Yield Curve Predictorsof Foreign Exchange Returns∗

Andrew Ang†

Columbia University and NBER

Joseph S. Chen‡

UC Davis

Preliminary Incomplete Version: 4 September 2009Do not circulate

JEL Classification: E43, F31, F37, G15, G17Keywords: carry trade, exchange rates, predictability, term structure,

uncovered interest rate parity

∗We thank Bob Hodrick and Antti Ilmanen for helpful discussions.†Columbia Business School, 3022 Broadway 413 Uris, New York NY 10027, ph: (212) 854-9154;

email: [email protected]; WWW: http://www.columbia.edu/∼aa610.‡Graduate School of Management, University of California, Davis, One Shields Avenue, 3216 Gal-

lagher Hall, Davis, CA 95616; ph: (530) 752-2924; email: [email protected]; WWW: http://www.jc-finance.com

Yield Curve Predictors of Foreign Exchange Returns

Abstract

We find there is significant information in foreign countries’ yield curves that is useful

for predicting foreign exchange returns in the cross-section. This predictive information goes

beyond the violation of uncovered interest parity and the carry trade. We investigate cross-

sectional foreign exchange rate predictability using both a portfolio formation perspective and

a cross-sectional panel regression framework. Differences across countries of both the levels

of interest rates and the changes in interest rates have significant ability to forecast the cross-

section of future currency returns. Furthermore, we find additional predictive information in the

slope of the yield curve. Our results are consistent with no-arbitrage models that suggests factors

that determine the term structure of yields should also determine foreign exchange returns.

1 Introduction

In no-arbitrage models, the foreign exchange risk premium is driven by differences in risk

factors affecting the pricing kernels in each country.1 These factors are reflected in the term

structure of foreign and domestic bond prices and the conditional dynamics of yield curves over

time. The vast majority of studies examining the predictability of foreign exchange returns use

only the very shortest maturities of bond yields, like the differences between two countries in

their one-month or three-month interest rates (also called carry).2 However, it is well known

that there is more than one risk factor affecting interest rates and many modern term structure

models, like Dai and Singleton (2000) among many others, specify the pricing kernel to contain

at least three or more factors. Thus, the entire term structure of interest rates in each country and

their dynamic behavior over time should contain observable information in addition to short-

term interest rate differentials that affects foreign exchange returns.

Our paper emphasizes the restrictions on the joint behavior between currencies and term

structure of interest rates. The focus in this paper is to examine the predictive power of infor-

mation in the shapes and dynamics of the term structure for predicting future foreign exchange

returns. We take as a benchmark case the difference in short-term interest rates, which determine

the well-known violations from the uncovered interest rate parity (UIP) and the profitability of

the carry trade. Then, motivated from multi-factor term structure models, we examine several

other predictors constructed from the term structure of yields.

In particular, we document the predictive ability present in levels, changes and slopes of the

cross-section of yield curves. For instance, a simple currency portfolio constructed based on

changes in short-term interest rate differentials across countries yields an annualized Sharpe ra-

tio of 0.683 and exhibits no significant skewness. As a comparison, a simple currency portfolio

based on the levels of the short rate (the carry trade portfolio) yields an annualized Sharpe ratio

of 0.870, but exhibits significant negative skewness. A currency portfolio based on changes

in long-term bond yields also exhibit a substantial Sharpe ratio of 0.502. Moreover, these

portoflios are not significantly correlated with each other. We verify this predictability in a

panel regression framework as well.

1 Earliest paper to note this relation is Fama (1984).2 There is a huge literature documenting deviations from the Unbiasedness Hypothesis where differences in

short rates, or equivalently forward rates, predict future exchange rates. Hodrick (1988), Lewis (1995) and Engel

(1996) are survey articles of the early literature. Sarno (2005) is a more recent update. This literature is exclusively

time-series studies, whereas we investigate the cross-sectional relations.

1

One notable feature of our empirical analysis is that we take a cross-sectional approach

to examine foreign exchange predicability as opposed to the more commonly examined time-

series predictability regressions in the literature. The cross-sectional approach lets us get closer

to examining foreign exchange predictability in a no-arbitrage framework. We show our for-

eign exchange predictability using both a portfolio formation framework and a cross-sectional

panel regression. Our results readily illustrates what a hypothetical arbitraguer would face. In

contrast, a time-series approach has the disadvantage that it does not necessarily translate to a

practical implementation by an arbitraguer.

To provide a motivating theoretical framework for interpreting our empirical results, we

illustrate a series of models in which factors that determine the term structure also impacts the

foreign exchanges returns. We consider various models commonly used in the term structure

literature and illustrate the models’ implications on foreign currency exchange returns. Our

main message is that any factor that affects the term structure of yields may also forecast foreign

exchange rates. We emphasize the predictive ability of the levels, the changes, and the slopes

of the yield curve. However, we do not take a stance on which model, if any, fits the data. We

only note that our foreign exchange predictability results we find in data are still consistent with

no-arbitrage pricing.

Our paper is structured as follows. Section 2 provides a brief summary of related paper. We

provide a motivation theoretical framework for our empirical investigation in Section 3. Section

4 describes our data and provides summary statistics. Section 5 considers currency returns from

a portfolio framework. We present our main empirical results in Section 6. Section 7 concludes.

2 Related Literature

This section is incomplete

Different horizons – only examined previously in time-series contexts, e.g. Chinn (2006).

FX portfolios – Burnside et al. (2006), Lustig, Roussanov and Verdelhan (2008)

Balduzzi et al. (1996) three factor model – level, central tendency, conditional volatility

Examined in the context of a general affine model by Dai and Singleton (2000).

Macro predictors of the yield curve – ignore. Ref Ang and Piazzesi (2003). Taylor rules in

ER’s literature Molodtsova and Papell (2008), Wang and Wu (2009). Other macro fundamen-

tals, long history. Engel, Mark and West (2007) differentials of macro variables. Cite Engle and

West (2005).

2

Literature on no-arbitrage term structure models of currency pricing Fama (1984), Backus,

Foresi and Telmer (2001), Brandt and Santa-Clara (2002 , Hodrick and Vassalou (2002), Bansal

(1997), Ahn (2004), Dong (2006), Graveline (2006), All two-country models.

Most related to Boudoukh, Richardson and Whitelaw (2006) – time series only on long-

maturity forward rates, equivalent to using information in long yields. Also Chen and Tsang

(2009) using level, slope and curvature constructed from splines.

Underreaction story? Burnside, Eichenbaum and Rebelo (2007) and Gourinchas and Tornell

(2004)

Changes in short rates – Ilmanen and Sayood (1998, 2002). In industry models, see John

Normand, JP Morgan.

Look at skewness of portfolios – Jurek (2008), Brunnermeier, Nagel and Pedersen (2009)

3 Motivating Framework

Under no-arbitrage conditions there exists a stochastic discount factor or pricing kernel, Mt+1,

which prices any payoff Pt+1 at time t+ 1 so that the price Pt at time t satisfies

Pt = Et[Mt+1Pt+1]. (1)

In particular, the price of a n-period zero coupon bond, P (n)t , is given by

P(n)t = Et[Mt+1P

(n−1)t+1 ] (2)

and the price of the one-period bond is simply the one-period risk-free rate, rt,

P(1)t = exp(−rt) = Et[Mt+1]. (3)

The pricing kernel embodies risk premiums, which potentially vary over time. Suppose the

domestic pricing kernel takes the form

Mt+1 = exp(−rt − 1

2λ2t − λtεt+1

), (4)

where λt is a time-varying price of risk which prices the shock to the short rate, εt+1. In our

analysis we specify all our shocks to be N(0, 1) and uncorrelated with each other. The price of

risk, λt, is potentially driven by multiple factors. Time-varying prices of risk give rise to time-

varying risk premia on long-term bonds. An enormous body of previous research has found

that priced risk factors include interest rate factors like the level and slope of the yield curve

3

and other yield curve variables, in addition to macro variables like inflation and output (see the

summary of affine term structure models by Piazzesi, 2003). In our exposition we concentrate

on yield curve factors.

We assume a similar pricing kernel in foreign country i:

M it+1 = exp

(−rit − 1

2(λit)

2 − λitεit+1

). (5)

The foreign pricing kernel prices all bonds in the foreign country through a similar relation to

equation (2),

Pi,(n)t = Et[M

it+1P

i,(n−1)t+1 ]

where P i,(n)t is the time t price of the foreign n-period zero coupon bond denominated in foreign

currency.

Let the spot exchange rate Sit at time t express the amount of U.S. dollars per unit of foreign

currency i. Increases in Sit represent an appreciating foreign currency relative to a depreciating

US dollar. Under complete markets the exchange rate change is the ratio of the pricing kernels

in the foreign and domestic country:

Sit+1

Sit=M i

t+1

Mt+1

, (6)

which is derived by many authors including Bekaert (1996), Bansal (1997), and Backus, Foresi

and Telmer (2001). We denote natural logarithms of our variables as sit+1 = logSit+1, mit+1 =

logM it+1 and mt+1 = logMt+1 The rate of foreign currency appreciation relative to US dollar ,

∆sit+1, is given by

∆sit+1 = sit+1 − sit = mit+1 −mt+1

= rt − rit + 12(λ2

t − (λit)2) + λtεt+1 − λitεit+1. (7)

Under this setting the foreign exchange risk premium of the ith currency, rpit, is half the differ-

ence in the spread of the conditional variances of the domestic and foreign pricing kernels:

rpit = Et(∆sit+1 + rit − rt) = 1

2(λ2

t − (λit)2). (8)

The risk premium, rpit, is the expected return to purchasing a foreign currency, investing the

proceeds in a foreign bond for one period earning the foreign interest rate, and then converting

back to domestic currency, which is given by Et[∆sit+1 + rit], in excess of investing in the US

one-period bond, which is given by rt. Note that uncovered interest rate parity (UIP) assumes

that the right-hand side of equation (8) is zero. In UIP, if foreign interest rate is greater than

4

the US interest rate, rit > rt , then the foreign currency is expected to depreciate. However,

equation (8) shows that any factor affecting the prices of domestic or foreign bonds potentially

has the ability to predict foreign exchange excess returns.3

Equation (8) is the motivating framework for examining the predictability of various factors

which drive risk premia in domestic or foreign bond markets, which may also predict foreign

exchange risk premia. We begin by showing how the standard carry trade assumes a one-factor

model for the price of risk which is the same as the short rate in Section 3.1. Then, in sections

3.2-3.4 we extend the framework to allow for multiple factors driving the prices of risk. In

this richer environment long-term bond yields and other statistics capturing the dynamics of

the yield curve may be simple instruments to capture these additional risk factors. Our goal is

not to develop a complicated term structure model that jointly prices domestic and foreign term

structures and exchange rates, but rather to provide motivation of how various transformations

of the yield curve may serve as approximations of factors driving risk premia. We summarize

in Section 3.5.

3.1 Differentials in Short Rates

We start with a simple one-factor model of the yield curve, which dates back to at least Vasicek

(1977). We parameterize the short rate in the U.S. and foreign country as

rt+1 = θ + ρrt + σrεr,t+1

rit+1 = θ + ρrit + σrεit+1 (9)

where for simplicity we assume the same parameters in the U.S. and the foreign country.

Long-term bonds reflect the risk premiums. The price of a two-period bond is given by

P(2)t = Et[Mt+1Et+1[Mt+2]]

= Et

[exp

(−rt − 1

2λ2t − λtεr,t+1 − rt+1

)](10)

which simplifies to

P(2)t = exp(1

2σ2r − rt − θ − ρrt − σrλt).

The yield on the two-period bond is

y(2)t = −1

2logP

(2)t = −1

4σ2r + 1

2(rt + θ + ρrt) + 1

2σrλt, (11)

3 In incomplete markets it is possible that certain factors affect only exchange rate returns and not domestic or

foreign bond prices. For example, Brandt and Santa-Clara (2002) incorporate an additional risk factor to match

exchange rate volatility but this factor is not priced and does not affect foreign exchange risk premiums.

5

which can also be written as

y(2)t = Jensen’s term + EHt + 1

2σrλt, (12)

where the Jensen’s term is given by −14σ2r and the Expectations Hypothesis term, EHt, is the

average expected short rate over the maturity of the long bond,

EHt = 12(rt + Et[rt+1]) = 1

2(rt + θ + ρrt).

Ignoring the Jensen’s term, the long-term yield comprises an Expectations Hypothesis term plus

a risk premium term, 12σrλt. Positive risk premia with λt > 0 give rise to an upward-sloping

yield curve. Note that the form of a long-bond yield in equation (12) holds under very general

parameterizations of a short-rate and risk premium processes.

We assume that the price of risk in each country is driven by a global factor, zt, and the local

short rates. Specifically, we define the conditional variances of the pricing kernel to be4

λ2t = zt − λrt

(λit)2 = zt − λrit. (13)

This is similar to the multi-factor setup of Backus, Foresi and Telmer (2001), Ahn (2004), and

Brandt and Santa-Clara (2002). Domestic long-maturity yields reflect both the global and local

price of risk components.

The foreign exchange risk premium is given by a linear difference in short rates:

rpit = 12λ(rit − rt), (14)

which is the standard carry trade predictor of foreign exchange returns.5 The common global

risk factor is not present in the exchange rate risk premium because it affects both the domestic

and foreign pricing kernels symmetrically. Under the condition λ > 0 then high interest rates in

the U.S. would coincide with low foreign exchange excess returns on average giving a version

of the carry trade. An equally weighted portfolio of i = 1 . . . N currencies all with the same

parameters would have a risk premium of

rppt = 12λ(rit − rt),

4 Strictly speaking these prices of risk may be negative and the square root is not defined. This can be avoided

by changing equation (9) to a Cox, Ingersoll and Ross (1985) model. As our goal is to motivate different yield

curve variables, we ignore the possibility of non-positivity.5 The linear form is purely for simplicity and we discuss first-order approximations to the quadratic form in

equation (8) below.

6

where rit = 1N

∑rit is the average short rate across countries.

Note that although long-term yields reflect the risk premium in equation (11), long-term

bonds have no extra predictive power for exchange rate returns above short rates differentials in

equation (14). In fact, using long-term bonds would lead to less predictive power for exchange

rate returns because long-term bonds embed both the common risk factor zt and the local short-

rate factors whereas only local risk factors matter for exchange rate determination. In this

simple setting only differences in short rates are useful for predicting foreign exchange returns.

We now turn to a richer specification for risk premia where there will be a role for long-term

bonds and other yield curve transformations in predicting exchange rates.

3.2 Yield Curve Changes

We make one change to the setup that provides a role for past yield curve dynamics to influence

exchange rate returns. We change the short rate to depend on both a time-varying conditional

mean, θt, as well as past short rates:

rt+1 = θt+1 + ρrt + σrεt+1

θt+1 = θ0 + φθt + σθvt+1, (15)

with corresponding equations with the same parameter values for the foreign short rate. This is a

two-factor short rate model formulated by Balduzzi, Das and Foresi (1998). Time-varying con-

ditional means are also used with other factors by Balduzzi et al. (1996) and Dai and Singleton

(2000). An economic motivation for a stochastic mean is given by Kozicki and Tinsley (2001)

who argue that the long-term average shifts due to agents’ perceptions of long-term inflation or

monetary policy targets.

Suppose that prices of risk now depend on conditional mean, θt, rather than rt:

λ2t = zt − λθt

(λit)2 = zt − λθit. (16)

An economic motivation for this would be that the end-point to which interest rates are mean

reverting determines risk premia rather than the temporary fluctuations of rt. Then, foreign

exchange excess returns depend on differentials in conditional means:

rpit = 12λ(θit − θt). (17)

7

The conditional mean θt is unobserved and there are several ways to estimate its value. First,

θt is priced in long-term bonds with equation (12) now taking the form

y(2)t = Jensen’s term + EHt + 1

2σr√zt − λθt,

where the Expectations Hypothesis term is

EHt = 12(rt + θ0 + φθt + ρrt).

But, long-term bond yields also reflect short-term rate movements, rt, and global factors, zt,

in addition to providing information about θt. Thus, extracting information on θt requires a

potentially complicated term structure model – we do not pursue this avenue because we seek

to use simple statistics of the yield curve in cross-sectional tests and joint estimations of term

structure models across multiple countries are computationally extremely difficult.

A second way to estimate θt is to exploit the dynamics of the short rate. Note that

rt − ρrt−1 = θt + σrεt

and since ρ ≈ 1, we have

θt ≈ ∆rt − σrεt.

A similar expression will hold for country i. Now the foreign exchange risk premium in equa-

tion (17) can be approximated by

rpit ≈ λ(∆rit −∆rt) + εrp,it , (18)

where εrp,it = σr(εt − εit).

Suppose we hold a portfolio of i = 1 . . . N currencies each with identical parameters with

equal weights in each currency. Suppose that the ith country risk premium error, εrp,it , where is

diversifiable across countries

1

N

N∑i=1

εrp,it → 0 as N →∞.

This is guaranteed by the assumption of independent errors we assume. Then, the currency

portfolio would have an average excess return of

rppt ≈ λ(

∆rit −∆rt

)(19)

where

∆rit =1

N

N∑i=1

∆rit

8

is the average change in short rates across countries. Intuitively, short rate changes provide

information about persistent time-varying conditional means. If these factors are priced then

ranking on changes in short rates across currencies may lead to differences in expected returns.

In our empirical work we also consider changes in long-term bond yields and term spreads,

which we now motivate in terms of levels.

3.3 Long Yields and Term Spreads

Rather than the price of risk depending on short rate factors, several authors including Brennan,

Wang and Xia (2004) and Lettau and Wachter (2009), among others, have parameterized the

price of risk factor to itself be a time-varying latent process. Brandt and Kang (2004) provide

an empirical estimation of such a specification. In this case the long yield or term spreads and

changes in long yields potentially have forecasting power for exchange rates. To illustrate this

case assume the short rate is given by the one-factor model in equation (9) and the pricing kernel

is given by the same form as equation (4). We make one change and assume that the price of

risk is itself a latent process and follows

λt+1 = λ0 + δλt + σλut+1. (20)

with identical parameters for country i.6

From equation (8) the exchange rate risk premium depends on the latent λt values, which is

repeated here for convenience:

rpit = 12(λ2

t − (λit)2).

This is a quadratic form and for pedagogical exposition we employ a linearization. We can

write

λ2t = (λt − E[λt] + E[λt])

2

= (λt − E[λt])2 + 2E[λt](λt − E[λt]) + E[λt]

2.

From equation (20) we can write

λ2t = constant + quadratic +

2λ0

1− δλt, (21)

6 An alternative approach is to let rt depend on the level and term spread directly, as in Brennan and Schwartz

(1979) and Schaefer and Schwartz (1984). Our example makes an extreme case where exchange rates are only

predicted by long-term bonds and not by interest rates.

9

where the quadratic term is (λt − E[λt])2. Assuming the quadratic variation is small then

λ2t ≈ constant +

2λ0

1− δλt,

and we can approximate the risk premium as

rpit =λ0

1− δ(λt − λit). (22)

Exchange rate returns depend on prices of risk, but these prices of risk are not observed in

short rate dynamics. In fact, in this stylized case foreign exchange excess returns cannot be

predicted by short rates. Prices of risk show up in long-bond prices or term spreads, which take

the form

y(2)t = −1

4σ2r + 1

2((1 + ρ)rt + θ) + 1

2σrλt

for the long yield and

y(2)t − rt = −1

4σ2r + 1

2((1− ρ)rt + θ) + 1

2σrλt

for the term spread. In particular, since ρ ≈ 1, the term spread provides a direct estimate of λt:

y(2)t − rt ≈ constant + 1

2σrλt.

Thus, we can obtain an estimate of the exchange rate risk premium using term spreads:

rpit ≈2λ0

σr(1− δ)

((y

(2),it − rit)− (y

(2)t − rt)

). (23)

3.4 Interest Rate Volatility

We finally consider a case where interest rate volatility predicts foreign exchange risk premiums.

We take a two-factor model of the short rate where volatility is stochastic:

rt+1 = θ + ρrt +√vtεt+1

vt+1 = v0 + κvt + σv√vtηt+1. (24)

This is the model of Longstaff and Schwartz (1992) where the second factor is identified with

the conditional volatility of the short rate. A similar specification is used by Balduzzi et al.

(1996).

We let the pricing kernel now price fluctuations in the short rate volatility, ηt+1. Specifically,

we assume

Mt+1 = exp(−rt − 1

2λ2vvt − λv

√vtηt+1

), (25)

10

where we shut off any potential pricing of risk for regular short rate shocks, εt+1, to highlight the

role of volatility. Assuming country i has the same parameters, the exchange rate risk premium

is then given by

rpit = 12(λ2

v(vt − vit)). (26)

Thus, interest rate volatility potentially may affect foreign exchange returns.

3.5 Summary

In summary, the expected return for investing in foreign currencies depends on the spread in

conditional volatilities of each country’s stochastic discount factor. Conditional volatility of a

country’s stochastic discount factor affects the term structure of yields. Therefore, any factor

that affects the domestic term structure of yields may potentially also forecast foreign exchange

risk premiums. In addition to differential spreads in short rates, which is the traditional carry

trade, foreign exchange returns may potentially be predicted by changes in interest rates, long-

bond yields and term spreads, and interest rate volatility. We now examine the predictive power

in the cross section of these various term structure factors.

4 Data and Summary Statistics

4.1 Data

The data used in our analysis consists of a panel of 22 foreign currencies that are foreign relative

to the US. The currencies are divided into a set of G10 currencies (Australia, Canada, Switzer-

land, Germany, France, United Kingdom, Japan, Norway, New Zealand and Sweden) and a set

of non-G10 developed countries (Austria, Belgium, Denmark, Spain, Finland, Greece, Hong

Kong, Ireland, Italy, Netherlands, Portugal, Singapore).7 During the sample period we study,

the Euro was introduced and many currencies became defunct. To account for the introduction

of the Euro, we eliminate a currency once it joins the European single currency, with one ex-

ception. Since the Euro itself is a valid currency, we splice the data for Germany with the data

for Euro. Germany is the country with the largest GDP among the countries in the Euro, hence

we consider the German Deutsche Mark to be representative of the Euro.

7 In out study, a country is developed if it was considered ”developed” by Morgan Stanley Capital International

(MSCI) as of June 2007.

11

We gather short-term and long-term interest rate variables from Global Financial Data at a

monthly frequency. For our analysis, we collect short-term interest rates that currency traders at

major financial institutions might realistically trade at. So we use the interbank deposit rates as

our preferred measure of short rate. For each of our currencies, we take the one-month London

interbank offered rates (LIBOR) or equivalent interbank offered rates traded elsewhere. If an

interbank offered rate is not available for a currency, we supplement the data with that country’s

3-month government bill rate, also obtained from Global Financial Data.8 We denote the short

rate as rit. We also collect long-term interest rate using the 10-year government bond, where

available. If the 10-year government bond rate is not available, we use the 5-year government

bond rate.9 We denote the long-term interest rate as yit and refer to it as ’long rate’. To ensure

that at least 6 currencies are represented among the G10 currencies, we begin our sample in

January 1979. Our sample ends in May 2007 and represents 341 months in total.

We also convert our interest rate variables to interest rates relative to US interest rates.10 We

also collect US dollar LIBOR rates, denoted rt and US 10-year constant maturity government

bond rate, denoted yt. These interest rate differentials, rit−rt and yit−yt, are our main predictive

variables of interest. We also compute term spread differentials defined as (yit − yt) − (rit −rt), and refer to it as the ’term spread’. Finally, we compute monthly changes in interest rate

differentials, denoted as ∆(rit − rt), ∆(yit − yt) and ∆ [(yit − yt)− (rit − rt)]For each currency, we obtain the end-of-month exchange rate in terms of dollar price of one

unit of foreign currency from Thomson Financial’s Datastream International, which we denote

as Sit . We define excess FX return on currency i over the next month, denoted Πit+1, as

Πit+1 = Sit+1/S

it(1 + rit)− (1 + rt). (27)

Note that this is the profit from borrowing one USD at rt to purchase 1/Sit units of foreign

currency i and depositing the proceeds at rit.

8 G10 currencies for which we used the 3-month government bill rates to increase sample length are AUD,

CAD, NZD and SEK. Among non-G10 developed countries, they are ATS, ESP, ITL, NLG, PTE and SGD.9 G10 currencies for which we used the 5-year government bond rates are AUD, CAD, CHF, FRF, NZD and

SEK. Among non-G10 developed countries, they are ATS, BEF, DKK and GRD.10 The portfolio strategies below takes zero position in the US dollar and all of our regression specification

includes time-fixed effects. Therefore, subtracting the US interest rate has no impact on our analysis.

12

4.2 Summary Statistics

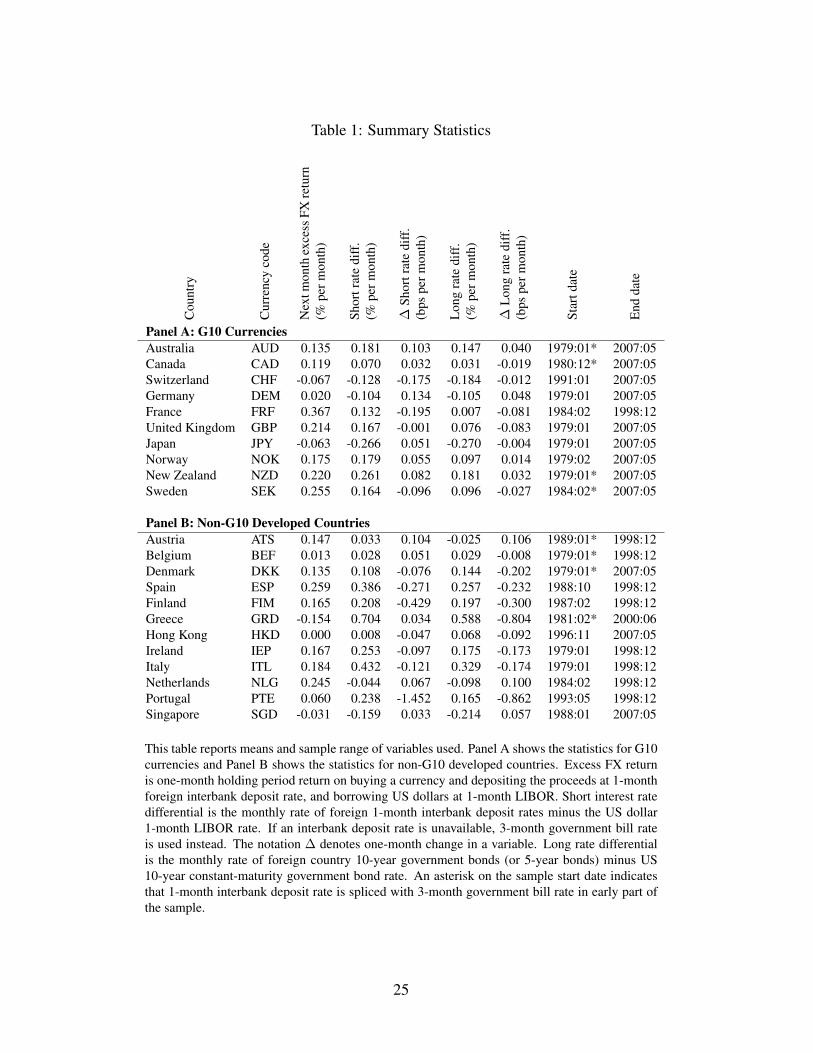

We begin by presenting some basic features of data to help guide our empirical design. Table 1

shows means and sample ranges of our variables for the G10 currencies in Panel A, and for non-

G10 currencies in Panel B. Our currency returns are express in terms of percent per month. For

example, investing in Australian dollar financed by US dollar and rebalancing every month has

resulted in a net profit of 0.135% per month, or 1.62% per year. During this period Australian

dollar interest rate was on average higher than the US dollar rate by 0.181% per month, or 2.17%

per year. In this period, the Australian dollar depreciated against the US dollar by approximately

this difference, but the trade was profitably because of the interest earned. The average monthly

change in the short rate was 0.103 basis points per month, indicating Australian interest rate

rose relative tot he US interest rate slightly over this period. Looking at the long bond rate and

its changes depicts a similar history.

Note among the G10 currencies, currencies with lower short rate than the US dollar (CHF,

DEM and JPY) tend to produce negative future excess currency returns. This positive relation

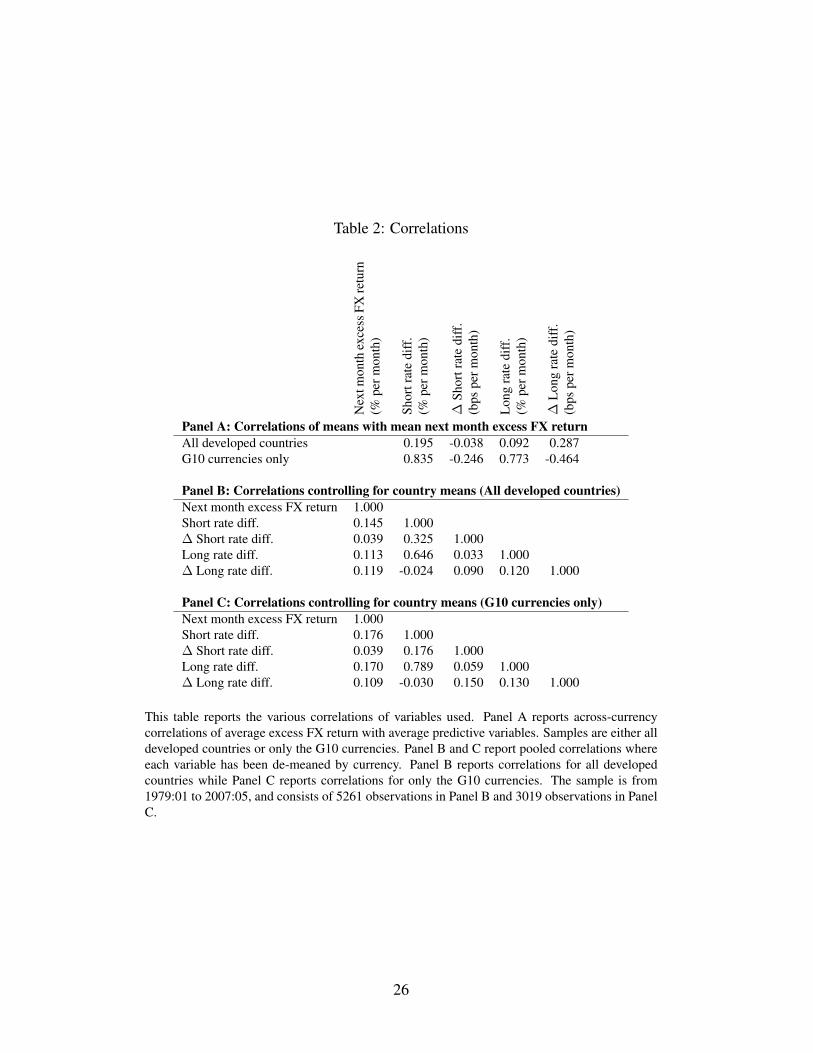

is the main driver of the carry trade. Panel A of Table 2 formally looks at this pattern in terms

of correlations between time-series averages of excess currency return and time-series averages

of predictive yield curve variables. The positive coorelation between average excess currency

return and average short rate differential exist across all developed countries, but it is much

more pronounced when only the G10 currencies are considered. However, when we look at the

relation with average changes in interest rates and average excess currency returns, it seems to

be a negative relation.

While Panel A of Table 2 looks at relationships of means across currencies, it does not say

anything about relationships of these variables across time. Panel B of Table 2 gives us a glimpse

of the time-series relationship by showing the correlations of our variables in a pooled sample,

where the variables have been de-meaned by country. In time-series, each of our yield curve

predictive variables are positively correlated with future excess currency return. We formally

examine this in our regressions later. Also note that while levels short-term and long-term

interest rates tend to be very highly correlated, the changes in these variables are not.

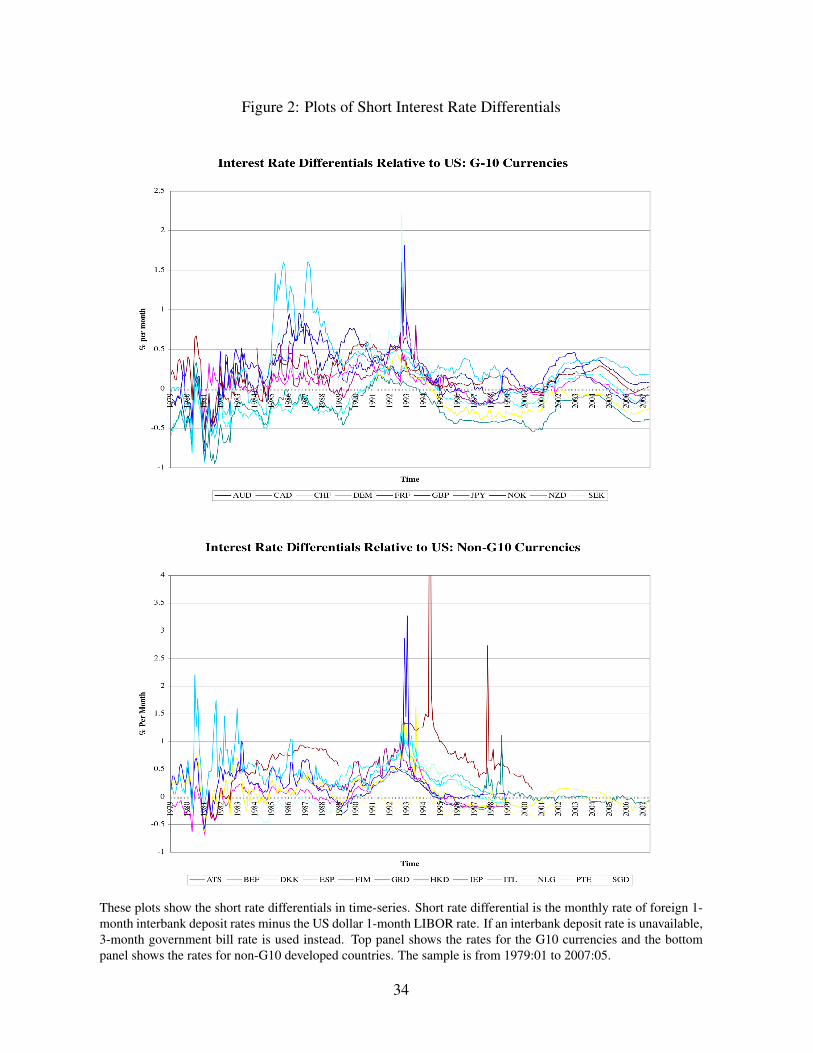

Figure 2 plots the short rate for all currencies in time-series. There are a couple of features

that are worthwhile noting. First, many currencies have experienced periods of crisis. In 1992

a financial crisis swept through much of Europe affecting DKK, FIM, IEP, NOK and SEK

particularly hard, but also ESP and FRF. AUD and NZD experienced persistently high interest

rate differential in late 1980’s. Notably, financial turmoil seems to be norm for GRD and ITL

13

for much of our sample. Second, there has been a regime change in cross-currency variation in

interest rate differential. In particular there appears markedly lower variation in interest rates

since the late 1990’s. Finally, there are numerous entries and exists of currencies, especially

with the introduction of the Euro. We will be mindful of controlling for these features of the

data in designing our portfolio formations and regression specifications.

5 Portfolio Results

We begin by exploring the relation between excess currency returns and yield curve predictors

from a portfolio perspective first. We start by examining the standard carry traded used by prac-

titioners and consider using alternative predictive variables from the term structure of interest

rates. Since the standard carry trade is essentially based on indicator functions, we consider an

alternative portfolio specification that is closer to running a regression in spirit. All of our port-

folio results are from the point of view of a currency trader in the US. We assume that the trader

is able to transact all developed country currencies at no cost and is able to borrow and deposit

at the prevailing interbank rates. Furthermore, we assume that the trader takes no position in

his home currency. Hence, all portfolios considered take long and short positions in currencies,

with appropriate foreign deposits and foreign financing, but has zero holdings on the US dollar.

5.1 The Benchmark Carry Trade

The basic carry trade ranks currencies by the short rate differentials. The carry trade entails

purchasing currencies with high interest rates and selling currencies with low interest rates.

Generally, currencies with the highest (lowest) one-third values of interest rates are purchased

(sold). Among the purchases and the sales, the standard carry trade takes equal positions.

Hence, if there are ten currencies to choose from, the carry trade buys the highest three interest

currencies and sell the lowest three interest rate currencies with equal weights. These portfolios

are reevaluated and rebalanced each month. Note that from the point of view of a carry trade

based in the US, the net holdings of US dollar is zero. The standard carry trade is often based

on only the G10 currencies, but can be expanded to include additional currencies.

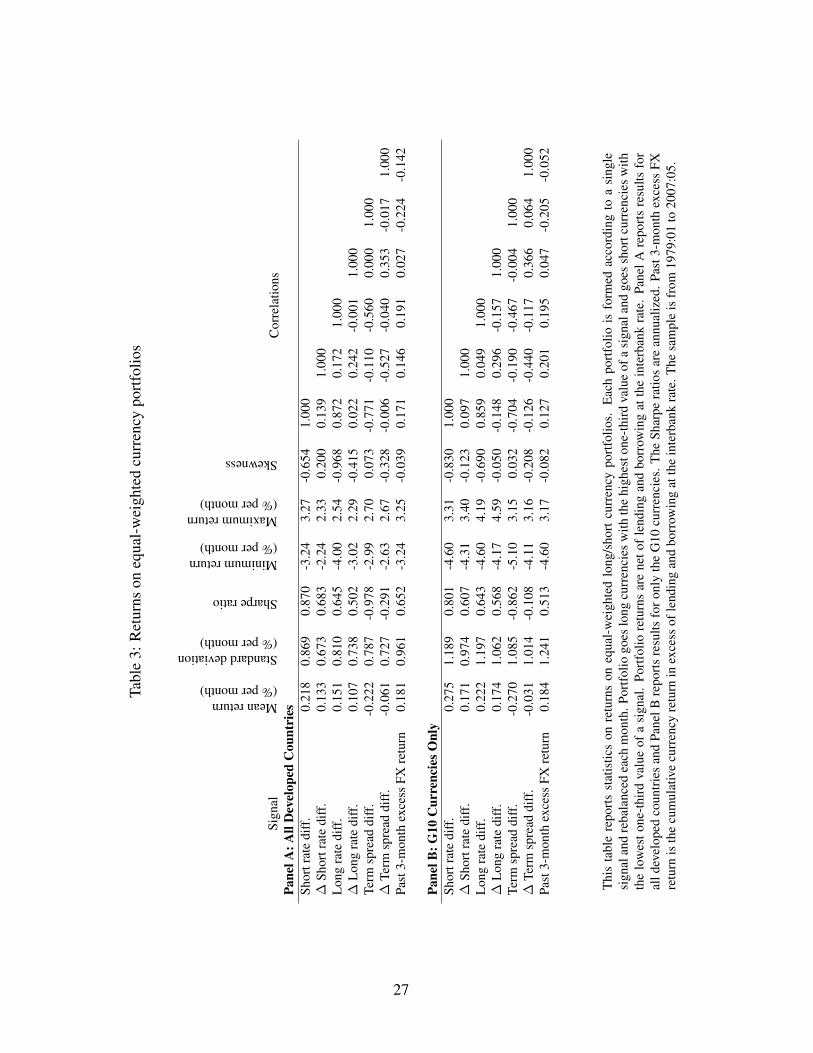

The summary statistics of our currency portfolios are presented in Table 3. Panel A consid-

ers the portfolios formed across all 22 developed country currencies while Panel B considers the

portfolios formed across only the G10 currencies. For each portfolio, we compute one-month

holding period returns and report their means and standard deviations. Since these portfolios are

14

zero cost positions, the returns can be thought of as profits on purchasing one US dollar worth of

high signal foreign currencies and borrowing one US dollar worth of low signal currencies. We

also report annualized Sharpe ratio, which is the ratio of means and standard deviations, scaled

by the square root of 12. Finally, we report minimum, maximum, and skewness of portfolio

returns and their correlations.

The first row of each panel describes the portfolio returns of the carry trade. When the trade

is conducted across all developed country currencies, the carry trade has averaged a return of

0.218% per month with a standard deviation of 0.869% per month. This translates to an impres-

sive annualized Sharpe ratio of 0.870. The results are mostly similar when only G10 currencies

are used. The average return is higher with only the G10 currencies, but the corresponding

Sharpe ratio is slightly lower. Since short rate differentials are very persistent, these portfolios

tend to have low monthly turnover. However, it is well known that these carry trade portfolio

returns have negative skewness and are prone to large losses. This tendency is more noticeable

when only G10 currencies are used.

5.2 Other Equal-Weighted Currency Portfolios

We now investigate if other parts of the yield curve has predictive information about future

currency returns in a portfolio framework. We construct additional currencies portfolios in the

same manner as the carry trade portfolios. However, rather than using the short rate differentials,

we also consider other signals as predictors of future currency returns. Specifically, we consider

the one-month changes in the short rate differentials, the long bond rate differentials, and the

one-month changes in the long bond rate differentials. To help separate the effects of the slope

of the yield curve from the level of the yield curve, we also look at the term spread differentials

and their one-month changes. As another benchmark, we also consider a currency momentum

portfolio, which is common in practice. The currency momentum portfolio uses information

in past currency returns and we use the past 3-month cumulative excess currency return as the

signal.

The second row of each panel of Table 3 shows the equal-weighted portfolio returns based

on changes in the short rate differentials. Across all developed country currencies, this trade

has averaged a return of 0.133% per month with a standard deviation of 0.673% per month.

This translates to an annualized Sharpe ratio of 0.683, which is large. The values are similar

when only G10 currencies are used. Unlike the carry trade, however, using changes in the

short rate leads to portfolio with higher turnover, but it leads to a portfolio without proneness to

15

large losses. In fact, when all developed country currencies are used, this portfolio has positive

skewness. Moreover, the correlation with carry trade returns is low at 0.139. In fact, a naive

strategy consisting of fifty-percent of this portfolio and fifty-percent in the carry trade portfolio

leads to a strategy with a Sharpe ratio of around 1.1.

The third and fourth rows in Table 3 show the portfolio returns when the long rate differen-

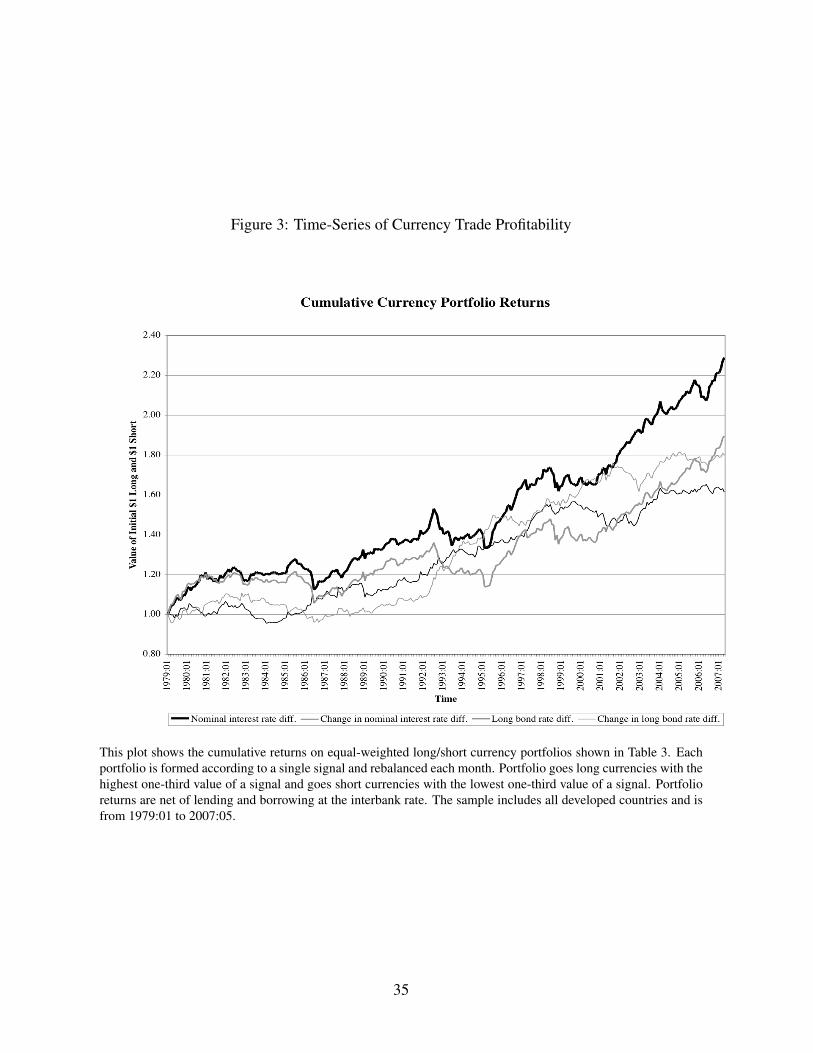

tials are used instead of the short rate differentials, in terms of both levels and changes. Figure

3 shows the time-series of cumulative returns on portfolios considered so far. Notice that using

the long rate leads to a portfolio with similar characteristics as the carry trade. In fact, the cor-

relation of this portfolio’s return with carry trade return is 0.872. Hence the levels of long rate

appears to have the same predictive information as the levels of short rate. However, the same

does not appear to be the case for portfolio based on changes in long rate differentials. This

portfolio produces a Sharpe ratio of 0.502, which is still significant. However, the correlations

with other portfolios we’ve considered are low to modest. The correlation of this portfolio with

the portfolio based on changes in the short rate differential is a modest 0.242. Hence there

appears to be some predictive information content in changes in the yield curve.

To organize the information about the yield curve differently, we fifth and sixth rows of

Table 3 show the portfolio returns based on levels and changes of the term spread. These

portfolios produce negative Sharpe ratios, so they should be reversed. That is, currencies with

low (or negative) term spread should be purchased and currencies with high slope of the yield

curve should be sold. Interestingly, combining the short rate differentials and the long rate

differentials produces the portfolio with the highest Sharpe ratio at 0.978. However, changes in

the term spread differentials produces a portfolio with only a very modest Sharpe ratio of 0.291.

If only G10 currencies are used the return is higher, but the Sharpe ratio is lower. However, it is

still the case that the negative skewness is mitigated and portfolios based on levels and changes

have low correlations with one another.

Finally, we consider currency momentum portfolios as another benchmark. The portfolio

returns are shown in the last row of Table 3. Currency momentum portfolio also produces re-

turns with high Sharpe ratio at 0.652 and no detectable skewness. To see if currency momentum

captures the same predictive information we examine the correlations of portfolio returns. All

correlations are fairly modest, and hence it does not appear that information in the yield curve

is the same as the information in past currency returns.

16

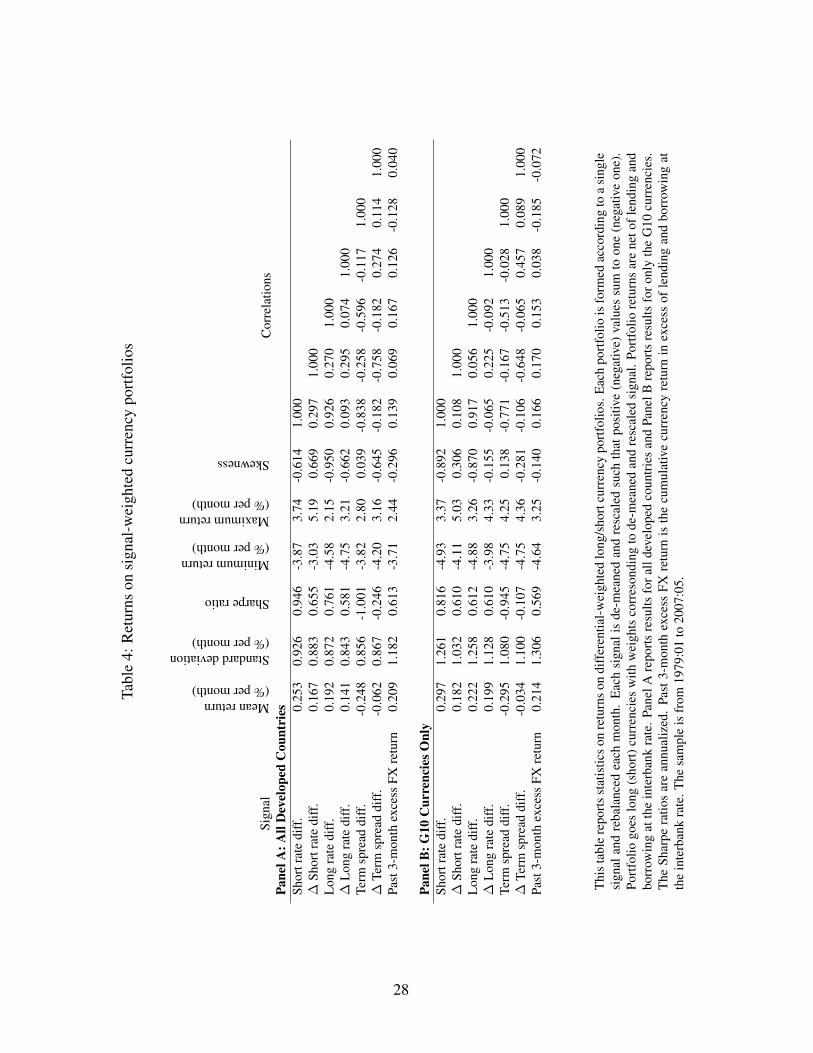

5.3 Signal-weighted Currency Portfolio Returns

One difficulty with examining portfolio returns is that it does not allow us to disentangle the ef-

fects of one signal from another. Hence, we will turn to a regression framework below. Another

difficulty with the carry trade portfolio is that it is based on an indicator function and places no

weight on the value of the signal. If three currencies are purchased, they are all given the same

weight, even though highest signal value may be very different from the third-highest signal

value, or the fourth-highest signal is very similar to the third-highest.

To mitigate this concern and to produce portfolios that are more like running a regression,

we create signal-weighted currency portfolios. For these portfolios, we maintain the perspec-

tive of a currency trader in the US who takes no position in the US dollar. During portfolio

formation each month, rather than using indicator function, we de-mean and rescale each sig-

nal. We rescale in a way such that the all positive (and hence all negative) signal values sum to

one. Except for the scaling, this is essentially standardizing the signals to be zero mean and a

unit variance. For each currency with a positive (negative) de-meaned and rescaled signal, we

purchase (sell) a US dollar amount equal to the adjusted signal. This ensures that the portfolio

is long and short an equal amount in total, total long and total short position sizes are fixed

constant across time in terms of US dollars, and the individual position size is proportional to

the de-meaned signal.

The returns on these signal-weighted currency returns are presented in Table 4. Overall,

we find similar results as equal-weighted currency returns, but with some differences. We find

that the signal-weighted carry trade still has an impressively high Sharpe ratio, but is negatively

skewed. The changes in the short rate produces a portfolio with high Sharpe ratio and more

positively skewed portfolios than before. The correlation between the two remain low. Currency

portfolio based on long rate differentials still looks similar to the carry trade. However, changes

in the long rate differentials appears to be predictive and contains information not already found

in the short rate.

The returns on currency portfolios based on term spread and currency momentum are similar

when signal-weighted as well. The term spread differentials still produce the single portfolio

with the greatest Sharpe ratio, and has little skewness. Expressing yield curve information this

way, changes in the term spread produces a portfolio with only a very modest Sharpe ratio.

Currency momentum portfolios also continue to produce high Sharpe ratios, but its returns have

low correlations with returns of portfolios formed using yield curve information.

These signal-weighted portfolios alleviate concerns that neither the truncation of outliers or

17

discreteness of the cut-off point somehow affect our currency portfolio results. These portfolios

are also much closer to running regressions and make comparisons easier. We turn to our

regression framework in the next section.

6 Predictive Regression Framework

6.1 Cross-Sectional Regression Specification

In our cross-sectional regression specification, we maintain comparability with our portfolio

results. The dependent variable is future excess currency returns, but we vary the horizon from

1-month to 12-month. Longer horizon returns are cumulated, but we express the returns in

monthly figures to make comparison easier. Our basic specification is a pooled-panel monthly

frequency regression with month fixed-effects. The month fixed-effects absorb any average

time-series variations in excess currency returns. This removes the effect of US dollar move-

ment across time relative to other currencies. All of our regressions use standard errors that

are heteroskedasticity-robust and double-clustered by month and currency. Hence, our stan-

dard errors account for variability in currency volatility over time, account for correlations of

currencies at any point in time, and account for auto-correlations of currencies.

There are also time-variations in the distribution of our signals. For example, we witnessed

in Figure 2 that there are periods of high variability and low variability in short rate differentials.

There are also outliers in data. To account for these features, we transform each of our inde-

pendent variables each month. We primarily consider regressors that have been transformed to

a uniform distribution ranging between 0 and 1, according to the rank of the variable. As an

example, if there are 10 currencies, the regressors are transformed to values of 0.05, 0.15, 0.25,

... and 0.95 according to the rank of the variable each month. For robustness checks, we also

standardize our regressors to be zero mean and unit variance within each month. For the most

part, we consider a sample consisting of all developed countries, but also consider a sample

consisting of only G10 currencies. We transform our regressors separately for each sample.

6.2 Regression Results

We begin by examining the univariate regressions in Table 5. Going across the columns, we

vary the holding period horizon of currencies as our dependent variable. Panel A predicts future

currency returns using short rate differentials and is comparable to the carry trade. Similar to the

18

carry trade, we find a positive relation between short rates and future excess currency returns.

As we vary the horizon, we find that predictability remains. Notice that even though the point

estimate falls with horizon, the t-statistics and remain largely unchanged.

We examine other yield curve predictors in Panels B through Panel D. We see the similar set

of results based on regressions as we did based on portfolios. Whether we use the changes in the

short rate differentials, the long rate differentials or the changes in the long rate differentials, we

continue to find positive relation between them and future currency returns. We also find that the

predictive ability is maintained but erodes as we increase the horizon. At some longer horizons,

we find that the predictability becomes weaker for the change in the long rate differentials. This

is in contrast to the negative correlations of the mean we observed in Panel A of Table 1. These

results suggest that there is a more complex time-series relation at play between the relation

between changes in interest rate and future exchange rates. The longer-horizon predictability

also suggests that portfolio strategies based on changes in interest rates can be constructed in a

way that portfolio turnover is not as high.

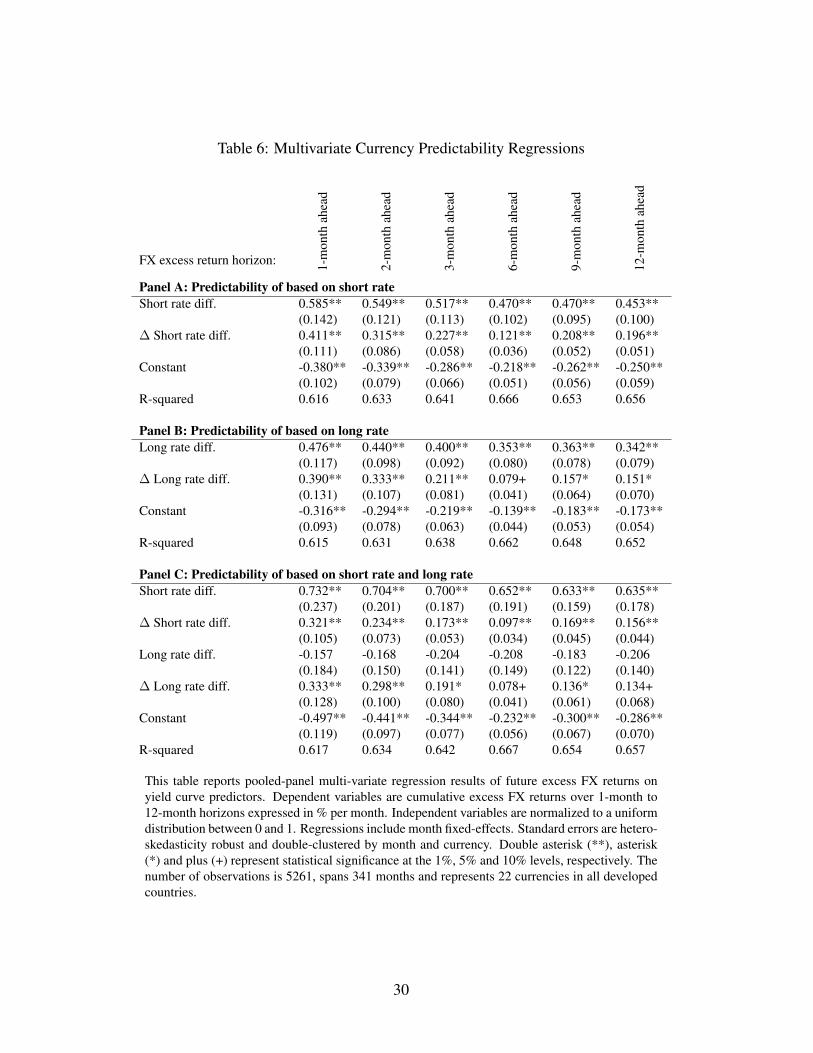

Given the regression framework, we can easily see if these yield curve predictors have in-

formation that are independent from one another through the use of multivariate regressions.

We compare levels and changes on short rate differentials in Panel A of Table 6, and compare

the levels and changes of long rate differentials in Panel B of Table 6. In both cases, the lev-

els of interest rate differentials and the changes in the interest rate differentials continue to be

significant as they did by themselves. This is similar to the low correlations we saw in the

portfolio framework. Hence we can conclude that both levels and changes of interest rates have

predictive information for future currency returns.

We compare the predictive ability of all four yield curve variables in Panel C of Table 6.

These are multivariate regressions where all four variables are used simultaneously. This speci-

fication allows us to understand how many different mechanisms are present. We find that when

all four variables are used, the long rate differentials no longer enter significantly, let alone pos-

itively. This is consistent with all the correlations we have seen thus far. It appears that long

rate differentials and short rate differentials, capture roughly the same set of information. How-

ever, we find that the changes in long rate differential is not driven out and remains positive and

statistically significant. Overall, it appears that there is more predictive information in the yield

curve than just levels and changes, and the shape of the yield is also important.

19

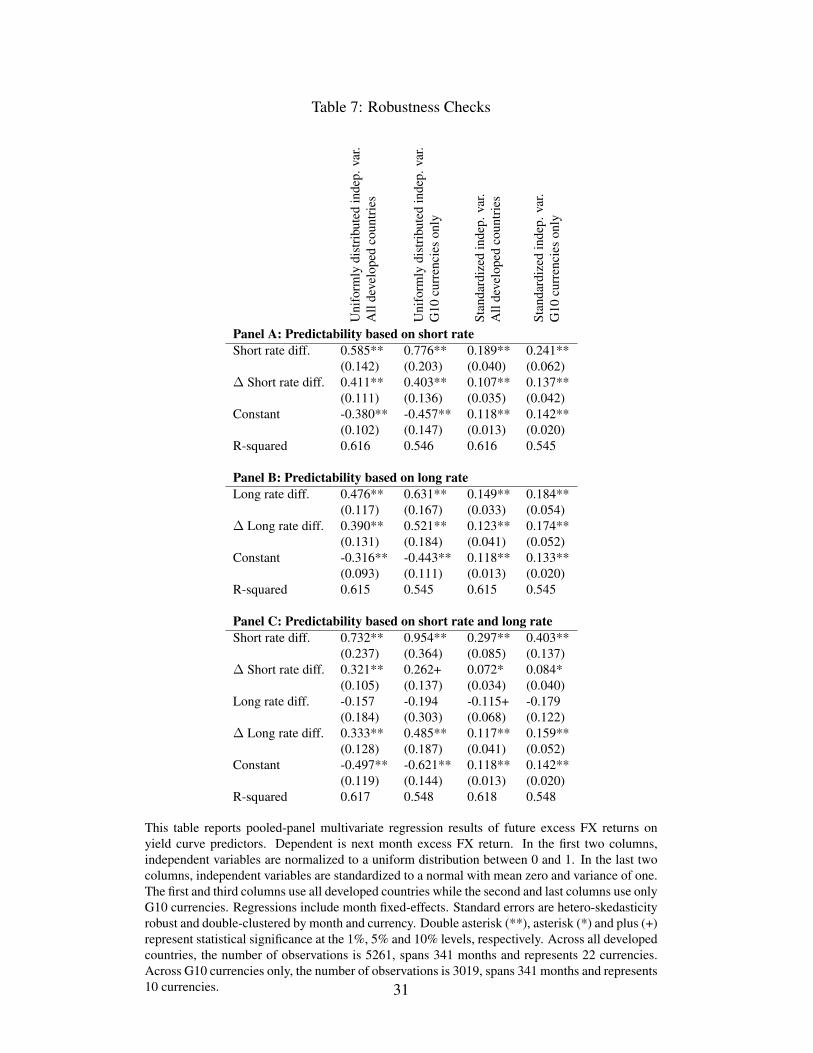

6.3 Robustness of Regressions Results

We address some robustness of our regression results in Table 7. We only consider the one-

month ahead excess currency return in our robustness, but vary the sample and the transfor-

mation of our regressors. The first column repeats the information in Table 6 for comparative

purposes. In the second column, we repeat the exercise but using only the G10 currencies.

We find that the point estimate on short rate differential is higher but with higher standard er-

rors, consistent with an observation on Table 3. Otherwise, we also find that the coefficient on

changes in short rate in Panel C is weaker and only significant at the 10% level. In the third and

fourth columns, we consider standardizing our regressors instead of putting them on a uniform

distribution. We find that all of our results remain qualitatively unchanged. If anything, the co-

efficient on changes in short rate is more robust to the sample, though it is now only significant

at the 5% level.

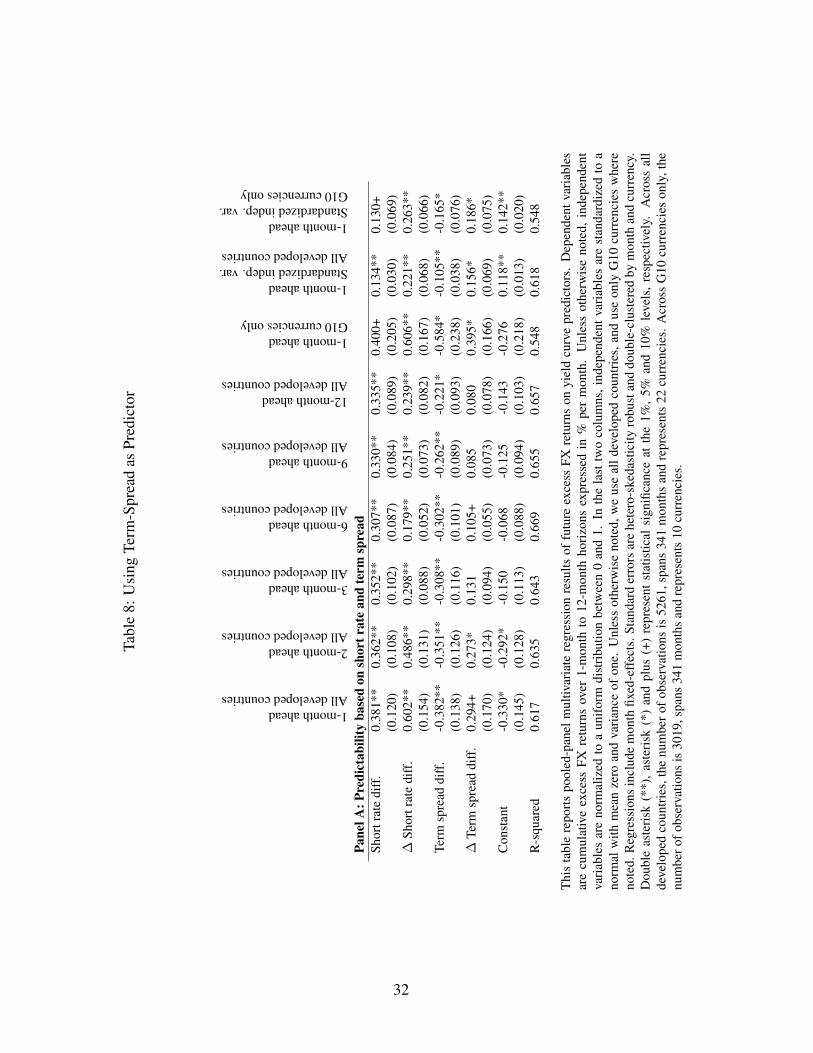

As an additional robustness, we consider using the information in the yield curve differently.

Rather than looking at the short rate differentials and the long rate differentials, we consider

using the short rate differentials and the term spread differentials. Similarly, we consider the

change in the term spread instead of the changes in the long rate differentials. Table 8 report

the regression results using the term spread differentials. These results are comparable to the

results in Panel C of Table 6 and Panel C of 7. Interestingly, rather than the change in the long

rate entering consistently significantly, we find that it’s the level of the term spread that enters

consistently. The changes in the term spreads also enter significantly at times. However, this

specification is not preferable because the term spread is strongly negative correlated with the

short rate, by construction. We see that this near collinearity drives out the predictability using

the short rate when only the G10 currencies are considered.

7 Conclusion

We find that there is significant information in foreign countries’ yield curves that is useful

for predicting foreign exchange returns in the cross-section. This predictability information

goes well beyond the uncovered interest parity and the violations of it, and it goes beyond

the well-known carry trade. We document that both the levels of interest rates as well as the

changes in interest rates have the ability to forecast future currency returns in the cross-section

of currencies. Moreover additional predictability information can be found by comparing the

movements in the short rates relative to that of the long rates. In particular, we find that in

20

addition to the levels and the changes of the short rate, the changes in the long rate or the levels

of the yield curve provides added predictability.

Overall, our empirical results are consistent with our motivating framework that risk fac-

tors the affect the yield curve should also affect the foreign exchange rates. Our findings fit

nicely with the term structure literature that document there appears to be multiple factors that

the term structure of interest rates. However, our paper only suggests that our findings can be

explained in a no-arbitrage model. We cannot rule out that profitability of the currency portfo-

lios we investigate is not due to mispricing rather than due to risk-exposure. We leave further

understanding of the economics behind our empirical findings to future work.

21

References[1] Ahn, D. H., 2004, “Common Factors and Local Factors: Implications for Term Structures and Exchange

Rates,” Journal of Financial and Quantitative Analysis, 39, 69-102.

[2] Ang, A., and M. Piazzesi, 2003, “A No-Arbitrage Vector Autoregression of Term Structure Dynamics withMacroeconomic and Latent Variables,” Journal of Monetary Economics, 50, 745-787.

[3] Backus, D. K., S. Foresi, and C. I. Telmer, 2001, “Affine Term Structure Models and the Forward PremiumAnomaly,” Journal of Finance, 56, 279-304.

[4] Balduzzi, P., S. R. Das, and S. Foresi, 1998, “The Central Tendency: A Second Factor in Bond Yields,”Review of Economics and Statistics, 80, 62-72.

[5] Balduzzi, P., S. R. Das, S. Foresi, and R. K. Sundaram, 1996, “A Simple Approach to Three-Factor AffineTerm Structure Models,” Journal of Fixed Income, 6, 43-53.

[6] Bansal, R., 1997, “An Exploration of the Forward Premium Puzzle in Currency Markets,” Review of Finan-cial Studies, 10, 369-403.

[7] Bekaert, G., 1996, “The Time Variation of Risk and Return in Foreign Exchange Markets,” Review of Fi-nancial Studies, 10, 369-403.

[8] Boudoukh, J., M. Richardson, and R. F. Whitelaw, 2006, “The Information in Long-Maturity Forward Rates:Implications for Exchange Rates and the Forward Premium Anomaly,” working paper, NYU.

[9] Brandt, M. W., and Q. Kang, 2004, “On the Relationship Between the Conditional Mean and Volatility ofStock Returns: A Latent VAR Approach,” Journal of Financial Economics, 72, 217-257.

[10] Brandt, M. W., and P. Santa-Clara, 2002, “Simulated Likelihood Estimation of Diffusions with an Applica-tion to Exchange Rate Dynamics in Incomplete Markets,” Journal of Financial Economics 63, 161-210.

[11] Brennan, M. J., and E. S. Schwartz, 1979, “A Continuous Time Approach to the Pricing of Bonds,” Journalof Banking and Finance, 3, 133-155.

[12] Brennan, M. J., A. W. Wang, and Y. Xia, 2004, “Estimation and Test of a Simple Model of IntertemporalAsset Pricing,” Journal of Finance, 59, 1743-1775.

[13] Brunnermeir, M. K., S. Nagel, and L. H. Pedersen, 2009, “Carry Trades and Currency Crashes,” in Ace-moglu, D., K. Rogoff, and M. Woodford, NBER Macroeconomics Annual, pp313-359, University ofChicago Press, Chicago IL.

[14] Burnside, C., M. S. Eichenbaum, I. Kleshchelski, and S. Rebelo, 2006, “The Returns to Currency Specula-tion,” NBER working paper 12489.

[15] Burnside, C., M. S. Eichenbaum, and S. Rebelo, 2007, “Understanding the Forward Premium Puzzle: AMicrostructure Approach,” NBER working paper 13278.

[16] Chen, Y. C., and K. P. Tsang, 2009, “What does the Yield Curve Tell Us about Exchange Rate Predictability,”working paper, University of Washington.

[17] Chinn, M. D., 2006, “The (Partial) Rehabilitation of Interest Rate Parity in the Floating Rate Era: LongerHorizons, Alternative Expectations, and Emerging Markets,” Journal of International Money and Finance,25, 7-21.

[18] Cox, J. C., J. E. Ingersoll, and S. A. Ross, 1985, “A Theory of the Term Structure of Interest Rates,”Econometrica, 53, 769-799.

22

[19] Dai, Q., and K. J. Singleton, 2000, “Specificaiton Analysis of Affine Term Structure Models,” Journal ofFinance, 55, 1943-1978.

[20] Dong, S., 2006, “Macro Variables Do Drive Exchange Rate Movements: Evidence from a No-ArbitrageModel,” working paper, Columbia University.

[21] Engel, C., 1996, “The Forward Discount Anomaly and the Risk Premium: A Survey of Recent Evidence,”Journal of Empirical Finance, 3, 123-92.

[22] Engel, C., and K. D. West, 2005, “Exchange Rates and Fundamentals,” Journal of Political Economy, 113,485-517.

[23] Engel, C., N. C. Mark, and K. D. West, 2007, “Exchange Rate Models are Not as Bad as You Think,” inAcemoglu, D., K. Rogoff, and M. Woodford, NBER Macroeconomics Annual, pp381-441, University ofChicago Press, Chicago IL.

[24] Fama, E., 1984, “Forward and Spot Exchange Rates,” Journal of Monetary Economics, 14, 319-338.

[25] Gourinchas, P. O., and A. Tornell, 2004, “Exchange Rate Puzzles and Distorted Beliefs,” Journal of Inter-national Economics, 64, 303-333.

[26] Graveline, J. J., 2006, “Exchange Rate Volatility and the Forward Premium Anomaly,” working paper, MIT.

[27] Hodrick, R. J., 1998, The Empirical Evidence on the Efficiency of Forward and Futures Foreign ExchangeMarkets, Harwood Academic, New York NY.

[28] Hodrick. R. J., and M. Vassalou, 2002, “Do we Need Multi-Country Models to Explain Exchange Rate andInterest Rate and Bond Return Dynamics?” Journal of Economic Dynamics and Control, 26, 1275-1299.

[29] Ilmanen, A., and R. Sayood, 1998, “Currency Allocaiton and Timing Based on Predictive Indicators,” Sa-lomon Smith Barney research report.

[30] Ilmanen, A., and R. Sayood, 2002, “Quantitative Forecasting Models and Active Diversification for Interna-tional Bonds,” Journal of Fixed Income, December, 40-51.

[31] Jurek, J. W., 2008, “Crash-Neutral Currency Carry Trades,” working paper, Princeton University.

[32] Kozicki, S., and P. A. Tinsley, 2001, “Shifting Endpoints in the Term Structure of Interest Rates,” Journal ofMonetary Economics, 47, 613-652.

[33] Lettau, M., and J. Wachter, 2009, “The Term Structures of Equity and Interest Rates,” working paper, UCBerkeley.

[34] Lewis, K. K., 1995, “Puzzles in International Financial Markets,” in Grossman, G. M. and Rogoff, K., eds,Handbook of International Economics, Elsevier, Amsterdam, pp1913-1972.

[35] Longstaff, F. A., and E. S. Schwartz, 1992, “Interest Rate Volatility and the Term Structure: A Two-FactorGeneral Equilibrium Model,” Journal of Finance, 47, 1259-1282.

[36] Lustig, H., N. Roussanov, and A. Verdelhan, 2008, “Common Risk Factors in Currency Markets,” NBERworking paper 14082.

[37] Molodtsova, T., and D. H. Papell, 2008, “Out-of-Sample Exchange Rate Predictability with Taylor RuleFundamentals,” working paper, Emory University.

[38] Piazzesi, 2003, “Affine Term Structure Models,” working paper, Stanford University.

23

[39] Sarno, L., 2005, “Towards a Solution to the Puzzles in Exchange Rate Economics: Where Do we Stand?”Canadian Journal of Economics, 38, 673-708.

[40] Schaefer, S. M., and E. S. Schwartz, 1979, “A Two-Factor Model of the Term Structure: An ApproximateAnalytical Solution,” Journal of Financial and Quantitative Analysis, 19, 413-424.

[41] Wang, J., and J. J. Wu, 2009, “The Taylor Rule and Interval Forecast for Exchange Rates,” working paper,Fed Board of Governors.

[42] Vasicek, O. A., 1977, “An Equilibrium Characterization of the Term Structure,” Journal of Financial Eco-nomics, 5, 177-188.

24

Table 1: Summary Statistics

Cou

ntry

Cur

renc

yco

de

Nex

tmon

thex

cess

FXre

turn

(%pe

rmon

th)

Shor

trat

edi

ff.

(%pe

rmon

th)

∆Sh

ortr

ate

diff

.(b

pspe

rmon

th)

Lon

gra

tedi

ff.

(%pe

rmon

th)

∆L

ong

rate

diff

.(b

pspe

rmon

th)

Star

tdat

e

End

date

Panel A: G10 CurrenciesAustralia AUD 0.135 0.181 0.103 0.147 0.040 1979:01* 2007:05Canada CAD 0.119 0.070 0.032 0.031 -0.019 1980:12* 2007:05Switzerland CHF -0.067 -0.128 -0.175 -0.184 -0.012 1991:01 2007:05Germany DEM 0.020 -0.104 0.134 -0.105 0.048 1979:01 2007:05France FRF 0.367 0.132 -0.195 0.007 -0.081 1984:02 1998:12United Kingdom GBP 0.214 0.167 -0.001 0.076 -0.083 1979:01 2007:05Japan JPY -0.063 -0.266 0.051 -0.270 -0.004 1979:01 2007:05Norway NOK 0.175 0.179 0.055 0.097 0.014 1979:02 2007:05New Zealand NZD 0.220 0.261 0.082 0.181 0.032 1979:01* 2007:05Sweden SEK 0.255 0.164 -0.096 0.096 -0.027 1984:02* 2007:05

Panel B: Non-G10 Developed CountriesAustria ATS 0.147 0.033 0.104 -0.025 0.106 1989:01* 1998:12Belgium BEF 0.013 0.028 0.051 0.029 -0.008 1979:01* 1998:12Denmark DKK 0.135 0.108 -0.076 0.144 -0.202 1979:01* 2007:05Spain ESP 0.259 0.386 -0.271 0.257 -0.232 1988:10 1998:12Finland FIM 0.165 0.208 -0.429 0.197 -0.300 1987:02 1998:12Greece GRD -0.154 0.704 0.034 0.588 -0.804 1981:02* 2000:06Hong Kong HKD 0.000 0.008 -0.047 0.068 -0.092 1996:11 2007:05Ireland IEP 0.167 0.253 -0.097 0.175 -0.173 1979:01 1998:12Italy ITL 0.184 0.432 -0.121 0.329 -0.174 1979:01 1998:12Netherlands NLG 0.245 -0.044 0.067 -0.098 0.100 1984:02 1998:12Portugal PTE 0.060 0.238 -1.452 0.165 -0.862 1993:05 1998:12Singapore SGD -0.031 -0.159 0.033 -0.214 0.057 1988:01 2007:05

This table reports means and sample range of variables used. Panel A shows the statistics for G10currencies and Panel B shows the statistics for non-G10 developed countries. Excess FX returnis one-month holding period return on buying a currency and depositing the proceeds at 1-monthforeign interbank deposit rate, and borrowing US dollars at 1-month LIBOR. Short interest ratedifferential is the monthly rate of foreign 1-month interbank deposit rates minus the US dollar1-month LIBOR rate. If an interbank deposit rate is unavailable, 3-month government bill rateis used instead. The notation ∆ denotes one-month change in a variable. Long rate differentialis the monthly rate of foreign country 10-year government bonds (or 5-year bonds) minus US10-year constant-maturity government bond rate. An asterisk on the sample start date indicatesthat 1-month interbank deposit rate is spliced with 3-month government bill rate in early part ofthe sample.

25

Table 2: Correlations

Nex

tmon

thex

cess

FXre

turn

(%pe

rmon

th)

Shor

trat

edi

ff.

(%pe

rmon

th)

∆Sh

ortr

ate

diff

.(b

pspe

rmon

th)

Lon

gra

tedi

ff.

(%pe

rmon

th)

∆L

ong

rate

diff

.(b

pspe

rmon

th)

Panel A: Correlations of means with mean next month excess FX returnAll developed countries 0.195 -0.038 0.092 0.287G10 currencies only 0.835 -0.246 0.773 -0.464

Panel B: Correlations controlling for country means (All developed countries)Next month excess FX return 1.000Short rate diff. 0.145 1.000∆ Short rate diff. 0.039 0.325 1.000Long rate diff. 0.113 0.646 0.033 1.000∆ Long rate diff. 0.119 -0.024 0.090 0.120 1.000

Panel C: Correlations controlling for country means (G10 currencies only)Next month excess FX return 1.000Short rate diff. 0.176 1.000∆ Short rate diff. 0.039 0.176 1.000Long rate diff. 0.170 0.789 0.059 1.000∆ Long rate diff. 0.109 -0.030 0.150 0.130 1.000

This table reports the various correlations of variables used. Panel A reports across-currencycorrelations of average excess FX return with average predictive variables. Samples are either alldeveloped countries or only the G10 currencies. Panel B and C report pooled correlations whereeach variable has been de-meaned by currency. Panel B reports correlations for all developedcountries while Panel C reports correlations for only the G10 currencies. The sample is from1979:01 to 2007:05, and consists of 5261 observations in Panel B and 3019 observations in PanelC.

26

Tabl

e3:

Ret

urns

oneq

ual-

wei

ghte

dcu

rren

cypo

rtfo

lios

Sign

al

Meanreturn(%permonth)

Standarddeviation(%permonth)

Sharperatio

Minimumreturn(%permonth)

Maximumreturn(%permonth)

Skewness

Cor

rela

tions

Pane

lA:A

llD

evel

oped

Cou

ntri

esSh

ortr

ate

diff

.0.

218

0.86

90.

870

-3.2

43.

27-0

.654

1.00

0∆

Shor

trat

edi

ff.

0.13

30.

673

0.68

3-2

.24

2.33

0.20

00.

139

1.00

0L

ong

rate

diff

.0.

151

0.81

00.

645

-4.0

02.

54-0

.968

0.87

20.

172

1.00

0∆

Lon

gra

tedi

ff.

0.10

70.

738

0.50

2-3

.02

2.29

-0.4

150.

022

0.24

2-0

.001

1.00

0Te

rmsp

read

diff

.-0

.222

0.78

7-0

.978

-2.9

92.

700.

073

-0.7

71-0

.110

-0.5

600.

000

1.00

0∆

Term

spre

addi

ff.

-0.0

610.

727

-0.2

91-2

.63

2.67

-0.3

28-0

.006

-0.5

27-0

.040

0.35

3-0

.017

1.00

0Pa

st3-

mon

thex

cess

FXre

turn

0.18

10.

961

0.65

2-3

.24

3.25

-0.0

390.

171

0.14

60.

191

0.02

7-0

.224

-0.1

42

Pane

lB:G

10C

urre

ncie

sOnl

ySh

ortr

ate

diff

.0.

275

1.18

90.

801

-4.6

03.

31-0

.830

1.00

0∆

Shor

trat

edi

ff.

0.17

10.

974

0.60

7-4

.31

3.40

-0.1

230.

097

1.00

0L

ong

rate

diff

.0.

222

1.19

70.

643

-4.6

04.

19-0

.690

0.85

90.

049

1.00

0∆

Lon

gra

tedi

ff.

0.17

41.

062

0.56

8-4

.17

4.59

-0.0

50-0

.148

0.29

6-0

.157

1.00

0Te

rmsp

read

diff

.-0

.270

1.08

5-0

.862

-5.1

03.

150.

032

-0.7

04-0

.190

-0.4

67-0

.004

1.00

0∆

Term

spre

addi

ff.

-0.0

311.

014

-0.1

08-4

.11

3.16

-0.2

08-0

.126

-0.4

40-0

.117

0.36

60.

064

1.00

0Pa

st3-

mon

thex

cess

FXre

turn

0.18

41.

241

0.51

3-4

.60

3.17

-0.0

820.

127

0.20

10.

195

0.04

7-0

.205

-0.0

52

Thi

sta

ble

repo

rts

stat

istic

son

retu

rns

oneq

ual-

wei

ghte

dlo

ng/s

hort

curr

ency

port

folio

s.E

ach

port

folio

isfo

rmed

acco

rdin

gto

asi

ngle

sign

alan

dre

bala

nced

each

mon

th.P

ortf

olio

goes

long

curr

enci

esw

ithth

ehi

ghes

tone

-thi

rdva

lue

ofa

sign

alan

dgo

essh

ortc

urre

ncie

sw

ithth

elo

wes

tone

-thi

rdva

lue

ofa

sign

al.

Port

folio

retu

rns

are

neto

fle

ndin

gan

dbo

rrow

ing

atth

ein

terb

ank

rate

.Pa

nelA

repo

rts

resu

ltsfo

ral

ldev

elop

edco

untr

ies

and

Pane

lBre

port

sre

sults

foro

nly

the

G10

curr

enci

es.T

heSh

arpe

ratio

sar

ean

nual

ized

.Pas

t3-m

onth

exce

ssFX

retu

rnis

the

cum

ulat

ive

curr

ency

retu

rnin

exce

ssof

lend

ing

and

borr

owin

gat

the

inte

rban

kra

te.T

hesa

mpl

eis

from

1979

:01

to20

07:0

5.

27

Tabl

e4:

Ret

urns

onsi

gnal

-wei

ghte

dcu

rren

cypo

rtfo

lios

Sign

al

Meanreturn(%permonth)

Standarddeviation(%permonth)

Sharperatio

Minimumreturn(%permonth)

Maximumreturn(%permonth)

Skewness

Cor

rela

tions

Pane

lA:A

llD

evel

oped

Cou

ntri

esSh

ortr

ate

diff

.0.

253

0.92

60.

946

-3.8

73.

74-0

.614

1.00

0∆

Shor

trat

edi

ff.

0.16

70.

883

0.65

5-3

.03

5.19

0.66

90.

297

1.00

0L

ong

rate

diff

.0.

192

0.87

20.

761

-4.5

82.

15-0

.950

0.92

60.

270

1.00

0∆

Lon

gra

tedi

ff.

0.14

10.

843

0.58

1-4

.75

3.21

-0.6

620.

093

0.29

50.

074

1.00

0Te

rmsp

read

diff

.-0

.248

0.85

6-1

.001

-3.8

22.

800.

039

-0.8

38-0

.258

-0.5

96-0

.117

1.00

0∆

Term

spre

addi

ff.

-0.0

620.

867

-0.2

46-4

.20

3.16

-0.6

45-0

.182

-0.7

58-0

.182

0.27

40.

114

1.00

0Pa

st3-

mon

thex

cess

FXre

turn

0.20

91.

182

0.61

3-3

.71

2.44

-0.2

960.

139

0.06

90.

167

0.12

6-0

.128

0.04

0

Pane

lB:G

10C

urre

ncie

sOnl

ySh

ortr

ate

diff

.0.

297

1.26

10.

816

-4.9

33.

37-0

.892

1.00

0∆

Shor

trat

edi

ff.

0.18

21.

032

0.61

0-4

.11

5.03

0.30

60.

108

1.00

0L

ong

rate

diff

.0.

222

1.25

80.

612

-4.8

83.

26-0

.870

0.91

70.

056

1.00

0∆

Lon

gra

tedi

ff.

0.19

91.

128

0.61

0-3

.98

4.33

-0.1

55-0

.065

0.22

5-0

.092

1.00

0Te

rmsp

read

diff

.-0

.295

1.08

0-0

.945

-4.7

54.

250.

138

-0.7

71-0

.167

-0.5

13-0

.028

1.00

0∆

Term

spre

addi

ff.

-0.0

341.

100

-0.1

07-4

.75

4.36

-0.2

81-0

.106

-0.6

48-0

.065

0.45

70.

089

1.00

0Pa

st3-

mon

thex

cess

FXre

turn

0.21

41.

306

0.56

9-4

.64

3.25

-0.1

400.

166

0.17

00.

153

0.03

8-0

.185

-0.0

72

Thi

sta

ble

repo

rts

stat

istic

son

retu

rns

ondi

ffer

entia

l-w

eigh

ted

long

/sho

rtcu

rren

cypo

rtfo

lios.

Eac

hpo

rtfo

liois

form

edac

cord

ing

toa

sing

lesi

gnal

and

reba

lanc

edea

chm

onth

.E

ach

sign

alis

de-m

eane

dan

dre

scal

edsu

chth

atpo

sitiv

e(n

egat

ive)

valu

essu

mto

one

(neg

ativ

eon

e).

Port

folio

goes

long

(sho

rt)c

urre

ncie

sw

ithw

eigh

tsco

rres

ondi

ngto

de-m

eane

dan

dre

scal

edsi

gnal

.Por

tfol

iore

turn

sar

ene

tofl

endi

ngan

dbo

rrow

ing

atth

ein

terb

ank

rate

.Pan

elA

repo

rts

resu

ltsfo

rall

deve

lope

dco

untr

ies

and

Pane

lBre

port

sre

sults

foro

nly

the

G10

curr

enci

es.

The

Shar

pera

tios

are

annu

aliz

ed.

Past

3-m

onth

exce

ssFX

retu

rnis

the

cum

ulat

ive

curr

ency

retu

rnin

exce

ssof

lend

ing

and

borr

owin

gat

the

inte

rban

kra

te.T

hesa

mpl

eis

from

1979

:01

to20

07:0

5.

28

Table 5: Univariate Currency Predictability Regressions

Excess FX return horizon: 1-m

onth

ahea

d

2-m

onth

ahea

d

3-m

onth

ahea

d

6-m

onth

ahea

d

9-m

onth

ahea

d

12-m

onth

ahea

d

Panel A: Predictability with short ratesShort rate diff. 0.600** 0.561** 0.526** 0.474** 0.478** 0.460**

(0.146) (0.124) (0.115) (0.102) (0.097) (0.101)Constant -0.183** -0.188** -0.177** -0.160** -0.162** -0.156**

(0.066) (0.055) (0.051) (0.045) (0.043) (0.045)R-squared 0.614 0.631 0.640 0.666 0.651 0.655

Panel B: Predictability with changes in short rates∆ Short rate diff. 0.433** 0.336** 0.247** 0.139** 0.226** 0.213**

(0.115) (0.089) (0.061) (0.039) (0.054) (0.055)Constant -0.099* -0.075+ -0.037 0.008 -0.036 -0.033

(0.049) (0.039) (0.030) (0.018) (0.030) (0.027)R-squared 0.613 0.627 0.634 0.657 0.644 0.649

Panel C: Predictability with long ratesLong rate diff. 0.481** 0.444** 0.402** 0.354** 0.364** 0.343**

(0.121) (0.100) (0.093) (0.080) (0.079) (0.080)Constant -0.123* -0.129** -0.115** -0.100** -0.105** -0.098**

(0.054) (0.043) (0.040) (0.034) (0.033) (0.034)R-squared 0.613 0.629 0.637 0.662 0.647 0.652

Panel D: Predictability with changes in long rates∆ Long rate diff. 0.396** 0.338** 0.215** 0.082+ 0.160* 0.154*

(0.134) (0.110) (0.083) (0.043) (0.067) (0.072)Constant -0.080 -0.076 -0.021 0.036+ -0.003 -0.003

(0.064) (0.052) (0.037) (0.018) (0.032) (0.031)R-squared 0.613 0.627 0.634 0.656 0.642 0.648

This table reports pooled-panel univariate regression results of future excess FX returns on yieldcurve predictors. Dependent variables are cumulative excess FX returns over 1-month to 12-month horizons expressed in % per month. Independent variables are normalized to a uniformdistribution between 0 and 1. Regressions include month fixed-effects. Standard errors are hetero-skedasticity robust and double-clustered by month and currency. Double asterisk (**), asterisk(*) and plus (+) represent statistical significance at the 1%, 5% and 10% levels, respectively. Thenumber of observations is 5261, spans 341 months and represents 22 currencies in all developedcountries.

29

Table 6: Multivariate Currency Predictability Regressions

FX excess return horizon: 1-m

onth

ahea

d

2-m

onth

ahea

d

3-m

onth

ahea

d

6-m

onth

ahea

d

9-m

onth

ahea

d

12-m

onth

ahea

d

Panel A: Predictability of based on short rateShort rate diff. 0.585** 0.549** 0.517** 0.470** 0.470** 0.453**

(0.142) (0.121) (0.113) (0.102) (0.095) (0.100)∆ Short rate diff. 0.411** 0.315** 0.227** 0.121** 0.208** 0.196**

(0.111) (0.086) (0.058) (0.036) (0.052) (0.051)Constant -0.380** -0.339** -0.286** -0.218** -0.262** -0.250**