Embed Size (px)

Citation preview

A

PROJECT REPORT

On

“Comparatives Study Between Top 5 Mutual Funds offered in Motilal Oswal Securities Ltd.’’

A Dissertation submitted to

(Session 2008-10)Submitted by:

CHITRANJAN I. BIRANWARPGDM, MBA

ROLL NO 8214

Academic Guide : Corporate Guide:Prof.Meghendra Gajpal Ms Sheela Kathane

KOHINOOR BUSINESS SCHOOLKHANDALA

(Affiliated to AICTE and YCMOU University)

1

TABLE OF CONTENTS

Introduction to Mutual Funds 4

Mutual Funds Industry Phases 21

Company Profile 24

Research Methodology 30

Introduction of AMCs 32

Performance Measures of Mutual Funds 36

Limitations of the study 46

Suggestions 47

Conclusion 47

References 49

Annexure 50

2

ACKNOWLEDGMENT “Knowledge is an experience gained in life, it is the choicest

possession, which should not be shelved but should be happily shared with others”.

I express my gratitude to my corporat guide Ms.Sheela Kathane and Faculty guide Pro.Meghendra Gajpal, KOHINOOR BUSINESS SCHOOL for their valuable critiques, assistance and encouragement, which enabled me to carry on the project successfully. They gave me a wonderful opportunity to work on this project. Their time-to-time guidance and incessant support helped me to broaden my outlook on the project I am highly obliged for their support throughout the Training.

I would like to thanks to all for give their valuable inputs and time.

3

Introduction to Mutual Funds:

A Mutual Fund is a trust that pools the savings of a number of investors who share a

common financial goal. The money thus collected is then invested in capital market

instruments such as shares, debentures and other securities. The income earned through

these investments and the capital appreciations realized are shared by its unit holders in

proportion to the number of units owned by them. Thus a Mutual Fund is the most

suitable investment for the common man as it offers an opportunity to invest in a

diversified, professionally managed basket of securities at a relatively low cost.

The flow chart below describes broadly the working of a Mutual Fund.

A Mutual Fund is a body corporate registered with the Securities and Exchange Board

of India (SEBI) that pools up the money from individual/corporate investors and invests

the same on behalf of the investors/unit holders, in Equity shares, Government

securities, Bonds, Call Money Markets etc, and distributes the profits. In the other

words, a Mutual Fund allows investors to indirectly take a position in a basket of assets.

Mutual Fund is a mechanism for pooling the resources by issuing units to the investors

and investing funds in securities in accordance with objectives as disclosed in offer

4

document. Investments in securities are spread among a wide cross-section of industries

and sectors thus the risk is reduced. Diversification reduces the risk because all stocks

may not move in the same direction in the same proportion at same time. Investors of

mutual funds are known as unit holders.

The investors in proportion to their investments share the profits or losses. The mutual

funds normally come out with a number of schemes with different investment

objectives which are launched from time to time. A Mutual Fund is required to be

registered with Securities Exchange Board of India (SEBI) which regulates securities

markets before it can collect funds from the public.

ORGANISATION OF A MUTUAL FUND:

There are many entities involved and the diagram below illustrates the organizational

set up of a Mutual Fund:

(For detailed definitions in the above chart refer to annexure 1)

Mutual Funds diversify their risk by holding a portfolio of instead of only one asset.

This is because by holding all your money in just one asset, the entire fortunes of your

portfolio depend on this one asset. By creating a portfolio of a variety of assets, this risk

is substantially reduced.

5

Mutual Fund investments are not totally risk free. In fact, investing in Mutual Funds

contains the same risk as investing in the markets, the only difference being that due to

professional management of funds the controllable risks are substantially reduced. A

very important risk involved in Mutual Fund investments is the market risk. However,

the company specific risks are largely eliminated due to professional fund management.

IMPORTANT CHARACTERISTICS OF A MUTUAL FUND

• A Mutual Fund actually belongs to the investors who have pooled their

Funds. The ownership of the mutual fund is in the hands of the Investors.

• A Mutual Fund is managed by investment professional and other

Service providers, who earns a fee for their services, from the funds.

• The pool of Funds is invested in a portfolio of marketable investments.

• The value of the portfolio is updated every day.

• The investor’s share in the fund is denominated by “units”. The value

of the units changes with change in the portfolio value, every day. The

Value of one unit of investment is called net asset value (NAV).

• The investment portfolio of the mutual fund is created according to The stated

Investment objectives of the Fund.

OBJECTIVES OF A MUTUAL FUND:

• To Provide an opportunity for lower income groups to acquire without

Much difficulty, property in the form of shares.

• To Cater mainly of the need of individual investors, whose means are small?

• To Manage investors portfolio that provides regular income, growth,

Safety, liquidity, tax advantage, professional management and diversification.

6

ADVANTAGES OF MUTUAL FUNDS:

• Reduced Risk.

• Diversified investment.

• Botheration free investment.

• Revolving type of investment (Reinvestment).

• Selection and timings of investment.

• Wide investment opportunities.

• Investments care.

• Tax benefits.

STRUCTURE OF A MUTUAL FUND

Sponsor

Mutual fund

Trustees

ASSET MANAGEMENT COMPANY

Custodian

Registrar

7

INVESTORS PROFILE:

An investor normally prioritizes his investment needs before undertaking an

investment. So different goals will be allocated to different proportions of the total

disposable amount. Investments for specific goals normally find their way into the debt

market as risk reduction is of prime importance, this is the area for the risk-averse

investors and here, Mutual Funds are generally the best option. One can avail of the

benefits of better returns with added benefits of anytime liquidity by investing in open-

ended debt funds at lower risk, this risk of default by any company that one has chosen

to invest in, can be minimized by investing in Mutual Funds as the fund managers

analyze the companies financials more minutely than an individual can do as they have

the expertise to do so.

Moving up the risk spectrum, there are people who would like to take some risk and

invest in equity funds/capital market. However, since their appetite for risk is also

limited, they would rather have some exposure to debt as well. For these investors,

balanced funds provide an easy route of investment, armed with expertise of investment

techniques, they can invest in equity as well as good quality debt thereby reducing risks

and providing the investor with better returns than he could otherwise manage. Since

they can reshuffle their portfolio as per market conditions, they are likely to generate

moderate returns even in pessimistic market conditions.

Next comes the risk takers, risk takers by their nature, would not be averse to investing

in high-risk avenues. Capital markets find their fancy more often than not,

because they have historically generated better returns than any other avenue,

provided, the money was judiciously invested. Though the risk associated is

generally on the higher side of the spectrum, the return-potential compensates for

the risk attached.

8

TYPES OF MUTUAL FUNDS:

1. OPEN-ENDED MUTUAL FUNDS:-

The holders of the shares in the Fund can resell them to the issuing Mutual Fund

company at the time. They receive in turn the net assets value (NAV) of the shares at

the time of re-sale. Such Mutual Fund Companies place their funds in the secondary

securities market. They do not participate in new issue market as do pension funds or

life insurance companies. Thus they influence market price of corporate securities.

Open-end investment companies can sell an unlimited number of Shares and thus keep

going larger. The open-end Mutual Fund Company Buys or sells their shares. These

companies sell new shares NAV plus a Loading or management fees and redeem shares

at NAV.In other words, the target amount and the period both are indefinite in such

funds

2. CLOSED-ENDED MUTUAL FUNDS:-

A closed–end Fund is open for sale to investors for a specific period, after which

further sales are closed. Any further transaction for buying the units or repurchasing

them, Happen in the secondary markets, where closed end Funds are listed. Therefore

new investors buy from the existing investors, and existing investors can liquidate their

units by selling them to other willing buyers. In a closed end Funds, thus the pool of

Funds can technically be kept constant. The asset management company (AMC)

however, can buy out the units from the investors, in the secondary markets, thus

reducing the amount of funds held by outside investors. The price at which units can be

sold or redeemed Depends on the market prices, which are fundamentally linked to the

NAV. Investors in closed end Funds receive either certificates or Depository receipts,

for their holdings in a closed end mutual Fund.

ORGANISATION AND MANAGEMENT OF MUTUAL FUNDS:-

In India Mutual Fund usually formed as trusts, three parties are generally involved viz.

• Settler of the trust or the sponsoring organization.

9

• The trust formed under the Indian trust act, 1982 or the trust company

registered under the Indian companies act, 1956

• Fund mangers or The merchant-banking unit

• Custodians.

MUTUAL FUNDS TRUST:-

Mutual fund trust is created by the sponsors under the Indian trust act, 1982

Which is the main body in the creation of Mutual Fund trust

The main functions of Mutual Fund trust are as follows:

♦ Planning and formulating Mutual Funds schemes.

♦ Seeking SEBI’s approval and authorization to these schemes.

♦ Marketing the schemes for public subscription.

♦ Seeking RBI approval in case NRI’s subscription to Mutual Fund is Invited

♦ Attending to trusteeship function. This function as per guidelines can be

assigned to separately established trust companies too. Trustees are required to

submit a consolidated report six monthly to SEBI to ensure that the guidelines

are fully being complied with trusted are also required to submit an annual

report to the investors in the fund.

FUND MANAGERS (OR) THE ASSES MANAGEMENT COMPANY

(AMC)

AMC has to discharge mainly three functions as under:

I. Taking investment decisions and making investments of the funds through

market dealer/brokers in the secondary market securities or directly in the

primary capital market or money market instruments

II. Realize fund position by taking account of all receivables and realizations,

moving corporate actions involving declaration of dividends,etc to compensate

investors for their investments in units; and

10

III. Maintaining proper accounting and information for pricing the units and arriving

at net asset value (NAV), the information about the listed schemes and the

transactions of units in the secondary market. AMC has to feed back the trustees

about its fund management operations and has to maintain a perfect information

system.

CUSTODIANS OF MUTUAL FUNDS:-

Mutual funds run by the subsidiaries of the nationalized banks had their respective

sponsor banks as custodians like canara bank, SBI, PNB, etc. Foreign banks with

higher degree of automation in handling the securities have assumed the role of

custodians for mutual funds. With the establishment of stock Holding Corporation

of India the work of custodian for mutual funds is now being handled by it for

various mutual funds. Besides, industrial investment trust company acts as sub-

custodian for stock Holding Corporation of India for domestic schemes of UTI,

BOI MF, LIC MF, etc

Fee structure:-

Custodian charges range between 0.15% to 0.20% on the net value of the

customer’s holding for custodian services space is one important factor which has

fixed cost element.

RESPONSIBILITY OF CUSTODIANS: -

♦ Receipt and delivery of securities

♦ Holding of securities.

♦ Collecting income

♦ Holding and processing cost

♦ Corporate actions etc

11

FUNCTIONS OF CUSTODIANS:-

♦ Safe custody

♦ Trade settlement

♦ Corporate action

♦ Transfer agents

RATE OF RETURN ON MUTUAL FUNDS:-

An investor in mutual fund earns return from two sources:

♦ Income from dividend paid by the mutual fund.

♦ Capital gains arising out of selling the units at a price higher than the

acquisition price

Formation and regulations:

1. Mutual funds are to be established in the form of trusts under the Indian trusts

act and are to be operated by separate asset management companies (AMC s)

2. AMC’s shall have a minimum Net worth of Rs. 5 crores;

3. AMC’s and Trustees of Mutual Funds are to be two separate legal entities and

that an AMC or its affiliate cannot act as a manager in any other fund;

4. Mutual funds dealing exclusively with money market instruments are to be

regulated by the Reserve Bank Of India

5. Mutual fund dealing primarily in the capital market and also partly money

market instruments are to be regulated by the Securities Exchange Board Of

India (SEBI)

6. All schemes floated by Mutual funds are to be registered with SEBI

Schemes:-

1. Mutual funds are allowed to start and operate both closed-end and open-end

schemes;

2. Each closed-end schemes must have a Minimum corpus (pooling up) of Rs 20

crore;

12

3. Each open-end scheme must have a Minimum corpus of Rs 50 crore

4. In the case of a Closed –End scheme if the Minimum amount of Rs 20 crore

or 60% of the target amount, which ever is higher is not raised then the entire

subscription has to be refunded to the investors;

5. In the case of an Open-Ended schemes, if the Minimum amount of Rs 50 crore

or 60 percent of the targeted amount, which ever is higher, is no raised then

the entire subscription has to be refunded to the investors.

Investment norms:-

1. No mutual fund, under all its schemes can own more than five percent of any

company’s paid up capital carrying voting rights;

2. No mutual fund, under all its schemes taken together can invest more than 10

percent of its funds in shares or debentures or other instruments of any single

company;

3. No mutual fund, under all its schemes taken together can invest more than 15

percent of its fund in the shares and debentures of any specific industry, except

those schemes which are specifically floated for investment in one or more

specified industries in respect to which a declaration has been made in the offer

letter.

4. No individual scheme of mutual funds can invest more than five percent of its

corpus in any one company’s share;

5. Mutual funds can invest only in transferable securities either in the money or in

the capital market. Privately placed debentures, securitized debt, and other

unquoted debt, and other unquoted debt instruments holding cannot exceed 10

percent in the case of growth funds and 40 percent in the case of income funds.

Distribution:

Mutual funds are required to distribute at least 90 percent of their profits annually in

any given year. Besides these, there are guidelines governing the operations of mutual

funds in dealing with shares and also seeking to ensure greater investor protection

through detailed disclosure and reporting by the mutual funds. SEBI has also been

13

granted with powers to over see the constitution as well as the operations of mutual

funds, including a common advertising code. Besides, SEBI can impose penalties on

Mutual funds after due investigation for their failure to comply with the guidelines.

MUTUAL FUND SCHEME TYPES:

Equity Diversified Schemes

These schemes mainly invest in equity. They seek to achieve long-term capital

appreciation by responding to the dynamically changing Indian economy by moving

across sectors such as Lifestyle, Pharma, Cyclical, Technology, etc.

♦ Sector Schemes

These schemes focus on particular sector as IT, Banking, etc. They seek to generate

long-term capital appreciation by investing in equity and related securities of

companies in that particular sector.

♦ Index Schemes

These schemes aim to provide returns that closely correspond to the return of a

particular stock market index such as BSE Sensex, NSE Nifty, etc. Such schemes invest

in all the stocks comprising the index in approximately the same weightage as they are

given in that index.

♦ Exchange Traded Funds (ETFs)

ETFs invest in stocks underlying a particular stock index like NSE Nifty or BSE

Sensex. They are similar to an index fund with one crucial difference. ETFs are listed

and traded on a stock exchange. In contrast, an index fund is bought and sold by the

fund and its distributors.

♦ Equity Tax Saving Schemes

14

These work on similar lines as diversified equity funds and seek to achieve long-term

capital appreciation by investing in the entire universe of stocks. The only difference

between these funds and equity-diversified funds is that they demand a lock-in of 3

years to gain tax benefits.

♦ Dynamic Funds

These schemes alter their exposure to different asset classes based on the market

scenario. Such funds typically try to book profits when the markets are overvalued and

remain fully invested in equities when the markets are undervalued. This is suitable for

investors who find it difficult to decide when to quit from equity.

♦ Balanced Schemes

These schemes seek to achieve long-term capital appreciation with stability of

investment and current income from a balanced portfolio of high quality equity and

fixed-income securities.

♦ Medium-Term Debt Schemes

These schemes have a portfolio of debt and money market instruments where the

average maturity of the underlying portfolio is in the range of five to seven years.

♦ Short-Term Debt Schemes

These schemes have a portfolio of debt and money market instruments where the

average maturity of the underlying portfolio is in the range of one to two years.

♦ Money Market Debt Schemes

These schemes invest in debt securities of a short-term nature, which generally means

securities of less than one-year maturity. The typical short-term interest-bearing

instruments these funds invest in Treasury Bills, Certificates of Deposit, Commercial

Paper and Inter-Bank Call Money Market.

♦ Medium-Term Gilt Schemes

15

These schemes invest in government securities. The average maturity of the securities

in the scheme is over three years.

♦ Short-Term Gilt Schemes

These schemes invest in government securities. The securities invested in are of short to

medium term maturities.

♦ Floating Rate Funds

They invest in debt securities with floating interest rates, which are generally linked to

some benchmark rate like MIBOR. Floating rate funds have a high relevance when

interest rates are on the rise helping investors to ride the interest rate rise.

♦ Monthly Income Plans (MIPS)

These are basically debt schemes, which make marginal investments in the range of 10-

25% in equity to boost the scheme’s returns. MIP schemes are ideal for investors who

seek slightly higher return that pure long-term debt schemes at marginally higher risk.

DIFFERENT MODES OF RECEIVING THE INCOME EARNED

FROM MUTUAL FUND INVESTMENTS

Mutual Funds offer three methods of receiving income:

♦ Growth Plan

In this plan, dividend is neither declared nor paid out to the investor but is built into the

value of the NAV. In other words, the NAV increases over time due to such incomes

and the investor realizes only the capital appreciation on redemption of his investment.

♦ Income Plan

16

In this plan, dividends are paid-out to the investor. In other words, the NAV only

reflects the capital appreciation or depreciation in market price of the underlying

portfolio.

♦ Dividend Re-investment Plan

In this case, dividend is declared but not paid out to the investor, instead, it is

reinvested back into the scheme at the then prevailing NAV. In other words, the

investor is given additional units and not cash as dividend.

MUTUAL FUND INVESTING STRATEGIES:

1. Systematic Investment Plans (SIPs)

These are best suited for young people who have started their careers and need to build

their wealth. SIPs entail an investor to invest a fixed sum of money at regular intervals

in the Mutual fund scheme the investor has chosen, an investor opting for SIP in xyz

Mutual Fund scheme will need to invest a certain sum on money every

month/quarter/half-year in the scheme.

2. Systematic Withdrawal Plans (SWPs)

These plans are best suited for people nearing retirement. In these plans, an investor

invests in a mutual fund scheme and is allowed to withdraw a fixed sum of money at

regular intervals to take care of his expenses

3. Systematic Transfer Plans (STPs)

They allow the investor to transfer on a periodic basis a specified amount from one

scheme to another within the same fund family – meaning two schemes belonging to

the same mutual fund. A transfer will be treated as redemption of units from the scheme

from which the transfer is made. Such redemption or investment will be at the

applicable NAV. This service allows the investor to manage his investments actively to

achieve his objectives. Many funds do not even charge any transaction fees for his

service – an added advantage for the active investor.

17

ADVANTAGES OF INVESTING TRHOURGH MUTUAL FUNDS :

There are several reasons that can be attributed to the growing popularity and suitability

of Mutual Funds as an investment vehicle especially for retail investors:

.

• DIVERSIFICATION

Diversification is spreading your investment amount over a larger number of

investments in order to reduce risk. For instance, if you have Rs.10,000 to invest in

Information Technology (IT) stocks, this amount will only buy you a handful of

stocks of perhaps one or two companies. A fall in the market price of any of these

company stocks will significantly erode your investment amount instead it makes

sense to invest in an IT sector mutual fund scheme so that your Rs.10,000 is spread

across a larger number of stocks thereby reducing your risk.

• PROFESSIONALS AT WORK

Few investors have the time or expertise to manage their personal investments every

day, to efficiently reinvest interest or dividend income, or to investigate the

thousands of securities available in the financial markets. Fund managers are

professionals and experienced in tracking the finance markets, having access to

extensive research and market information, which enables them to decide which

securities to buy and sell for the fund. For an individual investor like you, this

professionalism is built in when you invest in the Mutual Fund.

• REDUCTION OF TRANSACTION COSTS

While investing directly in securities, all the costs of investing such as brokerage,

custodial services etc. Borne by you are at the highest rates due to small transaction

sizes. However, when going through a fund, you have the benefit of economies of

18

scale; the fund pays lesser costs because of larger volumes, a benefit passed on to its

investors like you.

• EASY ACCESS TO YOUR MONEY

This is one of the most important benefits of a Mutual Fund. Often you hold shares

or bonds that you cannot directly, easily and quickly sell. In such situations, it could

take several days or even longer before you are able to liquidate his Mutual Fund

investment by selling the units to the fund itself and receive his money within 3

working days.

• TRANSPARENCY

The investor gets regular information on the value of his investment in addition to

disclosure on the specific investments made by the fund, the proportion invested in

each class of assets and the fund manager’s investment strategy and outlook.

• SAVING TAXES

Tax saving schemes of Mutual Funds offer investor a tax rebate under section 88 of

the Income Tax Act. Under this section, an investor can invest up to Rs.10,000 per

Financial year in a tax saving scheme. The rate of rebate under this section depends

on the investor’s total income.

• INVESTING IN STOCK MARKET INDEX

Index schemes of mutual funds give you the opportunity of investing in scrips that

make up a particular index in the same proportion of weightage that these scrips

have in the index. Thus, the return on your investment mirrors the movement of the

index.

• INVESTING IN GOVERNMENT SECURITIES

19

Gilt and Money Market Schemes of Mutual Funds also give you the opportunity to

invest in Government Securities and Money Markets (including the inter banking

call money market)

• WELL-REGULATED INDUSTRY

All Mutual Funds are registered with SEBI and they function within the provisions

of strict regulations designed to protect the interests of investors. The operations of

Mutual Funds are regularly monitored by SEBI.

• CONVENIENCE AND FLEXIBILITY

Mutual Funds offer their investors a number of facilities such as inter-fund transfers,

online checking of holding status etc, which direct investments don’t offer.

RISKS ASSOCIATED WITH MUTUAL FUNDS:-

Investing in Mutual Funds, as with any security, does not come without risk. One of the

most basic economic principles is that risk and reward are directly correlated. In other

words, the greater the potential risk the greater the potential return. The types of risk

commonly associated with Mutual Funds are:

1) MARKET RISK

Market risk relates to the market value of a security in the future. Market prices

fluctuate and are susceptible to economic and financial trends, supply and demand, and

many other factors that cannot be precisely predicted or controlled.

2) POLITICAL RISK

Changes in the tax laws, trade regulations, administered prices, etc are some of the

many political factors that create market risk. Although collectively, as citizens, we

have indirect control through the power of our vote individually, as investors, we have

virtually no control.

3) INFLATION RISK

20

Interest rate risk relates to future changes in interest rates. For instance, if an investor

invests in a long-term debt Mutual Fund scheme and interest rates increase, the NAV of

the scheme will fall because the scheme will be end up holding debt offering lower

interest rates.

4) BUSINESS RISK

Business risk is the uncertainty concerning the future existence, stability, and

profitability of the issuer of the security. Business risk is inherent in all business

ventures. The future financial stability of a company cannot be predicted or guaranteed,

nor can the price of its securities. Adverse changes in business circumstances will

reduce the market price of the company’s equity resulting in proportionate fall in the

NAV of the Mutual Fund scheme, which has invested in the equity of such a company.

5) ECONOMIC RISK

Economic risk involves uncertainty in the economy, which, in turn, can have an adverse

effect on a company’s business. For instance, if monsoons fail in a year, equity stocks

of agriculture-based companies will fall and NAVs of Mutual Funds, which have

invested in such stocks, will fall proportionately.

MUTUAL FUND INDUSTRY PHASES

The Mutual Fund industry in India started in 1963 with the formation of Unit Trust of

India, at the initiative of the Government of India and Reserve Bank of India. The

History of Mutual Funds in India can be broadly divided into four distinct phases.

• First Phase –(1964-87)

Unit Trust of India (UTI) was established on 1963 by an act of parliament. It was set up

by Reserve Bank of India and functioned under the regulatory and administrative

control of the Reserve Bank of India. In 1978 UTI was de-linked from the RBI and the

Industrial Development Bank of India (IDBI) took over the regulatory and

administrative control in place of RBI. The first scheme launched by UTI was Unit

21

Scheme 1964. At the end of 1988 UTI had Rs.6,700 crores of assets under

management.

• Second Phase - 1987-1993(Entry of Public Sector Funds)

1987 marked the entry of non-UTI, Public Sector Mutual Funds set up by Public Sector

Banks and Life Insurance Corporation of India (LIC) and General Insurance

Corporation of India (GIC). SBI Mutual Fund was the first non -UTI Mutual Fund

established in June 1987 followed by Canbank Mutual Fund (Dec 87), Punjab National

Bank Mutual Fund (Aug 89), Indian Bank Mutual Fund (Nov 89), Bank of India (Jun

90), Bank of Baroda Mutual Fund (Oct 92). LIC established its Mutual Fund in June

1989 while GIC had set up its Mutual Fund in June 1989 while GIC had set up its

Mutual Fund in December 1990.

At the end of 1993, the Mutual Fund industry had assets under management of

Rs.47,004 crores.

• Third Phase -1993-2003 (Entry of Private Sector funds)

With the entry of private sector funds in 1993, a new era started in the Indian Mutual

Fund industry, giving the Indian investors a wider choice of fund families. Also, 1993

was the year in which the first Mutual Fund Regulations came into being, under which

all Mutual Funds, except UTI were to be registered and governed. The erstwhile

Kothari pioneer (now merged with UTI were to be registered and governed. The

erstwhile Kothari pioneer (now merged with Franklin Templeton) was the first Private

Sector Mutual Fund registered in July 1993.

22

The 1993 SEBI (Mutual Fund) regulations were substituted by a more comprehensive

and revised Mutual Fund Regulations in 1996. The industry now functions under the

SEBI (Mutual Fund) regulations 1996.

The number of Mutual Fund houses went on increasing, with many foreign Mutual

Funds setting up funds in India and also the industry has witnessed several mergers and

acquisitions. As at the end of January 2003, there were 33 Mutual Funds with total

assets of Rs.1,21,805 Crores. The Unit Trust of India with Rs.44,541 crores of assets

under management was way ahead of other Mutual Funds.

• Fourth Phase –(since February 2003)

In February 2003, following the repeal of the Unit Trust of India Act 1963. UTI was

bifurcated into two separate entities. One is the specified Undertaking of the Unit Trust

of India with assets under management of Rs.29,835 crores As at the end of January

2003, representing broadly, the assets of US 64 scheme, assured return and certain other

schemes. The specified Undertaking of Unit Trust of India, functioning under an

administrator and under the rules framed by Government of India and does not come

under the purview of the Mutual Fund Regulations.

The second is the UTI Mutual Fund Ltd, sponsored by SBI, PNB, BOB and LIC. It is

registered with SEBI and functions under the Mutual Fund Regulations. With the

bifurcation of the erstwhile.

UTI which had in March 2000 more than Rs. 76,000crores of assets under management

and with the setting up of a UTI Mutual Fund, confirming to the SEBI Mutual Fund

Regulations, and with recent mergers taking place among different private sector funds,

the Mutual Fund industry has entered its current phase of consolidation and growth. As

at the end of October 31, 2003, there were 31 funds, which manage assets of Rs.1,

26,726crores under 386 schemes.

23

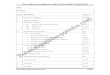

GROWTH IN ASSETS UNDER MANAGEMENT

24

COMPANY PROFILE

Company Profile of Motilal Oswal

Motilal Oswal Securities Ltd. (MOSL) is a leading

research and advisory based stock broking house of India, with a dominant position in

both institutional equities and wealth management. Motilal Oswal Financial Services is a

well diversified financial services group having businesses in securities, commodities,

investment banking and venture capital. With 1300 business locations and more than

3,85,000 customers in over 425 cities, Motilal Oswal is well suited to handle all your

wealth creation and wealth management needs. The company has in the last year placed

9.48% with two leading private equity investors - New Vernon Private Equity Limited

and Bessemer Venture Partners at post money company valuation of Rs. 1345 crore.

25

The organization finds its strength in its team of young, talented and confident

individuals. Qualified professionals carry out different functions under the able

leadership of its promoters, Mr. Motilal Oswal and Mr. Raamdeo Agrawal. Stringent

employee selection process, focus on continuous training and adoption of best

management practices drive the quest to achieving our Core Purpose and Values.

The Team of Motilal Oswal provides full fledged support to client's through

• Deal Advisory

• Valuation support

• Due diligence

• Implementation support

The Approach is characterized by High quality financial advice resulting in

outstanding execution through:

• Understanding client's businesses and needs and associated risk implications

• Adding value in valuation assumptions, structuring, negotiating, and

• Long term commitment and strong relationships

26

Research is the solid foundation on which Motilal Oswal Securities advice is based. Almost 10% of

revenue is invested on equity research and we hire and train the best resources to become advisors. At

present we have 24 equity analysts researching over 26 sectors. From a fundamental, technical and

derivatives research perspective; Motilal Oswal's research reports have received wide coverage in the

media (over a 1000 mentions last year).Motilal Oswal Securities has witnessed rapid organic growth

due to favorable market conditions as well as efforts put in by the company itself.

Board Of Directors

Chairman and Managing Director:- Motilal Oswal

Non-Executive Director:-Ramdeo Agrawal

Non-Executive Director:-Navin Agrawal

27

There are 8 products of Motilal Oswal’s and they are:

1) Equities:- Equity Research is an inherent strength of MOSL. They believe in picking investment

horizon, life stage, and return expectation and investment objectives. These are the some of the ways

through which they give suggestions to their clients and they are:-

a)Client profiling:- Profiling takes into consideration issues like your attitude towards risk, investment

horizon, life stage, and return expectation and investment objectives.

b) Investments & Trading:- MOSL Equity Advisor are experts in providing value based investment

solutions as well as advising you in positional trading, as per your profile.

c) Portfolio Tracking Software:- Your equity portfolio is continuously monitored using portfolio

tracking software.

d) Integrated Approach:- In this there is a combination of cash, derivatives and other leverage

products to help to reach investment goals.

e) Minimum requirements and fees structure:-portfolio size should be 2 lakh plus and fees structure

varies from case to case.

2) Derivatives:-Derivatives instrument provide good leverage opportunity, it is a great tool for

speculation. Their equity advisor will help to maximize your gains from existing corpus.

3) Online trading(e-Broking):- My broker is a single-screen cash and derivatives terminal with online

research-based advice. During the day they will send our Intra-day and delivery calls to help you to

take informed investment decisions.

4)IPO:-Book building and Fixed Price issue are the two types of Initial Public Offerings(IPO) through

which corporate can raise money in the capital market.

Book building public issue the bids are received at different price levels and the demand for the issue is

built up over a period of time. Fixed price issue the issue price is pre ascertained by the issuer.

28

5) Portfolio Management Services:- MOSt PMS help to earn the returns of equities, with maximum

ease and comfort. They offer different approaches to managing your investments.

• Value Portfolio

• Bull’s Eye portfolio

• Next Trillion Dollar Opportunity portfolio

6) Mutual Funds:-It is one of the safest, easiest and convenient ways of successful investment making.

Services offered:-

a) Need based advisory fully backed with solid research.

b) Dedicated mutual fund advisors to understand your needs and building a prudent portfolio.

c) Monthly review of portfolios.

d)monthly fact-sheet covering our analysis of various funds.

e)Knowledge sharing through educational seminars and workshops.

7) Commodities:-Motilal oswal commodities Broker Private Limited (MOCB) offers you an excellent

opportunity to take calls on the movement of prices of commodities traded commodities are global in

nature, les volatile and as liquid as equities thereby allowing you to achieve portfolio diversification.

Tradable Commodities

Precious Metals (Gold, Silver)

Base Metals (Copper and Zinc)

Energy (Crude Oil and Natural Gas)

Grains (Wheat)

Spices (Red Chilli, Cardamom, Jeera, Black Pepper, Turmeric)

Pulses (Chana, Urad, Tur)

Oil Ref. Soya Oil, Mentha Oil, RBD Palm Olien

Others Gaur Seed, Potato, Sugar, Maize, Castor seed, Gaur gum

29

8) Depository Services:-MOSL Depository offers MODES-a DEMAT account linked to the MOSt

Trading account. In the times of T+2 having a demat account linked to your trading account becomes

very convenient.

MOSt efficient centralized depository assures you receive innovative value added reports with

sectorised portfolio break-up and an efficient service at all times (online as well as offline). MOSt is a

member of both NSDL and CDSL and the service is available at all our outlets in India. Non-trading

members also can avail of MODES.

PERFORMANCE MEASURES OF MUTUAL FUNDS:

The most important and widely used measures of performance are:

• NAV Trends

• Funds fact

• Returns

• Risk

• Portfolio Structure

RESEARCH METHODOLOGY

The Methodology involves randomly selecting Open-Ended equity diversified schemes

of different fund houses of the country. The data collected for this project is basically

from two sources, they are:-

1. Primary sources: The monthly fact sheets of different fund houses and research

reports from banks.

2. Secondary sources: Collection of data from Internet and Books.

30

HYPOTHESIS

The Hypothesis of the study involves Comparison between following mutual funds that

we offered in motilal oswal securities ltd. Nagpur

1. SBI Magnum Global Fund-94

2. Reliance Growth Fund

3. Birla SunLife Equity Fund

4. HDFC Top-200

5. ICICI Prudential Dynamic Plan-Growth

NEED OF THE STUDY:

The project’s idea is to project Mutual Fund as a better avenue for investment on a

long-term or short-term basis. Mutual Fund is a productive package for a lay-investor

with limited finances, this project creates an awareness that the Mutual Fund is a

worthy investment practice. Mutual Fund is a globally proven instrument.

The driving force of Mutual Funds is the ‘safety of the principal’ guaranteed, plus the

added advantage of capital appreciation together with the income earned in the form of

interest or dividend. The various schemes of Mutual Funds provide the investor with a

wide range of investment options according to his risk bearing capacities and interest

besides; they also give handy return to the investor. Mutual Funds offers an investor to

invest even a small amount of money, each Mutual Fund has a defined investment

objective and strategy. Mutual Funds schemes are managed by respective asset

managed companies sponsored by financial institutions, banks, private companies or

international firms. A Mutual Fund is the ideal investment vehicle for today’s complex

and modern financial scenario.

The study is basically made to analyze the various open-ended equity diversifies

schemes of different Asset Management Companies to highlight the diversity of

investment that Mutual Fund offer. Thus, through the study one would understand how

31

a common man could fruitfully convert a pittance into great penny by wisely investing

into the right scheme according to his risk taking abilities.

SCOPE:

The study here has been limited to analyse open-ended equity diversified Growth

schemes of different Asset Management Companies namely SBI Mutual Fund,

Reliance Mutual Fund, HDFC Mutual Fund, Birla Mutual Fund, ICICI Mutual

Fund are analysed according to its performance against the other, based on factors like

NAV Trend, Sharpe’s Ratio, Treynor’s Ratio, β (Beta) Co-efficient, Returns

Portfolio structure.

OBJECTIVES:

1. To project Mutual Fund as the ‘productive avenue’ for investing activities.

2. To show the wide range of investment options available in Mutual Funds by

explaining its various schemes.

3. To compare the schemes based on different parameters and show which

scheme is best for the investor based on his risk profile.

4. To help an investor make a right choice of investment, while considering the

inherent risk factors.

5. To understand the recent trends in Mutual Funds world.

The comparison between these schemes is made based on the following factors.

A) NAV(Net asset value)

B) Fund fact

C) Portfolio structure

Portfolio attributes

Style box

32

Sector allocation

Assets allocation

D) Returns

E) Risk

Sharpe’s Ratio

Treynor’s Ratio

Fama model

β (Beta) co-efficient.

INTRODUCTION OF ASSET MANAGEMENT COMPANIES

33

HDFC Asset Management Company Limited (AMC)

HDFC Asset Management Company Ltd (AMC) was incorporated under the Companies Act, 1956, on December 10, 1999, and was approved to act as an Asset Management Company for the HDFC Mutual Fund by SEBI vide its letter dated July 3, 2000.The registered office of the AMC is situated at Ramon House, 3rd Floor, H.T. Parekh Marg, 169, Backbay Reclamation, Churchgate, Mumbai - 400 020. In terms of the Investment Management Agreement, the Trustee has appointed the HDFC Asset Management Company Limited to manage the Mutual Fund. The paid up capital of the AMC is Rs. 25.161 crore.

Reliance Capital Assets Management Ltd

34

Reliance Mutual Fund (RMF) is one of India’s leading Mutual Funds, with Average Assets Under Management (AAUM) of Rs. 1,02,730 Crs (AAUM for 31st May 09 ) and an investor base of over 71.30 Lacs.

"Reliance Mutual Fund schemes are managed by Reliance Capital Asset Management Limited

Reliance Capital Ltd. is one of India’s leading and fastest growing private sector financial services companies, and ranks among the top 3 private sector financial services and banking companies, in terms of net worth. Reliance Capital Ltd. has interests in asset management, life and general insurance, private equity and proprietary investments, stock broking and other financial services.

Sponsor : Reliance Capital Limited.

Trustee : Reliance Capital Trustee Co. Limited.

Investment Manager : Reliance Capital Asset Management Limited

ICICI Prudential Asset Management Company

ICICI Prudential Asset Management Company enjoys the strong parentage of Prudential plc, one of UK's largest players in the insurance & fund management sectors and ICICI Bank, a well-known and trusted name in financial services in India. ICICI Prudential Asset Management Company, in a span of just over eight years, has forged a position of pre-eminence in the Indian Mutual Fund industry as one of the largest asset management companies in the country with average assets under management of Rs. 65,576.64 Crore (as of May 31, 2009). The Company manages a comprehensive range of schemes to meet the varying investment needs of its investors spread across 230 cities in the country.

Birla Sun Life Asset Management Company

35

Birla Sun Life Asset Management Company Ltd. (BSLAMC), the investment managers of Birla Sun Life Mutual Fund, is a joint venture between the Aditya Birla Group and the Sun Life Financial Services Inc. of Canada. The joint venture brings together the Aditya Birla Group's experience in the Indian market and Sun Life's global experience.

Since its inception in 1994, Birla Sun Life Mutual fund has emerged as one of India's leading Mutual Funds managing assets of a large investor base. The fund offers a range of investment options, which include diversified and sector specific equity schemes, fund of fund schemes, hybrid and monthly income funds, a wide range of debt and treasury products and offshore funds.

SBI Mutual Fund (SBI MF) is one of the largest mutual funds in the country with an investor base of over 5.4 million. With over 20 years of rich experience in fund management, SBI MF brings forward its expertise in consistently delivering value to its investors.

SBI MF draws its strength from India's Largest Bank State Bank of India

Scheme objectives

HDFC TOP 200-growth

To generate long term capital appreciation from a portfolio of equity and equity-linked instruments primarily drawn from the companies in BSE 200 index.

Reliance Growth-Growth

The primary investment objective of the Scheme is to achieve long-term growth of capital by investment in equity and equity related securities through a research based investment approach.

ICICI Prudential Dynamic plan-growth

lCICI Prudential Dynamic Plan is a diversified equity fund that could be your ideal choice to make the most of dynamic changes in the market. It has the ability to capture

36

upside opportunities across value and growth, large and midcap , index and non-index stocks. On the flip side it also has ability to move into cash as markets get overvalued.

Birla Sun life Equity Fund-growth

Birla Sun Life Equity Fund is a diversified equity fund enabling investors to capitalize on the immense growth opportunities provided by the stock market while at the same time minimizing the risk.

SBI Magnum Global Fund 94 – Growth

To provide the investors maximum growth opportunity through well researched investments in Indian equities, PCDs and FCDs from selected industries with high growth potential and Bonds.

Comparative study of Mutual funds based on different parameter:-(Data are taken up to 8th June 2009)

NAV of Mutual funds:-

HDFC TOP 200-growth 140.26 (13yrs)Reliance Growth-Growth 327.38 (12yrs)ICICI Prudential Dynamic plan-growth 69.31 (7yrs)Birla Sun life Equity Fund-growth 195.66 (11yrs)SBI Magnum Global Fund 94 – Growth 35.97 (15yrs)

Funds facts:-

Schemes Type of

Scheme

Inception

Date

Fund Size

in Rs. Cr.

Expense

ratio(%)

Portfolio

Turnover

Ratio(%)

HDFC TOP 200-growth Open

Ended

Sep 11,

1996

3314.58 1.89 81.41

Reliance Growth-Growth Open Oct 8, 5235.33 1.83 108

37

Ended 1995ICICI Prudential Dynamic plan-

growth

Open

Ended

Oct 31,

2002

1461.43 2.00 168

Birla Sun life Equity Fund-growth Open

Ended

Aug 27,

1998

950.91 2.16 188

SBI Magnum Global Fund 94 –

Growth

Open

Ended

Sep 30,

1994

1116.9

5

2.15 43

Expense Ratio:-

Expense Ratio is defined as the ratio of expenses incurred by a scheme to its Average Weekly Net Assets. It means how much of investors money is going for expenses and how much is getting invested. This ratio should be as low as possible.

Portfolio Turnover:-

Portfolio Turnover is the ratio which helps us to find how aggressively the portfolio is being churned. If the fund manager churns the entire portfolio twice in a single year then we would say that the Portfolio Turnover rate is 200% or that the portfolio is churned once every 6 months.

PORTFOLIO:-

a)Portfolio attributes:

Scheme name P/E Dividend

Yield

Market Cap (Rs.

in crores)

No. of

StocksHDFC TOP 200-growth 16.75 as on

Apr – 2009

1.72 as on

Apr – 2009

52,404.75 as

on Apr - 2009

67

Reliance Growth-Growth 18.93 as on

Apr - 2009

1.52 as on

Apr – 2009

40,905.50 as

on Apr - 2009

30

ICICI Prudential Dynamic plan-

growth

16.83 as on

Apr - 2009

1.53 as on

Apr – 2009

58,697.44 as

on Apr - 2009

48

Birla Sun life Equity Fund-growth 18.07 as on

Apr - 2009

1.56 as on

Apr – 2009

74,636.62 as

on Apr - 2009

51

SBI Magnum Global Fund 94 –

Growth

11.84 as on

Apr - 2009

1.91 as on

Apr – 2009

4,135.62 as on

Apr – 2009

60

38

P/ E Ratio:-

P/ E Ratio stands for Price Earnings Ratio. It is also known as Price Earnings multiple. This is a ratio of the current market price (CMP) of a share to its earning per share (EPS).

A fund which invests in stocks based upon their P/E ratios. Thus when a stock is trading at a historically low P/E multiple, the fund will buy the stock, and when the P/E ratio is at the upper end of the band, the scheme will sell.

Style box:

HDFC TOP 200-growth

Reliance Growth-Growth

ICICI Prudential Dynamic plan-growth

Birla Sun life Equity Fund-growth

39

SBI Magnum Global Fund 94 – Growth

The idea is to classify funds based on both the size of the companies invested in and the

investment style of the manager.

The term “Value” refers to a style of investing that looks for high quality companies that

are out of favor with the market.

These companies are characterized by low P/E ratios, price-to-book ratios, and high

dividend yields, etc. the opposite of value is “Growth’’, which refers to companies that

have had (and are expected to continue to have) strong growth in earnings, sales, and

cash flow, etc.

A compromise between value and growth is “Blend,” which simply refers to companies

that are neither value nor growth stocks and so are classified as being somewhere in the

middle.

For example, a mutual fund that invests in large-cap companies who are in strong

financial shape but have recently seen their share price fall would be placed in the upper

left quadrant of the style box (large and value). The opposite of this would be a fund that

invests in startup technology companies with excellent growth prospects. Such a mutual

fund would reside in the bottom right quadrant

Sector allocation:-

HDFC TOP 200-

growth

Reliance

Growth-Growth

ICICI Prudential

Dynamic plan-

growth

Birla Sun life

Equity Fund-

growth

SBI Magnum

Global Fund 94 –

Growth

40

Auto & Auto

ancillaries 4.47

Banks 20.96

Cement 0.42

Computers -

Software &

Education 9.72

Consumer

Durables 3.75

Current Assets

3.06

Diversified 1.75

Electricals &

Electrical

Equipments 6.38

Electronics 0.15

Engineering &

Industrial

Machinery 1.76

Entertainment 1.79

Fertilizers,

Pesticides &

Agrochemicals

1.07

Finance 6.20

Food & Dairy

Products 2.69

Housing &

Construction 5.45

Metals 0.38

Oil & Gas,

Petroleum &

Refinery 10.49

Paints 0.15

Auto & Auto

ancillaries 1.89

Banks 10.34

Breweries &

Distilleries 1.22

Chemicals 1.32

Computers -

Software &

Education 6.16

Current Assets

17.45

Electricals &

Electrical

Equipments

1.19

Engineering &

Industrial

Machinery 1.66

Fertilizers,

Pesticides &

Agrochemicals

3.18

Finance 1.39

Food & Dairy

Products 1.14

Housing &

Construction

3.42

Mining &

Minerals 1.51

Miscellaneous

14.64

Oil & Gas,

Petroleum &

Auto & Auto

ancillaries 2.94

Banks 9.05

Cement 0.88

Chemicals 1.85

Computers -

Software &

Education 12.81

Current Assets

16.24

Diversified 2.28

Engineering &

Industrial

Machinery 3.70

Entertainment

0.62

Fertilizers,

Pesticides &

Agrochemicals

3.01

Housing &

Construction

1.38

Metals 3.37

Miscellaneous

-0.21

Oil & Gas,

Petroleum &

Refinery 10.10

Packaging 0.95

Paints 1.10

Paper 2.38

Personal Care

1.91

Banks 13.32

Breweries &

Distilleries 1.69

Cement 1.15

Computers -

Software &

Education

7.18 Consumer

Durables 1.03

Current Assets

6.02

Diversified

0.51

Electricals &

Electrical

Equipments

5.71

Engineering &

Industrial

Machinery 6.22

Entertainment

2.21

Finance 5.54

Housing &

Construction

5.83

Metals 1.60

Oil & Gas,

Petroleum &

Refinery 13.63

Pharmaceutical

s 2.62

Power

Generation,

Auto & Auto

ancillaries

4.88

Banks 6.82

cement 6.13

Computers -

Software &

Education 3.34

Current Assets

16.01

Electricals &

Electrical

Equipments

4.72

Engineering &

Industrial

Machinery

8.48

Entertainment

3.97

Fertilizers,

Pesticides &

Agrochemicals

4.33

Finance 1.82

Glass &

Ceramics 0.39

Housing &

Construction

12.02

Metals 0.63

Mining &

Minerals 0.98

Miscellaneous

41

Personal Care 2.08

Pharmaceuticals

8.15

Power Generation,

Transmission &

Equip 0.67

Rubber & Tyres

0.25

Steel 1.36

Telecom 3.59

Tobacco & Pan

Masala 2.77

Transport & Travel

0.51

Refinery 6.30

Paper 1.62

Pharmaceuticals

6.13

Plastic 4.12

Power

Generation,

Transmission &

Equip 1.82

Steel 4.96

Sugar 2.47

Telecom 3.79

Trading 2.29

Pharmaceuticals

12.37

Power

Generation,

Transmission &

Equip 2.37

Rubber & Tyres

0.45

Steel 0.43

Tea 1.13

Telecom 6.37

Tobacco & Pan

Masala 2.51

Transmission &

Equip 10.94

Printing &

Stationary 0.56

Steel 1.82

Telecom 7.64

Textiles 1.90

Tobacco & Pan

Masala 2.89

1.29

Oil & Gas,

Petroleum &

Refinery 3.47

Paints 0.33

Paper 0.19

Pharmaceuticals

5.47

Plastic 2.24

Power

Generation,

Transmission &

Equip 2.15

Shipping 1.14

Steel 4.72

Telecom 2.87

Textiles 1.6

Assets allocation:-

Scheme name Equity Debt Cash & Equivalent Chart

HDFC TOP 200-

growth

96.64 0.30 3.06

Reliance Growth-

Growth

82.56 0.00 17.44

ICICI Prudential

Dynamic plan-

growth

83.76 0.00 16.24

Birla Sun life

Equity Fund-

growth

93.98 0.00 6.02

42

SBI Magnum

Global Fund 94 –

Growth

83.18 1.44 15.38

RISK AND RETURN:-

RETURNS-( Scheme Performance (%) as on Jun 8, 2009)

Scheme name 3 Months 6 Months 1 Year 3 Years 5 Years Since

InceptionHDFC TOP 200-

growth

75.84 61.11 6.24 22.28 30.59 23.36

Reliance Growth-

Growth

77.42 62.78 -2.94 22.85 36.10 29.06

ICICI Prudential

Dynamic plan-growth

55.01 48.82 -4.36 18.32 31.97 34.04

Birla Sun life Equity

Fund-growth

76.05 56.45 -5.62 18.68 30.08 31.74

SBI Magnum Global

Fund 94 – Growth

96.13 75.12 -17.22 7.88 31.72 10.23

Returns:- Returns of different schemes are taken for the comparison and analysis

part in (CAGR) Compounded Annual Growth Rate.

Risk-

Scheme name Sharpe ratio Treynor ratio Fama Beta(β )HDFC TOP 200-

growth

-0.07 -0.39 0.32 0.88

Reliance Growth-

Growth

-0.14 -0.87 0.09 0.78

ICICI Prudential

Dynamic plan-

growth

-0.10 -0.61 0.11 0.80

Birla Sun life

Equity Fund-

growth

-0.13 -0.79 -0.03 0.89

SBI Magnum -0.20 -1.27 0.43 0.89

43

Global Fund 94 –

Growth

1) The Sharpe Measure :-

In this model, performance of a fund is evaluated on the basis of Sharpe Ratio, which is

a ratio of returns generated by the fund over and above risk free rate of return and the

total risk associated with it.

According to Sharpe, it is the total risk of the fund that the investors are concerned

about. So, the model evaluates funds on the basis of reward per unit of total risk.

Symbolically, it can be written as:

Sharpe Index (Si) = (Ri - Rf)/Si

Where,

Si is standard deviation of the fund,

Ri represents return on fund, and

Rf is risk free rate of return.

While a high and positive Sharpe Ratio shows a superior risk-adjusted

performance of a fund, a low and negative Sharpe Ratio is an indication of

unfavorable performance

2) The Treynor Measure:-

Developed by Jack Treynor, this performance measure evaluates funds on the basis of

Treynor's Index.

This Index is a ratio of return generated by the fund over and above risk free rate of

return (generally taken to be the return on securities backed by the government, as there

is no credit risk associated), during a given period and systematic risk associated with it

(beta). Symbolically, it can be represented as:

Treynor's Index (Ti) = (Ri - Rf)/Bi.

44

Where,

Ri represents return on fund,

Rf is risk free rate of return, and

Bi is beta of the fund.

All risk-averse investors would like to maximize this value.

While a high and positive Treynor's Index shows a superior risk-adjusted

performance of a fund, a low and negative Treynor's Index is an indication of

unfavorable performance.

.

Comparison of Sharpe and Treynor

Sharpe and Treynor measures are similar in a way, since they both divide the risk

premium by a numerical risk measure. The total risk is appropriate when we are

evaluating the risk return relationship for well-diversified portfolios. On the other hand,

the systematic risk is the relevant measure of risk when we are evaluating less than

fully diversified portfolios or individual stocks. For a well-diversified portfolio the total

risk is equal to systematic risk. Rankings based on total risk (Sharpe measure) and

systematic risk (Treynor measure) should be identical for a well-diversified portfolio,

as the total risk is reduced to systematic risk. Therefore, a poorly diversified fund that

ranks higher on Treynor measure, compared with another fund that is highly

diversified, will rank lower on Sharpe Measure.

3) Fama Model:-

The Eugene Fama model is an extension of Jenson model. This model compares the

performance, measured in terms of returns, of a fund with the required return

commensurate with the total risk associated with it. The difference between these two is

taken as a measure of the performance of the fund and is called Net Selectivity.

45

The Net Selectivity represents the stock selection skill of the fund manager, as it is the

excess returns over and above the return required to compensate for the total risk taken

by the fund manager.

Higher value of which indicates that fund manager has earned returns well above

the return commensurate with the level of risk taken by him.

Required return can be calculated as: Ri = Rf + Si/Sm*(Rm - Rf)

Where,

Ri represents return on fund,

Sm is standard deviation of market returns,

Rm is average market return during the given period, and

Rf is risk free rate of return.

The Net Selectivity is then calculated by subtracting this required return from

the actual return of the fund.

Among the above performance measures, model namely; Treynor measure use

Systematic risk is based on the premise that the Unsystematic risk is diversifiable.

These models are suitable for large investors like institutional investors with high risk

taking capacities as they do not face paucity of funds and can invest in a number of

options to dilute some risks. For them, a portfolio can be spread across a number of

stocks and sectors. However, Sharpe measure and Fama model that consider the entire

risk associated with fund are suitable for small investors, as the ordinary investor lacks

the necessary skill and resources to diversify. Moreover, the selection of the fund on the

basis of superior stock selection ability of the fund manager will also help in

safeguarding the money invested to a great extent. The investment in funds that have

generated big returns at higher levels of risks leaves the money all the more prone to

risks of all kinds that may exceed the individual investors' risk appetite.

46

C) β (Beta) Co-efficient:-

Systematic risk is measured in terms of Beta, which represents fluctuations in the NAV

of the fund vis-à-vis market. The more responsive the NAV of a Mutual Fund is to the

changes in the market; higher will be its beta. Beta is calculated by relating the returns

on a Mutual Fund with the returns in the market. While unsystematic risk can be

diversified through investments in a number of instruments, systematic risk cannot. By

using the risk return relationship, we try to assess the competitive strength of the

Mutual Funds vis-à-vis one another in a better way.

β (Beta) is calculated as N ( Σ XY) – Σ X Σ Y

N (Σ X2) – (Σ X) 2

LIMITATIONS OF THE STUDY

1. The study is limited only to the analysis of different schemes and its suitability

to different investors according to their risk-taking ability.

2. The study is based on secondary data available from monthly fact sheets,

websites and other books, as primary data was not accessible.

3. The study is limited by the detailed study of various schemes of Five Asset

Management Company.

SUGGESTIONS:-

• The Asset Management Company must design the portfolio in such a way, to

increase the returns.

47

• The Asset Management Company must design the portfolio in such a way, to lessen

the risk that is common in the market.

• The Asset Management Company must dedicate itself, because it motivates the

investors and potential investors to invest in Mutual Funds.

• The Asset Management Company must manage the Fund efficiently and with

dedication to earn the goodwill of the public.

• The Asset Management Company must make the most advantageous use of print

and electronic media in order to motivate the investors and potential investors to

invest in Mutual Funds.

CONCLUSIONS

After interpreting the above data the following conclusions have been made

HDFC Top 200-Growth

• It is a diversified aggressive equity fund.

• It is a open-ended equity scheme

• Since the β ratio is high it implies the risk is high

• As the returns in 1 year is more in HDFC top 200 compare to other four schemes.

• It is suitable for investors looking for medium risk and moderate returns with in a

time period of 1-3 years.

• Sharper’s ratio indicates that the portfolio management in HDFC top 200 is better

than other schemes.

• Treynors ratio indicates that the portfolio management in HDFC top 200 is better

than other schemes.

48

Reliance Growth -Growth

• It is a diversified equity fund.

• It is a open-ended equity scheme.

• NAV is highest in reliance in 12 years from its inception compare to other

schemes.

• Reliance have largest fund size of 5235.33crore rupees among all AMCs schemes

• Its expense ratio is very low as compare to other schemes. This is good indicator

of investors’ investment.

• In Reliance Growth the returns in 3 years and 5 years are more compare to other

four AMC’s schemes.

• P/E ratio in reliance is highest as compare to other mutual funds.

• Dividend yield is lowest among all schemes.

• Market capitalization of reliance growth is lowest as compare to other mutual

funds.

• It is suitable for investors looking for medium risk and moderate returns with in a

time period of 3-5 years.

ICICI Prudential Dynamic Plan-Growth

• It is a diversified equity fund.

• It is a open-ended equity scheme

• It is newest scheme of 7 year from its inception among the other schemes.

• In the ICICI Prudential Dynamic Plan returns in 3 and 6 months and from

inception are lower compare to other four AMC’s schemes.

• Since the β ratio is high it implies the risk is high

• In ICICI Prudential Dynamic Plan the returns are low in 3 months and 6 month

and from inception it is high as compare to other AMC’s schemes.

49

Birla Sun life Equity Fund-growth

• It is a diversified equity fund.

• It is a open-ended equity scheme

• Its expense ratio is very high as compare to other schemes. This is bad indicator

of investor’s investment.

• Portfolio turnover ratio is very high in Birla sun life equity fund.

• Market capitalization in this fund is highest as low compare to other AMC’s

schemes.

• In Birla Sun life equity fund the returns are lowest in last 5 years as compare to

other AMC’s schemes.

• In Birla sun life the returns are low compare to other AMC’s

• It is a value based fund

• It is a low risky fund

SBI Magnum Global Fund 94 – Growth

• It is a diversified equity fund.

• It is a open-ended equity scheme

• NAV is very low SBI Magnum Global Fund 94 as compare to other AMC’s

schemes.

• It is oldest fund

• In SBI the returns are lesser than other AMC’s

• It is a low risky fund

BIBLIOGRAPHY

Layman’s Guide to Mutual Funds By “Value research”

Mutual Funds Primer By “Times of india”

50

www.amfiindia.com

www.mutualfundsindia.com

www.valuereaserch.com

ANNEXURE’S

ANNEXURE-I

Sponsor

Sponsor is the person who acting alone or in combination with another body corporate

establishes a Mutual Fund. Sponsor must contribute at least 40% of the net worth of the

Investment Managed and meet the eligibility criteria prescribed under the securities and

Exchange Board of India (Mutual Fund) Regulations, 1996. The Sponsor is not

responsible or liable for any loss or short fall resulting from the operation of the

schemes beyond the initial contribution made by it towards setting up the Mutual Fund.

Trust

The Mutual Fund is constituted as a trust in accordance with the provisions of the

Indian Trusts Act, 1882 by the Sponsor. The trust deed is registered under the Indian

Registration Act, 1908.

Trustee

Trustee is usually a company (Corporate body) or a Board of Trustees (body of

individuals). The main responsibility of the trustee is to safeguard the interest of the

unit holders and inter alia ensure that the AMC functions in the interest of investors and

in accordance with the securities and Exchange Board of India (Mutual Funds)

Regulations, 1996, the provisions of the Trust Deed and the Offer Documents of the

51

respective Schemes. At least 2/3rd directors of the Trustee are independent directors

who are not associated with the Sponsor in any manner.

Asset Management Company (AMC)

The AMC if so authorized by the Trust Deed appoints the Registrar and Transfer Agent

to the Mutual Fund. The Registrar processes the application form, redemption requests

and dispatches account statements to the unit holders. The Registrar and Transfer agent

also handles communications with investors and updates investor records.

Unit Holders

Unit Holders are those investing in Mutual Fund.

Custodian

Custodian is the agency, which will have the legal possession of all the securities

purchased by the Mutual Fund.

SEBI

The Stock Exchange Board of India (SEBI) is regulatory authority of the Mutual Funds.

ANNEXURE II

Equity Fund is the one in which much of the portfolio is invested in corporate

securities and Debt Fund is the one in which much of the portfolio is invested in Gilt

and money market securities.

52

In an Open-ended Mutual Fund, there are no limits on the total size of the corpus.

Investors are permitted to enter and exit the open-ended Mutual Fund at any point of

time at a price that is linked to the net asset value (NAV).

In case of Closed-ended funds, the total size of the corpus is limited by the size of the

initial offer.

• A Dividend plan entails a regular payment of dividend to the investors.

• A Re-investment plan is a plan where these dividends are reinvested in the scheme

itself.

• A Growth plan is one where no dividends are declared and investor only gains

through capital appreciation in the NAV of the fund.

NAV is the net asset value of the fund. Simply put it reflects what the unit held by an

investor is worth at current market prices.

The broad guidelines issued for a Mutual Fund:

SEBI is the regulatory authority of Mutual Funds. SEBI has the following broad

guidelines pertaining to Mutual Funds:

• Mutual Funds should be formed as a trust under Indian Trust Act and should be operated by Asset Management Companies.

• Mutual Funds need to set up a Board of Trustee Companies. They should also have their Board of Directories.

• The net worth of the Asset Management Company should be at least Rs.10 crore.

• Asset Management Companies and Trustees of a MF should be two separate and distinct legal entities.

• The Asset Management Companies or any of its companies cannot act AS managers for any other fund.

• Asset Management Company has to get the approval of SEBI for its articles and Memorandum of Association.

53

• All Mutual Fund Schemes should be registered with SEBI.

• Mutual Funds should distribute minimum of 90% of their profits among the

investors.

54