Embed Size (px)

Citation preview

www.futurumcorfinan.com

Page 1

What Corporate Finance Textbooks Don’t Tell

You about Stated/Nominal vs Effective Annual

Interest Rates

Time is money (Benjamin Franklin)

“If time is money, shouldn’t we count those benjamins?”

Note:

IVP = Ignacio Velez-Pareja (Associate Professor of Finance at Universidad Tecnológica de

Bolívar in Cartagena, Colombia)

Karnen : Sukarnen (a student in corporate finance)

Introduction

We could find the explanations about the calculation of Stated and Effective Annual Interest

Rates (SAIR vs EAIR) in most of standard corporate finance textbooks, mainly put under the

Sukarnen

DILARANG MENG-COPY, MENYALIN,

ATAU MENDISTRIBUSIKAN

SEBAGIAN ATAU SELURUH TULISAN

INI TANPA PERSETUJUAN TERTULIS

DARI PENULIS

Untuk pertanyaan atau komentar bisa

diposting melalui website

www.futurumcorfinan.com

www.futurumcorfinan.com

Page 2

chapter “The Time Value of Money”. The basic idea behind SAIR and EAIR is that, it is not

always be possible to assume that compounding or discounting is an annual process, that is,

cash flows (inflows or outflows) arise either at the start or the end of the year. We could see this

in real practice, where:

the contractual payment for interest charge on loan is incurred on a semi-annual basis

or a quarterly basis;

interest charge on credit cards is applied on a monthly basis;

a fixed deposit scheme may offer daily compounding;

a car dealer may quote an interest rate on a monthly basis.

How should we compare interest rates that are quoted for different periods?

Thus, to have the “apples with apples” comparison, it is necessary to determine the effective

annual percentage rate, or effective annual interest rate.

The classic example of the section in the standard corporate finance textbooks regarding the

conversion of stated into the effective annual interest rate is as follows1:

3-5b Stated Versus Effective Annual Interest Rates

Both consumers and businesses need to make objective comparisons of loan costs or

investment returns over different compounding periods. To put interest rates on a common

basis for comparison, we must distinguish between stated and effective annual interest rates.

The stated annual rate is the contractual annual rate charged by a lender or promised by a

borrower. The effective annual rate (EAR), also known as the true annual return, is the annual

rate of interest actually paid or earned. The effective annual rate reflects the effect of

compounding frequency, whereas the stated annual rate does not. We can best illustrate the

differences between stated and effective rates with numerical examples.

Using the notation introduced earlier, we can calculate the effective annual rate by substituting

values for the stated annual rate (r) and the compounding frequency (m) into Equation 3.14:

1 Megginson, William L., and Scott B. Smart. Introduction to Corporate Finance. Mason (USA): South-Western, a part of Cengage Learning. 2009. Chapter 3 : The Time Value of Money. Page 109-110.

www.futurumcorfinan.com

Page 3

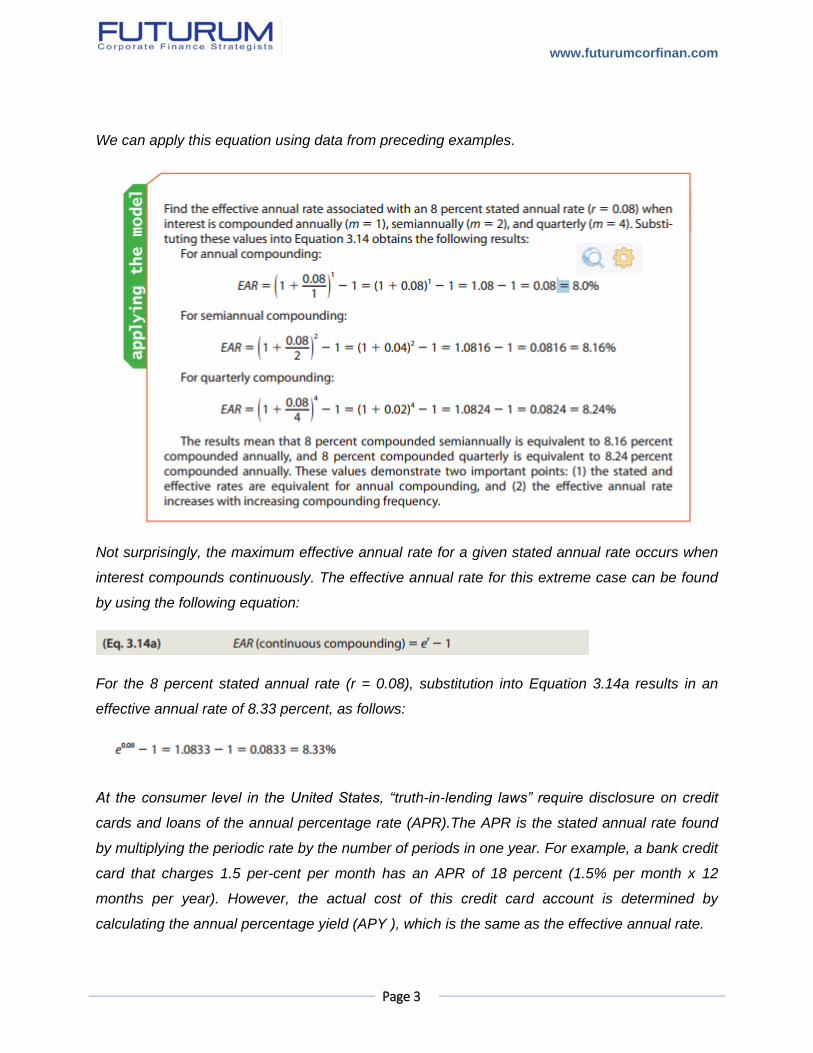

We can apply this equation using data from preceding examples.

Not surprisingly, the maximum effective annual rate for a given stated annual rate occurs when

interest compounds continuously. The effective annual rate for this extreme case can be found

by using the following equation:

For the 8 percent stated annual rate (r = 0.08), substitution into Equation 3.14a results in an

effective annual rate of 8.33 percent, as follows:

At the consumer level in the United States, “truth-in-lending laws” require disclosure on credit

cards and loans of the annual percentage rate (APR).The APR is the stated annual rate found

by multiplying the periodic rate by the number of periods in one year. For example, a bank credit

card that charges 1.5 per-cent per month has an APR of 18 percent (1.5% per month x 12

months per year). However, the actual cost of this credit card account is determined by

calculating the annual percentage yield (APY ), which is the same as the effective annual rate.

www.futurumcorfinan.com

Page 4

For the credit card example, 1.5 percent per month interest has an effective annual rate of

[(1.015)^12 – 1] = 0.1956, or 19.56 percent. If the stated rate is 1.75 percent per month, as is

the case with many U.S. credit card accounts, the APY is a whopping 23.14 percent. In other

words, if you are carrying a positive credit card balance with an interest rate like this, pay it off

as soon as possible!

Discussions

Unfortunately, most of these corporate finance textbooks just stop there without exploring

further and don’t even give words of caution to all those undergraduate students, which might

be the first time being exposed to the calculation of SAIR and EAIR.

There are two things I would like to “add” to the explanation of SAIR and EAIR.

First, the book doesn’t tell you that the “interest” is paid at the end of the period (known

as “in arrears”), and not at the beginning of the period (known as “in advance”).

In certain situation, the “interest” is collected in advance.

If this is the case, then how to calculate this periodic rate?

For instance,

Debt interest rate = 8% per annum

Quarters in one year = 4

Debt periodic interest rate?

Per textbook, it should be = (1+8%)^(1/4) -1 = 1.94%, since if we (1+1.94%)^4 - 1 = 8%.

To give you a bit expanded idea about this periodical interest rate, we have:

a) 8% per annum (this is effective rate compounded 1x)...and the question is how much

the effective rate for one year if it is compounded 4 times...then effective one year =

(1+8%/4)^4 - 1...Then we have 8.24% effective per year, or 2% per quarter.

b) 8% per annum is the effective rate for 4 times compounded, then per quarter,

(1+8%)^(1/4) -1 = 1.94% per quarter.

But, all above calculation as per textbook is standing on the assumption that the interest is

collected or paid at the end of the period/quarter, and not in advance or at the beginning of

the quarter.

www.futurumcorfinan.com

Page 5

Periodical interest rate in advance (= iPad) is determined as follows:

iPad = i/(1+i) and

i= iPad/(1-i_ad)

t=0 t=1

P P(1+i) at the end.

P(1-i_ad) P in advance

First case i = P(1+i)/P -1 = i (paid at the end of period).

Second case

i = P/P(1-i_ad) -1 = (P - P(1-i_ad))/[P(1-i_ad)] - 1 = i = iPad/(1-i_ad).

Or,

iPad = i/(1+i), then

i = iPad (1+i), then

i = iPad + iPad * i, then

i – (iPad * i) = iPad, then

i * (1 – iPad) = iPad, then

i = iPad/(1-i_ad)

The other way around,

iPad = i/(1+i)

So, if we put into the above example, the periodical/quarterly interest rate paid/collected in

advance is:

1 - (1/(1+8%)^(1/4)) = 1.91%, which if we compounded it four times (1+1.91%)^4- 1, we won't

get 8% per annum, as this interest is paid/collected in advance instead of in arrears.

www.futurumcorfinan.com

Page 6

As a recap, where:

i is periodical interest at the end of period, and

iPad is in advance.

If iPad=1.91% then i=1.947%

(1+i)^(1/4) is (1+i_periodical).

Second, by doing the conversion between compounding methods as explained in the

corporate finance textbooks, are they really “equivalent”?

I give one extreme example.

Suppose:

r1 is the annual rate with continuous compounding.

r2is the equivalent compounded m times per annum times per annum.

Then we have:

= (1 + r2/m)^m = e^r1

= r1 = m * ln (1 + r2/m), then

= r2 = m (e^(r1/m) – 1)

If we carefully look at the cash flows for this interest, then r1 and r2 above are based on

different cash flows, and in what financial sense, we could say that they are equivalent?

Think about it next time before just jumping to use all formulas given in the standard corporate

finance textbooks.

Ignacio Velez-Pareja (IVP) comments:

When you contract a loan, usually they specify the non-compounded rate (in Spanish, we say

nominal rate). However, if you have contracted the loan on a monthly or quarterly basis, then

you find the periodic rate (8%/12, 8%/4, etc.) It is this way of paying the interest that makes the

artificial compounded (we call it in Spanish, effective rate).

www.futurumcorfinan.com

Page 7

Hence, you have on a quarterly basis, 8% as non-compounded rate, 2% as a periodic

(quarterly) rate and the compounded rate. There is a very simple relationship between non-

compounded and periodical rates, as follows

1.Compounded: periodical rate times number of periods

2.Periodical; compounded rate /number of periods.

I don't give a penny for the compounded rate. That is a mathematical fiction. The most

relevant rate is the periodical rate (many people think it is the compounded rate and you could

tell me how many firms you know that pay interest on the basis of a compounded rate?) The

rate that should be used in WACC (for instance) should be the periodical. That one is the most

important rate, because that rate is the one you need to calculate the actual interest payment

and the sum of all those interest payments are what you deduct from the Income tax report.

Follow?

Hence,

If you have 8% per annum, compounded quarterly, you already know that the periodical is 2%.

That rate is the one the bank uses to calculate the interest you have to pay. The compounded is

(1+8%/4)^4-1= 8.2432%

BUT that 8.2432% has no real meaning. In fact, do you know that the assumption behind that

calculation is that you can save (or invest) exactly at the same rate you borrow money? It is as if

the bank has one window where it gives you the loan at, say 2% per quarter, and another one

where they pay you 2% per quarter. HOWEVER, that is true for the bank, because in

equilibrium, the money it receives from you is invested (most times) at the same rate you pay.

This is the considerations I give to my students:

Assume you have several people with different ways to "keep" the money and you will tell me

which is their opportunity cost.

They have two options: a) To pay a loan of 1,000 at the end of year with interest of 8% (you will

pay 1000+80 interest). b) to pay 20 per quarter and 1000 at the end of year. (20, 20, 20, 1020).

For instance:

1.Keeps the money in a safe box. Opportunity cost = 0%

2.Keeps the money in a savings account Opportunity cost 0.5% per month

www.futurumcorfinan.com

Page 8

3.Keeps the money in a CD Opportunity cost 1.2% per month

4.Keeps the money in a savings account Opportunity cost 2% per quarter

5.Keeps the money in a CD maturity 1 year Opportunity cost 8% per annum

6.Keeps the money in a savings account Opportunity cost 2.5% per quarter

If each of them contracts a loan to be paid quarterly at (% per annum with quarterly payments of

2% interest).

What each individual will prefer, a) or b)?. The capitalized cost is as said, 8.2432% per annum.

Will that loan cost the same to all of them? Figure out the case of the person with his money in

the safe box: will it cost more if she pays the loan in a lump sum at the end of the year (1,080)

or if she pays 20, 20, 20, 1020?.

The assumption in the compounded rate is that it is the same for ALL of them: 8.2432% per

annum. Is that true? Will it cost more or less for case 6? For case 1? For case 5?

Would you say that the extra cost of paying a) or b) is the same for all of them? I think it

is not the same and yet, the compounded rate is the same for all!!!

Karnen:

Ignacio, interesting, as you showed above that they have two options:

a) To pay a loan of 1,000 at the end of year with interest of 8% (you will pay 1000+80 interest).

b) To pay 20 per quarter and 1000 at the end of year. (20, 20, 20, 1020).

I don't think that two options could have the same interest rate, the risk of cash flows could be

different as far as I could see, with option b) looks safer, yet the compounded rate as the

textbooks taught us, that the rates for both options are the same.

IVP:

Dear Karnen

I see you are picking the most fictional case! Perpetuities!

However, that continuous interest applies to formulas such as the Black-Scholes model for

financial options.

www.futurumcorfinan.com

Page 9

This is a cash flow that you receive instantaneously, every Nano second. Can you even imagine

that?

Yet, I have seen, occasionally, a bank offering that interest rate. The difference with a practical

daily rate is nil.

It is a mathematical conception that exists only in the imagination. It says the effective rate of a

non-compounded rate of, say, 12% per annum, compounded instantaneously. It is as if money

were a liquid that flows through a Cane into your bank account. Just science fiction.

Note: The first perpetuities were issued in the 12th century in Italy, France and Spain. They

were initially and intentionally to circumvent the usury laws of the Catholic Church. that is

because no loan principal repayment, they were not considered as loans.

~~~~~~ ####### ~~~~~~

www.futurumcorfinan.com

Page 10

Disclaimer

This material was produced by and the opinions expressed are those of FUTURUM as of the date of

writing and are subject to change. The information and analysis contained in this publication have been

compiled or arrived at from sources believed to be reliable but FUTURUM does not make any

representation as to their accuracy or completeness and does not accept liability for any loss arising from

the use hereof. This material has been prepared for general informational purposes only and is not

intended to be relied upon as accounting, tax, or other professional advice. Please refer to your advisors

for specific advice.

This document may not be reproduced either in whole, or in part, without the written permission of the

authors and FUTURUM. For any questions or comments, please post it at www.futurumcorfinan.com

© FUTURUM. All Rights Reserved