Embed Size (px)

Citation preview

1

Macroeconomic Indicators of Bangladesh

Presented by:

Md. Shah NaoajAssistant Director

Banking Regulation and Policy DepartmentBangladesh Bank

Head Office

2

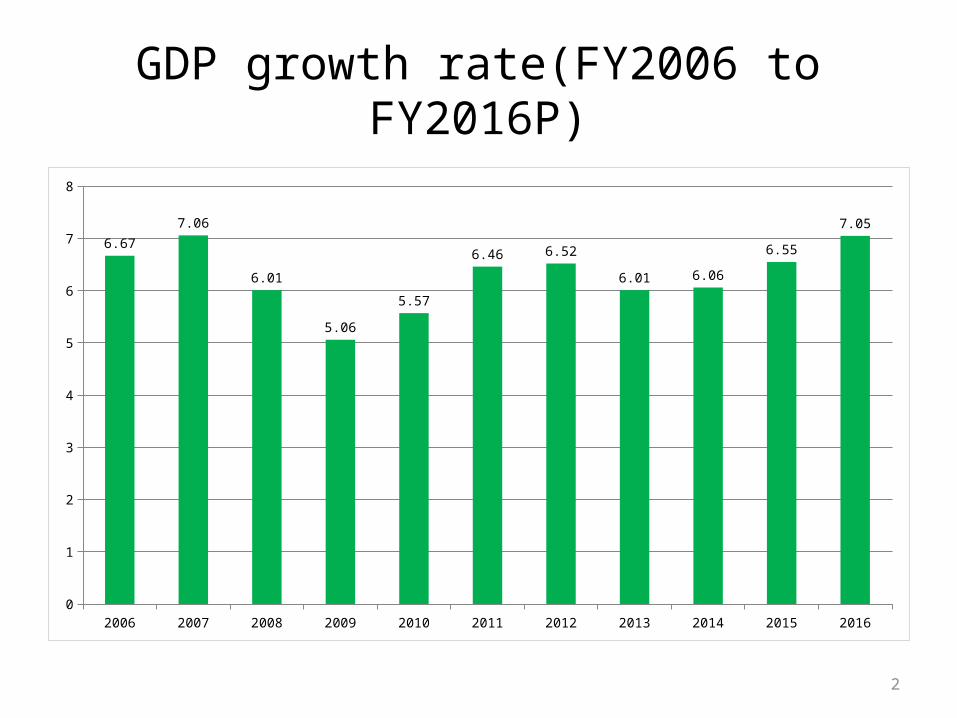

GDP growth rate(FY2006 to FY2016P)

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 20160

1

2

3

4

5

6

7

8

6.67

7.06

6.01

5.06

5.57

6.46 6.52

6.01 6.06

6.55

7.05

3

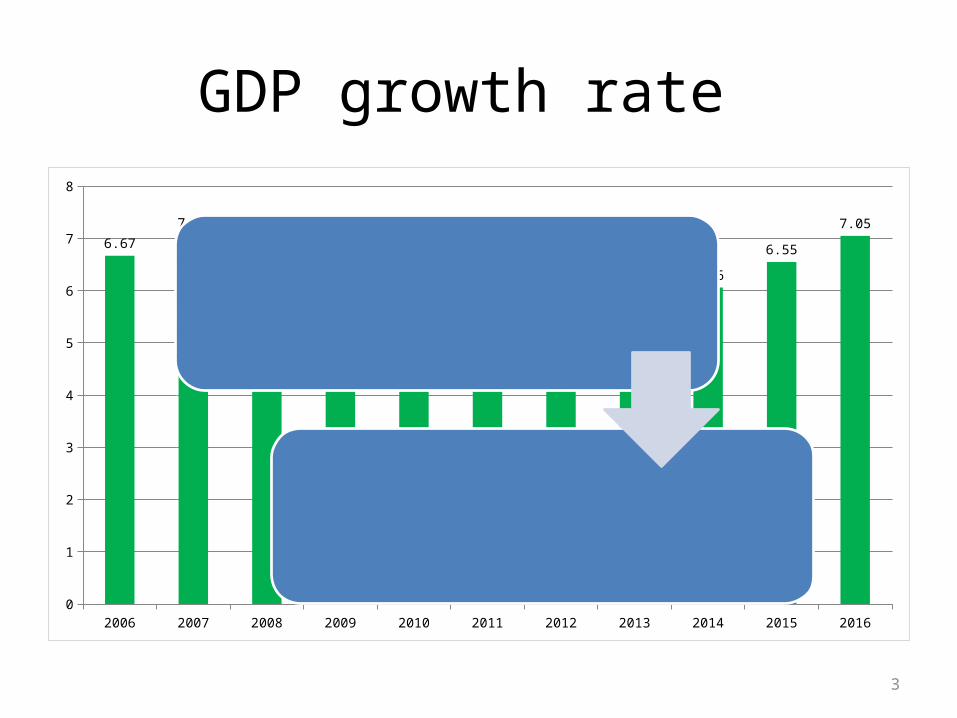

GDP growth rate

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 20160

1

2

3

4

5

6

7

8

6.67

7.06

6.01

5.06

5.57

6.46 6.52

6.01 6.06

6.55

7.05Despite slower growth in the promising external market, Bangladesh economy achieved reasonably a satisfactory growth during the FY15.

4

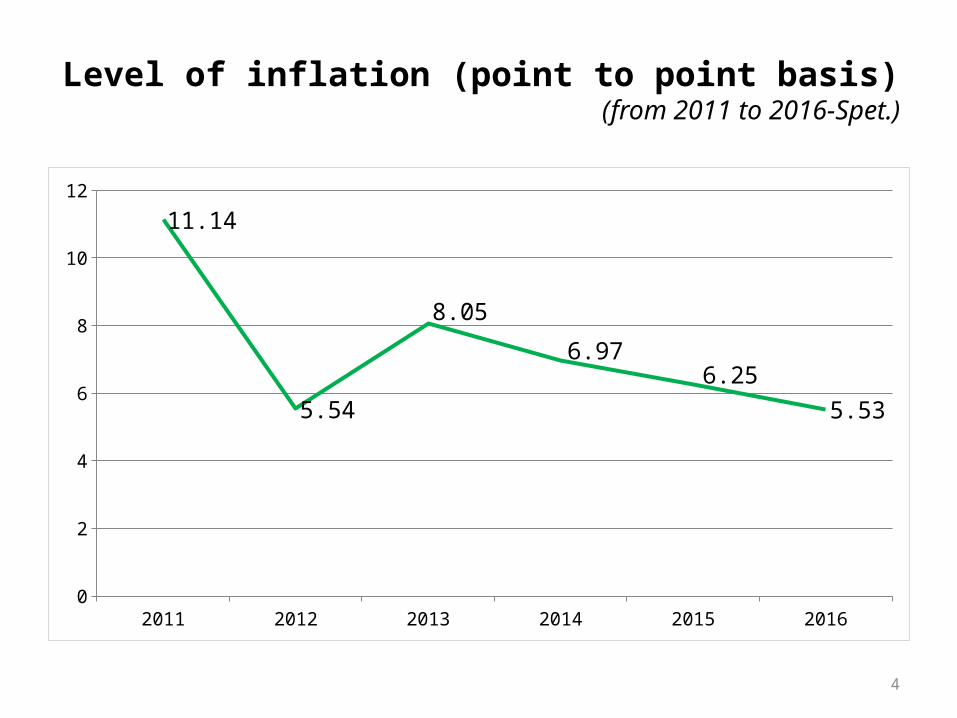

Level of inflation (point to point basis)(from 2011 to 2016-Spet.)

2011 2012 2013 2014 2015 20160

2

4

6

8

10

12

11.14

5.54

8.05

6.976.25

5.53

5

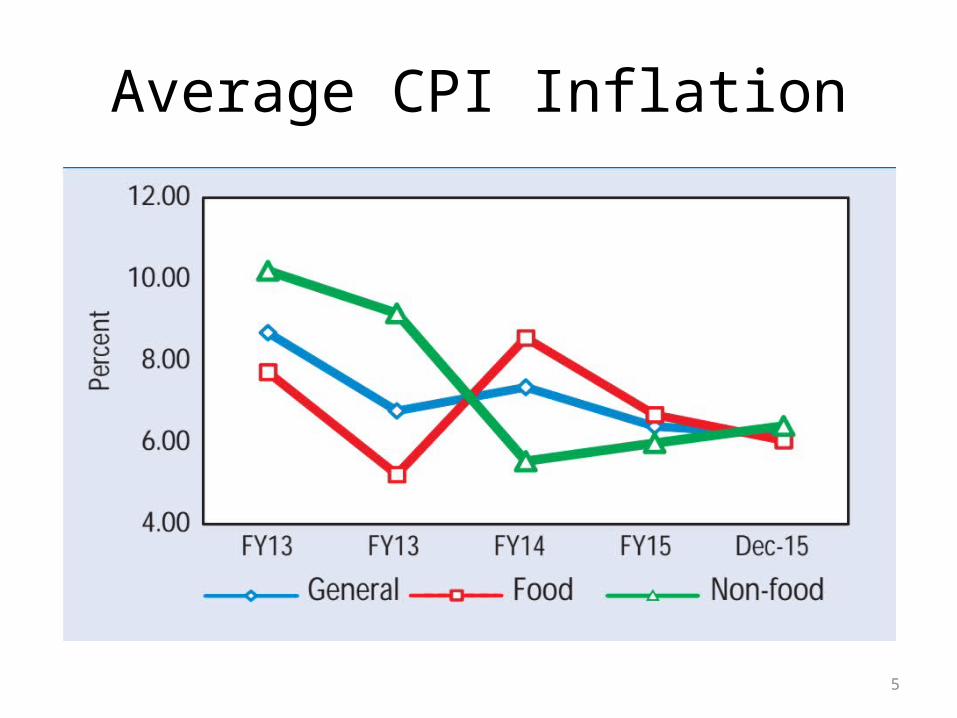

Average CPI Inflation

6

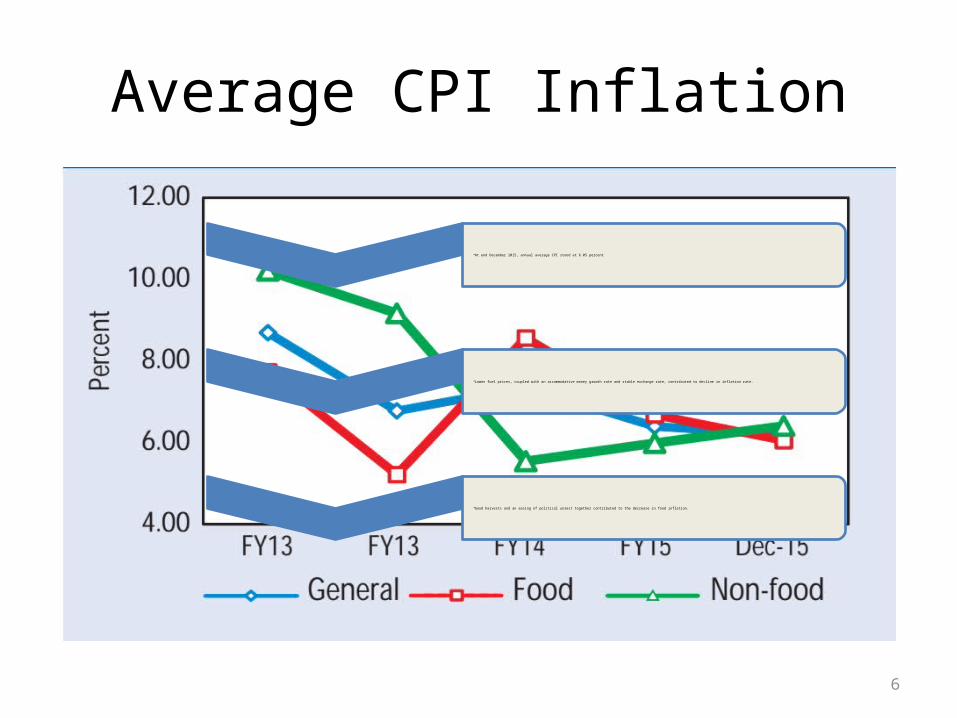

Average CPI Inflation

•At end December 2015, annual average CPI stood at 6.05 percent

•Lower fuel prices, coupled with an accommodative money growth rate and stable exchange rate, contributed to decline in inflation rate.

•Good harvests and an easing of political unrest together contributed to the decrease in food inflation.

7

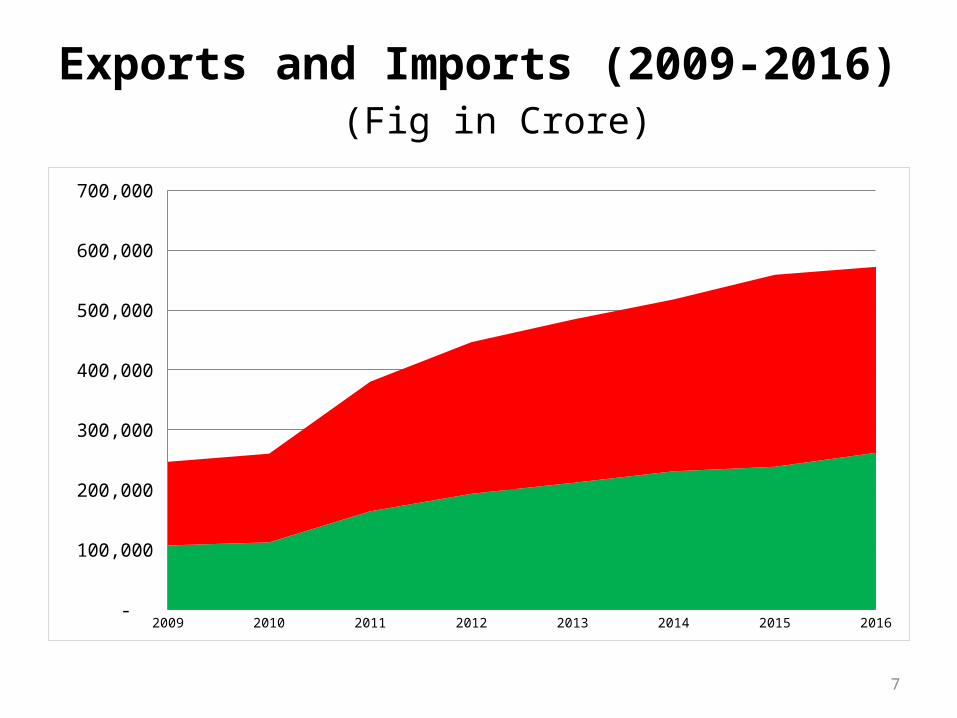

Exports and Imports (2009-2016)(Fig in Crore)

2009 2010 2011 2012 2013 2014 2015 2016 -

100,000

200,000

300,000

400,000

500,000

600,000

700,000

8

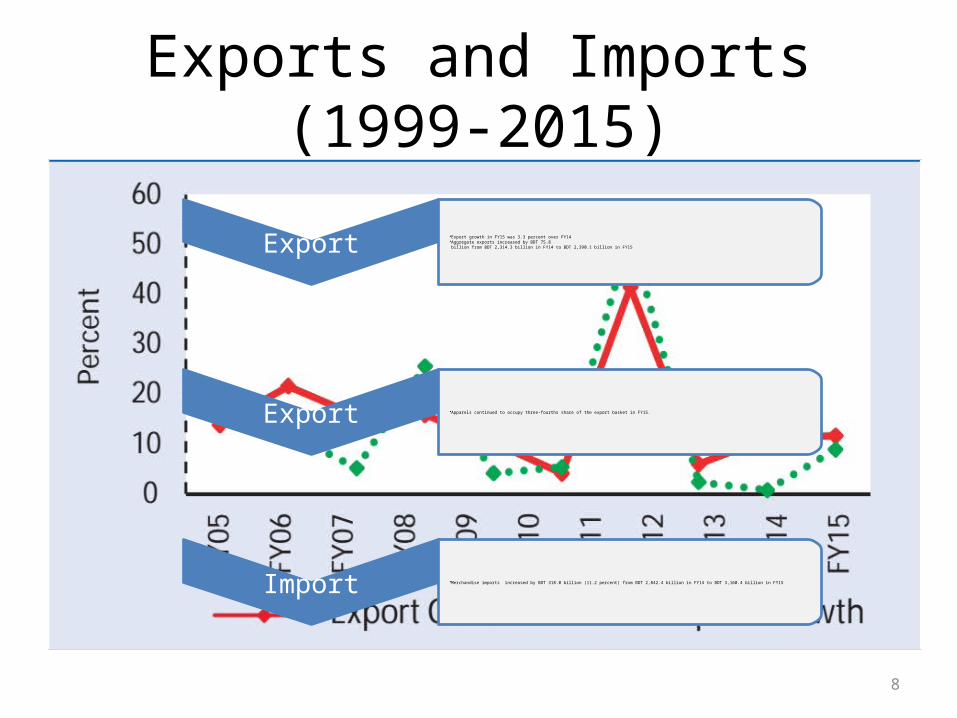

Exports and Imports (1999-2015)19

99

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

0

50000

100000

150000

200000

250000

300000

350000

ExportImport

Export•Export growth in FY15 was 3.3 percent over FY14•Aggregate exports increased by BDT 75.8billion from BDT 2,314.3 billion in FY14 to BDT 2,390.1 billion in FY15

Export •Apparels continued to occupy three-fourths share of the export basket in FY15.

Import •Merchandise imports increased by BDT 318.0 billion (11.2 percent) from BDT 2,842.4 billion in FY14 to BDT 3,160.4 billion in FY15

9

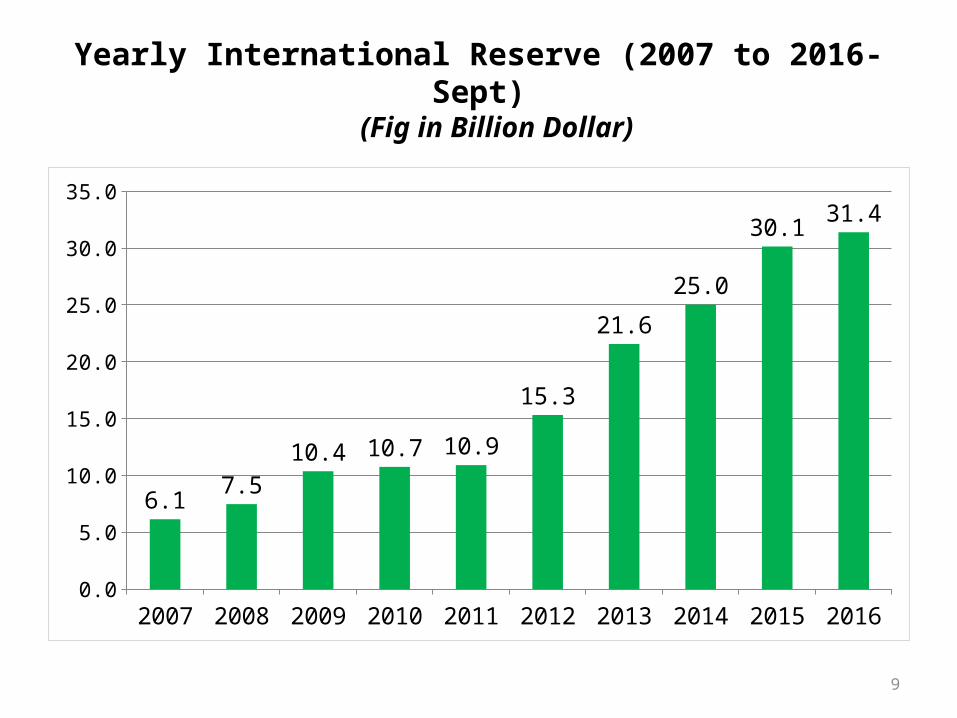

Yearly International Reserve (2007 to 2016-Sept) (Fig in Billion Dollar)

2007 2008 2009 2010 2011 2012 2013 2014 2015 20160.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

6.17.5

10.4 10.7 10.9

15.3

21.6

25.0

30.131.4

10

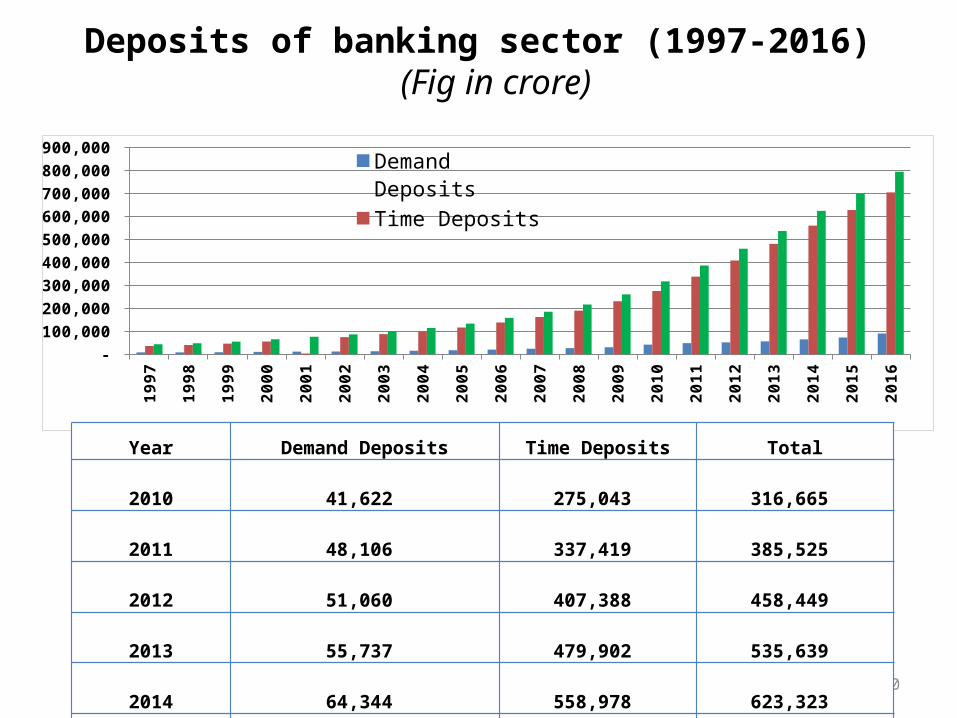

Deposits of banking sector (1997-2016)(Fig in crore)

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

- 100,000 200,000 300,000 400,000 500,000 600,000 700,000 800,000 900,000

Demand DepositsTime DepositsTotal

Year Demand Deposits Time Deposits Total 2010 41,622 275,043 316,665 2011 48,106 337,419 385,525 2012 51,060 407,388 458,449 2013 55,737 479,902 535,639 2014 64,344 558,978 623,323

2015 72,384 626,800 699,184

2016 89,759 703,947 793,706

11

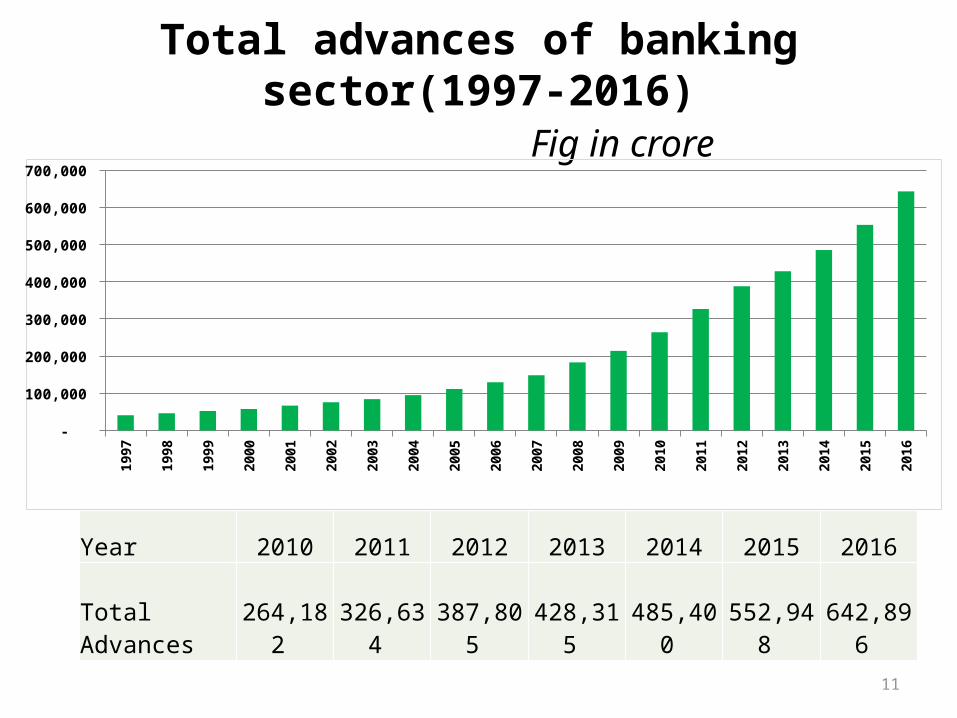

Total advances of banking sector(1997-2016)Fig in crore

Year 2010 2011 2012 2013 2014 2015 2016

Total Advances

264,182

326,634

387,805

428,315

485,400

552,948

642,896

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

-

100,000

200,000

300,000

400,000

500,000

600,000

700,000

12

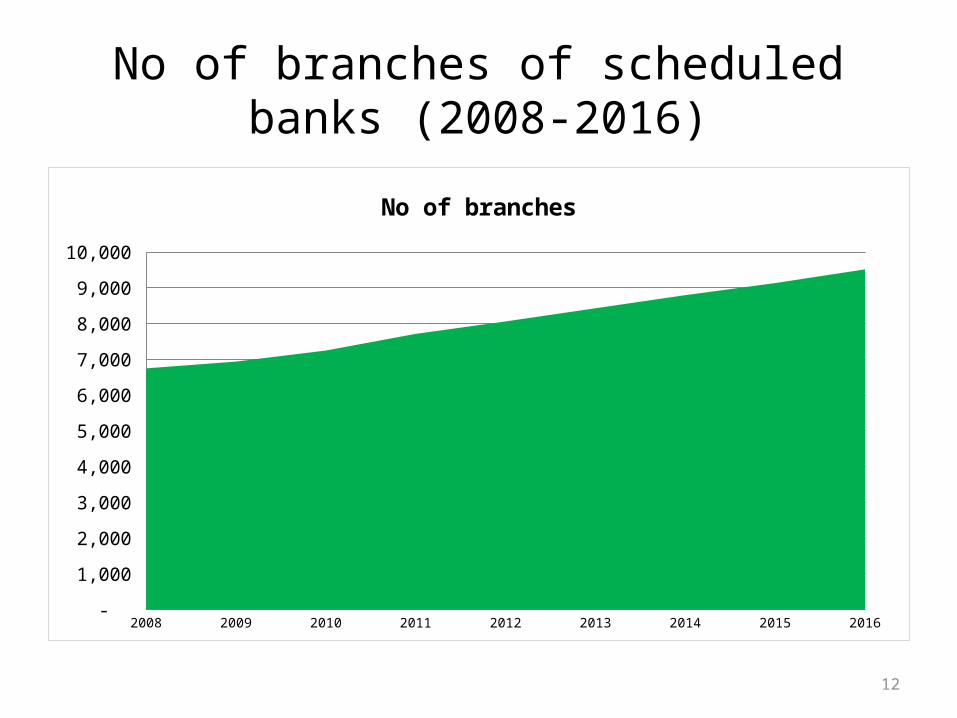

No of branches of scheduled banks (2008-2016)

2008 2009 2010 2011 2012 2013 2014 2015 2016 -

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

No of branches

13

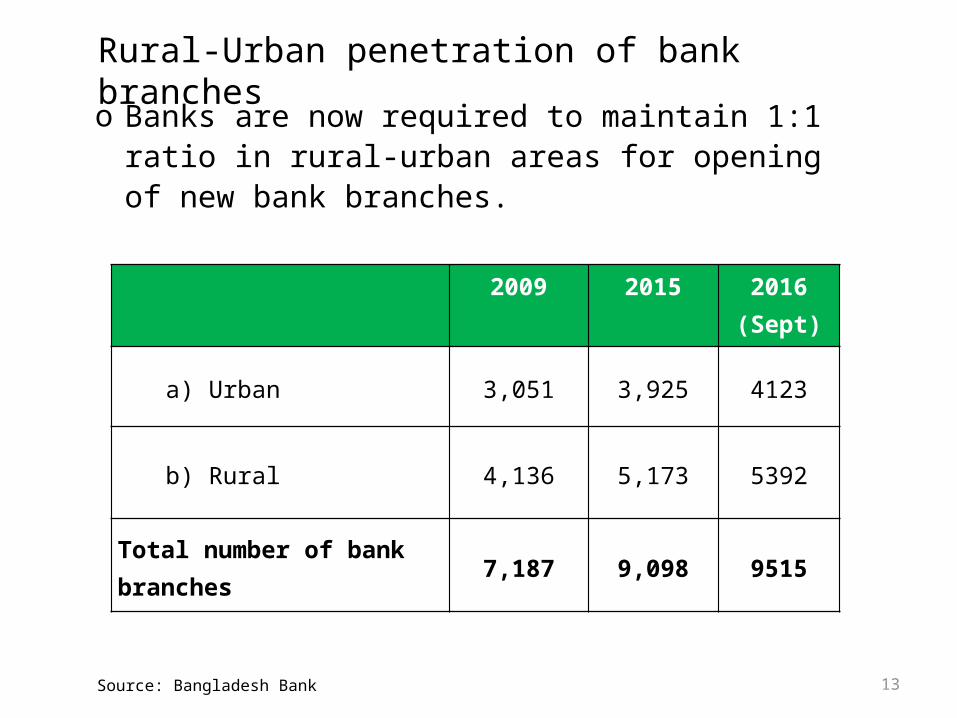

2009 2015 2016 (Sept)

a) Urban 3,051 3,925 4123

b) Rural 4,136 5,173 5392

Total number of bank branches 7,187 9,098 9515

o Banks are now required to maintain 1:1 ratio in rural-urban areas for opening of new bank branches.

Rural-Urban penetration of bank branches

Source: Bangladesh Bank

At a glance

A real GDP growth of 6.5 percent was recorded in FY15, 40 basis points higher than the growth recorded in FY14

The banking system, comprising 56 scheduled banks, experienced a positive growth in most of its income-earning

assets. .

Bangladesh has come a long way, especially over the past decade, and will continue to make sustained progress in the years ahead.

14