Embed Size (px)

Citation preview

Accenture 2015 Global Structural Reform StudyUnlocking the Potential of Global Structural Reform

2

The financial crisis of 2007-2008 highlighted the dangers of a financial system that was improperly aligned with the goals of systemic risk management. Since the crisis, global regulators have sought to re-shape institutions to be more resilient through a series of structural reform regulations. Today, Global Structural Reform (GSR) is presenting an even more complex ecosystem for financial institutions and, as such, constitutes a keyagenda point for senior management driving the future strategy of their post-crisis institutions.

3

Accenture’s 2015 Global Structural Reform Study – based on a survey of 131 banking, insurance and capital markets institutions across regions – confirms that, while institutions are investing in their response to GSR, their plans still appear focused on meeting regulatory demands alone, rather than accounting for the more strategic implications of structural reform. Our study concluded:

GSR is re-writing the financial services landscapePublication of regulations related to structural reform continues at a relentless pace, with rules often developed at a jurisdictional level without clear convergence. In our view, it seems inevitable that the financial services landscape will be re- written given the cumulative impact of GSR, especially for internationally active banks, meaning that reliance on traditional ways of working will no longer be viable. As a result, institutions will be faced with hard choices about their post- crisis business model.Investment is clear, but strategy less soThe sheer volume of GSR regulations and the complexity of changes they demand is driving significant investment in talent and technology as institutions organize theirresponses. Our experience suggests a need to validate whether strategic planning will fully account for the strategic implications of GSR, going beyond mere compliance and delivering long-term value for the institution.Unlock the potential of GSRGSR regulations are adding further complexity to a landscape already beset with macroeconomic and industry disruptions.Institutions cannot continue to solve for point regulations without considering other competing or complementary forces. There is no one solution for responding to this challenge; however, our experience suggests three principles to help extract greater value from the investment made:

1. Organize a long-term responseInstitutions need to think end-to- end across regulations, businesses and geographies, and be holistic in assessing and communicating impacts across the operating model to make smart investments and avoid multiple, competing projects.2. Unlock potential in a new ecosystemRemaining competitive and viable in the long term will require institutions to identify and capture the potential for innovationand improved financial performance provided by the new ecosystem.3. Demonstrate value to key stakeholdersThe value of GSR can only be realized if planning is effectively adopted throughout the business. As firms move past initial compliance, further tuning of the new operating model will be needed to help retain engagement and support from internal and external stakeholders.

Time for bold, strategic thinkingGSR is much more than another set of regulatory requirements. To help their institutions remain competitive and viable for the long term, senior management should approach structural reform with the same bold, strategic thinking as they are using for other industry challenges.

4

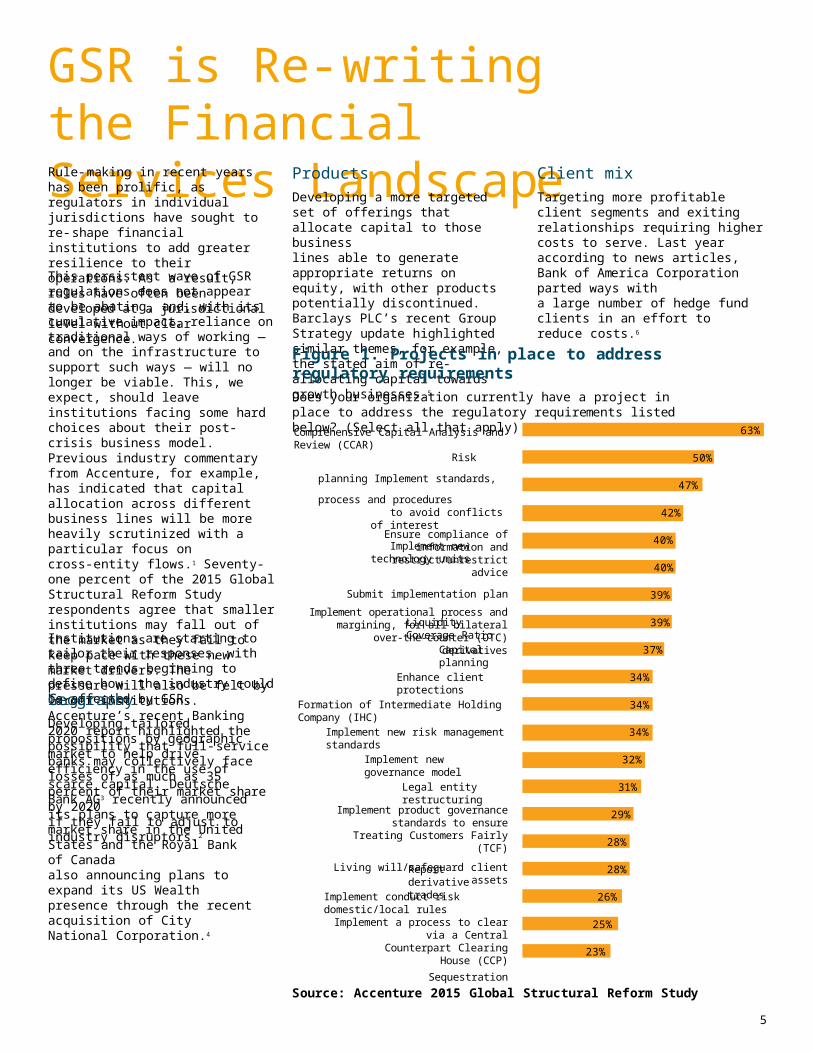

GSR is Re-writing the Financial Services LandscapeRule-making in recent years has been prolific, as regulators in individual jurisdictions have sought to re-shape financial institutions to add greater resilience to their operations. As a result, rules have often been developed at a jurisdictional level without clear convergence.This persistent wave of GSR regulations does not appear to be abating, and, with itscumulative impact, reliance on traditional ways of working — and on the infrastructure to support such ways — will no longer be viable. This, we expect, should leave institutions facing some hard choices about their post- crisis business model. Previous industry commentary from Accenture, for example, has indicated that capital allocation across different business lines will be more heavily scrutinized with a particular focus oncross-entity flows.1 Seventy- one percent of the 2015 Global Structural Reform Study respondents agree that smaller institutions may fall out of the market as they fail to keep pace with these new market drivers. Thepressure will also be felt by larger institutions. Accenture’s recent Banking 2020 report highlighted the possibility that full- service banks may collectively face losses of as much as 35 percent of their market share by 2020if they fail to adjust to industry disruptors.2

Institutions are starting to tailor their responses, with three trends beginning to define how the industry could be affected by GSR.GeographyDeveloping tailored propositions by geographic market to help drive efficiency in the use of scarce capital. Deutsche Bank AG3 recently announced its plans to capture more market share in the United States and the Royal Bank of Canadaalso announcing plans to expand its US Wealth presence through the recent acquisition of City National Corporation.4

ProductsDeveloping a more targeted set of offerings that allocate capital to those businesslines able to generate appropriate returns on equity, with other products potentially discontinued. Barclays PLC’s recent Group Strategy update highlighted similar themes, for example, the stated aim of re-allocating capital towards growth businesses.5

Client mixTargeting more profitable client segments and exiting relationships requiring higher costs to serve. Last year according to news articles, Bank of America Corporation parted ways witha large number of hedge fund clients in an effort to reduce costs.6

Figure 1. Projects in place to address regulatory requirementsDoes your organization currently have a project in place to address the regulatory requirements listed below? (Select all that apply)Comprehensive Capital Analysis and Review (CCAR)

Risk planning

Implement standards, process and proceduresto avoid conflicts of interest

Implement new technology unitsEnsure compliance of information

and restrict/unrestrict advice

Submit implementation plan

Implement operational process and margining, for all bilateral over-the-counter (OTC) derivatives

Liquidity Coverage Ratio

Capital planning

Enhance client protections

Formation of Intermediate Holding Company (IHC)

Implement new risk management standards

Implement new governance model

Legal entity restructuring

Implement product governance standards to ensure Treating Customers Fairly

(TCF)

Living will/safeguard client assetsReport derivative trades

Implement conduct risk domestic/local rules

Implement a process to clear via a Central Counterpart Clearing House (CCP)

Sequestration

63%

50%

47%

42%

40%

40%

39%

39%

37%

34%

34%

34%

32%

31%

29%

28%

28%

26%

25%

23%

Source: Accenture 2015 Global Structural Reform Study

5

6

Figure 2. Forecasted technology and non-technology spendWhat is your organization’s anticipated technology and non-technology spend (in USD) for FY14, in order to address the global regulatory change requirement?

Source: Accenture 2015 Global Structural Reform Study

>$500m

$250m - $500m

$100m - $250m

$10m - $100m

$1m - $10m

$0m - $1m

Technology Spend

Non-Technology Spend

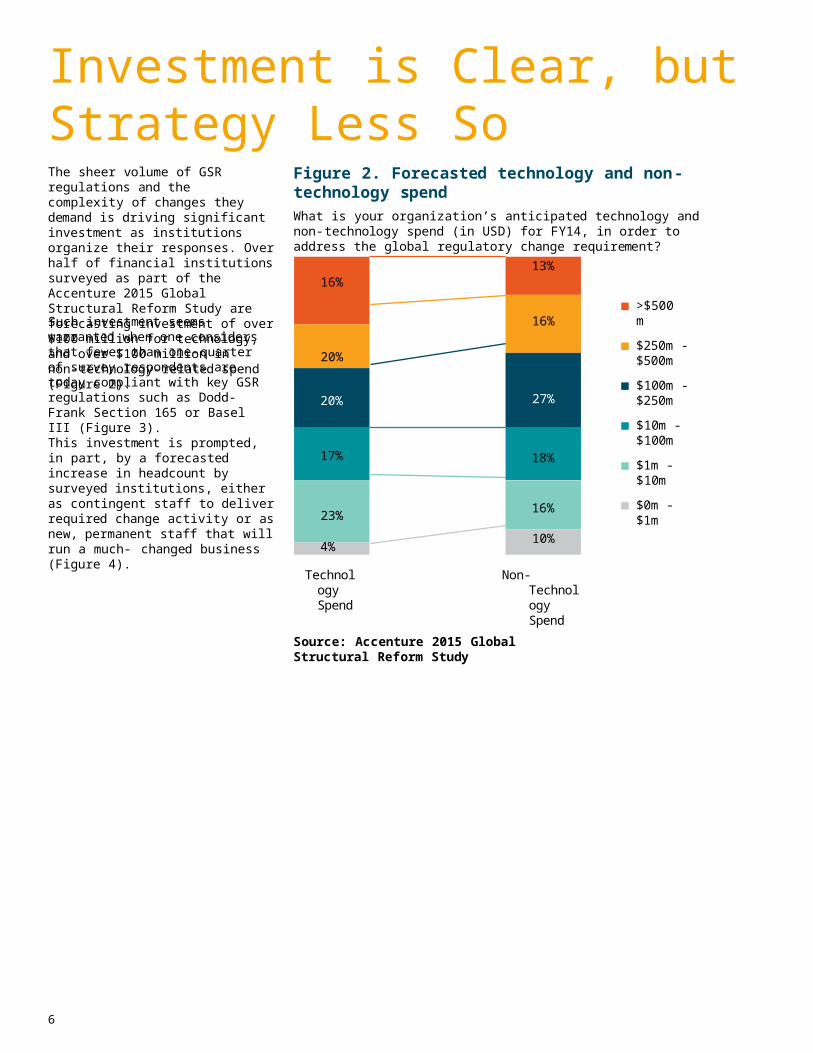

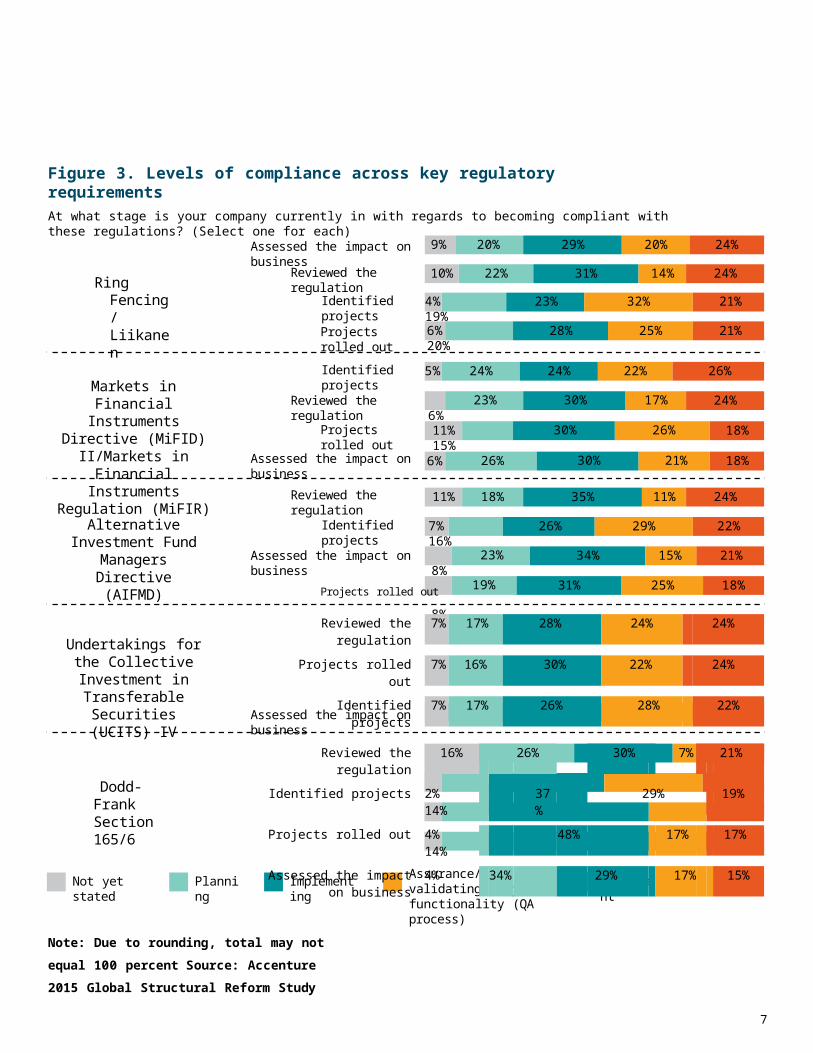

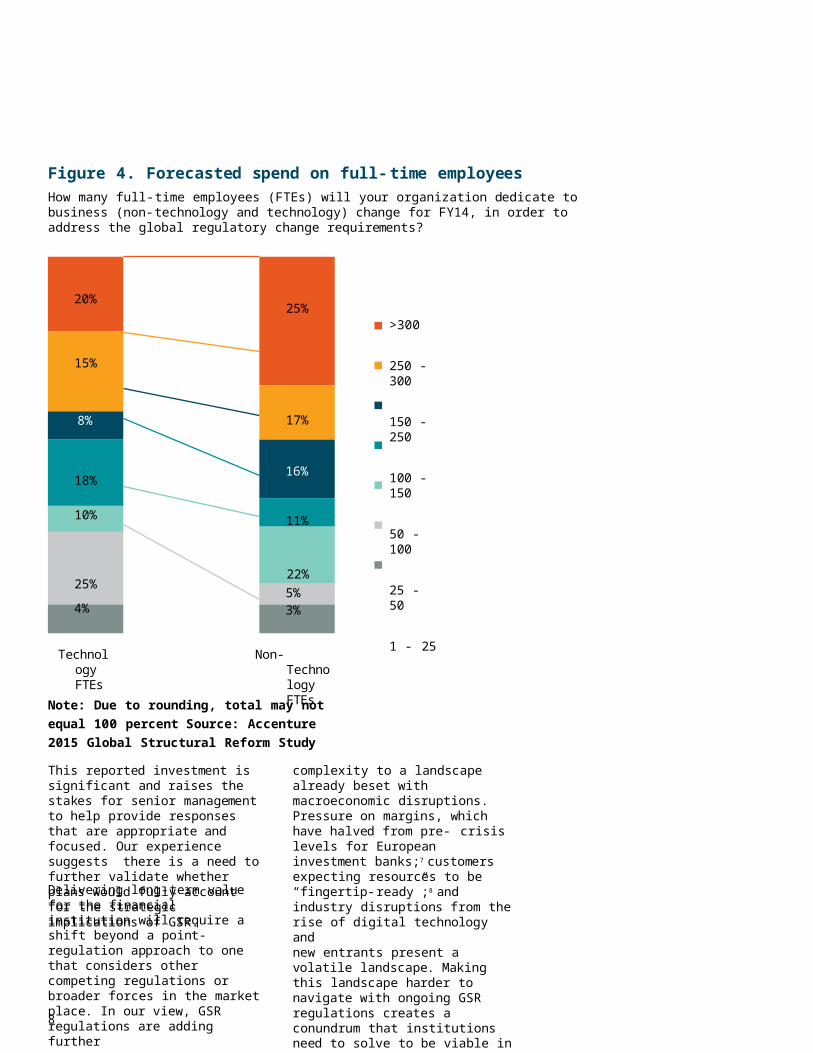

Investment is Clear, but Strategy Less SoThe sheer volume of GSR regulations and the complexity of changes they demand is driving significant investment as institutionsorganize their responses. Over half of financial institutions surveyed as part of the Accenture 2015 Global Structural Reform Study are forecasting investment of over $100 million for technology, and over $100 million innon-technology-related spend (Figure 2).Such investment seems warranted when one considers that fewer than one-quarter of survey respondents are today compliant with key GSR regulations such as Dodd- Frank Section 165 or Basel III (Figure 3).This investment is prompted, in part, by a forecasted increase in headcount by surveyed institutions, either as contingent staff to deliver required change activity or as new, permanent staff that will run a much- changed business (Figure 4).

16%13%

16%

20%

27%20%

17% 18%

23%16%

10%4%

7

Note: Due to rounding, total may not equal 100

percent Source: Accenture 2015 Global Structural

Reform Study

Figure 3. Levels of compliance across key regulatory requirementsAt what stage is your company currently in with regards to becoming compliant with these regulations? (Select one for each)

Reviewed the regulation 10% 22% 31% 14% 24%

24%

24%

22%

21%

21%

11%

8%

18%

18%

7% 16%

35%

34%

31% 25%

11%

29%

15%

15%

24%5% 24% 22% 26%

26%

6% 20% 28% 25% 21%

23%

23%

22%

17%30%

34%

18%11% 15% 30% 26%

4% 19% 23% 32% 21%

18%26%6% 30% 21%

20%9% 20% 29% 24%Assessed the impact on business

Projects rolled out

Identified projects

Identified projects

Reviewed the regulation 6%

Assessed the impact on business

Projects rolled out

Reviewed the regulation

Identified projects

Assessed the impact on business 8%

Projects rolled out 8%

Assessed the impact on business

Ring Fencing/ Liikanen

Markets in Financial Instruments Directive (MiFID)

II/Markets in Financial Instruments Regulation

(MiFIR)

Alternative Investment Fund Managers Directive

(AIFMD)

Undertakings for the Collective Investment in Transferable Securities

(UCITS) IV

19%

Dodd-Frank Section 165/6

Not yet stated Planning Implementing CompliantAssurance/validating project functionality (QA process)

Reviewed the regulation

7% 17% 28% 24% 24%

Projects rolled out 7% 16% 30% 22% 24%

Identified projects 7% 17% 26% 28% 22%

Reviewed the regulation 16% 26% 30% 7% 21%

Identified projects 2% 14% 37%

29% 19%

Projects rolled out 4% 14% 48% 17% 17%

Assessed the impact on business

4% 34% 29% 17% 15%

8

Note: Due to rounding, total may not equal 100 percent Source: Accenture 2015 Global Structural Reform Study

This reported investment is significant and raises the stakes for senior management to help provide responses that are appropriate and focused. Our experience suggests there is a need to further validate whether plans would fully account for the strategic implications of GSR.Delivering long-term value for the financial institution will require a shift beyond a point-regulation approach to one that considers other competing regulations or broader forces in the market place. In our view, GSR regulations are adding further

complexity to a landscape already beset with macroeconomic disruptions. Pressure on margins, which have halved from pre- crisis levels for European investment banks;7 customers expecting resources to be “fingertip-ready”;8 and industry disruptions from the rise of digital technology andnew entrants present a volatile landscape. Making this landscape harder to navigate with ongoing GSR regulations creates a conundrum that institutions need to solve to be viable in the long term, and to facilitate creating value from investments made.

Figure 4. Forecasted spend on full- time employeesHow many full-time employees (FTEs) will your organization dedicate to business (non-technology and technology) change for FY14, in order to address the global regulatory change requirements?

Technology FTEs

Non-Technology FTEs

>300

250 - 300

150 - 250

100 - 150

50 - 100

25 - 50

1 - 25

20%25%

15%

17%8%

18% 16%

11%10%

22%25%

5%

4% 3%

9

10

11

In our view, institutions cannot afford to adopt a wait-and-see approach in their response to the challenges presented by GSR. They should act quickly to seize the opportunity and not lose time strategically repositioning the organization, while remaining focused on solving for the ongoing pressures of regulatory compliance.

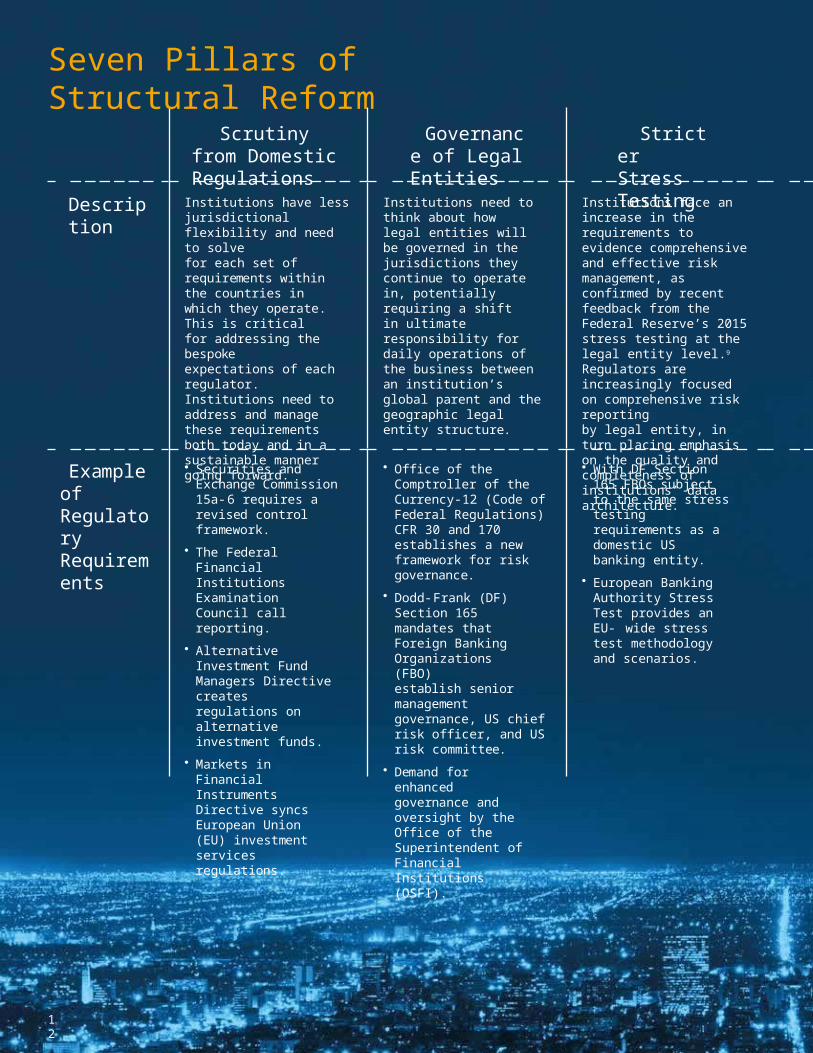

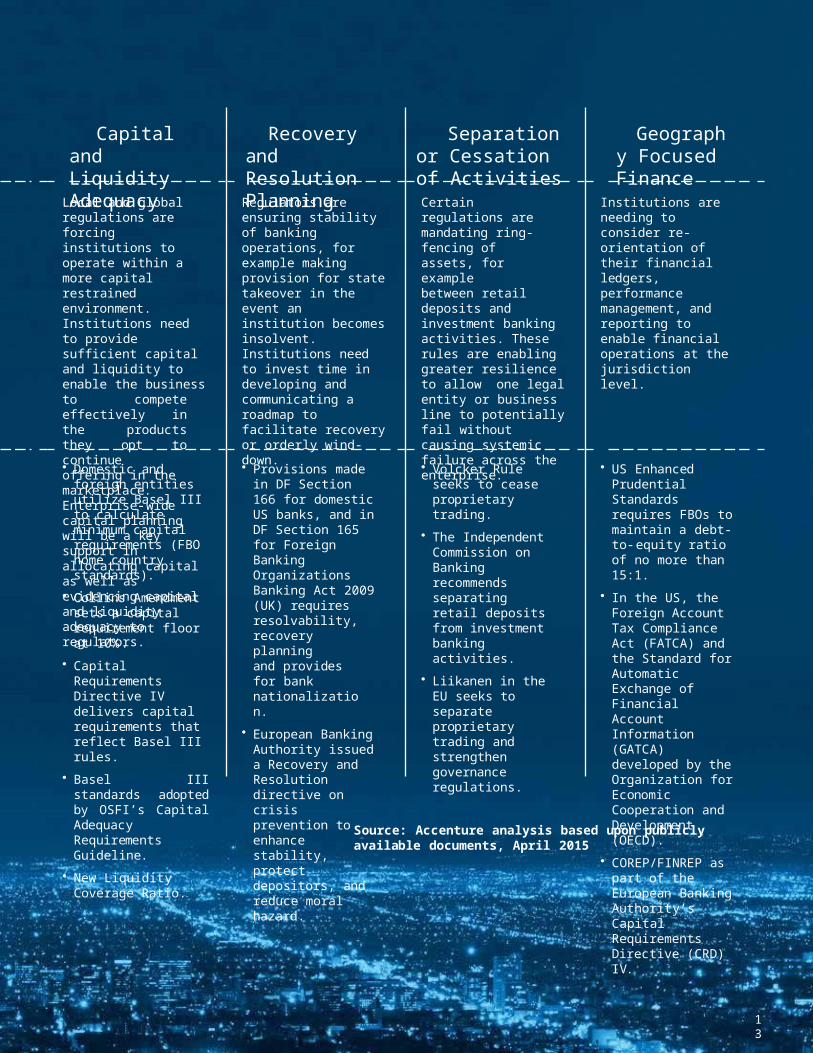

There is no one solution for responding to this challenge, and each institution’s response should be unique to its strengths and weaknessesas well as its future business expectations. However, our experience suggests the following three steps should be considered:1. Organize along-term responseInstitutions need to think end-to- end across regulations and geographies, and be holistic in assessing and communicating impacts across the business and operating model, both to streamline the change response and to identify smart investments. Ninety-sixpercent of the 2015 Global Structural Reform Study respondents cite the definition of a clear strategy and objectives as importantto driving an effective response.Accenture sees seven major pillars of structural reform that are forcingchange across each jurisdiction in which financial institutions operate. These can provide a framework for developing a longer-term plan. The chart that follows identifies the pillars and highlights some of the key regulatory requirements these structural reforms help address.

Unlock the Potential of GSR

12

Scrutiny from Domestic Regulations

Governance of Legal Entities

Stricter Stress Testing

Description

Institutions have less jurisdictional flexibility and need to solvefor each set of requirements within the countries in which they operate. This is critical for addressing the bespokeexpectations of each regulator. Institutions need to address and manage these requirements both today and in a sustainable manner going forward.

Institutions need to think about how legal entities will be governed in the jurisdictions they continue to operate in, potentially requiring a shiftin ultimate responsibility for daily operations of the business between an institution’s global parent and the geographic legal entity structure.

Institutions face an increase in the requirements to evidence comprehensive and effective risk management, as confirmed by recent feedback from the Federal Reserve’s 2015 stress testing at the legal entity level.9

Regulators are increasingly focused on comprehensive risk reportingby legal entity, in turn placing emphasis on the quality and completeness of institutions’ data architecture.

Example of Regulatory Requirements

• Securities and Exchange Commission 15a- 6 requires a revised control framework.

• The Federal Financial Institutions Examination Council call reporting.

• Alternative Investment Fund Managers Directive creates regulations on alternative investment funds.

• Markets in Financial Instruments Directive syncs European Union (EU) investment services regulations.

• Office of the Comptroller of the Currency-12 (Code of Federal Regulations) CFR 30 and 170 establishes a new framework for risk governance.

• Dodd-Frank (DF) Section 165 mandates that Foreign Banking Organizations (FBO)establish senior management governance, US chief risk officer, and US risk committee.

• Demand for enhanced governance and oversight by the Office of the Superintendent of Financial Institutions (OSFI).

• With DF Section 165 FBOs subject to the same stress testing requirements as a domestic US banking entity.

• European Banking Authority Stress Test provides an EU- wide stress test methodology and scenarios.

Seven Pillars of Structural Reform

13

Capital and Liquidity Adequacy

Recovery and Resolution Planning

Separation or Cessation of Activities

Geography Focused Finance

Local and global regulations are forcing institutions to operate within a more capital restrained environment.Institutions need to provide sufficient capital and liquidity to enable the businessto compete effectively in the products they opt to continue offering in themarketplace. Enterprise-wide capital planning will be a key support in allocating capital as well as evidencing capital and liquidity adequacy to regulators.

Regulators are ensuring stability of banking operations, for example making provision for state takeover in the event an institution becomes insolvent. Institutions need to invest time in developing and communicating a roadmap to facilitate recovery or orderly wind-down.

Certain regulations are mandating ring-fencing of assets, for examplebetween retail deposits and investment banking activities. These rules are enabling greater resilience to allow one legal entity or business line to potentially fail without causing systemic failure across the enterprise.

Institutions are needing to consider re-orientation of their financial ledgers,performance management, and reporting to enable financial operations at the jurisdiction level.

• Domestic and foreign entities utilize Basel III to calculate minimum capital requirements (FBO home country standards).

• Collins Amendment sets a capital requirement floor at 10% .

• Capital Requirements Directive IV delivers capital requirements that reflect Basel III rules.

• Basel III standards adopted by OSFI’s Capital Adequacy Requirements Guideline.

• New Liquidity Coverage Ratio.

• Provisions made in DF Section 166 for domestic US banks, and in DF Section 165 for Foreign Banking Organizations Banking Act 2009 (UK) requires resolvability, recovery planningand provides for bank nationalization.

• European Banking Authority issued a Recovery and Resolution directive on crisis prevention to enhance stability, protect depositors, and reduce moral hazard.

• Volcker Rule seeks to cease proprietary trading.

• The Independent Commission on Banking recommends separating retail deposits from investment banking activities.

• Liikanen in the EU seeks to separate proprietary trading and strengthen governance regulations.

• US Enhanced Prudential Standards requires FBOs to maintain a debt-to-equity ratio of no more than 15:1.

• In the US, the Foreign Account Tax Compliance Act (FATCA) and the Standard for Automatic Exchange of Financial Account Information (GATCA) developed by the Organization forEconomic Cooperation and Development (OECD).

• COREP/FINREP as part of the European Banking Authority’s Capital Requirements Directive (CRD) IV.

Source: Accenture analysis based upon publicly available documents, April 2015

14

15

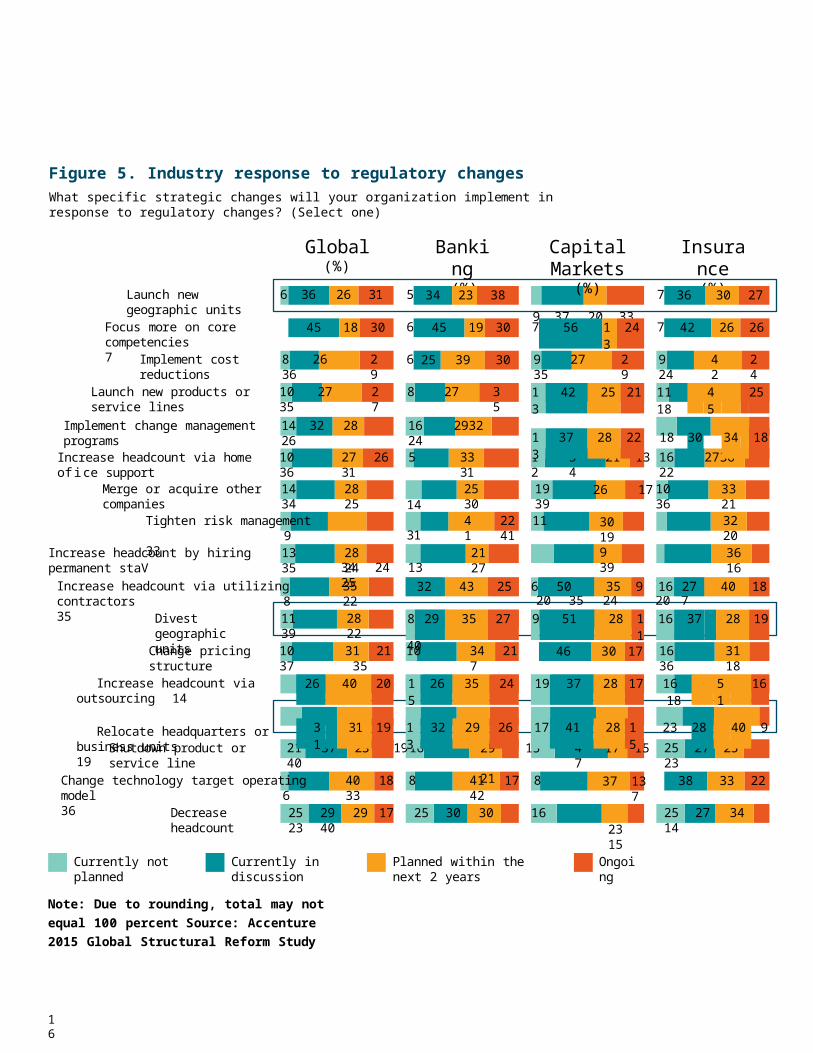

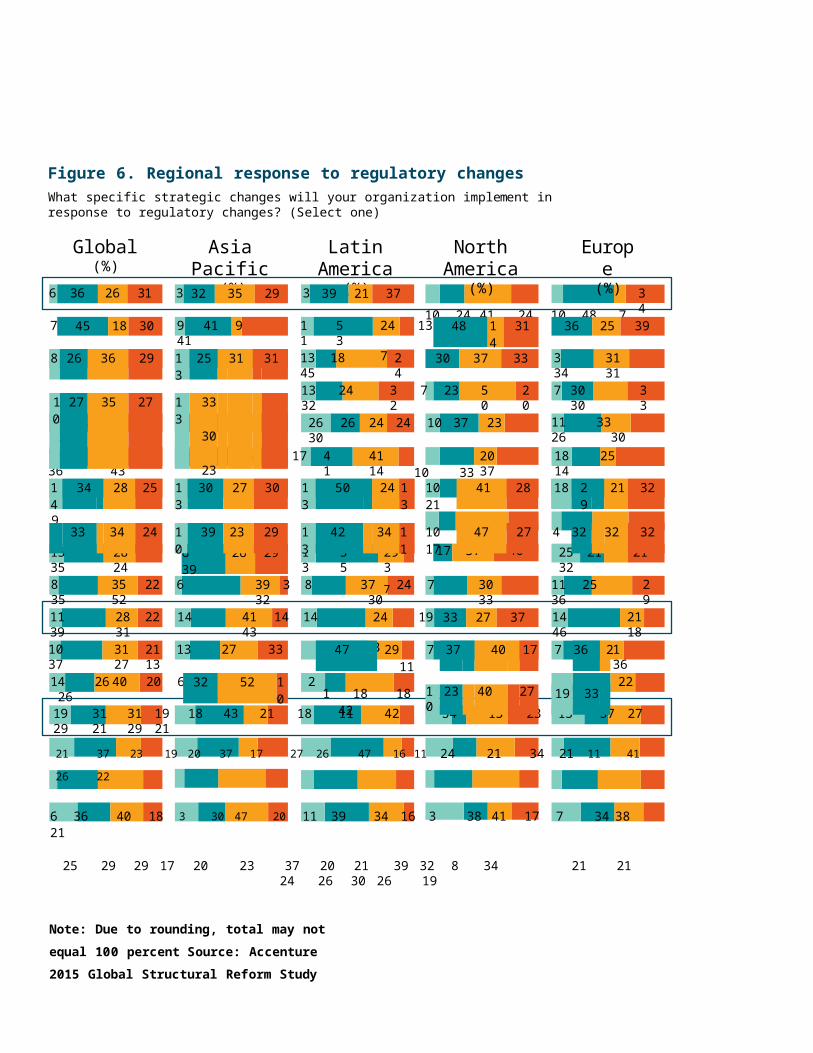

2. Unlock potential in a new ecosystemOnce regulatory needs and solutions are organized, institutions will need to think immediately about unlocking the potential value in changes and investments. In the case of major investments in change, institutions will need to closely consider the businesses they want to be in within this new financial services ecosystem.It will be too late to react whenregulatory changes have been implemented. If institutions want to remain competitive and viable for the long term, the time to act is now. Our experience would indicate the following areas may help financial institutions unlock new opportunities for sustainment and competitive growth.• Think local, not global. Institutions

need to consider the type of business they want to conduct in each of their locations and the practical operations required to sustain these businesses while best managing capital and costs.For multinational institutions, this would require aligning global capabilities with local capabilities in the jurisdictions in which they operate. This is a live discussion for many of our 2015 Global Structural Reform Study respondents, with 57 percent indicating they will tailor their geographic footprint in the next two years and half

divesting geographic units, relocating their headquarters, or business units (Figures 5 and 6). This shift in focus may lead to considering new technologies to help improve efficiency and effectiveness, or new operational models that arenot as cost, risk and capital-intensive. For example, we are seeing increased usage among our clients of managed services for know your customer (KYC) and post-trade processing utilities.

• Aim for market- driven specialization. Institutions can address competitive challenges by focusing resources and attention on certain customer, product, or geographic market segments. Such specialization can be performed upon thebasis of a common core of capabilities, and 48 percent of 2015 Global Structural Reform Study respondents indicate that they are indeed doubling down over the next two years on core competenciesin response to regulatory change. We believe the benefit of focusing on core competencies is greater local market recognition and competitive advantage.

• Focus on compliance and efficiency. Reputational risk could be a competitive advantage in the future, with clients and customers drawn to firms with strong ethical reputations that are also efficient in meeting their needs. To prepare for this possible opportunity, institutions should continue to integrate compliance into

their core processes. Expectations from regulators should continue to increase in this area, with the Federal Reserve recently announcing the first examination of US banks regarding their level of compliance with the Volcker Rule.10

• Think with an innovation mindset. Institutions should keep pace or even outpace niche providers in accessing the revenue streams that reflect the needs of today’s customers or clients. In our experience, digital- driven paymentsand portfolio management companies are capturing greater market share, and may become material threats to the longer-term viability of institutions’ business if sufficient planning is notin place. Sixty-two percent of our 2015 Global Structural Reform Studyrespondents are addressing this concern by planning to launch new products or services within the next two years.

Launch new geographic units

Implement cost reductions

Launch new products or service lines

Merge or acquire other companies

Divest geographic units

Change pricing structure

Shutdown product or service line

Decrease headcount

5

6

6

Focus more on core competencies 7

28 25 25 30

29

Change technology target operating model 6 36

8 26 36

10 27 35 35

35 22

28 22

27

14 34

Increase headcount via utilizing contractors 8 35

11 39

10 37

Increase headcount via outsourcing14

Relocate headquarters or business units19

8 27 29

31 21 10 35

21 37 23 19 1640

40 18 8 33

7

34 21 7

29 1521

1939

47

41 17 842

25 29 29 17 25 30 30 16 2340

9 2735

29

7

7

17 15

37 137

23 15

9 24

10 36

16 36

42 24

Increase headcount via home ofi ce support

10 36 3331

12 54 16 27 36 22

Implement change management programs 14 32 28 26 16 29 32 24

3321

Increase headcount by hiring permanent staV

28 2413 35 21 27 36 16

Tighten risk management 9 33

27 26 5 31

14

31

34 24 13 25

13

40

41 22 1141

21 13

26 17

3019939

20 35 24 20 7 42

3220

3118

25 27 2523

25 27 3414

Global(%)

6 36 26 31

Banking(%)

Capital Markets(%)

9 37 20 33

Insurance(%)

Currently not planned Currently in discussion OngoingPlanned within the next 2 years

16

Figure 5. Industry response to regulatory changesWhat specific strategic changes will your organization implement in response to regulatory changes? (Select one)

Note: Due to rounding, total may not equal 100 percent Source: Accenture 2015 Global Structural Reform Study

45 18 30

34 23 38

45 19 30

25 39 30

56 13 24

46 30 17

36 30 27

42 26 26

13 42 25 21 11 18 45 25

13 37 28 22 18 30 34 18

32 43 25 6 50 35 9 16 27 40 18

8 29 35 27 9 51 28 11

16 37 28 19

26 40 20 15

26 35 24 19 37 28 17 16 18 51 16

31 31 19 13 32 29 26 17 41 28 15 23 28 40 9

38 33 22

7

8 35

11 39

10 37

3

35 22 65228 22 1431

9 41 941

3

11

31 21 13 27 33 2713

53

39 3 8 32

41 14 1443

13 184513 2432

24

32

24 13 7

24 19 3

37 24 7 30

50 20

3033

7

3 34

1446

3030

11 2536

34

3131

33

10 36 27 26 10 43 30 17 5 41 4114

2037

18 25 1443

14 32 28 26 6 32

3923

7 23

26 26 24 24 10 37 2330

10 33

11 33 26 30

28 2413 35 13 55 29 3 7 25 21 2132

9

29

21 18

136

14 26 40 20 6 2 22 2619 31 31 19 18 43 21 18 11 42 34 13 23 13 37 27 29 21 29 21

Global(%)

6 36 26 31

Asia Pacific(%)

Latin America(%)

North America(%)

10 24 41 24

Europe(%)

10 48 7

Figure 6. Regional response to regulatory changesWhat specific strategic changes will your organization implement in response to regulatory changes? (Select one)

21 37 23 19 20 37 17 27 26 47 16 11 24 21 34 21 11 41 26

22

6 36 40 18 3 30 47 20 11 39 34 16 3 38 41 17 7 34 3821

25 29 29 17 20 23 37 20 21 39 32 8 34 21 21 24 26 30 26 19

Note: Due to rounding, total may not equal 100

percent Source: Accenture 2015 Global Structural

Reform Study

45 18 30

32 35 29

8 26 36 29 13 25 31 31

10

27 35 27 13 33

30

23

32 52 10

39 21 37

48 14 31

30 37 33

33 27 37

47 29 11 7 37 40 17 7 36 2

1 18 42 18 10 23 40 27 19 33

36 25 39

6 39 26 29 17 37 40

14

34 28 25 13

30 27 30 13 50 24 13 10 21

41 28 18 29

21 32

33 34 24 10 39 23 29 13 42 34 11 10 17 47 27 4 32 32 32

18

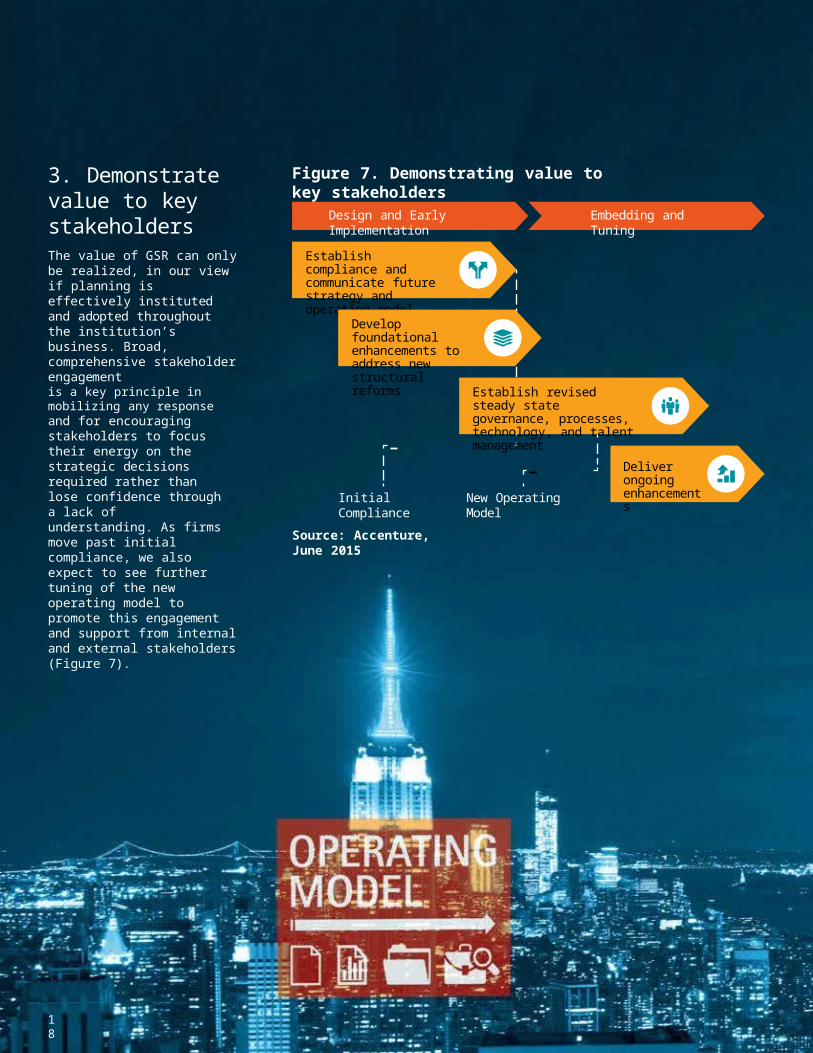

3. Demonstrate value to key stakeholdersThe value of GSR can only be realized, in our view if planning is effectively instituted and adopted throughout the institution’s business. Broad,comprehensive stakeholder engagementis a key principle in mobilizing any response and for encouraging stakeholders to focus their energy on the strategic decisions required rather than lose confidence through a lack of understanding. As firmsmove past initial compliance, we also expect to see further tuning of the new operating model to promote this engagement and support from internal and external stakeholders (Figure 7).

Establish compliance and communicate future strategy and operating model

Develop foundational enhancements to address new structural reforms

Establish revised steady state governance, processes, technology, and talent management

Deliver ongoing enhancements

Design and Early Implementation Embedding and Tuning

New Operating ModelInitial Compliance

Source: Accenture, June 2015

Figure 7. Demonstrating value to key stakeholders

19

GSR is much more than another set of regulatory requirements. Institutions should embrace structural reform with thebold thinking demanded by the creation of a new ecosystem within the financial services industry. Institutions will need to move beyond solutions for point regulations to a more strategic mindset that accounts for other competing or complementary forces.

The Accenture 2015 Global Structural Reform Study results indicate that financialinstitutions still have work to do to account for the full implications of GSR in their planning activity.Our current experience withclients facing the strategic challenges of GSR is that there is still time for effective decision making andaction that can help position institutions to remain competitive and viable in the longer term.

Time for Bold, Strategic Thinking

References1. “How Banks Can Find Opportunity in a

Flood of Regulations,” American Banker, November 10, 2014. Accessed at: http:// www.americanbanker.com/bankthink/how- banks-can-find-opportunity-in-a-flood-of- regulations-1071090-1.html

2. “Banking 2020: As the Storm Abates,North American Banks Must Chart a New Course to Capture EmergingOpportunities,” Accenture, October 2013. Accessed at: http://www.accenture.com/ SiteCollectionDocuments/PDF/Accenture- Banking-2020-POV.pdf

3. “RPT-Deutsche Bank bets big on U.S. for investment bank growth,” Reuters, March 2, 2015. Accessed at: http://www.reuters. com/article/2015/03/02/deutschebank- outlook-idUSL5N0W41S320150302

4. RBC to acquire City National Corporation, a premier U.S. private and commercial bank,” Royal Bank of Canada news release, January 22, 2015. Accessed at: http://www. rbc.com/newsroom/news/2015/20150122- rbc-nr.html

5. “Barclays PLC: Group Strategy Update – Building Barclays as the ‘Go-To’ bank,” Barclays, May 8, 2014. Accessed at: http://www.barclays.com/content/dam/ barclayspublic/docs/InvestorRelations/IRN ewsPresentations/2014Presentations/15- may-barclays-group-strategy-update.pdf

6. “BofA Said to Oust 150 Hedge Fund Clients Under New Rules,” BloombergBusiness, January 13, 2015. Accessed at: http://www. bloomberg.com/news/articles/2015-01-13/ bofa-said-to-oust-150-hedge-fund- clients-under-new-rules

7. “Shrinking margins and higher costs drive down investment banks’ returns”, Financial Times, November 4, 2014. Accessed at: http://www.ft.com/intl/cms/s/0/1ebb3d1c- 4e43-11e4-adfe-00144feab7de. html#axzz3VtU6lJPD (access required)

8. “The Everyday Bank – How Digital is Revolutionizing Banking and the Customer Ecosystem,” Accenture, January 2014. Accessed at: http://www.accenture. com/SiteCollectionDocuments/financial- services/accenture-everyday-bank.PDF

9. “Big Banks Struggle to Pass Fed’s ‘Stress Tests’,” Wall Street Journal, March 11, 2015. Accessed at: http://www.wsj.com/articles/ federal-reserve-rejects-2-banks-capital- plans-in-annual-stress-tests-1426105804 (access required)

10.“Volcker rule exam will look into banks’ structural data,” SmartBrief on Risk and Compliance, March 10, 2015. Access at: https://www2.smartbrief.com/servlet/ ArchiveServlet?issueid=25AC25BB-87AB- 420E-8DC3-5FD50869CE72&lmid=archives

About the AuthorsSamantha Regan is a Managing Director in Accenture’s Finance & Risk Services. She has 17 years of global experience working with C-suite executives and their businesses in compliance and regulatory initiatives.Samantha is the North America Lead for the Regulatory Remediation & Compliance Transformation group within Accenture’s Finance & Risk Services practice.

[email protected] Woo is a Senior Manager in Accenture’s Finance & Risk Services, and serves as the offerings lead for both Global Structural Reform and Prudential Standards. She has extensive experience in leading restructuring, M&A and joint ventures formation activities for financial institutions. Venetia also specializes in advising large institutions in credit risk, counterparty and capital adequacy functions and is the co- author of “The Effectiveness of Regulatory Stress Testing Disclosures.”

[email protected] Shorten is a Senior Manager in Accenture’s Finance & Risk Services, and serves as the Strategy and Target Operating Model offering lead for Regulatory Remediation & Compliance Transformation in North America.He has extensive experience workingwith C-Suite executives and their executive committees in Tier I investment banks and leading retail banking institutions in both the UK and the US to define and mobilize complex change delivery in response to government and regulatory mandate to change.

[email protected] Beck is a Manager in Accenture’s Finance & Risk Services. Specialized in strategy planning, surveillance, operational risk management and compliance risk management, Chris brings his solid experience and skills in these areas to help financial institutions define and implement their governance and risk management structures.

Acknowledgements

The authors would like to thank Craig Unterseher, Laura Bishop, Haralds Robeznieks and Evan Goldsmith for their contribution to this document.

About AccentureAccenture is a global management consulting, technology services and outsourcing company, with more than 323,000 people serving clients in more than 120 countries. Combining unparalleled experience, comprehensive capabilities across all industries and business functions, and extensive research on the world’smost successful companies, Accenture collaborates with clients to help them become high-performance businesses and governments. The company generated net revenues of US$30.0 billion for the fiscal year ended Aug. 31, 2014. Its home page is www.accenture.com.Disclaimer: This document is intended for general informational purposes only and does not take into account the reader’s specific circumstances, and may not reflect the most current developments.Accenture disclaims, to the fullest extent permitted by applicable law, any and all liability for the accuracy and completeness of the information in this document and for any acts or omissions made based on such information. Accenture does not provide legal, regulatory, audit, or tax advice. Readers are responsible for obtaining such advice from their own legal counsel or other licensed professionals.Stay ConnectedAccenture Finance & Risk Services: http://www.accenture.com/microsites/ financeandrisk/pages/index.aspx

Connect With Us https://www.linkedin.com/ groups?gid=3753715

Join Us https://www.facebook.com/ accenturestrategy

https://www.facebook.com/ accenture

Follow Us http://twitter.com/accenture

Watch Us www.youtube.com/accenture

15-1120

Copyright © 2015 Accenture All rights reserved.Accenture, its logo, and High Performance Deliveredare trademarks of Accenture.