Embed Size (px)

Citation preview

19-1

Auditing And Assurance Services 9th Edition Test Bank Messier

Test Bank Auditing and Assurance Services A Systematic Approach 9th

Edition Messier, Glover, Prawitt

Instant download: https://testbankarea.com/?p=362

Solutions Manual Auditing and Assurance Services : A Systematic

Approach 9th Edition Solutions Manual Messier, Glover, Prawitt.

Completed download:

https://testbankarea.com/download/auditing-assurance-services-a-

systematic-approach-9th-edition-solutions-manual-messier-glover-

prawitt/

Chapter 19

Professional Conduct, Independence, and Quality Control

True / False Questions

1. The term "ethics" refers to a person's propensity to follow the laws of the land.

True False

19-2

2. Professionalism refers to the conduct, aims, or qualities that characterize or mark a given

profession.

True False

3. When auditing a public company, a CPA must follow the auditing standards and Code of

Professional Conduct of the PCAOB.

True False

4. The AICPA Code of Professional Conduct deals mainly with behavior and actions of individual

auditors.

True False

5. The Principles of Professional Conduct set forth the minimum standards.

True False

6. Rules of Conduct are enforceable.

True False

7. Ethical rulings are enforceable.

True False

8. Principles are stated at a conceptual level, not a detailed level.

True False

9. The rules contained in Section 100 cover issues relating to independence, integrity, and auditing

standards.

True False

19-3

10. If an auditor is not independent of the client, it is unlikely that a user of financial statements will

place much reliance on the CPA's work.

True False

11. As per the Conceptual Framework for AICPA Independence Standards made effective in 2006, a

CPA is required to identify and assess the extent to which a threat to independence exists.

True False

12. An indirect financial interest is defined as a financial interest that is owned or is under the control

of an individual or entity.

True False

13. A financial interest is "beneficially owned" when an individual or entity is NOT the recorded owner

of the interest but has a right to some or all of the underlying benefits of ownership.

True False

14. If a CPA owns an insurance policy issued by an attest client, independence would be considered

impaired, even if the policy was purchased under the insurance company's normal terms and

procedures and does not offer an investment option.

True False

15. The independence standards issued by the PCAOB do not prohibit the provision of tax services to

an attest client.

True False

16. PCAOB rules require tax services provided by a public company auditor to be considered and

approved by the company's audit committee.

True False

19-4

Multiple Choice Questions

17. With respect to ethics, the rights-based approach

A. Suggests that auditors should always verify ownership of a client's material tangible assets.

B. Is primarily concerned with equity and impartiality.

C. Suggests that an individual's actions should not violate the rights of any individual.

D. Recognizes that decisions involve trade-offs between costs and benefits.

18. With respect to ethics, the utilitarian theory

A. Suggests that auditors should always verify ownership of a client's material tangible assets.

B. Is primarily concerned with equity and impartiality.

C. Suggests that an individual's actions should not violate the rights of any individual.

D. Recognizes that decisions involve trade-offs between costs and benefits.

19. With respect to ethics, the justice-based approach

A. Suggests that auditors should always verify ownership of a client's material tangible assets.

B. Is primarily concerned with equity and impartiality.

C. Suggests that an individual's actions should not violate the rights of any individual.

D. Recognizes that decisions involve trade-offs between costs and benefits.

20. In auditing a privately held entity, an auditor must follow the professional standards established by

all of the following except:

A. The AICPA's Auditing Standards Board.

B. The Professional Code of Conduct.

C. The Independence Standards Board.

D. The PCAOB.

19-5

21. Which of the following is not a Principle of Professional Conduct as defined by the Code of

Professional Conduct?

A. Integrity.

B. Due care.

C. Reporting.

D. Scope and nature of services.

22. What is meant by the Code of Professional Conduct's definition of "holding out"?

A. Informing a client about one's status as a CPA.

B. Withholding an audit report until the fee is paid.

C. Not sharing audit documentation with a successor auditor.

D. Not suggesting that management make an adjusting entry that is deemed immaterial.

23. For private companies, accounting firms are prohibited from providing

A. Outsourced internal audit services.

B. Audit services.

C. Review services.

D. None of these.

24. A violation of the profession's ethical standards would most likely have occurred when a CPA

A. Purchased a bookkeeping firm's practice of monthly write-ups for a percentage of fees received

over a three-year period.

B. Made arrangements with a bank to collect notes issued by a client in payment of fees due.

C. Named Smith formed a partnership with two other CPAs and used "Smith & Co." as the firm

name.

D. Issued an unqualified opinion on the 2011 financial statements when fees for the 2010 audit

were unpaid.

19-6

25. Which of the following is required for a firm to designate itself as a "Member of the American

Institute of Certified Public Accountants" on its letterhead?

A. At least one of the partners must be a member.

B. The partners whose names appear in the firm name must be members.

C. All partners must be members.

D. The firm must be a dues-paying member.

26. A violation of the profession's ethical standards would least likely have occurred when a CPA in

public practice

A. Used a records-retention agency to store the CPA's working papers and client records.

B. Served as an expert witness in a damage suit and received compensation based on the

amount awarded to the plaintiff.

C. Referred life insurance assignments to the CPA's spouse, who is a life insurance agent.

D. Failed to file his personal tax return.

27. According to the Code of Professional Conduct, which of the following individuals is not in a

position to influence an attest engagement (i.e., not a covered member)?

A. The office's managing partner who determines the compensation of the attest engagement

partner.

B. The office's IT expert, who consulted with the engagement partner regarding the client's IT

system.

C. The partner in another office in a nearby city who regularly plays golf with the engagement

partner.

D. The office's partner who monitors quality control over the attest engagement.

19-7

28. A CPA, while performing an audit, strives to achieve independence in appearance in order to

A. Reduce risk and liability.

B. Comply with the generally accepted standards of fieldwork.

C. Become independent in fact.

D. Maintain public confidence in the profession.

29. In which of the following instances would the independence of the CPA not be considered to be

impaired? The CPA has been retained as the auditor of a brokerage firm

A. Which owes the CPA audit fees for more than one year.

B. In which the CPA has a large active margin account.

C. In which the CPA's brother is the controller.

D. Which owes the CPA audit fees for current year services and has just filed a petition for

bankruptcy.

30. The SEC has issued independence rules that differ from the AICPA's in all of the following areas

except:

A. Working paper documentation.

B. Provision of other professional services.

C. Human resource and compensation-related issues.

D. Required communication.

31. Which of the following is not an element of quality control as defined by Statement of Quality

Control Standards No. 8?

A. Monitoring.

B. Independence.

C. Human resources.

D. Relevant ethical requirements.

19-8

32. A basic objective of a CPA firm is to provide professional services that conform to professional

standards. Reasonable assurance of achieving this basic objective is provided through

A. Compliance with generally accepted reporting standards.

B. A system of quality control.

C. A system of peer review.

D. Continuing professional education.

33. The quality control standards are concerned primarily with

A. Actions of individual auditors.

B. A firm's monitoring of its practice.

C. Disciplinary actions against individual auditors.

D. Preventing legal action.

34. Which of the following bodies ordinarily would have the authority to suspend or revoke a CPA's

license to practice public accounting?

A. The SEC.

B. The AICPA.

C. A state CPA society.

D. A state board of accountancy.

19-9

35. Which of the following statements best describes why the profession of certified public

accountants has deemed it essential to promulgate a code of conduct and to establish a

mechanism for enforcing observance of the code?

A. Ethical standards are established so that users of accounting services know what to expect, the

professionals know what behaviors are acceptable, and overseers can take disciplinary action

when appropriate.

B. A prerequisite to success is the establishment of an ethical code that stresses primarily the

professional's responsibility to clients and colleagues.

C. A requirement of most state laws calls for the profession to establish a code of conduct.

D. An essential means of self-protection for the profession is the establishment of flexible ethical

standards by the profession.

36. A CPA's license to practice will ordinarily be suspended or revoked automatically for

A. Controlling the bookkeeping for a compilation client.

B. Conviction of willful failure to file personal income tax return.

C. Refusing to respond to an inquiry by the AICPA practice review committee.

D. Accepting compensation while honoring a subpoena to appear as an expert witness.

37. A CPA's retention of client records as a means of enforcing payment of an overdue audit fee is an

action that is

A. Considered acceptable by the AICPA Code of Professional Conduct.

B. Ill-advised because it would impair the CPA's independence with respect to the client.

C. Considered discreditable to the profession.

D. A violation of generally accepted auditing standards.

19-10

38. Which of the following is allowable for a CPA?

A. A used car loan from a banking client where the client has a lien on the car.

B. An uncollateralized signature loan from a client.

C. Owning more than five percent of the outstanding shares of client stock in a retirement account.

D. The audit engagement partner serves on the client's audit committee.

39. In performing an audit, Jackson, CPA, discovers that the professional competence necessary for

the engagement is lacking. Jackson informs management of the situation and recommends

another local CPA firm and management engages this other firm. Under these circumstances

A. Jackson may request compensation from the other CPA firm for any professional services

rendered to it in connection with the engagement.

B. Jackson may accept a referral fee from the other CPA firm.

C. Jackson has violated the AICPA Code of Professional Conduct because of non-fulfillment of the

duty of performance.

D. Jackson's lack of competence should be construed to be a violation of generally accepted

auditing standards.

40. In which one of the following situations would a CPA be in violation of the AICPA Code of

Professional Conduct in determining a fee?

A. A fee based on whether the CPA's report on the client's financial statements results in the

approval of a bank loan.

B. A fee based on an estimate of the number of hours needed to complete the engagement by

auditors of various levels of experience.

C. A fee based on the nature of the service rendered and the CPA's particular expertise instead of

the actual time spent on the engagement.

D. A fee based on the fee charged by the prior auditor.

19-11

41. In connection with a lawsuit, a third party attempts to gain access to the auditor's working papers.

The client's defense of privileged communication will be successful only to the extent it is

protected by the

A. Auditor's acquiescence in use of this defense.

B. Common law.

C. AICPA Code of Professional Conduct.

D. State law.

42. The profession's ethical standards would most likely be considered to have been violated when

the CPA represents that specific consulting services will be performed for a stated fee and it is

apparent at the time of the representation that the

A. CPA would not be independent.

B. Fee was a competitive bid.

C. Actual fee would be substantially higher.

D. Actual fee would be substantially lower than the fees charged by other CPAs for comparable

services.

43. According to the ethical standards of the profession, which of the following acts is generally

prohibited?

A. Issuing a modified report explaining a failure to follow a governmental regulatory agency's

standards when conducting an attest service for a client.

B. Revealing confidential client information during a quality review of a professional practice by a

team from the state CPA society.

C. Accepting a contingent fee for representing a client in an examination of the client's federal tax

return by an IRS agent.

D. Retaining client records after an engagement is terminated prior to completion and the client

has demanded its return.

19-12

44. According to the ethical standards of the profession, which of the following acts is generally

prohibited?

A. Purchasing a product from a third party and reselling it to a client.

B. Writing a financial management newsletter promoted and sold by a publishing company.

C. Accepting a commission for recommending a product to an audit client.

D. Accepting engagements obtained through the efforts of third parties.

45. In which of the following circumstances would a CPA who audits XM Corporation lack

independence?

A. The CPA and XM's president are both on the board of directors of COD Corporation.

B. The CPA and XM's president each owns 25 percent of FOB Corporation, a closely-held

company.

C. The CPA has an automobile loan from XM, which is a savings and loan organization and the

loan is collateralized by the automobile.

D. The CPA reduced XM's usual audit fee by 40 percent because XM's financial condition was

unfavorable.

46. Mavis, CPA, has audited the financial statements of South Bay Sales Incorporated for several

years and had always been paid promptly for services rendered. Last year's audit invoices have

not been paid because South Bay is experiencing cash flow difficulties and the current year's audit

is scheduled to commence in one week. With respect to the past due audit fees, Mavis should

A. Perform the scheduled audit and allow South Bay to pay when the cash flow difficulties are

alleviated.

B. Perform the scheduled audit only after arranging a definite payment schedule and securing

notes signed by South Bay.

C. Inform South Bay's management that the past due audit fees are considered an impairment of

auditor independence.

D. Inform South Bay's management that the past due audit fees may be considered a loan on

which interest must be imputed for financial statement purposes.

19-13

47. In which of the following instances would the independence of the CPA not be considered to be

impaired? The CPA has been retained as the auditor of a

A. Charitable organization in which an employee of the CPA serves as treasurer.

B. Municipality in which the CPA owns $25,000 of the $2,500,000 indebtedness of the

municipality.

C. Restaurant where the CPA dines frequently.

D. Company in which the CPA's private investment club owns a one-tenth interest.

48. A CPA firm's personnel partner periodically studies the CPA firm's personnel advancement

experience to ascertain whether the individuals who were assigned increased degrees of

responsibility met predetermined criteria. This is evidence of the CPA firm's adherence to

prescribed standards of

A. Quality control.

B. Due professional care.

C. Supervision and review.

D. Fieldwork.

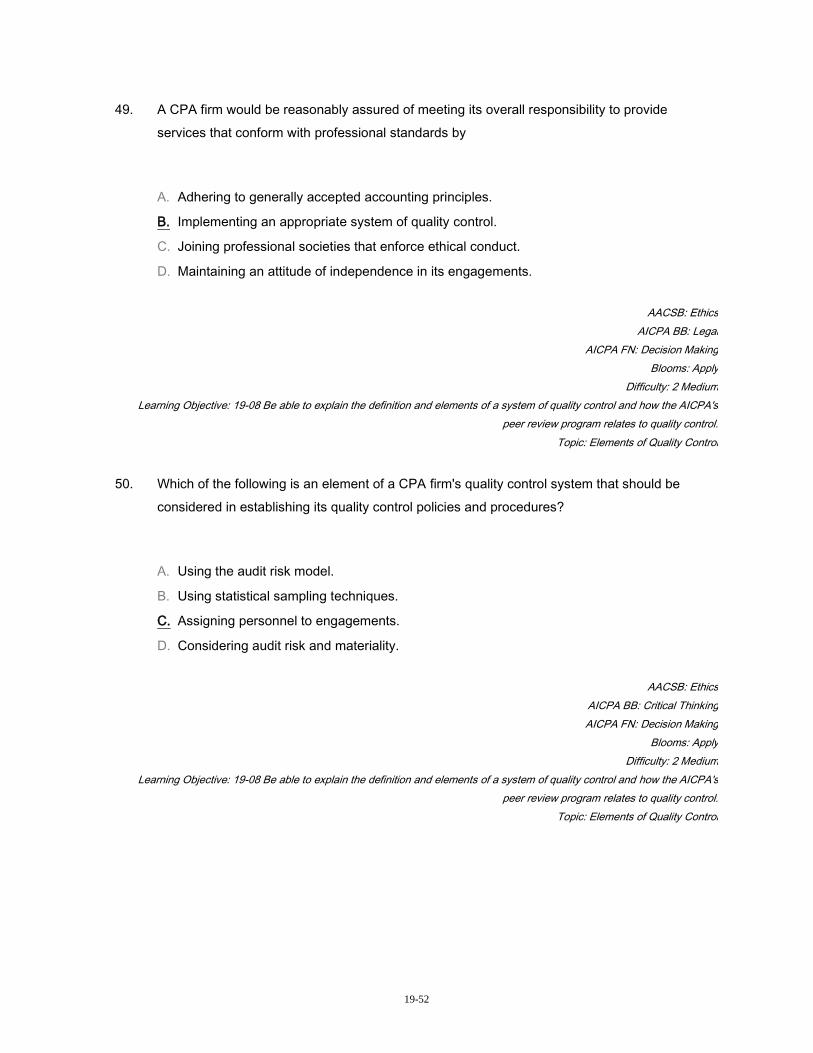

49. A CPA firm would be reasonably assured of meeting its overall responsibility to provide services

that conform with professional standards by

A. Adhering to generally accepted accounting principles.

B. Implementing an appropriate system of quality control.

C. Joining professional societies that enforce ethical conduct.

D. Maintaining an attitude of independence in its engagements.

19-14

50. Which of the following is an element of a CPA firm's quality control system that should be

considered in establishing its quality control policies and procedures?

A. Using the audit risk model.

B. Using statistical sampling techniques.

C. Assigning personnel to engagements.

D. Considering audit risk and materiality.

51. What is the primary purpose of the acceptance and continuance of client relationships and specific

engagements element of quality control?

A. Guarantee that firms do not associate with clients whose management lacks integrity.

B. Provide reasonable assurance that firms do not associate with clients whose management

lacks integrity.

C. Guarantee that firms will not be sued as a result of association with a client.

D. Provide reasonable assurance that firms will not be sued as a result of association with a client.

52. In order to achieve effective quality control, a firm of independent auditors should establish

policies and procedures for

A. Determining the minimum procedures necessary for unaudited financial statements.

B. Setting the scope of audit work.

C. Deciding whether to accept or continue a client.

D. Setting the scope of internal control study and evaluation.

53. Within the context of quality control, the primary purpose of continuing professional education and

training activities is to enable a CPA firm to provide personnel within the firm with

A. Technical training that ensures proficiency as an auditor.

B. Opportunities for career advancement outside the accounting firm.

C. Knowledge required to fulfill assigned responsibilities.

D. Knowledge required to perform a peer review.

19-15

54. A CPA firm evaluates its personnel advancement experience to ascertain whether individuals

assigned to increased degrees of responsibility meet predetermined criteria. This policy is

evidence of the firm's adherence to which of the following prescribed standards?

A. Professional ethics.

B. Supervision and review.

C. Accounting and review services.

D. Quality control.

55. The primary purpose of establishing quality control policies and procedures for deciding whether

to accept a new client is to

A. Enable the CPA firm to attest to the reliability of the client.

B. Satisfy the CPA firm's duty to the public concerning the acceptance of new clients.

C. Minimize the likelihood of association with clients whose management lacks integrity.

D. Anticipate before performing any fieldwork whether an unqualified opinion can be expressed.

56. Following the issuance of a PCAOB draft report, how many days does the CPA firm have to

respond to accusations?

A. 10 days.

B. 30 days.

C. 50 days.

D. 90 days.

19-16

57. A violation of the profession's ethical standards would most likely occur when a CPA who

A. Is also admitted to the Bar represents on letterhead to be both an attorney and a CPA.

B. Writes a newsletter on financial management also permits a publishing company to solicit

subscriptions by direct mail.

C. Is controller of a bank permits the bank to use the controller's CPA title in the listing of officers

in its publications.

D. Refused to hire a new employee does so because the CPA deemed the candidate to be "too

old."

58. In determining estimates of fees, an auditor may take into account each of the following, except

the:

A. Value of the service to the client.

B. Degree of responsibility assumed by undertaking the engagement.

C. Skills required to perform the service.

D. Attainment of specific findings.

59. An auditor is about to commence a recurring annual audit engagement. The continuing auditor's

independence would ordinarily be considered to be impaired if the prior year's audit fee

A. Was unusually large.

B. Has not been paid and will not be paid for at least twelve months.

C. Has not been paid and the client has filed a voluntary petition for bankruptcy.

D. Was renegotiated during the prior year audit based on the need for expanded testing.

19-17

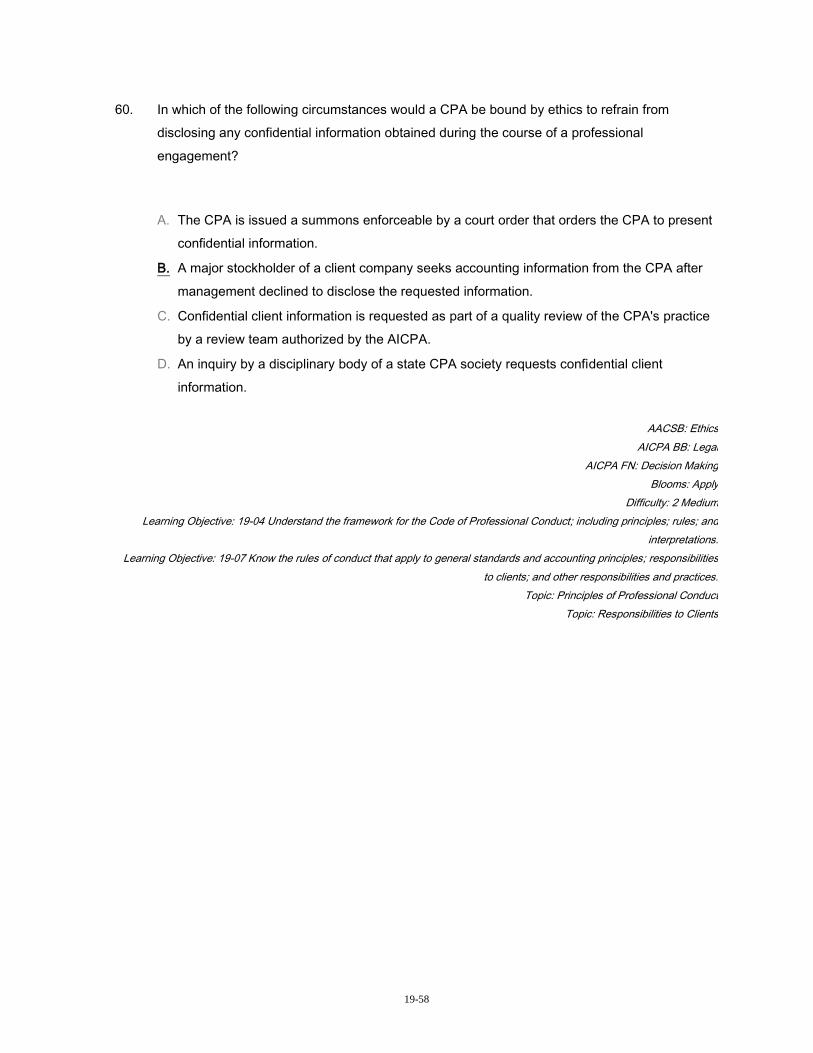

60. In which of the following circumstances would a CPA be bound by ethics to refrain from disclosing

any confidential information obtained during the course of a professional engagement?

A. The CPA is issued a summons enforceable by a court order that orders the CPA to present

confidential information.

B. A major stockholder of a client company seeks accounting information from the CPA after

management declined to disclose the requested information.

C. Confidential client information is requested as part of a quality review of the CPA's practice by a

review team authorized by the AICPA.

D. An inquiry by a disciplinary body of a state CPA society requests confidential client information.

61. Under which of the following circumstances would the independence of a CPA be considered

impaired if the CPA, who also is an attorney, serves as auditor and provides legal services to the

same client?

A. When the CPA, as legal agent, consummates a business acquisition for the client.

B. When the CPA's audit fees and legal fees are not billed separately.

C. When the CPA uses legal expertise to research a question of income tax law.

D. When the legal services consist of an analysis of the terms of an existing lease agreement.

62. According to the profession's ethical standards, a CPA would be considered independent in which

of the following instances?

A. A client leases part of an office building from the CPA, resulting in a material indirect financial

interest to the CPA.

B. The CPA has a material direct financial interest in a client, but transfers the interest into a blind

trust.

C. The CPA owns an office building and the mortgage on the building is guaranteed by a client.

D. The CPA belongs to a country club client in which membership requires an annual fee.

19-18

63. When auditing a public company, which of the following impairs an auditor's independence?

A. Offering audit services as well as preparing the tax return for the same client.

B. The auditor's spouse works in the assembly line of an audit client.

C. Lack of fee disclosure in the client's annual report.

D. The auditor has been a partner on the engagement for ten years.

Short Answer Questions

64. Why do professions establish codes of conduct that define ethical behaviors for members of the

profession?

65. Distinguish between the following theories of ethical behavior: utilitarianism, a rights-based

approach, and a justice-based approach.

19-19

66. Which professional and regulatory bodies establish the ethical and professional rules for auditors

of: (1) public companies and (2) private companies?

67. Listed below are definitions of the six Principles of Professional Conduct. For each, identify the

principle being defined.

a. A member should observe the profession's technical and ethical standards, strive continually to

improve competence and the quality of services, and discharge professional responsibility to the

best of the member's ability.

b. Members should exercise sensitive professional and moral judgments in all their activities.

c. A member should be free of conflicts of interest in discharging professional responsibilities.

d. A member in public practice should observe the Principles of the Code of Professional Conduct

in determining the type and extent of services to be provided.

e. Members should accept the obligation to act in a way that will honor the public trust and

demonstrate commitment to professionalism.

f. To maintain and broaden public confidence, members should perform all professional

responsibilities with the highest sense of _____________.

19-20

68. Ms. Lembke is a partner for DTS, a CPA firm. She is the lead partner for the firm's largest client,

The Grey Elephant. Ms. Zadina, who works in the same office as Ms. Lembke, has a sister who is

the controller for The Grey Elephant. Because of potential independence issues, Ms. Zadina does

no work for The Grey Elephant. Ms. Zadina is being considered for promotion to partner. What

independence issues should Ms. Lembke consider before promoting Ms. Zadina?

69. The SEC's rules with respect to services provided by auditors are predicated on three basic

principles of auditor objectivity and independence. What are the three basic principles?

70. Identify the primary purposes of Rules 201-203 of the Rules of Conduct.

19-21

71. When can a CPA disclose confidential information without the client's consent?

Matching Questions

19-22

72. Match each term below with its definition as provided by the AICPA Rules of Conduct.

1. Partner

A proprietor, part owner, or any individual who

assumes the risks and benefits of firm ownership

or who is otherwise held out by the firm to be the

equivalent of any of the aforementioned ____

2. Practice of

public

accounting

All services performed by member while

holding out as a CPA ____

3. Attest

engagement

The performance for a client by a member or a

member's firm while holding out as CPA(s) of the

professional services of accounting, tax, personal

financial planning, litigation support services, and

those professional services for which standards

are promulgated by bodies designated by

Council ____

4. Professional

services

Any person or entity, other than the member's

employer, that engages a member or a member's

firm to perform professional services ____

5. Holding out

Examples include financial statement audits,

reviews, and examinations of prospective

financial information ____

6. Client

Any action initiated by a member that informs

others of his or her status as a CPA or AICPA-

accredited specialist ____

19-23

Chapter 19 Professional Conduct, Independence, and Quality Control

Answer Key

True / False Questions

1. The term "ethics" refers to a person's propensity to follow the laws of the land.

FALSE

AACSB: Ethics

AICPA BB: Critical Thinking

AICPA FN: Decision Making

Blooms: Remember

Difficulty: 1 Easy

Learning Objective: 19-01 Know the definitions and general importance of ethics and professionalism.

Topic: Ethics and Professional Conduct

2. Professionalism refers to the conduct, aims, or qualities that characterize or mark a given

profession.

TRUE

AACSB: Ethics

AICPA BB: Critical Thinking

AICPA FN: Decision Making

Blooms: Remember

Difficulty: 1 Easy

Learning Objective: 19-01 Know the definitions and general importance of ethics and professionalism.

Topic: Ethics and Professional Conduct

19-24

3. When auditing a public company, a CPA must follow the auditing standards and Code of

Professional Conduct of the PCAOB.

TRUE

AACSB: Ethics

AICPA BB: Critical Thinking

AICPA FN: Decision Making

Blooms: Remember

Difficulty: 1 Easy

Learning Objective: 19-03 Know how professional ethics standards for auditors have developed over time and the entities

involved.

Topic: Standards for Auditor Professionalism

4. The AICPA Code of Professional Conduct deals mainly with behavior and actions of individual

auditors.

TRUE

AACSB: Ethics

AICPA BB: Critical Thinking

AICPA FN: Decision Making

Blooms: Remember

Difficulty: 1 Easy

Learning Objective: 19-04 Understand the framework for the Code of Professional Conduct; including principles; rules; and

interpretations.

Topic: The AICPA Code of Professional Conduct: A Comprehensive Framework for Auditors

5. The Principles of Professional Conduct set forth the minimum standards.

FALSE

AACSB: Ethics

AICPA BB: Critical Thinking

AICPA FN: Decision Making

Blooms: Remember

Difficulty: 1 Easy

Learning Objective: 19-04 Understand the framework for the Code of Professional Conduct; including principles; rules; and

interpretations.

Topic: The AICPA Code of Professional Conduct: A Comprehensive Framework for Auditors

19-25

6. Rules of Conduct are enforceable.

TRUE

AACSB: Ethics

AICPA BB: Critical Thinking

AICPA FN: Decision Making

Blooms: Remember

Difficulty: 1 Easy

Learning Objective: 19-04 Understand the framework for the Code of Professional Conduct; including principles; rules; and

interpretations.

Topic: The AICPA Code of Professional Conduct: A Comprehensive Framework for Auditors

7. Ethical rulings are enforceable.

FALSE

AACSB: Ethics

AICPA BB: Critical Thinking

AICPA FN: Decision Making

Blooms: Remember

Difficulty: 1 Easy

Learning Objective: 19-04 Understand the framework for the Code of Professional Conduct; including principles; rules; and

interpretations.

Topic: The AICPA Code of Professional Conduct: A Comprehensive Framework for Auditors

8. Principles are stated at a conceptual level, not a detailed level.

TRUE

AACSB: Ethics

AICPA BB: Critical Thinking

AICPA FN: Decision Making

Blooms: Remember

Difficulty: 1 Easy

Learning Objective: 19-04 Understand the framework for the Code of Professional Conduct; including principles; rules; and

interpretations.

Topic: Principles of Professional Conduct

19-26

9. The rules contained in Section 100 cover issues relating to independence, integrity, and

auditing standards.

FALSE

AACSB: Ethics

AICPA BB: Critical Thinking

AICPA FN: Decision Making

Blooms: Remember

Difficulty: 1 Easy

Learning Objective: 19-04 Understand the framework for the Code of Professional Conduct; including principles; rules; and

interpretations.

Topic: Rules of Conduct

10. If an auditor is not independent of the client, it is unlikely that a user of financial statements will

place much reliance on the CPA's work.

TRUE

AACSB: Ethics

AICPA BB: Critical Thinking

AICPA FN: Decision Making

Blooms: Understand

Difficulty: 1 Easy

Learning Objective: 19-05 Acquire a working knowledge of the rules of conduct that apply to independence; integrity; and

objectivity.

Topic: Independence, Integrity, and Objectivity

11. As per the Conceptual Framework for AICPA Independence Standards made effective in 2006,

a CPA is required to identify and assess the extent to which a threat to independence exists.

TRUE

AACSB: Ethics

AICPA BB: Legal

AICPA FN: Decision Making

Blooms: Remember

Difficulty: 1 Easy

Learning Objective: 19-05 Acquire a working knowledge of the rules of conduct that apply to independence; integrity; and

objectivity.

Topic: Independence, Integrity, and Objectivity

19-27

12. An indirect financial interest is defined as a financial interest that is owned or is under the

control of an individual or entity.

FALSE

AACSB: Ethics

AICPA BB: Legal

AICPA FN: Decision Making

Blooms: Remember

Difficulty: 1 Easy

Learning Objective: 19-05 Acquire a working knowledge of the rules of conduct that apply to independence; integrity; and

objectivity.

Topic: Independence, Integrity, and Objectivity

13. A financial interest is "beneficially owned" when an individual or entity is NOT the recorded

owner of the interest but has a right to some or all of the underlying benefits of ownership.

TRUE

AACSB: Ethics

AICPA BB: Legal

AICPA FN: Decision Making

Blooms: Understand

Difficulty: 1 Easy

Learning Objective: 19-05 Acquire a working knowledge of the rules of conduct that apply to independence; integrity; and

objectivity.

Topic: Independence, Integrity, and Objectivity

19-28

14. If a CPA owns an insurance policy issued by an attest client, independence would be

considered impaired, even if the policy was purchased under the insurance company's normal

terms and procedures and does not offer an investment option.

FALSE

AACSB: Ethics

AICPA BB: Legal

AICPA FN: Decision Making

Blooms: Apply

Difficulty: 2 Medium

Learning Objective: 19-05 Acquire a working knowledge of the rules of conduct that apply to independence; integrity; and

objectivity.

Topic: Independence, Integrity, and Objectivity

15. The independence standards issued by the PCAOB do not prohibit the provision of tax services

to an attest client.

TRUE

AACSB: Ethics

AICPA BB: Legal

AICPA FN: Decision Making

Blooms: Remember

Difficulty: 1 Easy

Learning Objective: 19-06 Know the basic differences between the SEC's independence rules for public company auditors and

AICPA standards for audits of nonpublic entities.

Topic: SEC and PCAOB Independence Requirements for Audits of Public Companies

19-29

16. PCAOB rules require tax services provided by a public company auditor to be considered and

approved by the company's audit committee.

TRUE

AACSB: Ethics

AICPA BB: Legal

AICPA FN: Decision Making

Blooms: Apply

Difficulty: 3 Hard

Learning Objective: 19-06 Know the basic differences between the SEC's independence rules for public company auditors and

AICPA standards for audits of nonpublic entities.

Topic: SEC and PCAOB Independence Requirements for Audits of Public Companies

Multiple Choice Questions

17. With respect to ethics, the rights-based approach

A. Suggests that auditors should always verify ownership of a client's material tangible assets.

B. Is primarily concerned with equity and impartiality.

C. Suggests that an individual's actions should not violate the rights of any individual.

D. Recognizes that decisions involve trade-offs between costs and benefits.

AACSB: Ethics

AICPA BB: Critical Thinking

AICPA FN: Decision Making

Blooms: Remember

Difficulty: 1 Easy

Learning Objective: 19-02 Be able to explain three basic theories of ethical behavior and understand how to deal with ethical

challenges through an example situation.

Topic: Theories of Ethical Behavior

19-30

18. With respect to ethics, the utilitarian theory

A. Suggests that auditors should always verify ownership of a client's material tangible assets.

B. Is primarily concerned with equity and impartiality.

C. Suggests that an individual's actions should not violate the rights of any individual.

D. Recognizes that decisions involve trade-offs between costs and benefits.

AACSB: Ethics

AICPA BB: Critical Thinking

AICPA FN: Decision Making

Blooms: Remember

Difficulty: 1 Easy

Learning Objective: 19-02 Be able to explain three basic theories of ethical behavior and understand how to deal with ethical

challenges through an example situation.

Topic: Theories of Ethical Behavior

19. With respect to ethics, the justice-based approach

A. Suggests that auditors should always verify ownership of a client's material tangible assets.

B. Is primarily concerned with equity and impartiality.

C. Suggests that an individual's actions should not violate the rights of any individual.

D. Recognizes that decisions involve trade-offs between costs and benefits.

AACSB: Ethics

AICPA BB: Critical Thinking

AICPA FN: Decision Making

Blooms: Remember

Difficulty: 1 Easy

Learning Objective: 19-02 Be able to explain three basic theories of ethical behavior and understand how to deal with ethical

challenges through an example situation.

Topic: Theories of Ethical Behavior

19-31

20. In auditing a privately held entity, an auditor must follow the professional standards established

by all of the following except:

A. The AICPA's Auditing Standards Board.

B. The Professional Code of Conduct.

C. The Independence Standards Board.

D. The PCAOB.

AACSB: Ethics

AICPA BB: Legal

AICPA FN: Decision Making

Blooms: Remember

Difficulty: 1 Easy

Learning Objective: 19-03 Know how professional ethics standards for auditors have developed over time and the entities

involved.

Topic: Standards for Auditor Professionalism

21. Which of the following is not a Principle of Professional Conduct as defined by the Code of

Professional Conduct?

A. Integrity.

B. Due care.

C. Reporting.

D. Scope and nature of services.

AACSB: Ethics

AICPA BB: Legal

AICPA FN: Decision Making

Blooms: Remember

Difficulty: 1 Easy

Learning Objective: 19-04 Understand the framework for the Code of Professional Conduct; including principles; rules; and

interpretations.

Topic: Principles of Professional Conduct

19-32

22. What is meant by the Code of Professional Conduct's definition of "holding out"?

A. Informing a client about one's status as a CPA.

B. Withholding an audit report until the fee is paid.

C. Not sharing audit documentation with a successor auditor.

D. Not suggesting that management make an adjusting entry that is deemed immaterial.

AACSB: Ethics

AICPA BB: Legal

AICPA FN: Decision Making

Blooms: Remember

Difficulty: 1 Easy

Learning Objective: 19-04 Understand the framework for the Code of Professional Conduct; including principles; rules; and

interpretations.

Topic: Rules of Conduct

Topic: The AICPA Code of Professional Conduct: A Comprehensive Framework for Auditors

23. For private companies, accounting firms are prohibited from providing

A. Outsourced internal audit services.

B. Audit services.

C. Review services.

D. None of these.

AACSB: Ethics

AICPA BB: Legal

AICPA FN: Decision Making

Blooms: Apply

Difficulty: 1 Easy

Learning Objective: 19-05 Acquire a working knowledge of the rules of conduct that apply to independence; integrity; and

objectivity.

Topic: Independence, Integrity, and Objectivity

19-33

24. A violation of the profession's ethical standards would most likely have occurred when a CPA

A. Purchased a bookkeeping firm's practice of monthly write-ups for a percentage of fees

received over a three-year period.

B. Made arrangements with a bank to collect notes issued by a client in payment of fees due.

C. Named Smith formed a partnership with two other CPAs and used "Smith & Co." as the firm

name.

D. Issued an unqualified opinion on the 2011 financial statements when fees for the 2010 audit

were unpaid.

AACSB: Ethics

AICPA BB: Legal

AICPA FN: Decision Making

Blooms: Apply

Difficulty: 1 Easy

Learning Objective: 19-05 Acquire a working knowledge of the rules of conduct that apply to independence; integrity; and

objectivity.

Learning Objective: 19-07 Know the rules of conduct that apply to general standards and accounting principles; responsibilities

to clients; and other responsibilities and practices.

Topic: Independence, Integrity, and Objectivity

Topic: Responsibilities to Clients

19-34

25. Which of the following is required for a firm to designate itself as a "Member of the American

Institute of Certified Public Accountants" on its letterhead?

A. At least one of the partners must be a member.

B. The partners whose names appear in the firm name must be members.

C. All partners must be members.

D. The firm must be a dues-paying member.

AACSB: Ethics

AICPA BB: Legal

AICPA FN: Decision Making

Blooms: Remember

Difficulty: 1 Easy

Learning Objective: 19-04 Understand the framework for the Code of Professional Conduct; including principles; rules; and

interpretations.

Learning Objective: 19-07 Know the rules of conduct that apply to general standards and accounting principles; responsibilities

to clients; and other responsibilities and practices.

Topic: Other Responsibilities and Practices

Topic: Principles of Professional Conduct

19-35

26. A violation of the profession's ethical standards would least likely have occurred when a CPA in

public practice

A. Used a records-retention agency to store the CPA's working papers and client records.

B. Served as an expert witness in a damage suit and received compensation based on the

amount awarded to the plaintiff.

C. Referred life insurance assignments to the CPA's spouse, who is a life insurance agent.

D. Failed to file his personal tax return.

AACSB: Ethics

AICPA BB: Legal

AICPA FN: Decision Making

Blooms: Understand

Difficulty: 1 Easy

Learning Objective: 19-04 Understand the framework for the Code of Professional Conduct; including principles; rules; and

interpretations.

Learning Objective: 19-07 Know the rules of conduct that apply to general standards and accounting principles; responsibilities

to clients; and other responsibilities and practices.

Topic: Other Responsibilities and Practices

Topic: Principles of Professional Conduct

19-36

27. According to the Code of Professional Conduct, which of the following individuals is not in a

position to influence an attest engagement (i.e., not a covered member)?

A. The office's managing partner who determines the compensation of the attest engagement

partner.

B. The office's IT expert, who consulted with the engagement partner regarding the client's IT

system.

C. The partner in another office in a nearby city who regularly plays golf with the engagement

partner.

D. The office's partner who monitors quality control over the attest engagement.

AACSB: Ethics

AICPA BB: Legal

AICPA FN: Decision Making

Blooms: Apply

Difficulty: 2 Medium

Learning Objective: 19-04 Understand the framework for the Code of Professional Conduct; including principles; rules; and

interpretations.

Topic: The AICPA Code of Professional Conduct: A Comprehensive Framework for Auditors

28. A CPA, while performing an audit, strives to achieve independence in appearance in order to

A. Reduce risk and liability.

B. Comply with the generally accepted standards of fieldwork.

C. Become independent in fact.

D. Maintain public confidence in the profession.

AACSB: Ethics

AICPA BB: Critical Thinking

AICPA FN: Decision Making

Blooms: Understand

Difficulty: 1 Easy

Learning Objective: 19-05 Acquire a working knowledge of the rules of conduct that apply to independence; integrity; and

objectivity.

Topic: Independence, Integrity, and Objectivity

19-37

29. In which of the following instances would the independence of the CPA not be considered to be

impaired? The CPA has been retained as the auditor of a brokerage firm

A. Which owes the CPA audit fees for more than one year.

B. In which the CPA has a large active margin account.

C. In which the CPA's brother is the controller.

D. Which owes the CPA audit fees for current year services and has just filed a petition for

bankruptcy.

AACSB: Ethics

AICPA BB: Legal

AICPA FN: Decision Making

Blooms: Apply

Difficulty: 1 Easy

Learning Objective: 19-05 Acquire a working knowledge of the rules of conduct that apply to independence; integrity; and

objectivity.

Topic: Independence, Integrity, and Objectivity

30. The SEC has issued independence rules that differ from the AICPA's in all of the following

areas except:

A. Working paper documentation.

B. Provision of other professional services.

C. Human resource and compensation-related issues.

D. Required communication.

AACSB: Ethics

AICPA BB: Legal

AICPA FN: Decision Making

Blooms: Remember

Difficulty: 1 Easy

Learning Objective: 19-06 Know the basic differences between the SEC's independence rules for public company auditors and

AICPA standards for audits of nonpublic entities.

Topic: SEC and PCAOB Independence Requirements for Audits of Public Companies

19-38

31. Which of the following is not an element of quality control as defined by Statement of Quality

Control Standards No. 8?

A. Monitoring.

B. Independence.

C. Human resources.

D. Relevant ethical requirements.

AACSB: Ethics

AICPA BB: Legal

AICPA FN: Decision Making

Blooms: Remember

Difficulty: 1 Easy

Learning Objective: 19-08 Be able to explain the definition and elements of a system of quality control and how the AICPA's

peer review program relates to quality control.

Topic: Elements of Quality Control

32. A basic objective of a CPA firm is to provide professional services that conform to professional

standards. Reasonable assurance of achieving this basic objective is provided through

A. Compliance with generally accepted reporting standards.

B. A system of quality control.

C. A system of peer review.

D. Continuing professional education.

AACSB: Ethics

AICPA BB: Legal

AICPA FN: Decision Making

Blooms: Remember

Difficulty: 1 Easy

Learning Objective: 19-08 Be able to explain the definition and elements of a system of quality control and how the AICPA's

peer review program relates to quality control.

Topic: Quality Control Standards

19-39

33. The quality control standards are concerned primarily with

A. Actions of individual auditors.

B. A firm's monitoring of its practice.

C. Disciplinary actions against individual auditors.

D. Preventing legal action.

AACSB: Ethics

AICPA BB: Legal

AICPA FN: Decision Making

Blooms: Remember

Difficulty: 1 Easy

Learning Objective: 19-08 Be able to explain the definition and elements of a system of quality control and how the AICPA's

peer review program relates to quality control.

Topic: Elements of Quality Control

Topic: Quality Control Standards

34. Which of the following bodies ordinarily would have the authority to suspend or revoke a CPA's

license to practice public accounting?

A. The SEC.

B. The AICPA.

C. A state CPA society.

D. A state board of accountancy.

AACSB: Ethics

AICPA BB: Legal

AICPA FN: Decision Making

Blooms: Remember

Difficulty: 3 Hard

Learning Objective: 19-07 Know the rules of conduct that apply to general standards and accounting principles; responsibilities

to clients; and other responsibilities and practices.

Topic: Other Responsibilities and Practices

19-40

35. Which of the following statements best describes why the profession of certified public

accountants has deemed it essential to promulgate a code of conduct and to establish a

mechanism for enforcing observance of the code?

A. Ethical standards are established so that users of accounting services know what to expect,

the professionals know what behaviors are acceptable, and overseers can take disciplinary

action when appropriate.

B. A prerequisite to success is the establishment of an ethical code that stresses primarily the

professional's responsibility to clients and colleagues.

C. A requirement of most state laws calls for the profession to establish a code of conduct.

D. An essential means of self-protection for the profession is the establishment of flexible

ethical standards by the profession.

AACSB: Ethics

AICPA BB: Critical Thinking

AICPA FN: Decision Making

Blooms: Understand

Difficulty: 2 Medium

Learning Objective: 19-01 Know the definitions and general importance of ethics and professionalism.

Topic: Ethics and Professional Conduct

19-41

36. A CPA's license to practice will ordinarily be suspended or revoked automatically for

A. Controlling the bookkeeping for a compilation client.

B. Conviction of willful failure to file personal income tax return.

C. Refusing to respond to an inquiry by the AICPA practice review committee.

D. Accepting compensation while honoring a subpoena to appear as an expert witness.

AACSB: Ethics

AICPA BB: Legal

AICPA FN: Decision Making

Blooms: Apply

Difficulty: 2 Medium

Learning Objective: 19-04 Understand the framework for the Code of Professional Conduct; including principles; rules; and

interpretations.

Learning Objective: 19-07 Know the rules of conduct that apply to general standards and accounting principles; responsibilities

to clients; and other responsibilities and practices.

Topic: Other Responsibilities and Practices

Topic: Principles of Professional Conduct

Topic: Rules of Conduct

37. A CPA's retention of client records as a means of enforcing payment of an overdue audit fee is

an action that is

A. Considered acceptable by the AICPA Code of Professional Conduct.

B. Ill-advised because it would impair the CPA's independence with respect to the client.

C. Considered discreditable to the profession.

D. A violation of generally accepted auditing standards.

AACSB: Ethics

AICPA BB: Legal

AICPA FN: Decision Making

Blooms: Apply

Difficulty: 2 Medium

Learning Objective: 19-07 Know the rules of conduct that apply to general standards and accounting principles; responsibilities

to clients; and other responsibilities and practices.

Topic: Other Responsibilities and Practices

19-42

38. Which of the following is allowable for a CPA?

A. A used car loan from a banking client where the client has a lien on the car.

B. An uncollateralized signature loan from a client.

C. Owning more than five percent of the outstanding shares of client stock in a retirement

account.

D. The audit engagement partner serves on the client's audit committee.

AACSB: Ethics

AICPA BB: Legal

AICPA FN: Decision Making

Blooms: Apply

Difficulty: 2 Medium

Learning Objective: 19-04 Understand the framework for the Code of Professional Conduct; including principles; rules; and

interpretations.

Learning Objective: 19-05 Acquire a working knowledge of the rules of conduct that apply to independence; integrity; and

objectivity.

Topic: Independence, Integrity, and Objectivity

Topic: Principles of Professional Conduct

19-43

39. In performing an audit, Jackson, CPA, discovers that the professional competence necessary

for the engagement is lacking. Jackson informs management of the situation and recommends

another local CPA firm and management engages this other firm. Under these circumstances

A. Jackson may request compensation from the other CPA firm for any professional services

rendered to it in connection with the engagement.

B. Jackson may accept a referral fee from the other CPA firm.

C. Jackson has violated the AICPA Code of Professional Conduct because of non-fulfillment of

the duty of performance.

D. Jackson's lack of competence should be construed to be a violation of generally accepted

auditing standards.

AACSB: Ethics

AICPA BB: Legal

AICPA FN: Decision Making

Blooms: Analyze

Difficulty: 2 Medium

Learning Objective: 19-04 Understand the framework for the Code of Professional Conduct; including principles; rules; and

interpretations.

Learning Objective: 19-07 Know the rules of conduct that apply to general standards and accounting principles; responsibilities

to clients; and other responsibilities and practices.

Topic: General Standards and Accounting Principles

Topic: Principles of Professional Conduct

19-44

40. In which one of the following situations would a CPA be in violation of the AICPA Code of

Professional Conduct in determining a fee?

A. A fee based on whether the CPA's report on the client's financial statements results in the

approval of a bank loan.

B. A fee based on an estimate of the number of hours needed to complete the engagement by

auditors of various levels of experience.

C. A fee based on the nature of the service rendered and the CPA's particular expertise

instead of the actual time spent on the engagement.

D. A fee based on the fee charged by the prior auditor.

AACSB: Ethics

AICPA BB: Legal

AICPA FN: Decision Making

Blooms: Analyze

Difficulty: 2 Medium

Learning Objective: 19-07 Know the rules of conduct that apply to general standards and accounting principles; responsibilities

to clients; and other responsibilities and practices.

Topic: Responsibilities to Clients

19-45

41. In connection with a lawsuit, a third party attempts to gain access to the auditor's working

papers. The client's defense of privileged communication will be successful only to the extent it

is protected by the

A. Auditor's acquiescence in use of this defense.

B. Common law.

C. AICPA Code of Professional Conduct.

D. State law.

AACSB: Ethics

AICPA BB: Legal

AICPA FN: Decision Making

Blooms: Apply

Difficulty: 3 Hard

Learning Objective: 19-04 Understand the framework for the Code of Professional Conduct; including principles; rules; and

interpretations.

Learning Objective: 19-07 Know the rules of conduct that apply to general standards and accounting principles; responsibilities

to clients; and other responsibilities and practices.

Topic: Principles of Professional Conduct

Topic: Responsibilities to Clients

19-46

42. The profession's ethical standards would most likely be considered to have been violated when

the CPA represents that specific consulting services will be performed for a stated fee and it is

apparent at the time of the representation that the

A. CPA would not be independent.

B. Fee was a competitive bid.

C. Actual fee would be substantially higher.

D. Actual fee would be substantially lower than the fees charged by other CPAs for

comparable services.

AACSB: Ethics

AICPA BB: Legal

AICPA FN: Decision Making

Blooms: Remember

Difficulty: 2 Medium

Learning Objective: 19-04 Understand the framework for the Code of Professional Conduct; including principles; rules; and

interpretations.

Learning Objective: 19-07 Know the rules of conduct that apply to general standards and accounting principles; responsibilities

to clients; and other responsibilities and practices.

Topic: Principles of Professional Conduct

Topic: Responsibilities to Clients

19-47

43. According to the ethical standards of the profession, which of the following acts is generally

prohibited?

A. Issuing a modified report explaining a failure to follow a governmental regulatory agency's

standards when conducting an attest service for a client.

B. Revealing confidential client information during a quality review of a professional practice by

a team from the state CPA society.

C. Accepting a contingent fee for representing a client in an examination of the client's federal

tax return by an IRS agent.

D. Retaining client records after an engagement is terminated prior to completion and the

client has demanded its return.

AACSB: Ethics

AICPA BB: Legal

AICPA FN: Decision Making

Blooms: Apply

Difficulty: 2 Medium

Learning Objective: 19-04 Understand the framework for the Code of Professional Conduct; including principles; rules; and

interpretations.

Learning Objective: 19-07 Know the rules of conduct that apply to general standards and accounting principles; responsibilities

to clients; and other responsibilities and practices.

Topic: Other Responsibilities and Practices

Topic: Principles of Professional Conduct

Topic: Responsibilities to Clients

19-48

44. According to the ethical standards of the profession, which of the following acts is generally

prohibited?

A. Purchasing a product from a third party and reselling it to a client.

B. Writing a financial management newsletter promoted and sold by a publishing company.

C. Accepting a commission for recommending a product to an audit client.

D. Accepting engagements obtained through the efforts of third parties.

AACSB: Ethics

AICPA BB: Legal

AICPA FN: Decision Making

Blooms: Apply

Difficulty: 2 Medium

Learning Objective: 19-04 Understand the framework for the Code of Professional Conduct; including principles; rules; and

interpretations.

Learning Objective: 19-07 Know the rules of conduct that apply to general standards and accounting principles; responsibilities

to clients; and other responsibilities and practices.

Topic: Other Responsibilities and Practices

Topic: Principles of Professional Conduct

19-49

45. In which of the following circumstances would a CPA who audits XM Corporation lack

independence?

A. The CPA and XM's president are both on the board of directors of COD Corporation.

B. The CPA and XM's president each owns 25 percent of FOB Corporation, a closely-held

company.

C. The CPA has an automobile loan from XM, which is a savings and loan organization and

the loan is collateralized by the automobile.

D. The CPA reduced XM's usual audit fee by 40 percent because XM's financial condition was

unfavorable.

AACSB: Ethics

AICPA BB: Legal

AICPA FN: Decision Making

Blooms: Analyze

Difficulty: 2 Medium

Learning Objective: 19-05 Acquire a working knowledge of the rules of conduct that apply to independence; integrity; and

objectivity.

Topic: Independence, Integrity, and Objectivity

19-50

46. Mavis, CPA, has audited the financial statements of South Bay Sales Incorporated for several

years and had always been paid promptly for services rendered. Last year's audit invoices

have not been paid because South Bay is experiencing cash flow difficulties and the current

year's audit is scheduled to commence in one week. With respect to the past due audit fees,

Mavis should

A. Perform the scheduled audit and allow South Bay to pay when the cash flow difficulties are

alleviated.

B. Perform the scheduled audit only after arranging a definite payment schedule and securing

notes signed by South Bay.

C. Inform South Bay's management that the past due audit fees are considered an impairment

of auditor independence.

D. Inform South Bay's management that the past due audit fees may be considered a loan on

which interest must be imputed for financial statement purposes.

AACSB: Ethics

AICPA BB: Legal

AICPA FN: Decision Making

Blooms: Apply

Difficulty: 2 Medium

Learning Objective: 19-05 Acquire a working knowledge of the rules of conduct that apply to independence; integrity; and

objectivity.

Topic: Independence, Integrity, and Objectivity

19-51

47. In which of the following instances would the independence of the CPA not be considered to be

impaired? The CPA has been retained as the auditor of a

A. Charitable organization in which an employee of the CPA serves as treasurer.

B. Municipality in which the CPA owns $25,000 of the $2,500,000 indebtedness of the

municipality.

C. Restaurant where the CPA dines frequently.

D. Company in which the CPA's private investment club owns a one-tenth interest.

AACSB: Ethics

AICPA BB: Legal

AICPA FN: Decision Making

Blooms: Apply

Difficulty: 2 Medium

Learning Objective: 19-05 Acquire a working knowledge of the rules of conduct that apply to independence; integrity; and

objectivity.

Topic: Independence, Integrity, and Objectivity

48. A CPA firm's personnel partner periodically studies the CPA firm's personnel advancement

experience to ascertain whether the individuals who were assigned increased degrees of

responsibility met predetermined criteria. This is evidence of the CPA firm's adherence to

prescribed standards of

A. Quality control.

B. Due professional care.

C. Supervision and review.

D. Fieldwork.

AACSB: Ethics

AICPA BB: Legal

AICPA FN: Decision Making

Blooms: Apply

Difficulty: 2 Medium

Learning Objective: 19-08 Be able to explain the definition and elements of a system of quality control and how the AICPA's

peer review program relates to quality control.

Topic: Elements of Quality Control

19-52

49. A CPA firm would be reasonably assured of meeting its overall responsibility to provide

services that conform with professional standards by

A. Adhering to generally accepted accounting principles.

B. Implementing an appropriate system of quality control.

C. Joining professional societies that enforce ethical conduct.

D. Maintaining an attitude of independence in its engagements.

AACSB: Ethics

AICPA BB: Legal

AICPA FN: Decision Making

Blooms: Apply

Difficulty: 2 Medium

Learning Objective: 19-08 Be able to explain the definition and elements of a system of quality control and how the AICPA's

peer review program relates to quality control.

Topic: Elements of Quality Control

50. Which of the following is an element of a CPA firm's quality control system that should be

considered in establishing its quality control policies and procedures?

A. Using the audit risk model.

B. Using statistical sampling techniques.

C. Assigning personnel to engagements.

D. Considering audit risk and materiality.

AACSB: Ethics

AICPA BB: Critical Thinking

AICPA FN: Decision Making

Blooms: Apply

Difficulty: 2 Medium

Learning Objective: 19-08 Be able to explain the definition and elements of a system of quality control and how the AICPA's

peer review program relates to quality control.

Topic: Elements of Quality Control

19-53

51. What is the primary purpose of the acceptance and continuance of client relationships and

specific engagements element of quality control?

A. Guarantee that firms do not associate with clients whose management lacks integrity.

B. Provide reasonable assurance that firms do not associate with clients whose management

lacks integrity.

C. Guarantee that firms will not be sued as a result of association with a client.

D. Provide reasonable assurance that firms will not be sued as a result of association with a

client.

AACSB: Ethics

AICPA BB: Industry

AICPA FN: Risk Analysis

Blooms: Apply

Difficulty: 2 Medium

Learning Objective: 19-08 Be able to explain the definition and elements of a system of quality control and how the AICPA's

peer review program relates to quality control.

Topic: Elements of Quality Control

52. In order to achieve effective quality control, a firm of independent auditors should establish

policies and procedures for

A. Determining the minimum procedures necessary for unaudited financial statements.

B. Setting the scope of audit work.

C. Deciding whether to accept or continue a client.

D. Setting the scope of internal control study and evaluation.

AACSB: Ethics

AICPA BB: Industry

AICPA FN: Risk Analysis

Blooms: Apply

Difficulty: 2 Medium

Learning Objective: 19-08 Be able to explain the definition and elements of a system of quality control and how the AICPA's

peer review program relates to quality control.

Topic: Elements of Quality Control

19-54

53. Within the context of quality control, the primary purpose of continuing professional education

and training activities is to enable a CPA firm to provide personnel within the firm with

A. Technical training that ensures proficiency as an auditor.

B. Opportunities for career advancement outside the accounting firm.

C. Knowledge required to fulfill assigned responsibilities.

D. Knowledge required to perform a peer review.

AACSB: Ethics

AICPA BB: Industry

AICPA FN: Decision Making

Blooms: Analyze

Difficulty: 2 Medium

Learning Objective: 19-08 Be able to explain the definition and elements of a system of quality control and how the AICPA's

peer review program relates to quality control.

Topic: Elements of Quality Control

54. A CPA firm evaluates its personnel advancement experience to ascertain whether individuals

assigned to increased degrees of responsibility meet predetermined criteria. This policy is

evidence of the firm's adherence to which of the following prescribed standards?

A. Professional ethics.

B. Supervision and review.

C. Accounting and review services.

D. Quality control.

AACSB: Ethics

AICPA BB: Legal

AICPA FN: Decision Making

Blooms: Understand

Difficulty: 2 Medium

Learning Objective: 19-08 Be able to explain the definition and elements of a system of quality control and how the AICPA's

peer review program relates to quality control.

Topic: Elements of Quality Control

19-55

55. The primary purpose of establishing quality control policies and procedures for deciding

whether to accept a new client is to

A. Enable the CPA firm to attest to the reliability of the client.

B. Satisfy the CPA firm's duty to the public concerning the acceptance of new clients.

C. Minimize the likelihood of association with clients whose management lacks integrity.

D. Anticipate before performing any fieldwork whether an unqualified opinion can be

expressed.

AACSB: Ethics

AICPA BB: Industry

AICPA FN: Risk Analysis

Blooms: Apply

Difficulty: 2 Medium

Learning Objective: 19-08 Be able to explain the definition and elements of a system of quality control and how the AICPA's

peer review program relates to quality control.

Topic: Elements of Quality Control

56. Following the issuance of a PCAOB draft report, how many days does the CPA firm have to

respond to accusations?

A. 10 days.

B. 30 days.

C. 50 days.

D. 90 days.

AACSB: Ethics

AICPA BB: Legal

AICPA FN: Decision Making

Blooms: Remember

Difficulty: 2 Medium

Learning Objective: 19-09 Be familiar with the PCAOB inspection program for accounting firms that audit public companies.

Topic: PCAOB Inspections of Registered Public Accounting Firms

19-56

57. A violation of the profession's ethical standards would most likely occur when a CPA who

A. Is also admitted to the Bar represents on letterhead to be both an attorney and a CPA.

B. Writes a newsletter on financial management also permits a publishing company to solicit

subscriptions by direct mail.

C. Is controller of a bank permits the bank to use the controller's CPA title in the listing of

officers in its publications.

D. Refused to hire a new employee does so because the CPA deemed the candidate to be

"too old."

AACSB: Ethics

AICPA BB: Legal

AICPA FN: Decision Making

Blooms: Apply

Difficulty: 1 Easy

Learning Objective: 19-04 Understand the framework for the Code of Professional Conduct; including principles; rules; and

interpretations.

Learning Objective: 19-07 Know the rules of conduct that apply to general standards and accounting principles; responsibilities

to clients; and other responsibilities and practices.

Topic: Other Responsibilities and Practices

Topic: Principles of Professional Conduct

58. In determining estimates of fees, an auditor may take into account each of the following, except

the:

A. Value of the service to the client.

B. Degree of responsibility assumed by undertaking the engagement.

C. Skills required to perform the service.

D. Attainment of specific findings.

AACSB: Ethics

AICPA BB: Legal

AICPA FN: Decision Making

Blooms: Apply

Difficulty: 2 Medium

Learning Objective: 19-07 Know the rules of conduct that apply to general standards and accounting principles; responsibilities

to clients; and other responsibilities and practices.

Topic: Responsibilities to Clients

19-57

59. An auditor is about to commence a recurring annual audit engagement. The continuing

auditor's independence would ordinarily be considered to be impaired if the prior year's audit

fee

A. Was unusually large.

B. Has not been paid and will not be paid for at least twelve months.

C. Has not been paid and the client has filed a voluntary petition for bankruptcy.

D. Was renegotiated during the prior year audit based on the need for expanded testing.

AACSB: Ethics

AICPA BB: Legal

AICPA FN: Decision Making

Blooms: Apply

Difficulty: 2 Medium

Learning Objective: 19-04 Understand the framework for the Code of Professional Conduct; including principles; rules; and

interpretations.

Learning Objective: 19-05 Acquire a working knowledge of the rules of conduct that apply to independence; integrity; and

objectivity.

Topic: Independence, Integrity, and Objectivity

Topic: Principles of Professional Conduct

19-58

60. In which of the following circumstances would a CPA be bound by ethics to refrain from

disclosing any confidential information obtained during the course of a professional

engagement?

A. The CPA is issued a summons enforceable by a court order that orders the CPA to present

confidential information.

B. A major stockholder of a client company seeks accounting information from the CPA after

management declined to disclose the requested information.

C. Confidential client information is requested as part of a quality review of the CPA's practice

by a review team authorized by the AICPA.

D. An inquiry by a disciplinary body of a state CPA society requests confidential client

information.

AACSB: Ethics

AICPA BB: Legal

AICPA FN: Decision Making

Blooms: Apply

Difficulty: 2 Medium

Learning Objective: 19-04 Understand the framework for the Code of Professional Conduct; including principles; rules; and

interpretations.

Learning Objective: 19-07 Know the rules of conduct that apply to general standards and accounting principles; responsibilities

to clients; and other responsibilities and practices.

Topic: Principles of Professional Conduct

Topic: Responsibilities to Clients

19-59

61. Under which of the following circumstances would the independence of a CPA be considered

impaired if the CPA, who also is an attorney, serves as auditor and provides legal services to

the same client?

A. When the CPA, as legal agent, consummates a business acquisition for the client.

B. When the CPA's audit fees and legal fees are not billed separately.

C. When the CPA uses legal expertise to research a question of income tax law.

D. When the legal services consist of an analysis of the terms of an existing lease agreement.

AACSB: Ethics

AICPA BB: Legal

AICPA FN: Decision Making

Blooms: Apply

Difficulty: 3 Hard

Learning Objective: 19-05 Acquire a working knowledge of the rules of conduct that apply to independence; integrity; and

objectivity.

Topic: Independence, Integrity, and Objectivity

62. According to the profession's ethical standards, a CPA would be considered independent in

which of the following instances?

A. A client leases part of an office building from the CPA, resulting in a material indirect

financial interest to the CPA.

B. The CPA has a material direct financial interest in a client, but transfers the interest into a

blind trust.

C. The CPA owns an office building and the mortgage on the building is guaranteed by a

client.

D. The CPA belongs to a country club client in which membership requires an annual fee.

AACSB: Ethics

AICPA BB: Legal

AICPA FN: Decision Making

Blooms: Apply

Difficulty: 3 Hard

Learning Objective: 19-05 Acquire a working knowledge of the rules of conduct that apply to independence; integrity; and

objectivity.

Topic: Independence, Integrity, and Objectivity

19-60

63. When auditing a public company, which of the following impairs an auditor's independence?

A. Offering audit services as well as preparing the tax return for the same client.

B. The auditor's spouse works in the assembly line of an audit client.

C. Lack of fee disclosure in the client's annual report.

D. The auditor has been a partner on the engagement for ten years.

AACSB: Ethics

AICPA BB: Legal

AICPA FN: Decision Making

Blooms: Analyze

Difficulty: 2 Medium

Learning Objective: 19-06 Know the basic differences between the SEC's independence rules for public company auditors and

AICPA standards for audits of nonpublic entities.

Topic: SEC and PCAOB Independence Requirements for Audits of Public Companies

Short Answer Questions

64. Why do professions establish codes of conduct that define ethical behaviors for members of

the profession?

These rules are established so that users of the professional services know what to expect

when they purchase such services. The rules also let members of the profession know what

behavior is acceptable and allow the profession to monitor the actions of its members and

apply discipline where appropriate.

AACSB: Ethics

AICPA BB: Critical Thinking

AICPA FN: Decision Making

Blooms: Remember

Difficulty: 1 Easy

Learning Objective: 19-01 Know the definitions and general importance of ethics and professionalism.

Topic: Ethics and Professional Conduct

19-61

65. Distinguish between the following theories of ethical behavior: utilitarianism, a rights-based

approach, and a justice-based approach.

Utilitarianism focuses on the consequences of a decision on all individuals involved, and not

just the decision maker. The ethical choice is the choice that provides the greatest good to the

greatest number of people. A rights-based approach focuses on respecting the rights of

individuals. The ethical choice is the choice that avoids violating the rights of any involved

individual. The justice-based approach is concerned with equity, fairness, and impartiality to all

involved. The ethical choice is the choice that fairly and equitably distributes resources among

the individuals or groups affected.

AACSB: Ethics

AICPA BB: Critical Thinking

AICPA FN: Decision Making

Blooms: Understand

Difficulty: 2 Medium

Learning Objective: 19-02 Be able to explain three basic theories of ethical behavior and understand how to deal with ethical

challenges through an example situation.