Embed Size (px)

Citation preview

Copyright © 2014 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced,

redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained

in this publication. However, no warranty is given to the accuracy of its content . Page 1

NewBase 07 January 2014 Khaled Al Awadi

NewBase For discussion or further details on the news below you may contact us on +971504822502 , Dubai , UAE

Libya pays price of strikes despite oil boom By: April Yee , http://www.thenational.ae/business

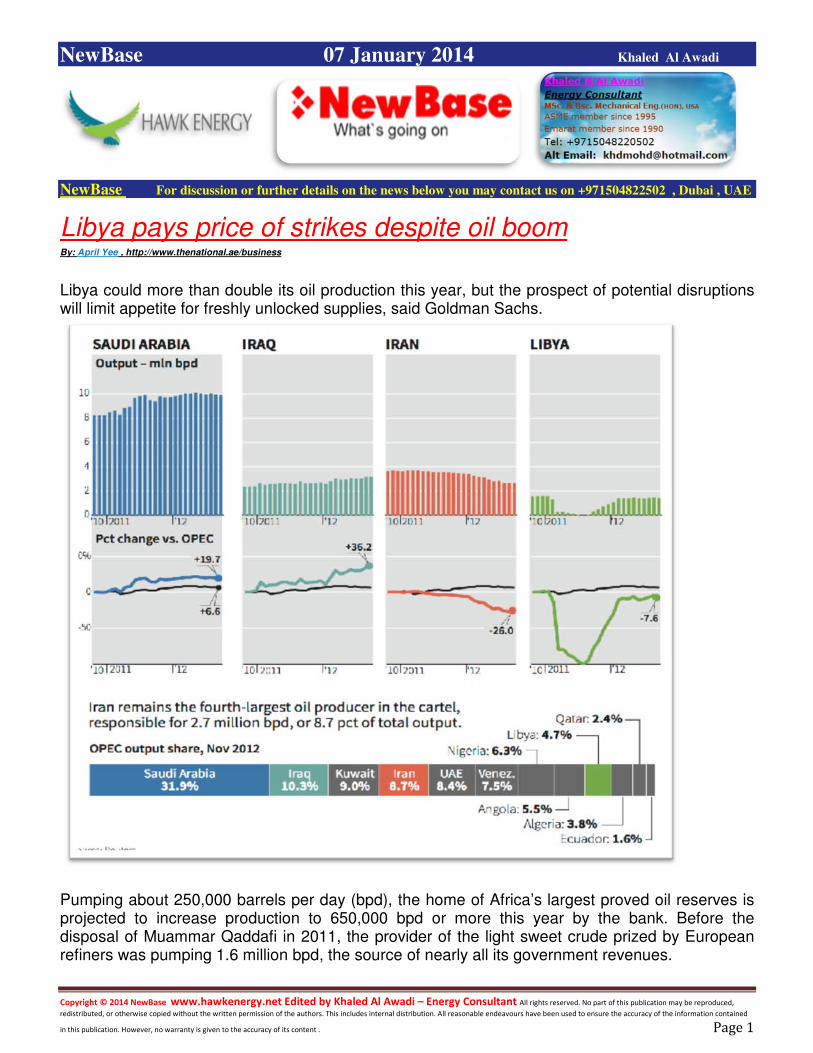

Libya could more than double its oil production this year, but the prospect of potential disruptions will limit appetite for freshly unlocked supplies, said Goldman Sachs.

Pumping about 250,000 barrels per day (bpd), the home of Africa’s largest proved oil reserves is projected to increase production to 650,000 bpd or more this year by the bank. Before the disposal of Muammar Qaddafi in 2011, the provider of the light sweet crude prized by European refiners was pumping 1.6 million bpd, the source of nearly all its government revenues.

Copyright © 2014 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced,

redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained

in this publication. However, no warranty is given to the accuracy of its content . Page 2

“In our view, Libya remains one of the key Opec suppliers to watch in 2014,” wrote a team of the bank’s analysts in a research note yesterday. But, it added: “The demand for Libyan crude oil will likely remain below potential. We believe that the elevated uncertainty around crude oil supply from Libya and the associated risks to potential customers [physical traders and refiners] will likely limit the marketability of Libyan crude grades in the short term.”

Sentiment about Libya’s production prospects buoyed this week as oil began flowing again from Al Sharara, one of the country’s largest fields. Operated by Spain’s Repsol, it is producing 60,000 bpd, according to Libya’s National Oil Corporation, representing a fifth of the field’s normal production. Despite the fresh supplies, which are expected to be able to reach international markets through the Zawiya terminal in the country’s west, Goldman kept its forecast of 650,000 bpd of average production this year steady.

“The recent developments in Libya are consistent with our Brent price forecast for 2014, in particular as we believe that a resolution of the conflicts in Western Libya does not necessarily increase the likelihood of a resolution of the conflicts in Eastern Libya,” said the bank. “Our supply forecast for Libya therefore remains unchanged at 650,000 bpd on average through 2014, while we believe that the risks to this supply forecast are skewed to the upside.” Brent crude futures inched up 92 cents to US$107.81 a barrel yesterday.

Two years after the revolution, Libya’s government is struggling to rein in militias and tribesmen who have refused to give up arms and have taken control of much of the country’s crude export facilities. Fifty-eight per cent of the country’s export capacity of crude and oil products remains offline, according to Goldman Sachs. The loss of the export capacity in the east has lost the country US$10 billion, according to Mustafa Abu Funas, the economy minister.

Several UAE companies have exploration prospects or operations in Libya, including Abu Dhabi’s Mubadala Petroleum, Dubai’s Al Ghurair Energy and the part Abu Dhabi-owned OMV of Austria. Almansoori, an Abu Dhabi oil services provider, and Al Maskari Holding, which had plans for a massive solar array, were also exploring prospects for new business.

Copyright © 2014 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced,

redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained

in this publication. However, no warranty is given to the accuracy of its content . Page 3

PSVM initiates deepwater development in block 31 offshore Angola http://www.offshore-mag.com/articles/ by :Jessica Tippee

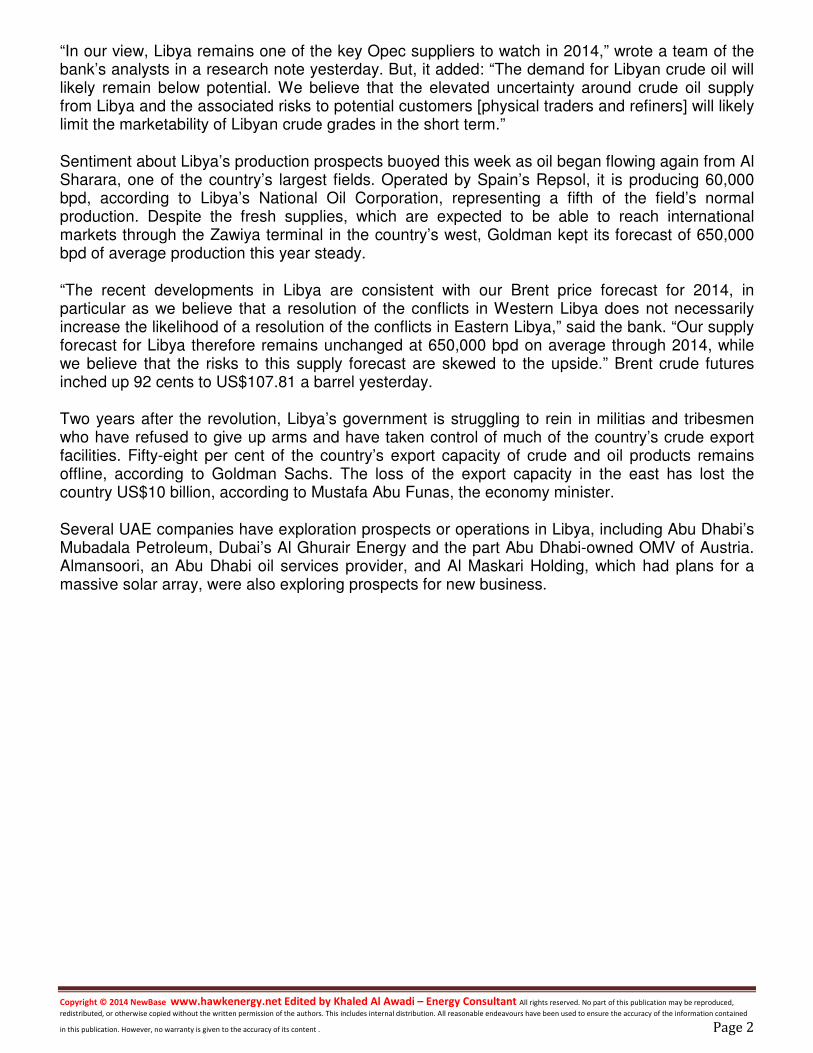

The first deepwater development in block 31 offshore Angola began production on Dec. 6, 2012. The $14-billion PSVM development consists of four oil fields - Plutão, Saturno, Vênus and Marte - in water depths between 1,500 and 2,500 m (4,921 and 8,202 ft).

Operated by BP, PVSM is the largest deepwater project in Africa and one of the biggest offshore oil and gas projects in the world in terms of water depth and subsea extension. Located in the northeast section of block 31 about 180 km (112 mi) offshore, PSVM consists of 48 wells (22 initial producers, 16 water injectors, two gas injectors, and eight later infills) connected to an FPSO through 15 subsea manifolds and associated subsea equipment.

The project's first phase comprises three wells in the Plutão field, where BP expects to ramp up production to 70,000 b/d. Additional wells will boost PSVM's output to 150,000 b/d as wells go onstream in the Saturno and Vênus fields this year and in the Marte field in 2014.

BP Exploration (Angola) Ltd. became operator of block 31 in May 1999. The company holds 26.67% interest along with partners Sonangol E.P. (25%), Sonangol P&P (20%), Statoil Angola A.S. (13.33%), Marathon International Petroleum Angola Block 31 Ltd. (10%), and SSI 31 Ltd. (5%). Sonangol E.P. is the concessionaire.

The Plutão, Saturno, Vênus, and Marte fields were discovered between 2002 and 2004. In July 2008, BP and its co-venturers received approval from Sociedade Nacional de Combustiveis de Angola (Sonangol E.P.) to proceed with the first deepwater project in block 31.

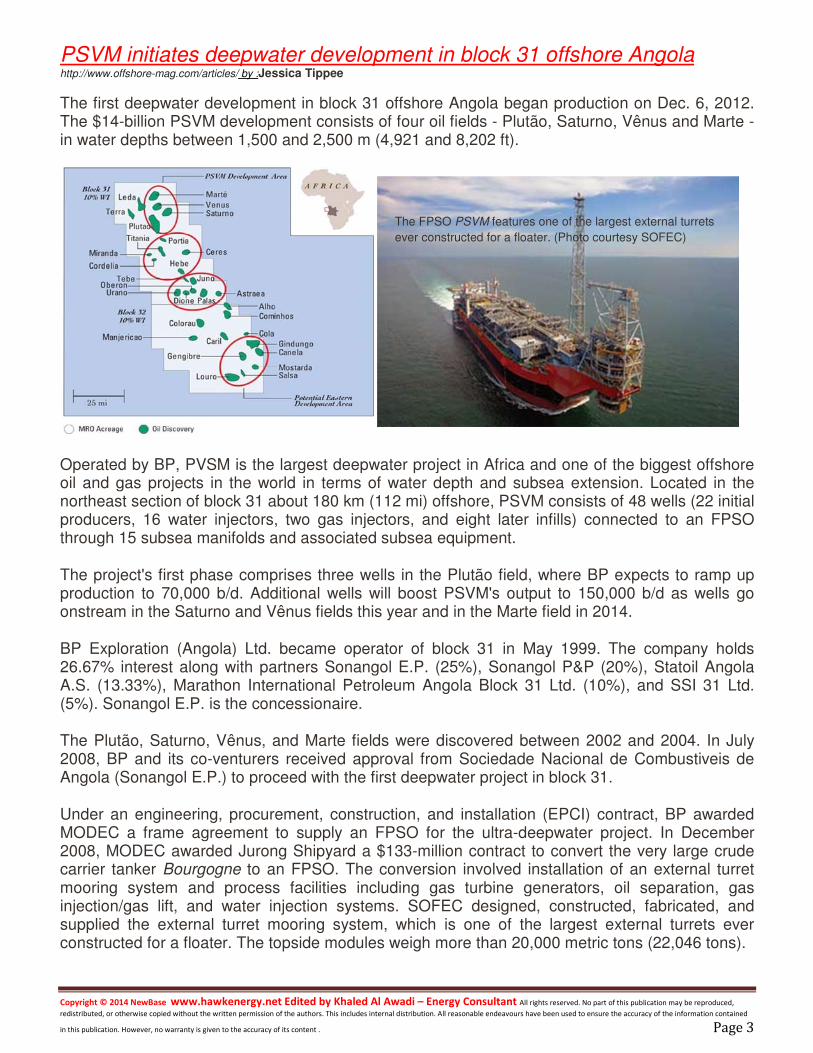

Under an engineering, procurement, construction, and installation (EPCI) contract, BP awarded MODEC a frame agreement to supply an FPSO for the ultra-deepwater project. In December 2008, MODEC awarded Jurong Shipyard a $133-million contract to convert the very large crude carrier tanker Bourgogne to an FPSO. The conversion involved installation of an external turret mooring system and process facilities including gas turbine generators, oil separation, gas injection/gas lift, and water injection systems. SOFEC designed, constructed, fabricated, and supplied the external turret mooring system, which is one of the largest external turrets ever constructed for a floater. The topside modules weigh more than 20,000 metric tons (22,046 tons).

The FPSO PSVM features one of the largest external turrets

ever constructed for a floater. (Photo courtesy SOFEC)

Copyright © 2014 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced,

redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained

in this publication. However, no warranty is given to the accuracy of its content . Page 4

FPSO PSVM, moored in 2,000 m (6,561 ft) of water, is the first FPSO in Angola ultra-deepwater. Designed to operate for 20 years without dry docking, the vessel has a production capacity of 157,000 b/d of oil and 245 MMcf/d (7 MMcm/d) of gas, with oil storage capacity of 1.8 MMbbl. The FPSO is 318 m (1,043 ft) long and 57 m (187 ft) wide.

First Subsea supplied 12 Ballgrab ball and taper connectors for the external turret's 12 mooring lines. Ballgrab connectors link the suction piles and ground chain segments, interfacing directly with the mooring lines' mooring shackles. MODEC Offshore Production Systems contracted VWS Westgarth to supply a water treatment package comprised of pre-treatment and seawater sulfate removal systems with a capacity of 31,800 cu m/d (200,000 b/d) of water. The company also supplied an integrated seawater reverse osmosis system for process wash water sized at 20,000 b/d of water.

The subsea infrastructure features nine wet insulated hybrid risers, 50 km (31 mi) of pipe-in-pipe production flowlines, 56 km (35 mi) of plastic lined water injection lines, plus seven two-slot and six four-slot manifolds. BP awarded Heerema Marine Contractors a $1-billion EPCI and testing contract for pipe-in-pipe production flowlines, service flowlines, and vertical riser systems. The offshore installation work was performed by the deepwater construction vessel Balder. The welding technology was supported by Pipeline Technique in Scotland.

Aker Subsea AS won a $69.8-million frame contract to manufacture and deliver 48 km (30 mi) of steel tube umbilicals. The dynamic section of the umbilicals features Aker's patented carbon fiber rod technology, which was developed for deepwater and ultra-deepwater conditions. This is the first time carbon fiber rod technology has been used in African waters.

Technip received a $112-million call-off contract for the engineering, procurement, and manufacture of 40 flexible jumpers. Project management and engineering was carried out by the company's operating center in Paris. The flexible jumpers were manufactured at the company's flexible pipe plant in Le Trait, France.

The company also was awarded a $404-million contract for the engineering, procurement, and manufacture of more than 64 km (40 mi) of rigid flowlines. Project management and engineering was carried out at the operating centers in Paris and Luanda, Angola. The flowlines were assembled at the Angoflex Ltda. spoolbase in Dande, Angola, and the offshore works were conducted using Technip's deepwater pipelay vessel Deep Blue.

Angoflex Ltda. and DUCO (Technip's wholly owned subsidiary) won a $112-million call-off contract for the engineering, procurement, and manufacture of 34 umbilicals with a total length of 43 km (27 mi). Project management and engineering was carried out by DUCO in Newcastle, UK. The umbilicals were manufactured at the Angoflex plant in Lobito, Angola. Subsea 7 installed more than 12,000 tons of subsea infrastructure using the multi-purpose support vessel Seven Seas.

The PSVM project was developed with more than 20% local content in the manufacture and assembly of key components in Soyo, Dande, Luanda, Porto Amboim, and Lobito construction yards. PSVM is the first of multiple developments expected in the 5,349-sq km (2,065-sq mi) block 31.

Copyright © 2014 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced,

redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained

in this publication. However, no warranty is given to the accuracy of its content . Page 5

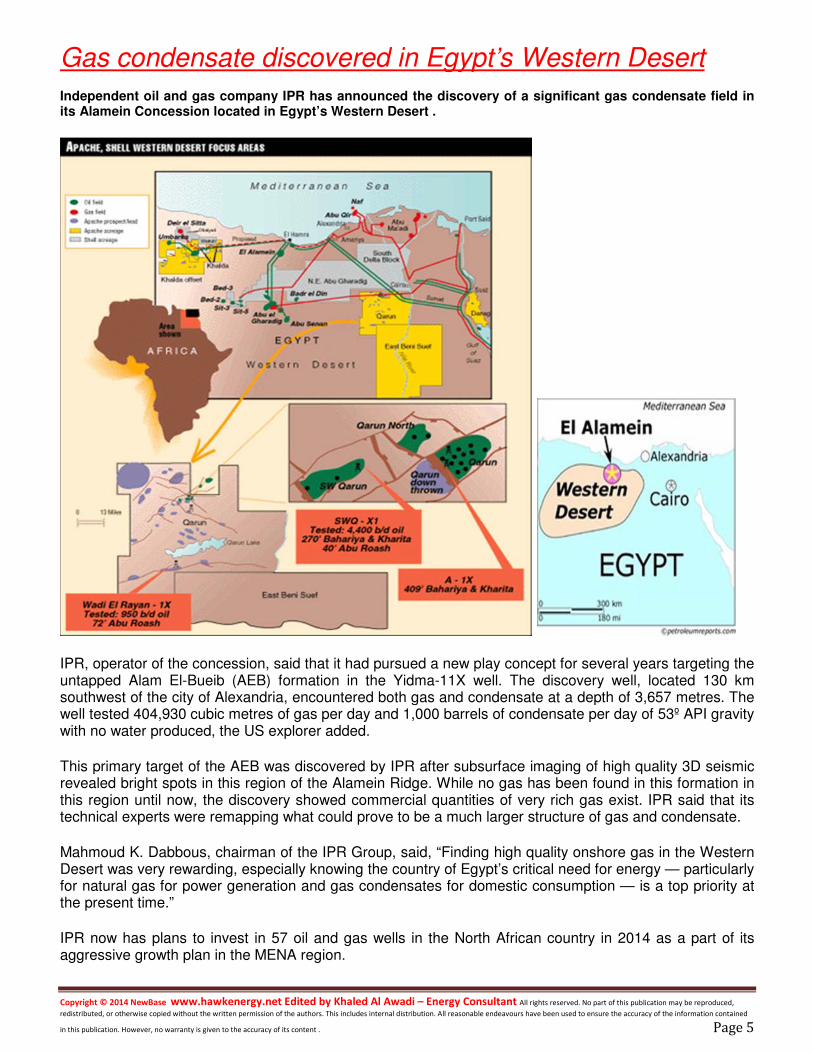

Gas condensate discovered in Egypt’s Western Desert

Independent oil and gas company IPR has announced the discovery of a significant gas condensate field in its Alamein Concession located in Egypt’s Western Desert .

IPR, operator of the concession, said that it had pursued a new play concept for several years targeting the untapped Alam El-Bueib (AEB) formation in the Yidma-11X well. The discovery well, located 130 km southwest of the city of Alexandria, encountered both gas and condensate at a depth of 3,657 metres. The well tested 404,930 cubic metres of gas per day and 1,000 barrels of condensate per day of 53º API gravity with no water produced, the US explorer added.

This primary target of the AEB was discovered by IPR after subsurface imaging of high quality 3D seismic revealed bright spots in this region of the Alamein Ridge. While no gas has been found in this formation in this region until now, the discovery showed commercial quantities of very rich gas exist. IPR said that its technical experts were remapping what could prove to be a much larger structure of gas and condensate.

Mahmoud K. Dabbous, chairman of the IPR Group, said, “Finding high quality onshore gas in the Western Desert was very rewarding, especially knowing the country of Egypt’s critical need for energy — particularly for natural gas for power generation and gas condensates for domestic consumption — is a top priority at the present time.”

IPR now has plans to invest in 57 oil and gas wells in the North African country in 2014 as a part of its aggressive growth plan in the MENA region.

Copyright © 2014 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced,

redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained

in this publication. However, no warranty is given to the accuracy of its content . Page 6

MENAP growth likely to pick up in 2014 as global issues improve

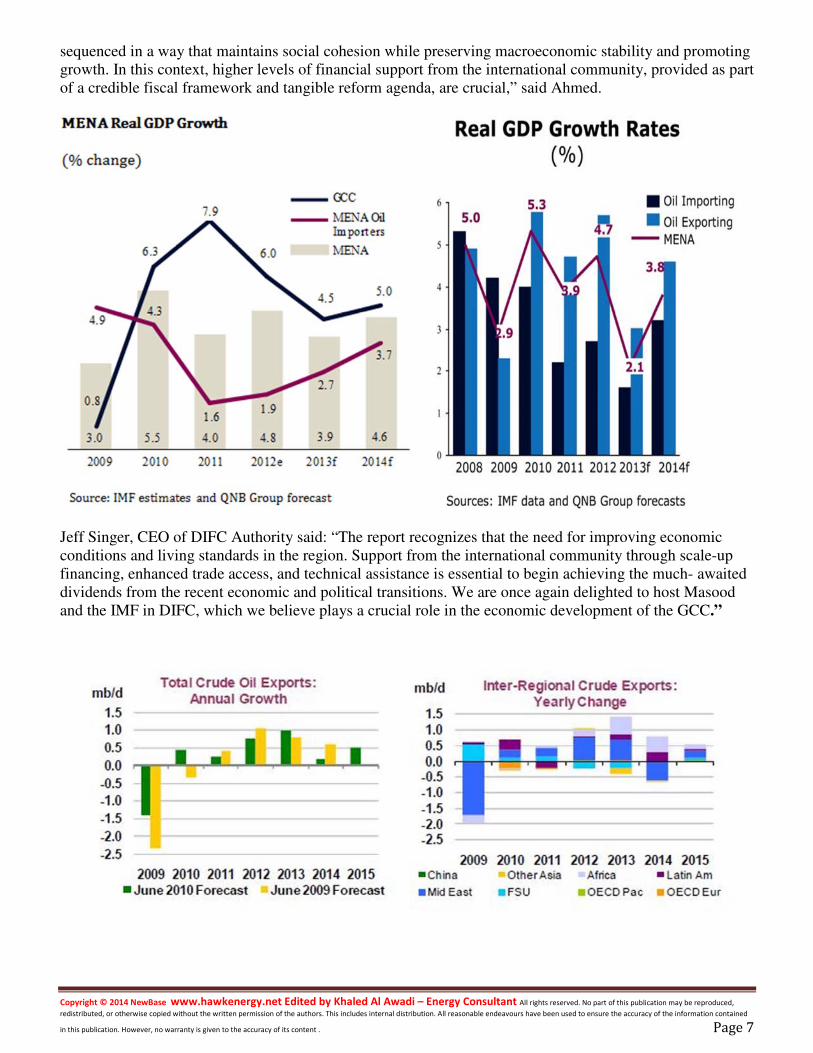

Growth in the Middle East North Africa, Afghanistan, and Pakistan region (MENAP) region is expected to decline to 2.25 percent by the end of the year, a 0.75 percentage point below its May 2013 projections. However, growth is likely to pick up in 2014 as global conditions improve and oil production recovers, the International Monetary Fund (IMF) said Tuesday at a press conference in Dubai to launch its Regional Economic Outlook Update MENAP.

The Report was introduced at an event hosted by Dubai International Financial Centre (DIFC), the financial and business hub connecting the region’s emerging markets with the markets of Europe, Asia and the Americas. IMF said the report has been released at a time when difficult political transitions and increased regional uncertainties arising from the complex civil war in Syria and the ongoing developments in Egypt weigh on confidence in the oil-importing countries. In this setting, the region risks being trapped in a vicious cycle of economic stagnation and persistent sociopolitical strife, underlining the urgent need for policy action that will enhance confidence, growth, and jobs. The Report cites that most oil-exporting countries in the region continue to enjoy steady growth in the non-oil sector, supported in part by high levels of public spending. Although headline growth has declined because of domestic oil supply disruptions and lower global demand, a recovery in oil production and a further strengthening of the non-oil economy will likely lift economic growth in 2014. “However, there are challenges on the horizon. While these countries are running an aggregate fiscal surplus, already half of them, mostly outside of the GCC, cannot balance their budgets and have limited buffers against shocks. Policies should therefore focus on strengthening budgets while minimizing the impact on growth and enhancing equity. High on the agenda is also to continue to pursue structural reforms to bolster private-sector growth, economic diversification, and job creation for nationals,” said Masood Ahmed, Director of the IMF’s Middle East and Central Asia Department, said at the launch conference of the report in Dubai. In the oil-importing countries, domestic and regional factors are the main sources of downside risks as many of them are Arab countries in transition, regional conflict, heightened political tensions, with delays in reforms continuing to weigh on growth. The immediate policy priority is to restore confidence and create jobs to help sustain the socio-political transitions. “Most countries also need to start putting their fiscal house in order and embark, without delay, on a bold reform agenda that will improve the business climate and enhance equity, to create higher levels of sustainable growth and job creation over the medium term. It is important that reform be paced and

Masood Ahmed, Director of the IMF’s

Middle East and Central Asia Department

Copyright © 2014 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced,

redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained

in this publication. However, no warranty is given to the accuracy of its content . Page 7

sequenced in a way that maintains social cohesion while preserving macroeconomic stability and promoting growth. In this context, higher levels of financial support from the international community, provided as part of a credible fiscal framework and tangible reform agenda, are crucial,” said Ahmed.

Jeff Singer, CEO of DIFC Authority said: “The report recognizes that the need for improving economic conditions and living standards in the region. Support from the international community through scale-up financing, enhanced trade access, and technical assistance is essential to begin achieving the much- awaited dividends from the recent economic and political transitions. We are once again delighted to host Masood and the IMF in DIFC, which we believe plays a crucial role in the economic development of the GCC.”

Copyright © 2014 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced,

redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained

in this publication. However, no warranty is given to the accuracy of its content . Page 8

Oil, gas and petrochemicals top industry in the UAE

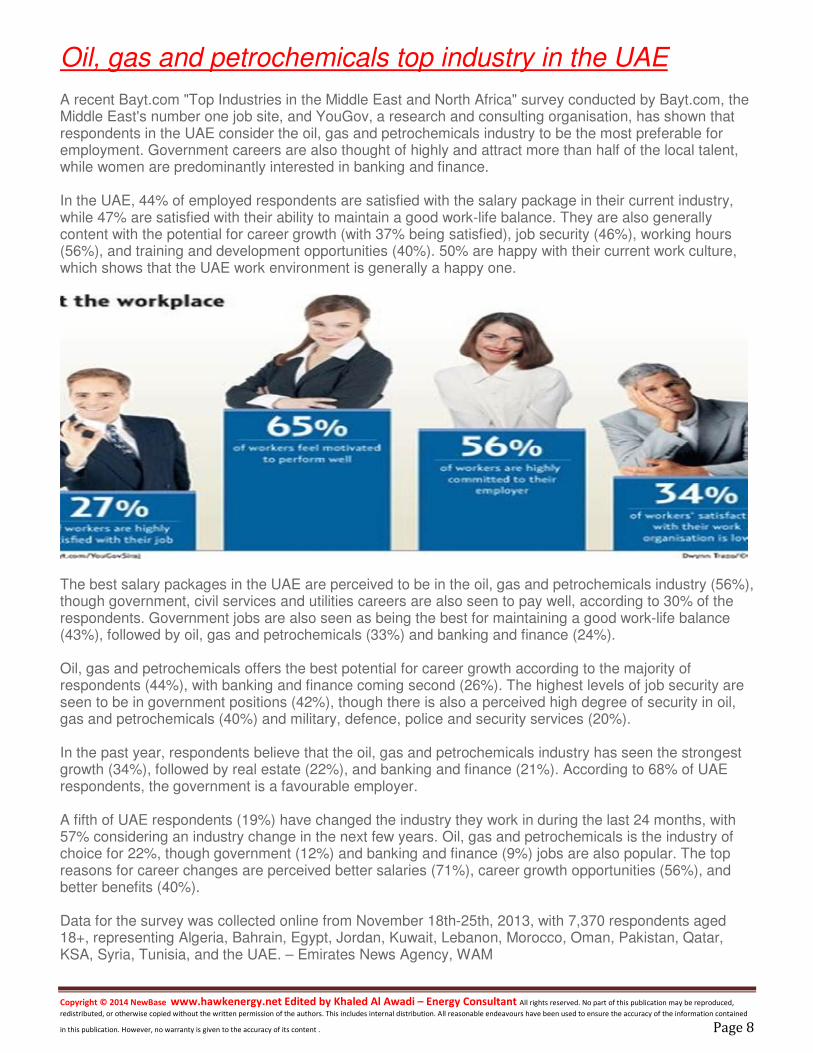

A recent Bayt.com "Top Industries in the Middle East and North Africa" survey conducted by Bayt.com, the Middle East's number one job site, and YouGov, a research and consulting organisation, has shown that respondents in the UAE consider the oil, gas and petrochemicals industry to be the most preferable for employment. Government careers are also thought of highly and attract more than half of the local talent, while women are predominantly interested in banking and finance. In the UAE, 44% of employed respondents are satisfied with the salary package in their current industry, while 47% are satisfied with their ability to maintain a good work-life balance. They are also generally content with the potential for career growth (with 37% being satisfied), job security (46%), working hours (56%), and training and development opportunities (40%). 50% are happy with their current work culture, which shows that the UAE work environment is generally a happy one.

The best salary packages in the UAE are perceived to be in the oil, gas and petrochemicals industry (56%), though government, civil services and utilities careers are also seen to pay well, according to 30% of the respondents. Government jobs are also seen as being the best for maintaining a good work-life balance (43%), followed by oil, gas and petrochemicals (33%) and banking and finance (24%). Oil, gas and petrochemicals offers the best potential for career growth according to the majority of respondents (44%), with banking and finance coming second (26%). The highest levels of job security are seen to be in government positions (42%), though there is also a perceived high degree of security in oil, gas and petrochemicals (40%) and military, defence, police and security services (20%). In the past year, respondents believe that the oil, gas and petrochemicals industry has seen the strongest growth (34%), followed by real estate (22%), and banking and finance (21%). According to 68% of UAE respondents, the government is a favourable employer. A fifth of UAE respondents (19%) have changed the industry they work in during the last 24 months, with 57% considering an industry change in the next few years. Oil, gas and petrochemicals is the industry of choice for 22%, though government (12%) and banking and finance (9%) jobs are also popular. The top reasons for career changes are perceived better salaries (71%), career growth opportunities (56%), and better benefits (40%). Data for the survey was collected online from November 18th-25th, 2013, with 7,370 respondents aged 18+, representing Algeria, Bahrain, Egypt, Jordan, Kuwait, Lebanon, Morocco, Oman, Pakistan, Qatar, KSA, Syria, Tunisia, and the UAE. – Emirates News Agency, WAM

Copyright © 2014 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced,

redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained

in this publication. However, no warranty is given to the accuracy of its content . Page 9

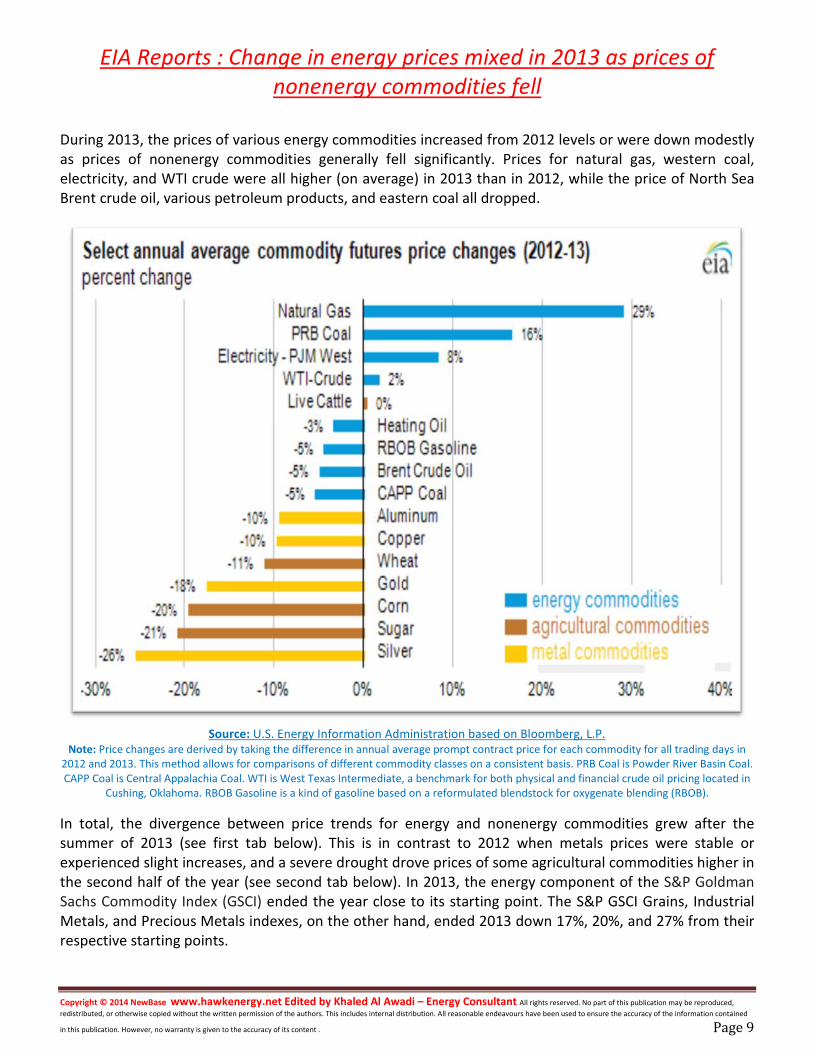

EIA Reports : Change in energy prices mixed in 2013 as prices of

nonenergy commodities fell

During 2013, the prices of various energy commodities increased from 2012 levels or were down modestly

as prices of nonenergy commodities generally fell significantly. Prices for natural gas, western coal,

electricity, and WTI crude were all higher (on average) in 2013 than in 2012, while the price of North Sea

Brent crude oil, various petroleum products, and eastern coal all dropped.

Source: U.S. Energy Information Administration based on Bloomberg, L.P.

Note: Price changes are derived by taking the difference in annual average prompt contract price for each commodity for all trading days in

2012 and 2013. This method allows for comparisons of different commodity classes on a consistent basis. PRB Coal is Powder River Basin Coal.

CAPP Coal is Central Appalachia Coal. WTI is West Texas Intermediate, a benchmark for both physical and financial crude oil pricing located in

Cushing, Oklahoma. RBOB Gasoline is a kind of gasoline based on a reformulated blendstock for oxygenate blending (RBOB).

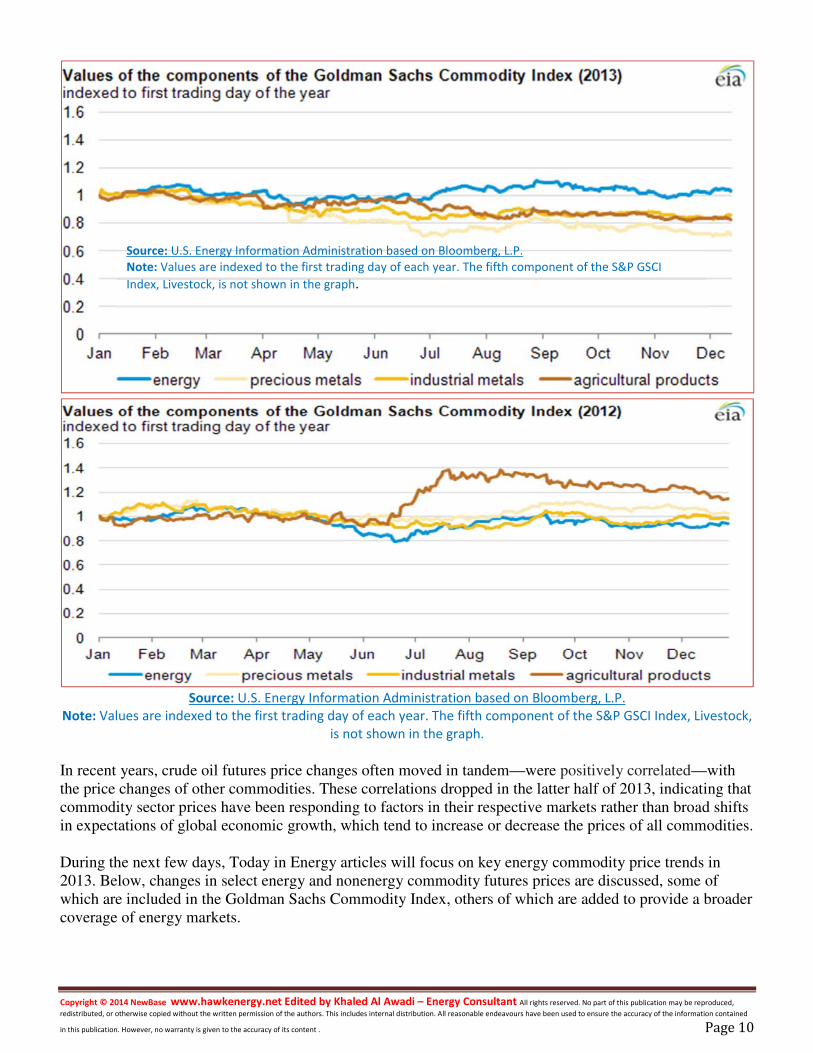

In total, the divergence between price trends for energy and nonenergy commodities grew after the

summer of 2013 (see first tab below). This is in contrast to 2012 when metals prices were stable or

experienced slight increases, and a severe drought drove prices of some agricultural commodities higher in

the second half of the year (see second tab below). In 2013, the energy component of the S&P Goldman

Sachs Commodity Index (GSCI) ended the year close to its starting point. The S&P GSCI Grains, Industrial

Metals, and Precious Metals indexes, on the other hand, ended 2013 down 17%, 20%, and 27% from their

respective starting points.

Copyright © 2014 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced,

redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained

in this publication. However, no warranty is given to the accuracy of its content . Page 10

Source: U.S. Energy Information Administration based on Bloomberg, L.P.

Note: Values are indexed to the first trading day of each year. The fifth component of the S&P GSCI Index, Livestock,

is not shown in the graph.

In recent years, crude oil futures price changes often moved in tandem—were positively correlated—with the price changes of other commodities. These correlations dropped in the latter half of 2013, indicating that commodity sector prices have been responding to factors in their respective markets rather than broad shifts in expectations of global economic growth, which tend to increase or decrease the prices of all commodities.

During the next few days, Today in Energy articles will focus on key energy commodity price trends in 2013. Below, changes in select energy and nonenergy commodity futures prices are discussed, some of which are included in the Goldman Sachs Commodity Index, others of which are added to provide a broader coverage of energy markets.

Source: U.S. Energy Information Administration based on Bloomberg, L.P.

Note: Values are indexed to the first trading day of each year. The fifth component of the S&P GSCI

Index, Livestock, is not shown in the graph.

Copyright © 2014 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced,

redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained

in this publication. However, no warranty is given to the accuracy of its content . Page 11

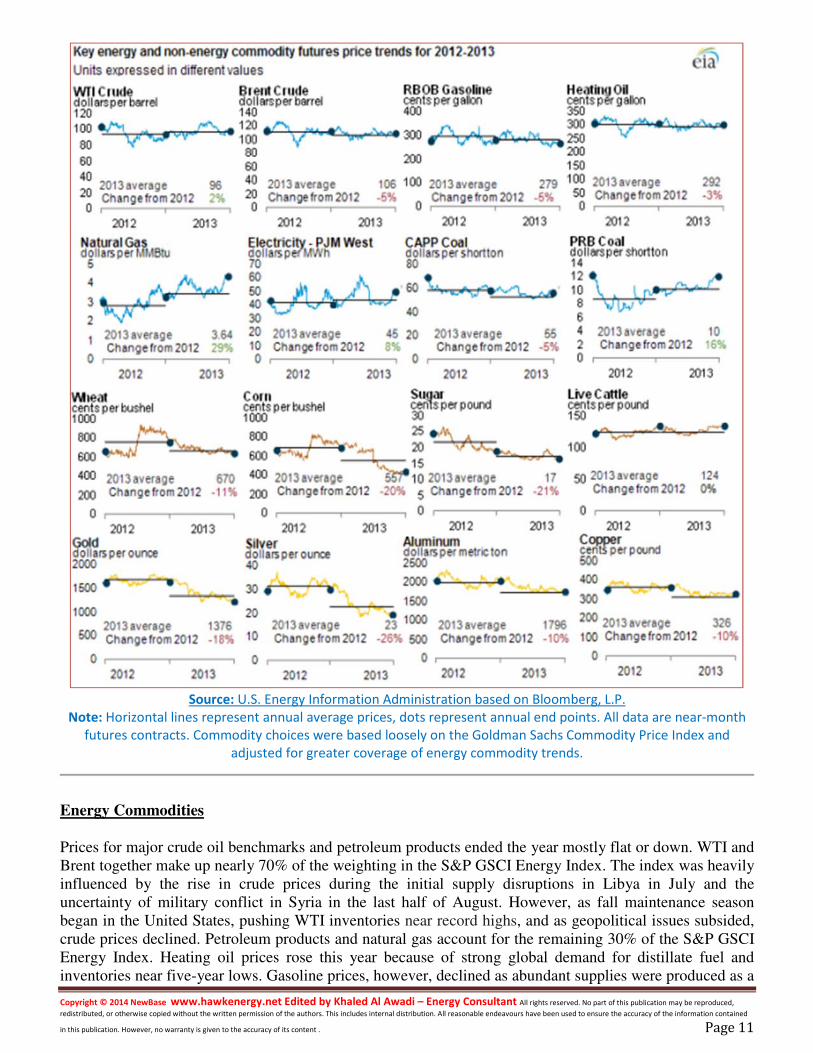

Source: U.S. Energy Information Administration based on Bloomberg, L.P.

Note: Horizontal lines represent annual average prices, dots represent annual end points. All data are near-month

futures contracts. Commodity choices were based loosely on the Goldman Sachs Commodity Price Index and

adjusted for greater coverage of energy commodity trends.

Energy Commodities

Prices for major crude oil benchmarks and petroleum products ended the year mostly flat or down. WTI and Brent together make up nearly 70% of the weighting in the S&P GSCI Energy Index. The index was heavily influenced by the rise in crude prices during the initial supply disruptions in Libya in July and the uncertainty of military conflict in Syria in the last half of August. However, as fall maintenance season began in the United States, pushing WTI inventories near record highs, and as geopolitical issues subsided, crude prices declined. Petroleum products and natural gas account for the remaining 30% of the S&P GSCI Energy Index. Heating oil prices rose this year because of strong global demand for distillate fuel and inventories near five-year lows. Gasoline prices, however, declined as abundant supplies were produced as a

Copyright © 2014 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced,

redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained

in this publication. However, no warranty is given to the accuracy of its content . Page 12

result of the high refinery runs needed to satisfy demand for heating oil and diesel fuel. U.S. natural gas prices ended higher in 2013 as cold weather across much of the country drove prices well above $4 per million British thermal units ($/MMBtu) in both the physical and financial markets. As a result, natural gas prices were 50 cents to $1/MMBtu above their level at the start of the year.

Throughout the week, several regional price patterns in both natural gas and electricity markets will be discussed in articles on each energy sector. Eastern coal from the Central Appalachian Basin, not a component of the S&P GSCI Energy Index, ended the year basically flat, which stands in contrast to the increase seen in the price of coal from Powder River Basin, mined in the western United States.

Grains Commodities

The S&P GSCI Grains index, a subindex of the larger Agriculture Index, includes corn, wheat, and soybeans, with corn accounting for just over 40% of the weighting. Corn prices declined sharply this year because of better-than-expected crop yields from favorable weather conditions during harvest season, leading a drop in the grains subindex in the last half of the year. The U.S. Department of Agriculture estimated that the 2013 corn crop production reached almost 14 billion bushels, the highest recorded, with an average corn crop yield of 160.4 bushels per acre, the second-highest yield recorded.

Metal Commodities

The S&P GSCI Industrial Metals Index is composed mostly of copper and aluminum, which make up 80% of the index. Copper prices declined in 2013 because of concerns that economic growth in large commodity-consuming countries, like China, is slowing, resulting in reduced demand. In addition, copper inventories, as tracked by the London Metal Exchange, increased from the beginning of 2013, peaking in the summer months, placing downward pressure on prices. The S&P GSCI Precious Metals Index had the largest decline out of these four indexes because of the decline in the price of gold, which accounts for 85% of the index. Reported by : http://www.eia.gov/todayinenergy/detail.cfm?id=14471

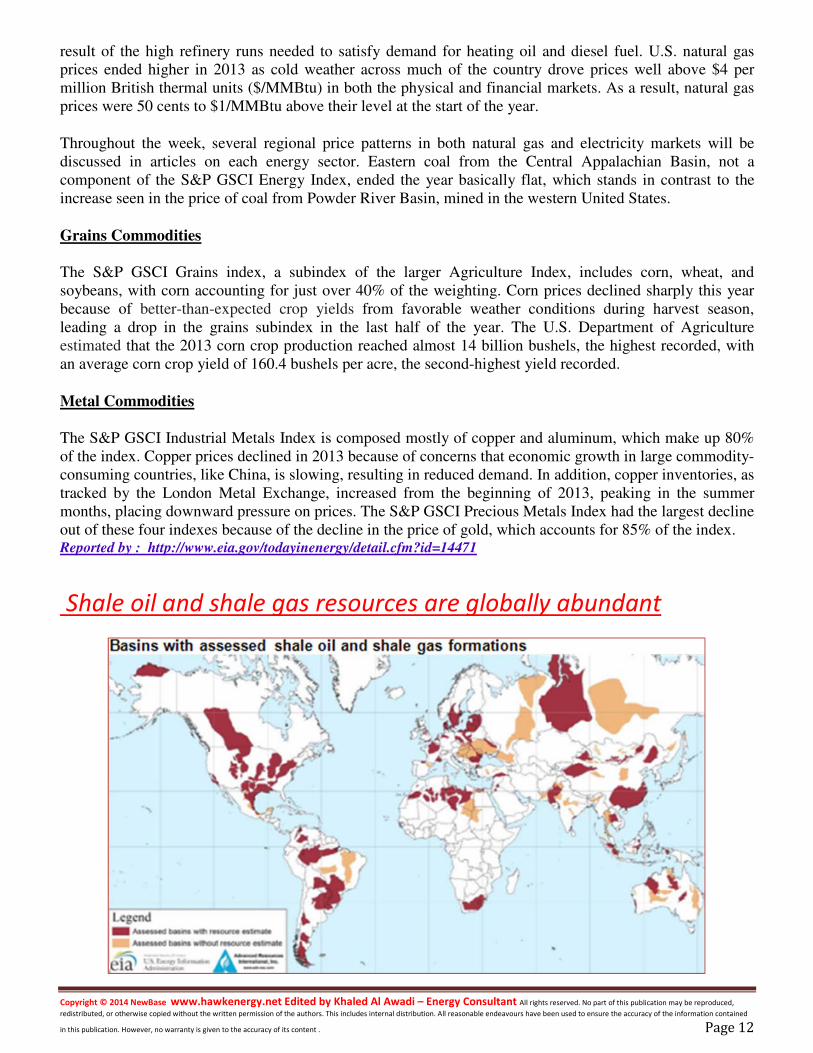

Shale oil and shale gas resources are globally abundant

Copyright © 2014 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced,

redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained

in this publication. However, no warranty is given to the accuracy of its content . Page 13

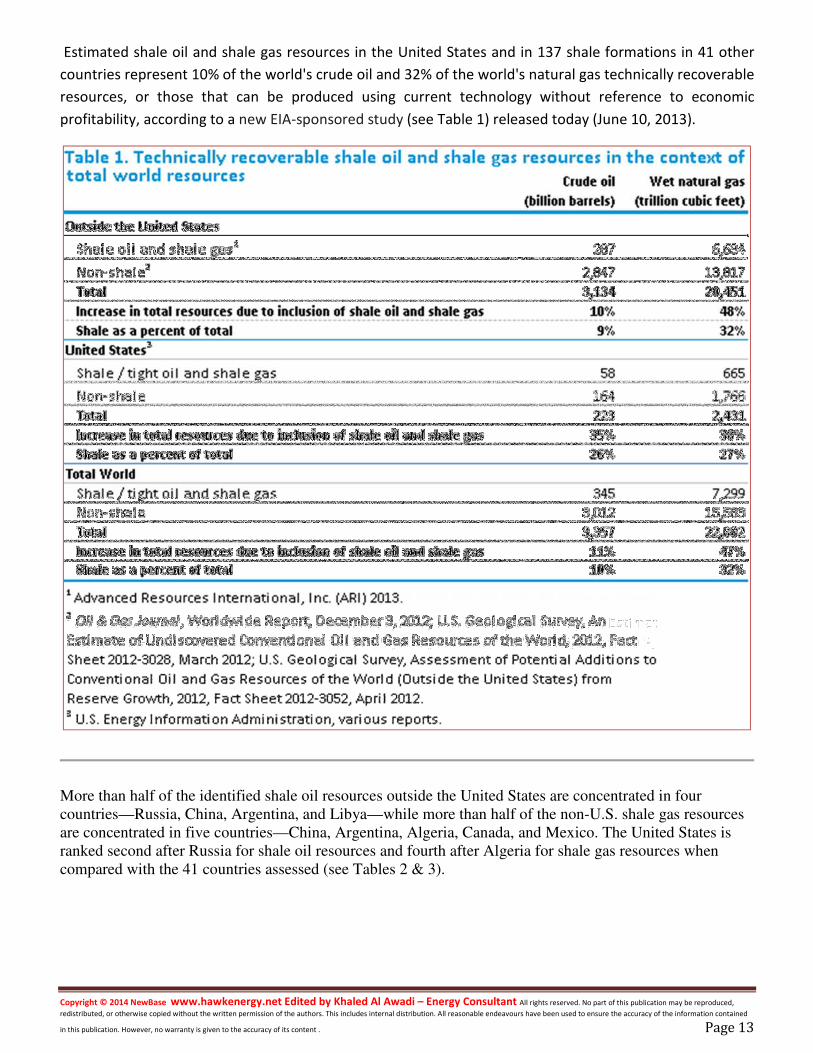

Estimated shale oil and shale gas resources in the United States and in 137 shale formations in 41 other

countries represent 10% of the world's crude oil and 32% of the world's natural gas technically recoverable

resources, or those that can be produced using current technology without reference to economic

profitability, according to a new EIA-sponsored study (see Table 1) released today (June 10, 2013).

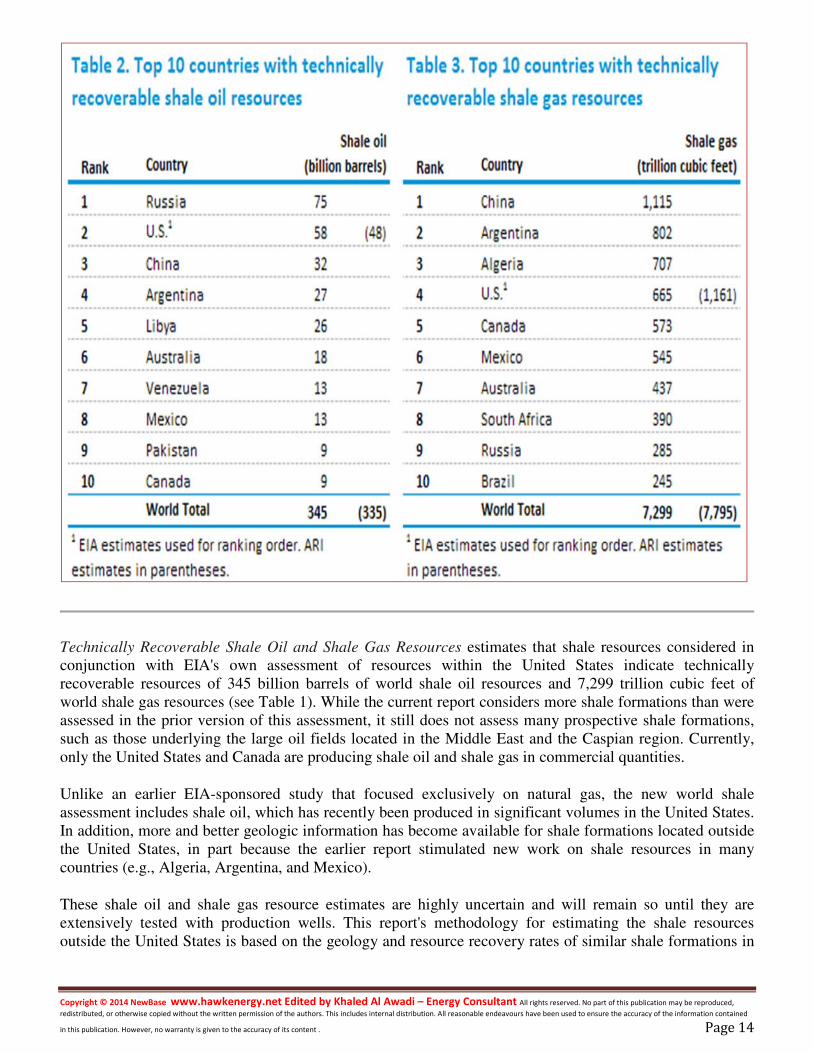

More than half of the identified shale oil resources outside the United States are concentrated in four countries—Russia, China, Argentina, and Libya—while more than half of the non-U.S. shale gas resources are concentrated in five countries—China, Argentina, Algeria, Canada, and Mexico. The United States is ranked second after Russia for shale oil resources and fourth after Algeria for shale gas resources when compared with the 41 countries assessed (see Tables 2 & 3).

Copyright © 2014 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced,

redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained

in this publication. However, no warranty is given to the accuracy of its content . Page 14

Technically Recoverable Shale Oil and Shale Gas Resources estimates that shale resources considered in conjunction with EIA's own assessment of resources within the United States indicate technically recoverable resources of 345 billion barrels of world shale oil resources and 7,299 trillion cubic feet of world shale gas resources (see Table 1). While the current report considers more shale formations than were assessed in the prior version of this assessment, it still does not assess many prospective shale formations, such as those underlying the large oil fields located in the Middle East and the Caspian region. Currently, only the United States and Canada are producing shale oil and shale gas in commercial quantities.

Unlike an earlier EIA-sponsored study that focused exclusively on natural gas, the new world shale assessment includes shale oil, which has recently been produced in significant volumes in the United States. In addition, more and better geologic information has become available for shale formations located outside the United States, in part because the earlier report stimulated new work on shale resources in many countries (e.g., Algeria, Argentina, and Mexico).

These shale oil and shale gas resource estimates are highly uncertain and will remain so until they are extensively tested with production wells. This report's methodology for estimating the shale resources outside the United States is based on the geology and resource recovery rates of similar shale formations in

Copyright © 2014 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced,

redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained

in this publication. However, no warranty is given to the accuracy of its content . Page 15

the United States (referred to as analogs) that have produced shale oil and shale gas from thousands of producing wells.

Because they have proven to be quickly producible in large volumes at a relatively low cost, shale / tight oil and shale gas resources have revolutionized U.S. oil and natural gas production, providing 29 percent of total U.S. crude oil production and 40 percent of total U.S. natural gas production in 2012. However, given the variation across the world's shale formations in both geology and above-the-ground conditions, the extent to which global technically recoverable shale resources will prove to be economically recoverable is not yet clear. The market impact of shale resources outside the United States will depend on their own production costs and volumes. For example, a potential shale well that costs twice as much and produces half the output of a typical U.S. well would be unlikely to back out current supply sources of oil or natural gas. In many cases, even significantly smaller differences in costs, well productivity, or both can make the difference between a resource that is a market game changer and one that is economically irrelevant at current market prices.

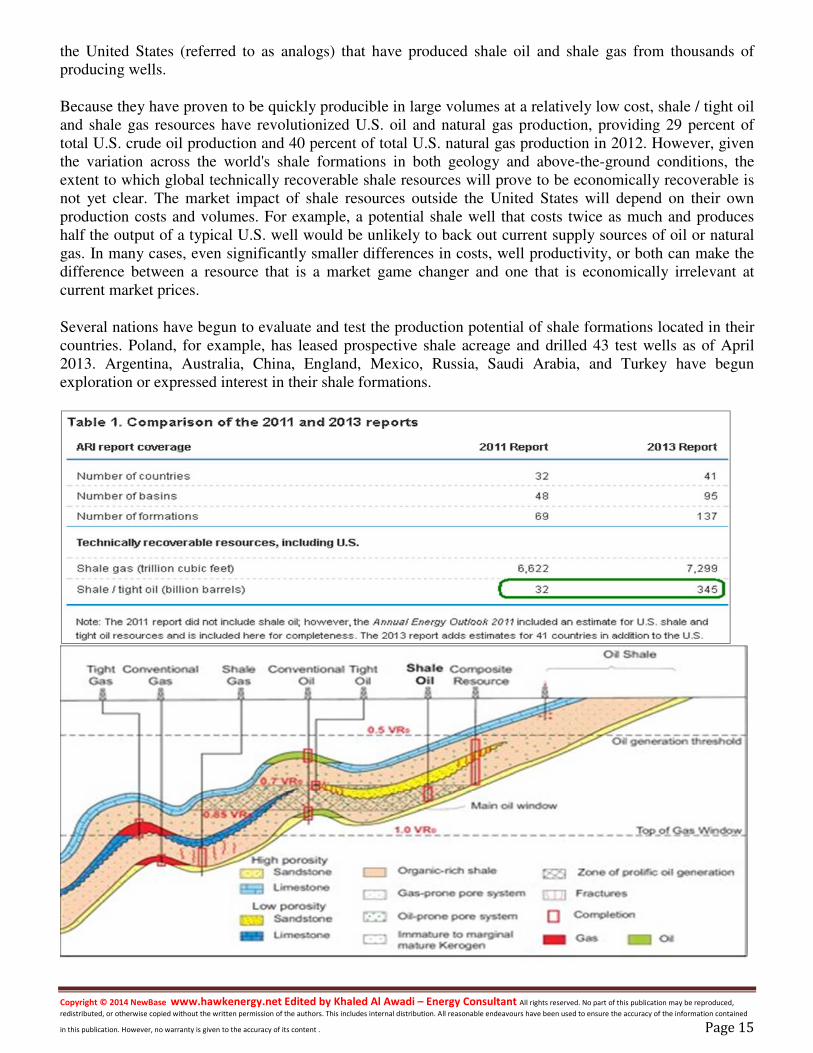

Several nations have begun to evaluate and test the production potential of shale formations located in their countries. Poland, for example, has leased prospective shale acreage and drilled 43 test wells as of April 2013. Argentina, Australia, China, England, Mexico, Russia, Saudi Arabia, and Turkey have begun exploration or expressed interest in their shale formations.

Copyright © 2014 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced,

redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained

in this publication. However, no warranty is given to the accuracy of its content . Page 16

NewBase For discussion or further details on the news below you may contact us on +971504822502 , Dubai , UAE

Your partner in Energy Service

Khaled Malallah Al Awadi, MSc. & BSc. Mechanical Engineering (HON), USA ASME member since 1995 Emarat member since 1990

Energy Services & Consultants Mobile : +97150-4822502

[email protected] [email protected]

Khaled Al Awadi is a UAE National with Khaled Al Awadi is a UAE National with Khaled Al Awadi is a UAE National with Khaled Al Awadi is a UAE National with a total of 24 yearsa total of 24 yearsa total of 24 yearsa total of 24 years of experience in theof experience in theof experience in theof experience in the Oil & Gas sector. Oil & Gas sector. Oil & Gas sector. Oil & Gas sector.

Currently working as Technical Affairs Specialist for Emirates General Petroleum Corp. “Emarat“ with Currently working as Technical Affairs Specialist for Emirates General Petroleum Corp. “Emarat“ with Currently working as Technical Affairs Specialist for Emirates General Petroleum Corp. “Emarat“ with Currently working as Technical Affairs Specialist for Emirates General Petroleum Corp. “Emarat“ with

external voluntary Energy consultation for the GCC area via Hawk Energy Service as a UAE external voluntary Energy consultation for the GCC area via Hawk Energy Service as a UAE external voluntary Energy consultation for the GCC area via Hawk Energy Service as a UAE external voluntary Energy consultation for the GCC area via Hawk Energy Service as a UAE operations base , Most operations base , Most operations base , Most operations base , Most

of the experience were spent as the Gas Operations Manager in Emarat , responsible for Emarat Gas Pipeline of the experience were spent as the Gas Operations Manager in Emarat , responsible for Emarat Gas Pipeline of the experience were spent as the Gas Operations Manager in Emarat , responsible for Emarat Gas Pipeline of the experience were spent as the Gas Operations Manager in Emarat , responsible for Emarat Gas Pipeline

Network Facility & gas compressor stations . Through the years , he has developed great experiences in the Network Facility & gas compressor stations . Through the years , he has developed great experiences in the Network Facility & gas compressor stations . Through the years , he has developed great experiences in the Network Facility & gas compressor stations . Through the years , he has developed great experiences in the

designing & condesigning & condesigning & condesigning & constructingstructingstructingstructing of gas pipelines, gas metering & regulating stations and in the engineering of supply of gas pipelines, gas metering & regulating stations and in the engineering of supply of gas pipelines, gas metering & regulating stations and in the engineering of supply of gas pipelines, gas metering & regulating stations and in the engineering of supply

routes. Many years were spent drafting, & compiling gas transportation , operation & maintenance agreements routes. Many years were spent drafting, & compiling gas transportation , operation & maintenance agreements routes. Many years were spent drafting, & compiling gas transportation , operation & maintenance agreements routes. Many years were spent drafting, & compiling gas transportation , operation & maintenance agreements

along with many MOUs for the local authorities. Healong with many MOUs for the local authorities. Healong with many MOUs for the local authorities. Healong with many MOUs for the local authorities. He has become a reference for many of the Oil & Gas Conferences has become a reference for many of the Oil & Gas Conferences has become a reference for many of the Oil & Gas Conferences has become a reference for many of the Oil & Gas Conferences

held in the UAE andheld in the UAE andheld in the UAE andheld in the UAE and Energy program broadcasted internationally , via GCC leading satelliteEnergy program broadcasted internationally , via GCC leading satelliteEnergy program broadcasted internationally , via GCC leading satelliteEnergy program broadcasted internationally , via GCC leading satellite ChannelsChannelsChannelsChannels . . . .

NewBase : For discussion or further details on the news above you may contact us on +971504822502 , Dubai , UAE

NewBase 07 January 2014 K. Al Awadi