Embed Size (px)

Citation preview

Japan stimulus shocks markets • pg. 7

Cultivating NextGen clients • pg. 3

Were market valuations too stretched? • pg. 4

November 6, 2014 | Volume 4 | Issue 7

First magazine focused on active investment management

THE TWO-WAY STREETof risk and return

JAMES FRANKE

PG. 8

TAX ALPHA

THE POWER OF

How can advisors level the playing field in a rising tax environment?

For Financial Professional Use Only. Services are offered through Security Distributors, Inc., a subsidiary of Security Benefit Corporation (“Security Benefit”). 99-00471-50 2014/09/09

Download our white paper today to learn more: The Power of Tax Alpha: Adding Value by Subtracting Tax

PowerOfTaxAlpha.com

over the years, including how we have selected investment strategies.

This serves two purposes: first, to make sure everybody’s on the same page and there aren’t any surprises for the heirs in the future. And secondly, I have found it to be a great practice development tool for me in terms of actually getting clients from that next generation to understand concepts they may not have been exposed to before.

For example, the whole area of active investment management, with its defensive strategies, risk manage-ment, and quantitative approach, can be quite an eye-opener for my clients’ adult children. It is a terrific way to effectively make a presentation on our investment beliefs and approach to a highly receptive audience.”

y business grew initially through seminars, where

I covered a number of financial topics, from the tax implications of various investment strategies, to Social Security claiming issues, to estate planning. I think after 2008-09, the seminar approach lost some of its luster. The audience was so numbed as to be unresponsive and the competition for an audience became very intense, with a great number of advisors trying to reach the same target market.

These days I focus far more on developing new clients from refer-rals and from the children of current clients. My clients are getting a bit older and many have grown children, anywhere from in their 20s to their 50s. It is an important strategy for my practice to involve those children in the planning and review process for their parents and to demonstrate the value I have added.

Not only does it increase the possi-bility that I end up transitioning as the advisor on assets that my initial client base ultimately leaves to their heirs, but there’s the opportunity to gain new clients with their own assets and finan-cial planning needs.

I almost always invite my clients to include their children in meetings, if they are of age—particularly those who will be responsible for executing the estate plan down the road. I also want them to be aware of more than just the mechanics of the estate plan-ning process—to really understand why we have done what we have done

Cultivating the next generation of clients

David Quick, CPA Dallas, TX

Foresters Equity Services, Inc.Hearthstone Financial, Inc.

M“

David J. Quick, CPA, is an Investment Advisor Representative offering securities and advisory services through Foresters Equity Services, Inc., member FINRA, SIPC and a Registered Investment Advisor. Hearthstone is independent of Foresters Equity Services, Inc. Hearthstone Financial, Inc. is not a CPA firm.

Read text only

Advertising proactiveadvisormagazine.com/advertising

Reprintsproactiveadvisormagazine.com/reprints

Contactproactiveadvisormagazine.com/contact

Proactive Advisor MagazineCopyright 2014 © Dynamic Performance Publishing, Inc. All rights reserved. Reproduction of printed form, whole or in part, without permission is prohibited.

EditorDavid Wismer

Associate EditorElizabeth Whitley

Contributing WritersGreg Gann

David Wismer

Graphic DesignerTravis Bramble

Contributing PhotographerSara Stathas

November 6, 2014Volume 4 | Issue 7

Proactive Advisor Magazine is dedicated to promoting and educating on active investment management. Distribution reaches a wide audience of financial professionals who advise clients on investments and portfolio management. Each issue features an experienced investment advisor who offers insights on active money management, client service, and investment approaches. Additionally, Proactive Advisor Magazine offers an up-close look at a topic with current relevance to the field of active management.

The opinions and forecasts expressed herein are those of the author and may not actually come to pass. Any opinions and viewpoints regarding the future of the markets should not be construed as recommendations of any specific security nor specific investment advice. The analysis and information in this edition and on our website is for informational purposes only. No part of the material presented in this edition or on our websites is intended as an investment recommendation or investment advice. Neither the information nor any opinion expressed nor any portfolio constitutes a solicitation to purchase or sell securities or any investment program.

November 6, 2014 | proactiveadvisormagazine.com 3

TIPS & TOOLS

Among the many investment methodolo-gies utilized on Wall Street, there are two very popular yet diverse approaches to investment management, with sound data to support each. The first makes the case to purchase under-valued assets that are believed to have become mispriced by the market. Often this involves buying securities that have been beaten down by some event such as a merger or acquisition, a bankruptcy, a poor earnings or sales report, or a misinterpretation of future demand.

The second approach is more growth- and momentum-oriented, and could be classified as trend following. Where a value approach searches for laggards, the trend-following ap-proach looks for winners. The philosophy of trend followers is that winners often continue to win, and whatever momentum was moving them upward will continue until there is a sign of a reversal. Value investors are skeptical of the additional appreciation potential of an asset which has already been bid up. They are looking for bargains and the margin of safety that they perceive comes from purchasing an asset at a discount.

To a value investor the acquisition cost is paramount. For trend followers, market mo-mentum supersedes valuation. A trend follower operates with the belief that whatever led to an asset’s value being beaten down will continue.

Read text only

By Greg Gann

Bull market or bear, Wall Street always has a “wall of worry” to navigate—the discipline of active investment management may help.

proactiveadvisormagazine.com | November 6, 20144

* There should be a correlation between the stock market value and GDP. A strong stock market should correlate with strong GDP. A strong market with weak GDP indicates possible distortions.

** The Shiller cyclically adjusted price/earnings ratio (CAPE) averages annual earnings for the S&P 500 over a 10-year period to smooth out distortions that can occur in any particular year.

Reconciling these two opposing philoso-phies is a challenge. On the one hand, science proves that a body in motion tends to stay in motion. This clearly supports the trend fol-lowers. However, science and math also clearly support the principle of a reversion to the mean. Applying this principle to investments suggests periods of lower returns are systemat-ically followed by periods of higher returns and vice versa. This means that if a security, overall market index, or asset class has experienced a period of unusually high returns, it is likely to mean revert. This runs afoul of the mantra of trend followers.

So, who is right? And, moreover, are the two approaches mutually exclusive? I believe that they are mutually compatible and that the asset purchase price does, in fact, matter. I also believe a force in motion tends to become more energized while in motion. However, even the “Energizer Bunny” eventually runs out of steam.

The power behind momentum can result in trends continuing beyond reasonable expecta-tions, causing valuations to dramatically inflate. At some point the momentum can move valuations beyond the tipping point. When market participants believe that valuations have extended beyond a tipping point, which can be triggered by external events unrelated to valua-tions, they cease bidding, thereby reversing the trend.

Recently, the Dow and S&P 500 were both trading around all-time highs. We’ve had a

market that has reacted to negative economic data by surging higher, in anticipation of fur-ther stimulus—or a delay in the inevitable Fed raising of interest rates. Yet it rises on positive data as well. Regardless of whether it is central bank-induced, manipulated, or irrationally exuberant, the fact is that the momentum has been strong enough to increase equity prices on both good and bad news. Momentum has been resilient in dismissing even the three market valuations metrics listed above.

As wealth managers and students of behav-ioral finance, we know that clients often seek to increase and decrease risk at the worst times. In a bull market, a client might tell you that he or she can handle a 20% reduction in asset valu-ation. However, when the inevitable correction finally rears its head, you know that the client is likely to blame you and hold you responsible. This is the grand conundrum associated with managing clients’ money.

Those who adhere to the long-term trend-following models have historically been

continue on pg. 11

rewarded handsomely, particularly during the last two years. There is a huge debate as to whether today’s market is fairly valued or overvalued. Only time will tell. But, there are few who would argue that it is undervalued and that bargains abound.

If this momentum continues and prices continue their ascent, at some time an inflection point will surely come. We intuitively know this. And therein lies the rub. If we allocate offen-sively to capture on-going upside potential, we risk either losing principal or embedded gains if that inflection point comes sooner rather than later. Yet, if we refrain from investing so as to limit risk and to keep our powder dry, we risk underperforming and alienating our clients as a result.

For me, the distortions in markets that have resulted from quantitative easing have become more extreme and harder to navigate than even the dot-com era. I fight the battle between mo-mentum and fair valuation and fundamentals every single day. I believe that momentum has

The price/sales ratio for the S&P 500 recently was at 1.77. Excluding the 2000 high, this was the most elevated reading in 60 years.

1Warren Buffett’s favorite market value indicator compares the market capitalization of the S&P 500 to GDP.As valued by this metric, 2014 readings were higher than 2007.*

2The Shiller price/earnings ratio (or CAPE ratio) reached a level in 2014 only achieved on three other occasions out of 130 years of data (1929, 2000, and 2007).**

3

Market valuation Metrics

November 6, 2014 | proactiveadvisormagazine.com 5

300

250

200

150

100

50

01980 1985 1990 1995 2000 2005 2010 2015

End of 2013

End of 2014

Yen-

Trill

ions

Japan stimulus shocks global markets

lobal stocks surged late last week as Japan surprised markets with a new

bout of quantitative easing, lower oil prices brought cheaper gasoline at the pump, U.S. consumer confidence improved, and markets took in stride the Fed closure of its bond buying program.

The Bank of Japan voted to enlarge the monetary base by 80 trillion yen, or $724 billion, about a 23% increase from its previous target. Declining oil and energy costs, as well as a lower projected inflation rate in Japan and worldwide, encouraged Bank of Japan Governor Haruhiko Kuroda to raise the monetary base target. According to EconomyWatch.com, most economists had expected Japan to keep its stimulus target at the prior guidance of 60 to 70 trillion yen.

The yen plunged to a seven-year low following the announcement. Bloomberg noted that Japan’s currency tumbled beyond 111 per dollar for the first time in more than six years, while the Topix stock index jumped the most since June 2013 on the news.

Adding impetus to the global stock rally, Japan’s public pension fund, the world’s biggest, boosted its target for equity holdings. Japan’s Government Pension Investment Fund

G

Source: Nordea Markets and Macrobond

said it will put half its holdings in local and foreign stocks, double previous levels, and invest in alternative assets—lowering reliance on domestic bonds and having the effect of boosting equity markets outside of Japan.

Japan’s announcement was seen as further evidence of the continuing commitment to “Abenomics,” named for the aggressive policy

measures announced by Japanese prime minister Shinzo Abe after his December 2012 election. His ongoing goal, says the Financial Times, is to revive Japan’s sluggish economy with “three arrows”: a massive fiscal stimulus, more aggressive monetary easing from the Bank of Japan, and structural reforms to boost Japan’s competitiveness.

Read text only

Swimming nakedWith the markets recovering strongly from every dip since 2009, it is nonetheless important to remember Warren Buffett’s famous quote—and keep an eye on risk as well as reward.

Scars from past downturns resurfaceYears of market highs followed by recent swings stoke behavioral finance issues again.

What advisors can learn about lifetime client valueThe lifetime value of an ongoing client relation-ship is so high that advisory firms could arguably spend far more on marketing, business develop-ment, and extra low-cost services for clients.

JAPAN’S MONETARY BASE

7November 6, 2014 | proactiveadvisormagazine.com

TOPPING THE CHARTS

L NKS WEEK

Read text only

By David WismerPhotography by Sara Stathas

JAMES FRANKE

THETWO-WAY STREETof risk and return

Striking the delicate balance between protecting client assets and generating growth is at the core of his active management approach.

8 proactiveadvisormagazine.com | November 6, 2014

James FrankeMilwaukee, Wisconsin

Founder: Franke Martens Group

Broker-dealer: Harbour Investments, Inc.

Graduate: University of Wisconsin-Milwaukee

Designations: Chartered Financial Consultant, Chartered Life Underwriter

Member: Financial Planning Association

Estimated AUM: $30M

Proactive Advisor Magazine: Jim, how would you describe your client service philosophy?

James Franke: I started in the industry on the insurance side, and pretty rapidly progressed as a full-service financial planner and invest-ment advisor. I was one of the relatively early recipients of the American College’s Chartered Financial Consultant designation and also am a Chartered Life Underwriter.

I think the insurance background estab-lished my philosophy on how to deal with clients and the fact that it is really a two-way street. To survive and prosper in this business, you have to be client-oriented. Helping people get to where they want to go will help you build a business with a strong and enduring foundation.

In expanding your expertise from insur-ance to the advisory side, how did you develop an investment style for clients?

In the 1990s, the markets were doing great and the traditional theories of portfolio alloca-tion were working pretty flawlessly for clients. Since then, the fundamental change in the nature of markets, globalization, and the access to data has really altered all of the old models. Risk management, which was usually confined to the limited abilities of those allocation models, has taken on a whole new perspective and emphasis given the severe market correc-tions we have seen since 2000.

The nature of my client base has also affect-ed how I think about risk. The majority of my clients have more or less matured along with me and have a very different outlook as they think about or enter into retirement. They are not willing to subject their lifelong building of assets to the whims of the stock market. Their first priority is to protect what they have, and the growth of assets is a close second. They are very receptive to new ways of thinking about investment strategies.

Please explain.

First, I talk about the old way—and I do that with clients all of the time. Many people have the misunderstanding that mutual funds

are somehow structured to help protect against market downturns, or have the ability to go to cash in a significant way. Mutual funds tend to market themselves as being “actively managed.” But that is very misleading, as they really are just managed against the objective or benchmark of that particular fund, typically staying close to fully invested. This historically has created a lot of confusion for individual investors and certainly does not help when the entire market goes down.

I think 2008 was the last straw for a lot of people. Many of my clients and prospects are fearful about the equity markets. It is my job to discuss and understand their goals, aspira-tions, and financial needs as they try and build toward their specific life objectives. It is also my responsibility to understand their risk profile within that framework—and I often dig deeper than most risk questionnaires. What were their real thoughts, emotions, and fears during the market meltdown? How can we help them overcome their obstacles—whether financial or behavioral?

This leads to a discussion of active money management. Some clients have a natural incli-nation toward being very conservative with their investments—it is hard to blame them. But

when I describe an active investment approach that is geared toward protecting downside risk while taking advantage of market returns, they become very receptive to the message.

Where does this fit in with your overall financial planning approach?

I tend to use a “bucket” approach to seg-ment, or earmark, assets depending on the individual’s or couple’s specific objectives. A lot of clients want the assurance of a guaranteed stream of income entering retirement, for which we use an annuity or other insurance product. But here’s the interesting paradox if a client is extremely conservative: there is an even bigger risk of not generating enough asset growth to fully fund their retirement. It can be a delicate balance for many people.

This is where explaining an actively man-aged investment approach can help. To use a broad example, a client with a fairly conserva-tive outlook may have a portion of their assets in a guaranteed product to ensure a consistent income stream. But they may also have a portion in an actively managed portfolio, which can be geared very specifically to their risk profile and help with their longer-term asset growth.

continue on pg. 10

November 6, 2014 | proactiveadvisormagazine.com 9

Show your clients a

friendlier

bear market

800-347-3539 | f lexibleplan.com

Past performance does not guarantee future results.

The opportunity for profits

carries with it the possibility of losses.

800-347-3539 | flexibleplan.com

A complete list of all of our recommendations over the last 12 months and Brochure Form ADV Part 2A are available upon request.

L E A R N M O R E

There is another benefit to our more holistic approach to active management that most people do not realize—and that is the degree to which we can have actively managed portfolios along the risk spectrum. Even the most conser-vative clients can allocate some of their money in equity markets in a very risk-controlled fashion. And for the very aggressive investor, there are strategies that may be leveraged, while still staying in tune with market conditions. For most every client, we find the right balance of comfort that still meets their overall planning needs.

When I am asked whether active strategies can achieve market returns in a strong bull market, the answer is yes—depending on the amount of risk you are willing to assume. Those strategies designed to deliver market returns will generally do so, but that obviously introduces a higher level of volatility. Still, even with more aggressive strategies, the working principle is that they should be able to avoid the largest market drawdowns, or even profit in bearish market conditions if a trend is clearly identified.

What is the biggest challenge you face with clients?

I touched upon the issue of fear or nervous-ness about the markets, but I think with our active management approach we have come a long way in addressing that. The other issue is the explosion of information that is readily available to everyone about financial issues, investing, and retirement planning. On the one hand, it is certainly a good thing to have more informed clients. However, it has also led to people viewing things as overly complicated and confusing. There are so many voices out there—good and bad information.

One of my personal goals for clients is sim-plification and organization. That may take a fair amount of work upfront, but it really pays off in the long run. I like to think our firm is very good at client education, and our goal is helping people realize how to best utilize their financial resources to create a positive impact on their quality of life.

continued from pg. 9

James Franke is an Investment Advisor Representative offering securities and advisory services through Harbour Investments, Inc., member FINRA/SIPC. Franke Martens Group is independent of Harbour Investments, Inc.

10 proactiveadvisormagazine.com | November 6, 2014

There can be no assurance that any investment product will achieve its investment objective(s). There are risks associated with investing, including the entire loss of principal invested. Investing involves market risk. The investment return and principal value of any investment product will fluctuate with changes in market conditions. Guggenheim Investments represents the investment management businesses of Gug-genheim Partners, LLC. Securities offered through Guggenheim Funds Distributors, LLC. Guggenheim Funds Distributors, LLC is affiliated with Guggenheim Partners, LLC. x0515 #12526

Uncover the True Cost of Trading Mutual Funds and ETFs

The reflexive perception that ETFs cost less, simply based on their low expense ratios, and are more cost-effective than mutual funds, is not entirely true. In addition to an expense ratio, there are additional considerations that should be considered when making an informed choice between ETFs and funds— including spreads and commissions. This informative white paper from Rydex Funds provides an in-depth look at the cost of ownership of no-transaction-fee (NTF) mutual funds and ETFs—with a focus on active investing strategies.

Request your free copy.Call 630.505.3749 or visit guggenheiminvestments.com/rydex

Chicago | New York City | Santa Monica

Rydex Funds

A Comparison of ETFs and Mutual Funds—The True Cost of Investing

pushed prices too high, too fast, and beyond fair valuation. A similar situation occurred with house prices from 2000-07, as they increased much longer than what was reasonable.

My point is that we should not be surprised by further significant market corrections, but none of us knows when they will occur and what will incite a specific inflection point. It’s questionable how much more runway can possibly exist for stocks and bonds. Yet, interest rates through traditional perceived safe havens, such as money markets or CDs, present a losing proposition even during this period of low inflation.

Within this context, I am only comfortable allocating to actively managed strategies. I want managers who are nimble enough to act on data in real time and can respond accordingly.

For me, this is not the time for buy-and-hold, but a time for buy-and-monitor. I seek active managers who are unconstrained, unbiased, and unemotional with an extensive toolbox that includes more than long-only stock and bond positions. I want that toolbox to include, in addition to equities and fixed income, other means of realizing positive performance in other asset classes.

With a stock market that has nearly tripled in five years, where fundamentals have been shrugged off and hope has been pegged to the indefinite continuation of monetary stimulus, criticism of active investment management is certainly in vogue. Right now, passive invest-ing, as promoted by the herd (and the financial media), is said to be “winning.” However, there are many more innings, and the reasons for active management will once again be realized as the full market cycle completes.

When values capitulate and trends revert, active managers who stayed with their discipline will likely become vindicated once again. Now is the time to hold firm to our convictions and lead—as opposed to following the herd.

continued from pg. 5

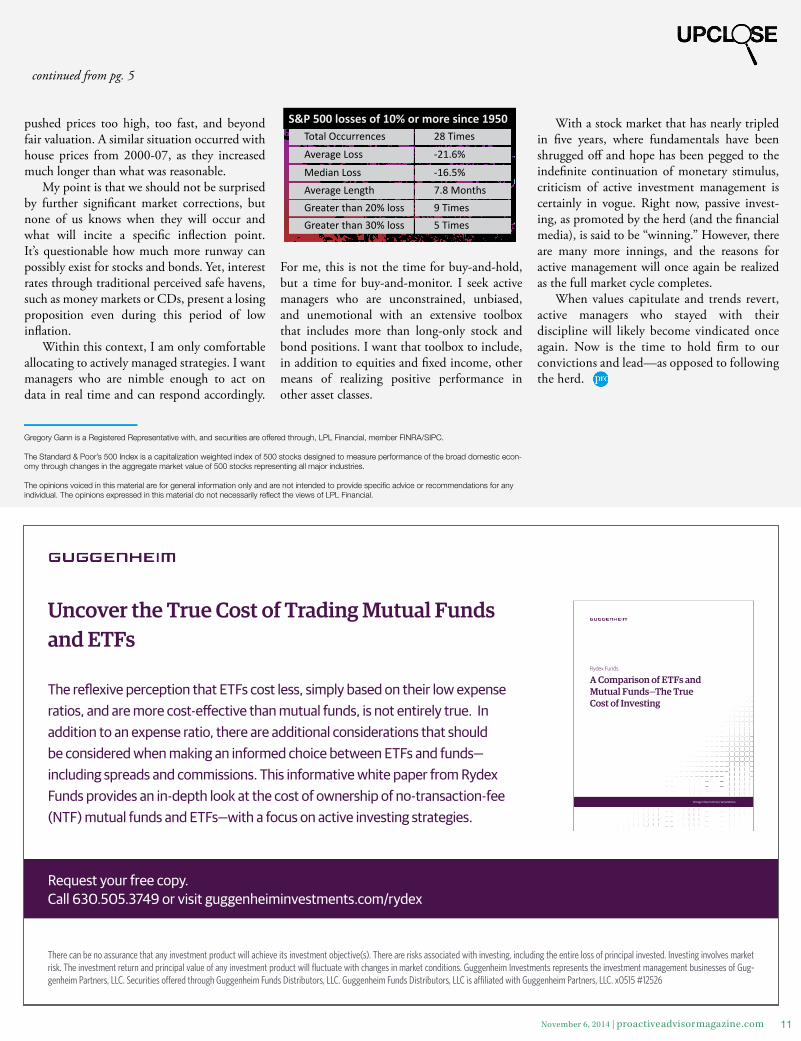

Total Occurrences

Average Loss

Median LossAverage LengthGreater than 20% lossGreater than 30% loss

28 Times

-21.6%

-16.5%7.8 Months9 Times5 Times

S&P 500 losses of 10% or more since 1950

Gregory Gann is a Registered Representative with, and securities are offered through, LPL Financial, member FINRA/SIPC.

The Standard & Poor’s 500 Index is a capitalization weighted index of 500 stocks designed to measure performance of the broad domestic econ-omy through changes in the aggregate market value of 500 stocks representing all major industries.

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. The opinions expressed in this material do not necessarily reflect the views of LPL Financial.

11November 6, 2014 | proactiveadvisormagazine.com