Embed Size (px)

Citation preview

Copyright © 2014 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced,

redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained

in this publication. However, no warranty is given to the accuracy of its content . Page 1

NewBase 13 January 2015 - Issue No. 517 Khaled Al Awadi

NewBase For discussion or further details on the news below you may contact us on +971504822502 , Dubai , UAE

UAE on course to increasing oil production capacity Gulf News + NewBase

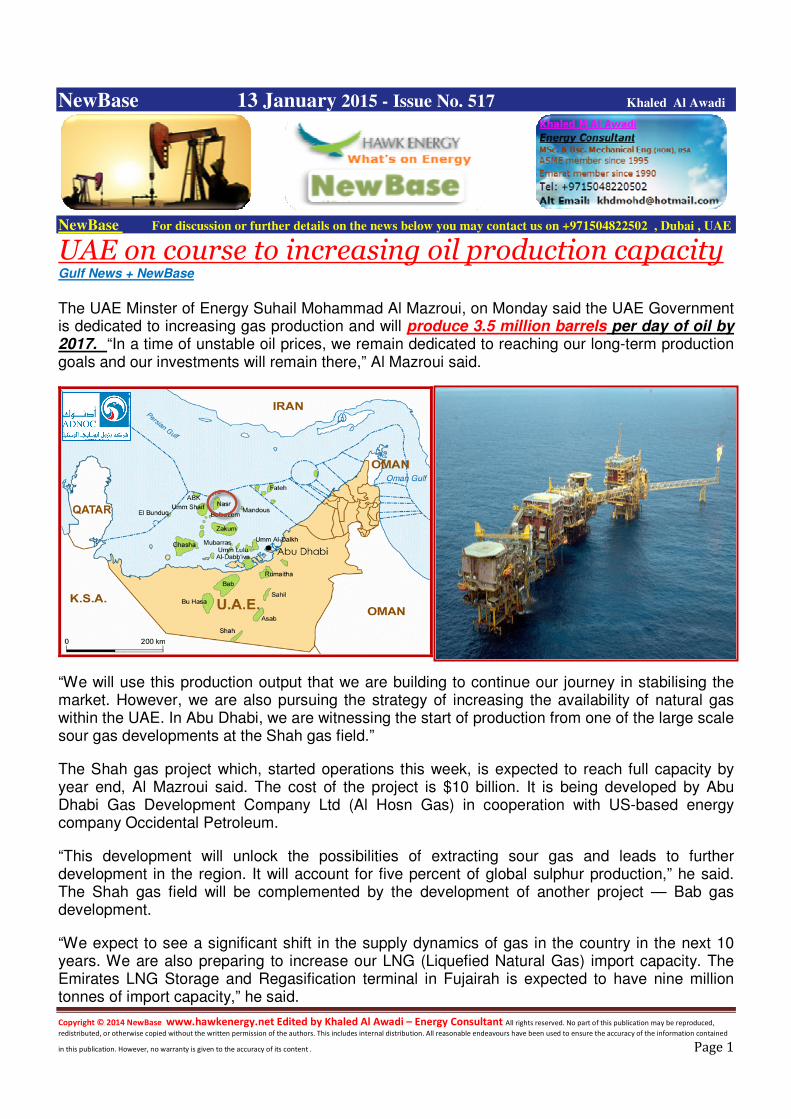

The UAE Minster of Energy Suhail Mohammad Al Mazroui, on Monday said the UAE Government is dedicated to increasing gas production and will produce 3.5 million barrels per day of oil by 2017. “In a time of unstable oil prices, we remain dedicated to reaching our long-term production goals and our investments will remain there,” Al Mazroui said.

“We will use this production output that we are building to continue our journey in stabilising the market. However, we are also pursuing the strategy of increasing the availability of natural gas within the UAE. In Abu Dhabi, we are witnessing the start of production from one of the large scale sour gas developments at the Shah gas field.”

The Shah gas project which, started operations this week, is expected to reach full capacity by year end, Al Mazroui said. The cost of the project is $10 billion. It is being developed by Abu Dhabi Gas Development Company Ltd (Al Hosn Gas) in cooperation with US-based energy company Occidental Petroleum.

“This development will unlock the possibilities of extracting sour gas and leads to further development in the region. It will account for five percent of global sulphur production,” he said. The Shah gas field will be complemented by the development of another project — Bab gas development.

“We expect to see a significant shift in the supply dynamics of gas in the country in the next 10 years. We are also preparing to increase our LNG (Liquefied Natural Gas) import capacity. The Emirates LNG Storage and Regasification terminal in Fujairah is expected to have nine million tonnes of import capacity,” he said.

Copyright © 2014 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced,

redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained

in this publication. However, no warranty is given to the accuracy of its content . Page 2

Al Mazroui added that with the increasing in demand of natural gas and increase in gas prices, the UAE has decided to diversify the sources of power generation to nuclear and renewable energy to reduce the future import of gas volumes. “We will embrace a new energy equation once the nuclear reactors get commissioned by 2020.”

Speaking at an event, Abdullah Nasser Al Suwaidi, Chief Executive of Abu Dhabi National Oil Company (Adnoc), said the Shah sour gas project has started two days ago.

“We look forward to reaching full capacity this year,” he said.

The processed sulphur granules from sour gas will be transported on a purpose-built 266km railway line to the Ruwais port terminal for export. The gas field is located about 210km south-west of Abu Dhabi.

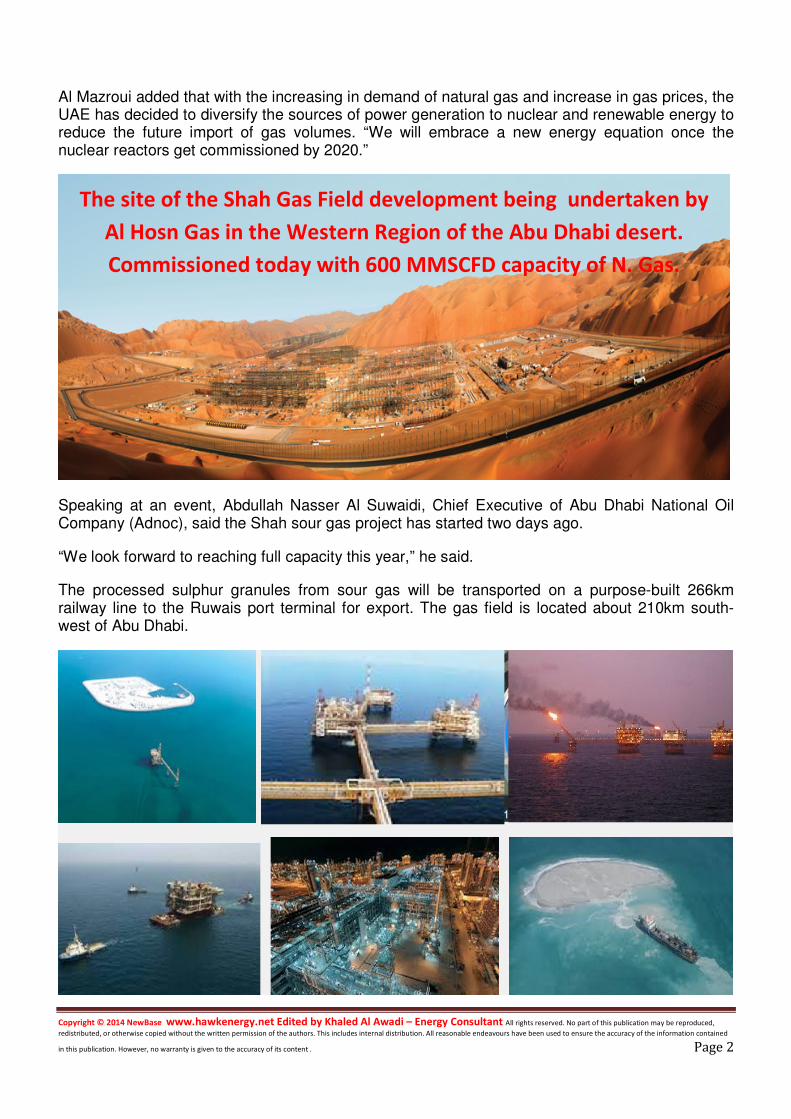

The site of the Shah Gas Field development being undertaken by

Al Hosn Gas in the Western Region of the Abu Dhabi desert.

Commissioned today with 600 MMSCFD capacity of N. Gas.

Copyright © 2014 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced,

redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained

in this publication. However, no warranty is given to the accuracy of its content . Page 3

UAE’s Shah Gas Project Online, To Reach Full Capacity By Year-End – ADNOC The project will process around one billion cubic fe et a day (bcf/d) of sour gas into 0.5

bcf/d of usable gas.

The United Arab Emirates’ Shah gas project has started operations and is expected to reach full capacity by year end, the head of state-run Abu Dhabi National Oil Company (ADNOC) said on Monday.

The multi-billion dollar, technically challenging project with U.S.-based Occidental Petroleum is meant to produce usable gas from Shah’s high-sulphur field. “Successful commissioning of Shah gas project has started… We look forward to reaching full capacity this year,” ADNOC Chief Executive Abdulla Nasser Al Suwaidi told an energy event in Abu Dhabi.

The project to process around one billion cubic feet a day (bcf/d) of sour gas into 0.5 bcf/d of usable gas in the remote desert is vital for keeping the UAE supplied with fuel and reducing its growing gas imports. As well as gas for industry and power generation, Shah will produce significant volumes of condensate, a light oil that can be used to make vehicle fuels.

“With the Shah gas development start-up we will see the UAE accounting for almost five per cent of global sulphur production,” the UAE energy minister Suhail bin Mohammed al-Mazrouei said at the same event.

The UAE had said it plans to produce 22,000 tonnes of sulphur a day by 2015, which positions it to be a leading world sulphur exporter.

Sulphur is used in the manufacturing of fertilisers and sulphuric acid, which is used in oil refining, wastewater processing and mineral extraction.ADNOC holds a 60 per cent share in the Shah gas development joint venture, called Al Hosn Gas, while Occidental holds 40 per cent.

Ma Sha Allah

Copyright © 2014 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced,

redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained

in this publication. However, no warranty is given to the accuracy of its content . Page 4

Qatar set to see new project deals worth $30bn in 2015

Meed + NewBase

Qatar’s infrastructure projects pipeline is set to soar with more than $30bn worth of new project deals in 2015, according to the latest data from online projects tracker Meed Projects. The record year has come on the back of major project awards on Ashghal’s Expressway and Local Roads and Drainage Programmes as well as significant investment in real estate and transport projects such as Msheireb, Lusail and the New Port Project.

This year will be boosted by forecasted project awards on the $5bn-plus Al-Karaana petrochemical complex, the $2bn-plus rolling stock and systems contract on the Doha Metro, and five main

multi-billion-dollar packages on the mega water reservoirs main packages.

“Despite falling oil prices, Qatar has the project pipeline, the political impetus, and the financial reserves to continue project spending as it prepares to host the FIFA 2022 World Cup,” said Ed James, director (Analysis) at Meed Projects. “With around $30bn worth of projects, 2014 witnessed a 25% increase in project spending as compare to the year 2013, and there will continue to be an upward trend in project activity.” Project spending will be boosted by the fact that Qatar continues to be the fastest-growing economy in the GCC in the years to 2020 as the country presses ahead with one of the world’s most comprehensive and ambitious economic development and infrastructure programmes, the annual Meed Qatar Projects Conference in Doha on March 10 & 11 March 2015 will be told. According to the Qatar’s Ministry of Development Planning & Statistics, Qatar’s economy will expand by 7.7% in 2015, providing evidence that the world’s leading LNG exporter expects lower oil prices will have minimal impact on growth. “Solid expansion in non-hydrocarbon activities will continue to drive overall economic momentum, propelled by investment spending, an expansionary fiscal stance and population growth,” the ministry said. “In calendar years 2014-2016, the overall fiscal balance is expected to stay in surplus.” Qatar is the Middle East’s “most creditworthy” economy. The Standard & Poor’s credit rating is AA. Moody’s rating for Qatar sovereign debt is Aa2. The IMF’s annual Article IV report on the Qatar economy published earlier this year showed Qatar’s budget and balance of payments’ surpluses were by far the highest in the region and were among the largest in the world. Its financial reserves are more than 100% of GDP.

10 - 11 March 2015

Grand Hyatt, Doha

Copyright © 2014 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced,

redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained

in this publication. However, no warranty is given to the accuracy of its content . Page 5

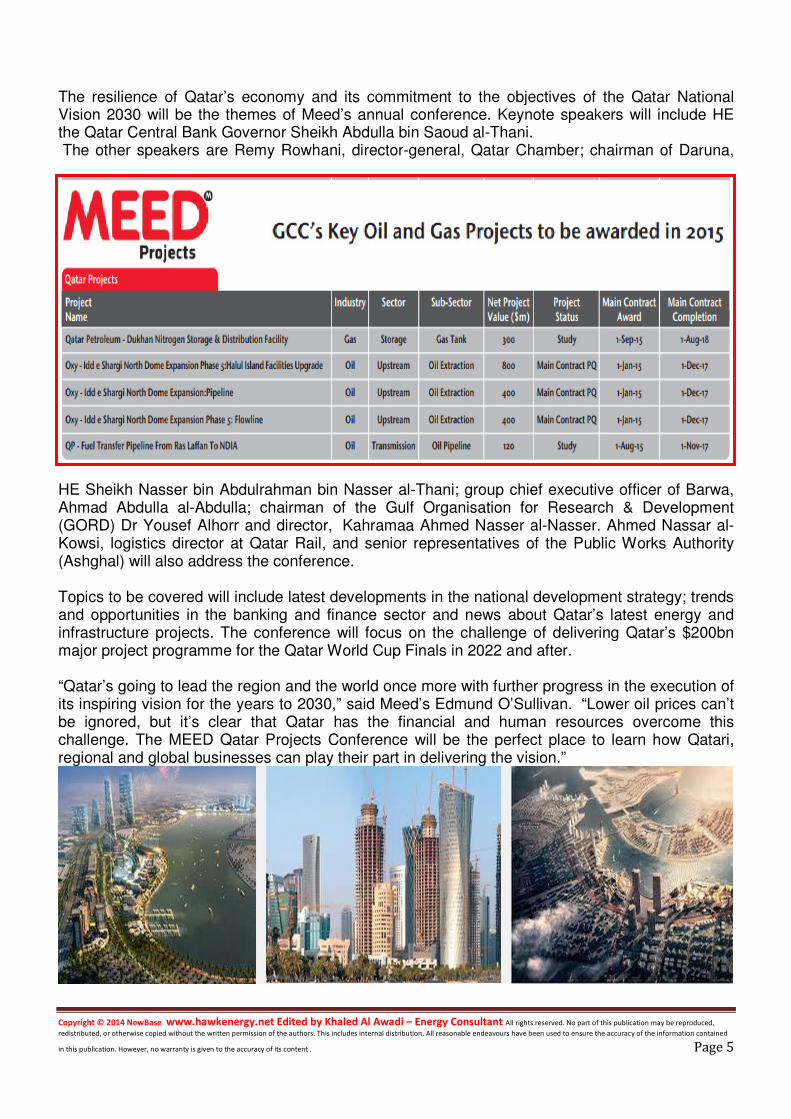

The resilience of Qatar’s economy and its commitment to the objectives of the Qatar National Vision 2030 will be the themes of Meed’s annual conference. Keynote speakers will include HE the Qatar Central Bank Governor Sheikh Abdulla bin Saoud al-Thani. The other speakers are Remy Rowhani, director-general, Qatar Chamber; chairman of Daruna,

HE Sheikh Nasser bin Abdulrahman bin Nasser al-Thani; group chief executive officer of Barwa, Ahmad Abdulla al-Abdulla; chairman of the Gulf Organisation for Research & Development (GORD) Dr Yousef Alhorr and director, Kahramaa Ahmed Nasser al-Nasser. Ahmed Nassar al-Kowsi, logistics director at Qatar Rail, and senior representatives of the Public Works Authority (Ashghal) will also address the conference. Topics to be covered will include latest developments in the national development strategy; trends and opportunities in the banking and finance sector and news about Qatar’s latest energy and infrastructure projects. The conference will focus on the challenge of delivering Qatar’s $200bn major project programme for the Qatar World Cup Finals in 2022 and after. “Qatar’s going to lead the region and the world once more with further progress in the execution of its inspiring vision for the years to 2030,” said Meed’s Edmund O’Sullivan. “Lower oil prices can’t be ignored, but it’s clear that Qatar has the financial and human resources overcome this challenge. The MEED Qatar Projects Conference will be the perfect place to learn how Qatari, regional and global businesses can play their part in delivering the vision.”

Copyright © 2014 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced,

redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained

in this publication. However, no warranty is given to the accuracy of its content . Page 6

Robust downstream industries supports GCC economies Oman Observer

The robust growth of downstream industries will enable the GCC economies to strengthen their economic diversification efforts and by-pass market volatilities, according to a new report by the Gulf Petrochemicals and Chemicals Association (GPCA) and the international consultancy firm Nexant.

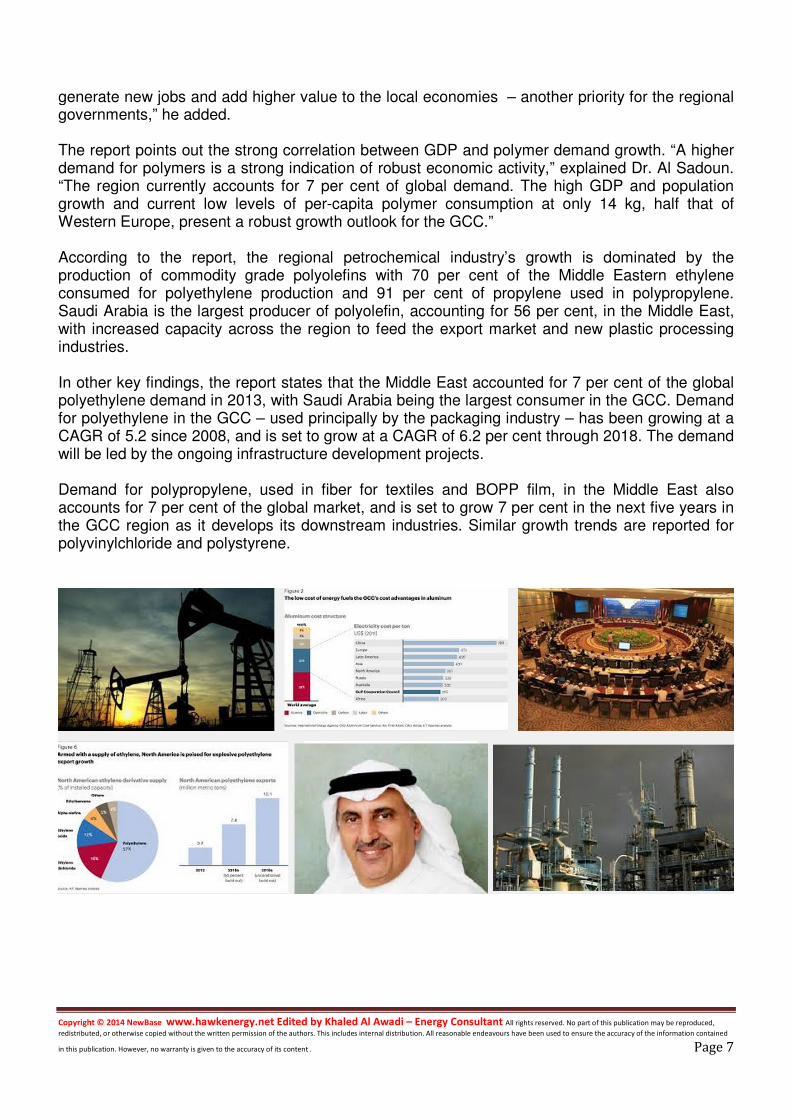

The report titled ‘A New Horizon for the GCC Plastic Processing Industry’ will be released during the 6th edition of GPCA PlastiCon 2015, the annual international conference for plastics conversion underway in Dubai. Presenting a compelling overview of the industry, the report highlights that polymer production in the GCC region has increased dramatically led by thriving exports and rising local demand. Plastics exports made up for the largest non-oil sector contribution to the Saudi Arabian economy accounting for 35 per cent of the non-oil export revenues. The report states that the focus of Saudi Arabia and the UAE to boost the growth of small and medium enterprises (SMEs) for plastic processing will further benefit the industry. “Saudi Arabia aims to be a world top-10 exporter of plastics and create 17,000 additional jobs in the sector, while Abu Dhabi is fast emerging as an important hub for plastic convertors,” said Dr Abdulwahab al Sadoun, Secretary-General, GPCA. “One of the prevailing trends across the region is the focus on optimising petrochemical integration to support the economic diversification programmes in the GCC,” said Dr Al Sadoun. “With the current low oil prices, this shift towards plastic processing has the potential to be a game changer for the region. It will not only drive increased exports but also support local industries that

Copyright © 2014 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced,

redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained

in this publication. However, no warranty is given to the accuracy of its content . Page 7

generate new jobs and add higher value to the local economies – another priority for the regional governments,” he added. The report points out the strong correlation between GDP and polymer demand growth. “A higher demand for polymers is a strong indication of robust economic activity,” explained Dr. Al Sadoun. “The region currently accounts for 7 per cent of global demand. The high GDP and population growth and current low levels of per-capita polymer consumption at only 14 kg, half that of Western Europe, present a robust growth outlook for the GCC.” According to the report, the regional petrochemical industry’s growth is dominated by the production of commodity grade polyolefins with 70 per cent of the Middle Eastern ethylene consumed for polyethylene production and 91 per cent of propylene used in polypropylene. Saudi Arabia is the largest producer of polyolefin, accounting for 56 per cent, in the Middle East, with increased capacity across the region to feed the export market and new plastic processing industries. In other key findings, the report states that the Middle East accounted for 7 per cent of the global polyethylene demand in 2013, with Saudi Arabia being the largest consumer in the GCC. Demand for polyethylene in the GCC – used principally by the packaging industry – has been growing at a CAGR of 5.2 since 2008, and is set to grow at a CAGR of 6.2 per cent through 2018. The demand will be led by the ongoing infrastructure development projects. Demand for polypropylene, used in fiber for textiles and BOPP film, in the Middle East also accounts for 7 per cent of the global market, and is set to grow 7 per cent in the next five years in the GCC region as it develops its downstream industries. Similar growth trends are reported for polyvinylchloride and polystyrene.

Copyright © 2014 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced,

redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained

in this publication. However, no warranty is given to the accuracy of its content . Page 8

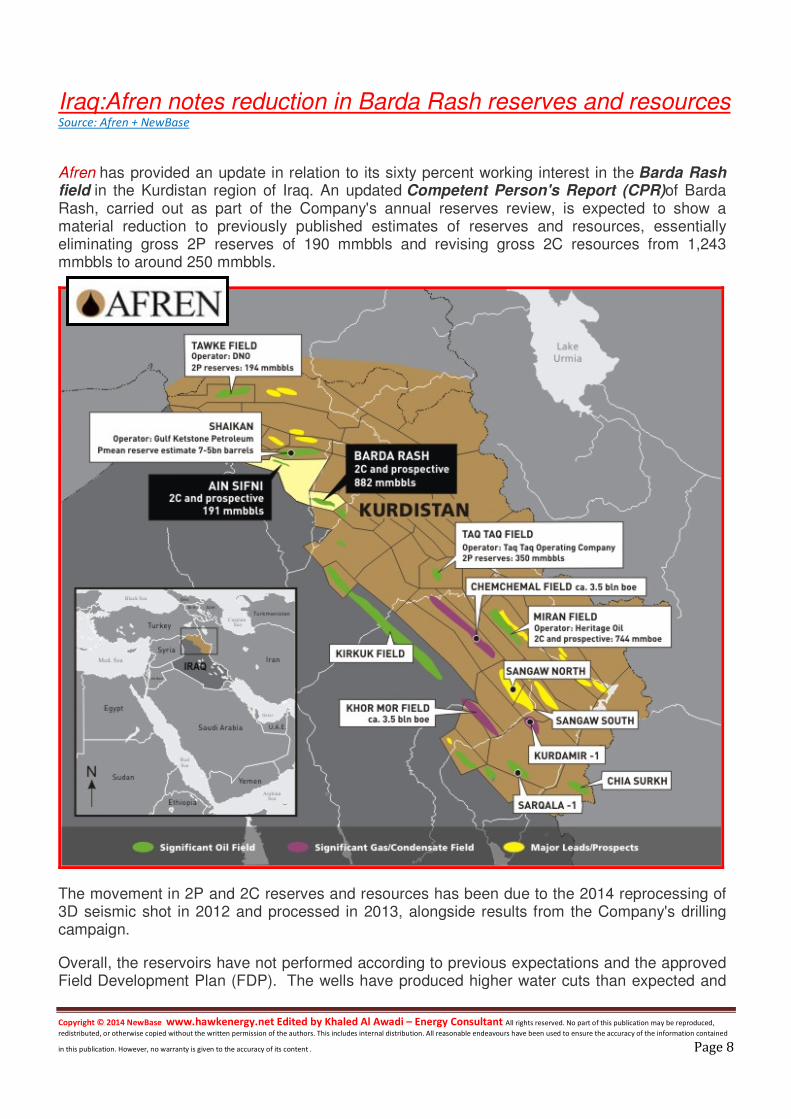

Iraq:Afren notes reduction in Barda Rash reserves and resources Source: Afren + NewBase

Afren has provided an update in relation to its sixty percent working interest in the Barda Rash field in the Kurdistan region of Iraq. An updated Competent Person's Report (CPR)of Barda Rash, carried out as part of the Company's annual reserves review, is expected to show a material reduction to previously published estimates of reserves and resources, essentially eliminating gross 2P reserves of 190 mmbbls and revising gross 2C resources from 1,243 mmbbls to around 250 mmbbls.

The movement in 2P and 2C reserves and resources has been due to the 2014 reprocessing of 3D seismic shot in 2012 and processed in 2013, alongside results from the Company's drilling campaign.

Overall, the reservoirs have not performed according to previous expectations and the approved Field Development Plan (FDP). The wells have produced higher water cuts than expected and

Copyright © 2014 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced,

redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained

in this publication. However, no warranty is given to the accuracy of its content . Page 9

the Company has encountered operational challenges associated with the drilling of difficult complex fractured reservoirs. Production from these reservoirs could potentially be achieved with the implementation of recovery schemes requiring significant capital expenditure, which may well be appropriate for a company with a different strategic focus.

Furthermore, while recent results at the field have indicated the presence of light oil accumulations from the deeper Triassic Kurra Chine reservoirs, these have a high level of associated Hydrogen Sulfide (H2S), which would require significant capital expenditure to develop. In light of the above, the Company is now considering its strategic options for the Barda Rash field.

As part of the current work programme on Barda Rash, the Company will continue with its commitment to complete the testing of the BR-5 well. The Company will publish the completed CPR once it is

finalised.

Toby Hayward, Interim Chief Executive Officer, commented:

'We are naturally disappointed with the CPR and will now consider our strategic options for Barda Rash. Meanwhile, we will continue to focus on our core portfolio in Africa and allocate capital to our highest cash return projects.'

About Afren

Afren plc is an international independent exploration and production (E&P) company with a Premium Listing on the London Stock Exchange (symbol AFR) and a constituent of the FTSE 250 Index.

Afren is a dynamic, entrepreneurial organisation with a portfolio ofworld-class assets located in several of the world’s most prolific and fast-emerging hydrocarbon basins in Africa and the Middle East. Our activities span the full-cycle E&P value chain of exploration, appraisal, development through to production. Our success depends on our ability to deliver long-term value for all our stakeholders through a clear and consistent strategy, which recognises that our responsibilities go beyond our operations.

To leverage our track record of operational delivery and effective portfolio and financial management our business has been strategically positioned into three core business units, Nigeria and other West Africa, Afren East Africa Exploration and the Kurdistan region of Iraq.

Copyright © 2014 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced,

redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained

in this publication. However, no warranty is given to the accuracy of its content . Page 10

India: Adani Enterprises & Woodside sign LNG MoU Woodside + NewBase

LNG player Woodside said that it has executed a memorandum of understanding with

India’s Adani Enterprises.

The MoU was signed at a ceremony in Gujarat, attended by senior company representatives and Andrew Robb, Australia’s Minister for Trade and Investment.

Under the terms of the non-binding MoU, Woodside and Adani agree to cooperate in identifying, investigating and developing potential business arrangements and commercial initiatives.

Woodside CEO and Managing Director Peter Coleman said that the MoU marked a

significant milestone in strengthening relations between the two companies.

According to Coleman, Woodside sees India as an important emerging LNG market in which the company sees enormous supply potential as infrastructure is developed.

The MoU was signed by Adani Chairman Gautam Adani and Woodside’s CEO and Managing Director Peter Coleman.

Copyright © 2014 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced,

redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained

in this publication. However, no warranty is given to the accuracy of its content . Page 11

Wood Mackenzie reviews UK Upstream sector Source: Wood Mackenzie

Investment continued to boom in the UK in 2014 with US$19 billion (£12 billion) of capital expenditure pumped into the sector – keeping the UK in the top 10 countries for upstream spend globally. Wood Mackenzie’s annual United Kingdom (UK) Upstream review, says this investment meant after several years of steep decline, UK production stabilised and is even expected to grow in the near term. However, Wood Mackenzie also warns that 2014 was a very challenging year for the United Kingdom Continental Shelf (UKCS) with rising costs, poor exploration results and falling oil prices squeezing already tight project economics – casting further concern over the outlook for 2015 and beyond. Erin Moffat, UK Upstream Senior Research Analyst for Wood Mackenzie explains: “In 2014, the investment boom that began in 2011 continued with capital investment at US$19 billion, driven by sustained high levels of activity and high costs including progress on the development of more technically challenging projects.” “The UK remained in the top 10 countries for upstream spending globally” According to Wood Mackenzie’s latest analysis, this sustained level of investment ensured the UK remained in the top 10 countries for upstream spending globally, with nearly a third of the total UK spend – around US$6 billion (or £3.8 billion) – associated with just five assets last year – Mariner, Schiehallion, Laggan, Clair and Golden Eagle.

Pressure for tax cuts However, Moffat continues: “The high cost environment in the UK meant that project returns were already subject to increased scrutiny during 2014. The dramatic fall in oil price towards the end of last year only adds to this. The UK Government reduced the tax rate by 2% in December 2014, but we expect growing pressure to reduce it further. At an oil price of $60/barrel, 95% of pre-sanction oil & gas reserves in the UK generate less than a 15% return on investment. “UKCS exploration and appraisal activity continued to fall in 2014, with the number of exploration wells decreasing by 18% to just 23 wells” “This has intensified concerns over future UKCS investment as further cuts or delays to projects are likely. A low oil price could also impact producing fields with high operating costs, with the potential for shut-ins. We estimate US$3.2 billion (£2.0 billion) of spend associated with pre sanction projects could be at risk over the next two years as a result of current oil prices. Without this, UK Upstream spend in 2016 would be around US$10 billion (£6.3 billion) – just over half of 2014 levels.” “UKCS exploration and appraisal activity continued to fall in 2014, with the number of exploration wells decreasing by 18% to just 23 wells. 2014 drilling was considerably lower than the previous ten year average of 81 wells per year, due to restricted access to finance for some players, high costs, a stretched service sector, and a focus by some companies on progressing large, capital intensive development projects. The current oil price means 2015 will unsurprisingly bring further budget cuts – with exploration spend top of the list.” Moffat adds.

Copyright © 2014 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced,

redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained

in this publication. However, no warranty is given to the accuracy of its content . Page 12

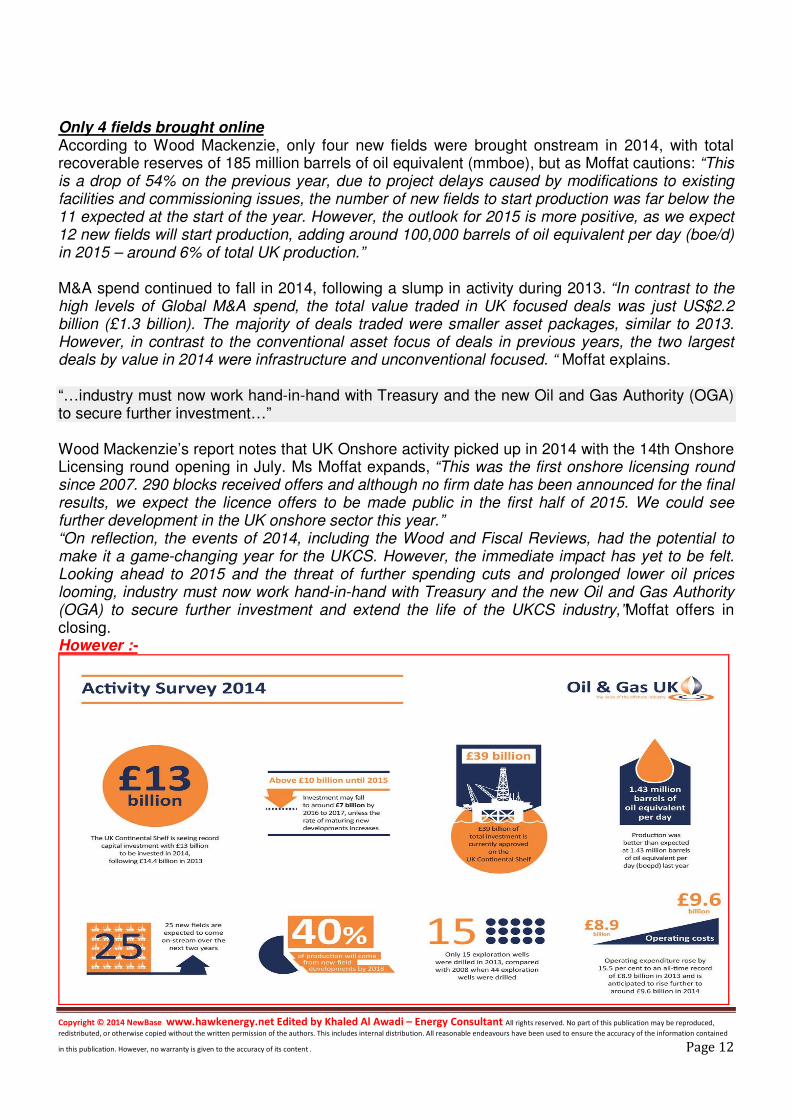

Only 4 fields brought online According to Wood Mackenzie, only four new fields were brought onstream in 2014, with total recoverable reserves of 185 million barrels of oil equivalent (mmboe), but as Moffat cautions: “This is a drop of 54% on the previous year, due to project delays caused by modifications to existing facilities and commissioning issues, the number of new fields to start production was far below the 11 expected at the start of the year. However, the outlook for 2015 is more positive, as we expect 12 new fields will start production, adding around 100,000 barrels of oil equivalent per day (boe/d) in 2015 – around 6% of total UK production.” M&A spend continued to fall in 2014, following a slump in activity during 2013. “In contrast to the high levels of Global M&A spend, the total value traded in UK focused deals was just US$2.2 billion (£1.3 billion). The majority of deals traded were smaller asset packages, similar to 2013. However, in contrast to the conventional asset focus of deals in previous years, the two largest deals by value in 2014 were infrastructure and unconventional focused. “ Moffat explains. “…industry must now work hand-in-hand with Treasury and the new Oil and Gas Authority (OGA) to secure further investment…” Wood Mackenzie’s report notes that UK Onshore activity picked up in 2014 with the 14th Onshore Licensing round opening in July. Ms Moffat expands, “This was the first onshore licensing round since 2007. 290 blocks received offers and although no firm date has been announced for the final results, we expect the licence offers to be made public in the first half of 2015. We could see further development in the UK onshore sector this year.” “On reflection, the events of 2014, including the Wood and Fiscal Reviews, had the potential to make it a game-changing year for the UKCS. However, the immediate impact has yet to be felt. Looking ahead to 2015 and the threat of further spending cuts and prolonged lower oil prices looming, industry must now work hand-in-hand with Treasury and the new Oil and Gas Authority (OGA) to secure further investment and extend the life of the UKCS industry,”Moffat offers in closing. However :-

Copyright © 2014 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced,

redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained

in this publication. However, no warranty is given to the accuracy of its content . Page 13

Oil Price Drop Special Coverage

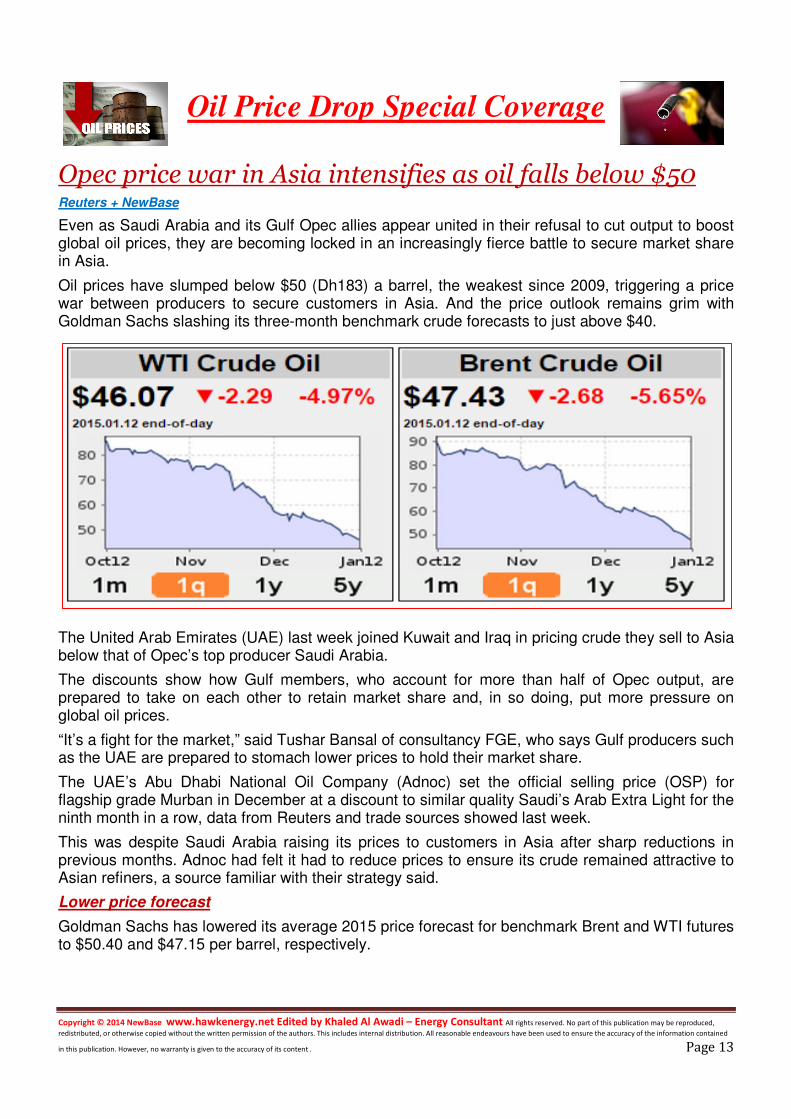

Opec price war in Asia intensifies as oil falls below $50 Reuters + NewBase

Even as Saudi Arabia and its Gulf Opec allies appear united in their refusal to cut output to boost global oil prices, they are becoming locked in an increasingly fierce battle to secure market share in Asia.

Oil prices have slumped below $50 (Dh183) a barrel, the weakest since 2009, triggering a price war between producers to secure customers in Asia. And the price outlook remains grim with Goldman Sachs slashing its three-month benchmark crude forecasts to just above $40.

The United Arab Emirates (UAE) last week joined Kuwait and Iraq in pricing crude they sell to Asia below that of Opec’s top producer Saudi Arabia.

The discounts show how Gulf members, who account for more than half of Opec output, are prepared to take on each other to retain market share and, in so doing, put more pressure on global oil prices.

“It’s a fight for the market,” said Tushar Bansal of consultancy FGE, who says Gulf producers such as the UAE are prepared to stomach lower prices to hold their market share.

The UAE’s Abu Dhabi National Oil Company (Adnoc) set the official selling price (OSP) for flagship grade Murban in December at a discount to similar quality Saudi’s Arab Extra Light for the ninth month in a row, data from Reuters and trade sources showed last week.

This was despite Saudi Arabia raising its prices to customers in Asia after sharp reductions in previous months. Adnoc had felt it had to reduce prices to ensure its crude remained attractive to Asian refiners, a source familiar with their strategy said.

Lower price forecast

Goldman Sachs has lowered its average 2015 price forecast for benchmark Brent and WTI futures to $50.40 and $47.15 per barrel, respectively.

Copyright © 2014 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced,

redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained

in this publication. However, no warranty is given to the accuracy of its content . Page 14

The US bank cut its three-month price forecast for Brent to $42 from $80 and US crude to $41, down from $70, adding it would need to stay near $40 for most of the first half of 2015 before it would hold up shale oil investments.

“To keep all capital sidelined and curtail investment in shale until the market has rebalanced, we believe prices need to stay lower for longer,” its analysts said in a report. As well as targeting North American shale, oil ministers from Opec, including the UAE, have called for exporters, such as Russia, to cut output to lift prices. Russia, in turn, wants Opec and Saudi Arabia in particular to cut production first.

Over the past decade, UAE’s Murban OSP has been on average 15 cents a barrel higher than Saudi’s Extra Light OSP, but the relationship between the grades switched since April last year, the data showed. In September, Murban was priced at the widest discount to Extra Light in over a decade at $2.28.

Another Abu Dhabi grade, Upper Zakum, also flipped into a discount against Saudi’s Arab Medium in December, even though Upper Zakum has been priced at an average premium of $1.11 a barrel above the Saudi grade in the last decade.

Adnoc sets its prices two months behind those of Saudi, Kuwait and Iraq, which gives the UAE’s main producer more time to react to market changes.

The UAE, Opec’s fifth largest producer, has been expanding its output and remains on track to boost production capacity to 3.5 million barrels per day by 2017, up from about 2.8 million bpd, its oil minister said in remarks published last week.

The UAE’s price cuts have spurred demand for Abu Dhabi grades in the spot market, with Taiwanese refiner CPC Corp buying volumes of Murban crude at the start of the year. But Bansal of consultancy FGE warned that to restore market balance output cuts will have to come from Opec and non-Opec producers.

“If no one blinks, then prices will continue to drop.”

The long and the short view of oil fall’s impact on US investment The National + NewBase

There are two schools of thought about the effect of lower oil prices on US upstream investment: those who expe ct a quick, chilling effect on the booming shale oil sector, and those who see investment remaining resilient as fleet-footed smaller players cut costs further. Count the chief

executive of the newly merged Amec Foster Wheeler oil services conglomerate in the latter camp.

“Many of the small operators in the US are really entrepreneurs — these are not the BPs or the Exxons — and they have enough money, banker’s money, to sustain investment for six, seven more months at least,” says Samir Brikho, previously head of the UK-based oil services group Amec, which completed a

US$3 billion takeover of US-listed Foster Wheeler in November.

It is one of the central questions facing the industry since oil prices collapsed at the end of last year: how long will it take for the strategy being pursued by Saudi Arabia and its allies, of

Copyright © 2014 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced,

redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained

in this publication. However, no warranty is given to the accuracy of its content . Page 15

encouraging lower oil prices to force off the market higher-cost production from North America and elsewhere, to stabilise the market?

The answer, according to Mr Brikho, is that it will take quite some time. “Why do many people think that this cycle is going to be longer than before and at a lower [price] base? Because if Saudi is going to be successful in squeezing producers out they need to continue to do this for a minimum period of six to nine months,” he reckons.

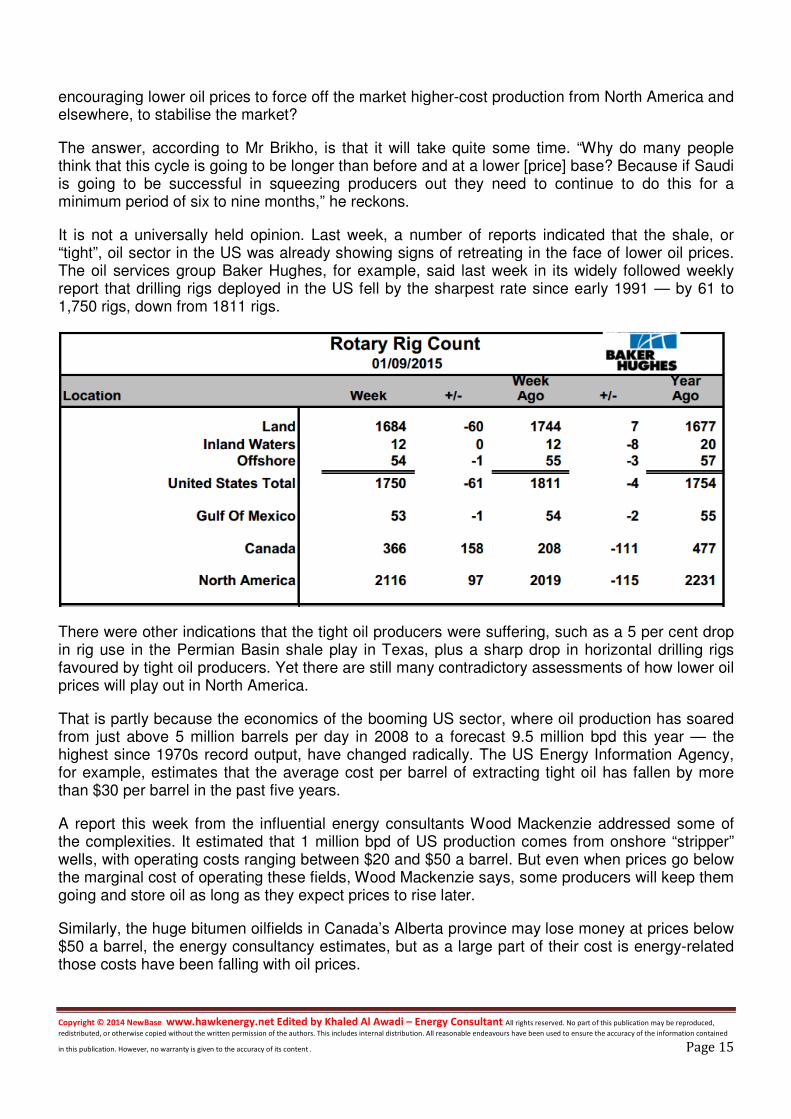

It is not a universally held opinion. Last week, a number of reports indicated that the shale, or “tight”, oil sector in the US was already showing signs of retreating in the face of lower oil prices. The oil services group Baker Hughes, for example, said last week in its widely followed weekly report that drilling rigs deployed in the US fell by the sharpest rate since early 1991 — by 61 to 1,750 rigs, down from 1811 rigs.

There were other indications that the tight oil producers were suffering, such as a 5 per cent drop in rig use in the Permian Basin shale play in Texas, plus a sharp drop in horizontal drilling rigs favoured by tight oil producers. Yet there are still many contradictory assessments of how lower oil prices will play out in North America.

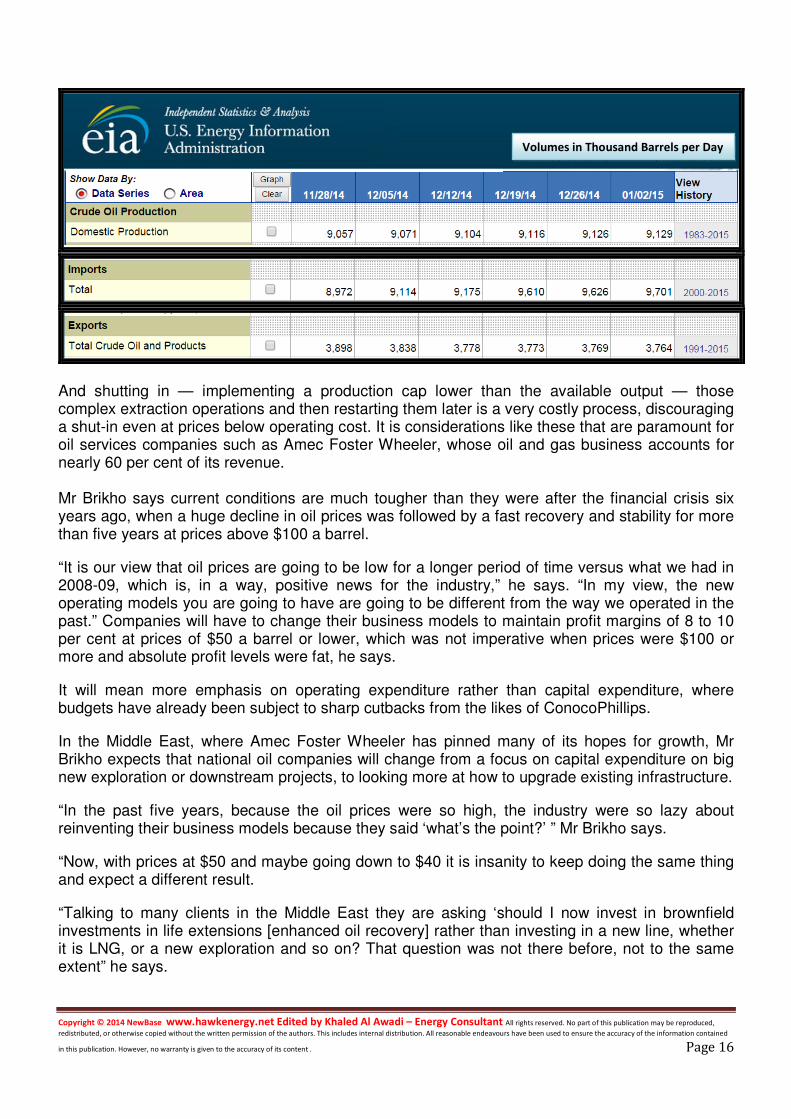

That is partly because the economics of the booming US sector, where oil production has soared from just above 5 million barrels per day in 2008 to a forecast 9.5 million bpd this year — the highest since 1970s record output, have changed radically. The US Energy Information Agency, for example, estimates that the average cost per barrel of extracting tight oil has fallen by more than $30 per barrel in the past five years.

A report this week from the influential energy consultants Wood Mackenzie addressed some of the complexities. It estimated that 1 million bpd of US production comes from onshore “stripper” wells, with operating costs ranging between $20 and $50 a barrel. But even when prices go below the marginal cost of operating these fields, Wood Mackenzie says, some producers will keep them going and store oil as long as they expect prices to rise later.

Similarly, the huge bitumen oilfields in Canada’s Alberta province may lose money at prices below $50 a barrel, the energy consultancy estimates, but as a large part of their cost is energy-related those costs have been falling with oil prices.

Copyright © 2014 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced,

redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained

in this publication. However, no warranty is given to the accuracy of its content . Page 16

And shutting in — implementing a production cap lower than the available output — those complex extraction operations and then restarting them later is a very costly process, discouraging a shut-in even at prices below operating cost. It is considerations like these that are paramount for oil services companies such as Amec Foster Wheeler, whose oil and gas business accounts for nearly 60 per cent of its revenue. Mr Brikho says current conditions are much tougher than they were after the financial crisis six years ago, when a huge decline in oil prices was followed by a fast recovery and stability for more than five years at prices above $100 a barrel.

“It is our view that oil prices are going to be low for a longer period of time versus what we had in 2008-09, which is, in a way, positive news for the industry,” he says. “In my view, the new operating models you are going to have are going to be different from the way we operated in the past.” Companies will have to change their business models to maintain profit margins of 8 to 10 per cent at prices of $50 a barrel or lower, which was not imperative when prices were $100 or more and absolute profit levels were fat, he says.

It will mean more emphasis on operating expenditure rather than capital expenditure, where budgets have already been subject to sharp cutbacks from the likes of ConocoPhillips.

In the Middle East, where Amec Foster Wheeler has pinned many of its hopes for growth, Mr Brikho expects that national oil companies will change from a focus on capital expenditure on big new exploration or downstream projects, to looking more at how to upgrade existing infrastructure.

“In the past five years, because the oil prices were so high, the industry were so lazy about reinventing their business models because they said ‘what’s the point?’ ” Mr Brikho says.

“Now, with prices at $50 and maybe going down to $40 it is insanity to keep doing the same thing and expect a different result.

“Talking to many clients in the Middle East they are asking ‘should I now invest in brownfield investments in life extensions [enhanced oil recovery] rather than investing in a new line, whether it is LNG, or a new exploration and so on? That question was not there before, not to the same extent” he says.

Volumes in Thousand Barrels per Day

Copyright © 2014 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced,

redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained

in this publication. However, no warranty is given to the accuracy of its content . Page 17

A new report from the consulting group McKinsey supports the view that business models will need to change.

The rising costs and more demanding conditions of giant offshore projects means that with lower oil prices they will need to drive costs down by focusing on specific basins where they have expertise, it argues.

“The new caution in capital expenditure will require companies to choose the projects best suited to their strengths, which in turn means not only thinking hard about capabilities, but also knowing more precisely the financial effect that the different factors have in each basin,” according to McKinsey’s Thomas Seitz and Kassia Yanosek.

There may be an element of wishful thinking in Mr Brikho’s expectation that the industry will continue to spend, even if companies concentrate more on lower-margin operating expenditure to make up for reduced capital expenditure.

Amec Foster Wheeler’s shares are down about one-third from their peak in June last year, trading at about 840 pence in London in early January. But that is much better than a lot of its peers — Petrofac is down closer to 60 per cent, while shares in Italy’s Saipem have lost two-thirds of their value compared with June figures.

Amec Foster Wheeler’s resilience has a lot to do with its more diversified portfolio — power, which makes up about 20 per cent of revenues, grew at 16 per cent in the half year to June, while oil and gas revenues fell by 4 per cent.

The company also has about 20 per cent of its business in renewable energy, including nuclear. It has supplied an estimated 10 per cent of the US photovoltaic solar market capacity and is bidding for a slice of the big Saudi solar investment that is expected.

It will need that diversification to weather the oil price storm.

Copyright © 2014 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced,

redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained

in this publication. However, no warranty is given to the accuracy of its content . Page 18

NewBase For discussion or further details on the news below you may contact us on +971504822502 , Dubai , UAE

Your Guide to Energy events in your area

Copyright © 2014 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced,

redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained

in this publication. However, no warranty is given to the accuracy of its content . Page 19

NewBase For discussion or further details on the news below you may contact us on +971504822502 , Dubai , UAE

Your partner in Energy Services

NewBase energy news is produced daily (Sunday to Thursday) and

sponsored by Hawk Energy Service – Dubai, UAE.

For additional free subscription emails please contact Hawk Energy

Khaled Malallah Al Awadi, Energy Consultant MS & BS Mechanical Engineering (HON), USA Emarat member since 1990 ASME member since 1995 Hawk Energy member 2010

Mobile : +97150-4822502 [email protected] [email protected]

Khaled Al Awadi is a UAE National with a total of 25 years of experience in the Oil & Gas sector. Currently working as Technical Affairs Specialist for Emirates General Petroleum Corp. “Emarat“ with external voluntary Energy consultation for the GCC area via Hawk Energy Service as a UAE operations base , Most of the experience were spent as the Gas Operations Manager in Emarat , responsible for Emarat Gas Pipeline Network Facility & gas compressor stations . Through the years , he has developed great experiences in the designing & constructing of gas pipelines, gas metering &

regulating stations and in the engineering of supply routes. Many years were spent drafting, & compiling gas transportation , operation & maintenance agreements along with many MOUs for the local authorities. He has become a reference for many of the Oil & Gas Conferences held in the UAE and Energy program broadcasted internationally , via GCC leading satellite Channels.

NewBase : For discussion or further details on the news above you may contact us on +971504822502 , Dubai , UAE

NewBase 13 January 2015 K. Al Awadi

Copyright © 2014 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced,

redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained

in this publication. However, no warranty is given to the accuracy of its content . Page 20

Copyright © 2014 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced,

redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained

in this publication. However, no warranty is given to the accuracy of its content . Page 21