Embed Size (px)

Citation preview

CORPORATE GOVERNANCE IN INDIA

M A D E B Y

S A H I L N A G PA L

R O L L N O . 2 3 2

B . C O M ( H O N S ) 4 T H S E M E S T E R

S E C T I O N D

SRI GURU NANAK DEV KHALSA COLLEGE

UNIVERSITY OF DELHI

CONTENTS

Introduction

Definition

Key players

Principles of Corporate Governance

Objectives of Corporate Governance

Corporate Governance in India

Securities Exchange Board Of India

Satyam Scandal

Conclusion

INTRODUCTION

The last few years have seen some major scams and corporate collapse across the globe.

In India, the major example is Satyam which is one of the largest IT companies in India.

All these events have caused the pendulum of public faith to shift away from free market to a more closely regulated one

DEFINITION

A system of law and sound approaches by which corporations are directed and controlled

Corporate governance are the policies, procedures and rules governing the relationships between the shareholders, directors and managers in a company, as defined by the applicable laws, the corporate charter, the company’s bylaws, and formal policies

KEY PLAYERS IN CORPORATE GOVERNANCE

Management

Board of Directors

Customers

Shareholders

Employees

Regulators

Suppliers

PRINCIPLES IN CORPORATE GOVERNANCE

Rights and equitable treatment of shareholders

Interests of other stakeholders

Role and responsibilities of the board

Integrity and ethical behaviour

Disclosure and transparency

OBJECTIVES OF CORPORATE GOVERNANCE

Enhance the performance of companies

Enhance access to capital

Enhance long term prosperity

Provide barrier to corrupt dealings

Impacts on the society as a whole

CORPORATE GOVERNANCE IN INDIA

The Indian corporate scenario was more or less stagnant till the early 90s.

The position and goals of the Indian corporate sector has changed a lot after the liberalization of 90s.

India’s economic reform programme made a steady progress in 1994.

India with its 20 million shareholders, is one of the largest emerging markets in terms of the market capitalization.

SECURITIES EXCHANGE BOARD OF INDIA

On April 12, 1988, SEBI was established with objective of protecting the rights of small investors and regulating and developing the stock markets in India.

In 1992, the Bombay Stock Exchange (BSE),the leading stock exchange in India, witnessed the first major scam masterminded by Harshad Mehta.

SECURITIES EXCHANGE BOARD OF INDIA

Analysts unanimously felt that if more powers had been given to SEBI, the scam would not have happened.

As a result the Government of India brought in a separate legislation by the name of ‘SEBI Act 1992’and conferred statutory powers to it.

Since then, SEBI had introduced several stock market reforms. These reforms significantly transformed the face of Indian Stock Markets

SATYAM SCANDAL

Overstated assets and income

The results announced on October 17, 2009 overstated quarterly Revenues by percent and profits by 97 percent.

The global head of internal audit also illegally obtained loans for the company.

Created 13000 fake salary accounts

Created fake customer identities and generated fake invoices to inflate revenue

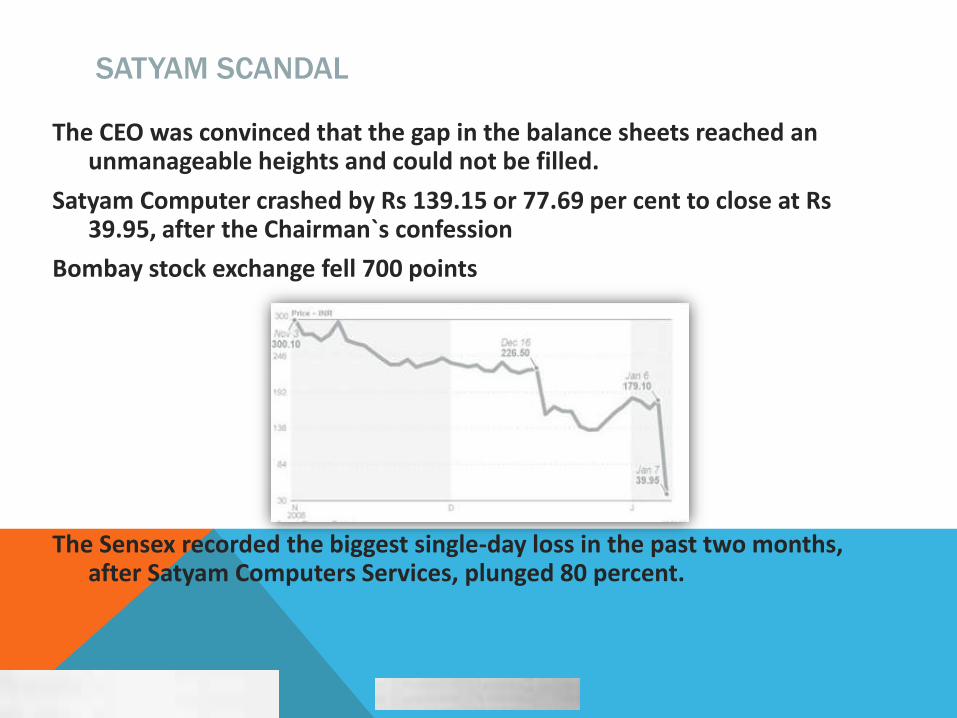

SATYAM SCANDAL

The CEO was convinced that the gap in the balance sheets reached an unmanageable heights and could not be filled.

Satyam Computer crashed by Rs 139.15 or 77.69 per cent to close at Rs 39.95, after the Chairman`s confession

Bombay stock exchange fell 700 points

The Sensex recorded the biggest single-day loss in the past two months, after Satyam Computers Services, plunged 80 percent.

SEBI and Clause 49

1. SEBI asked Indian firms above a certain size to implement Clause

49, a regulation that strengthens the role of independent directors

serving on corporate boards.

1. On August 26, 2003, SEBI announced an amended Clause 49 of the

listing agreement which every public company listed on an Indian

stock exchange is required to sign. The amended clauses come into

immediate effect for companies seeking a new listing.

ॐ 13

The major changes to Clause 49…

1.Independent Directors —1/3 to ½depending whether the chairman of

the board is a non-executive or executive position.

2 .Non-Executive Directors ----The total term of office of non-executive

directors is now limited to three terms of three years each.

3. Board of Directors-----The board is required to frame a code of

conduct for all board members and senior management and each of them

have to annually affirm compliance with the code.

ॐ 14

Clause 49..4.Audit Committee----Financial statements and the draft audit report of

management discussion and analysis of…

• Financial condition

• Result of operations of compliance with laws

• Risk management letters

• Letters of weaknesses in internal controls issued by statutory

• Internal auditors

• Removal and terms of remuneration of the chief internal auditor

5.Whistleblower Policy ----This policy has to be communicated to all

employees and whistleblowers should be protected from unfair treatment

and termination.

6.Subsidiary Companies-----50% non-executive directors & 1/3 &

½independent directors depending on whether the chairman is non-

executive or executive. ॐ 15

ॐ 16

7.Disclosures----Contingent liabilities./Basis of related party transactions.

/Risk management/ . Proceeds from initial public offering/ .

Remuneration of directors.

8.Certifications --- reviewed the necessary financial statements and

directors’report; established and maintained internal controls,

disclosed to the auditors and informed the auditors and audit

committee of any significant changes in internal control

and/or of accounting policies during the year.

CONCLUSION

Corporate governance And economic development are intrinsically linked.

Effective corporate governance systems promote the development of strong financial systems

Which, in turn, have an unmistakably positive effect on economic growth and poverty reduction.

THANK YOU