and security, and education and healthcare2 Source: IPR March 20043 Source: IPR March 2004, CSG estimates

Enterprise + Public Sector addressable market defined as companies with >1,000 employees, SMB 1-999 employees

Segment growth: Enterprise

Network andService Providers

Financial Services Industry

Manufacturing Regional industries

75% of enterprise revenue in FY03

• Network equipment providers

• Service providers • Media & entertainment

• Banking• Payments• Financial markets • Insurance

• Automotive• High tech• Life sciences• Oil & gas• Consumer goods• Aerospace and

defense

• Retail • Utilities • Logistics

Adaptive Enterprise

Unique vertical plus horizontal offerings taken to market with industry expertise

Drive existing horizontal offerings

Examples

Focus on key industries

Enterprise addressable market $320B in 03 and growing at 5.0%

3950

87105

108

125

108860

100

200

300

400

2003 2007

CAGR

$320B

$389B

4.9%

3.8%

6.6% N&SP

Mfg

Regional

WW Enterprise segment

5.8% FSI

HP positioned to win

• HP is Walmart’s technology supplier of the year

• 50% of SAP implementations and 80% of world’s semiconductor fabs run on HP

• 80M people and 35 operators depend on HP OpenCall

• HP powers 100+ stock exchanges and 2 of every 3 credit card transactions

Source: IPR March 2004

Enterprise = companies >1,000 employees

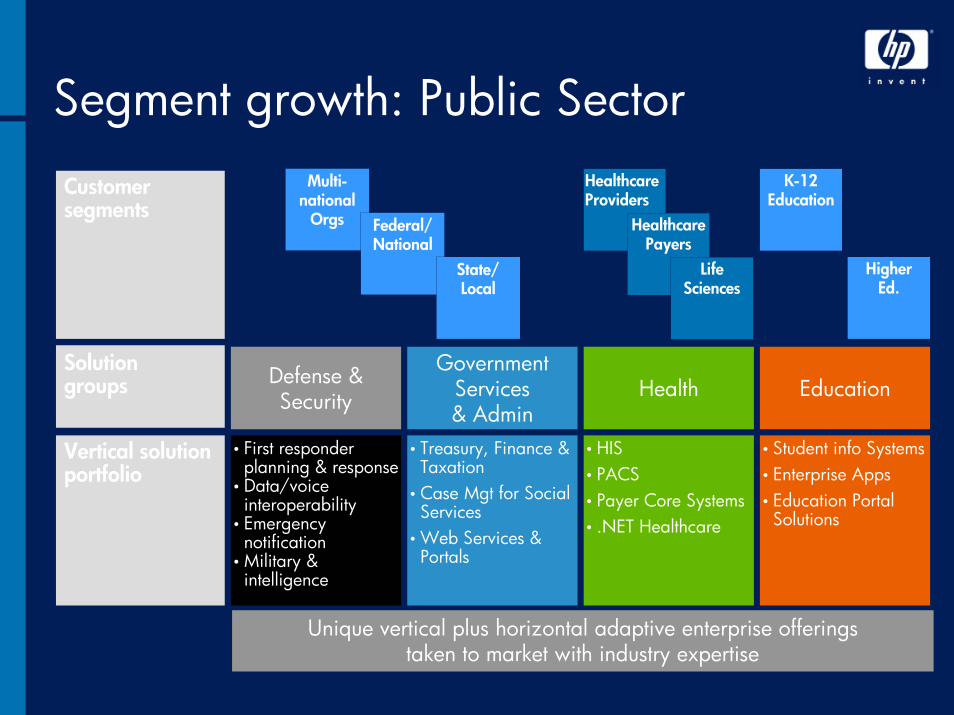

Segment growth: Public SectorK-12

Education

HigherEd.

HealthDefense & Security

Government Services & Admin

Education

• First responder planning & response

• Data/voice interoperability

• Emergency notification

• Military & intelligence

• Treasury, Finance & Taxation

• Case Mgt for Social Services

• Web Services & Portals

Customersegments

• HIS • PACS• Payer Core Systems• .NET Healthcare

• Student info Systems• Enterprise Apps• Education Portal

Solutions

Multi-national

Orgs Federal/National

State/ Local

Healthcare Providers

Healthcare Payers

Life Sciences

Solutiongroups

Vertical solutionportfolio

Unique vertical plus horizontal adaptive enterprise offerings taken to market with industry expertise

Public Sector addressable market $118B in 03 and growing at 5.1%

HP positioned to win• Classroom 2000 in Northern Ireland

• Healthcare Integrated Delivery Network for U.S. Department of Veteran Affairs (one of the largest such networks in existence)

• Over 80% of the U.S. 911 Emergency call centers (Chicago, NYC)

• White House, Kremlin, British Cabinet, Vatican City, United States Postal Service

Plan to accelerate• Improve account coverage

• Enhance market presence• Build critical partnerships

• Strengthen service capabilities

7391

12

1433

37

2003 2007

CAGR5.1%

Government

Healthcare

Education

$118B

$142B

Source: IPR March 2004

Segment growth: SMBCustomer needs Smart Office programs & solutions

Integrated infrastructure• File and Print• Communication & Collaboration• Ready Office• Business Protection• SMB Servers + Storage• Smart Services + SupportJoint offerings with• Microsoft• Intuit• SAPNew offerings to drive growth• Office communications ($4B mkt)*• Security ($5.1B mkt)*

*Source: E-Marketer, In Stat, Forrester, EC Security Briefing; IPR

Reliability“There is enough risk in day to day business…I don’t need technology risk, too.”

Ease of ownershipAllowing daily focus on the business, not the technology

Expertise and supportAddressing gaps in internal staff bandwidthand capabilities

Standardization and integrationEnabling better investment protection and leverage of prior technology purchase decisions

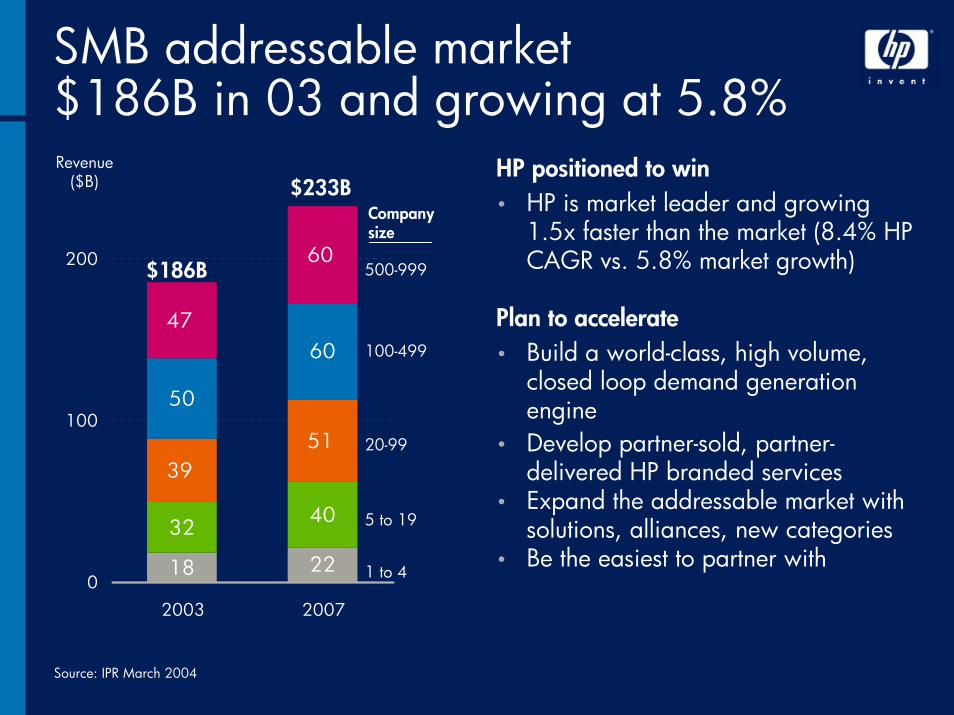

SMB addressable market $186B in 03 and growing at 5.8%

18 22

32 40

3951

50

6047

60

0

100

200

2003 2007

Revenue($B) $233B

500-999

100-499

20-99

5 to 19

1 to 4

$186B

Companysize

HP positioned to win• HP is market leader and growing

1.5x faster than the market (8.4% HP CAGR vs. 5.8% market growth)

Plan to accelerate• Build a world-class, high volume,

closed loop demand generation engine

• Develop partner-sold, partner-delivered HP branded services

• Expand the addressable market with solutions, alliances, new categories

• Be the easiest to partner with

Source: IPR March 2004

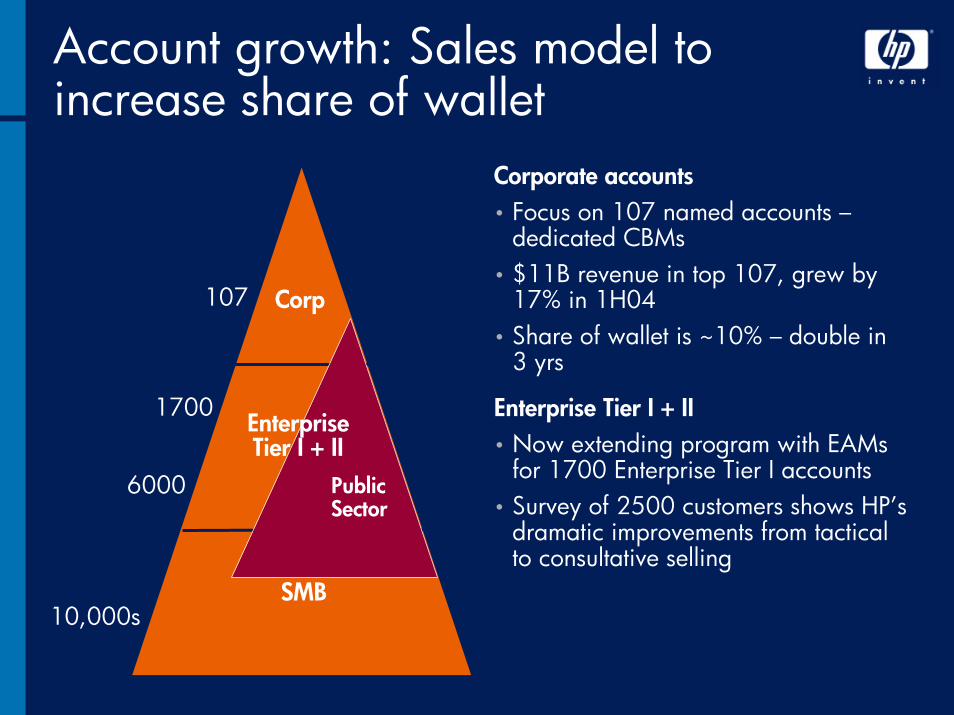

Account growth: Sales model to increase share of wallet

SMB

Corp

PublicSector

Corporate accounts• Focus on 107 named accounts –

dedicated CBMs• $11B revenue in top 107, grew by

17% in 1H04• Share of wallet is ~10% – double in

3 yrs

Enterprise Tier I + II • Now extending program with EAMs

for 1700 Enterprise Tier I accounts• Survey of 2500 customers shows HP’s

dramatic improvements from tactical to consultative selling

107

1700

6000

EnterpriseTier I + II

10,000s

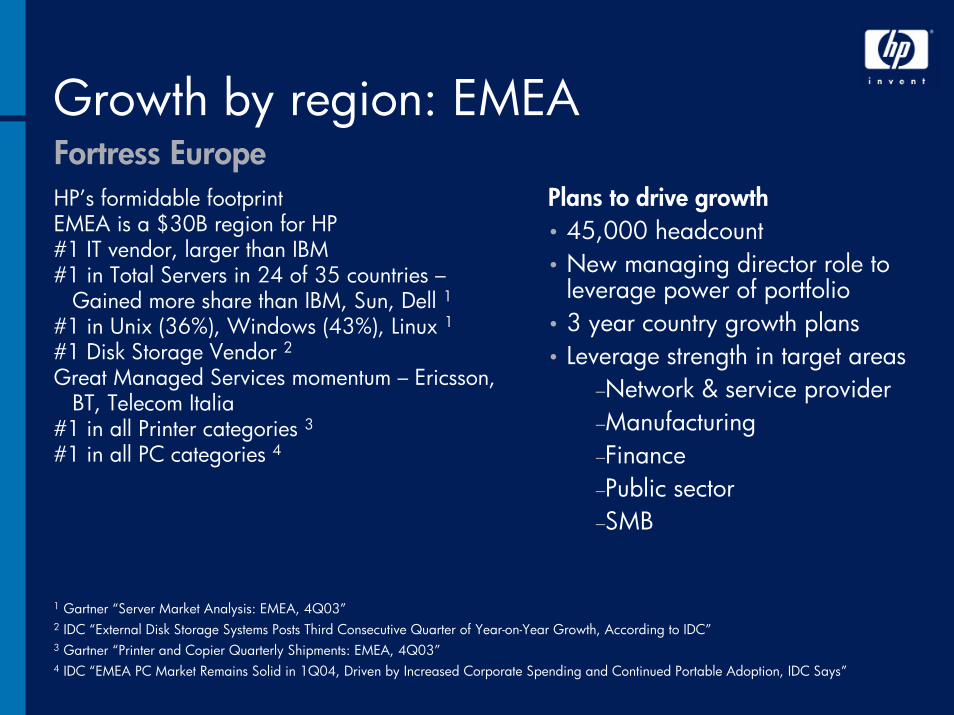

Growth by region: EMEAFortress EuropeHP’s formidable footprintEMEA is a $30B region for HP#1 IT vendor, larger than IBM#1 in Total Servers in 24 of 35 countries –

Gained more share than IBM, Sun, Dell 1#1 in Unix (36%), Windows (43%), Linux 1#1 Disk Storage Vendor 2Great Managed Services momentum – Ericsson,

BT, Telecom Italia#1 in all Printer categories 3#1 in all PC categories 4

Plans to drive growth• 45,000 headcount• New managing director role to

leverage power of portfolio• 3 year country growth plans• Leverage strength in target areas

–Network & service provider–Manufacturing–Finance–Public sector–SMB

1 Gartner “Server Market Analysis: EMEA, 4Q03”2 IDC “External Disk Storage Systems Posts Third Consecutive Quarter of Year-on-Year Growth, According to IDC”3 Gartner “Printer and Copier Quarterly Shipments: EMEA, 4Q03”4 IDC “EMEA PC Market Remains Solid in 1Q04, Driven by Increased Corporate Spending and Continued Portable Adoption, IDC Says”

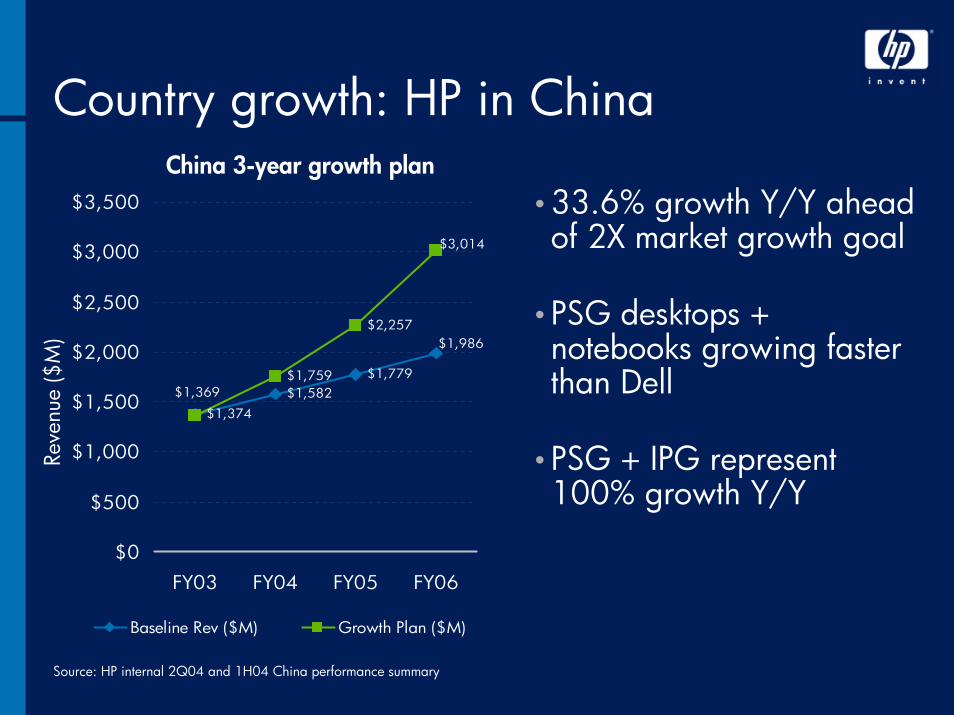

Country growth: HP in China

$1,374$1,582

$1,779$1,759

$2,257$1,986

$3,014

$1,369

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

$3,500

FY03 FY04 FY05 FY06

Baseline Rev ($M) Growth Plan ($M)

China 3-year growth plan

Reve

nue

($M

)

•33.6% growth Y/Y ahead of 2X market growth goal

•PSG desktops + notebooks growing faster than Dell

•PSG + IPG represent 100% growth Y/Y

Source: HP internal 2Q04 and 1H04 China performance summary

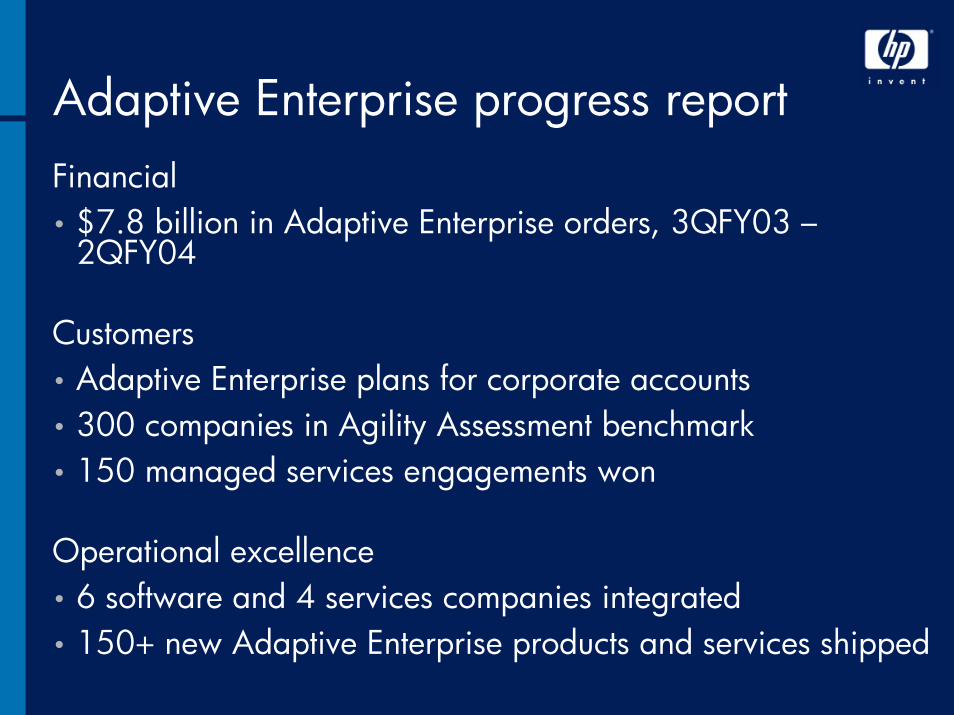

Adaptive Enterprise progress reportFinancial• $7.8 billion in Adaptive Enterprise orders, 3QFY03 –

2QFY04

Customers• Adaptive Enterprise plans for corporate accounts• 300 companies in Agility Assessment benchmark • 150 managed services engagements won

Operational excellence• 6 software and 4 services companies integrated • 150+ new Adaptive Enterprise products and services shipped

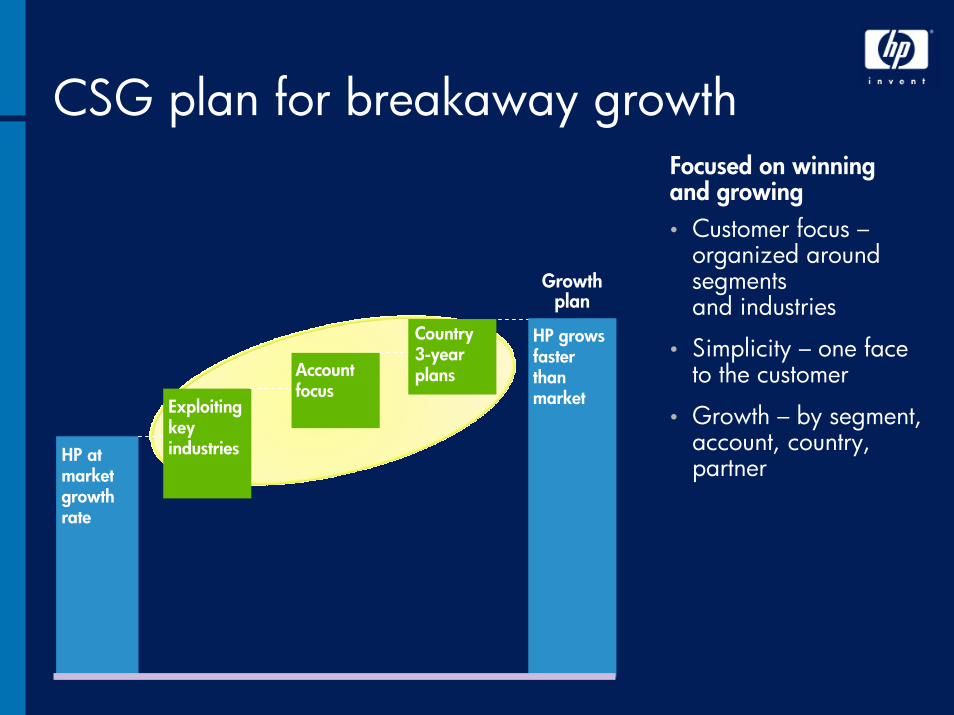

CSG plan for breakaway growth

Growthplan

Exploiting keyindustries

Country 3-yearplans

HP grows faster than market

Accountfocus

HP at market growth rate

• Customer focus –organized around segments and industries

• Simplicity – one face to the customer

• Growth – by segment, account, country, partner

Focused on winningand growing

Recommended