Embed Size (px)

Citation preview

Copyright © 2014 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced,

redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained

in this publication. However, no warranty is given to the accuracy of its content . Page 1

NewBase 30 November 2014 - Issue No. 489 Khaled Al Awadi

NewBase For discussion or further details on the news below you may contact us on +971504822502 , Dubai , UAE

UAE powers up with energy growth The National + NewBase

Power generation in the UAE will increase by more than 1.5 gigawatts in 2017, enough to power around 150,000 homes, according to a new report.

The State of Energy Report in the UAE 2015, prepared by the Dubai Carbon Centre of Excellence and the United Nations, highlights energy projects across the UAE focusing on energy diversification and government policy.

The report reveals that the UAE will increase power generation with a mix of energy sources from natural gas to solar and nuclear power.

From 2008 to 2012, national power demand grew 37 per cent. Abu Dhabi increased its power-generating capacity by 43.6 per cent and Dubai increased capacity 44.5 per cent. The UAE’s energy demand is growing at about 9 per cent a year.

One of the three projects listed in the report is the Shah Gas Development, a joint venture between Abu Dhabi National Oil Company (Adnoc) and Occidental Petroleum. The project is the first of its kind in the country, and is anticipated to come online early next year.

Located in Abu Dhabi’s Liwa desert, the Shah marks the country’s first venture into sour gas processing and is expected to add 5 million cubic feet per day. Sour gas contains a high amount of hydrogen sulphide, which makes processing more costly. However, this type of gas makes up the majority of the UAE’s natural gas.

Copyright © 2014 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced,

redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained

in this publication. However, no warranty is given to the accuracy of its content . Page 2

Natural gas represents 99 per cent of Abu Dhabi’s power generation mix. Abu Dhabi Water and Electricity Authority (Adwea) expects the emirate’s power consumption to rise by 11.3 per cent each year, forcing Abu Dhabi to tap the more difficult gas.

The UAE is also looking to diversify its energy mix with the goal of generating 24 per cent of its total power generation by clean energy projects by 2020. “We continue to draw a clear strategy in energy, and we believe our economy is based on diversification,” the UAE Minister of Energy Suhail Al Mazrouei said last week.

The Minister of Economy Sultan Al Mansouri said that the country was the front-runner for branching out from the oil and gas sector. “The UAE is the most diversified economy in the Middle East,” Mr Al Mansouri said.

Two major clean energy projects are expected to feed electricity into the grid in two years. The second phase in the Mohamed bin Rashid Al Maktoum Solar Park will generate 100 megawatts of solar photovoltaic (PV) power. Dubai Electricity and Water Authority (Dewa) issued the tender for the

second phase on November 20. Dewa expects the project to be completed in 2017.

“The Mohammed bin Rashid Al Maktoum Solar Park [will be] one of the largest renewable energy projects in the region and demonstrates our commitment to achieve our vision to become a sustainable world-class utility,” said Saeed Mohammed Al Tayer, the Dewa managing director and chief executive.

The third project expected to increase power generation in three years’ time is Emirates Nuclear Energy Corporation’s power plant in Barakah capable of generating 1.4 GW, which is located 300 kilometres west of Abu Dhabi. Enec said in September that more than 57 per cent of the first of four reactors had been completed.

Enec expects the second unit to follow in 2018 and units three and four will come online in 2019 and 2020, respectively. The company said that the four reactors would provide about 25 per cent of the country’s electricity needs.

Copyright © 2014 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced,

redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained

in this publication. However, no warranty is given to the accuracy of its content . Page 3

Qatar:Oryx GTL forum focuses on its 2015 shutdown Gulf Times + NewBase

In line with Oryx GTL’s commitment to sustainable development and actively pursuing stakeholder satisfaction, the company’s Contracts and Materials Department held its ‘3rd Annual Contractors/Suppliers Forum’ at the Sharq Village recently.

The forum was chaired by Oryx GTL’s chief commercial officer (CCO), Mohamed Sharif Ibrahim al-Mushiri, supported by Mohamed Faraj Ezran, contracts manager and Johannes Van Der Merwe, acting/materials manager. The forum was also attended by the executive management, managers and staff members of Oryx GTL’s Commercial Group as well as the company’s contractors and suppliers.

The theme of the forum was ‘Connect, Exchange, Cooperate’, which was aimed at facilitating interaction between Oryx GTL and

the participating companies towards improvement in compliance, practices and business relationship, with emphasis on the 2015 shutdown. Al-Mushiri expressed his happiness and gratitude to all attendees for their presence.

In keeping with Oryx GTL’s values and safety culture, the first presentation by Gideon Jankowitz, security supervisor was titled ‘HSE Safety Moment’ on ‘Vehicle Access to Site.’

Other presenters during this event were Dana al-Dafaa, contracts specialist, who presented ‘Vision and Values Moment’ on ‘Create a Winning Team’; Philip Thorpe-Willett, head (contracts) provided an update on outstanding actions from last year’s forum; Gerardus Toet, process optimisation specialist, spoke on ‘Business Continuity’ and Lakhdar Barka, head (contract services) presented ‘2015 shutdown cost control’.

Nawaf al-Amri, materials buyer, provided an input on procurement and warehouse issues with regards to 2015 shutdown and Michael Lineses, contracts specialist, provided a presentation on this year’s improvements.

Yasser Habib, head (procurement) presented answers to questions raised in advance by the attendees and thereafter the master of ceremony. Ahmad Alsheeb hosted the Q&A open session, where all attendees had the opportunity to freely express their views, ask questions, discuss issues and areas of improvement as well as share their expectations on various business issues and practices such as clarity of specifications, bid submission and evaluation, amongst others.

Copyright © 2014 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced,

redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained

in this publication. However, no warranty is given to the accuracy of its content . Page 4

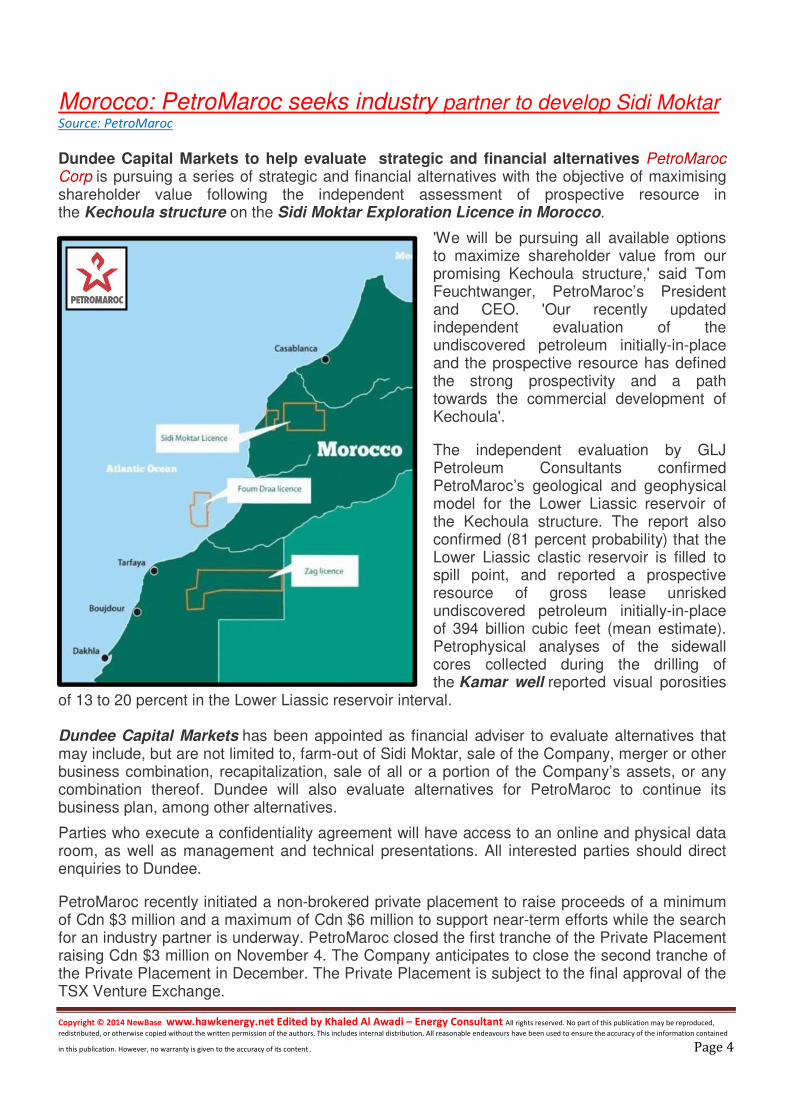

Morocco: PetroMaroc seeks industry partner to develop Sidi Moktar Source: PetroMaroc

Dundee Capital Markets to help evaluate strategic and financial alternatives PetroMaroc Corp is pursuing a series of strategic and financial alternatives with the objective of maximising shareholder value following the independent assessment of prospective resource in the Kechoula structure on the Sidi Moktar Exploration Licence in Morocco.

'We will be pursuing all available options to maximize shareholder value from our promising Kechoula structure,' said Tom Feuchtwanger, PetroMaroc’s President and CEO. 'Our recently updated independent evaluation of the undiscovered petroleum initially-in-place and the prospective resource has defined the strong prospectivity and a path towards the commercial development of Kechoula'.

The independent evaluation by GLJ Petroleum Consultants confirmed PetroMaroc’s geological and geophysical model for the Lower Liassic reservoir of the Kechoula structure. The report also confirmed (81 percent probability) that the Lower Liassic clastic reservoir is filled to spill point, and reported a prospective resource of gross lease unrisked undiscovered petroleum initially-in-place of 394 billion cubic feet (mean estimate). Petrophysical analyses of the sidewall cores collected during the drilling of the Kamar well reported visual porosities

of 13 to 20 percent in the Lower Liassic reservoir interval. Dundee Capital Markets has been appointed as financial adviser to evaluate alternatives that may include, but are not limited to, farm-out of Sidi Moktar, sale of the Company, merger or other business combination, recapitalization, sale of all or a portion of the Company’s assets, or any combination thereof. Dundee will also evaluate alternatives for PetroMaroc to continue its business plan, among other alternatives.

Parties who execute a confidentiality agreement will have access to an online and physical data room, as well as management and technical presentations. All interested parties should direct enquiries to Dundee.

PetroMaroc recently initiated a non-brokered private placement to raise proceeds of a minimum of Cdn $3 million and a maximum of Cdn $6 million to support near-term efforts while the search for an industry partner is underway. PetroMaroc closed the first tranche of the Private Placement raising Cdn $3 million on November 4. The Company anticipates to close the second tranche of the Private Placement in December. The Private Placement is subject to the final approval of the TSX Venture Exchange.

Copyright © 2014 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced,

redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained

in this publication. However, no warranty is given to the accuracy of its content . Page 5

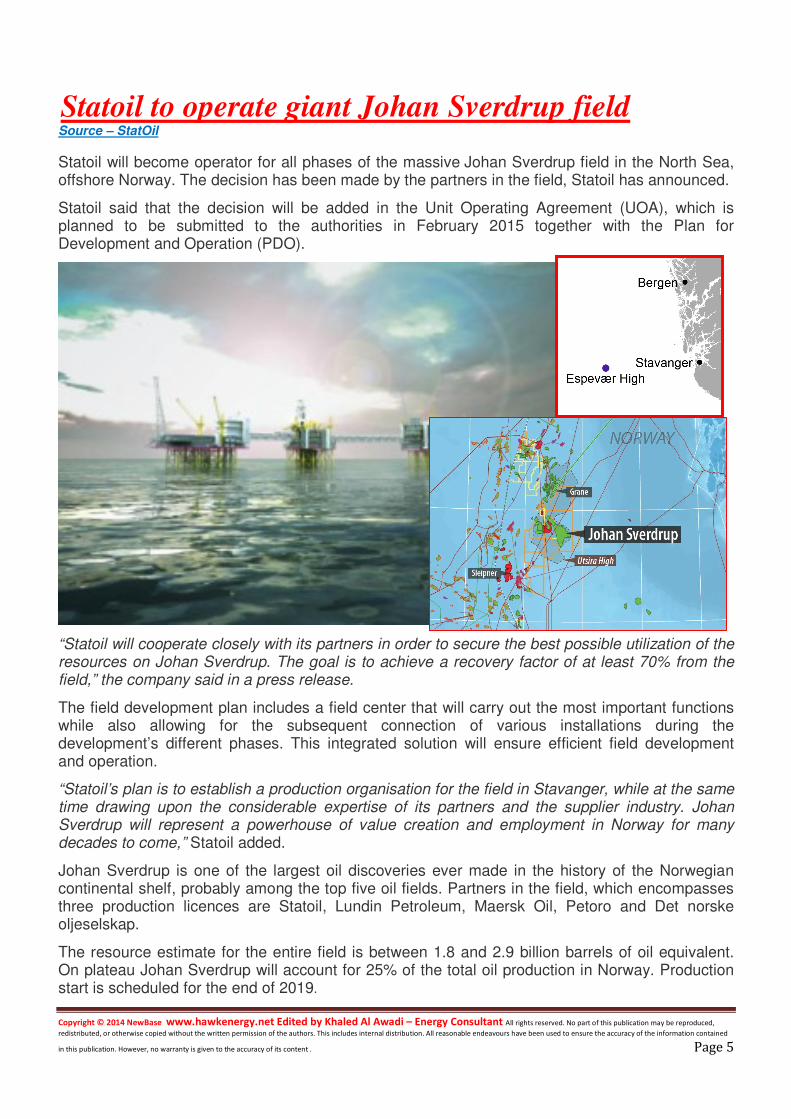

Statoil to operate giant Johan Sverdrup field Source – StatOil

Statoil will become operator for all phases of the massive Johan Sverdrup field in the North Sea, offshore Norway. The decision has been made by the partners in the field, Statoil has announced.

Statoil said that the decision will be added in the Unit Operating Agreement (UOA), which is planned to be submitted to the authorities in February 2015 together with the Plan for Development and Operation (PDO).

“Statoil will cooperate closely with its partners in order to secure the best possible utilization of the resources on Johan Sverdrup. The goal is to achieve a recovery factor of at least 70% from the field,” the company said in a press release.

The field development plan includes a field center that will carry out the most important functions while also allowing for the subsequent connection of various installations during the development’s different phases. This integrated solution will ensure efficient field development and operation.

“Statoil’s plan is to establish a production organisation for the field in Stavanger, while at the same time drawing upon the considerable expertise of its partners and the supplier industry. Johan Sverdrup will represent a powerhouse of value creation and employment in Norway for many decades to come,” Statoil added.

Johan Sverdrup is one of the largest oil discoveries ever made in the history of the Norwegian continental shelf, probably among the top five oil fields. Partners in the field, which encompasses three production licences are Statoil, Lundin Petroleum, Maersk Oil, Petoro and Det norske oljeselskap.

The resource estimate for the entire field is between 1.8 and 2.9 billion barrels of oil equivalent. On plateau Johan Sverdrup will account for 25% of the total oil production in Norway. Production start is scheduled for the end of 2019.

Copyright © 2014 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced,

redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained

in this publication. However, no warranty is given to the accuracy of its content . Page 6

U.S. gasoline prices this Thanksgiving are the lowest since 2009

Source: U.S. Energy Information Administration,

U.S. retail regular-grade gasoline prices continue to decline, averaging $2.82 per gallon (gal) as of November 24. This average is 47 cents lower than a year ago, and the lowest price heading into a Thanksgiving holiday since 2009. Traditionally, the Thanksgiving holiday is one of the most traveled times of the year in the United States, and much of that travel is by car. AAA estimates that during this Thanksgiving holiday weekend (November 26-30), 41.3 million people in the United States will travel more than 50 miles from home by car. This level of travel, 4.3% higher than the same time last year, is the highest number of travelers by car for Thanksgiving in seven years and the third highest since AAA began publishing the data in 2000.

Gasoline prices across the country reflect differences in gasoline quality, taxes, and the characteristics of regional market supply and demand balances. West Coast prices typically exceed the U.S. average because of stricter fuel specifications in California and the region's isolation from other domestic markets. Regional differences in gasoline prices are also attributable to variations in state and local taxes and differences in regional supply costs. Much of the decline in gasoline prices since mid-2014 is attributable to falling crude oil prices. The combination of robust U.S. crude oil production growth, a return of Libyan production (despite recent setbacks), weakening expectations for the global economy (particularly in China), and seasonally low refinery demand has reduced oil prices. North Sea Brent spot prices have fallen from a July monthly average of $112 per barrel (bbl) to a November monthly average of $80/bbl (through November 24). The average U.S. retail regular-grade gasoline price has fallen 88 cents/gal since the start of July.

Copyright © 2014 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced,

redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained

in this publication. However, no warranty is given to the accuracy of its content . Page 7

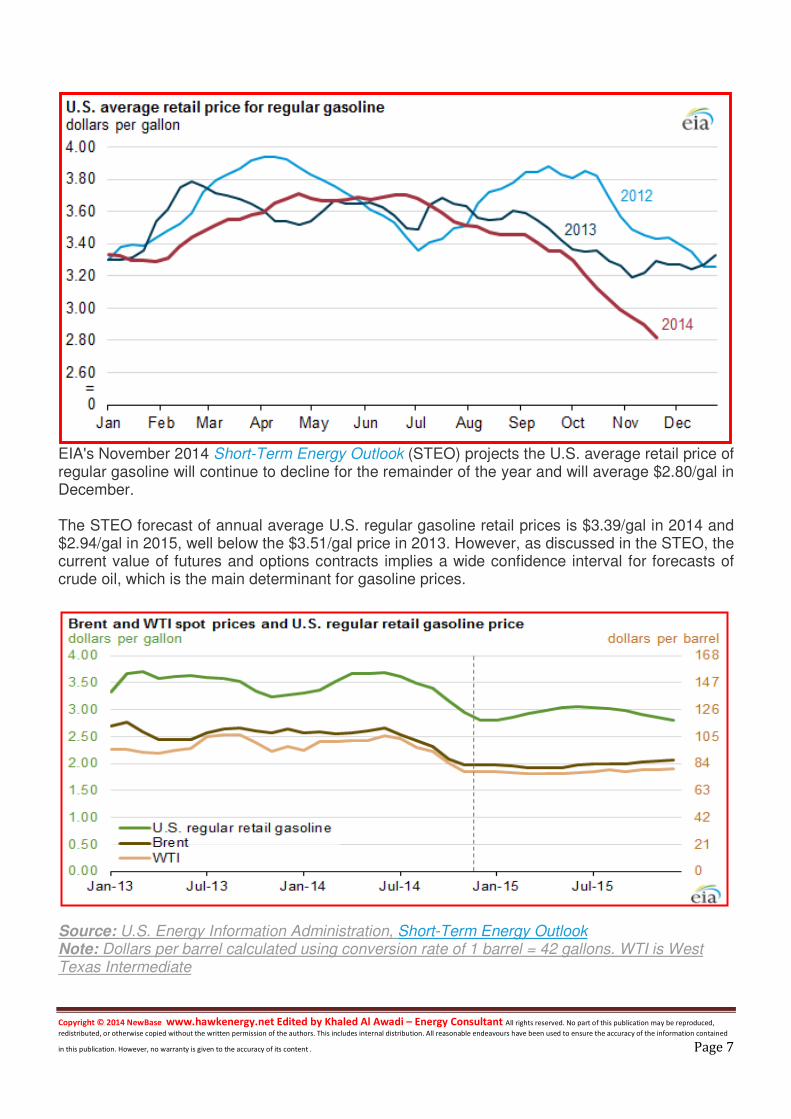

EIA's November 2014 Short-Term Energy Outlook (STEO) projects the U.S. average retail price of regular gasoline will continue to decline for the remainder of the year and will average $2.80/gal in December. The STEO forecast of annual average U.S. regular gasoline retail prices is $3.39/gal in 2014 and $2.94/gal in 2015, well below the $3.51/gal price in 2013. However, as discussed in the STEO, the current value of futures and options contracts implies a wide confidence interval for forecasts of crude oil, which is the main determinant for gasoline prices.

Source: U.S. Energy Information Administration, Short-Term Energy Outlook Note: Dollars per barrel calculated using conversion rate of 1 barrel = 42 gallons. WTI is West Texas Intermediate

Copyright © 2014 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced,

redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained

in this publication. However, no warranty is given to the accuracy of its content . Page 8

US: Cost cuts for unconventional oil, gas to have sweeping impact Saudi gazette + NewBase With research concluding up to 40 percent savings in operational costs for unconventional wells in the United States, the Middle East must innovate their energy strategy to remain relevant, according to Accenture’s new report titled “Achieving high performance in unconventional operations, integrated planning, services, logistics and materials management”. The report said oil and gas operators in the United States can reduce the costs of constructing, drilling and completing unconventional wells, as well as the overall time it takes to complete them, by up to 40 percent through better planning and management of logistics, contractors and materials.

For particularly high performers, these could mean costs reductions of $1.3 million to $2.6 million, on a $6.5 million well, and much more for the low performers. Operators can achieve these savings by adopting a more integrated planning process, better management of service contractors, and improved logistics and materials management for fresh and reused water and installed equipment. “Our global research team has found that operators of the Eagle Ford Shale model in the top quartile spend about $6 million per well, some still struggle to deliver wells for twice that amount,” said Omar Boulos, managing director, Accenture in the Middle East. “To generate the maximum savings and efficiencies, operators need to carefully balance their investments in technology, continuous improvement and people, and in the low-margin environment of unconventionals, trade-offs will need to be made.

Copyright © 2014 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced,

redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained

in this publication. However, no warranty is given to the accuracy of its content . Page 9

For example: Is investment in new rig technology a better choice than offering incentives to your service provider to ensure consistency of crew?” Technological developments in unconventional exploration in the United States could also have serious consequences for the downstream industry in the Arabian Gulf. “Historically speaking, the petrochemicals producers in the GCC countries have enjoyed access to favorably priced feedstock, which has led to the emergence of a dynamic downstream industry,” Boulos further said. “The emergence of feedstock alternatives in the United States is leading analysts to forecast much activity in the downstream sector in North America, particularly in the fertilizers market. This could potentially affect the profit margins of the GCC petrochemicals sector which is an export driven industry.” Accenture’s report covers several planning and management issues and ways operators can improve performance, including: • Integrated Planning – With hundreds or thousands of wells in a single field and production forecasts largely driven by drilling new wells, the lack of an integrated planning approach in unconventional operations can lead to missed production targets and capital overruns. To avoid this, operators will need to apply planning tools, simplify planning schedules, break down organizational silos and integrate service providers into the planning process. • Logistics Management – At 5 million gallons and 1,000 truck movements per well, efficient water use and movements continue to provide a competitive advantage in unconventional operations. But there’s also an opportunity to improve non-water movements, such as proppant and aggregates. It’s critical to make the best use of rail, road and pipeline transport and select the most optimal locations for permanent and temporary storage. • Management of Drilling and Other Service Contractors – Unconventional development is characterized by a large number of service providers and a large number of handovers on the site. Operators need to ensure better collaboration between these contractors and apply strict financial controls and management to meet risk, commercial and operational requirements. • Materials Management – Given the number of wells on a multi-well pad and 24-hour crews, an unconventional operation requires a much higher volume of materials than a conventional one. The management of these materials needs to be efficient and agile to ensure timely delivery, in order to minimize downtime and avoid tying up working capital and racking up needless storage expenses. “Our research suggests that large independent operators are best positioned to implement these improvements, as they tend to have a trade-off mind-set when it comes to investments in technology, continuous improvement and people,” Boulo noted. “They know that you cannot invest in all three all of the time as that would be too expensive,” he added.

Copyright © 2014 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced,

redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained

in this publication. However, no warranty is given to the accuracy of its content . Page 10

Oil Price Drop Special Coverage

Oil and gas price collapse Washington Post + NewBase

The news in the markets is dramatic: Crude oil prices dropped below $70 (Dh257) per barrel. This continues a dramatic price decline for a commodity that in late June cost more than $100 per barrel.

The shift has markedly lowered US gas prices (which are now well below $3 per gallon) and thus, may be beefing up the US economy heading into the Christmas spending season, by putting considerably more money in consumers’ wallets. But what’s driving this trend — which is quickly becoming the single most important economic story of 2014?

1. Opec: First and most immediately, there’s the fact that the Organisation of Petroleum Exporting Countries decided not to cut oil production at their meeting Thursday. This was Opec’s “most important [meeting] in years,” the Post’s Steven Mufson reported on Tuesday, because it came amid a pre-existing downtrend in prices, and everybody wanted to know if Opec would take any action to halt the decline.

It didn’t — and crude oil prices immediately tanked.

But where did the broader and longer term downtrend come from? Three more answers:

2. Booming US and world oil production: Even as Opec kept production steady, it has been growing elsewhere. The United States, most of all, has seen a major growth in oil production, thanks to the shale oil revolution. The figures from the Energy Information Administration are truly dramatic: Almost twice as many barrels a day of crude oil are being produced now in the US, versus in 2005.

Production of oil has also been up in many other countries. Canada increased its total production from just more than 3,300 barrels per day in 2009 to over 4,000 in 2013 and Russia increased from 9,900 barrels per day in 2009 to 10,500 barrels per day over the same time period. Libya, meanwhile, is bouncing back after production tanked in 2011 due to the country’s civil war.

In sum, there’s just more oil out there for people to buy, which is having a predictable effect on prices, pushing them downward.

3. Slack demand in many regions including Japan and Europe: There’s also the fact that while the U.S. has recovered steadily from the Great Recession, many other countries have not. They’re struggling, and that is dampening oil demand.

In Europe, for instance, while total petroleum consumption averaged well over 14,000 barrels per day in 2010 and 2011, it was less than 13,000 in the first quarter of this year, and not much higher in the second quarter. There’s a similar story to be told about Japan, where demand is also dropping, according to the Energy Information Administration.

Copyright © 2014 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced,

redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained

in this publication. However, no warranty is given to the accuracy of its content . Page 11

4. Strides in vehicle fuel efficiency: In the US, we’re also using less fuel in our cars because those cars are more efficient. The average fuel efficiency of a newly purchased light-duty passenger vehicle in this country was 36 miles (58 kilometres) per gallon in 2013. Back in 1980, it was 24.3 miles (39 kilometres) per gallon.

So in sum, the trend in oil prices is fundamentally due to that most basic of economic factors: Supply and demand.

So what happens next? Does the trend continue, or is it possible we’ve already overshot and are due for a reversal in oil prices? Observers can’t be sure but there are some reasons to think a bounceback could be possible. And in the long term, overall fuel consumption is definitely projected to increase, not decline, out towards 2040 — driven largely by developing nations.

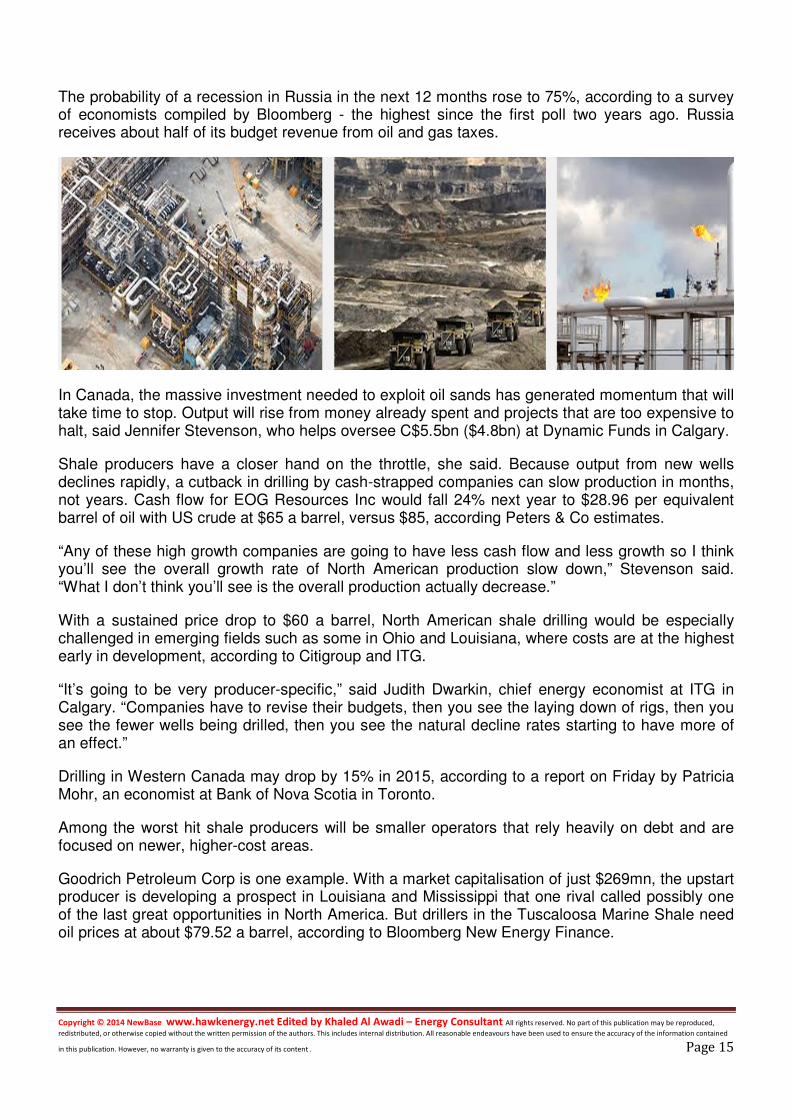

Oil prices sink as struggle for global market clout heats up

WITH Venezuela leading the campaign for an output cut and most others not in favor, fireworks at the OPEC Secretariat in Vienna,

during the five hour long ministerial last Thursday, seemed inevitable. On one hand, there were some stressing on measures to ensure long-term market stability and on the other there were few, apparently pressed by the immediate budgetary concerns, who were on a lookout for immediate remedial measures. By Wednesday evening, a day prior to the meeting, the writing was very much on the wall. An

output rollover appeared imminent. With a deal between Iran and P5+1 at least deferred for the time being and a possible deluge from Tehran out of reckoning for at least another six months, OPEC hawk Iran too appeared getting close to the majority position. The situation began to crystallize further when Russia, producing 10.5 million bpd or 11 percent of global oil, opted out of a voluntary output restraint

regimen - despite some initial hints. At a meeting with Saudi Oil Minister Ali Al-Naimi and

Copyright © 2014 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced,

redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained

in this publication. However, no warranty is given to the accuracy of its content . Page 12

officials from Venezuela and non-OPEC member Mexico prior to the OPEC moot, Russia’s most influential oil official, state firm Rosneft’s head Igor Sechin, emerged with a surprise message - Russia will not reduce output even if oil falls to $60 per barrel. Sechin added that he expected low oil prices to do more damage to producing nations with higher costs, in a clear reference to the US shale boom. Gulf Arab OPEC members also streamlined their position, reaching a consensus ‘not to cut output’ at this moment. Naimi asserted the oil market “will stabilize itself eventually.” UAE Oil Minister Suhail bin Mohammed Al-Mazroui too added his voice to the chorus, saying “market will fix itself ultimately.” Kuwait’s oil minister too was not much behind. “We have to live either with $80 or with $60 or with $100,” Ali Saleh Al-Omair told reporters. He then asserted “oversupply came from the evolution of the unconventional oil production ... I think everyone needs to play a role in balancing the market, not OPEC unilaterally.” And interestingly, Iran insisting until then on an output cut, too seemed to be getting close to the dominant opinion within OPEC. Prior to the meeting, Iranian Oil Minister Bijan Namdar Zangeneh indicated that he and Saudi Oil Minister Al-Naimi were “very close” in their positions. “The most important thing for all of us is the unity and solidarity of OPEC, and in this situation I believe we need to have the contribution of non-OPEC producers for managing the market,” Zangeneh told reporters. And thus despite the realization that the current output regimen was almost a million bpd more than the call on its crude, a rollover was imminent. In a statement after the meeting, OPEC asserted that the ministers “in the interest of restoring market equilibrium” had decided to maintain its current production levels. The battle royal to protect OPEC markets share has begun, screaming headlines said all around immediately after. If OPEC were to cut exports without similar action by its competitors, it would lose further market share, including to North American shale oil producers, Reuters said. OPEC was no more ready to shoulder the entire output cut burden. Speaking to CNBC, Nigeria’s Petroleum Minister and the newly elected OPEC president Diezani Alison-Madueke said non-OPEC oil producers also need to “share the burden” of any future cut in production. “In keeping the production target at 30 mbpd, OPEC is clearly signaling that it will no longer bear the burden of market adjustment alone and this decision puts the onus on other producers, especially US tight oil to adjust as well,” a note from Barclays Instant Insights said. Russian intransigence on output cut was also noted. Neil Atkinson, the head of analysis at Lloyd’s List Intelligence emphasized that Saudi Arabia was right to be patient in making a decision and will use the next three months to put further pressure on non-OPEC producers—like Russia—to come to an agreement on production. OPEC in its communiqué said: “The Conference also noted, importantly, that, although world oil demand is forecast to increase during the year 2015, this will, yet again, be offset by the projected increase of 1.36 million bpd in non-OPEC supply.” And this was no more apparently acceptable to OPEC ministers.

Copyright © 2014 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced,

redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained

in this publication. However, no warranty is given to the accuracy of its content . Page 13

And with OPEC moving to protect its markets share, global media is buzzing; it is evoking memories of 1986 oil price and market war. Then too, like the currently ongoing shale revolution, oil output from Alaska’s North Slope and the North Sea came on line (combined production of around 5-6 million barrels a day), and began chipping at OPEC’s market share.

The current scenario has some similarities. A Deutsche Bank report said that around 40% of shale oil production in the United States next year, would be unviable if the price of oil fell below $80 per barrel. However, Maria van der Hoeven, executive director of the International Energy Agency, is of the opinion that 82 percent of the American shale oil firms had a break-even price of $60 or lower. Javed Mian writing in Stray Reflections says: “The median North

American shale development needs an oil price of $57 to break even today, compared to $70 last year according to research firm IHS.” Analysts at Citibank recently said that the price of oil would have to fall below $50 a barrel for completely halting shale oil production in the United States. Also, many shale oil companies would continue to remain viable for an oil price of anywhere between $40 to $60 a barrel. Indeed no single figure is available. Opinions though vary - and by far. Dimension of the current moves on the global energy chessboard are simply too many and the rumblings of it would be felt for long - one could now say with some certainty.

Opec refusal means weakest left behind Bloomberg

Saudi Arabia and its Opec allies’ firm stand against cutting crude output to slow the plunge in oil

prices has set the energy world on a painful course that will leave the weakest behind, from

governments to US wildcatters.

A grand experiment has begun, one in which the group of producing nations - sometimes called the central bank of oil - is leaving the market to decide who is strongest and how to cut as much as 2mn bpd of surplus supply.

Copyright © 2014 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced,

redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained

in this publication. However, no warranty is given to the accuracy of its content . Page 14

Oil patch executives including billionaire Harold Hamm have vowed to drill on, asserting they can profit well below $70 a barrel, with output unlikely to fall for at least a year. Marginal producers in less profitable US shale areas, as well as countries from Iran to Russia and operations from Canada to Norway will see the knife sooner, according to analyses by Wells Fargo & Co, IHS Inc and ITG Investment Research.

“We’re in a very nerve-wracking environment right now and will be for probably the next couple of years,” Jamie Webster, senior director for global crude markets at IHS, said on Friday in a phone interview. “This is a different game. This isn’t just about additional barrels, this is about barrels that are going to keep coming and keep coming.”

Investors punished oil producers, as Hamm’s Continental Resources Inc fell 20%, the most in six years, amid a swift plunge in crude to below $70 for the first time since 2010. Exxon Mobil Corp declined 4.2% to close at $90.54 in New York. Talisman Energy Inc, based in Calgary, was down 2.7% on Friday in Toronto after dropping 14% the day before.

A production cut by the 12-member Organisation of Petroleum Exporting Countries would have been the quickest way

to tighten the world’s oil supplies and boost prices. In the US, output is expected either to remain flat or rise by almost 1mn bpd next year, according to the Paris-based International Energy Agency and ITG.

That is because only about 4% of shale production needs $80 or more to be profitable. Most drilling in the Bakken formation, one of the main drivers of shale oil output, returns cash at or below $42 a barrel, the IEA estimates.

ITG estimates it will take six months before lower prices slow production growth from US shale, which is responsible for propelling the country’s production to the highest in more than three decades.

Elsewhere, oil markets already have begun to pressure governments that rely on higher prices to finance their budgets, fuel subsidies to citizens and expand drilling. Venezuela’s oil income has fallen by 35%, President Nicolas Maduro said on state television November 19.

Nigeria increased interest rates for the first time in three years on November 26 and devalued its currency. The government is planning to cut spending by 6% next year, Finance Minister Ngozi Okonjo-Iweala said on November 16. Both Nigeria and Venezuela are part of Opec.

Several countries within Opec such as Iran, Iraq, Nigeria and Venezuela, as well as non-Opec states such as Russia and Norway, will probably have to cut production with lower oil prices in 2015 and beyond, Roger Read, an analyst at Wells Fargo, said on Friday in a note to investors.

Copyright © 2014 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced,

redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained

in this publication. However, no warranty is given to the accuracy of its content . Page 15

The probability of a recession in Russia in the next 12 months rose to 75%, according to a survey of economists compiled by Bloomberg - the highest since the first poll two years ago. Russia receives about half of its budget revenue from oil and gas taxes.

In Canada, the massive investment needed to exploit oil sands has generated momentum that will take time to stop. Output will rise from money already spent and projects that are too expensive to halt, said Jennifer Stevenson, who helps oversee C$5.5bn ($4.8bn) at Dynamic Funds in Calgary.

Shale producers have a closer hand on the throttle, she said. Because output from new wells declines rapidly, a cutback in drilling by cash-strapped companies can slow production in months, not years. Cash flow for EOG Resources Inc would fall 24% next year to $28.96 per equivalent barrel of oil with US crude at $65 a barrel, versus $85, according Peters & Co estimates.

“Any of these high growth companies are going to have less cash flow and less growth so I think you’ll see the overall growth rate of North American production slow down,” Stevenson said. “What I don’t think you’ll see is the overall production actually decrease.”

With a sustained price drop to $60 a barrel, North American shale drilling would be especially challenged in emerging fields such as some in Ohio and Louisiana, where costs are at the highest early in development, according to Citigroup and ITG.

“It’s going to be very producer-specific,” said Judith Dwarkin, chief energy economist at ITG in Calgary. “Companies have to revise their budgets, then you see the laying down of rigs, then you see the fewer wells being drilled, then you see the natural decline rates starting to have more of an effect.”

Drilling in Western Canada may drop by 15% in 2015, according to a report on Friday by Patricia Mohr, an economist at Bank of Nova Scotia in Toronto.

Among the worst hit shale producers will be smaller operators that rely heavily on debt and are focused on newer, higher-cost areas.

Goodrich Petroleum Corp is one example. With a market capitalisation of just $269mn, the upstart producer is developing a prospect in Louisiana and Mississippi that one rival called possibly one of the last great opportunities in North America. But drillers in the Tuscaloosa Marine Shale need oil prices at about $79.52 a barrel, according to Bloomberg New Energy Finance.

Copyright © 2014 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced,

redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained

in this publication. However, no warranty is given to the accuracy of its content . Page 16

Lower oil prices changing risk profile in EMs The Peninsula + NewBase

The recent drop in oil prices is changing the risk profile of Emerging Markets (EMs). Significant

adjustments to global financial markets in the second half of 2014 include a large drop in

commodity prices, the end of quantitative easing (QE) in the US, and a stronger US dollar, the

QNB Group said. These developments, particularly the drop in oil prices, have led to a divergence

in EM performance and risks going forward. At this juncture, the most exposed countries are

Russia and Ukraine, followed by other commodity producers like Brazil and South Africa.

We have previously identified the EMs most at risk of a balance of payments crisis (see our

Economic Commentary dated June 6, 2014). This analysis focused on the fragile five (Brazil,

India, Indonesia, South Africa and Turkey) EMs that were most severely impacted by the capital

outflows following the announcement in mid-2013 of the QE tapering by the US Federal Reserve

(Fed). We now have added Russia and Ukraine to our list of EMs that face a material risk of a

crisis (owing to the fallout between the two countries as well as the recent drop in oil prices) to

make up the so-called Suspect Seven.

Copyright © 2014 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced,

redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained

in this publication. However, no warranty is given to the accuracy of its content . Page 17

Overall, the second half of 2014 has resulted in a significant EM differentiation between those

markets that have been able to take the necessary measures to reduce their current account

deficits and stabilize their currencies (India and Indonesia) and those that are still struggling to

contain the loss of confidence in their economies (Brazil, Russia, Ukraine and to a lesser extent

South Africa). Much of the loss of confidence in the latter group has been driven by lower global

commodity prices, including oil.

The improvement in financial market sentiment towards the ‘Suspect Seven’ has occurred despite

a steady downward revision in the outlook for these economies, with the main exception of India.

According to Bloomberg consensus, real GDP growth is now expected to be 5.4 percent in 2014

up from 4.7 percent expected in June. Indonesia is the only other Suspect Seven expected to

grow by over 5 percent in 2014.

Lower oil prices have been a key differentiator of EM performance during the second half of 2014.

Brent oil prices peaked in mid-June at $115 per barrel. Since then prices have fallen over 30

percent to around $80 currently. Falling oil prices have helped improve external balances in India

and Indonesia and their governments have also taken the opportunity presented by lower oil

prices to increase fuel prices and reduce their subsidy bills.

Indian Prime Minister Narendra Modi announced in mid-October that the government would stop

fixing diesel prices, eliminating half of total fuel subsidies, which cost the government around 9.4

percent of the budget last year. Indonesian President Joko Widodo announced in mid-November a

30 percent increase in fuel prices, which follows a 33 percent increase in June 2013. Fuel

subsidies are expected to reach around 19 percent of the Indonesian budget this year.

Russia has been the hardest hit by falling oil prices — the exchange rate has weakened 34.9

percent since the end of June as falling oil prices have exacerbated weaknesses relating to

international sections associated with tensions in Ukraine.

Ukraine itself is in a particularly dire situation. The economy is now expected to contract by 7

percent this year. Sovereign default was narrowly averted in May with an agreement for external

support from the IMF and other donors totaling $27bn. International reserves fell to just $12.6bn

from $16.3bn at end-September. The central bank gave up on efforts to defend the currency in

early October and is now running short of reserves. Without continued external support, Ukraine is

likely to experience a sovereign default.

In Brazil, falling oil and commodity prices have also added to concerns about political uncertainty

Copyright © 2014 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced,

redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained

in this publication. However, no warranty is given to the accuracy of its content . Page 18

that stem from the October presidential elections and delays to appointing a new government.

This has led to a sharp depreciation of the Brazilian real of 13.9 percent since the end of June

2014.

The outlook for South Africa has deteriorated slightly during the second half of the year as the

economy is predominantly reliant on commodities. Falling commodity prices have led to a

downward revision in consensus real GDP growth forecasts from 1.9 percent in June to 1.5

percent currently.

The small weakening of Turkey’s currency since June has mainly been driven by a deterioration in

the security situation in neighbouring countries. Turkey faces some major challenges with a

current account deficit expected to be over 5 percent this year, although, as a net oil importer, the

drop in oil prices should help.

Another important factor that has supported EMs is further unexpected monetary easing in China

and Japan, which has eased global liquidity conditions. Previously, financial markets had been

concerned about the ending of QE in the US in October. However, the People’s Bank of China

unexpectedly cut lending and deposit rates on November 24. Additionally, the Bank of Japan

surprised markets by expanding its QE programme at the end of October with much of the

additional liquidity expected to flow to EMs in search of higher yields.

Overall, recent developments in global financial markets have helped stabilise some of the fragile

EMs that were previously thought to be at risk. However, recent developments, including lower oil

and commodity prices, have been less positive for commodity exporting countries, particularly

Russia and Brazil, which are suffering as a result. Political tensions in Ukraine are pushing the

country close to the brink. If Ukraine goes down, contagion could further destabilises Russia.

Copyright © 2014 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced,

redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained

in this publication. However, no warranty is given to the accuracy of its content . Page 19

NewBase For discussion or further details on the news below you may contact us on +971504822502 , Dubai , UAE

Your Guide to Energy events in your area

Copyright © 2014 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced,

redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained

in this publication. However, no warranty is given to the accuracy of its content . Page 20

NewBase For discussion or further details on the news below you may contact us on +971504822502 , Dubai , UAE

Your partner in Energy Services

NewBase energy news is produced daily (Sunday to Thursday) and

sponsored by Hawk Energy Service – Dubai, UAE.

For additional free subscription emails please contact Hawk Energy

Khaled Malallah Al Awadi, Energy Consultant MSc. & BSc. Mechanical Engineering (HON), USA ASME member since 1995 Emarat member since 1990

Mobile : +97150-4822502 [email protected] [email protected]

Khaled Al Awadi is a UAE National with a total of 25 years of experience in the Oil & Gas sector. Currently working as Technical Affairs Specialist for Emirates General Petroleum Corp. “Emarat“ with external voluntary Energy consultation for the GCC area via Hawk Energy Service as a UAE operations base , Most of the experience were spent as the Gas Operations Manager in Emarat , responsible for Emarat Gas Pipeline Network Facility & gas compressor stations . Through the years , he has developed great

experiences in the designing & constructing of gas pipelines, gas metering & regulating stations and in the engineering of supply routes. Many years were spent drafting, & compiling gas transportation , operation & maintenance agreements along with many MOUs for the local authorities. He has become a reference for many of the Oil & Gas Conferences held in the UAE and Energy program broadcasted internationally , via GCC leading satellite Channels.

NewBase : For discussion or further details on the news above you may contact us on +971504822502 , Dubai , UAE

NewBase 30 November 2014 K. Al Awadi

Copyright © 2014 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced,

redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained

in this publication. However, no warranty is given to the accuracy of its content . Page 21