Embed Size (px)

Citation preview

Published in July 2014

The current low level of CAPEX is a result of over-capitalization, which happened during the bull run in the late 2000s

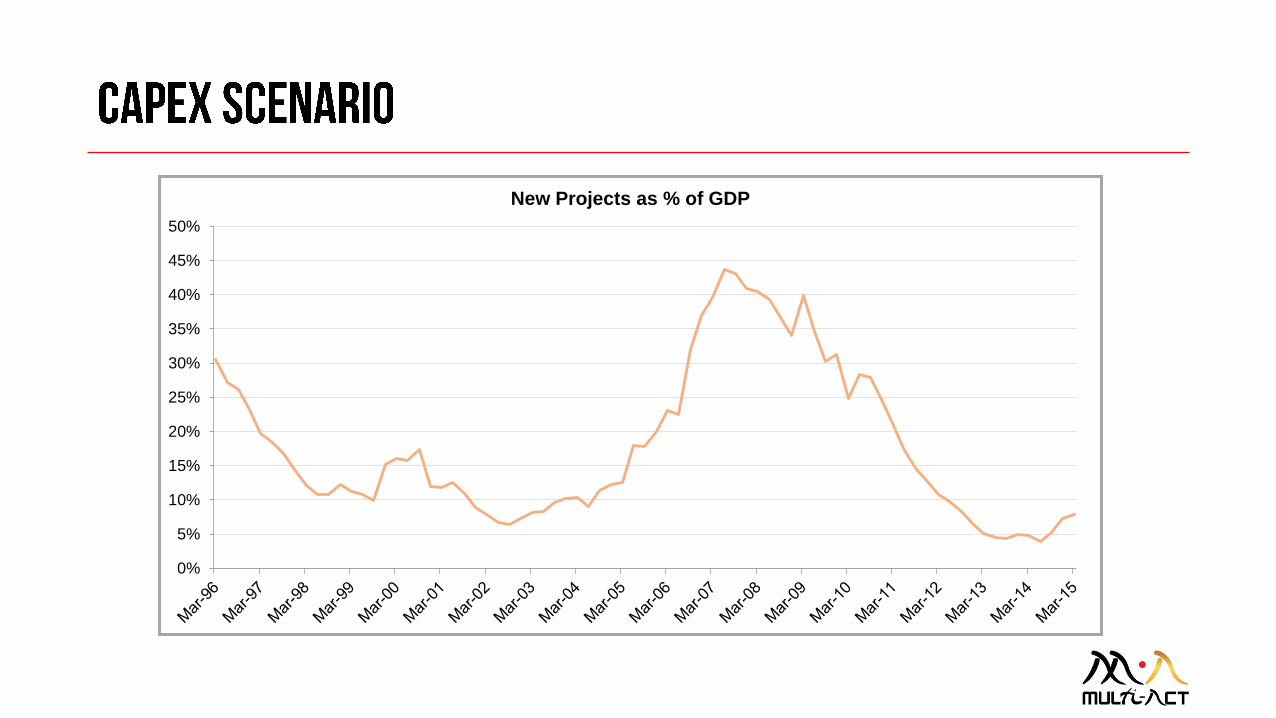

In India, CAPEX level has been falling since 2006 and is now the same as it was in the year 2001. Hence, new capital investment as a percentage of total GDP is at par with the lowest levels of the past 30 years

(as seen on next page).

Higher Capital Expenditure (CAPEX) in a country is believed to be a good indicator of economic growth, as it is indicative of the level of confidence in a country’s growth story.

About 40% of GDP was spent on CAPEX during 2006-09 indicating surge in investor optimism. In some sectors it led to excess credit creation which resulted in malinvestment.

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

New Projects as % of GDP

Direct beneficiaries of this turn in the cycle – the infrastructure stocks – might be susceptible to corporate governance issues and balance sheet weakness. However, the peripheral high quality (HQ) stocks, which

will be the indirect beneficiaries of revival, could be safer to invest in.

If the aforementioned CAPEX revival does set in, then there is an investment opportunity for picking stocks in high quality companies.

According to an April 2013 Credit Suisse report, investment will register a fiscal year average growth of 8% in 2013-14 and 12% in 2014-15, up from 1.5% in 2012-13.

Although the current dismal level of CAPEX indicates investor pessimism, it is also a sign of an imminent revival in the CAPEX cycle.

However, most of the private sector companies in infrastructure and power space have highly leveraged balance sheets which constrain them from raising more funds via the debt market.

Gradual beginnings of the revival are already visible in infrastructure sectors such as steel manufacturing and power.

India still requires huge investments in both infrastructure and power. Once issues like policy paralysis, debt-heavy private sector balance sheets and the equity markets (which are interlinked) get sorted– one

can expect a revival in the domestic CAPEX cycle.

A recent example of this happening has been the February sale by Tata Power of its 30% stake in PT Arutmin Indonesia coal asset to the Bakrie family.

The only way out for these companies is to offload their assets. This would reduce the debt burden and give them headroom to fund on-going or future projects.

Since infrastructure and power sectors are not doing too well in the equity markets, they are cash strapped in more than one way.

Through the following years, it has still been at a level comparable to 2001 levels but is expected to show further improvement in the next two years.

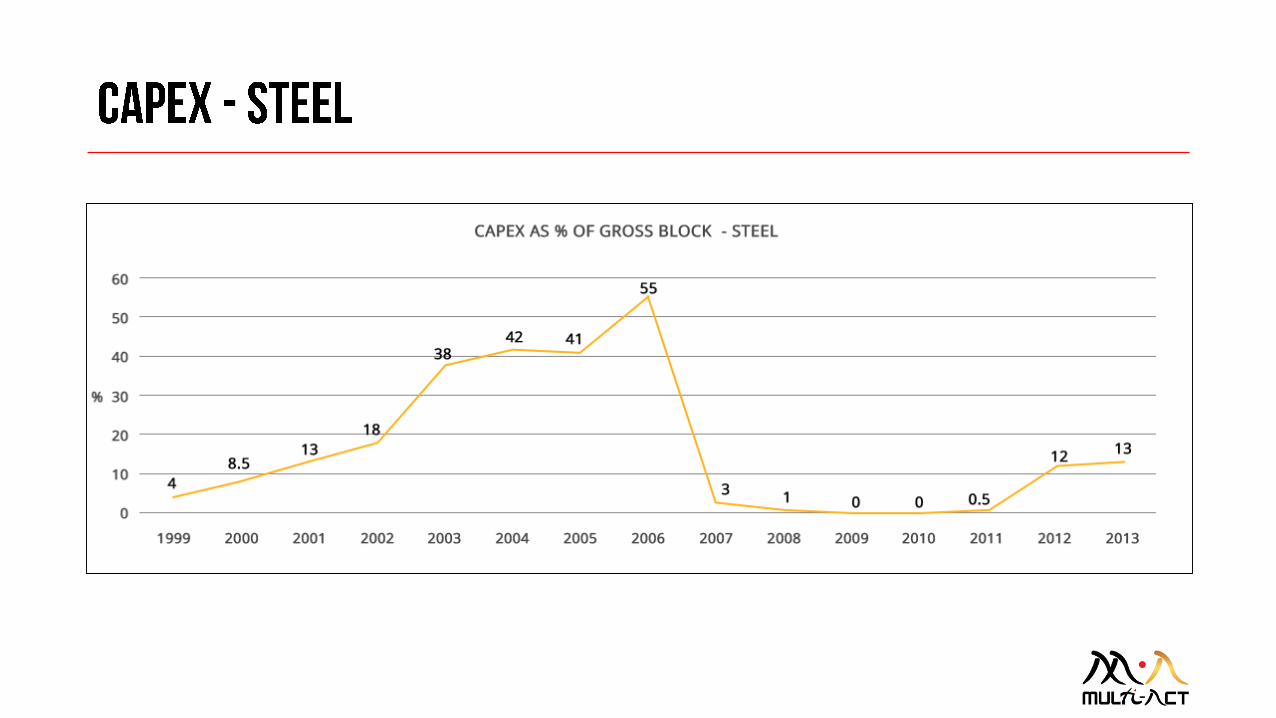

In the steel manufacturing sector, capital investment recovery is visible clearly from mid-2011 when CAPEX has shown an upward movement.

The chart above represents the combined CAPEX cycle of four large steel-producing companies in India — Tata Steel, Steel Authority of India Limited (SAIL), JSW Steel and Bhushan Steel Limited.

The best strategy would be to invest in high quality stocks that would indirectly benefit from the revival in the CAPEX cycle because when the cycle turns, investment recovery will begin with these

small and mid-sized companies.

CAPEX recovery makes it a good time to invest in high quality steel and other infrastructure stocks. If chosen now, these stocks will provide a high level of ‘margin of safety’ to the investor.

As most of the infrastructure and power stocks are doused with balance sheets and corporate governance issues, directly investing in the bigger names is not a safe bet for an investor.

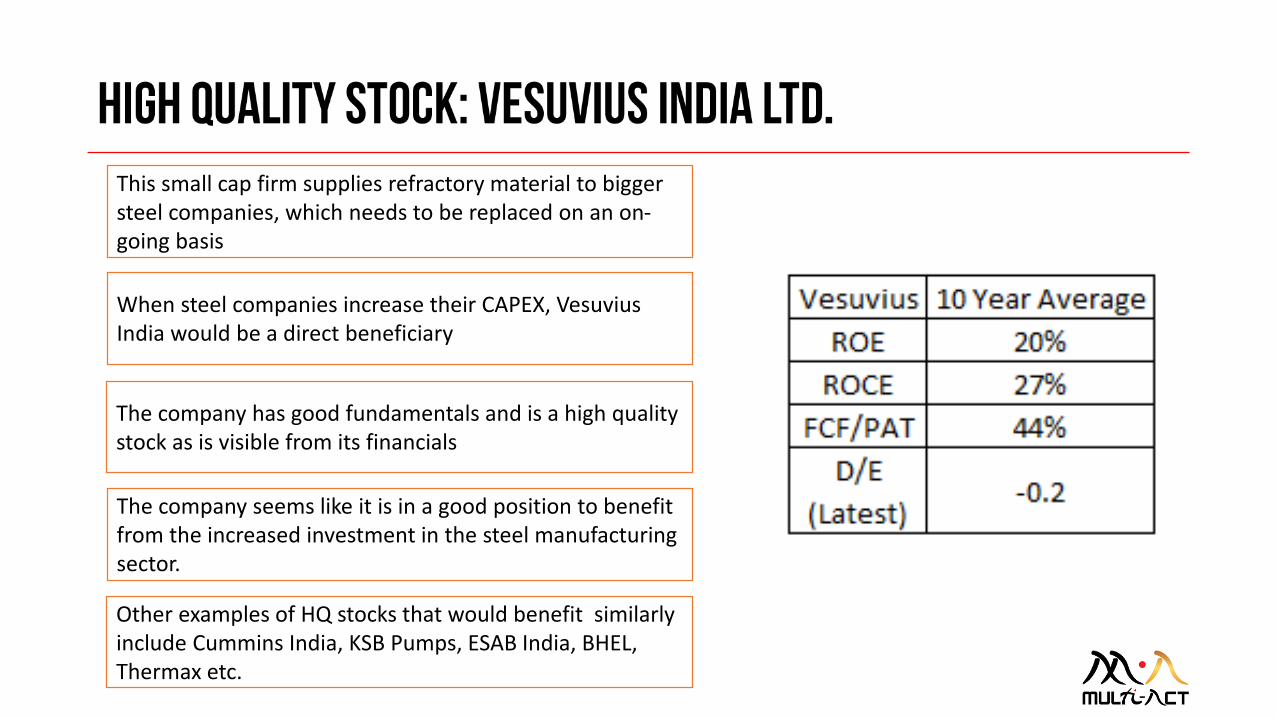

Other examples of HQ stocks that would benefit similarly include Cummins India, KSB Pumps, ESAB India, BHEL, Thermax etc.

The company has good fundamentals and is a high quality stock as is visible from its financials

When steel companies increase their CAPEX, Vesuvius India would be a direct beneficiary

This small cap firm supplies refractory material to bigger steel companies, which needs to be replaced on an on-going basis

The company seems like it is in a good position to benefit from the increased investment in the steel manufacturing sector.

• The Indian CAPEX cycle is turning, owing to which the steel industry is on the brink of revival.

• While it is an interesting time for cyclical stocks overall, the first wave of recovery will register more on the smaller HQ companies.

• Investors can enjoy a greater ‘safety of margin’ by investing in these indirect benefiters of CAPEX revival.

Statutory Details of the Portfolio Manager:Multi-Act Equity Consultancy Private Limited - SEBI Registered Portfolio Manager having Registration No. INP000002965

Disclaimer The views expressed in this article are for educational and reading purpose only. Multi-Act Equity Consultancy Private Limited (MAECL) does not solicit any course of action based on these views and the reader is advised to exercise independent judgment and act upon the same based on its/his/her sole discretion, their own investigations and risk-reward preferences. The article is prepared on the basis of publicly available information, internally developed data and from sources believed to be reliable. Due care has been taken to ensure that the facts are accurate and the views are fair. MAECL, its associates or any of their respective directors, employees, affiliates or representatives do not assume any responsibility for, or warrant the accuracy, completeness, adequacy and reliability of such views and consequently are not liable for any direct, indirect, special, incidental, consequential, punitive or exemplary damages, including lost profits arising in any way for decisions taken based on the said article. It is stated that, as permitted by SEBI Regulations and the internal Dealing Policy, the associates, employees, affiliates of MAECL may have interests in securities referred (if any). The contents herein – information or views – do not amount to distribution, guidelines, an offer or solicitation of any offer to buy or sell any securities or financial instruments, directly or indirectly, in the United States of America (US), in Canada, in jurisdictions where such distribution or offer is not authorized and in FATF non-compliant jurisdiction and are particularly not for US persons (being persons resident in the US, corporations, partnerships or other entities created or organized in or under the laws of the US or any person falling within the definition of the term “US person” under Regulation S promulgated under the US Securities Act of 1933, as amended) and persons of Canada.

Risk factors General risk factors • a. Securities investments are subject to market risks and there is no assurance or guarantee that the objective of the investments will be achieved.• b. Past performance of MAECL does not indicate its future performance. • b. As with any investment in securities, the value of investments can go up or down depending on the factors and forces affecting the capital market.

MAECL is not responsible / liable for any losses resulting from such factors.• c. Securities investments are subject to external risks such as war, natural calamities, and policy changes of local / international markets which affect

stock markets.• d. MAECL has renewed its SEBI PMS registration effective October 14, 2014 and has commenced its portfolio management activities with effect from

January 2011. However MAECL has more than 10 years of experience in managing its own funds invested in the domestic market.