Embed Size (px)

Citation preview

The hidden treasure of high frequency dynamics:

from intrinsic time to 12 new scaling laws

Richard Olsen

OLSENLiquidity Investing

Dec 2009 2The intrinsic time framework

OLSENLiquidity Investing

Information content of tick data

Intrinsic time: event-based approach

12 new scaling laws

Outlook

Outline

Conclusion

Dec 2009 3The intrinsic time framework

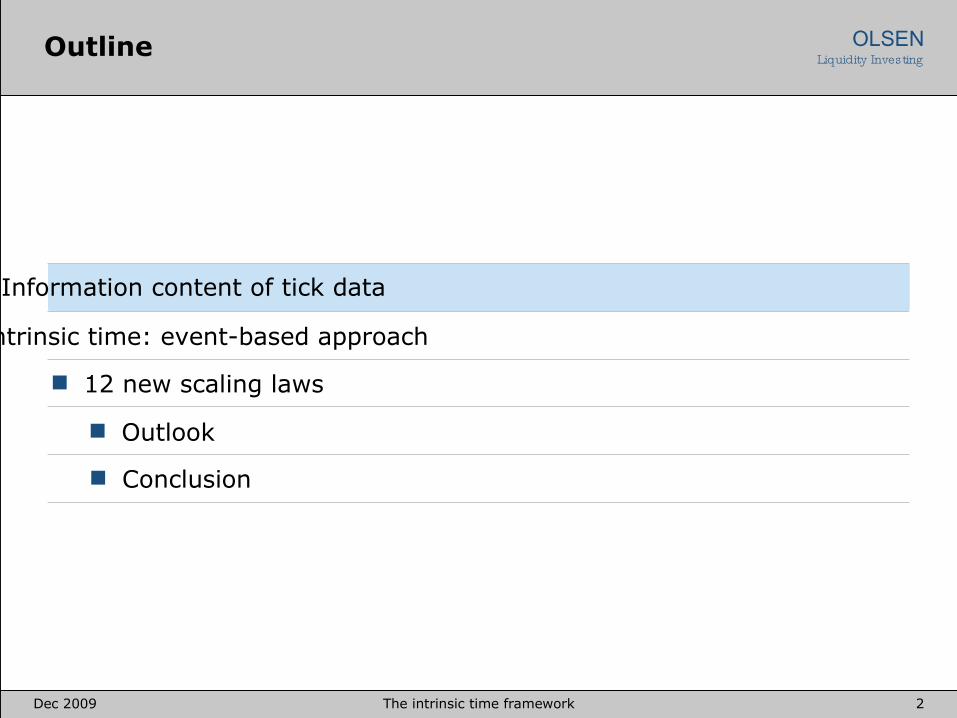

OLSENLiquidity InvestingYou only see what you look at

Daily Data High-Frequency Data

1 day 1 25‘000

1 year 250 5‘000‘000

10 years 2‘500 50‘000‘000

100 years 25’000 500’000’000

Within a 24 hour time window, the world is more or less the same, so one day of tick data is more valuable than 100 years of daily data.

One day of high frequency tick by tick data is equivalent 100 years of daily data.

Dec 2009 4The intrinsic time framework

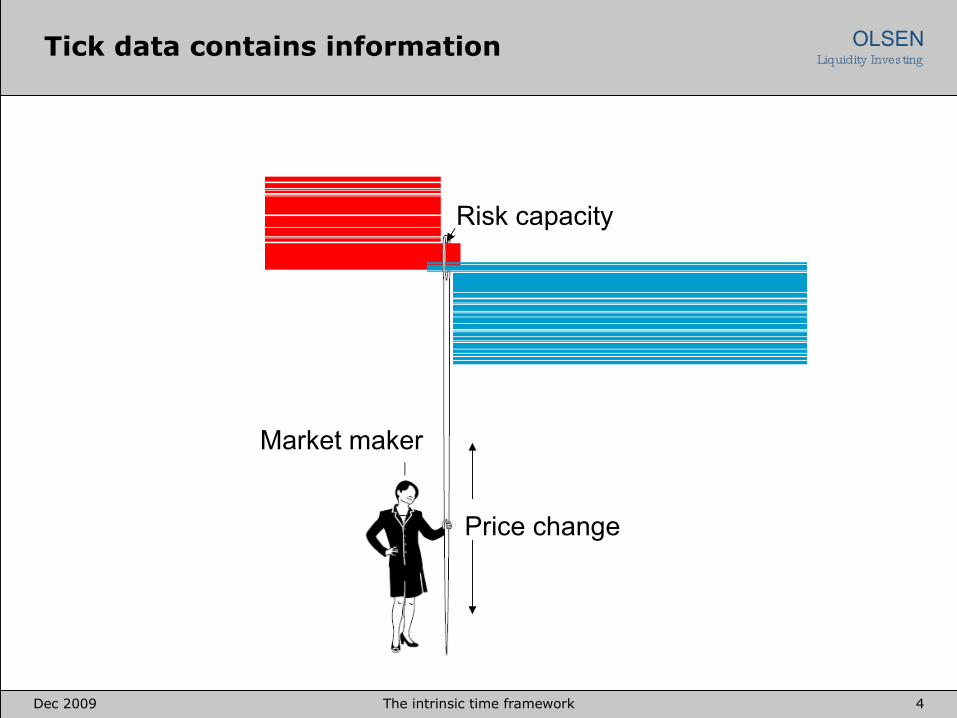

OLSENLiquidity InvestingTick data contains information

Risk capacity

Market maker

Price change

Dec 2009 5The intrinsic time framework

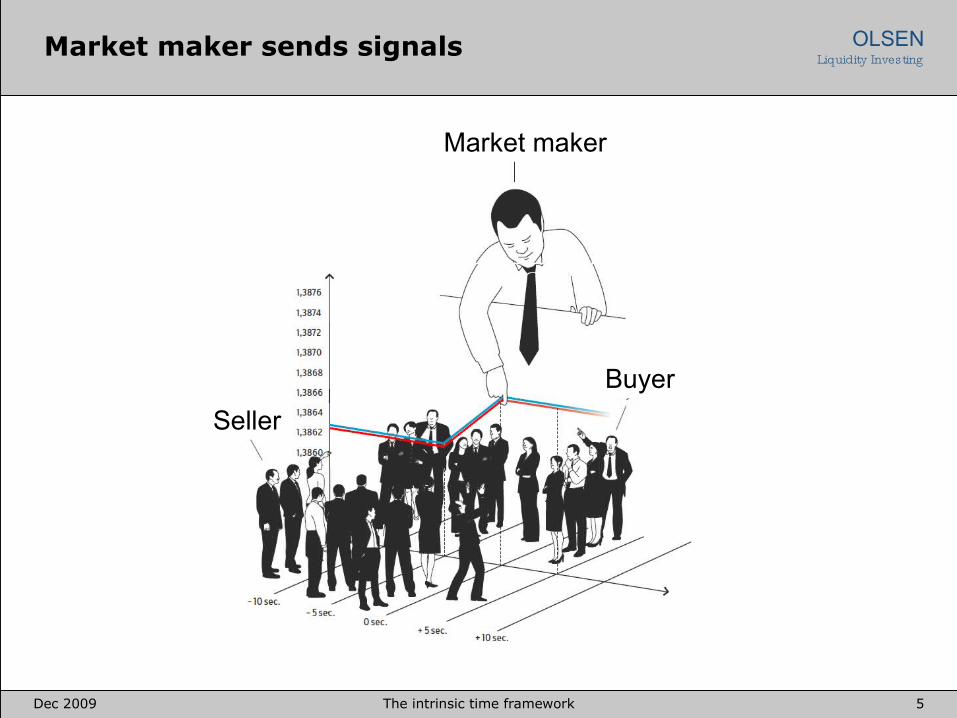

OLSENLiquidity InvestingMarket maker sends signals

Market maker

Buyer

Seller

Dec 2009 6The intrinsic time framework

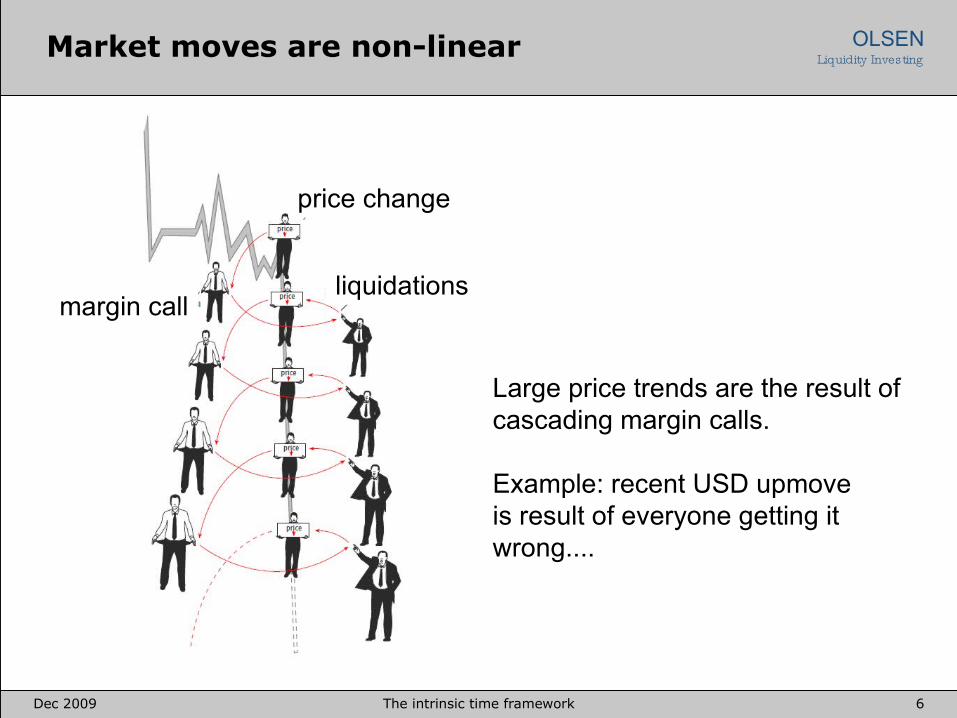

OLSENLiquidity InvestingMarket moves are non-linear

price change

liquidationsmargin call

Large price trends are the result of cascading margin calls.

Example: recent USD upmoveis result of everyone getting it wrong....

Dec 2009 7The intrinsic time framework

OLSENLiquidity Investing

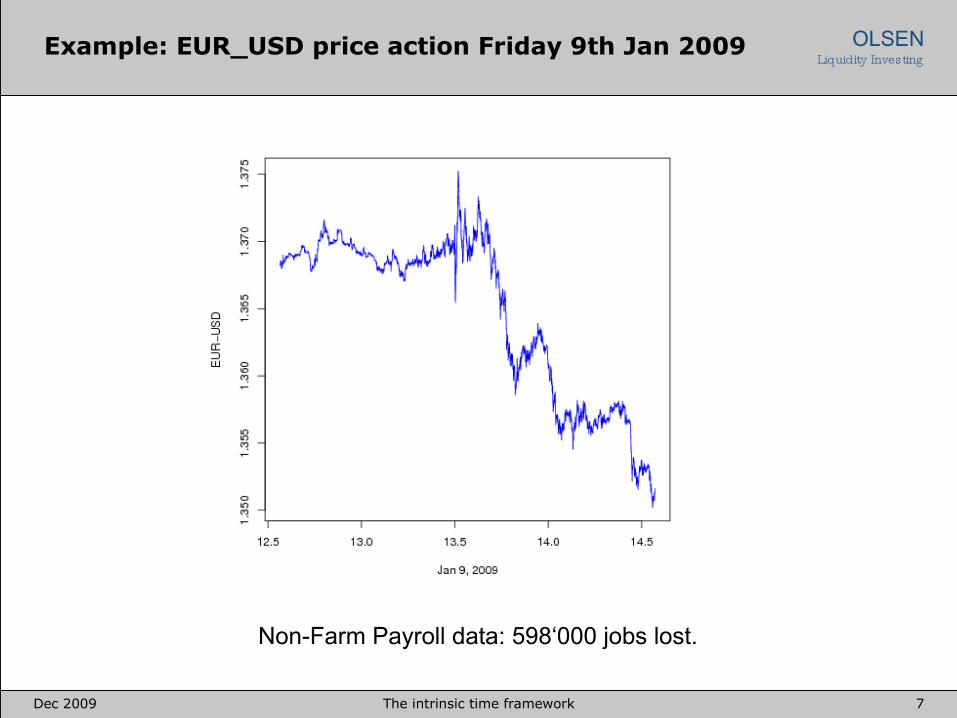

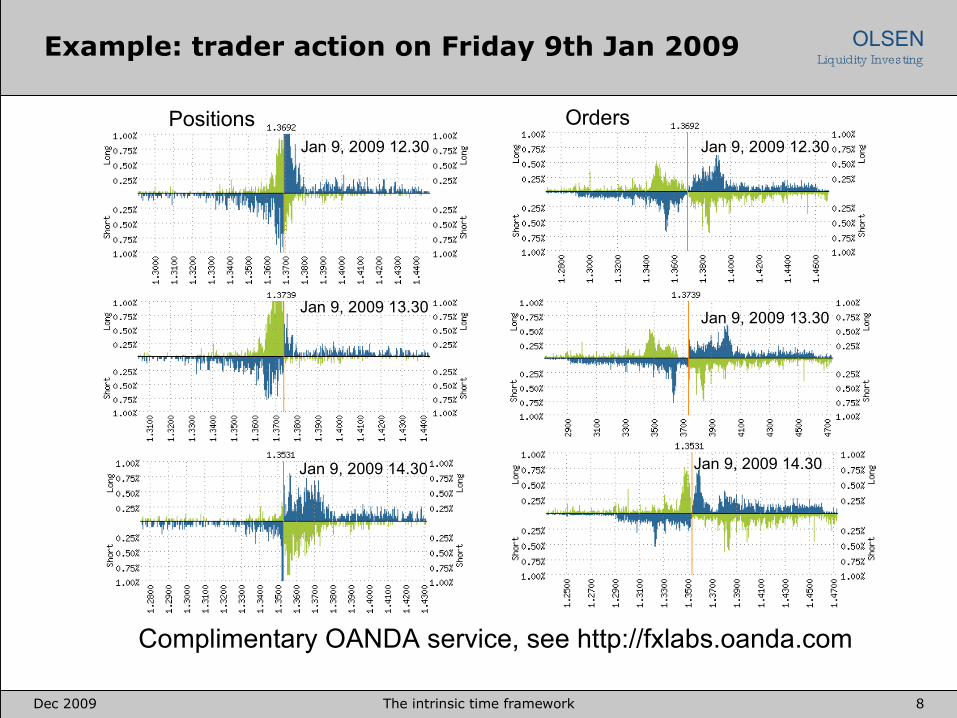

Example: EUR_USD price action Friday 9th Jan 2009

Non-Farm Payroll data: 598‘000 jobs lost.

Dec 2009 8The intrinsic time framework

OLSENLiquidity InvestingExample: trader action on Friday 9th Jan 2009

OrdersPositionsJan 9, 2009 12.30

Jan 9, 2009 13.30

Jan 9, 2009 14.30

Jan 9, 2009 12.30

Jan 9, 2009 13.30

Jan 9, 2009 14.30

Complimentary OANDA service, see http://fxlabs.oanda.com

Dec 2009 9The intrinsic time framework

OLSENLiquidity Investing

Information content of tick data

Intrinsic time: event-based approach

Scaling laws

Outlook

Outline

Conclusion

Dec 2009 10The intrinsic time framework

OLSENLiquidity InvestingEUR-USD, Nov 21 2008, daily return

A significant part of the activity is disregarded

Dec 2009 11The intrinsic time framework

OLSENLiquidity InvestingEUR-USD, Nov 21 2008, daily return

Some activity is still disregarded, especially in the afternoon

Dec 2009 12The intrinsic time framework

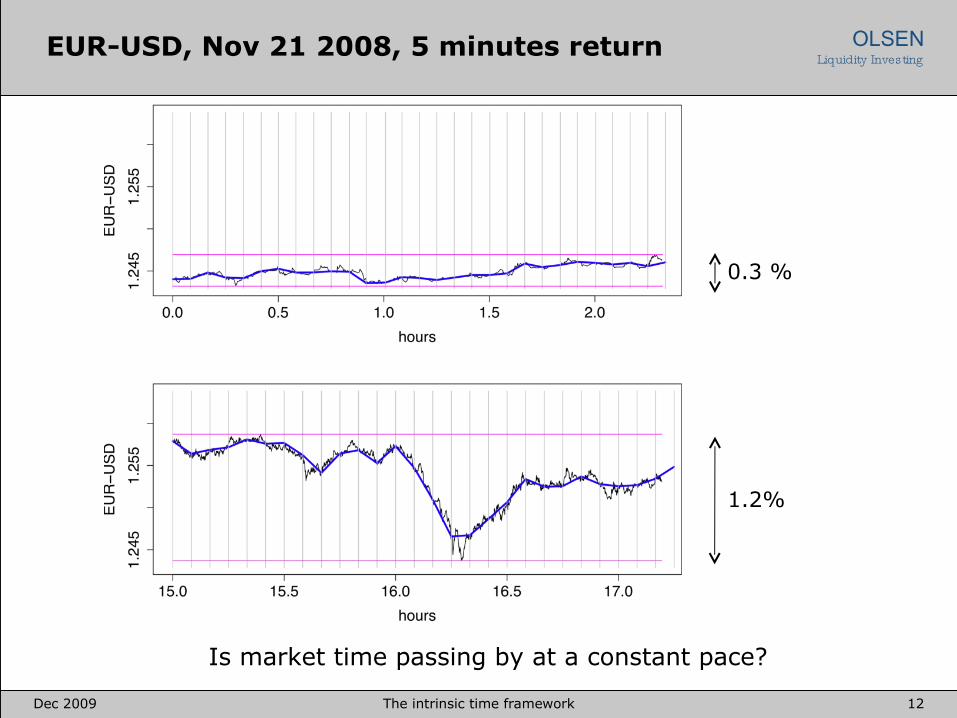

OLSENLiquidity InvestingEUR-USD, Nov 21 2008, 5 minutes return

0.3 %

1.2%

Is market time passing by at a constant pace?

Dec 2009 13The intrinsic time framework

OLSENLiquidity InvestingIn need of an event-based approach?

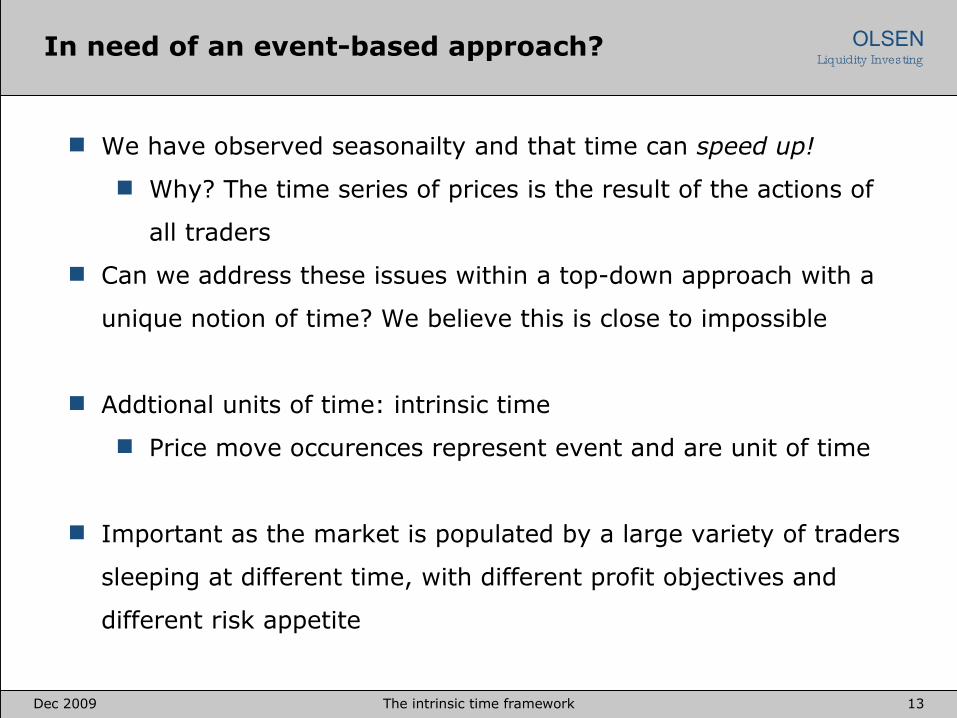

We have observed seasonailty and that time can speed up!

Why? The time series of prices is the result of the actions of

all traders

Can we address these issues within a top-down approach with a

unique notion of time? We believe this is close to impossible

Addtional units of time: intrinsic time

Price move occurences represent event and are unit of time

Important as the market is populated by a large variety of traders

sleeping at different time, with different profit objectives and

different risk appetite

Dec 2009 14The intrinsic time framework

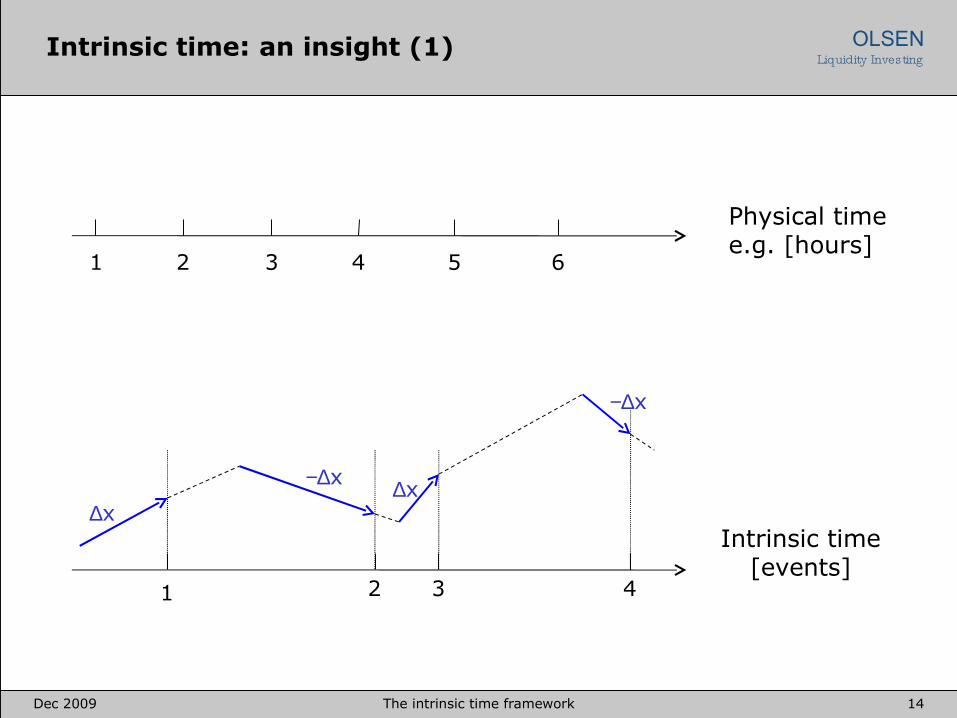

OLSENLiquidity InvestingIntrinsic time: an insight (1)

Physical timee.g. [hours]

1 2 3 4 5 6

Intrinsic time[events]

1 2 3 4

∆x

−∆x

−∆x

∆x

Dec 2009 15The intrinsic time framework

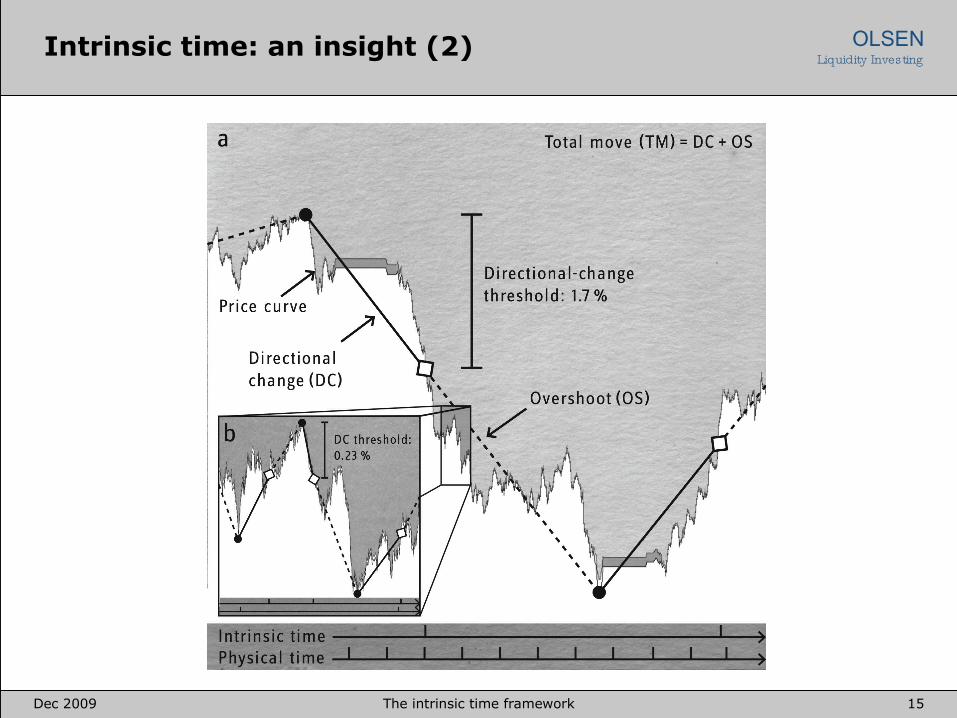

OLSENLiquidity InvestingIntrinsic time: an insight (2)

Dec 2009 16The intrinsic time framework

OLSENLiquidity InvestingIntrinsic time: pros and cons

Pros:

Full activity at a given price scales is observed

Seasonality and herding can be handled

Overshoot sections quantify the departure from the current price

level

Map how market participants see the market

Cope with the discountinuous nature of the market

Cons:

Relation to physical time and to price scales need to be

established

Volatility has to be defined

Dec 2009 17The intrinsic time framework

OLSENLiquidity Investing

Information content of tick data

Intrinsic time: event-based approach

Scaling laws

Outlook

Outline

Conclusion

Dec 2009 18The intrinsic time framework

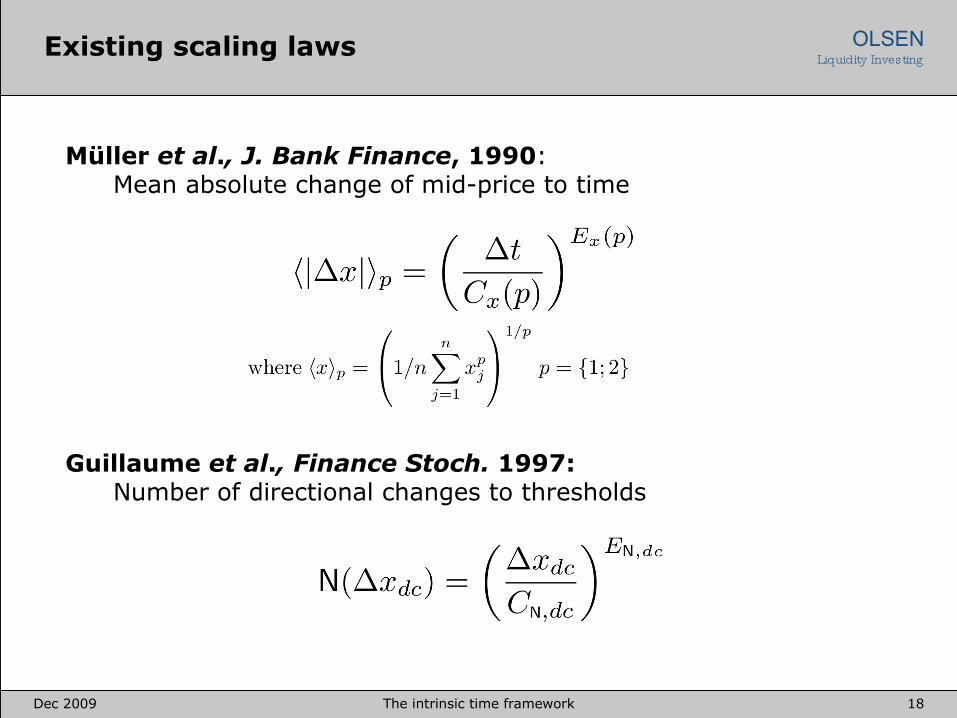

OLSENLiquidity InvestingExisting scaling laws

Müller et al., J. Bank Finance, 1990: Mean absolute change of mid-price to time

Guillaume et al., Finance Stoch. 1997:Number of directional changes to thresholds

Dec 2009 19The intrinsic time framework

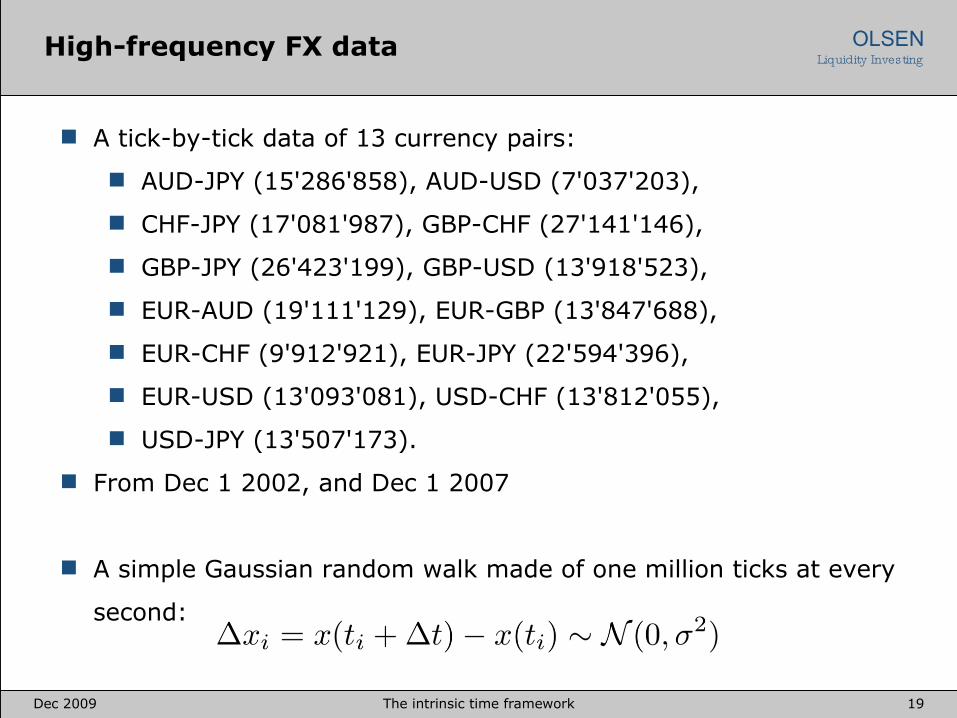

OLSENLiquidity InvestingHigh-frequency FX data

A tick-by-tick data of 13 currency pairs:

AUD-JPY (15'286'858), AUD-USD (7'037'203),

CHF-JPY (17'081'987), GBP-CHF (27'141'146),

GBP-JPY (26'423'199), GBP-USD (13'918'523),

EUR-AUD (19'111'129), EUR-GBP (13'847'688),

EUR-CHF (9'912'921), EUR-JPY (22'594'396),

EUR-USD (13'093'081), USD-CHF (13'812'055),

USD-JPY (13'507'173).

From Dec 1 2002, and Dec 1 2007

A simple Gaussian random walk made of one million ticks at every

second:

Dec 2009 20The intrinsic time framework

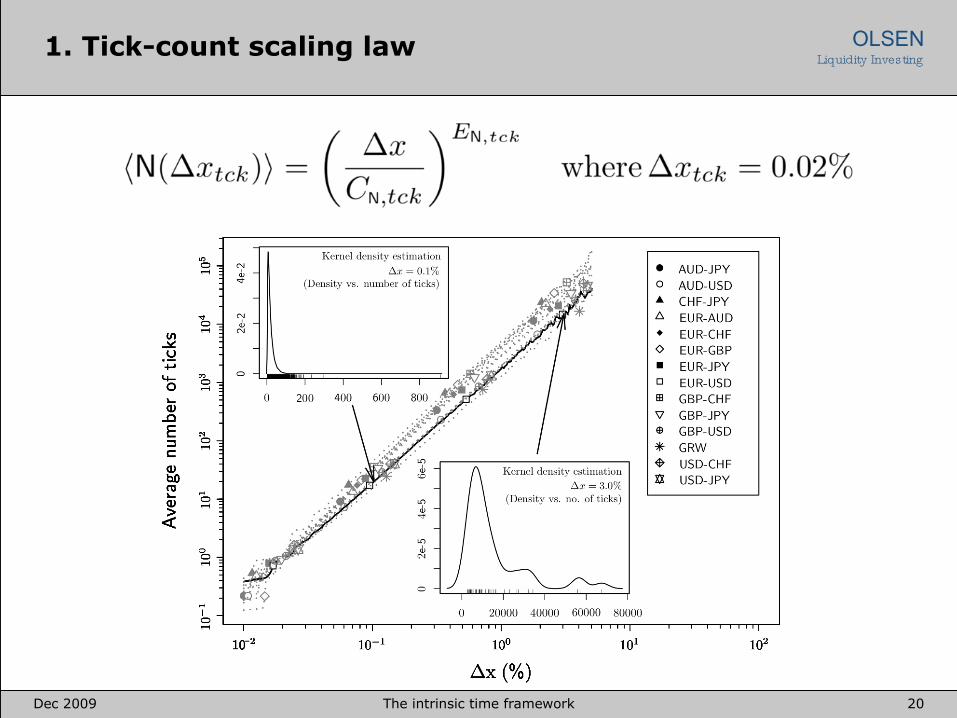

OLSENLiquidity Investing1. Tick-count scaling law

Dec 2009 21The intrinsic time framework

OLSENLiquidity InvestingOther laws at a glance (1)

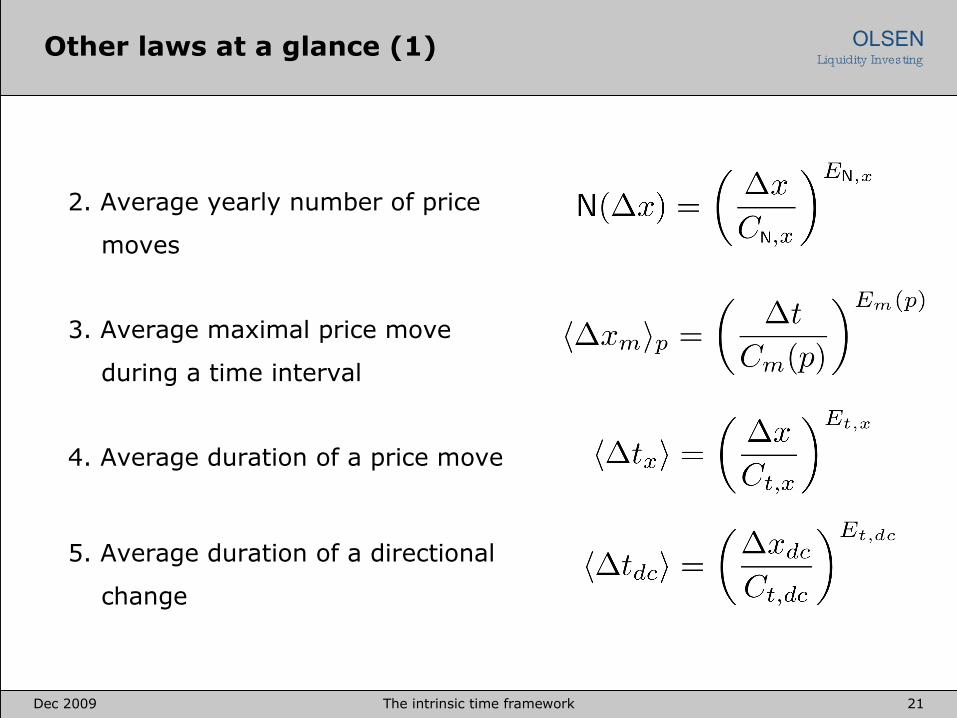

2. Average yearly number of price

moves

3. Average maximal price move

during a time interval

4. Average duration of a price move

5. Average duration of a directional

change

Dec 2009 22The intrinsic time framework

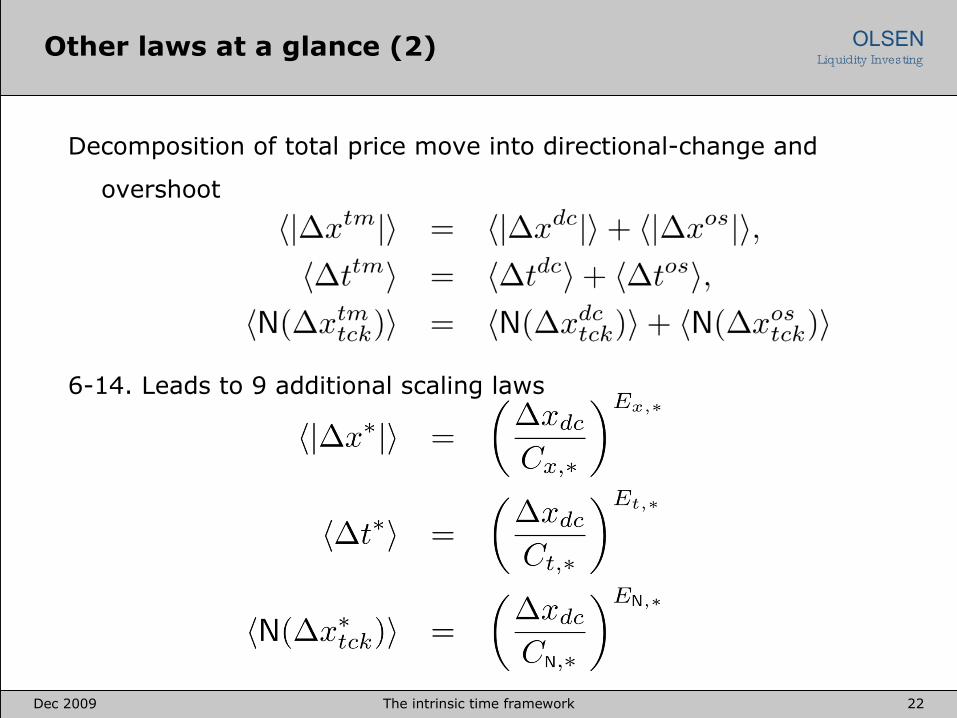

OLSENLiquidity InvestingOther laws at a glance (2)

Decomposition of total price move into directional-change and

overshoot

6-14. Leads to 9 additional scaling laws

Dec 2009 23The intrinsic time framework

OLSENLiquidity InvestingOther laws at a glance (3)

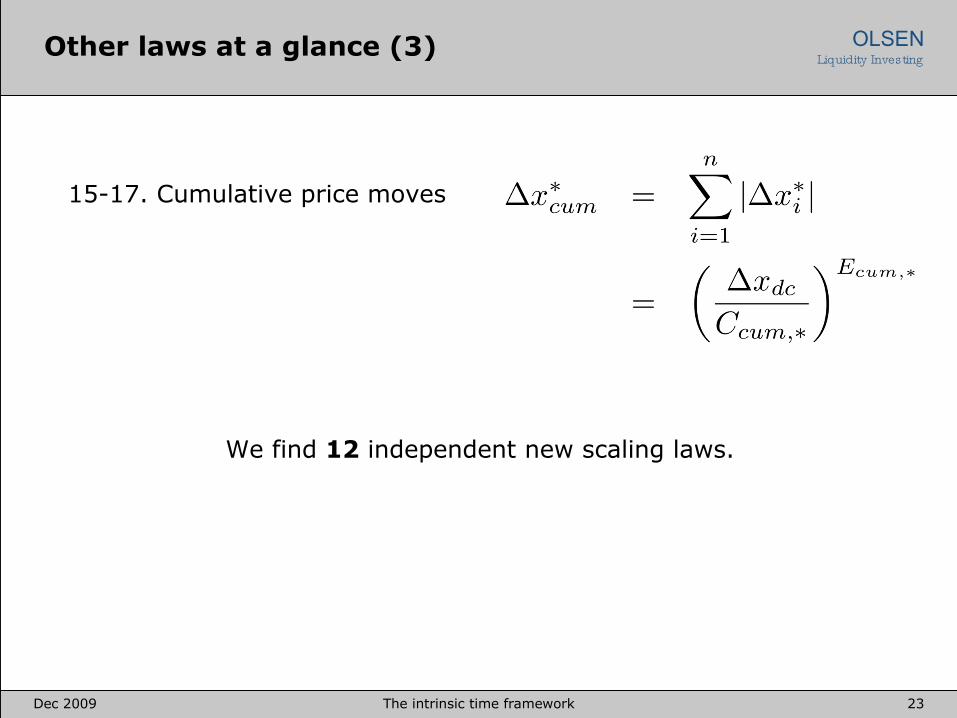

15-17. Cumulative price moves

We find 12 independent new scaling laws.

Dec 2009 24The intrinsic time framework

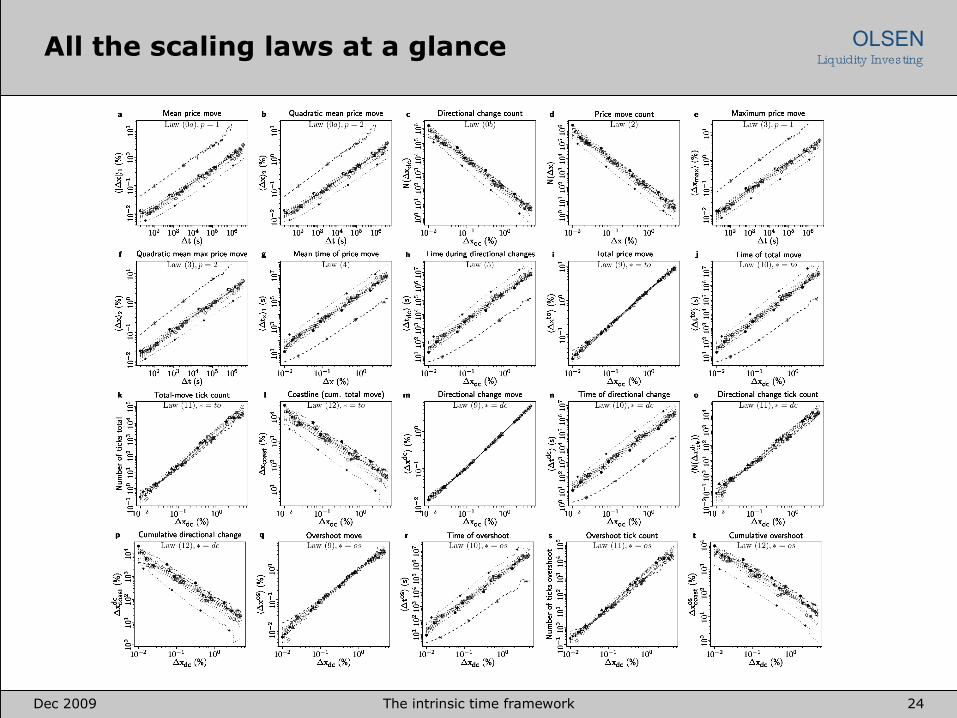

OLSENLiquidity InvestingAll the scaling laws at a glance

Dec 2009 25The intrinsic time framework

OLSENLiquidity InvestingThe coastline of prices (1)

The coastline associated to a price scale is the sum of all price

moves of a given price scale.

Why is it important?

quantifies the profit potential

allows for active management of positions

A variation (transaction costs taken into account) of the total

move scaling law allows us to estimate its average length

0.05%: 1604%

0.1%: 1463%

1%: 161%

5%: 34.5%

The GRW shows up to a factor 2 times smaller coastline

Dec 2009 26The intrinsic time framework

OLSENLiquidity InvestingThe coastline of prices (2)

For 0.05% threshold, daily length: EUR-CHF 1.8%, AUD-JPY 9.1%

The coastline measures on average 6.4% per day

On average, daily a mean maximal move of 0.6% is observed

On average it takes 220 days to observe a 6.4% price move

Dec 2009 27The intrinsic time framework

OLSENLiquidity Investing

Information content of tick data

Intrinsic time: event-based approach

Scaling laws

Outlook

Outline

Conclusion

Dec 2009 28The intrinsic time framework

OLSENLiquidity InvestingOutlook (1)

Sparsity of data to explain macro trends

Treasure of tick by tick data: resource for model building

Comprehensive data repository of observed and synthetic data

Self-similar model building

Intrinsic time approach

Dec 2009 29The intrinsic time framework

OLSENLiquidity InvestingOutlook (2)

Call to action: global economic crisis

Global information system

Collaboration

Data repository

Descriptive economics

Actual deliverables: real time services

Dec 2009 30The intrinsic time framework

OLSENLiquidity Investing

Motivation

Intrinsic time: event-based approach

Scaling laws

Outlook

Outline

Conclusion

Dec 2009 31The intrinsic time framework

OLSENLiquidity InvestingFinance as the next computer technology

· other industries have succeeded, why not economics and finance?

· human beings, complexity, unforeseen events.

· high frequency finance, new concepts, significant financial resouces.

· Yes, it is feasible · Thank you.

Dec 2009 32The intrinsic time framework

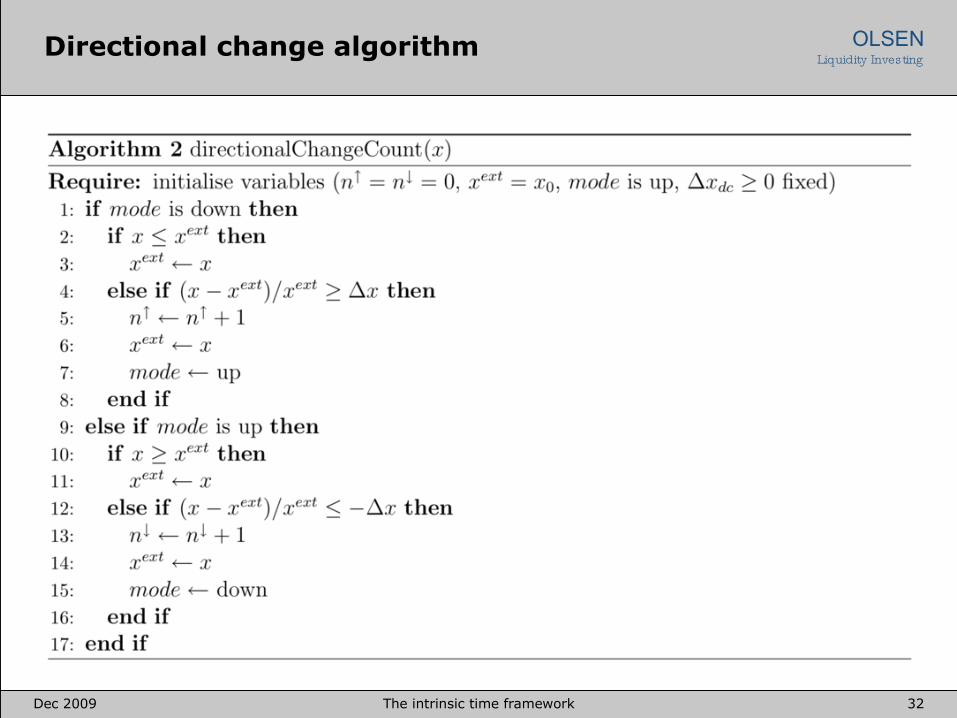

OLSENLiquidity InvestingDirectional change algorithm

Dec 2009 33The intrinsic time framework

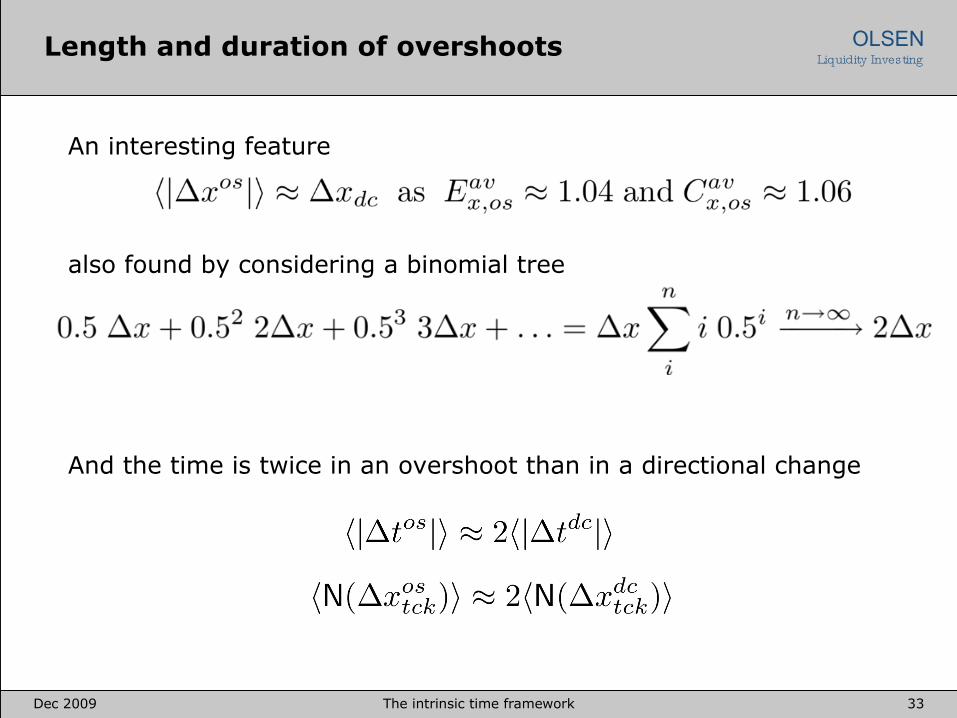

OLSENLiquidity InvestingLength and duration of overshoots

An interesting feature

also found by considering a binomial tree

And the time is twice in an overshoot than in a directional change

Dec 2009 34The intrinsic time framework

OLSENLiquidity InvestingComparison with a GRW

A GRW has strikingly similar properties than the average

properties of the market data

Noticable difference: average maximum price move is 8 times

larger than observed with the market data

Duration of price move

Exponent 0.500 when p=2

Average exponent 0.457 for market data, p=2

It is not 0.500 for any other law

Dec 2009 35The intrinsic time framework

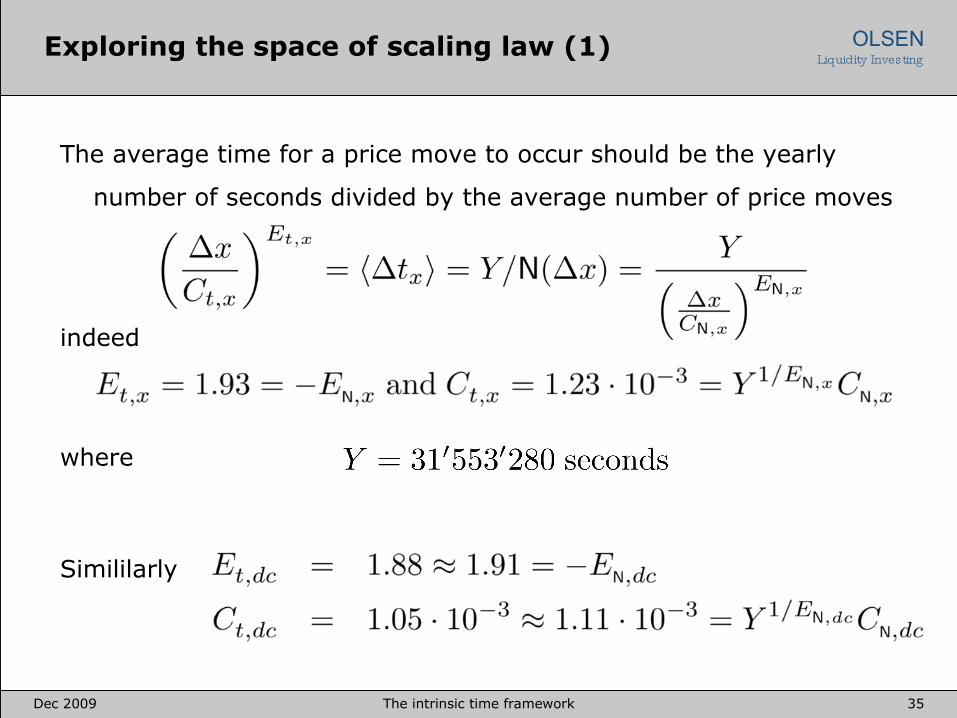

OLSENLiquidity InvestingExploring the space of scaling law (1)

where

Simililarly

The average time for a price move to occur should be the yearly

number of seconds divided by the average number of price moves

indeed

Dec 2009 36The intrinsic time framework

OLSENLiquidity InvestingExploring the space of scaling law (2)

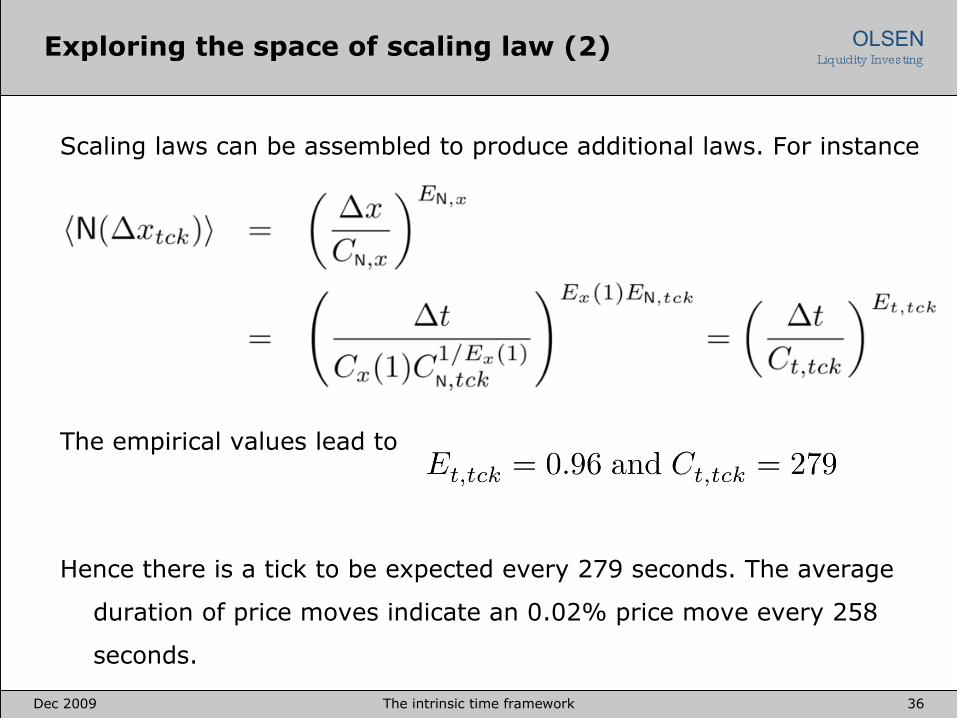

The empirical values lead to

Hence there is a tick to be expected every 279 seconds. The average

duration of price moves indicate an 0.02% price move every 258

seconds.

Scaling laws can be assembled to produce additional laws. For instance