Embed Size (px)

Citation preview

Bringing smart policies to life

Digital Financial Services for Financial

Inclusion

John Owens, Senior Policy Advisor, AFI

26 March 2015

Bangkok, Thailand

Bringing smart policies to life

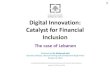

Global Financial Inclusion Indicators

Source: Demirguc-Kunt & Klapper (2012), World Bank Policy Research Paper 6025

2.5 billion of adults do not have access to formal financial system

AFI | Alliance for Financial Inclusion

Bringing smart policies to life

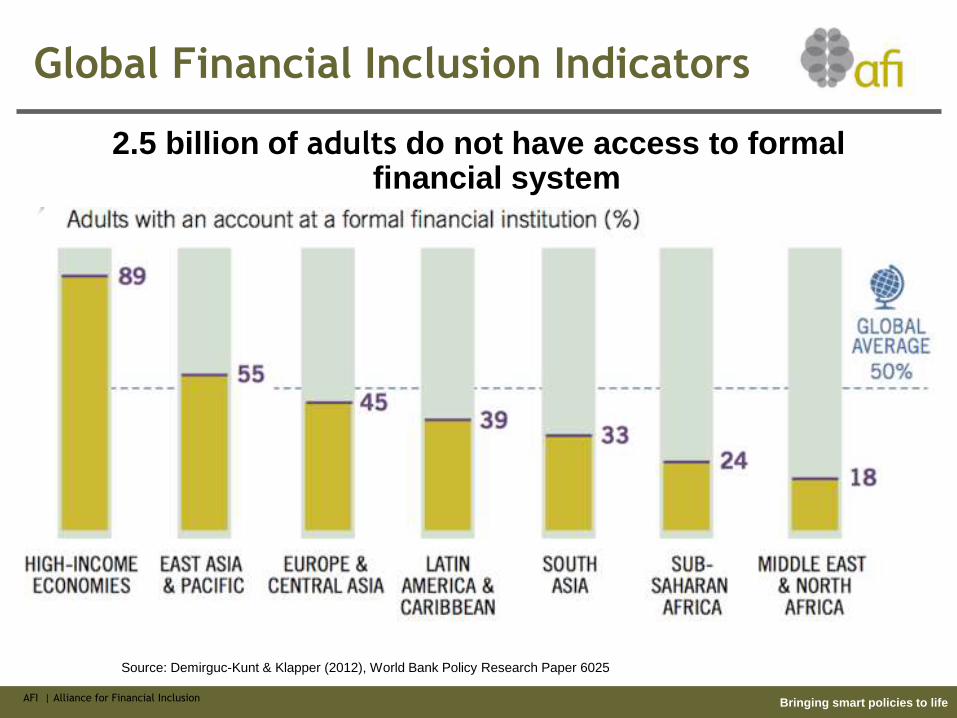

Overview of AFI

AFI is a global network of policymakers in developing and emerging countries

•Founded in 2008, AFI’s goal is to support developing countries to develop and implement successful financial inclusion policies

•The goal of the AFI network is to accelerate the adoption of innovative

financial inclusion policy solutions, with the ultimate aim of making financial

services more accessible to the billions of people who do not have access

to the formal financial system.

Bringing smart policies to life

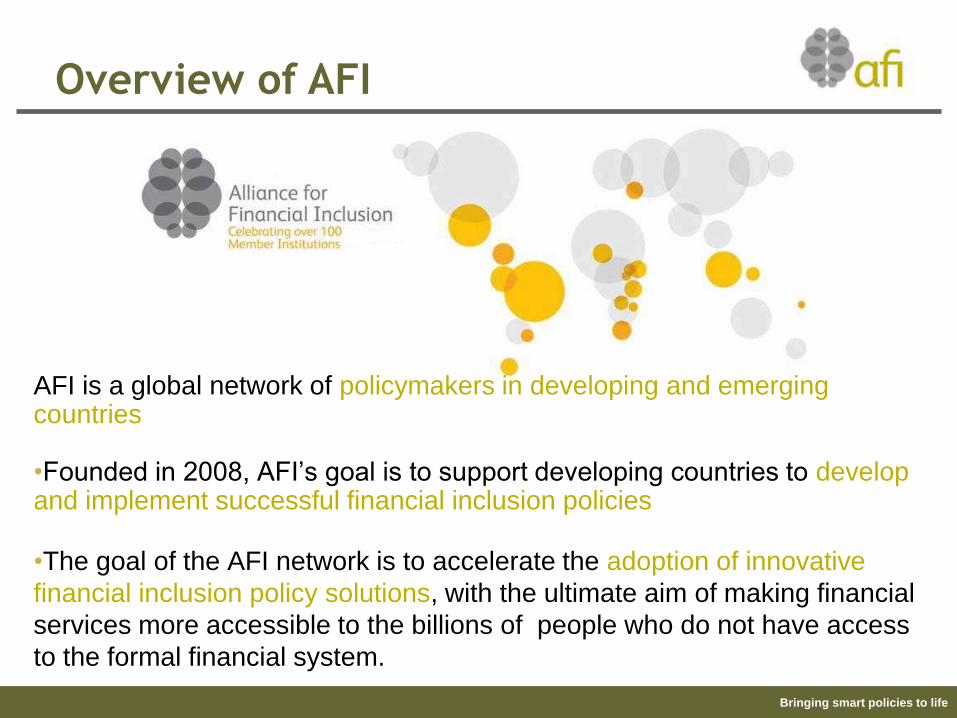

The AFI Timeline

• 125 Institutions, 95

countries

• Unique Peer Learning

network (working

groups)

• G20 Implementing

partner

• Maya Declaration

• More than 70 tangible

policy reforms

Concept design

Building the

Network

Activating the

Network

Enhancing Network

value

Policy-Driving

Network

Transition Planning

Independence

2008 2009 2010 2011 2012 2013-2015 2015-

Bringing smart policies to life

Growing Relevance of Financial Inclusion Globally

• Financial Inclusion is no longer only a development concern

but a cornerstone of economic development framework and

model

• Ministries of Finance and Central Banks are including Financial

Inclusion in their mandate together with stability and integrity

• Financial Inclusion is more and more understood in a broad

framework including access, usage and quality of a range of

financial services

• Developed countries are increasingly facing financial exclusion

problem

• G20 recognizes the benefits of financial inclusion for inclusive

growth, stability and integrity

AFI | Alliance for Financial Inclusion

Bringing smart policies to life

Opportunities

• Growing alignment of interests among governments,

private sector and global community

• Greater understanding on the issues related to financial

inclusion as well as more data

• Recognition of country specific conditions and developing

and emerging country-led approaches

• More open communications with International Standard

Setting Bodies

• Technological innovation and enabling regulatory

framework are driving new digital financial service

models that support financial inclusion

AFI | Alliance for Financial Inclusion

Bringing smart policies to life

Benefits & Opportunities of

Digital Financial Services

Source IFC Infographic: Bonny Jennings www.itldesign.co.za IAFI | Alliance for Financial Inclusion

Bringing smart policies to lifeAFI | Alliance for Financial Inclusion

E-money Services

Mobile Financial Services

Use of Agents

Key Models of Digital Financial

Services

Bringing smart policies to lifeAFI | Alliance for Financial Inclusion

Convergence & Interoperability

Financial

Inclusion

Bringing smart policies to life

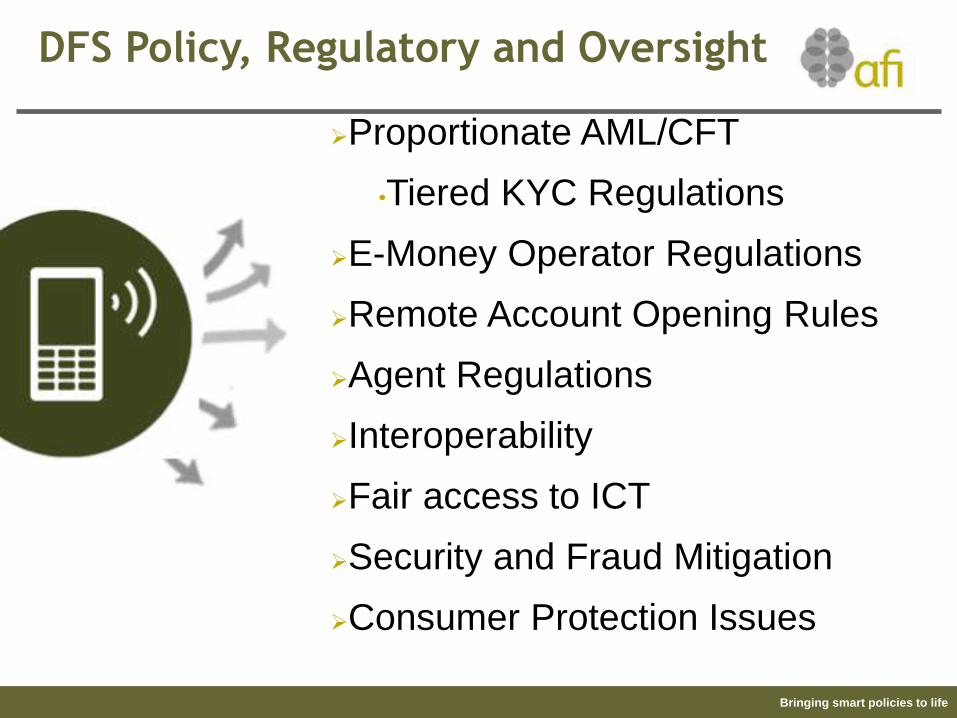

DFS Policy, Regulatory and Oversight

Proportionate AML/CFT

•Tiered KYC Regulations

E-Money Operator Regulations

Remote Account Opening Rules

Agent Regulations

Interoperability

Fair access to ICT

Security and Fraud Mitigation

Consumer Protection Issues

Bringing smart policies to life

Regulatory Coordination

• Telecom operators as financial service

providers & banks as telecom operators

• USSD, Fair Access, Data Security

• Who provides oversight?

• Overlapping issues among regulators

• Coordination is critical and needs to be

improved

Bringing smart policies to life

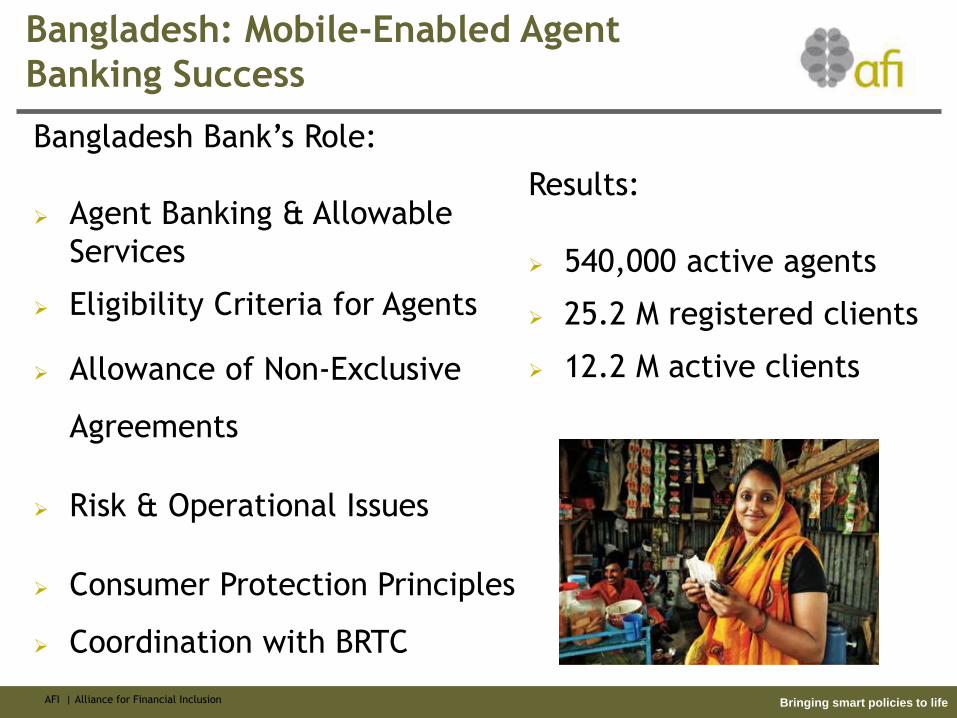

Bangladesh: Mobile-Enabled Agent

Banking Success

AFI | Alliance for Financial Inclusion

Bangladesh Bank’s Role:

Agent Banking & Allowable

Services

Eligibility Criteria for Agents

Allowance of Non-Exclusive

Agreements

Risk & Operational Issues

Consumer Protection Principles

Coordination with BRTC

Results:

540,000 active agents

25.2 M registered clients

12.2 M active clients

Bringing smart policies to life

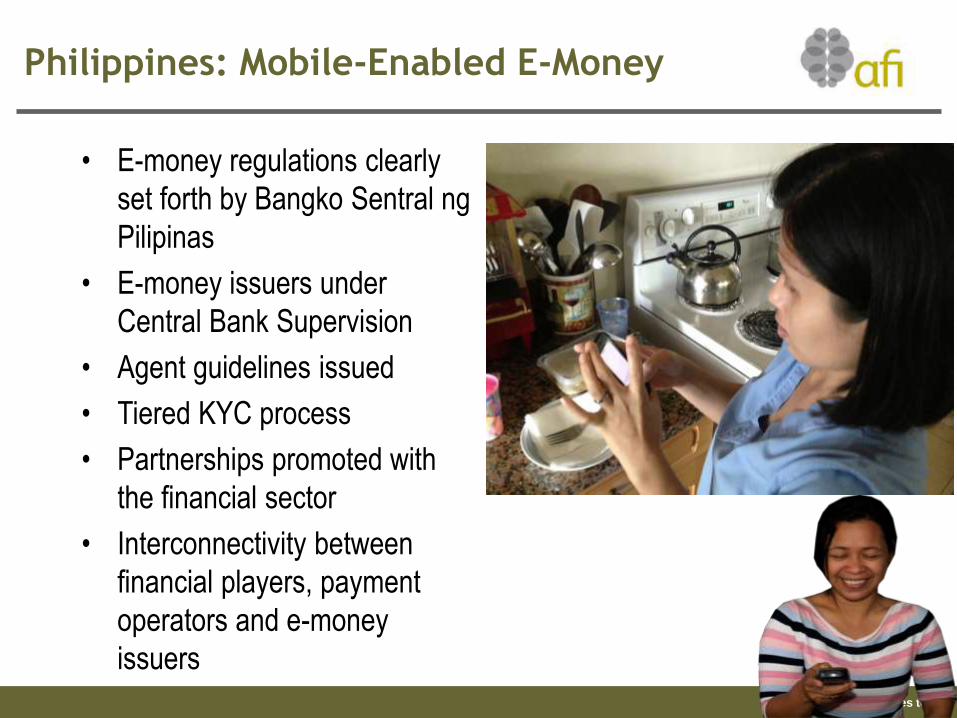

Philippines: Mobile-Enabled E-Money

• E-money regulations clearly

set forth by Bangko Sentral ng

Pilipinas

• E-money issuers under

Central Bank Supervision

• Agent guidelines issued

• Tiered KYC process

• Partnerships promoted with

the financial sector

• Interconnectivity between

financial players, payment

operators and e-money

issuers

Bringing smart policies to life

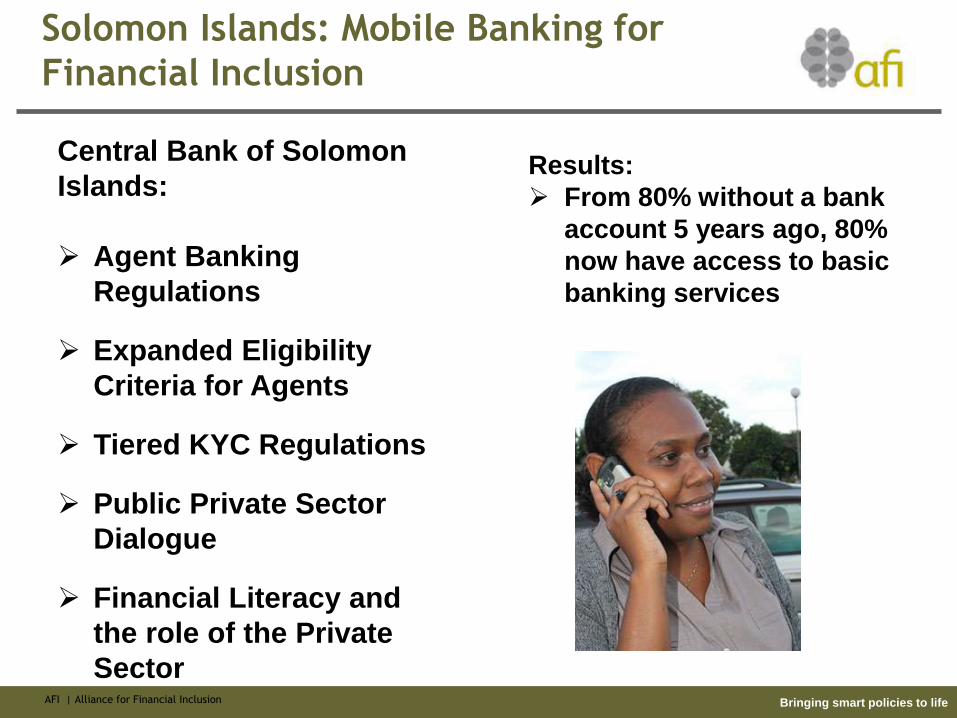

Solomon Islands: Mobile Banking for

Financial Inclusion

AFI | Alliance for Financial Inclusion

Central Bank of Solomon

Islands:

Agent Banking

Regulations

Expanded Eligibility

Criteria for Agents

Tiered KYC Regulations

Public Private Sector

Dialogue

Financial Literacy and

the role of the Private

Sector

Results:

From 80% without a bank

account 5 years ago, 80%

now have access to basic

banking services

Bringing smart policies to life

Bringing

smart

policiesto life [email protected]

www.afi-global.org

Thank [email protected]

@NewsAFI