Embed Size (px)

Citation preview

INDIAN PHARMA INDUSTRTY

Areas of CoverageSantha

nam-

Introduction

-Players-

competitors

Dipti-products

-substitute

Saurabh

-nature -Industry outlook

-Brokerage

reports

Basheer-Factors bearing

demands -End users

Basically deals with medicinal drugs which are use in the diagnosis, cure, mitigation, treatment, or prevention of disease

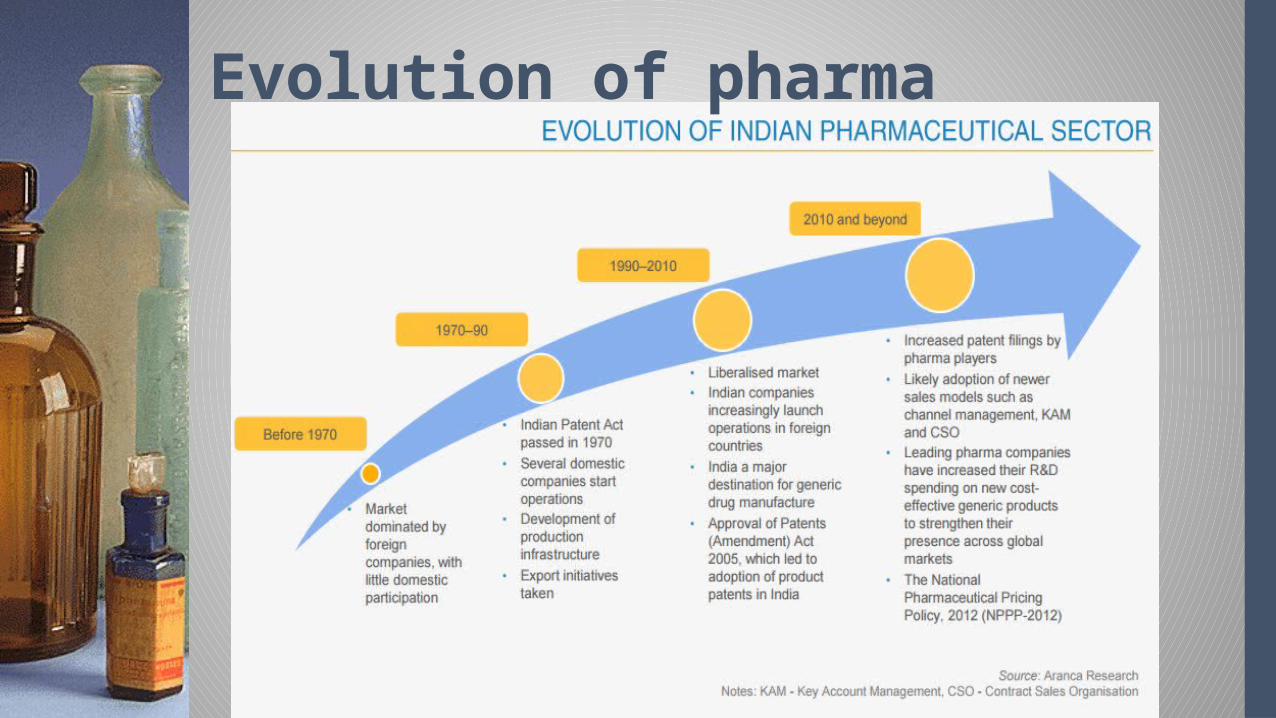

Over the past 40 years or so the Indian pharmaceutical sector witnessed rapid

growth and transformation. The annual growth rate was about 17% since 2004 and more

than 12% since 1947 with a volume of just Rs. 10 core in 1947 to a sales turnover of about US $ 5.5 billion in 2004.

One of the fastest developing utility sector.Expected to grow at higher phase.Lower cost of production.Likely to surpass other countries and reach third position in

growth.

OVERVIEW

Evolution of pharma

› ANTI-BIOTICS› PAEDIATRIC › GYNAEC › ORTHO › ANTI COUGH & COLD › ANTI ACID & GASTRIC › ANALGESICS & NSAID› MULTI VITAMIN & ANTI OXIDANT› HEPATO PROTECTIVE (LIVER RELATED)› DERMA › GENITO URINARY› INJECTABLE

Products

Products

ProductsHIV INFECTI

ON-

ATRIPLA-

COMPLERA

-INSENT

RESS

OSTEOARTHRI

TIS-

GLUCOSAMINE

-CHONDROITIN

-PRIMORINE

SMOKING

CESSATIONS

-NICTRO

INS-

HABITROL

-ZYBAN

EXPECTORANT

S-

DURATUSS

-MUCINEX

CANCER-

HELEVAN-

IBRANCE

Pharmaceutical industry has substitutes of Ayurveda and natural therapy or remedies .1. HIV infection:- garlic.2.. Osteoarthritis:- cinnamon powder and honey,

mustard oil and camphor3. Smoking cessations :- herbal cigarettes,

turmeric tulsi, cinnamon ,gangal, mulethi paste.

4. Expectorants:- honey and ginger, and lime.5. Cancer :- aloevera and apple cider

vinegar ,termeric,green tea,asahwgandha.

SUBSTITUTES

• is a system of traditional medicine originating in Tamil Nadu in South India.•Siddha is more about the 8 element and the supernatural powers in humans.•the basic concepts of the Siddha medicine are similar to Ayurveda. The only difference appears to be that the siddha medicine recognizes predominance of

Examples :-1.Na (tongue): black in Vaatham, yellow or red in pitham, white in kabam, ulcerated in anemia.2.Varnam (color): dark in Vaatham, yellow or red in pitham, pale in kabam.3.Kural (voice): normal in Vaatham, high-pitched in pitham, low-pitched in kabam, slurred in alcoholism.

(ii)siddha

BASIS AYURVEDA

SIDDHA

vaatham Old age childhoodkabam childhood Old age pitham adults adults

Factors bearing demand

Environmental

Conditions

population

Natural Calamities

War, Mindset of

people

USERS OF INDIAN PHARMA› INTAS-One of the largest

Animal Healthcare Company.

› Animal Pharmaceuticals products are available in over 8,500 veterinary clinics nationwide.

People

› Indian pharma has more than 545 subsidiary companies outside India.

› US, Europe, Japan, Africa, Australia are top countries who use Indian Pharma products.

› Many such products used are generic medicines

› Preferred because of low cost of medicines.

Companies

Company Name Market Cap(Rs. cr)

Sun Pharma 177,118.59

Lupin 82,753.62

Dr. Reddys Labs 53,059.00

Cipla 50,944.95

Aurobindo Pharm 48,159.56

Cadila Health 41,420.63

Divis Labs 29,955.47

GlaxoSmithKline 27,596.24

Glenmark 26,864.09

Torrent Pharma 25,647.40

Wockhardt 17,694.43

Piramal Enter 16,911.18

Alembic Pharma 12,589.09

Ajanta Pharma 11,697.13

Pfizer 11,550.84

Company Name Net Sales(Rs. cr)

Cipla 10,131.78

Dr. Reddys Labs 10,011.00

Lupin 9,752.47

Aurobindo Pharm 8,095.10

Sun Pharma 8,017.19

Cadila Health 5,284.40

Glenmark 5,085.60

Torrent Pharma 3,475.49

GlaxoSmithKline 3,287.58

Jubilant Life 3,176.30

Ipca Labs 3,085.14

Divis Labs 3,084.01

Piramal Enter 2,401.41

Abbott India 2,288.65

Biocon 2,241.60

PLAYERS

Key Players –Recent Stock Updates

Resources

Raw materials Human Resource

Suppliers

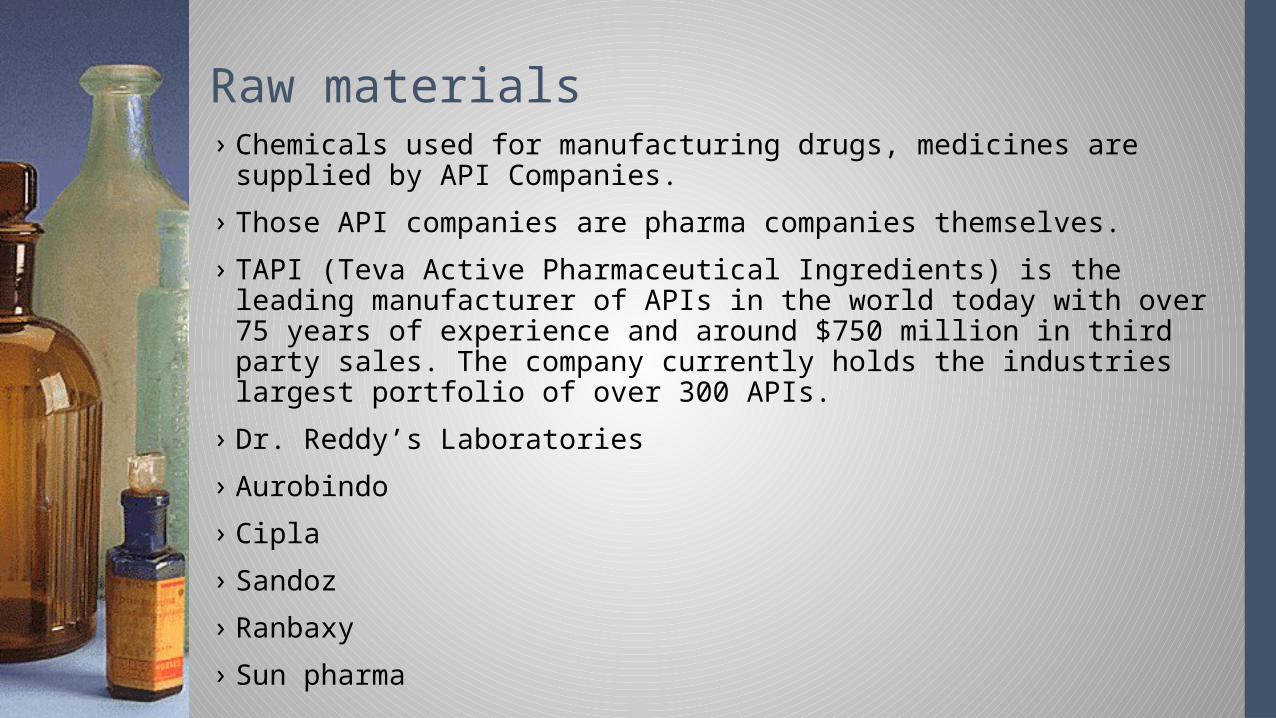

› Chemicals used for manufacturing drugs, medicines are supplied by API Companies.

› Those API companies are pharma companies themselves.› TAPI (Teva Active Pharmaceutical Ingredients) is the leading

manufacturer of APIs in the world today with over 75 years of experience and around $750 million in third party sales. The company currently holds the industries largest portfolio of over 300 APIs.

› Dr. Reddy’s Laboratories› Aurobindo› Cipla › Sandoz› Ranbaxy› Sun pharma

Raw materials

Companies Offering

Zenatek Software Solutions for Tracking and Monitoring Pharma Cargo

Ypsomed Pen Injectors, Pen Needles and Auto-Injectors for Self-Injection

WILCO Leak Detection and Inspection Machines

Vertellus Biomaterials Biocompatible Polymer Coatings for Drug Delivery

UPS Healthcare Healthcare and Pharmaceutical Logistics Services

Testo Thermometers, Humidity Meters, pH Meters and Data Loggers

SHL Autoinjectors, Pen Injectors and Inhaler Systems

Qualicaps Capsules and Pharmaceutical Processing Equipment

NATURE OF PHARMA INDUSTRY

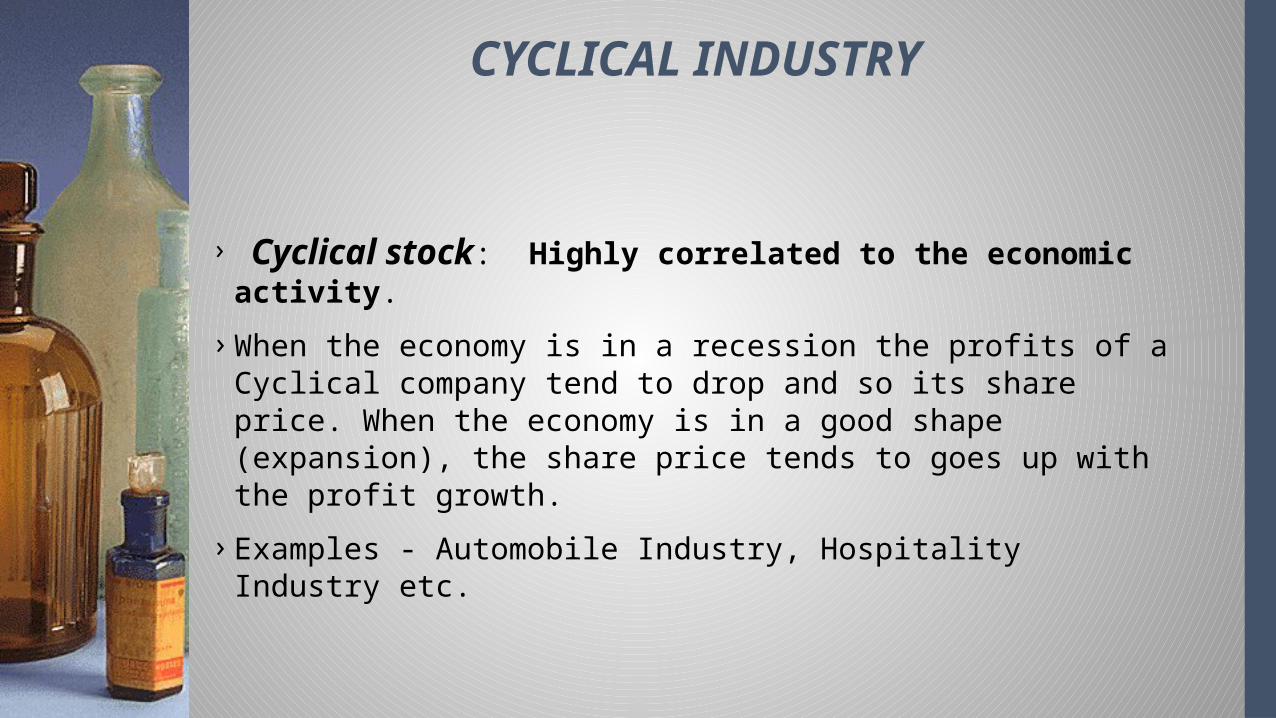

› Cyclical stock: Highly correlated to the economic activity.

› When the economy is in a recession the profits of a Cyclical company tend to drop and so its share price. When the economy is in a good shape (expansion), the share price tends to goes up with the profit growth.

› Examples - Automobile Industry, Hospitality Industry etc.

CYCLICAL INDUSTRY

› Non cyclical stock : Is very Low Correlated to the economic activities.

› The price of the share and the profits of the company does not depends on how the economy is behaving, whether the economy is experiencing the super normal, having a constant growth or there is a slowdown in the economy.

› Examples- Power, Household products, Education, Paper Industry etc.

NON CYCLICAL/ DEFENSIVE INDUSTRY

SUMMARIZATION OF BROKERAGE REPORTS

› Sun Pharma continues to maintain its top rank by sales and achieved 17.5% growth in October 2015. – Ranbaxy’s growth of 17.8% in October was the

highest since its acquisition by Sun Pharma. – As per PL’s view, manpower and product rationalisations

could be the reasons of underperformance in Ranbaxy since acquisition.

PRABHUDAS LILLADHAR’S REPORT

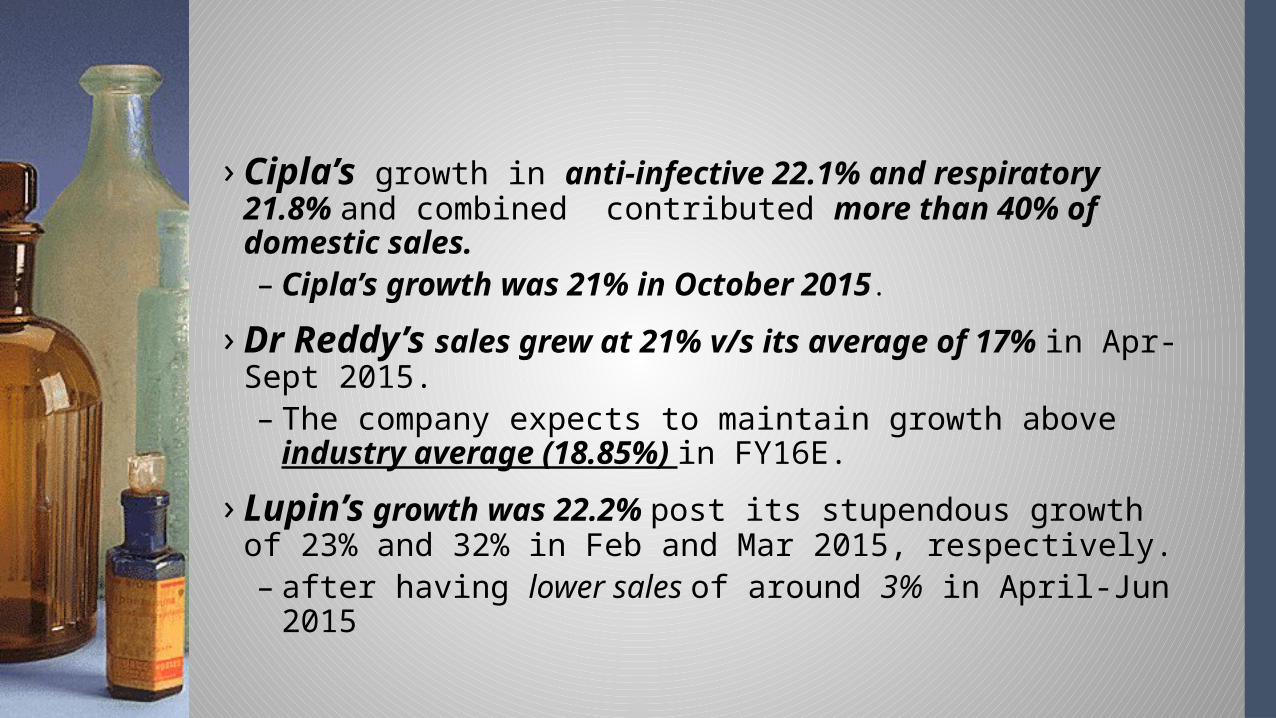

› Cipla’s growth in anti‐infective 22.1% and respiratory 21.8% and combined contributed more than 40% of domestic sales. – Cipla’s growth was 21% in October 2015.

› Dr Reddy’s sales grew at 21% v/s its average of 17% in Apr‐Sept 2015. – The company expects to maintain growth above

industry average (18.85%) in FY16E. › Lupin’s growth was 22.2% post its stupendous growth

of 23% and 32% in Feb and Mar 2015, respectively.– after having lower sales of around 3% in April‐Jun 2015

SUN PHARMA ACCUMULATE

CIPLA ACCUMULATE

DR. REDDY’S LAB BUY

LUPIN SELL

RATINGS BY PL BROKER

› Sun Pharma’s : Revenues fell to 6837.6cr i.e. 14.8% YoY (I-direct estimate: 7064.1 cr) mainly due to a decline in US sales.– Domestic sales increased mere 1.3% YoY to 1818.7 crore (I-

direct estimate: 1996.7cr) due to inventory adjustment.– EBITDA margins declined 837 bps YoY to 28.3% (I-direct

estimate: 27.2%)› Cipla’s: Revenues grew 24.8% YoY to Rs 3452.4 crore, on

account of 50.8% growth in export formulation to Rs 1874 crore. EBIDTA rose to 22.9% and Net Profit by 44.4% YOY to 431.2 cr.

ICICI DIRECT’S REPORT

› Dr. Reddy’s Lab : Revenues showed growth of 11% YoY to INR 39890mn. – EBITDA margin stood at 28.6% expanded by

590bps on account of increase in gross margins due to better business mix & lower SGA expenses.

– R&D expenses stood at 11.4% in line with management guidance due to scale up in development activities of complex generics.

SUN PHARMA HOLD

CIPLA HOLD

Dr. REDDY’S LAB HOLD

› The IPM size is expected to grow to US$ 85 bn by 2020 at CAGR of 23.9%.

› By 2020, India is likely to be among the TOP THREE pharmaceutical markets by incremental growth and SIXTH largest market globally in Absolute size .

› The life style segments such as cardiovascular, anti-diabetes, anti-depressants and anti-cancers will continue to be lucrative and fast growing due to increased urbanisation and change in lifestyle patterns.

› The government is focusing on speedy introduction of generic drugs into the market. This also will benefit Indian pharma companies.

› Intense competition and consequent price erosion would prevail in future also.

FORECASTING

› The GOI has unveiled ‘Pharma Vision 2020’ aimed at India making a Global Leader in end to end drug manufacturer.

› India will see the largest M&A in Pharma and Health Care sector.

› Cipla, Sun Pharma, Dr. Reddy & Lupin might become the part of Government’s ‘JAN AUSHADHI’ project.– There are 117 stores across the country and planning to

expand 600 in next two years.

› The share of generic drugs is expected to continue increasing it could represent about 90 per cent of the prescription drug market by 2016

› Due to their competence in generic drugs, growth in this market offers a great opportunity for Indian firms.

› Generic drug market is expected to grow in the next few years, with many drugs going off-patent in the US and other countries.

› India’s OTC drugs market stood at USD 3 billion in 2011 and is expected to expand at a CAGR of 16.3 per cent to USD6.6 billion over 2016.– There is a huge market for OTC drugs as the penetration of

chemists in the rural market increases.

› http://www.themedica.com/› http://www.pharmaceutical-technology.com/› http://www.mdtvalliance.org/› http://www.pharmarawmaterialmanufacturers.com/› http://www.moneycontrol.com/› http://www.investopedia.com/› http://www.ibef.org/› http://www.slideshare.net/

Reference

![2015 Launch of Excellence & Equity [xe] project](https://img.pdfslide.net/doc/110x75/55d11340bb61eb66708b46b0/2015-launch-of-excellence-equity-xe-project.jpg)