Embed Size (px)

Citation preview

Positioning the bank at the heart of the expanding payments ecosystem Cards & Payments, Asia 2016

Devabalan Theyventheran

February 2014

Strictly Private and Confidential

Loon Wing Yuen Director Innovation Group Information and Operations Division

Suntec City, Singapore 21st. April, 2016

2

Agenda

Positioning the bank at the heart of the expanding payments ecosystem

►Banking on trust: how to leverage the faith customers have in their bank

►The other side of trust: doing away with it with blockchains and how can banks leverage this

►Technology and fin-tech startups: the growing collaboration imperative

►Big Data Science: how Big Data and Data Science can improve the payments value proposition

3

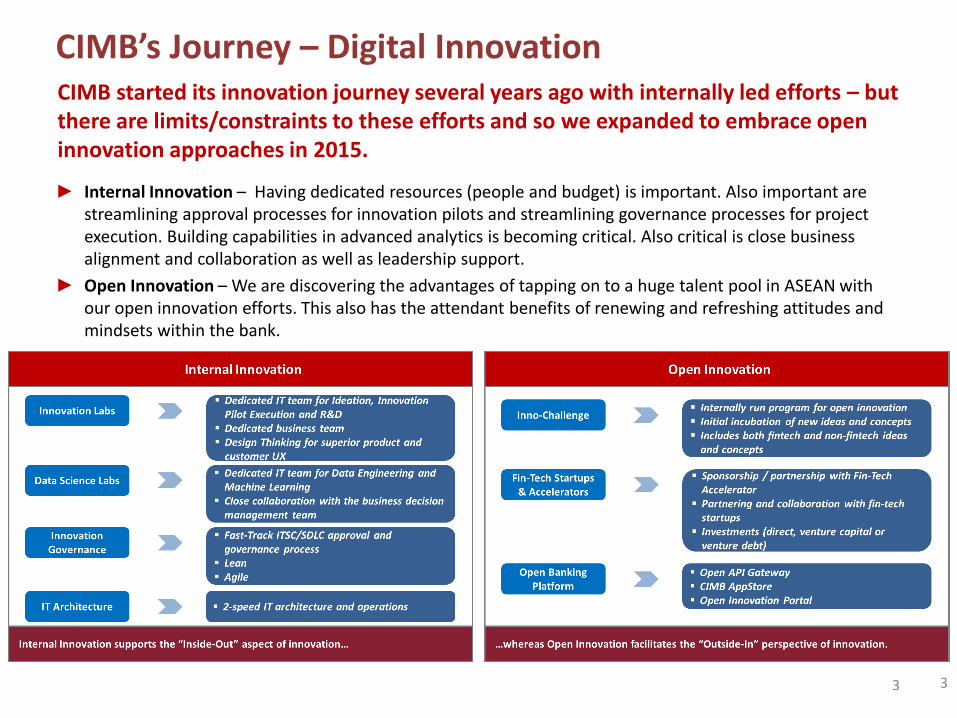

CIMB started its innovation journey several years ago with internally led efforts – but there are limits/constraints to these efforts and so we expanded to embrace open innovation approaches in 2015.

► Internal Innovation – Having dedicated resources (people and budget) is important. Also important are streamlining approval processes for innovation pilots and streamlining governance processes for project execution. Building capabilities in advanced analytics is becoming critical. Also critical is close business alignment and collaboration as well as leadership support.

► Open Innovation – We are discovering the advantages of tapping on to a huge talent pool in ASEAN with our open innovation efforts. This also has the attendant benefits of renewing and refreshing attitudes and mindsets within the bank.

CIMB’s Journey – Digital Innovation

3

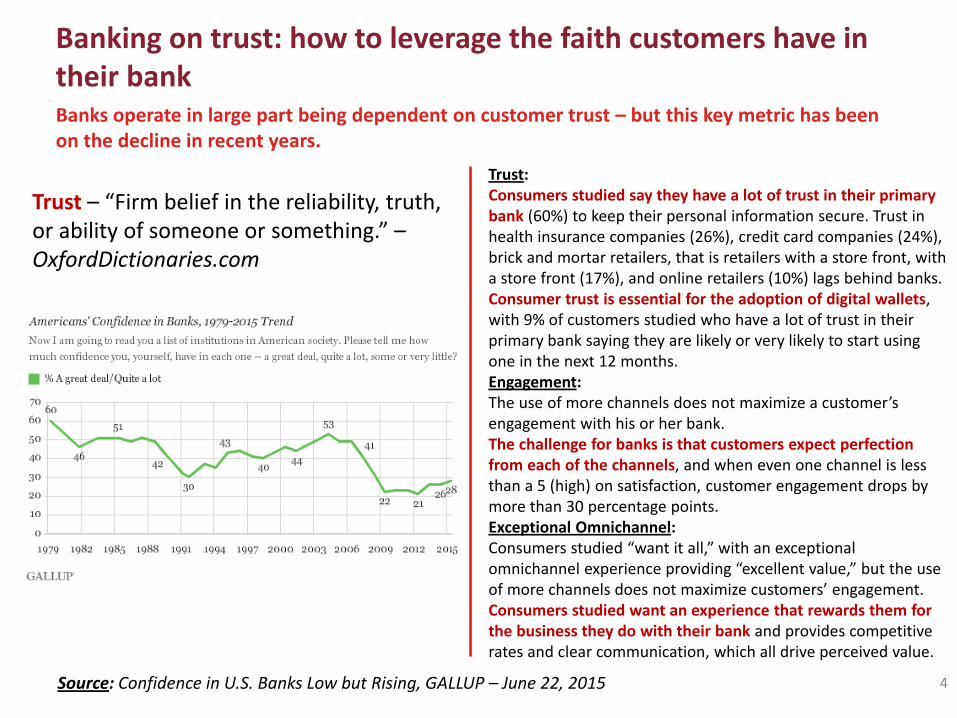

Banking on trust: how to leverage the faith customers have in their bank Banks operate in large part being dependent on customer trust – but this key metric has been on the decline in recent years.

Trust – “Firm belief in the reliability, truth, or ability of someone or something.” – OxfordDictionaries.com

Source: Confidence in U.S. Banks Low but Rising, GALLUP – June 22, 2015

Trust: Consumers studied say they have a lot of trust in their primary bank (60%) to keep their personal information secure. Trust in health insurance companies (26%), credit card companies (24%), brick and mortar retailers, that is retailers with a store front, with a store front (17%), and online retailers (10%) lags behind banks. Consumer trust is essential for the adoption of digital wallets, with 9% of customers studied who have a lot of trust in their primary bank saying they are likely or very likely to start using one in the next 12 months. Engagement: The use of more channels does not maximize a customer’s engagement with his or her bank. The challenge for banks is that customers expect perfection from each of the channels, and when even one channel is less than a 5 (high) on satisfaction, customer engagement drops by more than 30 percentage points. Exceptional Omnichannel: Consumers studied “want it all,” with an exceptional omnichannel experience providing “excellent value,” but the use of more channels does not maximize customers’ engagement. Consumers studied want an experience that rewards them for the business they do with their bank and provides competitive rates and clear communication, which all drive perceived value.

4

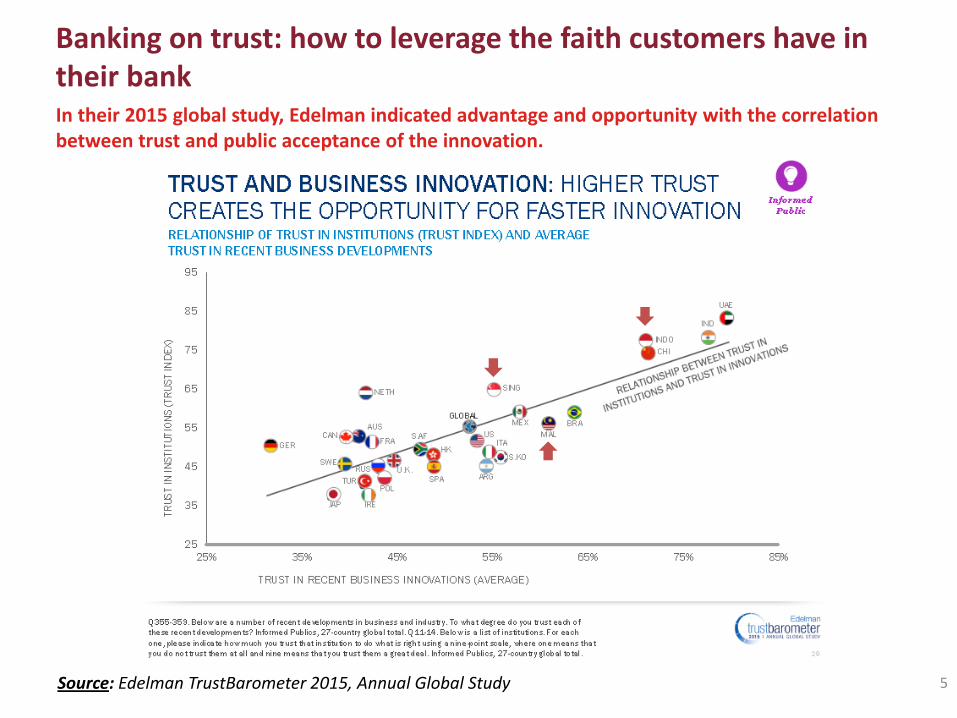

Banking on trust: how to leverage the faith customers have in their bank In their 2015 global study, Edelman indicated advantage and opportunity with the correlation between trust and public acceptance of the innovation.

Source: Edelman TrustBarometer 2015, Annual Global Study 5

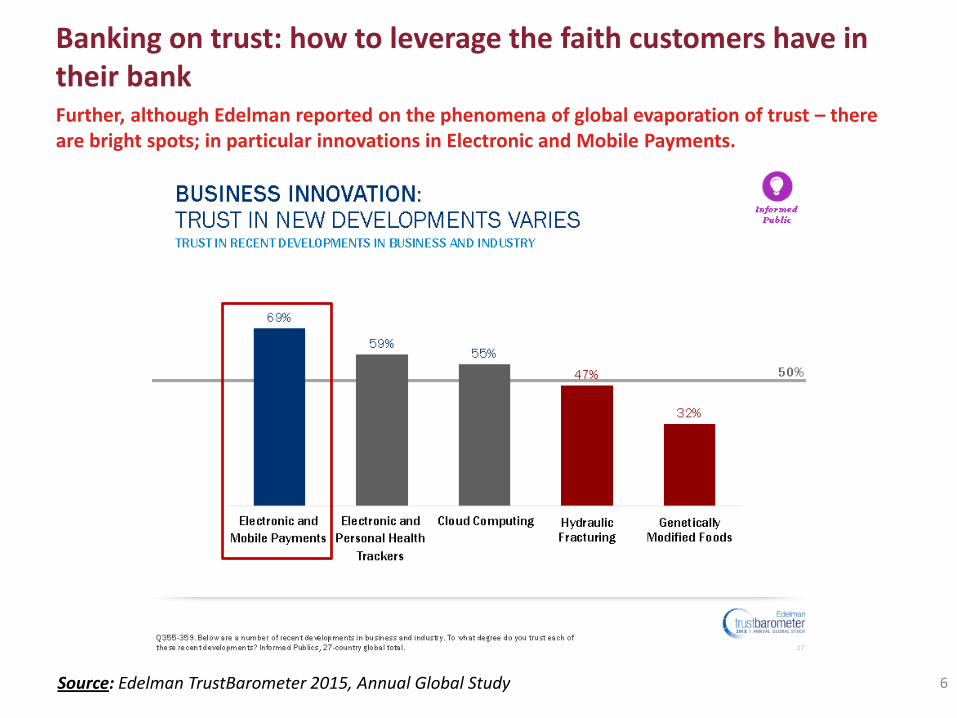

Banking on trust: how to leverage the faith customers have in their bank Further, although Edelman reported on the phenomena of global evaporation of trust – there are bright spots; in particular innovations in Electronic and Mobile Payments.

Source: Edelman TrustBarometer 2015, Annual Global Study 6

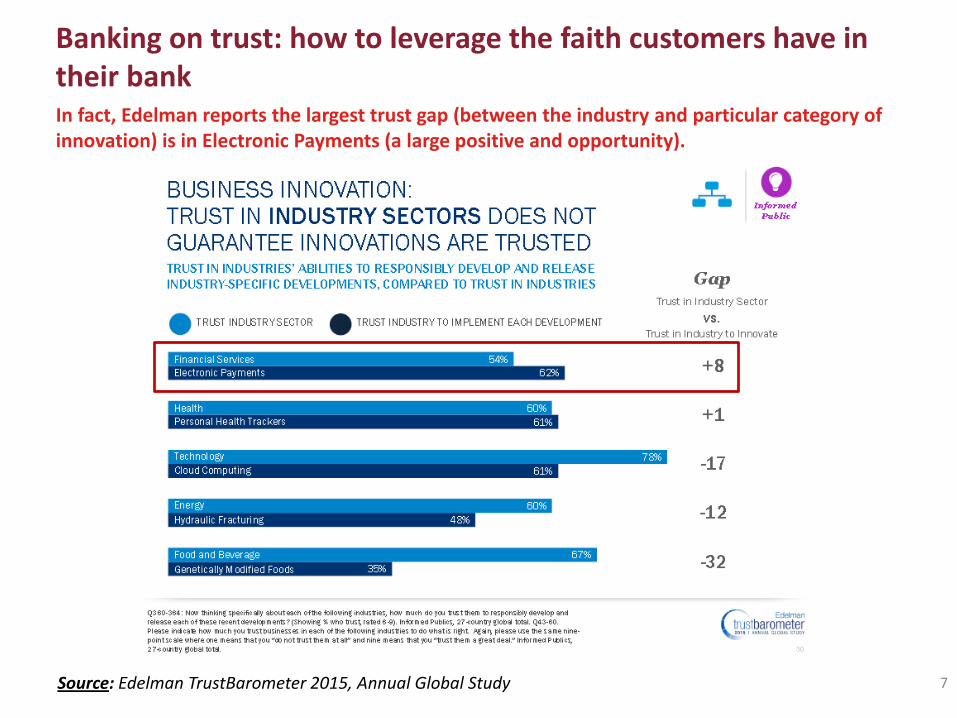

Banking on trust: how to leverage the faith customers have in their bank In fact, Edelman reports the largest trust gap (between the industry and particular category of innovation) is in Electronic Payments (a large positive and opportunity).

Source: Edelman TrustBarometer 2015, Annual Global Study 7

Banking on trust: how to leverage the faith customers have in their bank And there are clear advantages to gaining trust with customers.

Source: Edelman TrustBarometer 2015, Annual Global Study 8

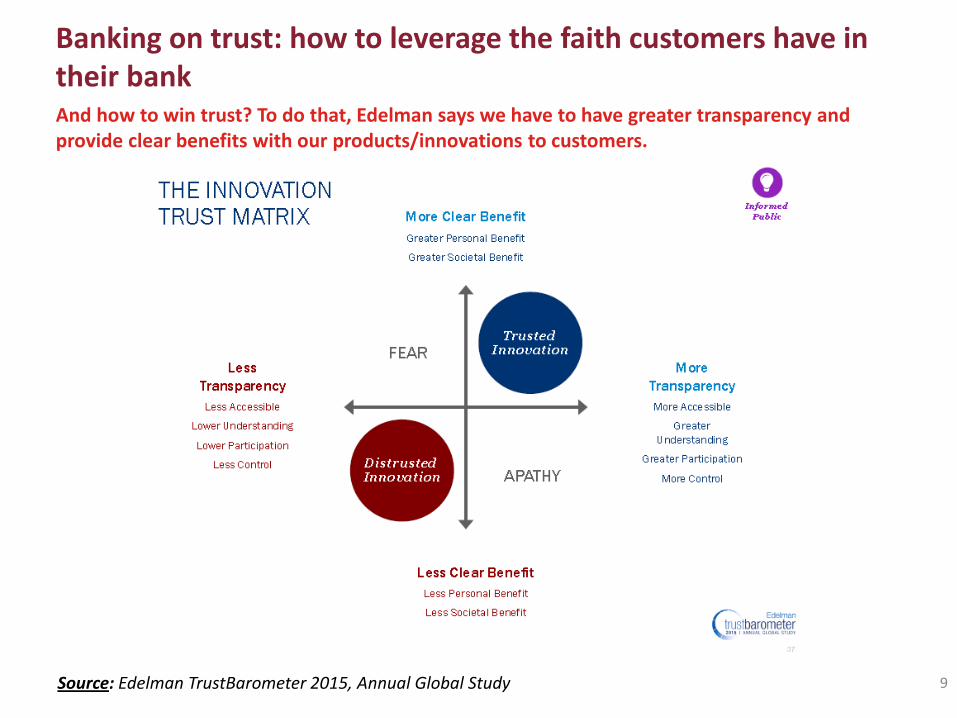

Banking on trust: how to leverage the faith customers have in their bank And how to win trust? To do that, Edelman says we have to have greater transparency and provide clear benefits with our products/innovations to customers.

Source: Edelman TrustBarometer 2015, Annual Global Study 9

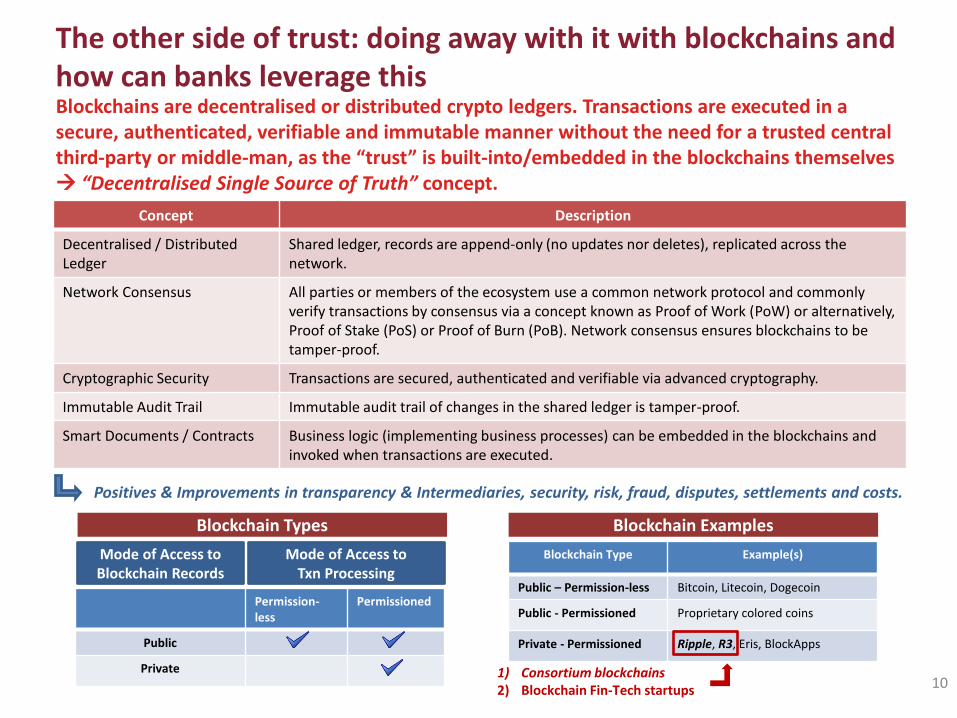

The other side of trust: doing away with it with blockchains and how can banks leverage this Blockchains are decentralised or distributed crypto ledgers. Transactions are executed in a secure, authenticated, verifiable and immutable manner without the need for a trusted central third-party or middle-man, as the “trust” is built-into/embedded in the blockchains themselves “Decentralised Single Source of Truth” concept.

10

Concept Description

Decentralised / Distributed Ledger

Shared ledger, records are append-only (no updates nor deletes), replicated across the network.

Network Consensus All parties or members of the ecosystem use a common network protocol and commonly verify transactions by consensus via a concept known as Proof of Work (PoW) or alternatively, Proof of Stake (PoS) or Proof of Burn (PoB). Network consensus ensures blockchains to be tamper-proof.

Cryptographic Security Transactions are secured, authenticated and verifiable via advanced cryptography.

Immutable Audit Trail Immutable audit trail of changes in the shared ledger is tamper-proof.

Smart Documents / Contracts Business logic (implementing business processes) can be embedded in the blockchains and invoked when transactions are executed.

Blockchain Types

Mode of Access to Blockchain Records

Mode of Access to Txn Processing

Permission- less

Permissioned

Public

Private

Blockchain Examples

Blockchain Type Example(s)

Public – Permission-less Bitcoin, Litecoin, Dogecoin

Public - Permissioned Proprietary colored coins

Private - Permissioned Ripple, R3, Eris, BlockApps

Positives & Improvements in transparency & Intermediaries, security, risk, fraud, disputes, settlements and costs.

1) Consortium blockchains 2) Blockchain Fin-Tech startups

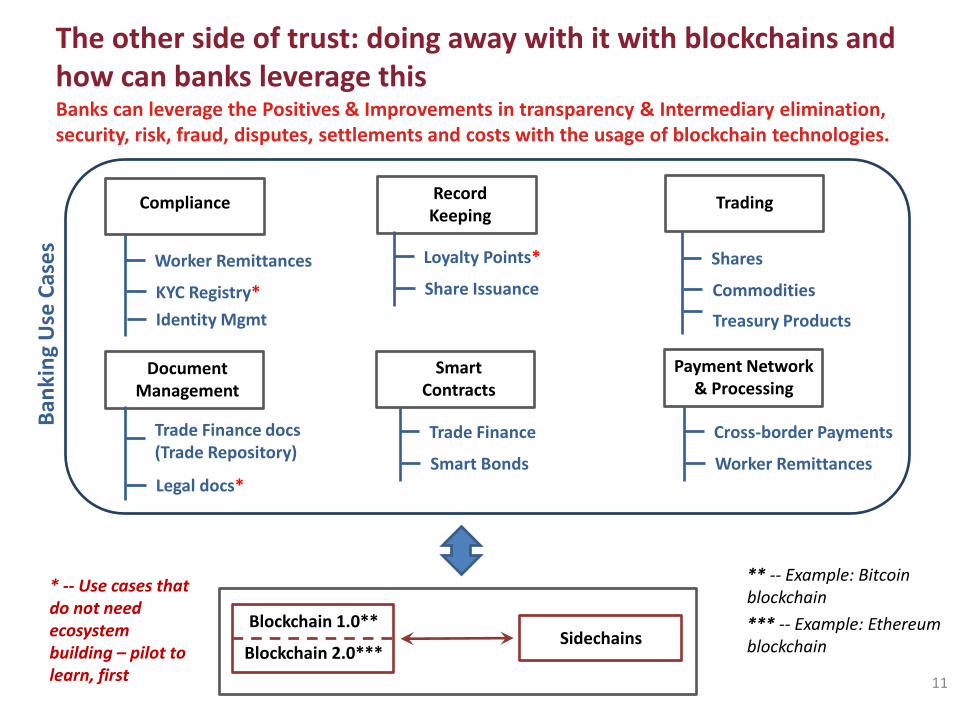

The other side of trust: doing away with it with blockchains and how can banks leverage this Banks can leverage the Positives & Improvements in transparency & Intermediary elimination, security, risk, fraud, disputes, settlements and costs with the usage of blockchain technologies.

11

Payment Network & Processing

Compliance Record Keeping

Trading

Document Management

Smart Contracts

Worker Remittances

KYC Registry*

Identity Mgmt

Loyalty Points*

Share Issuance

Shares

Commodities

Treasury Products

Trade Finance docs (Trade Repository)

Legal docs*

Trade Finance

Smart Bonds

Cross-border Payments

Worker Remittances

Blockchain 1.0**

Blockchain 2.0*** Sidechains

Ban

kin

g U

se C

ase

s

* -- Use cases that do not need ecosystem building – pilot to learn, first

** -- Example: Bitcoin blockchain

*** -- Example: Ethereum blockchain

12

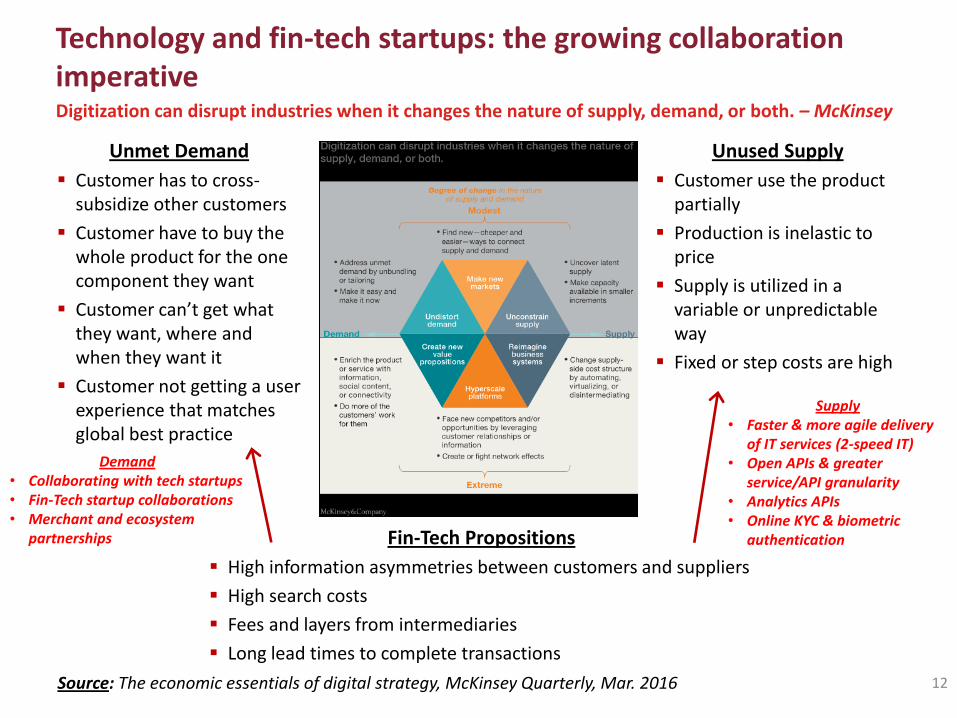

Technology and fin-tech startups: the growing collaboration imperative Digitization can disrupt industries when it changes the nature of supply, demand, or both. – McKinsey

Unused Supply

Customer use the product partially

Production is inelastic to price

Supply is utilized in a variable or unpredictable way

Fixed or step costs are high

Source: The economic essentials of digital strategy, McKinsey Quarterly, Mar. 2016

Unmet Demand

Customer has to cross-subsidize other customers

Customer have to buy the whole product for the one component they want

Customer can’t get what they want, where and when they want it

Customer not getting a user experience that matches global best practice

Fin-Tech Propositions

High information asymmetries between customers and suppliers

High search costs

Fees and layers from intermediaries

Long lead times to complete transactions

Demand • Collaborating with tech startups • Fin-Tech startup collaborations • Merchant and ecosystem

partnerships

Supply • Faster & more agile delivery

of IT services (2-speed IT) • Open APIs & greater

service/API granularity • Analytics APIs • Online KYC & biometric

authentication

13

Technology and fin-tech startups: the growing collaboration imperative The strengths and weaknesses of banks and that of fin-techs are largely complementary, opening up synergistic opportunities.

Fin-Tech Bank

Advantage Digital mindset Agility and culture of bias for speed Digital skills Big Data skills Culture of tolerance for failure Minimal regulatory oversight Technology architectures that are open

Trusted financial brand Existing licenses Infrastructure (security, KYC, AML, fraud) Specialised financial knowledge (risk, regulatory

compliance, complex financial products) Operational strength (clearing, settlement,

liquidity mgmt, FX, ALM) Customer base Client knowledge (of corporate clients and

treasurers)

Disadvantage The need to “scale trust” Small customer base

Siloed (processes, products and organisation) Legacy mindset Cost of maintaining legacy infrastructure leaves

little room for investments in innovation Technology infrastructure is insular

► B2C Fin-Techs Payments (for consumers) || B2B Fin-Techs Treasury (for corporate treasurers)

► As customers’ digital lifestyles grow in breadth and sophistication, it will be difficult for banks to meet all their needs

► Availability of Bank+Fintech Collaboration Infra is important (eg. OpenBanking APIs & SDK, Payment Hub ISO 20022 capable, Analytics APIs, etc.)

14

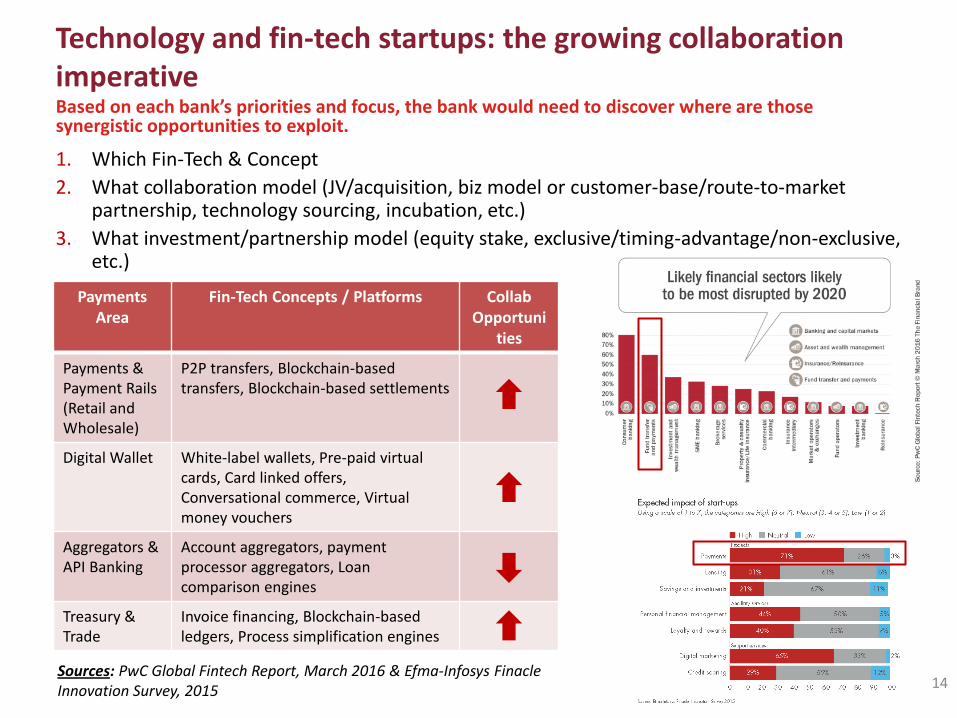

Technology and fin-tech startups: the growing collaboration imperative Based on each bank’s priorities and focus, the bank would need to discover where are those synergistic opportunities to exploit.

1. Which Fin-Tech & Concept

2. What collaboration model (JV/acquisition, biz model or customer-base/route-to-market partnership, technology sourcing, incubation, etc.)

3. What investment/partnership model (equity stake, exclusive/timing-advantage/non-exclusive, etc.)

Payments Area

Fin-Tech Concepts / Platforms Collab Opportuni

ties

Payments & Payment Rails (Retail and Wholesale)

P2P transfers, Blockchain-based transfers, Blockchain-based settlements

Digital Wallet White-label wallets, Pre-paid virtual cards, Card linked offers, Conversational commerce, Virtual money vouchers

Aggregators & API Banking

Account aggregators, payment processor aggregators, Loan comparison engines

Treasury & Trade

Invoice financing, Blockchain-based ledgers, Process simplification engines

Sources: PwC Global Fintech Report, March 2016 & Efma-Infosys Finacle Innovation Survey, 2015

15

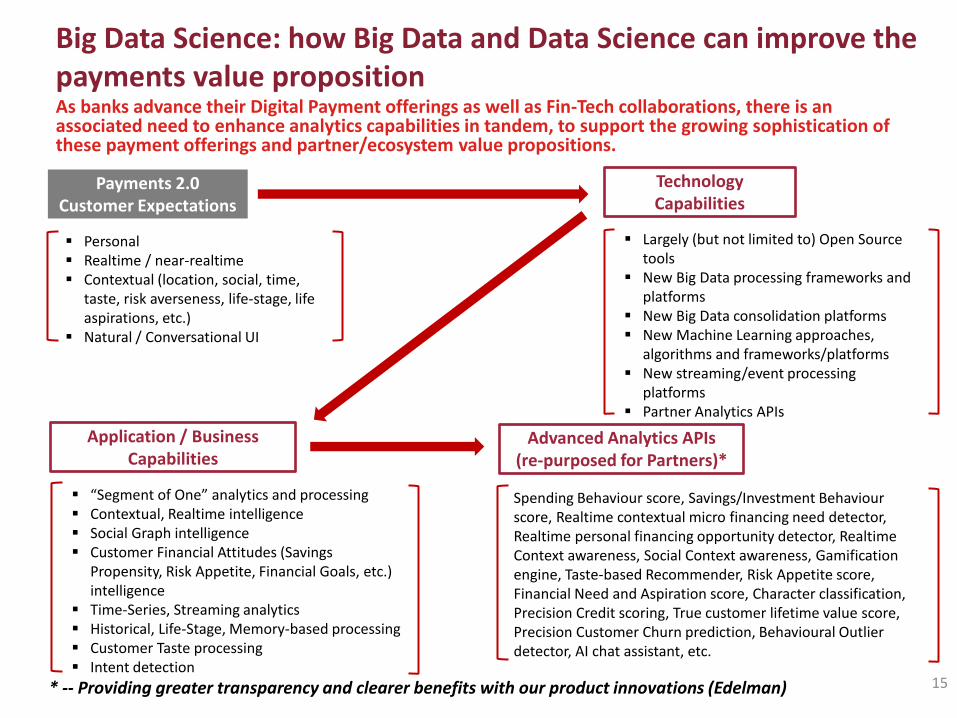

Technology Capabilities

Largely (but not limited to) Open Source tools

New Big Data processing frameworks and platforms

New Big Data consolidation platforms New Machine Learning approaches,

algorithms and frameworks/platforms New streaming/event processing

platforms Partner Analytics APIs

Application / Business Capabilities

“Segment of One” analytics and processing Contextual, Realtime intelligence Social Graph intelligence Customer Financial Attitudes (Savings

Propensity, Risk Appetite, Financial Goals, etc.) intelligence

Time-Series, Streaming analytics Historical, Life-Stage, Memory-based processing Customer Taste processing Intent detection

Advanced Analytics APIs (re-purposed for Partners)*

Spending Behaviour score, Savings/Investment Behaviour score, Realtime contextual micro financing need detector, Realtime personal financing opportunity detector, Realtime Context awareness, Social Context awareness, Gamification engine, Taste-based Recommender, Risk Appetite score, Financial Need and Aspiration score, Character classification, Precision Credit scoring, True customer lifetime value score, Precision Customer Churn prediction, Behavioural Outlier detector, AI chat assistant, etc.

Big Data Science: how Big Data and Data Science can improve the payments value proposition

Payments 2.0 Customer Expectations

Personal Realtime / near-realtime Contextual (location, social, time,

taste, risk averseness, life-stage, life aspirations, etc.)

Natural / Conversational UI

As banks advance their Digital Payment offerings as well as Fin-Tech collaborations, there is an associated need to enhance analytics capabilities in tandem, to support the growing sophistication of these payment offerings and partner/ecosystem value propositions.

* -- Providing greater transparency and clearer benefits with our product innovations (Edelman)

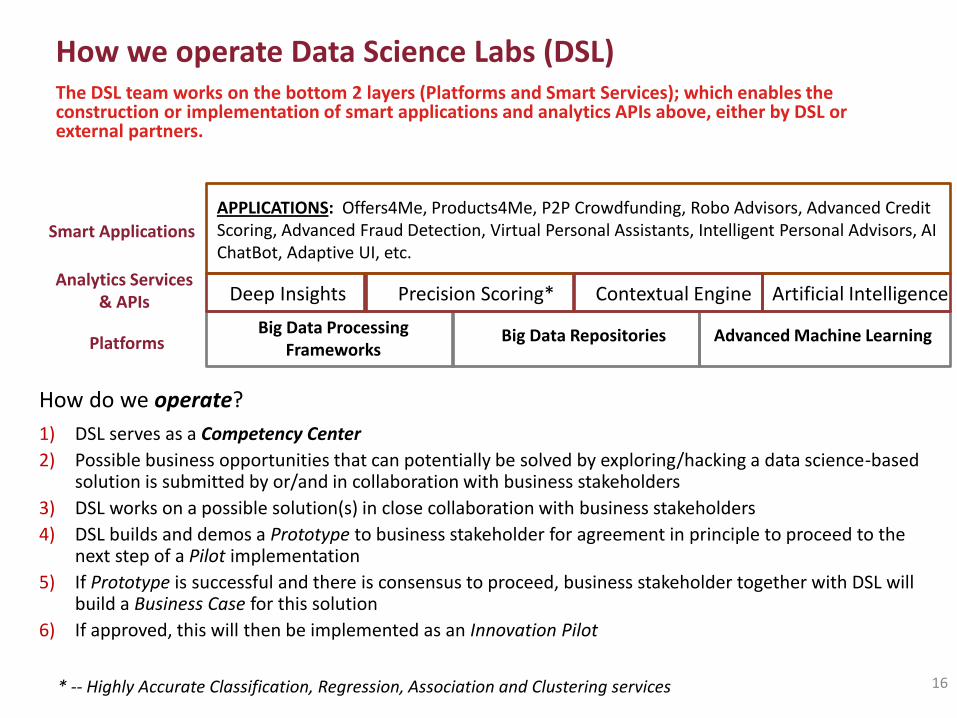

How we operate Data Science Labs (DSL) The DSL team works on the bottom 2 layers (Platforms and Smart Services); which enables the construction or implementation of smart applications and analytics APIs above, either by DSL or external partners.

16 * -- Highly Accurate Classification, Regression, Association and Clustering services

Platforms Big Data Processing

Frameworks Big Data Repositories Advanced Machine Learning

Deep Insights Precision Scoring* Artificial Intelligence

APPLICATIONS: Offers4Me, Products4Me, P2P Crowdfunding, Robo Advisors, Advanced Credit Scoring, Advanced Fraud Detection, Virtual Personal Assistants, Intelligent Personal Advisors, AI ChatBot, Adaptive UI, etc.

Analytics Services & APIs

Smart Applications

How do we operate?

1) DSL serves as a Competency Center

2) Possible business opportunities that can potentially be solved by exploring/hacking a data science-based solution is submitted by or/and in collaboration with business stakeholders

3) DSL works on a possible solution(s) in close collaboration with business stakeholders

4) DSL builds and demos a Prototype to business stakeholder for agreement in principle to proceed to the next step of a Pilot implementation

5) If Prototype is successful and there is consensus to proceed, business stakeholder together with DSL will build a Business Case for this solution

6) If approved, this will then be implemented as an Innovation Pilot

Contextual Engine

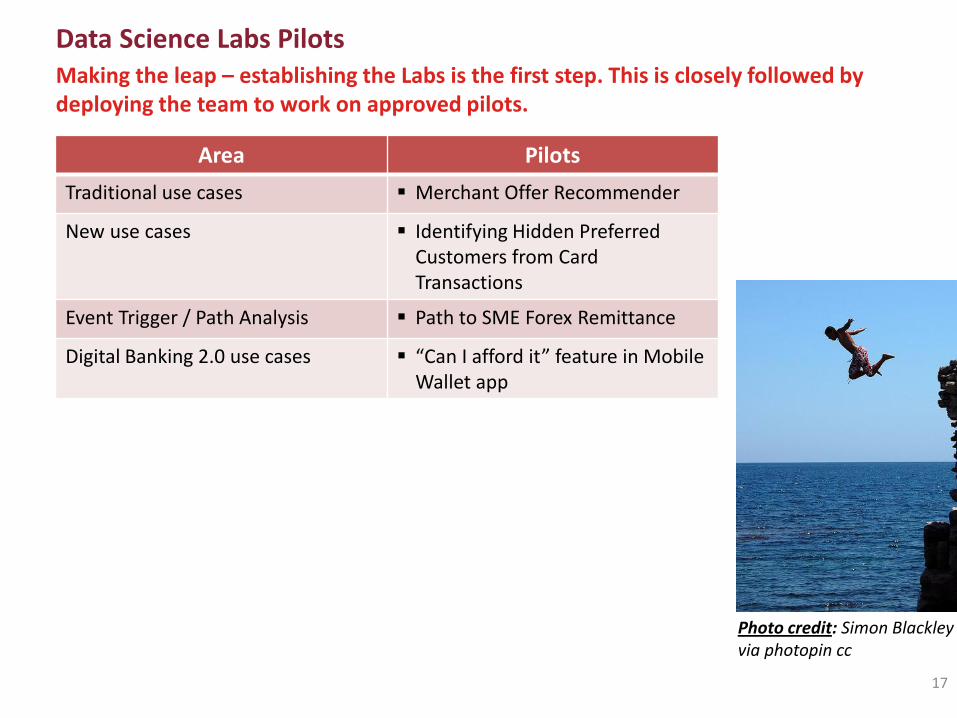

Data Science Labs Pilots Making the leap – establishing the Labs is the first step. This is closely followed by deploying the team to work on approved pilots.

17

Area Pilots

Traditional use cases Merchant Offer Recommender

New use cases Identifying Hidden Preferred Customers from Card Transactions

Event Trigger / Path Analysis Path to SME Forex Remittance

Digital Banking 2.0 use cases “Can I afford it” feature in Mobile Wallet app

Photo credit: Simon Blackley via photopin cc

Summary Positioning the bank at the heart of the expanding payments ecosystem and the path to payments self-disruption.

18

Photo credit: www.p360.dk

► Leverage customer trust in banking

► Opportunity in the area of public trust in the area of Payments and Wallet innovations (in the ASEAN region)

► Testing the Blockchain waters with consortium partners or blockchain-based fin-tech startups

► Or just pilot blockchain use cases that do not need ecosystem building – to learn, first

► Leverage existing customer trust and scale, and choose how best to collaborate with Fin-Tech startups – with the attendant work to open up banking APIs for this collaboration and ecosystem expansion

► Leveraging Big Data Science capabilities to providing greater transparency and clearer benefits with our product innovations

► Re-purposing Advanced Analytics APIs for external partners and ecosystems

Thank You Terima Kasih