Embed Size (px)

Citation preview

Debt & Disequilibrium

UFM Market Trends

Guatemala 23 March 2017

1

Alejandro Jenkins

2

Les querelles ne dureraient pas longtemps, si le tort n’était que d’un côté.

– La Rochefoucauld, maxime 496

UsuryDa queste due,* se tu ti rechi a mente lo Genesì dal principio, convene prender sua vita e avanzar la gente; e perché l’usuriere altra via tene,per sé natura e per la sua seguace dispregia, poi ch’in altro pon la spene.

– Inferno XI * (natura e arte)

• Weber: prevalence of debt slavery → Abrahamic prohibition of interest

3

Dalí, The Usurers (1951-60)

Interpretations of the Great Depression

• Hayek: monetary expansion induced malinvestment

• Keynes: excessive saving depressed aggregate demand

• Schumpeter: adjustment of the market to technological change and other exogenous shocks

4

Great Depression, cont.• Fisher: debt need not be

macroeconomically neutral

• Schumpeter, Friedman, Tobin: “greatest economist the US has ever produced”

• Smith: “A student once asked Leontief why there was no Fisherian school. Leontief said: ‘He wrote too clearly’.”

5

Irving Fisher (1867-1947)

Vernon L. Smith (n. 1927)

6

Rien ne persuade tant le gens qui ont peu de sens, que ce qu’ils n’entendent pas.

– Retz, Mémoires III

Equilibrium• In microeconomics, efficient outcome is one in

which all possible gains from voluntary exchange are realized

• No one could be better off without making another worse off

• Also Pareto optimality or, in a pricing context, general equilibrium

• Refers only to exchange

7

Equilibrium, cont.• Worked out by Fisher,

Samuelson et al. by analogy with thermodynamic equilibrium

• Directly influenced by statistical mechanics of Willard Gibbs (1839 - 1903)

• Arrow-Debreu welfare theorems (1951, 59) assume complete markets & perfect information

8

Assets• Consumption market: good or

service exchanged once (e.g., hamburgers, haircuts)

• Asset market: same good exchanged many times (e.g. capital stock, real state)

• Bachelier (1900), Mandelbrot (1963) & Samuelson (1965) showed the efficiency asset prices follow random walks (sub-martingales)

9

Assets, cont.• Smith et al. find experimentally

that consumption markets equilibrate very robustly

• Not the case for assets

• Debate on asset market efficiency reflected in 2013 Nobel Prize for Fama, Hansen & Shiller

• In an efficient asset market, risks would be correctly estimated

10

Fuente: http://www.uchicago.edu/features/what_makes_nobel_speeches_endure/

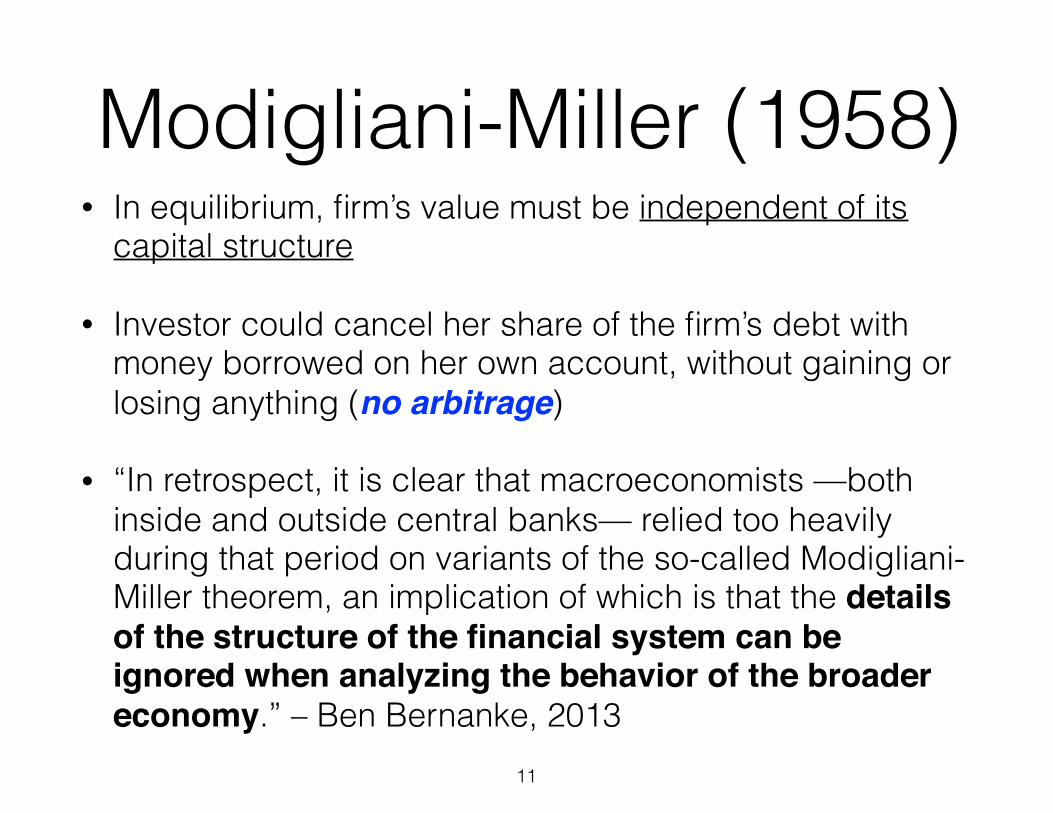

Modigliani-Miller (1958)• In equilibrium, firm’s value must be independent of its

capital structure

• Investor could cancel her share of the firm’s debt with money borrowed on her own account, without gaining or losing anything (no arbitrage)

• “In retrospect, it is clear that macroeconomists —both inside and outside central banks— relied too heavily during that period on variants of the so-called Modigliani-Miller theorem, an implication of which is that the details of the structure of the financial system can be ignored when analyzing the behavior of the broader economy.” – Ben Bernanke, 2013

11

Monetary paradox• Friedman rule: in equilibrium, private opportunity cost

of holding liquidity should equal social cost of providing it

• Cost to central bank of providing liquidity is negligible

• → optimum would be 0% nominal rate on riskless bond

• → deflation equal to real interest rate

• Not even Friedman took this seriously as policy (cf. his “k-percent rule”)

12

13

My pulse, as yours, doth temperately keep time, And makes as healthful music: it is not madness

That I have utter’d. – Hamlet III, 4

• “If statistical observation leads us to believe that a given magnitude varies periodically, and if we look for the cause of those oscillations, we may suppose that that magnitude executes either

• (a) forced oscillations, or

• (b) self-oscillations, which may be either sinusoidal [weakly nonlinear] (bα) or of relaxation type [strongly nonlinear] (bβ).”

- Econometrica 1, 328 (1933)

14

Self-oscillation

15

http://www.youtube.com/watch?v=eAXVa__XWZ8

Credit: M. de Pablo

This article appeared in a journal published by Elsevier. The attachedcopy is furnished to the author for internal non-commercial researchand education use, including for instruction at the authors institution

and sharing with colleagues.

Other uses, including reproduction and distribution, or selling orlicensing copies, or posting to personal, institutional or third party

websites are prohibited.

In most cases authors are permitted to post their version of thearticle (e.g. in Word or Tex form) to their personal website orinstitutional repository. Authors requiring further information

regarding Elsevier’s archiving and manuscript policies areencouraged to visit:

http://www.elsevier.com/authorsrights

• AJ, “Self-Oscillation”, Phys. Rep. 525, 167 (2013), [arXiv:1109.6640 [physics.class-ph]]

• Micro-dynamics of markets totally different from physical systems

• …but uses & limitations of macroscopic equilibrium have similarities in statistical mechanics and economics

• AJ, “Towards a Microeconomic Theory of the Finance-Driven Business Cycle”, Laissez-Faire 42, 12 (2015) + refs.

16

https://arxiv.org/abs/1312.0323

Edward Hopper, The “Martha KcKeen” of Wellfleet, oil on canvas (1943)Museo Thyssen-Bornemisza, Madrid

17

Rayleigh - van der Pol

10 20 30 40 50 60 t

-2

-1

1

2V

V (0) = 0.1 , V̇ (0) = 0

10 20 30 40 50 60 t

- 3

-2

-1

1

2

3

4V

V (0) = 4 , V̇ (0) = �4

V̈ � 0.2�1� V 2

�V̇ + V = 0

18

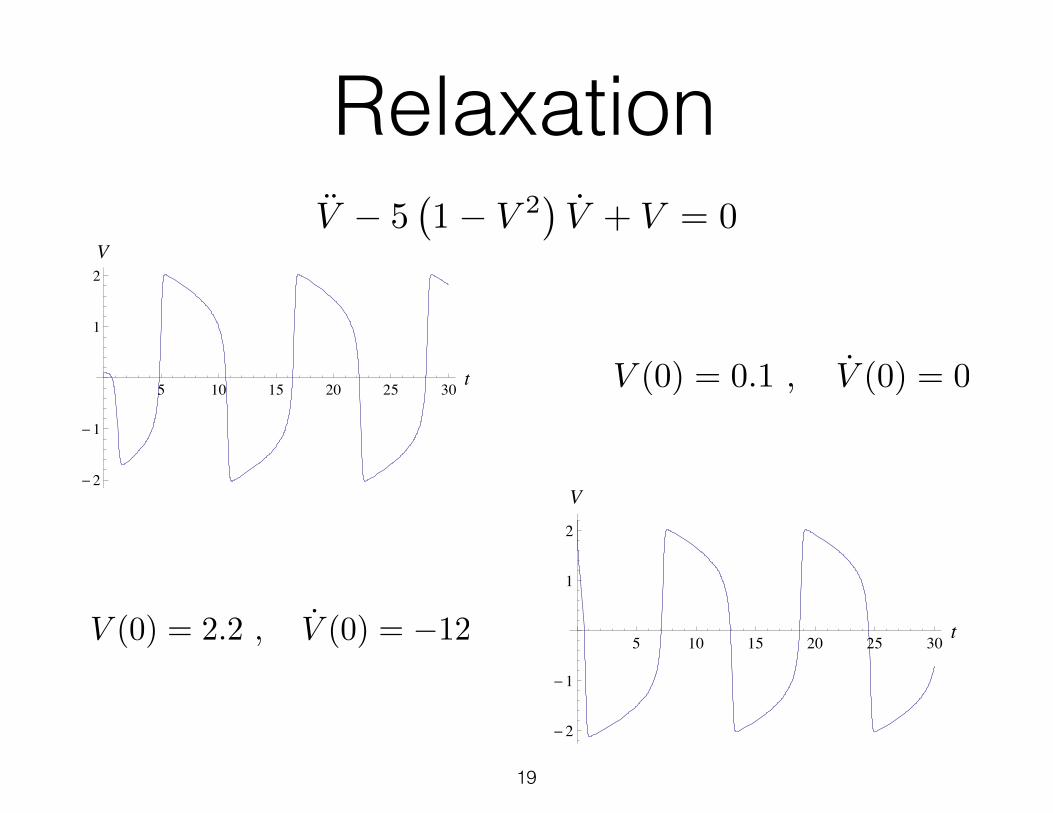

Relaxation

5 10 15 20 25 30 t

-2

-1

1

2V

V (0) = 0.1 , V̇ (0) = 0

5 10 15 20 25 30 t

-2

-1

1

2

V

V (0) = 2.2 , V̇ (0) = �12

V̈ � 5�1� V 2

�V̇ + V = 0

19

Macro models• Linearly unstable relation between income,

capital & investment introduced in 1930s by Kalecki, Hansen & Samuelson

• Non-linear models with relaxation limit cycles by Goodwin, Kaldor, Hicks, et al.

• Lucas critique: anticipation of a regular cycle would make it go away

• Is business cycle efficient?

20

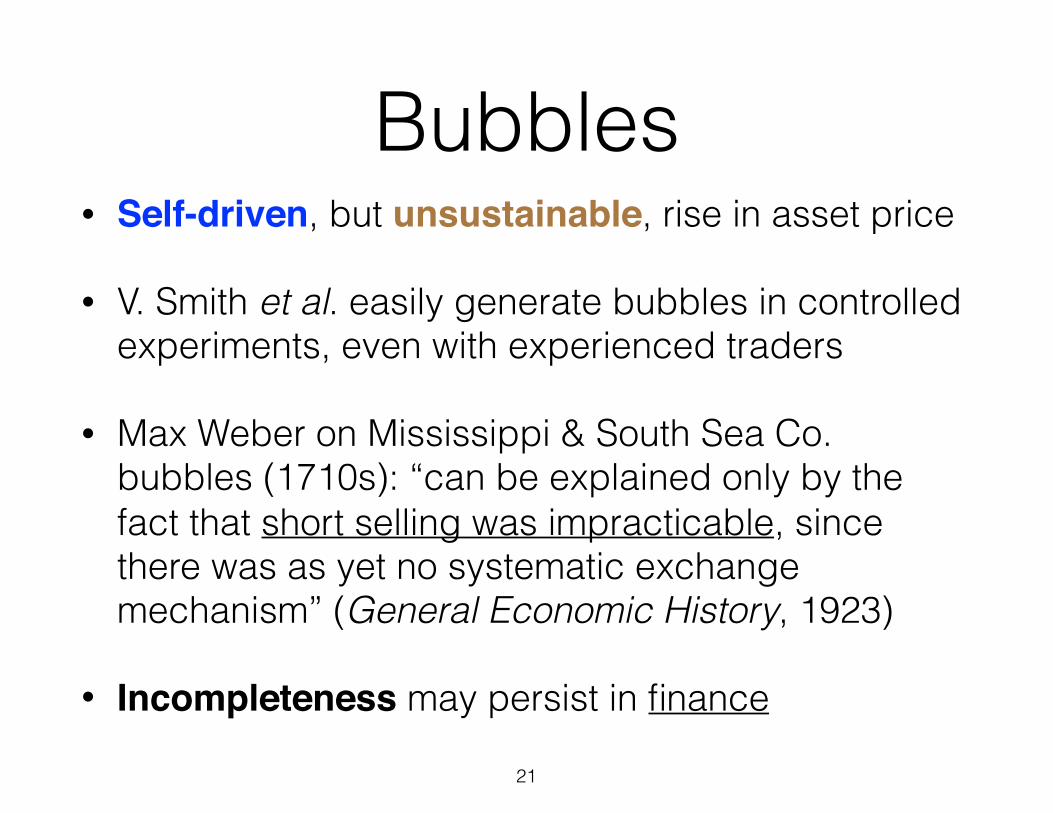

Bubbles• Self-driven, but unsustainable, rise in asset price

• V. Smith et al. easily generate bubbles in controlled experiments, even with experienced traders

• Max Weber on Mississippi & South Sea Co. bubbles (1710s): “can be explained only by the fact that short selling was impracticable, since there was as yet no systematic exchange mechanism” (General Economic History, 1923)

• Incompleteness may persist in finance

21

22

Relaxation oscillations are commonplace not only in physics, but also in physiology (heart beats) and economics (business cycles) as well. In fact, the expression ‘history repeats itself’ is probably a description of a large-scale integrated relaxation oscillation phenomenon.

– Sargent, Scully & Lamb, Laser Physics (1978)

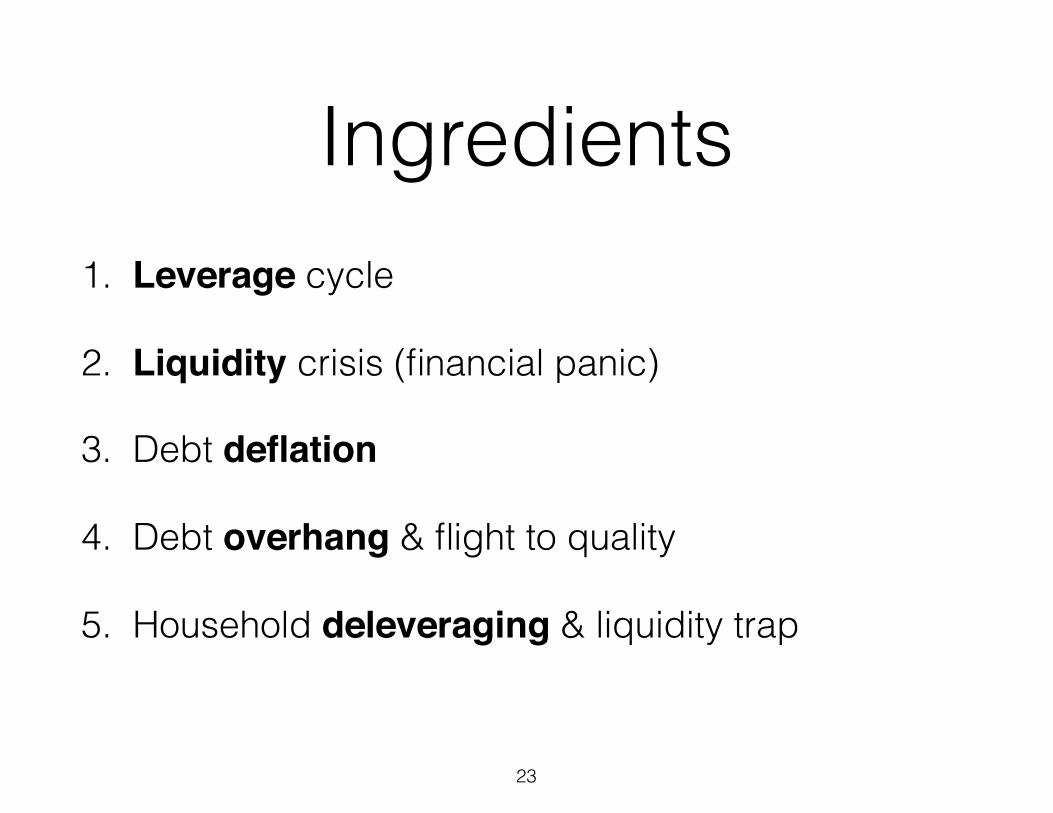

Ingredients1. Leverage cycle

2. Liquidity crisis (financial panic)

3. Debt deflation

4. Debt overhang & flight to quality

5. Household deleveraging & liquidity trap

23

Leverage cycle

• John Geanakoplos (2010): market determination of leverage for buying an asset on credit, as in mortgage

• More leverage allows more optimistic investors to set price

• Higher asset price improves collateral, promoting credit

• Positive feedback between leverage and price24

leverage =

(purchase value� down payment)

down payment

Leverage, cont.• Credit default swaps (CDS)

complete market by allowing pessimist to leverage their bets.

• CDS standardized for US secondary housing market towards the end of 2005

• see The Big Short

25

Information• Optimism & pessimism wouldn’t exist under perfect

info.

• Hayek, Stigler, et al. stressed that economically relevant info. is not given, but emerges through market process

• Absence of CDS pre-2006 relevant not just as incompleteness per se

• Prevented info. held by pessimist potential investors from being incorporated into asset prices in a timely way

26

Liquidity crisis• Bubble followed by rapid fall in asset prices

• Widespread defaults among leveraged buyers

• Losses to banks, which also carry asset in their balances

• Depositors withdraw funds, forcing hasty liquidations (fire sale)

• Asset prices fall further; financial institutions may grow illiquid

• Financial panic: joint defaults, counterparty credit risk, etc.

27

Debt overhang• Borrowers end up as owners of depressed asset; lenders end up

as owners of debt

• Wealth transfer from net borrowers (‘households’) to net lenders (‘banks’)

• Fisher: net lenders have lower marginal propensity to consume

• Smith: borrowers may end up with negative equity (‘underwater’)

• → households can’t enjoy most of their new income

• Principal-agent problem between banks and households causes investor’s flight to quality

28

Debt deflation• Fractional reserve banking

causes spike in demand for liquidity to contract monetary supply (money’s ‘perverse elasticity’)

• Deflation aggravates debt overhang

• Can be combatted by increased supply of liquidity (quantitative easing)

29

(1936)

Keynesianism• Debt overhang and principal-agent problem could

help explain Keynes’s excessive saving

• Underwater households can’t spend or invest at normal levels

• → fall in aggregate demand

• Money paid to households goes quickly to bank

• Bank won’t lend back while household is underwater → liquidity trap

30

Keynesianism, cont.• Inflation relieves debt overhang, but has other

undesirable consequences

• Government’s deficit spending even more problematic

cf. Eggertsson & Krugman (2012)

• Wiping out savers harmful in the long run, even if it relieves crisis

31

32

Source: S. D. Gjerstad y V. L. Smith, Rethinking Housing Bubbles (Cambridge U. P., 2014), p. 258

Statistical mechanics• Theoretical physics suffers very analogous blind spot

• ‘Non-equilibrium thermodynamics’ usually focused on stochastic fluctuations about equilibrium

• Mostly fails to describe dynamics of engines (self-oscillators)

• Engines are powered by external gradient of temperature or chemical potential

• e.g., life on Earth maintained by temperature difference between Sun’s surface (6,000 K) & Earth’s surface (300 K)

33

Debt dynamics• People save some of their income, even at negative rates

• Banks exist because of info. problems in finding efficient use for these savings

• Fisher & Rothbard’s mistake: Equilibrium yield curve (rate v. term) not determined by deposit contracts alone

• There’s usually scope for arbitrage of terms

• i.e., pay low rate on short-term deposit one expects to be renewed, while lending out that money at higher rates and longer terms

• Why free markets disfavor 100% reserve banking

34

Debt dynamics, cont.• Maturity mismatch makes liquidity crises possible,

but it’s partly a free-market phenomenon

• Financial markets probably remain far from equilibrium

• This may explain many macroeconomic paradoxes

• Yield curve doesn’t translate into structure of production (Hayek’s mistake)

35

Sustained non-equilibrium• Savings analogous to

reservoir of chemical energy in biological cell

• E. Moreno: “the economy is alive”

• No savings → no business cycle

• but also far lower living standard!

36

37

Confusion’s cure lives not in these confusions

– Romeo & Juliet IV, 5

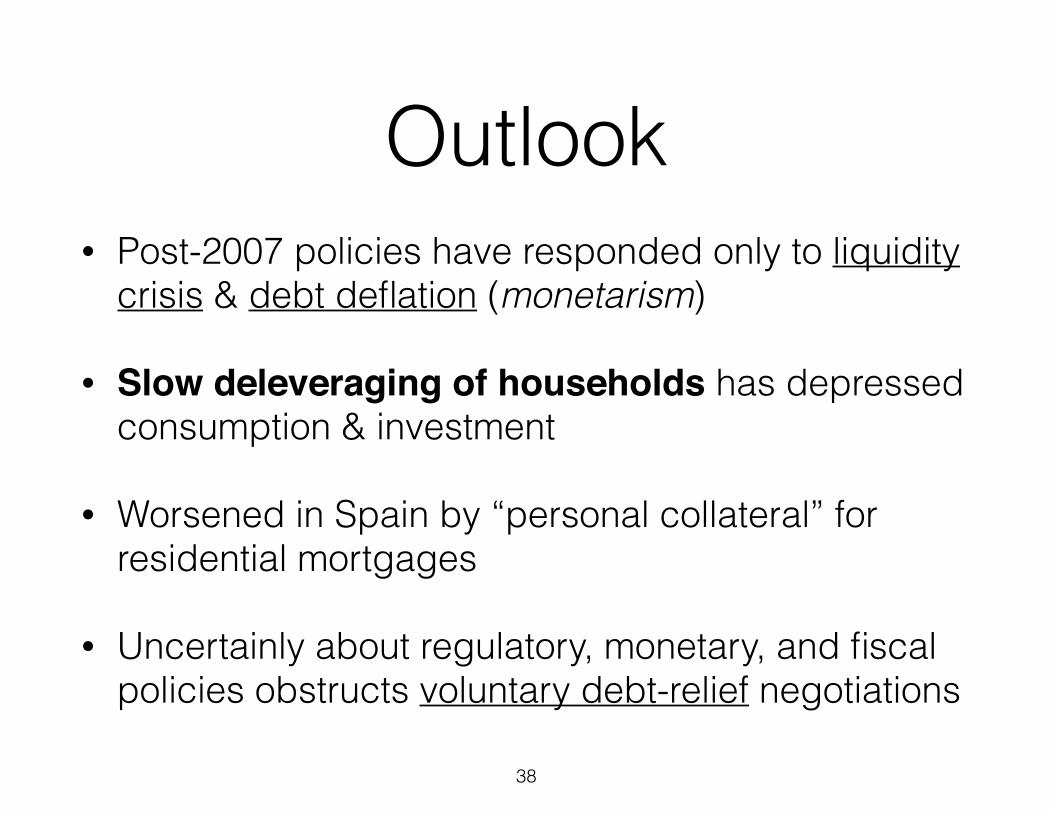

Outlook• Post-2007 policies have responded only to liquidity

crisis & debt deflation (monetarism)

• Slow deleveraging of households has depressed consumption & investment

• Worsened in Spain by “personal collateral” for residential mortgages

• Uncertainly about regulatory, monetary, and fiscal policies obstructs voluntary debt-relief negotiations

38

Outlook, cont.• Bailing out “solvent but illiquid” financial institutions

involves grave risk of corruption

• e.g., deep & long-lasting damage to efficiency of Japanese banking post-1992

• Monetary expansion (zero interest, quantitative easing) meets banks’ elevated liquidity demand

• Inflation & deficit spending weakly focused on problem of underwater households, while involving grave unintended consequences

39

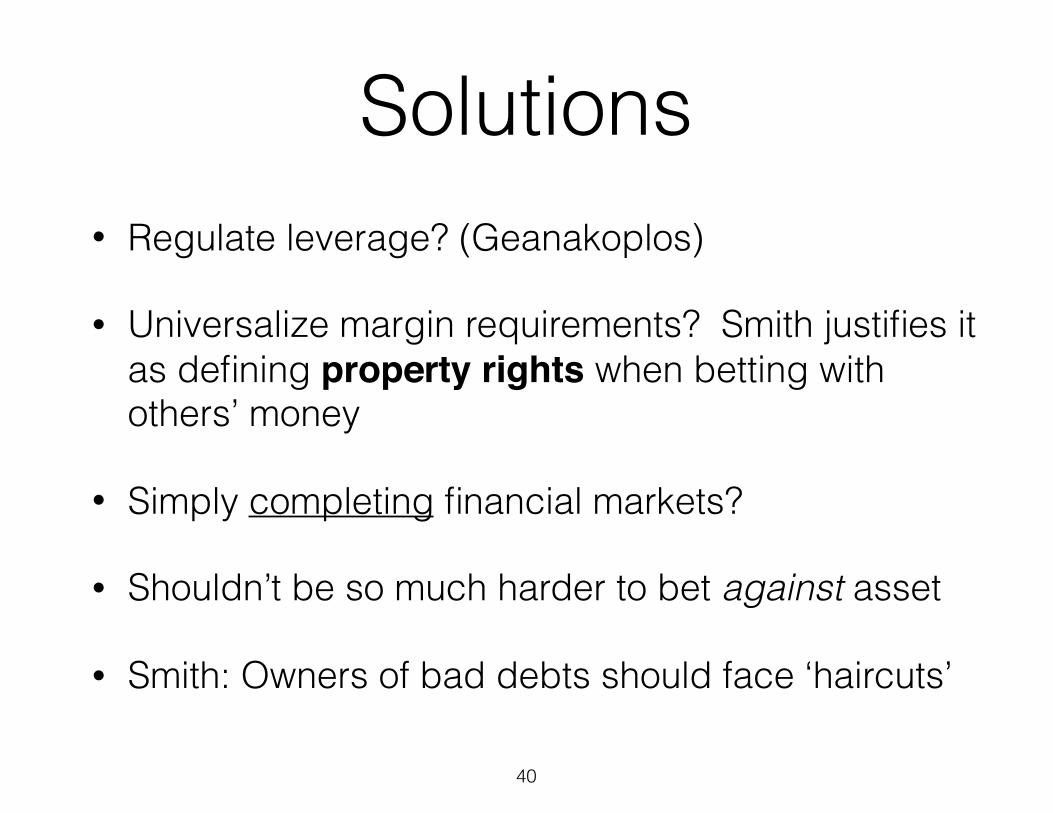

Solutions• Regulate leverage? (Geanakoplos)

• Universalize margin requirements? Smith justifies it as defining property rights when betting with others’ money

• Simply completing financial markets?

• Shouldn’t be so much harder to bet against asset

• Smith: Owners of bad debts should face ‘haircuts’

40

![AGGREGATE DEMAND, IDLE TIME, AND UNEMPLOYMENT …saez/michaillat-saezNBER14ADjuly.pdf · Barro and Grossman [1971] general disequilibrium model but replaces the disequilibrium framework](https://img.pdfslide.net/doc/110x75/5eb7249ba629f1440c52857c/aggregate-demand-idle-time-and-unemployment-saezmichaillat-saeznber14adjulypdf.jpg)