Embed Size (px)

Citation preview

September 2015 | Tweet @CDSBGlobal

Communicating value creation through natural capital to the mainstreamCDSB Framework for reporting natural capital and environmental information

September 2015 | Tweet @CDSBGlobal

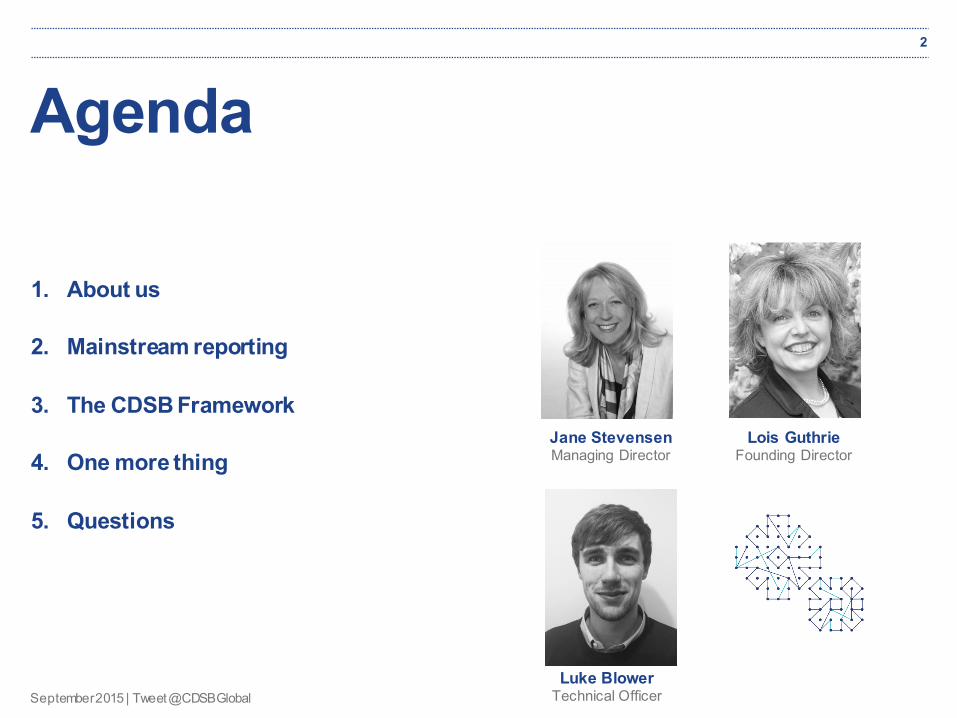

Agenda

1. About us

2. Mainstream reporting

3. The CDSB Framework

4. One more thing

5. Questions

2

Jane StevensenManaging Director

Lois GuthrieFounding Director

Luke BlowerTechnical Officer

September 2015 | Tweet @CDSBGlobal

About us

September 2015 | Tweet @CDSBGlobal

Climate Disclosure Standards Board4

September 2015 | Tweet @CDSBGlobal

We are committed to advancing and aligning the global mainstream corporate reporting model to equate natural capital with financial capital.

September 2015 | Tweet @CDSBGlobal

Mainstream Reporting

September 2015 | Tweet @CDSBGlobal

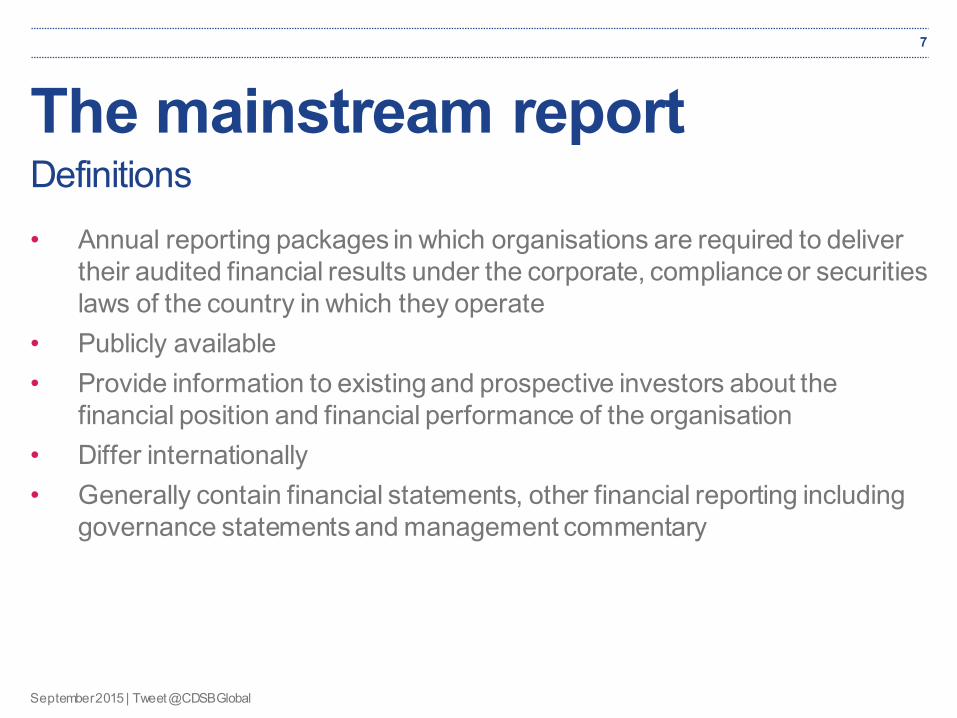

The mainstream report

• Annual reporting packages in which organisations are required to deliver their audited financial results under the corporate, compliance or securities laws of the country in which they operate

• Publicly available• Provide information to existing and prospective investors about the

financial position and financial performance of the organisation• Differ internationally• Generally contain financial statements, other financial reporting including

governance statements and management commentary

7

Definitions

September 2015 | Tweet @CDSBGlobal

The mainstream report

1. Financial statements 2. Governance disclosures3. Management commentary4. Other information

8

Elements

September 2015 | Tweet @CDSBGlobal

9

Influences

And many others…..

The mainstream report

September 2015 | Tweet @CDSBGlobal

The mainstream report10

Language

September 2015 | Tweet @CDSBGlobal

The mainstream report

• Standards • Metrics • Characterisation• Layout • Home

11

Financial reporting Non-financial reporting

• Explosion of mandatory / voluntary reporting provisions

• Confused and complex landscape

• Difficulty understanding what and how to disclose

• National and regional variations• Different audiences – investors,

customers, stakeholders

September 2015 | Tweet @CDSBGlobal

The mainstream report

1. A wide range of factors determine the value of an organisation –readers want to know about the company’s performance so they can assess its value

2. Some of the factors are easy to account for like cash, inventory, land, machinery, buildings

3. Some are not like relationships with suppliers and customers, natural resources etc.

4. A business’ value is determined by all forms of “capital” 5. Investors are beginning to take account of all types of capital in

determining performance – they want to know the full story

12

Why environmental information?

September 2015 | Tweet @CDSBGlobal

The CDSB Framework

September 2015 | Tweet @CDSBGlobal

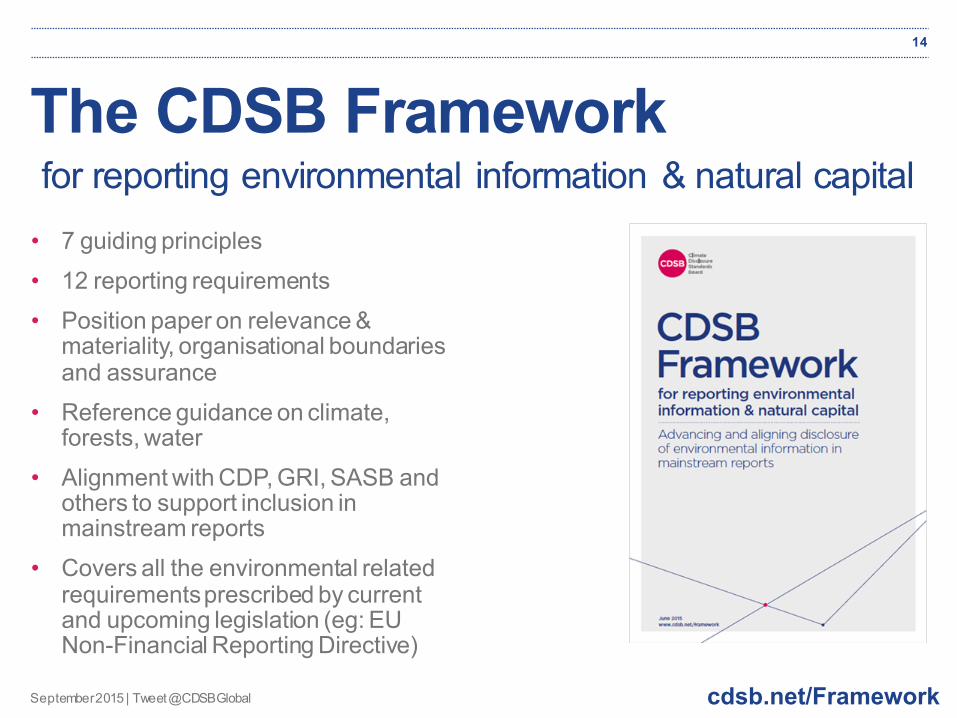

The CDSB Framework

• 7 guiding principles• 12 reporting requirements• Position paper on relevance &

materiality, organisational boundaries and assurance

• Reference guidance on climate, forests, water

• Alignment with CDP, GRI, SASB and others to support inclusion in mainstream reports

• Covers all the environmental related requirements prescribed by current and upcoming legislation (eg: EU Non-Financial Reporting Directive)

for reporting environmental information & natural capital

cdsb.net/Framework

14

September 2015 | Tweet @CDSBGlobal

Objectives of the Framework15

• Align with the objective of financial reporting

• Encourage standardization of environmental & natural capital reporting

• Clear, concise and comparable presentation

• Connect environmental performance with overall strategy, performance and prospects

• Simplify the reporting process

• Support compliance

• Support assurance activities

cdsb.net/Framework

September 2015 | Tweet @CDSBGlobal

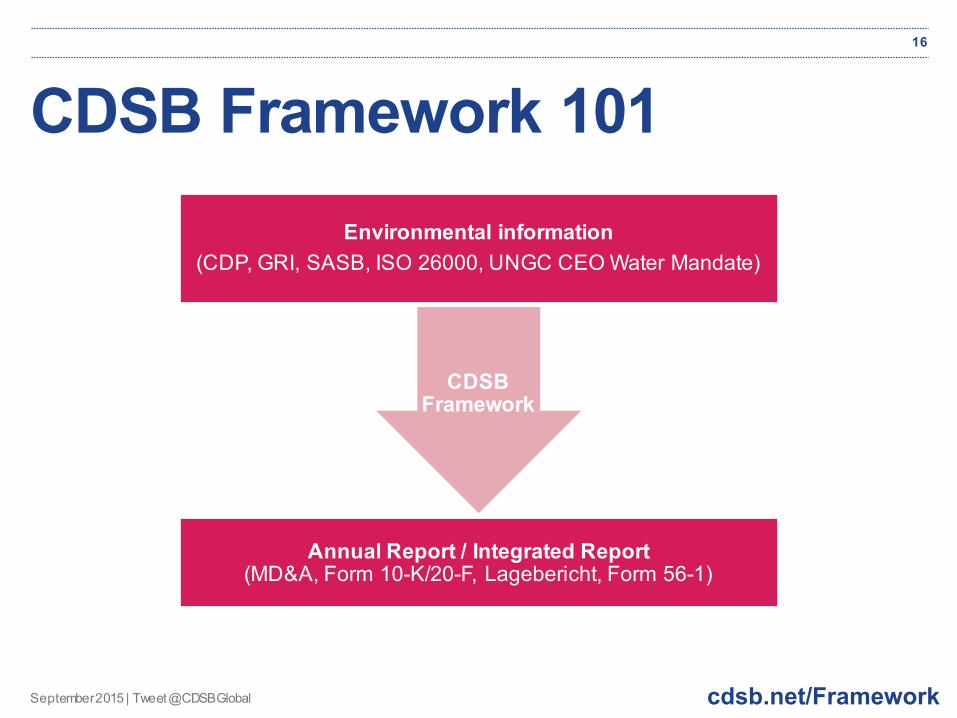

CDSB Framework 10116

Environmental information(CDP, GRI, SASB, ISO 26000, UNGC CEO Water Mandate)

CDSB Framework

Annual Report / Integrated Report(MD&A, Form 10-K/20-F, Lagebericht, Form 56-1)

cdsb.net/Framework

September 2015 | Tweet @CDSBGlobal

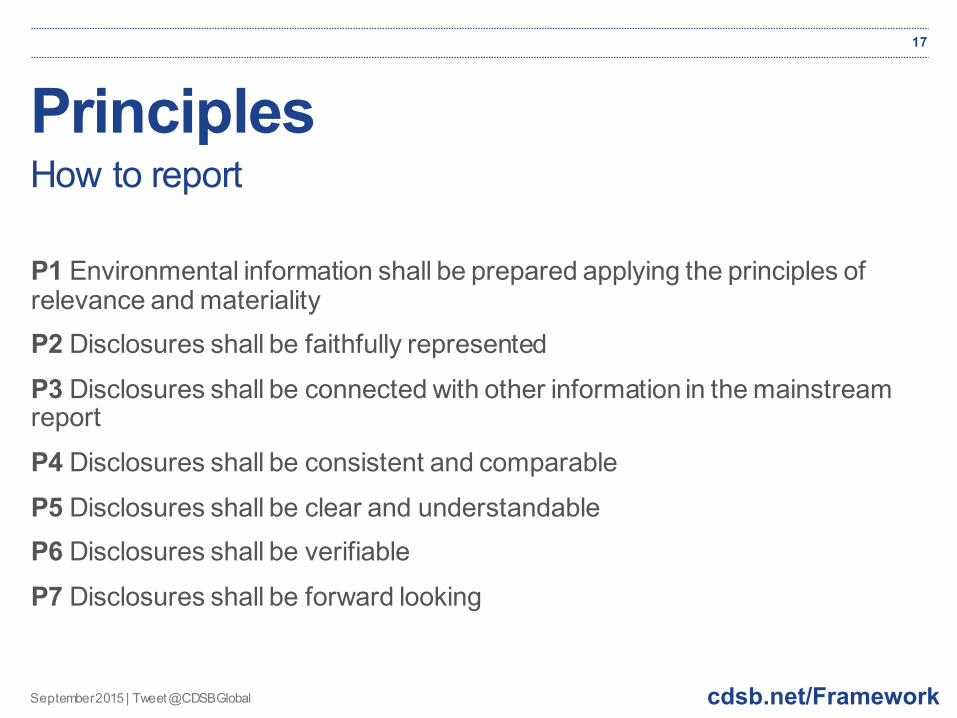

Principles

P1 Environmental information shall be prepared applying the principles of relevance and materialityP2 Disclosures shall be faithfully representedP3 Disclosures shall be connected with other information in the mainstream reportP4 Disclosures shall be consistent and comparableP5 Disclosures shall be clear and understandableP6 Disclosures shall be verifiableP7 Disclosures shall be forward looking

17

How to report

cdsb.net/Framework

September 2015 | Tweet @CDSBGlobal

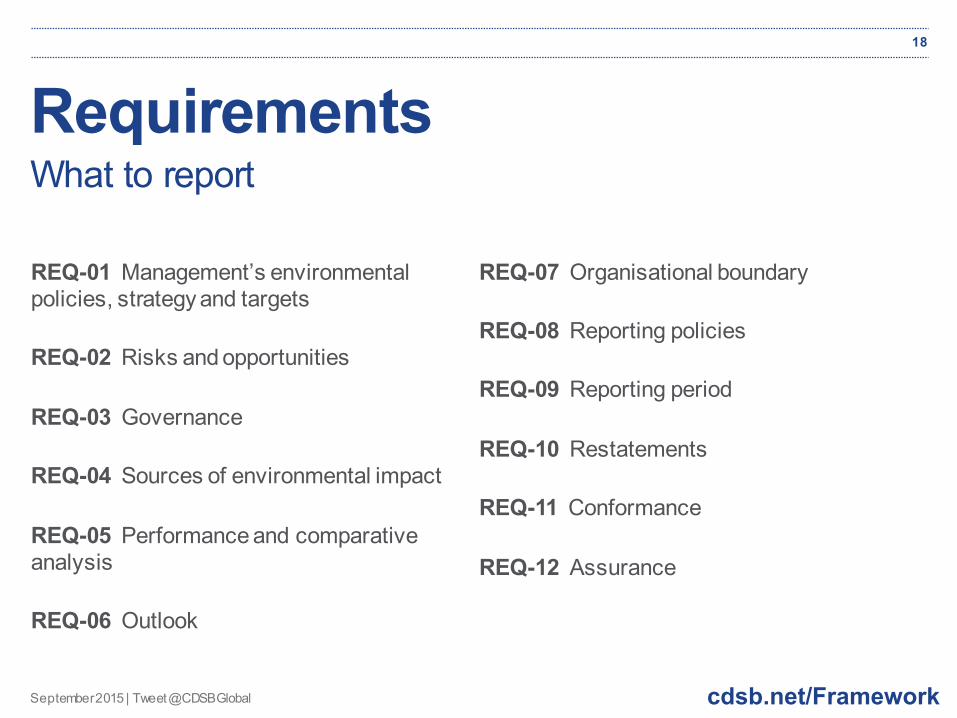

Requirements

REQ-01 Management’s environmental policies, strategy and targets

REQ-02 Risks and opportunities

REQ-03 Governance

REQ-04 Sources of environmental impact

REQ-05 Performance and comparative analysis

REQ-06 Outlook

REQ-07 Organisational boundary

REQ-08 Reporting policies

REQ-09 Reporting period

REQ-10 Restatements

REQ-11 Conformance

REQ-12 Assurance

18

What to report

cdsb.net/Framework

September 2015 | Tweet @CDSBGlobal

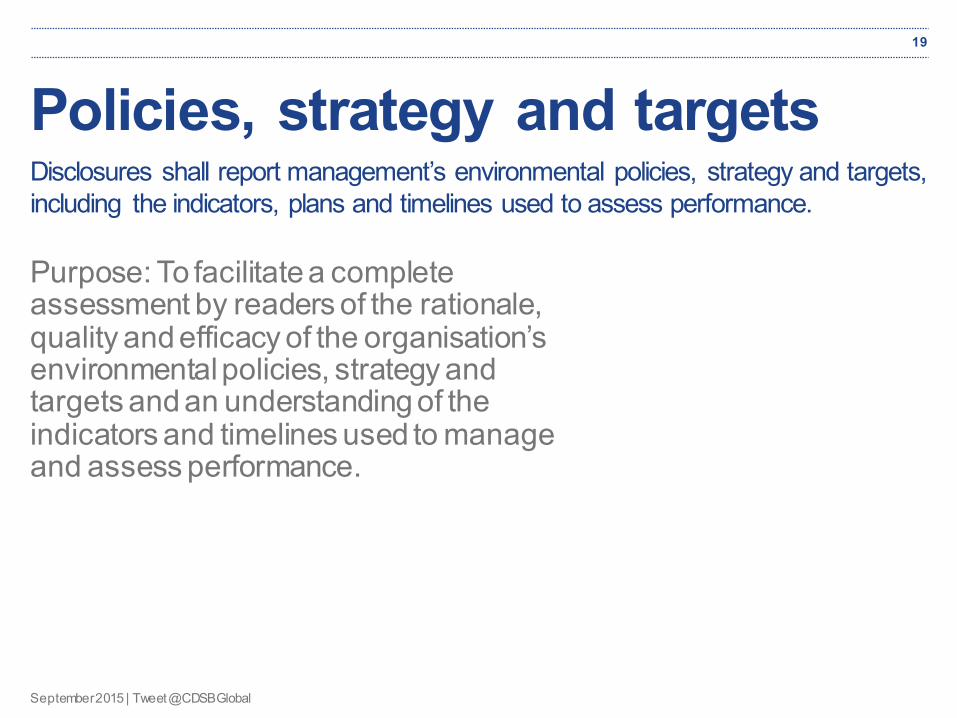

Policies, strategy and targets

Purpose: To facilitate a complete assessment by readers of the rationale, quality and efficacy of the organisation’s environmental policies, strategy and targets and an understanding of the indicators and timelines used to manage and assess performance.

19

Disclosures shall report management’s environmental policies, strategy and targets, including the indicators, plans and timelines used to assess performance.

September 2015 | Tweet @CDSBGlobal

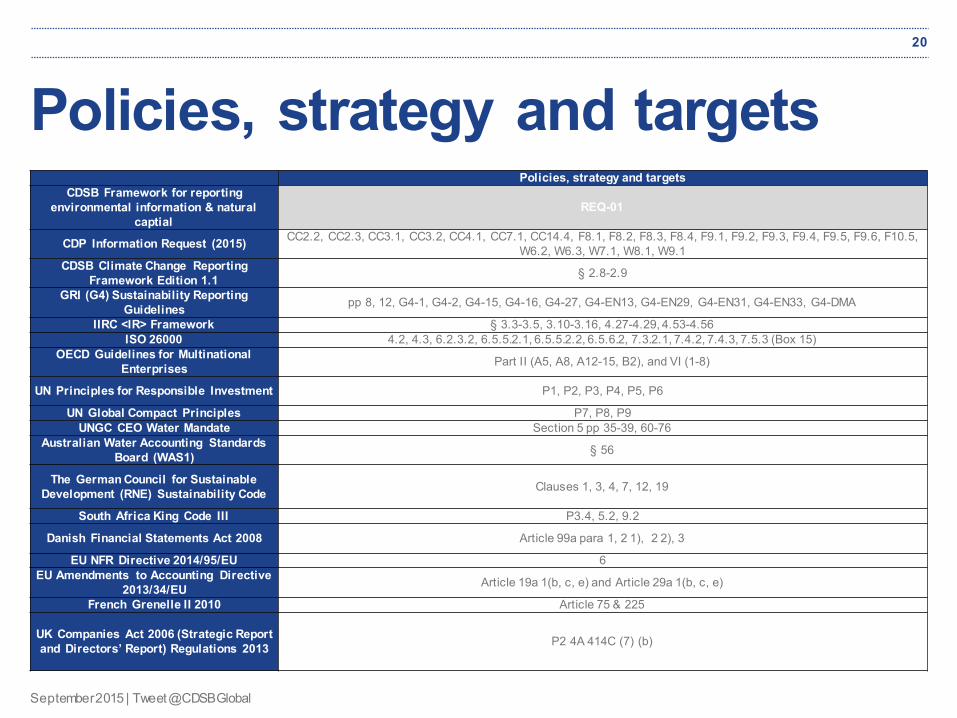

Policies, strategy and targets20

Policies, strategy and targetsCDSB Framework for reporting

environmental information & natural captial

REQ-01

CDP Information Request (2015) CC2.2, CC2.3, CC3.1, CC3.2, CC4.1, CC7.1, CC14.4, F8.1, F8.2, F8.3, F8.4, F9.1, F9.2, F9.3, F9.4, F9.5, F9.6, F10.5, W6.2, W6.3, W7.1, W8.1, W9.1

CDSB Climate Change Reporting Framework Edition 1.1 § 2.8-2.9

GRI (G4) Sustainability Reporting Guidelines pp 8, 12, G4-1, G4-2, G4-15, G4-16, G4-27, G4-EN13, G4-EN29, G4-EN31, G4-EN33, G4-DMA

IIRC <IR> Framework § 3.3-3.5, 3.10-3.16, 4.27-4.29, 4.53-4.56ISO 26000 4.2, 4.3, 6.2.3.2, 6.5.5.2.1, 6.5.5.2.2, 6.5.6.2, 7.3.2.1, 7.4.2, 7.4.3, 7.5.3 (Box 15)

OECD Guidelines for Multinational Enterprises Part II (A5, A8, A12-15, B2), and VI (1-8)

UN Principles for Responsible Investment P1, P2, P3, P4, P5, P6

UN Global Compact Principles P7, P8, P9UNGC CEO Water Mandate Section 5 pp 35-39, 60-76

Australian Water Accounting Standards Board (WAS1) § 56

The German Council for Sustainable Development (RNE) Sustainability Code Clauses 1, 3, 4, 7, 12, 19

South Africa King Code III P3.4, 5.2, 9.2

Danish Financial Statements Act 2008 Article 99a para 1, 2 1), 2 2), 3

EU NFR Directive 2014/95/EU 6EU Amendments to Accounting Directive

2013/34/EU Article 19a 1(b, c, e) and Article 29a 1(b, c, e)

French Grenelle II 2010 Article 75 & 225

UK Companies Act 2006 (Strategic Report and Directors’ Report) Regulations 2013 P2 4A 414C (7) (b)

September 2015 | Tweet @CDSBGlobal

Policies, strategy and targets21

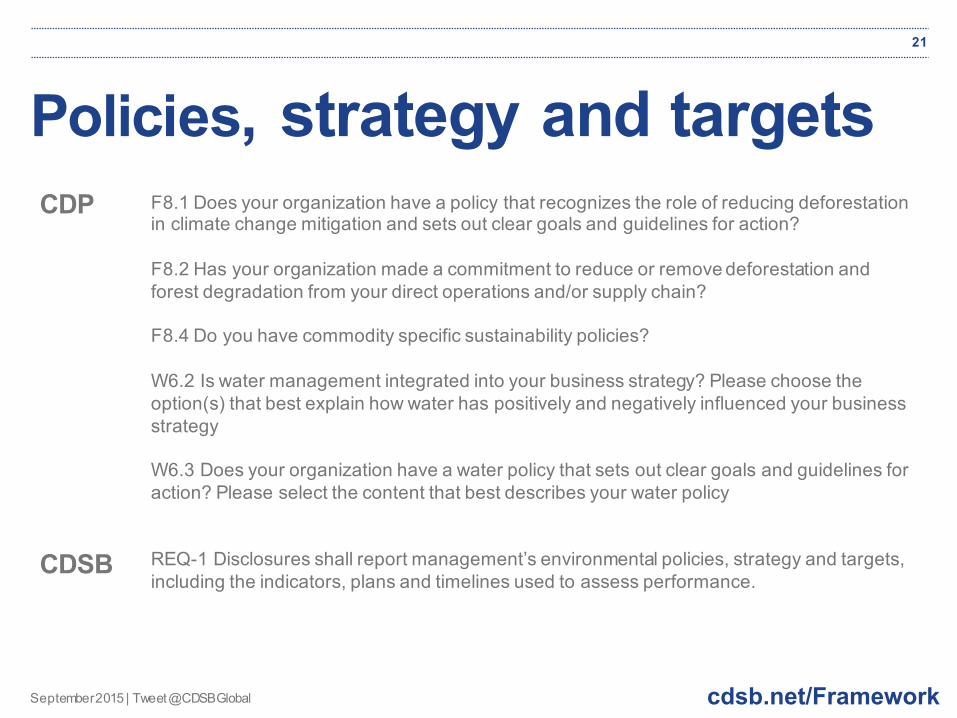

F8.1 Does your organization have a policy that recognizes the role of reducing deforestation in climate change mitigation and sets out clear goals and guidelines for action?

F8.2 Has your organization made a commitment to reduce or remove deforestation and forest degradation from your direct operations and/or supply chain?

F8.4 Do you have commodity specific sustainability policies?

W6.2 Is water management integrated into your business strategy? Please choose the option(s) that best explain how water has positively and negatively influenced your business strategy

W6.3 Does your organization have a water policy that sets out clear goals and guidelines for action? Please select the content that best describes your water policy

REQ-1 Disclosures shall report management’s environmental policies, strategy and targets, including the indicators, plans and timelines used to assess performance.

CDP

CDSB

cdsb.net/Framework

September 2015 | Tweet @CDSBGlobal

Policies, strategy and targets

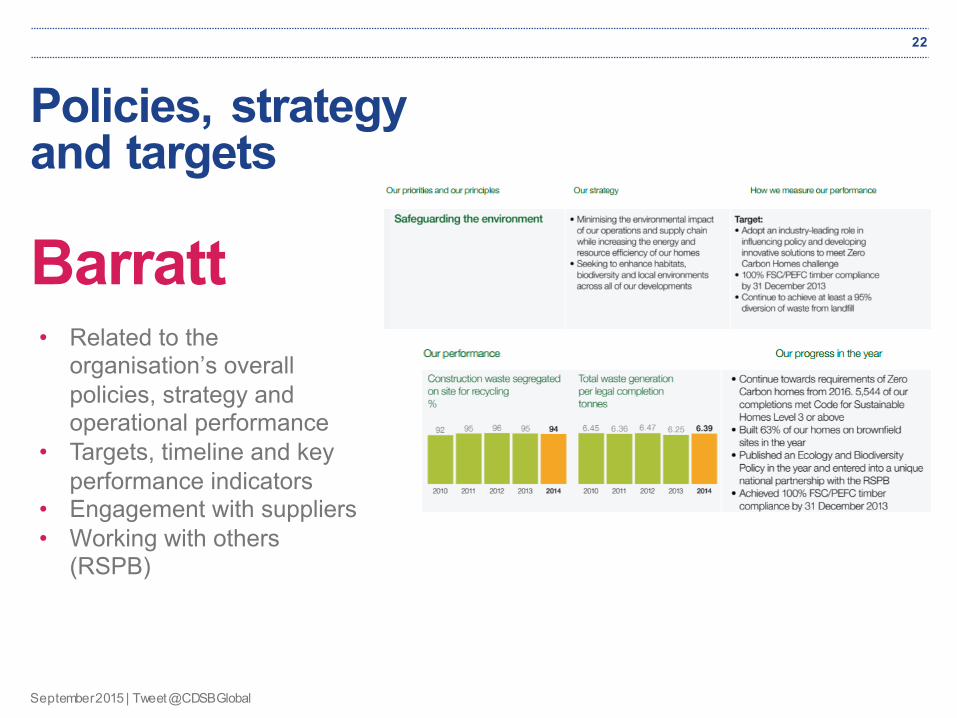

Barratt

22

• Related to the organisation’s overall policies, strategy and operational performance

• Targets, timeline and key performance indicators

• Engagement with suppliers• Working with others

(RSPB)

September 2015 | Tweet @CDSBGlobal

Sources of environmental impacts

Purpose: To report, using qualitative and quantitative results, the degree to which material sources of environmental impact have arisen over the reporting period and to cite methodologies used for the preparation of results. Sources of environmental impact are the activities of and outputs from the organisation that actually or potentially influence or contribute to environmental impacts

23

Quantitative and qualitative results, together with the methodologies used to prepare them, shall be reported to reflect material sources of environmental impact.

September 2015 | Tweet @CDSBGlobal

Environmental impacts

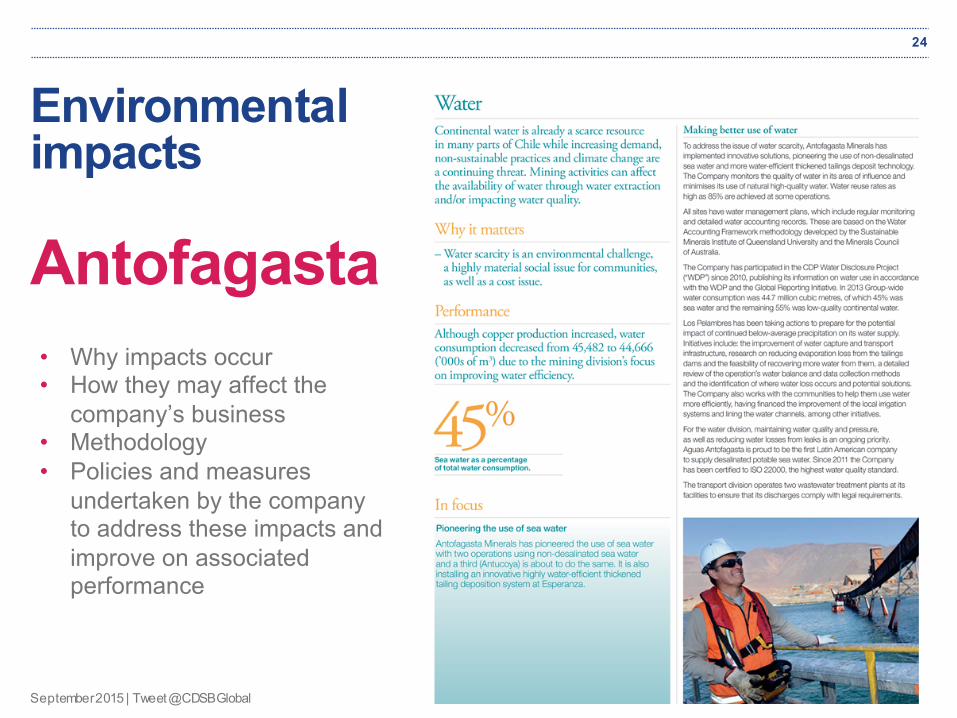

Antofagasta

24

• Why impacts occur• How they may affect the

company’s business• Methodology• Policies and measures

undertaken by the company to address these impacts and improve on associated performance

September 2015 | Tweet @CDSBGlobal

Performance and comparative analysis

Purpose: To communicate to readers how the organisation’s environmental results compare with results for previous reporting periods and with performance targets set in previous periods.

25

Disclosures shall include an analysis of the information disclosed compared with any performance targets set and with results reported in previous periods.

September 2015 | Tweet @CDSBGlobal

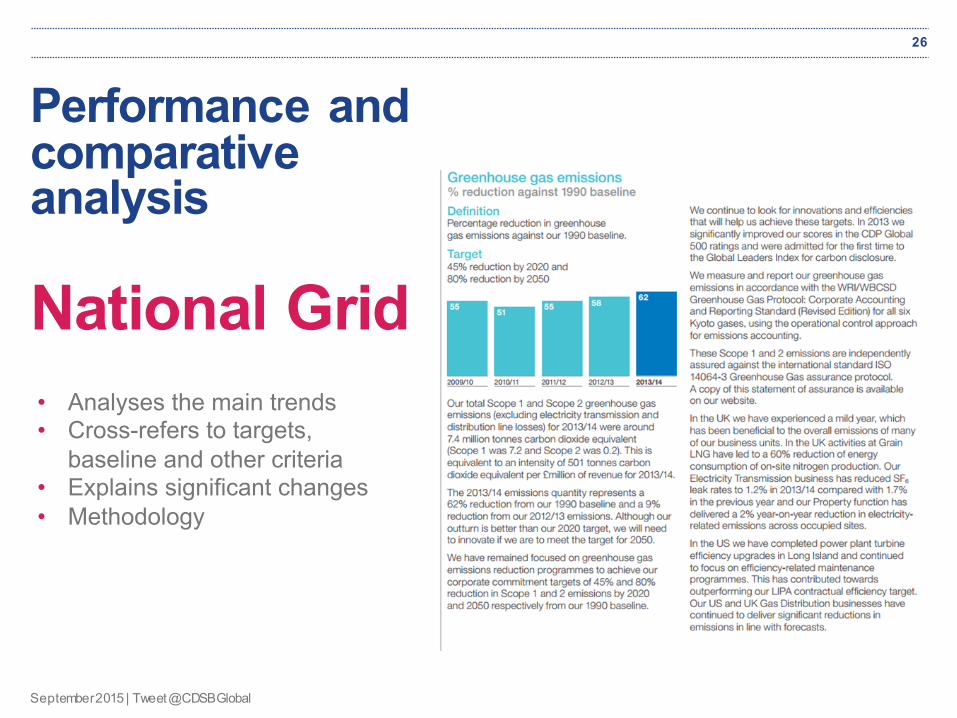

Performance and comparative analysis

National Grid

26

• Analyses the main trends• Cross-refers to targets,

baseline and other criteria• Explains significant changes• Methodology

September 2015 | Tweet @CDSBGlobal

Conformance

Purpose: To inform readers about whether, and to what extent, the principles and requirements of the CDSB Framework have been applied.

27

Disclosures shall include a statement of conformance with the CDSB Framework.

September 2015 | Tweet @CDSBGlobal

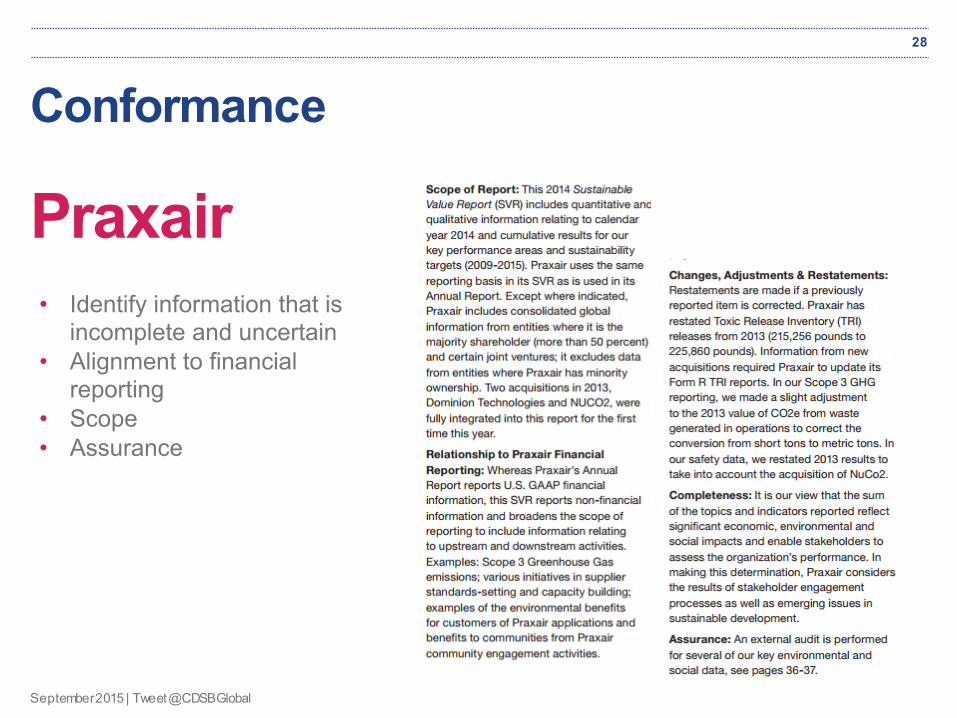

Conformance

Praxair

28

• Identify information that is incomplete and uncertain

• Alignment to financial reporting

• Scope• Assurance

September 2015 | Tweet @CDSBGlobal

One more thing…

September 2015 | Tweet @CDSBGlobal

Be the first

Looking for companies to:• Provide high quality information to your

current and potential investors • Report natural capital in line with

Integrated ReportingCDSB will:• Provide feedback on the company’s

reporting so far to give recommendations on how to improve it further during the project

• Answer questions &provide guidance during the preparation of the report

• Promote report as case study

Get in touch at [email protected].

30

Looking for ambitious companies to showcase the Framework

September 2015 | Tweet @CDSBGlobal

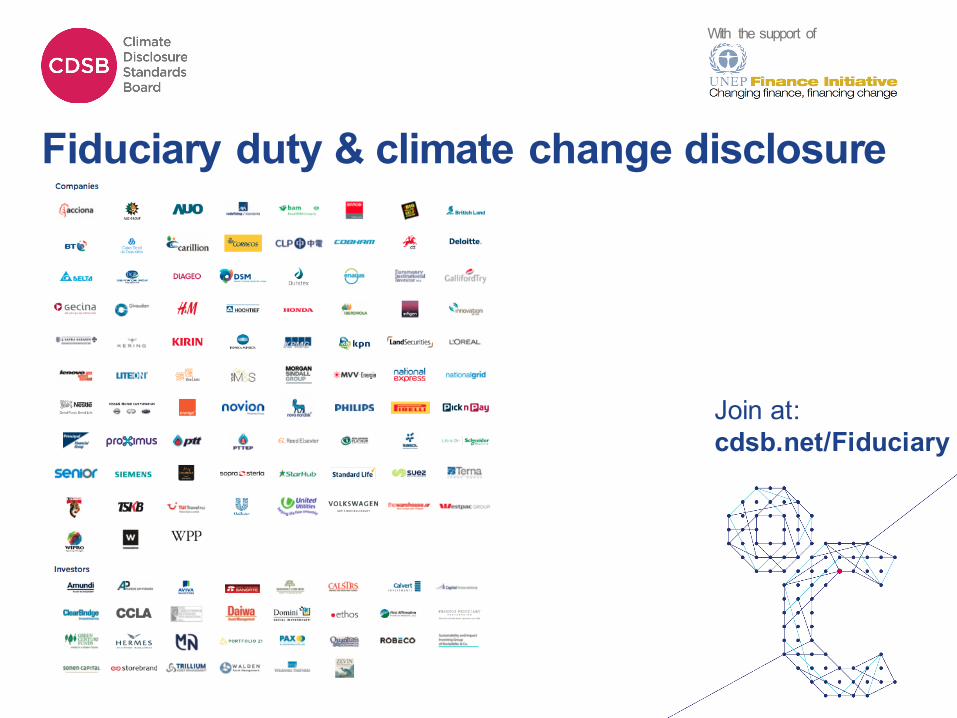

Fiduciary duty & climate change disclosure

With the support of

Join at:cdsb.net/Fiduciary

September 2015 | Tweet @CDSBGlobal

Questions?

- Mainstream reporting

- The CDSB Framework

- Principles

- Requirements

- Fiduciary duty

- Pilot programme

32