Embed Size (px)

Citation preview

Foreign Earned Income Exclusion

Derland G. Bahr, CPA

Foreign Earned Income Exclusion

Up to a maximum of 99,200 for 2014To qualify you must either be a Bona Fide Resident or meet the Physical Presence Test

In this slideshow we will look at the Physical Presence Test since it is the more common of the two methods.

Physical Presence Test330 day rule

330 day ruleTo qualify to take any credit. You must have foreign earned income and be overseas 330 days out of any 365 day period.

It can be from June 1, 2014 to May 31, 2015It can be a calendar year.It can run from Oct 13, 2012 to Oct 12,2013

Physical Presence Test330 day rule

330 day ruleThe key is you cannot be back in the United States for more than 35 days within the 365 day period you choose.

You can be in a different county.E.g., you work as a contractor in Afghanistan for 310 daysYou go to Germany for 20 days before coming homeThus, you were overseas for 330 days within a 12 month period, therefore you qualify for an exclusion.

If you don’t meet this test you do not qualify for any exclusion!

Physical Presence Test330 day rule

330 day ruleLet’s use a similar example

E.g., you work as a contractor in Afghanistan for 325 daysYou come straight home. You were only out of the states for two additional days (327 total)You come back home without leaving the states again that year.

You fail to meet the 330 day rule thus you do not quality for any exemption.

Physical Presence Test330 day rule

330 day ruleIf, however, you come back and get your wife and go to the Caribbean for a week you would have 330 days out of the states within the 12 month period and you would qualify.The key, the 330 day rule is all or nothing, either you qualify or you do not.

Physical Presence TestDays within the Calendar Year

Determining the amount of exclusionThe amount of exclusion is prorated based on the number of days within your 365 day period that fall within the calendar year for the tax return you are filing.

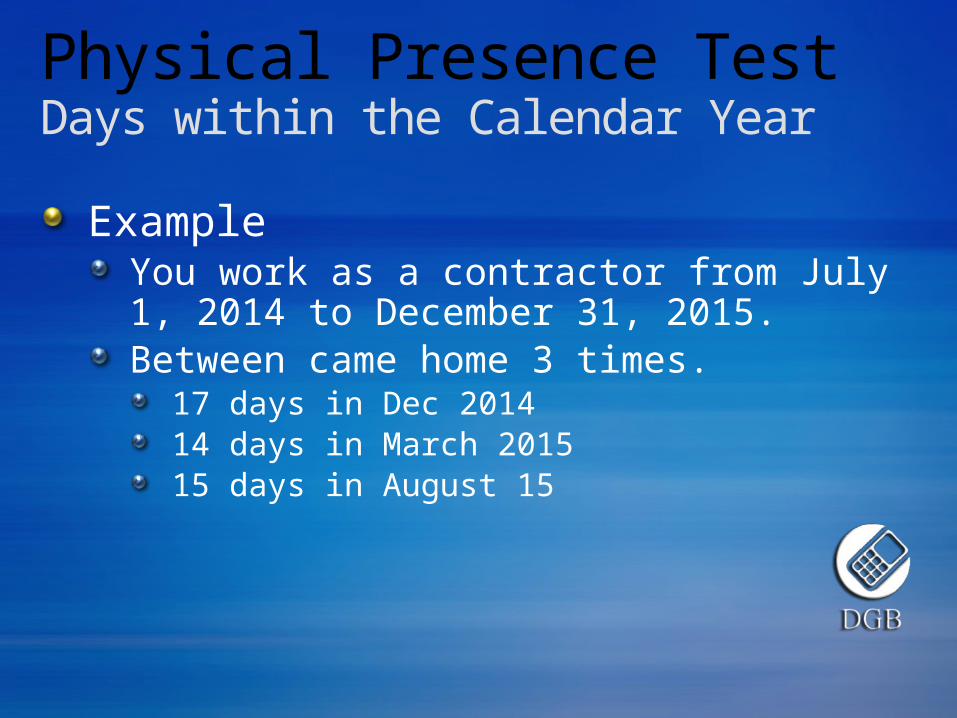

Physical Presence TestDays within the Calendar Year

ExampleYou work as a contractor from July 1, 2014 to December 31, 2015.Between came home 3 times.

17 days in Dec 201414 days in March 201515 days in August 15

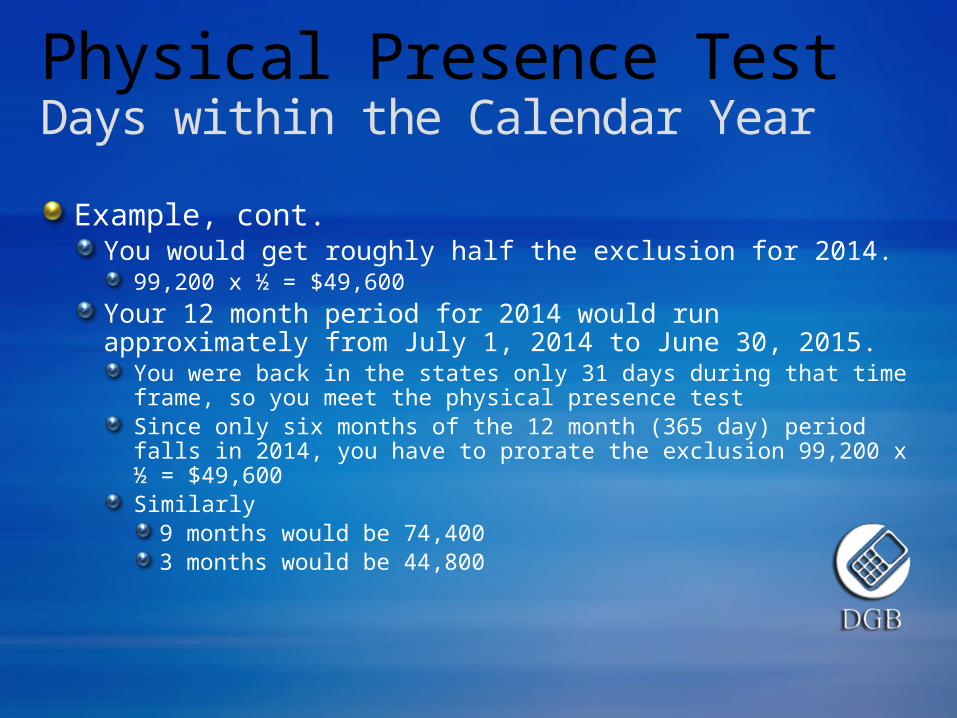

Physical Presence TestDays within the Calendar Year

Example, cont.You would get roughly half the exclusion for 2014.

99,200 x ½ = $49,600Your 12 month period for 2014 would run approximately from July 1, 2014 to June 30, 2015.

You were back in the states only 31 days during that time frame, so you meet the physical presence testSince only six months of the 12 month (365 day) period falls in 2014, you have to prorate the exclusion 99,200 x ½ = $49,600Similarly

9 months would be 74,4003 months would be 44,800

Physical Presence TestDays within the Calendar Year

Example, cont.You would get entire exclusion for 2015Using the example you would be overseas from Jan 1, 2015 to Dec. 31, 2015.

Between those dates you are only back in the states for 29 days.Since all twelve months of the period fall in 2015, you can take the full exclusion ($100,800) in 2015.

Physical Presence TestDays within the Calendar Year

Notice, your 12 month periods can overlapFor 2014 taxes you use July 1, 2014 to June 30, 2015 to meet the qualifications.For 2015 you use Jan. 1, 2015 to Dec. 31, 2015 to get the full exclusion

Thus, you use Jan – June 2015 to meet the 330 day rule for both yearsThis is okay – 12 month periods can overlap!

Foreign Earned Income Exclusion: Other notes

Any taxable income you do have is taxed at the higher rates.Example you have $130,000 in income. You qualify for a $90,000 foreign earned income exclusion and you have $20,000 in itemized deductions. Thus, you have $20,000 in taxable income. That income is taxed at the 25% bracket rather than the 10 and 15% brackets.

Foreign Earned Income Exclusion: Other notes

You must report your income and then take the exclusion.If not, the IRS will get a copy of the W-2 and assume all the income is taxable.

Foreign Earned Income Exclusion: Other notes

Example: I have seen a couple think it is not taxable; therefore, they just don’t report the foreign income. Due to the wife’s moderate income the software they used showed they qualified for earned income credit. The got a huge refund. They ended up having to pay it back.

Foreign Earned Income Exclusion: Other notes

Example, cont.: While foreign earned income is non-taxable for federal income tax purposes. It is added back in to determine whether you qualify for earned income credit, etc.This is different from military combat pay which is not added back to determine the credit.

Summary and Conclusions:

You must be overseas 330 days out of a 365 day period to qualify for a credit at all. The 365 day period does not have to be a calendar year.The credit is prorated based on the number of days in your 365 day period that falls within the calendar year for a specific tax return.Two different 365 day periods can overlap.You must report the income and take the exclusion. It affects other parts of your return.

Contact us for more information

You can email or fax us your information and we would be happy to prepare a return for you even if you are overseas.Our office is near Fort Hood, TX. I have prepared many foreign earned income exclusions.Email: [email protected]: derlandbahrcpa.comPhone 254-432-5724