Embed Size (px)

Citation preview

Global change, labour market

dynamics and the sectoral structure

of production

SECOND EUROPE–LATIN AMERICA ECONOMIC FORUM

Paris, OECD, 20 - 21 May 2014

Tilman Altenburg,

Deutsches Institut für Entwicklungspolitik/ German Development Institute (DIE)

© Deutsches Institut für Entwicklungspolitik (DIE) 2

– Labour market performance depends on systemic

relationships between fiscal policies, exchange rate

polcies, industrial policies, education policies, labour

market policies, social policies etc.

– Focus in this section: links between global change,

labour market dynamics and sectoral structure of

production (=> incomplete picture!)

– ... and a comparative perspective on Europe and LAC

© Deutsches Institut für Entwicklungspolitik (DIE) 3

Europe: stylized picture

Unemployment rates in EU (11%), Euro area (12%) unprecedented in

recent history:

– Financial crisis as a trigger: failure to manage financial markets well

& accumulation of fiscal deficits => recession, deleveraging

– But also deeper structural problems in a global economy in which

wealth is shifting from OECD to emerging markets, mainly Asia

– Real wage increases in many countries > productivity growth

– Eastern & Southern European countries in a sandwich position

– Skills not matching labour market demand, long unemployment

spells indicate structural problems; mismatch esp for unskilled

workers and those who lost public sector jobs.

Essentially, productivity agenda is needed !

© Deutsches Institut für Entwicklungspolitik (DIE) 4

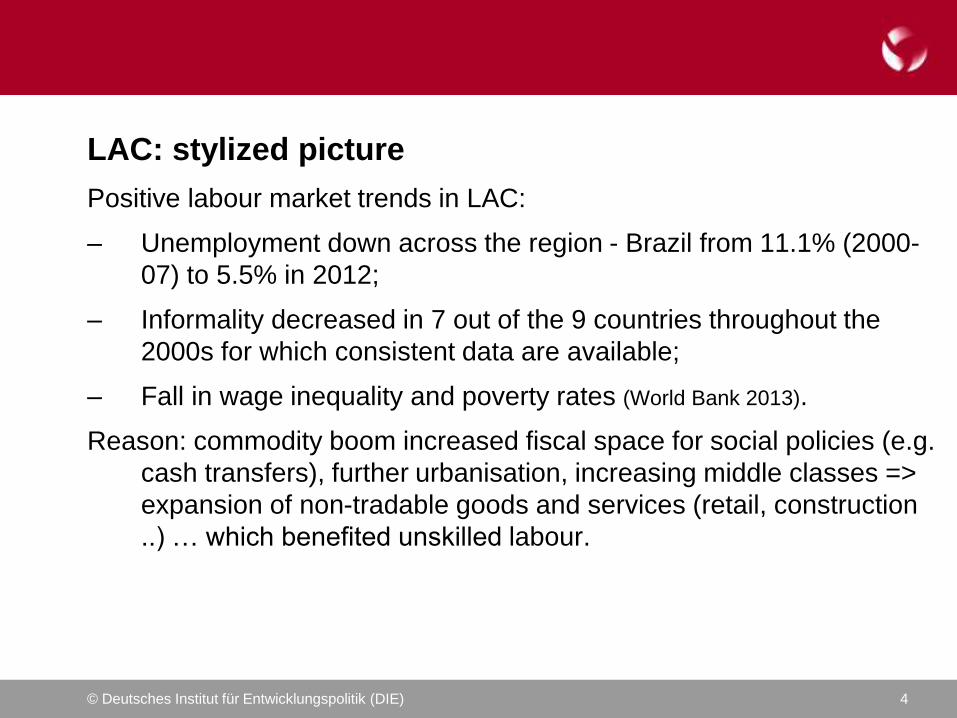

LAC: stylized picture

Positive labour market trends in LAC:

– Unemployment down across the region - Brazil from 11.1% (2000-

07) to 5.5% in 2012;

– Informality decreased in 7 out of the 9 countries throughout the

2000s for which consistent data are available;

– Fall in wage inequality and poverty rates (World Bank 2013).

Reason: commodity boom increased fiscal space for social policies (e.g.

cash transfers), further urbanisation, increasing middle classes =>

expansion of non-tradable goods and services (retail, construction

..) … which benefited unskilled labour.

© Deutsches Institut für Entwicklungspolitik (DIE) 5

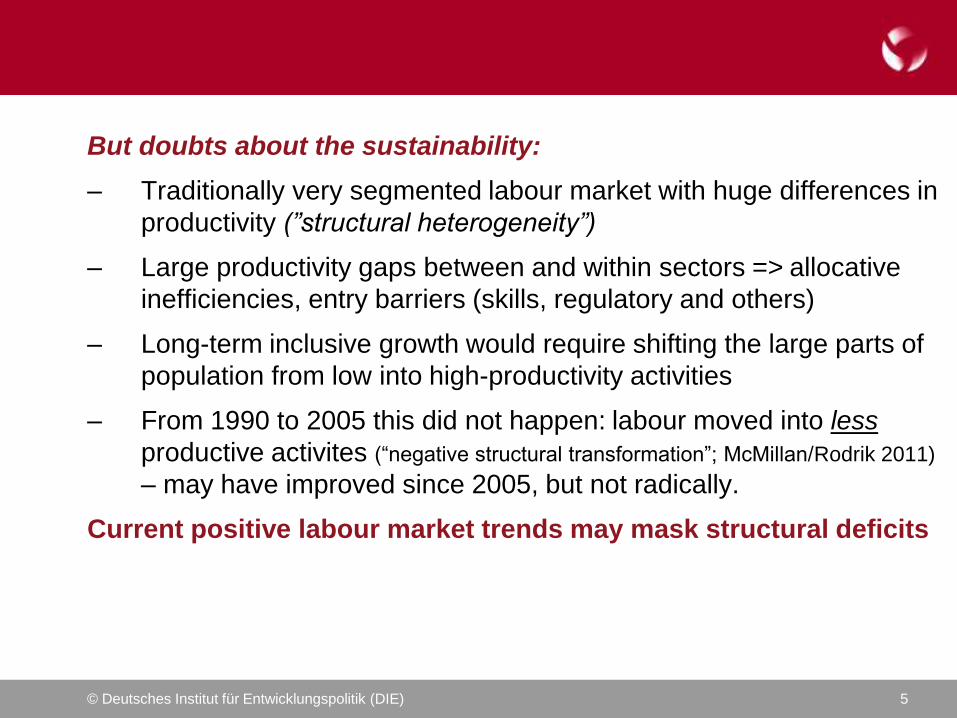

But doubts about the sustainability:

– Traditionally very segmented labour market with huge differences in

productivity (”structural heterogeneity”)

– Large productivity gaps between and within sectors => allocative

inefficiencies, entry barriers (skills, regulatory and others)

– Long-term inclusive growth would require shifting the large parts of

population from low into high-productivity activities

– From 1990 to 2005 this did not happen: labour moved into less

productive activites (“negative structural transformation”; McMillan/Rodrik 2011)

– may have improved since 2005, but not radically.

Current positive labour market trends may mask structural deficits

© Deutsches Institut für Entwicklungspolitik (DIE)

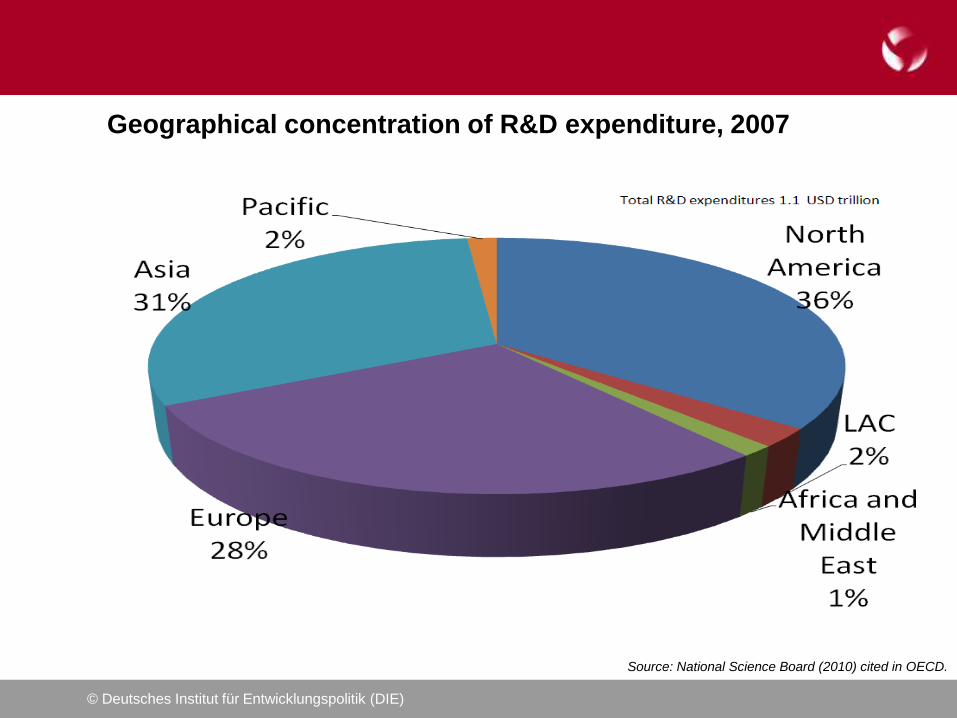

Geographical concentration of R&D expenditure, 2007

Source: National Science Board (2010) cited in OECD.

© Deutsches Institut für Entwicklungspolitik (DIE)

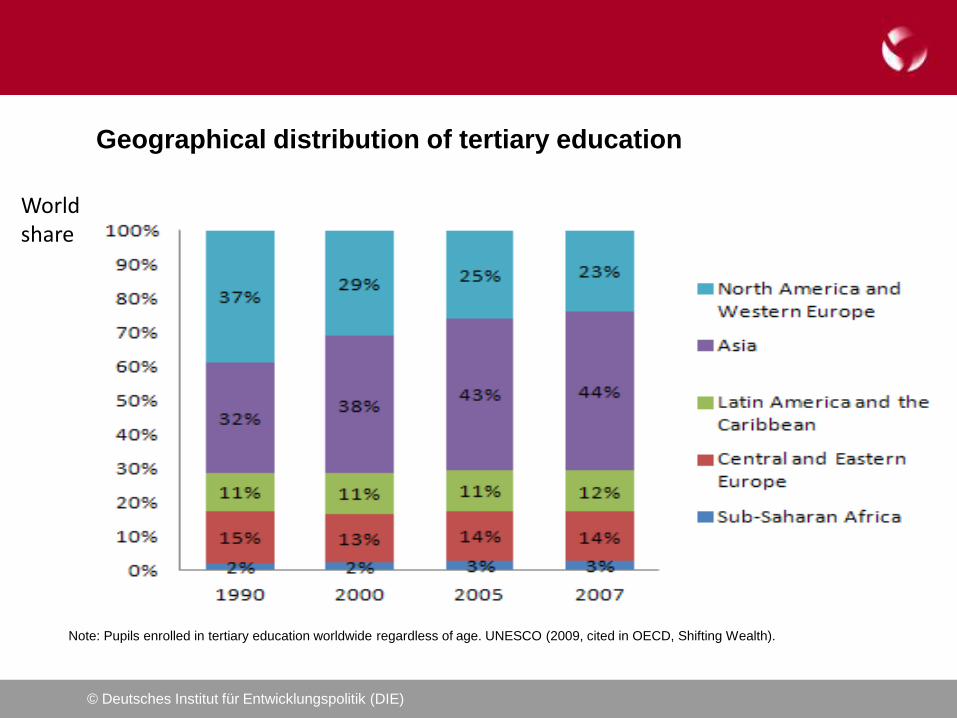

Geographical distribution of tertiary education

Note: Pupils enrolled in tertiary education worldwide regardless of age. UNESCO (2009, cited in OECD, Shifting Wealth).

World share

© Deutsches Institut für Entwicklungspolitik (DIE) 8

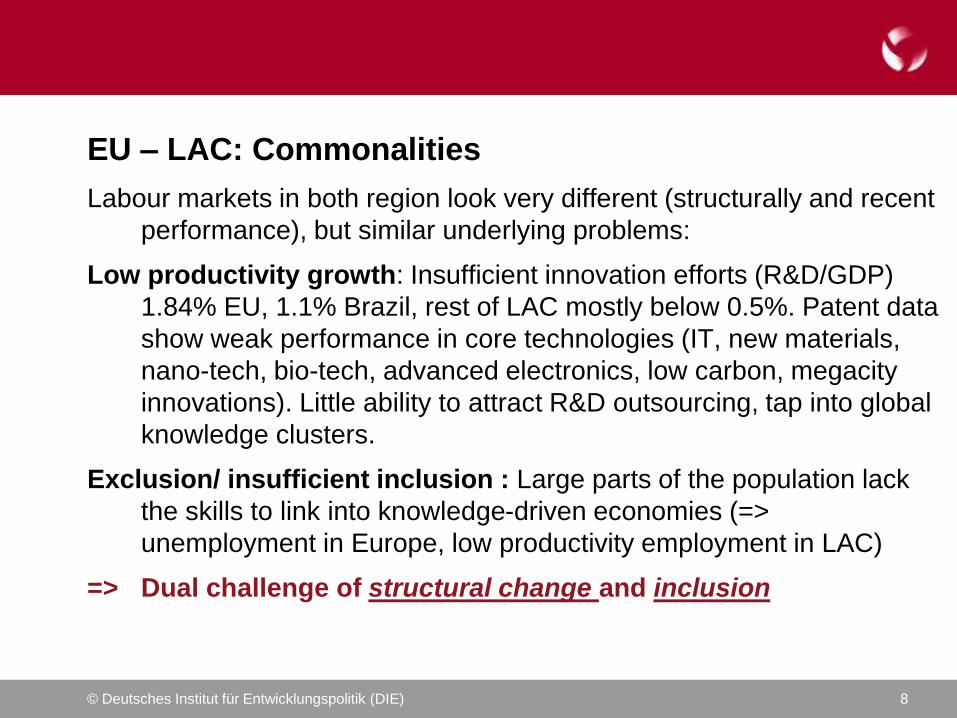

EU – LAC: Commonalities

Labour markets in both region look very different (structurally and recent

performance), but similar underlying problems:

Low productivity growth: Insufficient innovation efforts (R&D/GDP)

1.84% EU, 1.1% Brazil, rest of LAC mostly below 0.5%. Patent data

show weak performance in core technologies (IT, new materials,

nano-tech, bio-tech, advanced electronics, low carbon, megacity

innovations). Little ability to attract R&D outsourcing, tap into global

knowledge clusters.

Exclusion/ insufficient inclusion : Large parts of the population lack

the skills to link into knowledge-driven economies (=>

unemployment in Europe, low productivity employment in LAC)

=> Dual challenge of structural change and inclusion

© Deutsches Institut für Entwicklungspolitik (DIE) 9

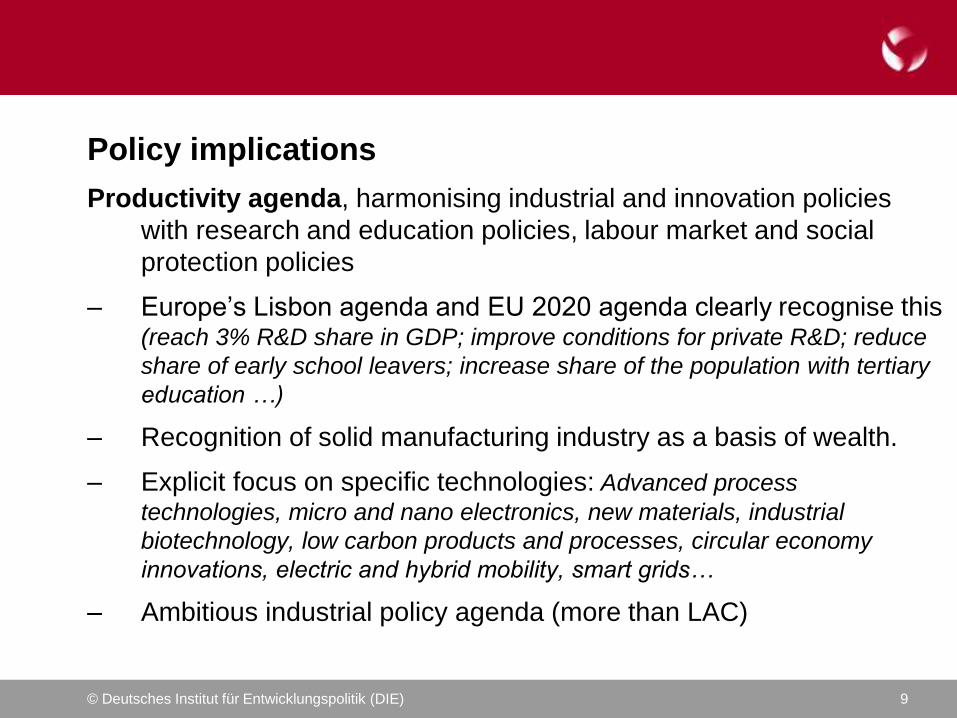

Policy implications

Productivity agenda, harmonising industrial and innovation policies

with research and education policies, labour market and social

protection policies

– Europe’s Lisbon agenda and EU 2020 agenda clearly recognise this (reach 3% R&D share in GDP; improve conditions for private R&D; reduce

share of early school leavers; increase share of the population with tertiary

education …)

– Recognition of solid manufacturing industry as a basis of wealth.

– Explicit focus on specific technologies: Advanced process

technologies, micro and nano electronics, new materials, industrial

biotechnology, low carbon products and processes, circular economy

innovations, electric and hybrid mobility, smart grids…

– Ambitious industrial policy agenda (more than LAC)

© Deutsches Institut für Entwicklungspolitik (DIE) 10

Policy implications

– but Lisbon targets not achieved, little progress. … no political

majorities for redirecting expenditure patterns.

– Government spending in indebted countries likely to remain low =>

greater focus on policy reforms to reduce labour costs, increase and

work incentives, extending the time span people work …

– … not the „high road“ strategy one would like to see, socially

conflictive, but unavoidable when competitiveness has eroded and

fiscal space narrowed.

© Deutsches Institut für Entwicklungspolitik (DIE) 11

Policy implications

Link between competitiveness, structural change and jobs (and

income) complicated.

Competitiveness goes along with increasing labour productivity =>

labour absorption only increases if growth > labour saving effects

Trade-offs between “job creation” and “productivity” agendas (at least

temporarily):

© Deutsches Institut für Entwicklungspolitik (DIE) 12

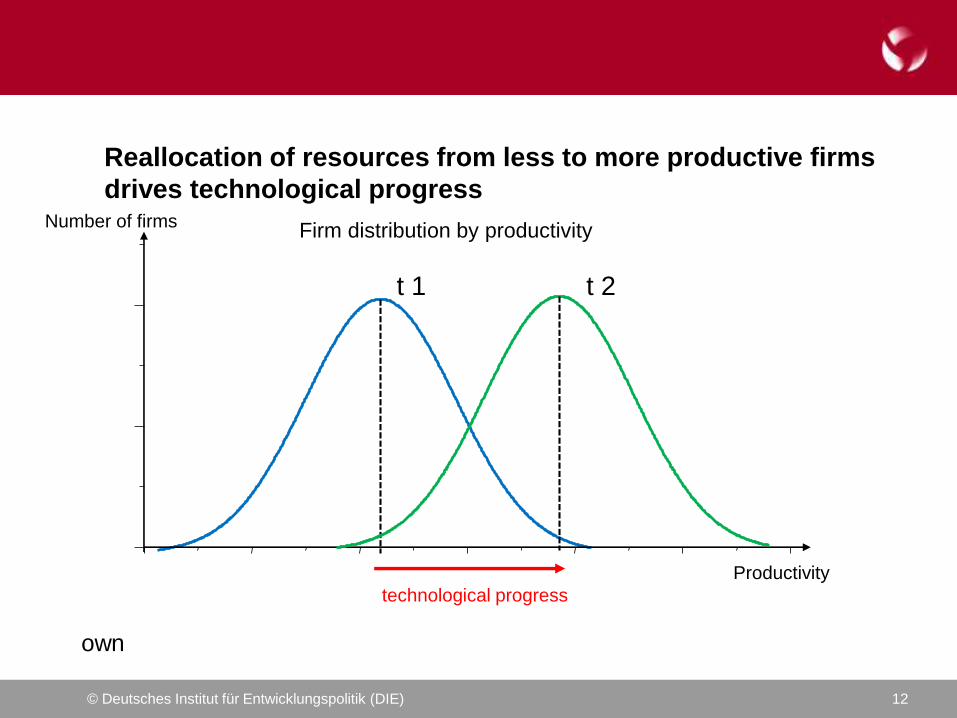

Number of firms

Productivity

Firm distribution by productivity

t 2t 1

technological progress

Reallocation of resources from less to more productive firms

drives technological progress

own

© Deutsches Institut für Entwicklungspolitik (DIE) 13

Policy implications

Protecting sunset industries, SMEs, peripheral regions may preserve

jobs but slow down productivity-enhancing structural transformation

• Benefits to small firms may create incentives for sub-optimal firm sizes

• grants to firms in disadvantaged regions may keep uncompetitive firms

alive; (UK: grants helped local employment creation; but employment growth only

in small less productive firms => overall productivity down (Criscuolo et al. 2012).

– Encouraging high productivity activities makes sense

– Encouraging below average productivity firms makes sense

• if they absorb production factors from even less productive activities

• If they increase productivity of the entire production system via

economies of specilization;

– … but not if resources move towards lower productivity (e.g. when

crowding out of less competitive manufacturing industries pushes

people into informality; or when firms deliberately stay small)

© Deutsches Institut für Entwicklungspolitik (DIE) 14

A final word

– Complex trade-offs between job-focused and productivity focused

policies, macroeconomic management, social and education

policies

– No technically optimal combination: How much people are willing to

sacrifice for a competitiveness agenda (in terms of real wage

reduction, longer work hours, hire&fire, environmental trade-offs … )

varies between societies

– Societies need to be aware of the trade-offs and negotiate their own

consensus

More peer reviews, but careful with country rankings.

© Deutsches Institut für Entwicklungspolitik (DIE) 15

Thank you for your attention!

Deutsches Institut für Entwicklungspolitik/German Development Institute (DIE)

Tulpenfeld 6

D-53113 Bonn

Telefon: +49 (0)228-949 27-0

E-Mail: [email protected]

www.die-gdi.de

www.facebook.com/DIE.Bonn

www.youtube.com/DIEnewsflash