Embed Size (px)

Citation preview

India : Economic Growth (GDP)July-Sept 2014

FINALYTIKSINDIA-in-FOCUS

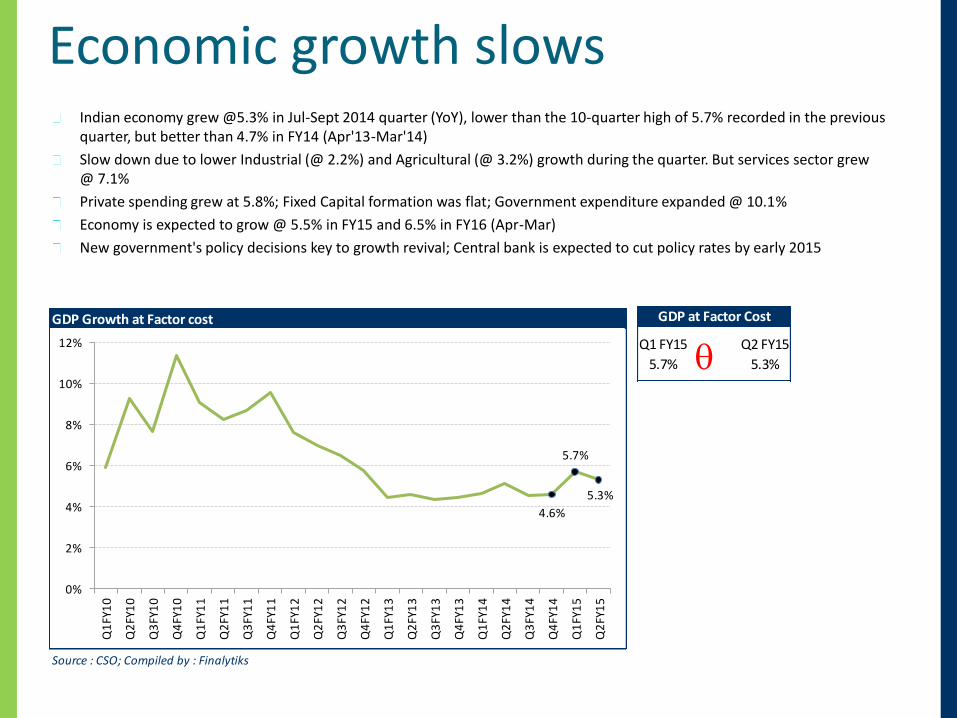

Economic growth slowsIndian economy grew @5.3% in Jul-Sept 2014 quarter (YoY), lower than the 10-quarter high of 5.7% recorded in the previous quarter, but better than 4.7% in FY14 (Apr'13-Mar'14)

Slow down due to lower Industrial (@ 2.2%) and Agricultural (@ 3.2%) growth during the quarter. But services sector grew @ 7.1%

Private spending grew at 5.8%; Fixed Capital formation was flat; Government expenditure expanded @ 10.1%

Economy is expected to grow @ 5.5% in FY15 and 6.5% in FY16 (Apr-Mar)

New government's policy decisions key to growth revival; Central bank is expected to cut policy rates by early 2015

GDP Growth at Factor cost

Source : CSO; Compiled by : Finalytiks

4.6%

5.7%

5.3%

0%

2%

4%

6%

8%

10%

12%

Q1

FY1

0

Q2

FY1

0

Q3

FY1

0

Q4

FY1

0

Q1

FY1

1

Q2

FY1

1

Q3

FY1

1

Q4

FY1

1

Q1

FY1

2

Q2

FY1

2

Q3

FY1

2

Q4

FY1

2

Q1

FY1

3

Q2

FY1

3

Q3

FY1

3

Q4

FY1

3

Q1

FY1

4

Q2

FY1

4

Q3

FY1

4

Q4

FY1

4

Q1

FY1

5

Q2

FY1

5

Q1 FY15 Q2 FY15

5.7% 5.3%q

GDP at Factor Cost

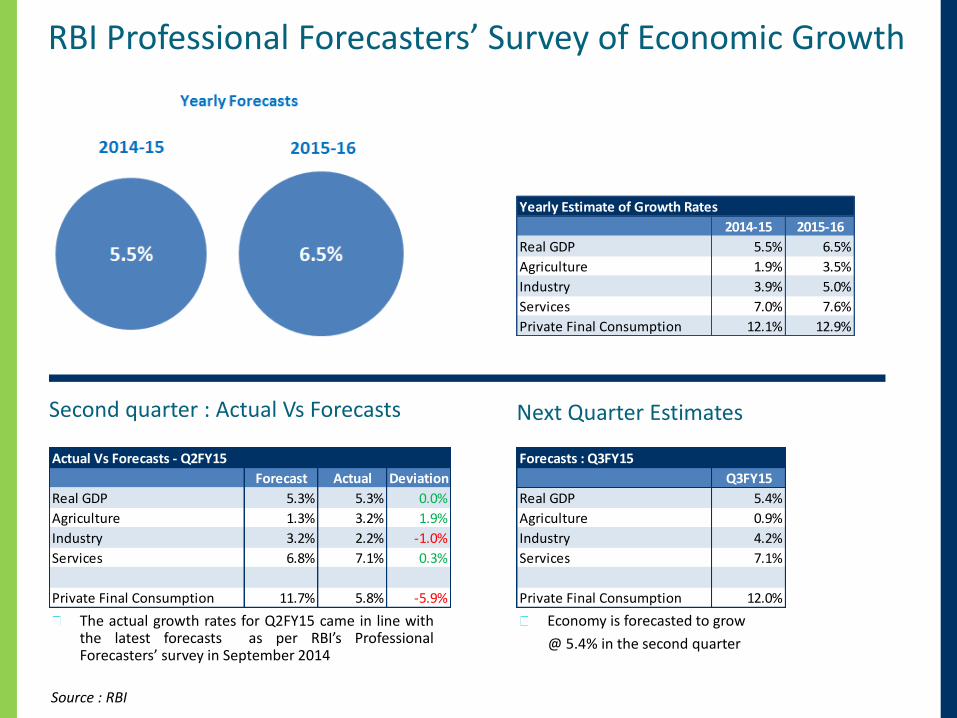

RBI Professional Forecasters’ Survey of Economic Growth

Second quarter : Actual Vs Forecasts

The actual growth rates for Q2FY15 came in line withthe latest forecasts as per RBI’s ProfessionalForecasters’ survey in September 2014

Source : RBI

Economy is forecasted to grow

@ 5.4% in the second quarter

Next Quarter Estimates

Yearly Estimate of Growth Rates

2014-15 2015-16

Real GDP 5.5% 6.5%

Agriculture 1.9% 3.5%

Industry 3.9% 5.0%

Services 7.0% 7.6%

Private Final Consumption 12.1% 12.9%

Actual Vs Forecasts - Q2FY15

Forecast Actual Deviation

Real GDP 5.3% 5.3% 0.0%

Agriculture 1.3% 3.2% 1.9%

Industry 3.2% 2.2% -1.0%

Services 6.8% 7.1% 0.3%

Private Final Consumption 11.7% 5.8% -5.9%

Forecasts : Q3FY15

Q3FY15

Real GDP 5.4%

Agriculture 0.9%

Industry 4.2%

Services 7.1%

Private Final Consumption 12.0%

Key trigger events to watch forGovernment policies will determine the course of India’s growth

The change of government has given a fillip to investor confidence in India. The policy decisions on the much awaitedeconomic reforms (infrastructure, mining & financial sector) are going to be the key trigger points for the Indian economy.Apart from these, the budget to be presented by end of February 2015 is one of the most eagerly awaited events in the nextone year

The central bank’s (RBI) decision on the policy rates is a much awaited event. It kept the policy rates unchanged in the latestpolicy review meeting, but sounded dovish. Inflation is below RBI’s Jan 2015 target of 8%. The central bank is concernedabout upside risks to its inflation target. The market widely expects deep cuts in policy rates starting H1 CY15

12-month moving average of GDP growth, points to mild recovery after bottoming out in early 2014

GDP growth at Factor cost & 12-Month Moving Average

Source : CSO; Compiled by : Finalytiks

5.3%

5.0%

4%

5%

6%

7%

8%

9%

10%

11%

12%

Q1

FY1

0

Q2

FY1

0

Q3

FY1

0

Q4

FY1

0

Q1

FY1

1

Q2

FY1

1

Q3

FY1

1

Q4

FY1

1

Q1

FY1

2

Q2

FY1

2

Q3

FY1

2

Q4

FY1

2

Q1

FY1

3

Q2

FY1

3

Q3

FY1

3

Q4

FY1

3

Q1

FY1

4

Q2

FY1

4

Q3

FY1

4

Q4

FY1

4

Q1

FY1

5

Q2

FY1

5

GDP at factor cost 12-Month Moving Average

Economy slows

Q1 FY15 Q2 FY15 Q1 FY15 Q2 FY15

5.7% 5.3% 5.9% 6.0%

Q1 FY15 Q2 FY15 Q1 FY15 Q2 FY15 Q1 FY15 Q2 FY15

3.8% 3.2% 4.2% 2.2% 6.8% 7.1%

Q1 FY15 Q2 FY15 Q1 FY15 Q2 FY15 Q1 FY15 Q2 FY15

8.8% 10.1% 5.6% 5.8% 7.0% 0.0%

Q1 FY15 Q2 FY15 Q1 FY15 Q2 FY15 Q1 FY15 Q2 FY15

11.5% -1.6% -0.4% 1.1% -30.2% 13.4%

Imports Net Exports (Negative)

p

Gross Domestic Product Growth - Current Vs. Previous QuarterGDP at Factor Cost GDP at Market Price

Economic Activity Based Classification (at Factor cost)Agriculture & Allied Industry Services

q p

q pq

p p q

q p

Expenditure Based Classification (at Market prices)

Government Final

Consumption Expenditure

Private Final

Consumption Expenditure

Gross Fixed

Capital Formation

Exports

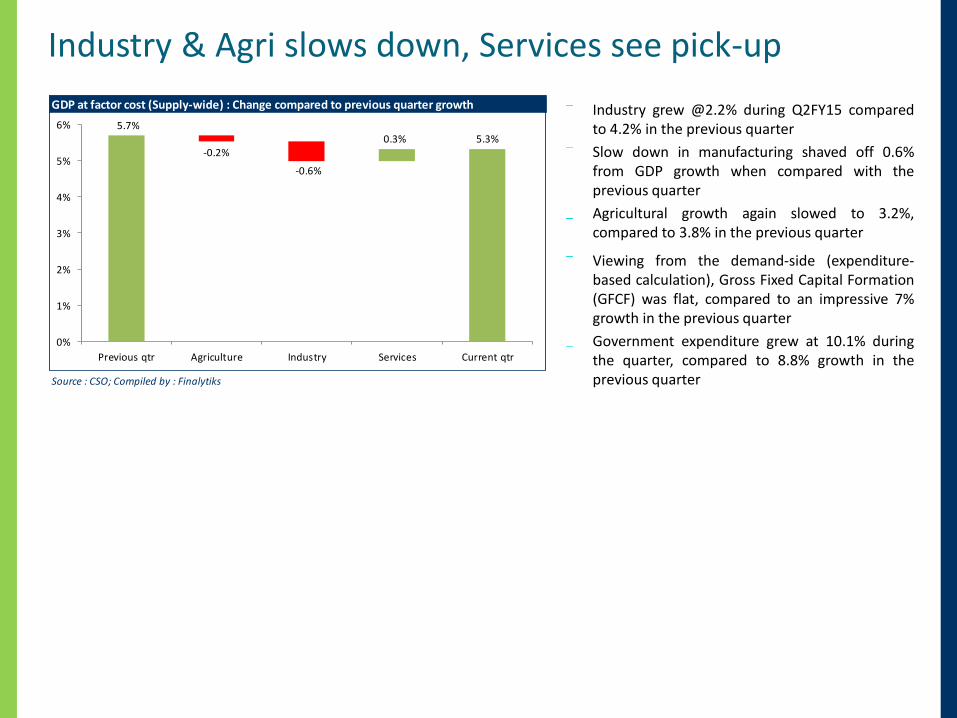

Industry & Agri slows down, Services see pick-up

Industry grew @2.2% during Q2FY15 comparedto 4.2% in the previous quarter

Slow down in manufacturing shaved off 0.6%from GDP growth when compared with theprevious quarter

Agricultural growth again slowed to 3.2%,compared to 3.8% in the previous quarter

Viewing from the demand-side (expenditure-based calculation), Gross Fixed Capital Formation(GFCF) was flat, compared to an impressive 7%growth in the previous quarter

Government expenditure grew at 10.1% duringthe quarter, compared to 8.8% growth in theprevious quarter

GDP at factor cost (Supply-wide) : Change compared to previous quarter growth

Source : CSO; Compiled by : Finalytiks

5.7%

-0.2%

-0.6%

0.3% 5.3%

0%

1%

2%

3%

4%

5%

6%

Previous qtr Agriculture Industry Services Current qtr

GDP : at factor cost (Supply-side)Agriculture grew @3.2% compared to 3.8% in the previousquarter. This is slightly lower than the CAGR of 3.9% overthe past 10 years

Industry grew @2.2% compared to 4.2% in the previousquarter, way lower than 10-year CAGR of 6.6%

Services sector continued to support the economicgrowth, and grew @7.1% during the quarter, compared to6.8% during the previous quarter. But again, this is lowerthan 10-year CAGR of 8.9%

Agriculture growth (YoY %)

Source : CSO; Compiled by : Finalytiks

6.3%

3.8%

3.2%

-2%

0%

2%

4%

6%

8%

10%

12%

14%

Q1

FY1

0

Q2

FY1

0

Q3

FY1

0

Q4

FY1

0

Q1

FY1

1

Q2

FY1

1

Q3

FY1

1

Q4

FY1

1

Q1

FY1

2

Q2

FY1

2

Q3

FY1

2

Q4

FY1

2

Q1

FY1

3

Q2

FY1

3

Q3

FY1

3

Q4

FY1

3

Q1

FY1

4

Q2

FY1

4

Q3

FY1

4

Q4

FY1

4

Q1

FY1

5

Q2

FY1

5

Industrial growth (YoY %)

Source : CSO; Compiled by : Finalytiks

-0.2%

4.2%

2.2%

-2%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

Q1

FY1

0

Q2

FY1

0

Q3

FY1

0

Q4

FY1

0

Q1

FY1

1

Q2

FY1

1

Q3

FY1

1

Q4

FY1

1

Q1

FY1

2

Q2

FY1

2

Q3

FY1

2

Q4

FY1

2

Q1

FY1

3

Q2

FY1

3

Q3

FY1

3

Q4

FY1

3

Q1

FY1

4

Q2

FY1

4

Q3

FY1

4

Q4

FY1

4

Q1

FY1

5

Q2

FY1

5

Services growth (YoY %)

Source : CSO; Compiled by : Finalytiks

6.4%6.8%

7.1%

0%

2%

4%

6%

8%

10%

12%

14%

Q1

FY1

0

Q2

FY1

0

Q3

FY1

0

Q4

FY1

0

Q1

FY1

1

Q2

FY1

1

Q3

FY1

1

Q4

FY1

1

Q1

FY1

2

Q2

FY1

2

Q3

FY1

2

Q4

FY1

2

Q1

FY1

3

Q2

FY1

3

Q3

FY1

3

Q4

FY1

3

Q1

FY1

4

Q2

FY1

4

Q3

FY1

4

Q4

FY1

4

Q1

FY1

5

Q2

FY1

5

GDP : Sector wiseServices sector, representing >60% of theeconomy, contributed 4.4% out of total growth of5.3%. That is roughly 83% contribution out oftotal growth

Industry, representing ~26% of the economy,contributed 0.6% to the total growth

Agriculture contributed 0.4% to GDP growth. Itrepresents ~11% of the economy

Contribution to Total GDP growth by each sector

Source : CSO; Compiled by : Finalytiks

4.5% 4.6%4.4% 4.4% 4.7%

5.2%

4.6% 4.6%

5.7%5.3%

-1%

0%

1%

2%

3%

4%

5%

6%

7%

Q1FY13 Q2FY13 Q3FY13 Q4FY13 Q1FY14 Q2FY14 Q3FY14 Q4FY14 Q1FY15 Q2FY15

Agriculture & allied Industry Services GDP at factor cost

Sector wise composition of GDP in second quarter of Financial year

Agriculture Industry Services

10.8% 25.9% 63.3%

Source : CSO; Compiled by : Finalytiks

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Q2FY05 Q2FY06 Q2FY07 Q2FY08 Q2FY09 Q2FY10 Q2FY11 Q2FY12 Q2FY13 Q2FY14 Q2FY15

GDP : Industrial GrowthManufacturing growth was @0.1% compared to 3.5%. Theprevious quarter growth was the highest in the past 10quarters

Construction grew @4.6% compared to 4.8% in the previousquarter

Electricity, Gas & Water supply slowed to 8.7%, compared to10.2% in the previous quarter. The previous quarter growthwas the highest in the past 3 years

Mining grew @1.9%, compared to 2.1% in the previousquarter. Mining continued to grow for two quarters, aftercontracting for 8 consecutive quarters

Manufacturing growth (YoY %)

Source : CSO; Compiled by : Finalytiks

-1.4%

3.5%

0.1%

-0.2%

4.2%2.2%

-5%

0%

5%

10%

15%

20%

25%

Q1

FY1

0

Q2

FY1

0

Q3

FY1

0

Q4

FY1

0

Q1

FY1

1

Q2

FY1

1

Q3

FY1

1

Q4

FY1

1

Q1

FY1

2

Q2

FY1

2

Q3

FY1

2

Q4

FY1

2

Q1

FY1

3

Q2

FY1

3

Q3

FY1

3

Q4

FY1

3

Q1

FY1

4

Q2

FY1

4

Q3

FY1

4

Q4

FY1

4

Q1

FY1

5

Q2

FY1

5

Manufacturing Industry

Construction growth (YoY %)

Source : CSO; Compiled by : Finalytiks

0.7%

4.8% 4.6%

-0.2%

4.2%

2.2%

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

Q1

FY1

0

Q2

FY1

0

Q3

FY1

0

Q4

FY1

0

Q1

FY1

1

Q2

FY1

1

Q3

FY1

1

Q4

FY1

1

Q1

FY1

2

Q2

FY1

2

Q3

FY1

2

Q4

FY1

2

Q1

FY1

3

Q2

FY1

3

Q3

FY1

3

Q4

FY1

3

Q1

FY1

4

Q2

FY1

4

Q3

FY1

4

Q4

FY1

4

Q1

FY1

5

Q2

FY1

5Construction Industry

Mining & Electricity growth (YoY %)

Source : CSO; Compiled by : Finalytiks

-0.4%

2.1% 1.9%

7.2%

10.2%

8.7%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

Q1

FY1

0

Q2

FY1

0

Q3

FY1

0

Q4

FY1

0

Q1

FY1

1

Q2

FY1

1

Q3

FY1

1

Q4

FY1

1

Q1

FY1

2

Q2

FY1

2

Q3

FY1

2

Q4

FY1

2

Q1

FY1

3

Q2

FY1

3

Q3

FY1

3

Q4

FY1

3

Q1

FY1

4

Q2

FY1

4

Q3

FY1

4

Q4

FY1

4

Q1

FY1

5

Q2

FY1

5

Mining & Quarrying Electricity, Gas & Water supply

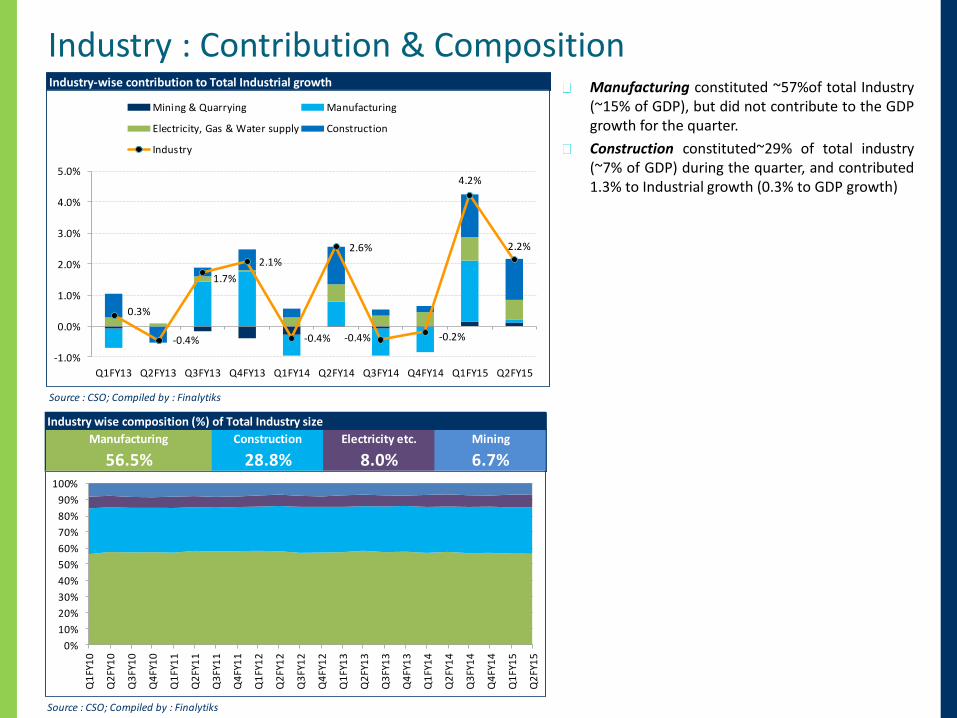

Industry : Contribution & CompositionManufacturing constituted ~57%of total Industry(~15% of GDP), but did not contribute to the GDPgrowth for the quarter.

Construction constituted~29% of total industry(~7% of GDP) during the quarter, and contributed1.3% to Industrial growth (0.3% to GDP growth)

Industry-wise contribution to Total Industrial growth

Source : CSO; Compiled by : Finalytiks

0.3%

-0.4%

1.7%

2.1%

-0.4%

2.6%

-0.4% -0.2%

4.2%

2.2%

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

Q1FY13 Q2FY13 Q3FY13 Q4FY13 Q1FY14 Q2FY14 Q3FY14 Q4FY14 Q1FY15 Q2FY15

Mining & Quarrying Manufacturing

Electricity, Gas & Water supply Construction

Industry

Industry wise composition (%) of Total Industry size

Manufacturing Construction Electricity etc. Mining

56.5% 28.8% 8.0% 6.7%

Source : CSO; Compiled by : Finalytiks

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Q1

FY1

0

Q2

FY1

0

Q3

FY1

0

Q4

FY1

0

Q1

FY1

1

Q2

FY1

1

Q3

FY1

1

Q4

FY1

1

Q1

FY1

2

Q2

FY1

2

Q3

FY1

2

Q4

FY1

2

Q1

FY1

3

Q2

FY1

3

Q3

FY1

3

Q4

FY1

3

Q1

FY1

4

Q2

FY1

4

Q3

FY1

4

Q4

FY1

4

Q1

FY1

5

Q2

FY1

5

GDP : Services sectorTrade, Hotels, Transport & Communication slowed downto 3.8% YoY. The sector has been slowing since Q1FY12,and has grown below 5% in 11 out of the past 13 quarters

Finance, Insurance, Real estate & Business services slowedto 9.5%, compared to 10.4% in the previous quarter. Thissector is one of the fastest growing sectors. The sector hasgrown at above 10% for 32 out of the past 38 quarters(since the beginning of 2004-05 series). Current quartergrowth is the lowest in the past 14 quarters

Community, Social & Personal services grew @9.6%compared to 9.1% in the previous quarter. This is in linewith increase in government spending of 10.1% during thequarter

Trade, Hotels, Transport, Communication

Source : CSO; Compiled by : Finalytiks

3.9%

2.8%

3.8%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

Q1

FY1

0

Q2

FY1

0

Q3

FY1

0

Q4

FY1

0

Q1

FY1

1

Q2

FY1

1

Q3

FY1

1

Q4

FY1

1

Q1

FY1

2

Q2

FY1

2

Q3

FY1

2

Q4

FY1

2

Q1

FY1

3

Q2

FY1

3

Q3

FY1

3

Q4

FY1

3

Q1

FY1

4

Q2

FY1

4

Q3

FY1

4

Q4

FY1

4

Q1

FY1

5

Q2

FY1

5

Finance, Insurance, Real estate, Business services

Source : CSO; Compiled by : Finalytiks

12.4%

10.4%

9.5%

0%

2%

4%

6%

8%

10%

12%

14%

16%

Q1

FY1

0

Q2

FY1

0

Q3

FY1

0

Q4

FY1

0

Q1

FY1

1

Q2

FY1

1

Q3

FY1

1

Q4

FY1

1

Q1

FY1

2

Q2

FY1

2

Q3

FY1

2

Q4

FY1

2

Q1

FY1

3

Q2

FY1

3

Q3

FY1

3

Q4

FY1

3

Q1

FY1

4

Q2

FY1

4

Q3

FY1

4

Q4

FY1

4

Q1

FY1

5

Q2

FY1

5

Community, Social & Personal services

Source : CSO; Compiled by : Finalytiks

3.3%

9.1%9.6%

-5%

0%

5%

10%

15%

20%

Q1

FY1

0

Q2

FY1

0

Q3

FY1

0

Q4

FY1

0

Q1

FY1

1

Q2

FY1

1

Q3

FY1

1

Q4

FY1

1

Q1

FY1

2

Q2

FY1

2

Q3

FY1

2

Q4

FY1

2

Q1

FY1

3

Q2

FY1

3

Q3

FY1

3

Q4

FY1

3

Q1

FY1

4

Q2

FY1

4

Q3

FY1

4

Q4

FY1

4

Q1

FY1

5

Q2

FY1

5

Services Sector : Contribution & Composition

Trade, Hotels, Transport & Communicationcontributed 1.6% out of the total services sectorgrowth of 7.1%. Despite having the highestweight among services sector (~42% of servicessector), it was the lowest contributor to growthamong the three services sectors. The sectorconstitutes 27% of the GDP and contributed just1% to GDP growth.

Financing, Insurance, Real estate & Businessservices continued to contribute strongly togrowth, contributing 3.2% to services sectorgrowth. This sector was also the top contributorto GDP growth, adding 2% out of the GDP growthof 5.3%. Since the slowdown of Trade etc., fromFY 2011-12, Financing etc. has been the topcontributor to GDP growth

Community, Social & Personal servicescontributed 2.2% to services sector growth and1.3% to total GDP growth (constitutes ~23% ofservices; ~15% of GDP).

Contribution to Services sector growth

Source : CSO; Compiled by : Finalytiks

7.2%

6.3%

7.2%

6.4%6.8% 7.1%

0%

1%

2%

3%

4%

5%

6%

7%

8%

Q1FY13 Q2FY13 Q3FY13 Q4FY13 Q1FY14 Q2FY14

Trade, Hotels, Transpt & Communi Finance, Insur, Real est & Bus serv

Community, Social & Personal Serv Services

Composition of Services Sector

Trade, Hotels, Transport & Financing, Insurance, Real Community, Social &

Communication Estate & Business Services Personal Services

42.2% 34.8% 23.0%

Source : CSO; Compiled by : Finalytiks

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Q1

FY1

0

Q2

FY1

0

Q3

FY1

0

Q4

FY1

0

Q1

FY1

1

Q2

FY1

1

Q3

FY1

1

Q4

FY1

1

Q1

FY1

2

Q2

FY1

2

Q3

FY1

2

Q4

FY1

2

Q1

FY1

3

Q2

FY1

3

Q3

FY1

3

Q4

FY1

3

Q1

FY1

4

Q2

FY1

4

Q3

FY1

4

Q4

FY1

4

Q1

FY1

5

Q2

FY1

5

GDP – Quarterly Growth : Supply-side Sector wise GDP Growth (at Factor Cost)

Q1FY13 Q2FY13 Q3FY13 Q4FY13 Q1FY14 Q2FY14 Q3FY14 Q4FY14 Q1FY15 Q2FY15

Agriculture, Forestry & Fishing 1.8% 1.8% 0.8% 1.6% 4.0% 5.0% 3.7% 6.3% 3.8% 3.2%

Mining & Quarrying -1.1% -0.1% -2.0% -4.8% -3.9% 0.0% -1.2% -0.4% 2.1% 1.9%

Manufacturing -1.1% 0.0% 2.5% 3.0% -1.2% 1.3% -1.5% -1.4% 3.5% 0.1%

Electricity, Gas & Water Supply 4.2% 1.3% 2.6% 0.9% 3.8% 7.8% 5.0% 7.2% 10.2% 8.7%

Construction 2.8% -1.9% 1.0% 2.4% 1.1% 4.4% 0.6% 0.7% 4.8% 4.6%

Total Industry 0.3% -0.4% 1.7% 2.1% -0.4% 2.6% -0.4% -0.2% 4.2% 2.2%

Trade, Hotels, Transport & Communication 4.0% 5.6% 5.9% 4.8% 1.6% 3.6% 2.9% 3.9% 2.8% 3.8%

Financing, Insurance, Real Estate & Business Services 11.7% 10.6% 10.2% 11.2% 12.9% 12.1% 14.1% 12.4% 10.4% 9.5%

Community, Social & Personal Services 7.6% 7.4% 4.0% 2.8% 10.6% 3.6% 5.7% 3.3% 9.1% 9.6%

Total Services 7.2% 7.6% 6.9% 6.3% 7.2% 6.3% 7.2% 6.4% 6.8% 7.1%

GDP At Factor Cost 4.5% 4.6% 4.4% 4.4% 4.7% 5.2% 4.6% 4.6% 5.7% 5.3%

Red highlight means that growth rate has improved compared to the previous quarter, Green highlight indicates that it has decreased

Sector wise contribution to GDP Growth (at Factor Cost)Q1FY13 Q2FY13 Q3FY13 Q4FY13 Q1FY14 Q2FY14 Q3FY14 Q4FY14 Q1FY15 Q2FY15

Agriculture, Forestry & Fishing 0.3% 0.2% 0.1% 0.2% 0.5% 0.6% 0.6% 0.9% 0.5% 0.4%

Mining & Quarrying 0.0% 0.0% 0.0% -0.1% -0.1% 0.0% 0.0% 0.0% 0.0% 0.0%

Manufacturing -0.2% 0.0% 0.4% 0.5% -0.2% 0.2% -0.2% -0.2% 0.5% 0.0%

Electricity, Gas & Water Supply 0.1% 0.0% 0.0% 0.0% 0.1% 0.2% 0.1% 0.1% 0.2% 0.2%

Construction 0.2% -0.1% 0.1% 0.2% 0.1% 0.3% 0.0% 0.1% 0.4% 0.3%

Total Industry contribution to GDP 0.1% -0.1% 0.5% 0.6% -0.1% 0.7% -0.1% -0.1% 1.1% 0.6%

Trade, Hotels, Transport & Communication 1.1% 1.5% 1.5% 1.3% 0.4% 1.0% 0.8% 1.1% 0.7% 1.0%

Financing, Insurance, Real Estate And Business Services 2.1% 2.0% 1.8% 1.9% 2.5% 2.4% 2.6% 2.3% 2.2% 2.0%

Community, Social & Personal Services 0.9% 1.0% 0.5% 0.4% 1.3% 0.5% 0.7% 0.4% 1.1% 1.3%

Total Services sector contribution to GDP 4.1% 4.5% 3.8% 3.6% 4.2% 3.9% 4.0% 3.8% 4.1% 4.4%

GDP At Factor Cost (Total) 4.5% 4.6% 4.4% 4.4% 4.7% 5.2% 4.6% 4.6% 5.7% 5.3%

Red highlight means that contribution to GDP growth rate has improved compared to the previous quarter, Green highlight indicates that it has decreased

Source : CSO; Compiled by : Finalytiks

GDP – Yearly Growth : Supply-side Sector wise GDP Growth (at Factor Cost)

Industry/Items 2006-07 2007-08 2008-09 2009-10 2010-11 2011-12 2012-13 2013-14

Agriculture, Forestry & Fishing 4.2% 5.8% 0.1% 0.8% 8.6% 5.0% 1.4% 4.7%

Mining & Quarrying 7.5% 3.7% 2.1% 5.9% 6.5% 0.1% -2.2% -1.4%

Manufacturing 14.3% 10.3% 4.3% 11.3% 8.9% 7.4% 1.1% -0.7%

Electricity, Gas & Water Supply 9.3% 8.3% 4.6% 6.2% 5.3% 8.4% 2.3% 5.9%

Construction 10.3% 10.8% 5.3% 6.7% 5.7% 10.8% 1.1% 1.6%

Total Industry 12.2% 9.7% 4.4% 9.2% 7.6% 7.8% 1.0% 0.4%

Trade, Hotels, Transport & Communication 11.6% 10.9% 7.5% 10.4% 12.2% 4.3% 5.1% 3.0%

Financing, Insurance, Real Estate And Business Services 14.0% 12.0% 12.0% 9.7% 10.0% 11.3% 10.9% 12.9%

Community, Social & Personal Services 2.8% 6.9% 12.5% 11.7% 4.2% 4.9% 5.3% 5.6%

Total Services 10.1% 10.3% 10.0% 10.5% 9.7% 6.6% 7.0% 6.8%

GDP At Factor Cost 9.6% 9.3% 6.7% 8.6% 8.9% 6.7% 4.5% 4.7%

Red highlight means that growth rate has improved compared to the previous year, Green highlight indicates that it has decreased

Sector wise contribution to GDP Growth (at Factor Cost)2006-07 2007-08 2008-09 2009-10 2010-11 2011-12 2012-13 2013-14

Agriculture, Forestry & Fishing 0.8% 1.0% 0.0% 0.1% 1.3% 0.7% 0.2% 0.7%

Mining & Quarrying 0.2% 0.1% 0.1% 0.1% 0.2% 0.0% 0.0% 0.0%

Manufacturing 2.2% 1.6% 0.7% 1.8% 1.4% 1.2% 0.2% -0.1%

Electricity, Gas & Water Supply 0.2% 0.2% 0.1% 0.1% 0.1% 0.2% 0.0% 0.1%

Construction 0.8% 0.9% 0.4% 0.5% 0.4% 0.8% 0.1% 0.1%

Total Industry contribution to GDP 3.4% 2.8% 1.3% 2.6% 2.1% 2.2% 0.3% 0.1%

Trade, Hotels, Transport & Communication 2.9% 2.8% 1.9% 2.7% 3.2% 1.2% 1.4% 0.8%

Financing, Insurance, Real Estate And Business Services 2.1% 1.9% 1.9% 1.6% 1.7% 2.0% 2.0% 2.5%

Community, Social & Personal Services 0.4% 0.9% 1.6% 1.5% 0.6% 0.6% 0.7% 0.7%

Total Services sector contribution to GDP 5.4% 5.5% 5.4% 5.9% 5.5% 3.8% 4.0% 4.0%

GDP At Factor Cost (Total) 9.6% 9.3% 6.7% 8.6% 8.9% 6.7% 4.5% 4.7%

Red highlight means that contribution to GDP growth rate has improved compared to the previous year, Green highlight indicates that it has decreased

Source : CSO; Compiled by : Finalytiks

GDP : Expenditure (Demand-side)

Government spending increased by 10.1% during thequarter, compared to 8.8% in the previous quarter.Government expenditure constituted ~11% of theeconomy

Private consumption continued to disappoint with aslow growth of 5.8% compared to 5.6% recorded in theprevious quarter. Private consumption constituted~60% of GDP

Gross Fixed Capital Formation was flat, compared to avery impressive 7% in the previous quarter

Contribution of each demand-side component to Total GDP growth (at Market Price)

Source : CSO; Compiled by : Finalytiks

4.2% 5.2%

4.4%

6.1% 5.9% 6.0%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

Q1FY13 Q2FY13 Q3FY13 Q4FY13 Q1FY14 Q2FY14

Government FCE Private FCE Gross Fixed CF

Change in stock Valuables Net exports

Discrepancies GDP at market prices

Composition of GDP from Demand (expenditure) side

Source : CSO; Compiled by : Finalytiks

-20%

0%

20%

40%

60%

80%

100%

120%

-20%

0%

20%

40%

60%

80%

100%

120%

20

09-1

0: Q

1

20

09-1

0: Q

2

20

09-1

0: Q

3

20

09-1

0: Q

4

20

10-1

1: Q

1

20

10-1

1: Q

2

20

10-1

1: Q

3

20

10-1

1: Q

4

20

11-1

2: Q

1

20

11-1

2: Q

2

20

11-1

2: Q

3

20

11-1

2: Q

4

20

12-1

3: Q

1

20

12-1

3: Q

2

20

12-1

3: Q

3

20

12-1

3: Q

4

20

13-1

4: Q

1

20

13-1

4: Q

2

20

13-1

4: Q

3

20

13-1

4: Q

4

20

14-1

5: Q

1

20

14-1

5: Q

2

Government FCE Private FCE Gross Fixed Capital Formation Others Net exports

Q1 FY15 Q2 FY15 Q1 FY15 Q2 FY15 Q1 FY15 Q2 FY15

8.8% 10.1% 5.6% 5.8% 7.0% 0.0%

Q1 FY15 Q2 FY15 Q1 FY15 Q2 FY15 Q1 FY15 Q2 FY15

11.5% -1.6% -0.4% 1.1% -30.2% 13.4%

Imports Net Exports (Negative)

p

p p q

q p

Expenditure Based Classification (at Market prices)

Government Final

Consumption Expenditure

Private Final

Consumption Expenditure

Gross Fixed

Capital Formation

Exports

GDP : Government expenditureGovernment expenditure picked up furtherduring the quarter

Higher government expenditure had a positiveimpact on Community, Social & Personalservices, which grew by 9.6%, compared to 9.1%in the previous quarter

Lower spending by the government to containfiscal deficit in the fourth quarter of FY 2013-14led to government consumption contracting by0.4% in Q4FY14

Fiscal deficit has reached ~90% of the full yearestimated deficit as at the end of October 2014.This is at the same level as at the end of October2013

Government Final Consumption Expenditure

Source : CSO; Compiled by : Finalytiks

-0.4%

8.8%

10.1%

-5%

0%

5%

10%

15%

20%

25%

30%

Q1

FY1

0

Q2

FY1

0

Q3

FY1

0

Q4

FY1

0

Q1

FY1

1

Q2

FY1

1

Q3

FY1

1

Q4

FY1

1

Q1

FY1

2

Q2

FY1

2

Q3

FY1

2

Q4

FY1

2

Q1

FY1

3

Q2

FY1

3

Q3

FY1

3

Q4

FY1

3

Q1

FY1

4

Q2

FY1

4

Q3

FY1

4

Q4

FY1

4

Q1

FY1

5

Q2

FY1

5

Fiscal deficit build up (% of Full year fiscal deficit)

Source : Ministry of Finance; Compiled by : Finalytiks

75.0%

90.1%

89.6%

0%

20%

40%

60%

80%

100%

120%

Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar

2012-13 2013-14 2014-15

Govt expenditure Vs Community, Social & Personal services

Source : CSO; Compiled by : Finalytiks

-0.4%

8.8%

10.1%

3.3%

9.1%

9.6%

-5%

0%

5%

10%

15%

20%

25%

30%

Q1

FY1

0

Q2

FY1

0

Q3

FY1

0

Q4

FY1

0

Q1

FY1

1

Q2

FY1

1

Q3

FY1

1

Q4

FY1

1

Q1

FY1

2

Q2

FY1

2

Q3

FY1

2

Q4

FY1

2

Q1

FY1

3

Q2

FY1

3

Q3

FY1

3

Q4

FY1

3

Q1

FY1

4

Q2

FY1

4

Q3

FY1

4

Q4

FY1

4

Q1

FY1

5

Q2

FY1

5

Govt final consumption exp Community, Social & Personal serv

GDP : Private consumptionPrivate consumption was the black-spot in theGDP numbers, growing at 5.8% growth in thecurrent quarter, compared to 5.6% in the previousquarter

12-month moving average shows a growing trend

Private consumption constitutes ~60% of theGDP, when viewed from the demand-side, andhence is the most important factor in GDPgrowth. Lack of major turn-around in privatespending is a cause of worry

After ruling at high levels for 2 years, retail-levelinflation has come down of late

With RBI determined to contain inflationarypressures, interest rates are yet to come down.Hence credit-based purchases might be gettingpostponed, as consumers are unwilling to take onhigher-rate debt

Inflation is below RBI’s Jan 2015 target of 8%. RBIleft interest rates unchanged in the previousmonetary policy review, citing upside risks to itsinflation target. RBI is not expected to cut interestrates this year, but sounded dovish in the lastpolicy briefing. The market widely expects deepcuts in policy rates starting 1HCY15

Private Final Consumption Expenditure & 12-month moving average

Source : CSO; Compiled by : Finalytiks

5.6%5.8%

4.9%5.6%

0%

2%

4%

6%

8%

10%

12%

14%

Q1

FY1

0

Q2

FY1

0

Q3

FY1

0

Q4

FY1

0

Q1

FY1

1

Q2

FY1

1

Q3

FY1

1

Q4

FY1

1

Q1

FY1

2

Q2

FY1

2

Q3

FY1

2

Q4

FY1

2

Q1

FY1

3

Q2

FY1

3

Q3

FY1

3

Q4

FY1

3

Q1

FY1

4

Q2

FY1

4

Q3

FY1

4

Q4

FY1

4

Q1

FY1

5

Q2

FY1

5

Private Final Consumption Expenditure 12-month moving average growth

GDP : Fixed Capital FormationGross Fixed Capital Formation, did not grow inthe current quarter, compared to a growth of 7%in the previous quarter.

12-month moving average point to upwardmovement, from near-contraction growth rates,experienced in the past two years

Private spending has to pick up, to giveconfidence for corporates to invest in capex

Gross Fixed Capital Formation & 12-month moving average

Source : CSO; Compiled by : Finalytiks

-0.9%

7.0%

0.0%

1.4%

-5%

0%

5%

10%

15%

20%

25%

Q1

FY1

0

Q2

FY1

0

Q3

FY1

0

Q4

FY1

0

Q1

FY1

1

Q2

FY1

1

Q3

FY1

1

Q4

FY1

1

Q1

FY1

2

Q2

FY1

2

Q3

FY1

2

Q4

FY1

2

Q1

FY1

3

Q2

FY1

3

Q3

FY1

3

Q4

FY1

3

Q1

FY1

4

Q2

FY1

4

Q3

FY1

4

Q4

FY1

4

Q1

FY1

5

Q2

FY1

5

Gross Fixed Capital Formation 12-month moving average growth

GDP : Exports & ImportsExports, after growing at double digits for theconsecutive 4 quarters, contracted by 1.6% duringthe quarter

Imports grew at 1.1%, after shrinking for 3consecutive quarters

Net exports (which is negative, i.e., on net basis,India is importing goods) have widened, withimports growing and exports contracting

Exports & Imports

Source : CSO; Compiled by : Finalytiks

11.5%

-1.6%

-0.4%1.1%

-20%

-10%

0%

10%

20%

30%

40%Q

1FY

10

Q2

FY1

0

Q3

FY1

0

Q4

FY1

0

Q1

FY1

1

Q2

FY1

1

Q3

FY1

1

Q4

FY1

1

Q1

FY1

2

Q2

FY1

2

Q3

FY1

2

Q4

FY1

2

Q1

FY1

3

Q2

FY1

3

Q3

FY1

3

Q4

FY1

3

Q1

FY1

4

Q2

FY1

4

Q3

FY1

4

Q4

FY1

4

Q1

FY1

5

Q2

FY1

5

Exports Imports

Net exports (Negative)

Source : CSO; Compiled by : Finalytiks

-47.5%

-30.2%

13.4%

-60%

-40%

-20%

0%

20%

40%

60%

80%

100%

120%

Q1

FY1

0

Q2

FY1

0

Q3

FY1

0

Q4

FY1

0

Q1

FY1

1

Q2

FY1

1

Q3

FY1

1

Q4

FY1

1

Q1

FY1

2

Q2

FY1

2

Q3

FY1

2

Q4

FY1

2

Q1

FY1

3

Q2

FY1

3

Q3

FY1

3

Q4

FY1

3

Q1

FY1

4

Q2

FY1

4

Q3

FY1

4

Q4

FY1

4

Q1

FY1

5

Q2

FY1

5

GDP : Exports – Rupee & Growth of Major economies

Indian Rupee (INR) has depreciated significantlyover the past 2 years. Though as per RealEffective Exchange Rates (36-countries, trade-weighted), INR continues to be in over-valuedterritory, the degree of over-valuation hassignificantly reduced (REER value more than 100shows over-valuation)

With EU growth in positive territory (YoY basis, to enable comparison with India) major developed countries have recovered from recession, and the growth rates have stabilised

Despite Japan falling in to recession recently, pick-up in EU & US augurs well for the export sector, with INR depreciation adding to the cost-competitiveness of Indian goods.

Major Global Economics : GDP growth YoY

Source: OECD

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

Q1

-200

9

Q2

-200

9

Q3

-200

9

Q4

-200

9

Q1

-201

0

Q2

-201

0

Q3

-201

0

Q4

-201

0

Q1

-201

1

Q2

-201

1

Q3

-201

1

Q4

-201

1

Q1

-201

2

Q2

-201

2

Q3

-201

2

Q4

-201

2

Q1

-201

3

Q2

-201

3

Q3

-201

3

Q4

-201

3

Q1

-201

4

Q2

-201

4

Q3

-201

4

G20 China EU (28 countries) US

REER Vs Nominal rates

Source: RBI, Compiled by : Finalytiks

90

95

100

105

110

115

120 30

35

40

45

50

55

60

65

70

Ap

r-0

4

Oct

-04

Ap

r-0

5

Oct

-05

Ap

r-0

6

Oct

-06

Ap

r-0

7

Oct

-07

Ap

r-0

8

Oct

-08

Ap

r-0

9

Oct

-09

Ap

r-1

0

Oct

-10

Ap

r-1

1

Oct

-11

Ap

r-1

2

Oct

-12

Ap

r-1

3

Oct

-13

Ap

r-1

4

Oct

-14

INR/USD Nominal (LHS) CPI based REER (RHS)

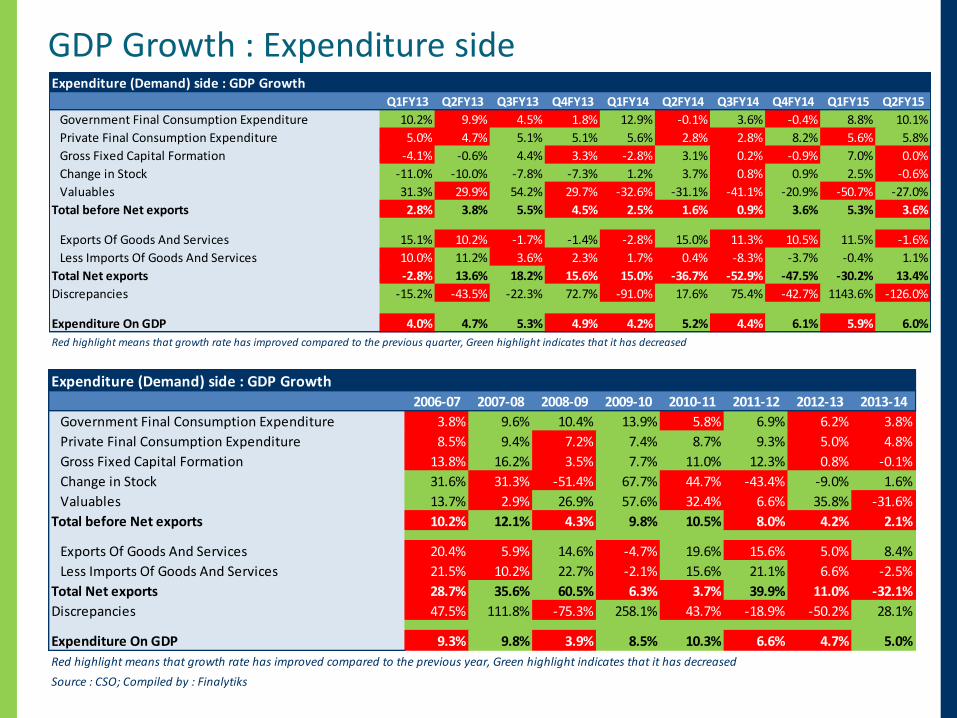

GDP Growth : Expenditure sideExpenditure (Demand) side : GDP Growth

Q1FY13 Q2FY13 Q3FY13 Q4FY13 Q1FY14 Q2FY14 Q3FY14 Q4FY14 Q1FY15 Q2FY15

Government Final Consumption Expenditure 10.2% 9.9% 4.5% 1.8% 12.9% -0.1% 3.6% -0.4% 8.8% 10.1%

Private Final Consumption Expenditure 5.0% 4.7% 5.1% 5.1% 5.6% 2.8% 2.8% 8.2% 5.6% 5.8%

Gross Fixed Capital Formation -4.1% -0.6% 4.4% 3.3% -2.8% 3.1% 0.2% -0.9% 7.0% 0.0%

Change in Stock -11.0% -10.0% -7.8% -7.3% 1.2% 3.7% 0.8% 0.9% 2.5% -0.6%

Valuables 31.3% 29.9% 54.2% 29.7% -32.6% -31.1% -41.1% -20.9% -50.7% -27.0%

Total before Net exports 2.8% 3.8% 5.5% 4.5% 2.5% 1.6% 0.9% 3.6% 5.3% 3.6%

Exports Of Goods And Services 15.1% 10.2% -1.7% -1.4% -2.8% 15.0% 11.3% 10.5% 11.5% -1.6%

Less Imports Of Goods And Services 10.0% 11.2% 3.6% 2.3% 1.7% 0.4% -8.3% -3.7% -0.4% 1.1%

Total Net exports -2.8% 13.6% 18.2% 15.6% 15.0% -36.7% -52.9% -47.5% -30.2% 13.4%

Discrepancies -15.2% -43.5% -22.3% 72.7% -91.0% 17.6% 75.4% -42.7% 1143.6% -126.0%

Expenditure On GDP 4.0% 4.7% 5.3% 4.9% 4.2% 5.2% 4.4% 6.1% 5.9% 6.0%

Red highlight means that growth rate has improved compared to the previous quarter, Green highlight indicates that it has decreased

Expenditure (Demand) side : GDP Growth2006-07 2007-08 2008-09 2009-10 2010-11 2011-12 2012-13 2013-14

Government Final Consumption Expenditure 3.8% 9.6% 10.4% 13.9% 5.8% 6.9% 6.2% 3.8%

Private Final Consumption Expenditure 8.5% 9.4% 7.2% 7.4% 8.7% 9.3% 5.0% 4.8%

Gross Fixed Capital Formation 13.8% 16.2% 3.5% 7.7% 11.0% 12.3% 0.8% -0.1%

Change in Stock 31.6% 31.3% -51.4% 67.7% 44.7% -43.4% -9.0% 1.6%

Valuables 13.7% 2.9% 26.9% 57.6% 32.4% 6.6% 35.8% -31.6%

Total before Net exports 10.2% 12.1% 4.3% 9.8% 10.5% 8.0% 4.2% 2.1%

Exports Of Goods And Services 20.4% 5.9% 14.6% -4.7% 19.6% 15.6% 5.0% 8.4%

Less Imports Of Goods And Services 21.5% 10.2% 22.7% -2.1% 15.6% 21.1% 6.6% -2.5%

Total Net exports 28.7% 35.6% 60.5% 6.3% 3.7% 39.9% 11.0% -32.1%

Discrepancies 47.5% 111.8% -75.3% 258.1% 43.7% -18.9% -50.2% 28.1%

Expenditure On GDP 9.3% 9.8% 3.9% 8.5% 10.3% 6.6% 4.7% 5.0%

Red highlight means that growth rate has improved compared to the previous year, Green highlight indicates that it has decreased

Source : CSO; Compiled by : Finalytiks

Appendix / DisclaimerAll growth rates / changes mentioned in this article are changes over the same period of previous year (i.e., year-on-year). This is because, India does not publish seasonally adjusted numbers of GDP / inflation

Disclaimer : The information set forth herein has been obtained or derived from sources generally available to the publicand believed by the author to be reliable, but the author does not make any representation or warranty, express orimplied, as to its accuracy or completeness. The information is not intended to be used as the basis of any investmentdecisions by any person or entity. This information does not constitute investment advice, nor is it an offer or asolicitation of an offer to buy or sell any security. Readers are advised to do their own research before undertakinginvestment actions.

Your feedback is very valuable to me. Kindly send your feedback to [email protected]

FINALYTIKS

INDIA-in-FOCUS