Embed Size (px)

Citation preview

BUDGET ANALYSIS: 2014-2015

By:- Pankaj Kakkad (12213013)Rambabu Kumar (12213015)Shivam Bhagat (12213016)

WHAT IS BUDGET?A budget is an annual statement of the estimated

receipts and expenditures of the government during a financial year.

(a)This is a financial forecast for the next accounting year.

(b) It sets the sources of government receipts and expenditure for the coming financial year.

In the words of Prof. Taylor “A budget is a master plan of the government, it is an imperative instrument of economic policy to guide the proper allocation of resources”.

BUDGET – A FLASH BACKThe budget process of our country predates the independence.

Budget was first introduced on 7th April 1860 .

The first Finance Member ,James Wilson presented the budget.

Liaquat Ali Khan, member of the interim Govt. presented the budget of 1947-48.

After independence, India’s first Finance Minister R.K. Shanmukhan Chetty, presented the 1st budget on 26th November, 1947. and concentrated on agriculture while over the next ten years the focus moved to the industrial sector with a focus on forestry, fishing and textile.

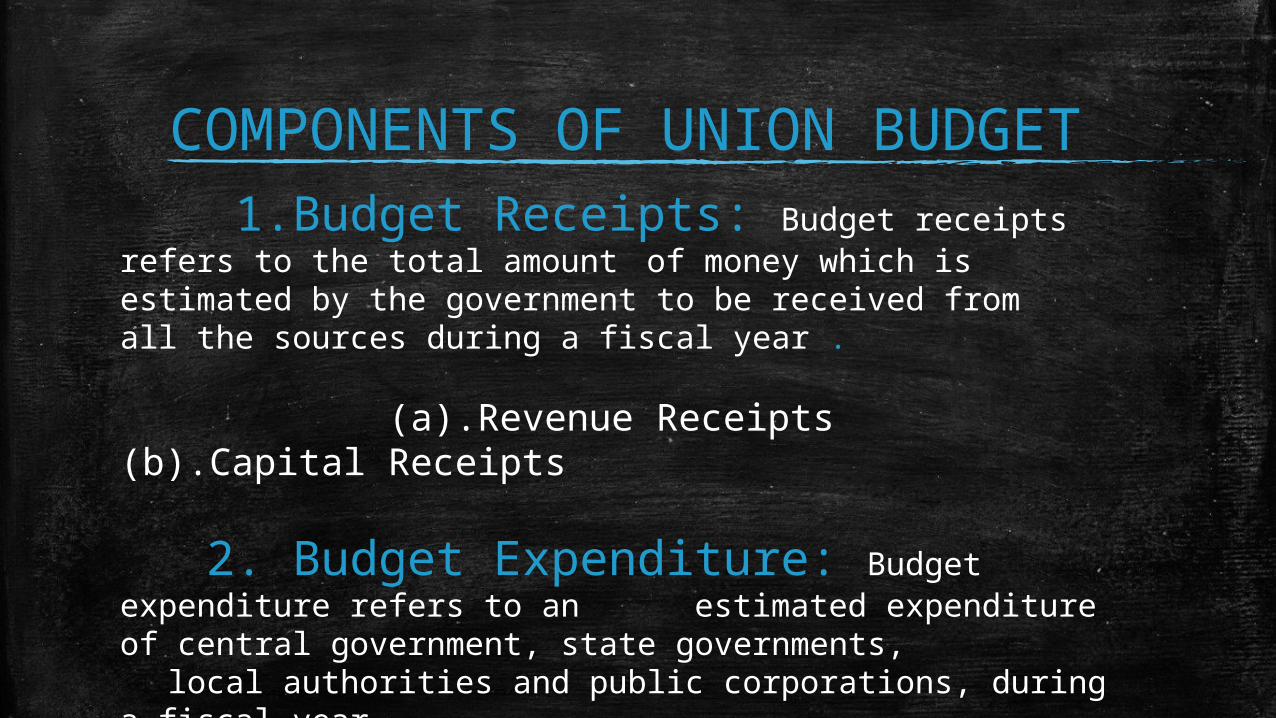

1.Budget Receipts: Budget receipts refers to the total amount of money which is estimated by the government to be received from all the sources during a fiscal year . (a).Revenue Receipts (b).Capital Receipts

2. Budget Expenditure: Budget expenditure refers to an estimated expenditure of central government, state governments,

local authorities and public corporations, during a fiscal year.

(a). Revenue Expenditure (b). Capital Expenditure

COMPONENTS OF UNION BUDGET

KEY POINT:

Revenue receipts are those receipts which do not create a liability or which do not reduce assets. It comprise of tax revenue and non-tax revenue.

Capital receipts are those receipts which raise funds either by incurring a liability or by disposing of assets. It is divided in following categories:

(i) Borrowing and other liabilities(ii) Recovery of loans(iii) Disinvestment

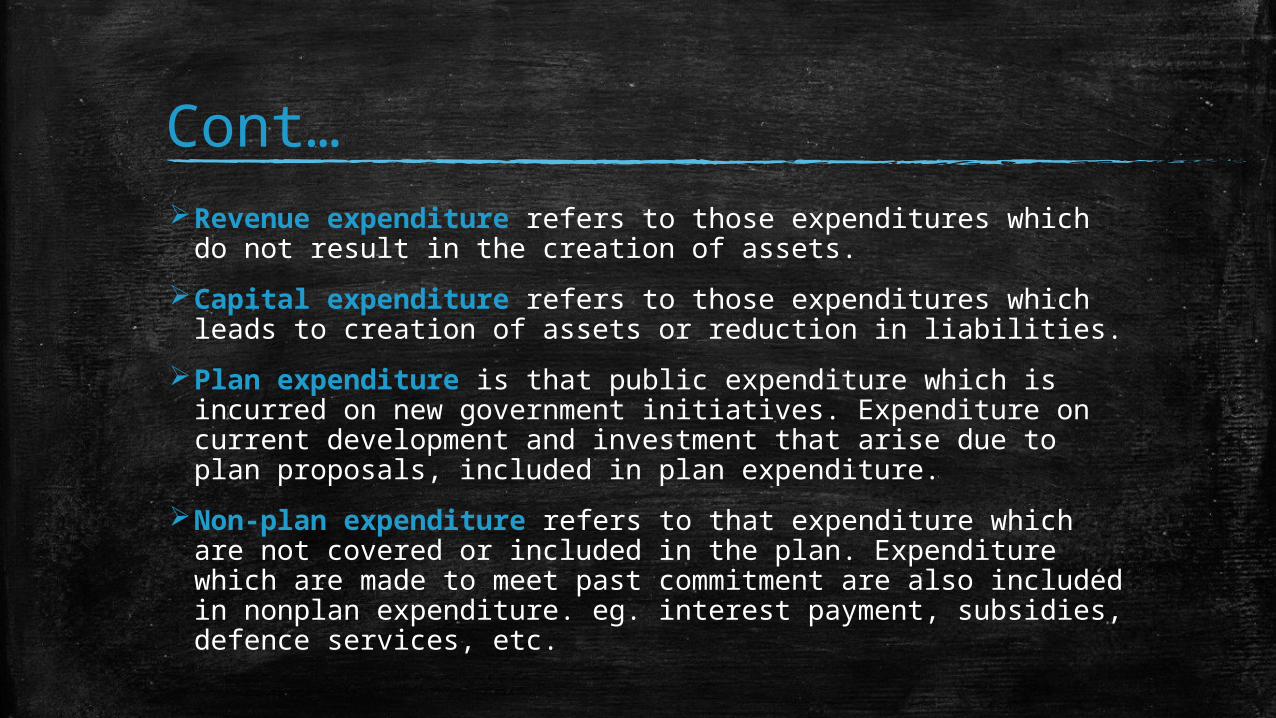

Cont…Revenue expenditure refers to those expenditures which do

not result in the creation of assets.

Capital expenditure refers to those expenditures which leads to creation of assets or reduction in liabilities.

Plan expenditure is that public expenditure which is incurred on new government initiatives. Expenditure on current development and investment that arise due to plan proposals, included in plan expenditure.

Non-plan expenditure refers to that expenditure which are not covered or included in the plan. Expenditure which are made to meet past commitment are also included in nonplan expenditure. eg. interest payment, subsidies, defence services, etc.

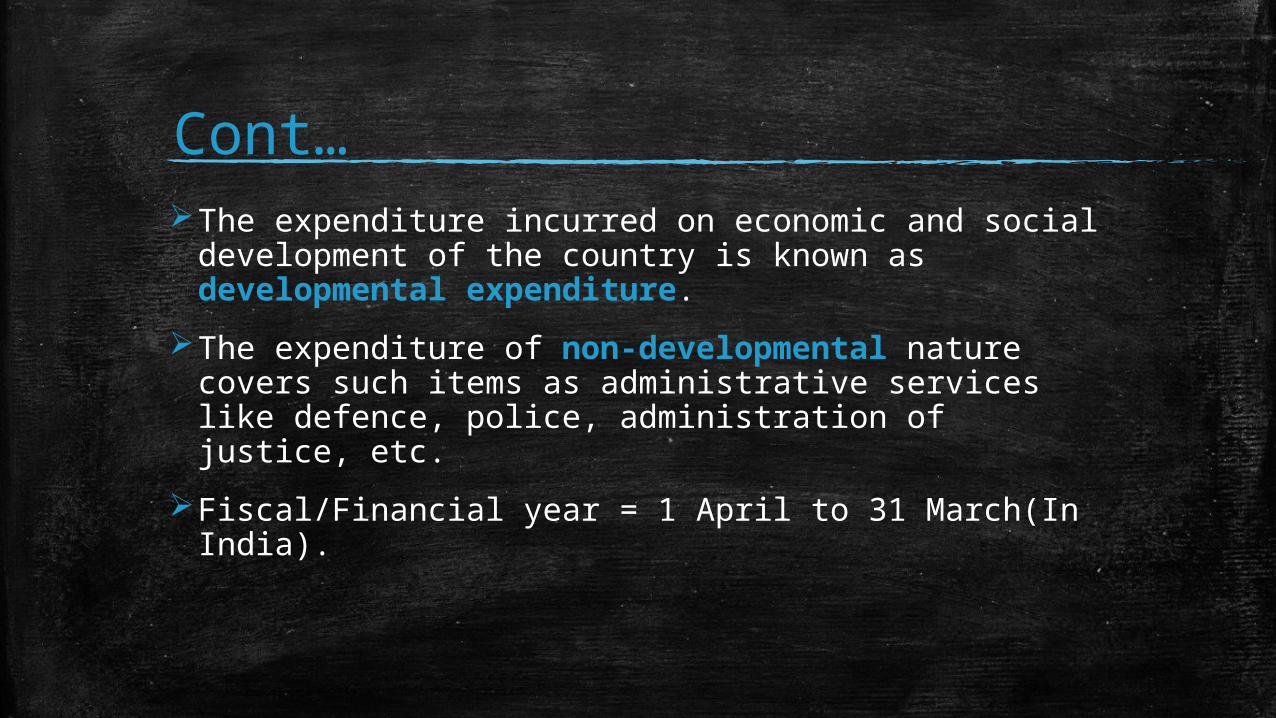

Cont…The expenditure incurred on economic and social

development of the country is known as developmental expenditure.

The expenditure of non-developmental nature covers such items as administrative services like defence, police, administration of justice, etc.

Fiscal/Financial year = 1 April to 31 March(In India).

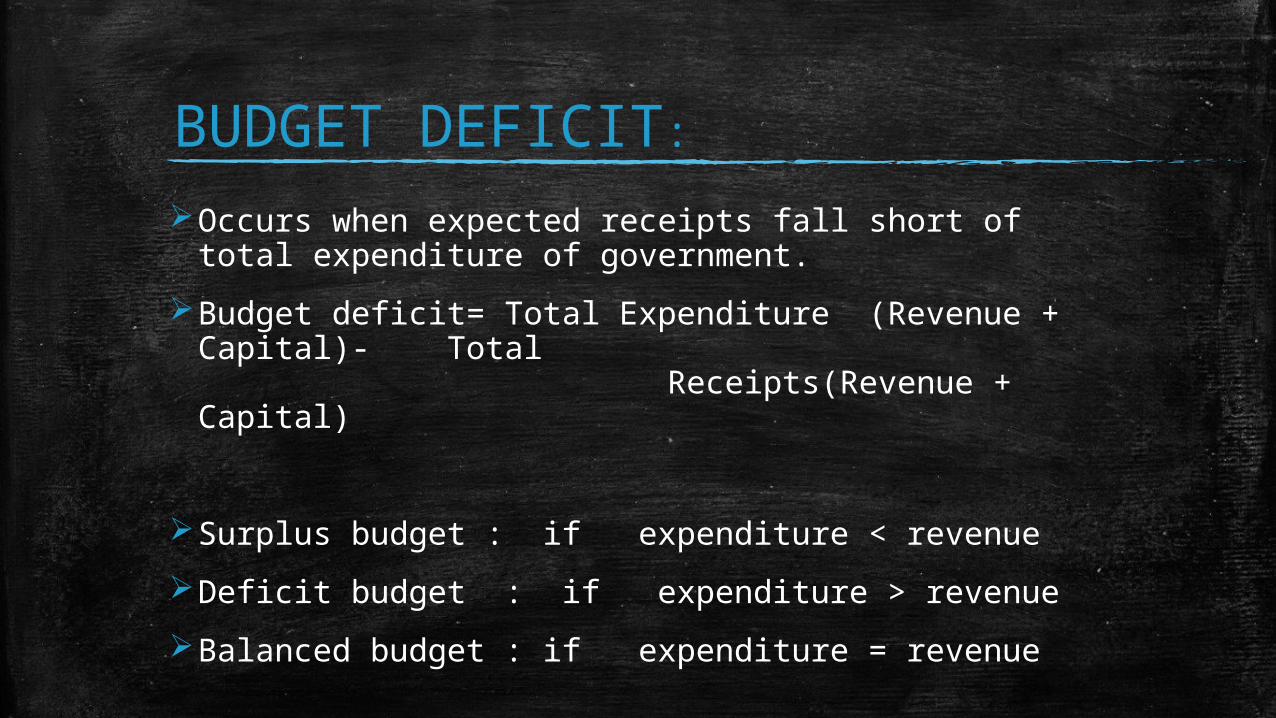

BUDGET DEFICIT:Occurs when expected receipts fall short of total

expenditure of government.

Budget deficit= Total Expenditure (Revenue + Capital)- Total Receipts(Revenue + Capital)

Surplus budget : if expenditure < revenue

Deficit budget : if expenditure > revenue

Balanced budget : if expenditure = revenue

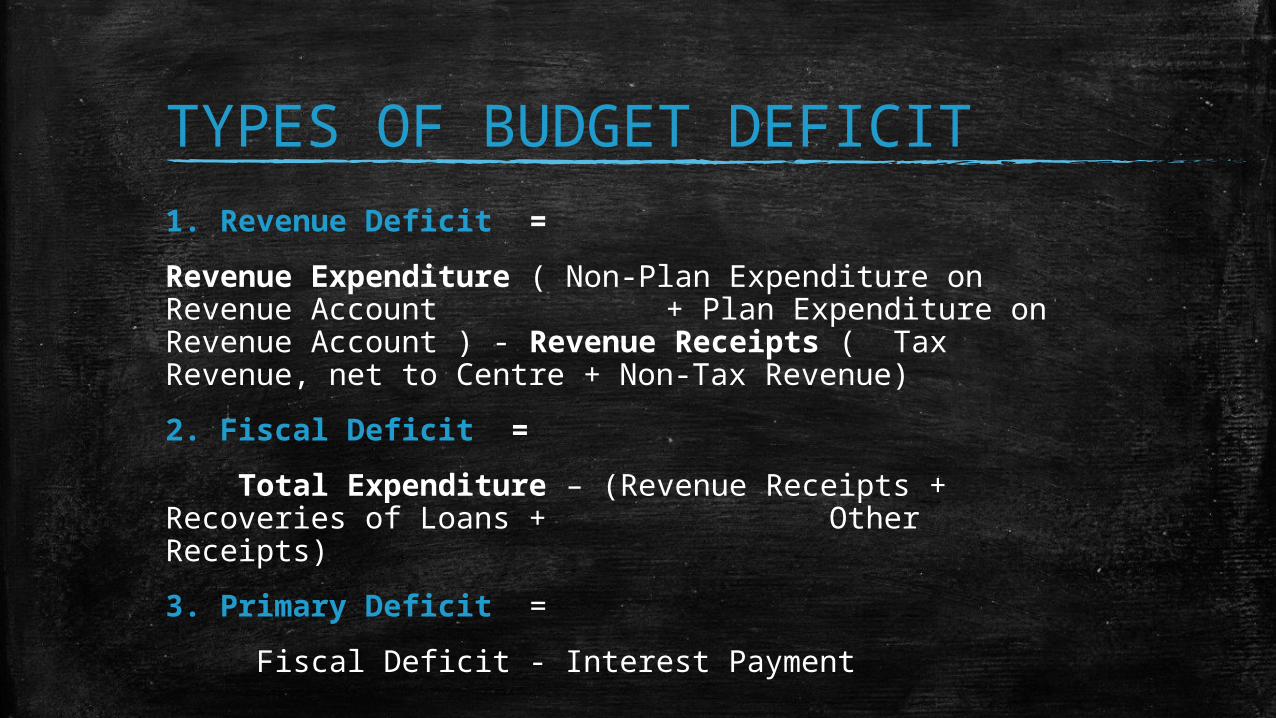

TYPES OF BUDGET DEFICIT

1. Revenue Deficit =

Revenue Expenditure ( Non-Plan Expenditure on Revenue Account + Plan Expenditure on Revenue Account ) - Revenue Receipts ( Tax Revenue, net to Centre + Non-Tax Revenue)

2. Fiscal Deficit =

Total Expenditure – (Revenue Receipts + Recoveries of Loans + Other Receipts)

3. Primary Deficit =

Fiscal Deficit - Interest Payment

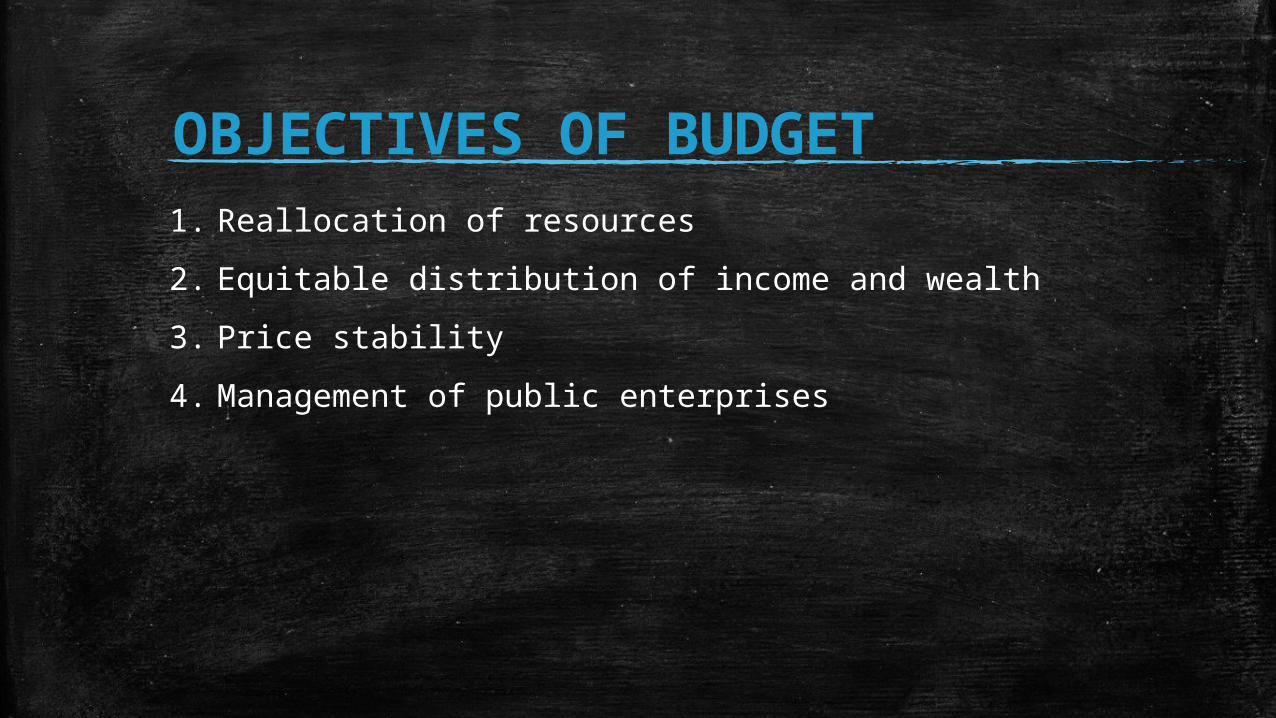

OBJECTIVES OF BUDGET 1. Reallocation of resources

2. Equitable distribution of income and wealth

3. Price stability

4. Management of public enterprises

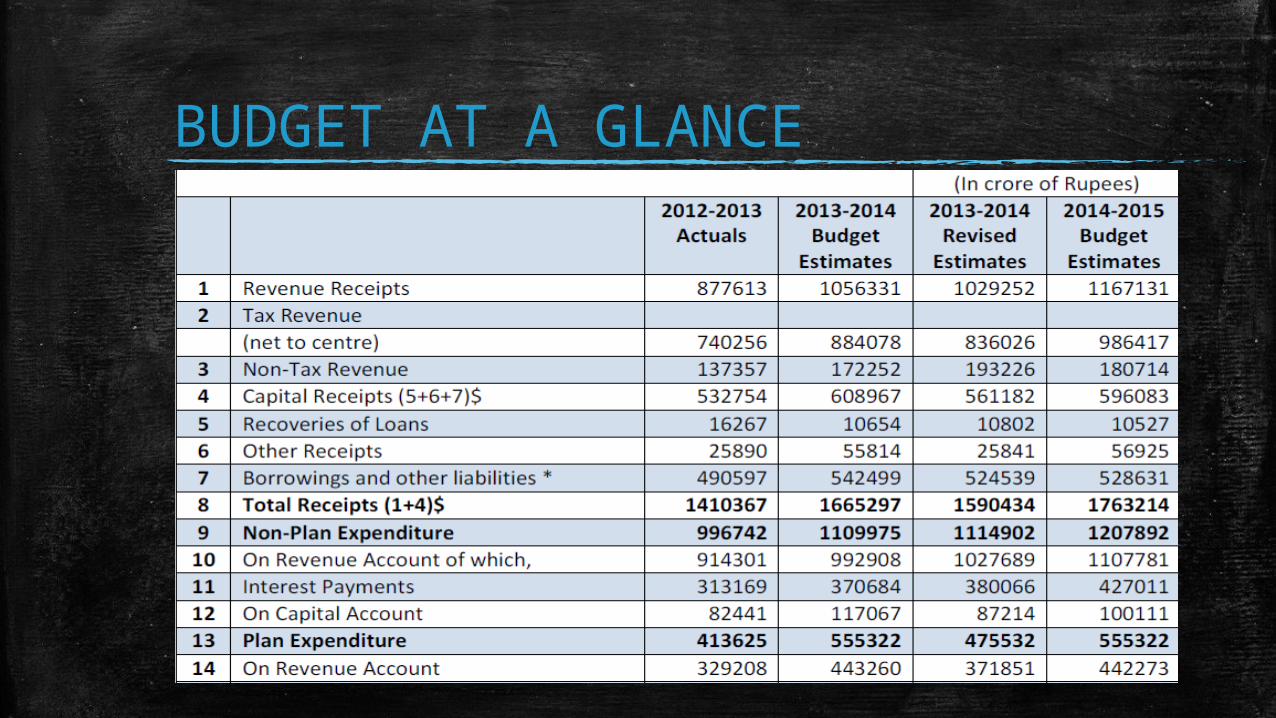

BUDGET AT A GLANCE

Cont…

ANALYSIS OF INDIAN UNION BUDGET

1.AGRICULTURE: RS. 22049 crore is decided for this sector for 2013-2014

which increased to RS. 27049 crore for 2014-2015.

▪ To increase the production to 6% which was 3.6 % in the previous year.

▪ Continuation of interest subvention scheme for agriculture sector along with a Credit Target of Rs 7 lakh crore for FY 2014-15 to adequately meet the financing needs of farmers and would help sustain the agricultural growth.

2.FISCAL CONSOLIDATION:

▪ announcement to contain the fiscal deficit at 4.6 % of GDP for 2013-14, which is lower than 4.8% budgeted for the year. This would help to channelize resources for investment and help contain inflation

▪ achieved at the cost of a cut in developmental expenditure, which is crucial for asset creation in the country

CURRENT ACCOUNT DEFICIT:

▪ The Current Account Deficit (CAD) that has threatened to exceed last year’s CAD of USD 88 billion, is expected to be contained at USD 45 billion

▪ will help stabilising the rupee

TAX REFORMS:

The Finance Minister’s appeal to all political parties to evolve a consensus to enactment of GST

▪ Direct Taxes Code (DTC) will be puton the website of the Ministry of Finance for a public discussion

▪ rationalize the current indirect tax regime, eliminate tax cascading and put the Indian economy on higher growth trajectory

3.MANUFACTURING:

The share of manufacturing has continued to hover at around 16 percent of GDP for the last two decades

The government has set a target of taking the share of manufacturing in GDP to 25 percent by 2022 which will create 100 million jobs within the decade requires the sector to record a growth of 12-14% per annum

▪ STEPS TAKEN : reduction of excise duty on capital goods and consumer non-durables from 12% to 10%

▪ reduction in excise duty from 12% to 8% on small cars, two wheelers and commercial vehicles and from 30% to 24% on SUVs

▪ 8 National Investment and Manufacturing Zones (NIMZ) along Delhi Mumbai Industrial Corridor (DMIC) have been announced. 9 Projects had been approved by the DMIC trust

▪ PROMOTING MSME:

▪ The MSME sector is known for its immense contribution for promoting employment intensive growth in the country

▪ Initial contribution of Rs. 100 crore to the corpus of ‘India Inclusive Innovation Fund’ under the Ministry of MSME

4.REFORMING FINANCIAL SECTOR:

▪ Key announcements made in the Budget for the Financial Sector

▪ BANKING:

▪ Finance Minister has managed to make some important allocations for the banking sector.

▪ Given the stressed assets in the banking sector, the Finance Minister’s allocated Rs 11,300 crore for strengthening the capital base of public sector banks .

Allocation of funds (Rs 200 Cr) for IFC Venture Fund would provide the much-needed boost to nurture innovation and entrepreneurship

Liberalizing the framework for Rupee denominated bond market and the launching of rupee denominated bond by IFC

Will help in internationalisation of Indian Currency

To enable smoother clearing and settlement for international investors looking to invest in Indian bonds and to increase capital inflow

FINANCIAL MARKETS:

5.EDUCATION LOAN:

▪ Rs 2600 crore is provided for education loan.

▪ to provide significant support to students during their non-earning years.

▪ Nearly 9 lakh students borrowers will benefit to the tune of approximately Rs 2,600 crore.

Completed With help of Dr. Balraj Rao.