Embed Size (px)

Citation preview

Copyright © 2014 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced,

redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained

in this publication. However, no warranty is given to the accuracy of its content . Page 1

NewBase 14 September 2014 Khaled Al Awadi

NewBase For discussion or further details on the news below you may contact us on +971504822502 , Dubai , UAE

Dark clouds in the offing for oil Saudi Gazette (SYED RASHID HUSAIN) + NewBase

Oil futures were registered at an eight-month low this week. On the New York Mercantile Exchange, it was registered hovering around $91a barrel - the lowest since January 9. Brent was also below $100 - floating around the $98 mark - the lowest seen since April 2013.

Demand growth is slowing. Demand for OPEC oil will be lower this year as well as next year, the OPEC monthly oil report said. Global demand is to grow by 1.05 million bpd in 2014 to 91.2 million barrels, 50,000bbls lower from earlier projections and the demand next year is expected to grow 1.19 million barrels per day only - representing a marginal downward adjustment. Balance of supply and demand for OPEC crude in 2014 was revised down by 0.2

million bpd from the previous month to stand at 29.5 million bpd In 2015. And the Paris-based IEA was also not far behind - trimming its forecast for the rise in global oil demand this year for the third month in a row, terming the recent slowdown in demand "nothing short of remarkable." In its Monthly Oil Report, the IEA said it expected global oil demand to grow by 0.9 million bpd in 2014, a decrease of 65,000 bpd compared to last month's forecast and down by 300,000 bpd since July. According to the IEA, oil demand growth in the second quarter was at its lowest in 2½ years. Markets are reacting. Analysts are concerned. Brent futures are unlikely to repeat their performance in the past two years, when dips below $100 a barrel were met by swift rebounds, analysts at JBC Energy Market were reported as saying. Forecasts for economic growth are being lowered, and worries about a potential recession are resurfacing in some parts of the world, they added. With demand growth slowing down, output is on radar. Saudi Arabia trimmed 400,000 bpd in output last month, OPEC monthly market report said. As per the IEA, Saudi Arabia cut its output by 330,000 barrels a day last month.

Copyright © 2014 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced,

redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained

in this publication. However, no warranty is given to the accuracy of its content . Page 2

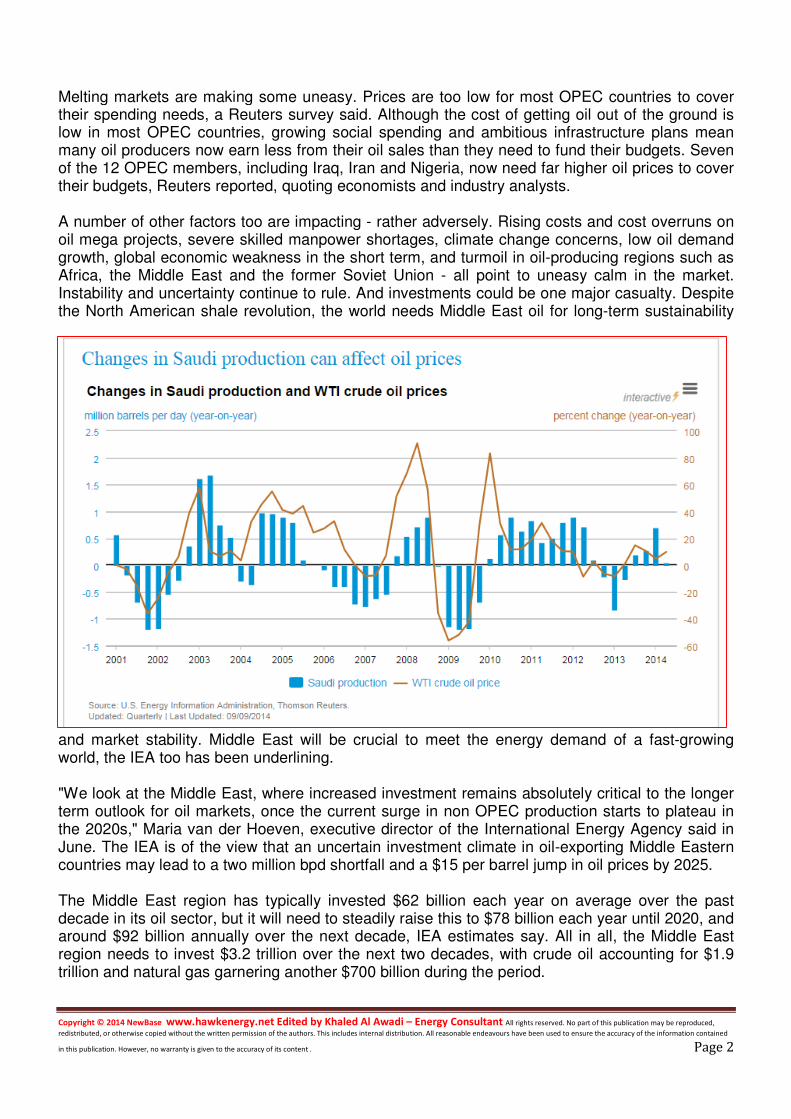

Melting markets are making some uneasy. Prices are too low for most OPEC countries to cover their spending needs, a Reuters survey said. Although the cost of getting oil out of the ground is low in most OPEC countries, growing social spending and ambitious infrastructure plans mean many oil producers now earn less from their oil sales than they need to fund their budgets. Seven of the 12 OPEC members, including Iraq, Iran and Nigeria, now need far higher oil prices to cover their budgets, Reuters reported, quoting economists and industry analysts. A number of other factors too are impacting - rather adversely. Rising costs and cost overruns on oil mega projects, severe skilled manpower shortages, climate change concerns, low oil demand growth, global economic weakness in the short term, and turmoil in oil-producing regions such as Africa, the Middle East and the former Soviet Union - all point to uneasy calm in the market. Instability and uncertainty continue to rule. And investments could be one major casualty. Despite the North American shale revolution, the world needs Middle East oil for long-term sustainability

and market stability. Middle East will be crucial to meet the energy demand of a fast-growing world, the IEA too has been underlining. "We look at the Middle East, where increased investment remains absolutely critical to the longer term outlook for oil markets, once the current surge in non OPEC production starts to plateau in the 2020s," Maria van der Hoeven, executive director of the International Energy Agency said in June. The IEA is of the view that an uncertain investment climate in oil-exporting Middle Eastern countries may lead to a two million bpd shortfall and a $15 per barrel jump in oil prices by 2025. The Middle East region has typically invested $62 billion each year on average over the past decade in its oil sector, but it will need to steadily raise this to $78 billion each year until 2020, and around $92 billion annually over the next decade, IEA estimates say. All in all, the Middle East region needs to invest $3.2 trillion over the next two decades, with crude oil accounting for $1.9 trillion and natural gas garnering another $700 billion during the period.

Copyright © 2014 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced,

redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained

in this publication. However, no warranty is given to the accuracy of its content . Page 3

"Yet the required upturn in investment is by no means guaranteed, even though the oil resources of the Middle East remain ample and are among the cheapest in the world to develop," the IEA insisted. There is also a creeping danger that OPEC revenues from oil exports will level off, especially if non-OPEC supplies continue to rein in oil prices. Lower or flat prices could deter Middle Eastern countries further from investing heavily in the energy sector, as required.

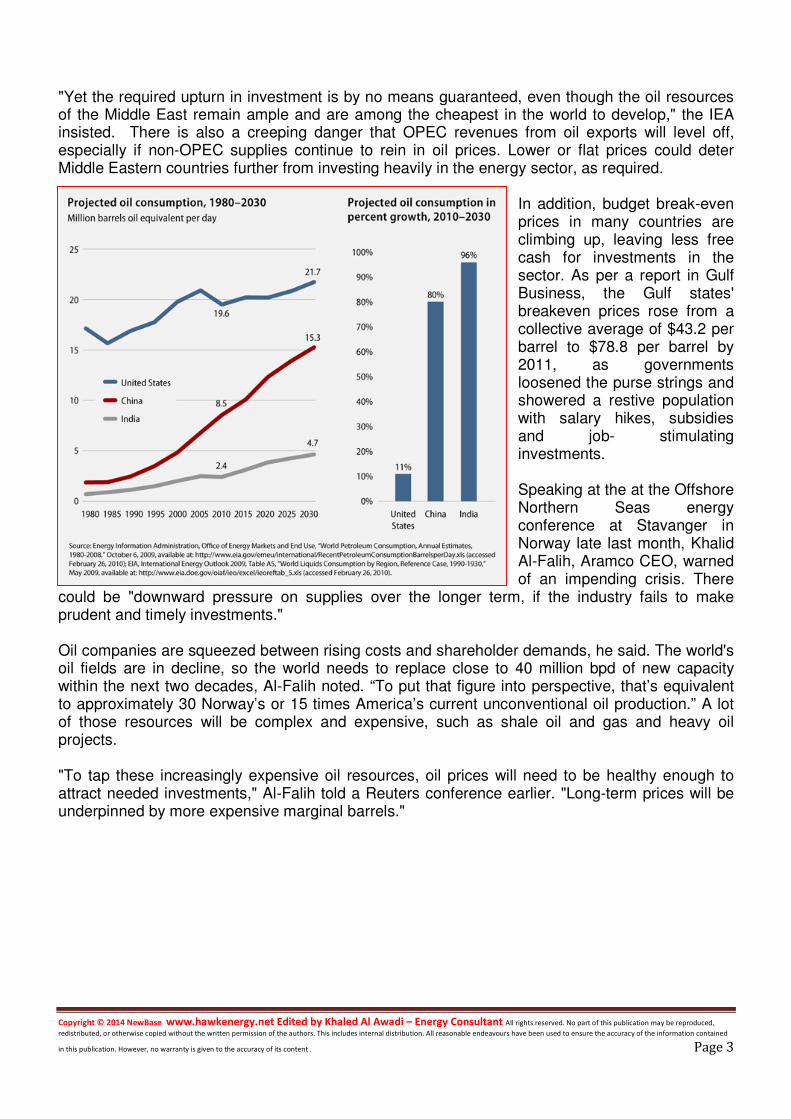

In addition, budget break-even prices in many countries are climbing up, leaving less free cash for investments in the sector. As per a report in Gulf Business, the Gulf states' breakeven prices rose from a collective average of $43.2 per barrel to $78.8 per barrel by 2011, as governments loosened the purse strings and showered a restive population with salary hikes, subsidies and job- stimulating investments. Speaking at the at the Offshore Northern Seas energy conference at Stavanger in Norway late last month, Khalid Al-Falih, Aramco CEO, warned of an impending crisis. There

could be "downward pressure on supplies over the longer term, if the industry fails to make prudent and timely investments." Oil companies are squeezed between rising costs and shareholder demands, he said. The world's oil fields are in decline, so the world needs to replace close to 40 million bpd of new capacity within the next two decades, Al-Falih noted. “To put that figure into perspective, that’s equivalent to approximately 30 Norway’s or 15 times America’s current unconventional oil production.” A lot of those resources will be complex and expensive, such as shale oil and gas and heavy oil projects. "To tap these increasingly expensive oil resources, oil prices will need to be healthy enough to attract needed investments," Al-Falih told a Reuters conference earlier. "Long-term prices will be underpinned by more expensive marginal barrels."

Copyright © 2014 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced,

redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained

in this publication. However, no warranty is given to the accuracy of its content . Page 4

Despite decline in some regions, world oil consumption still seen rising

Source: U.S. Energy Information Administration, International Energy Outlook 2014

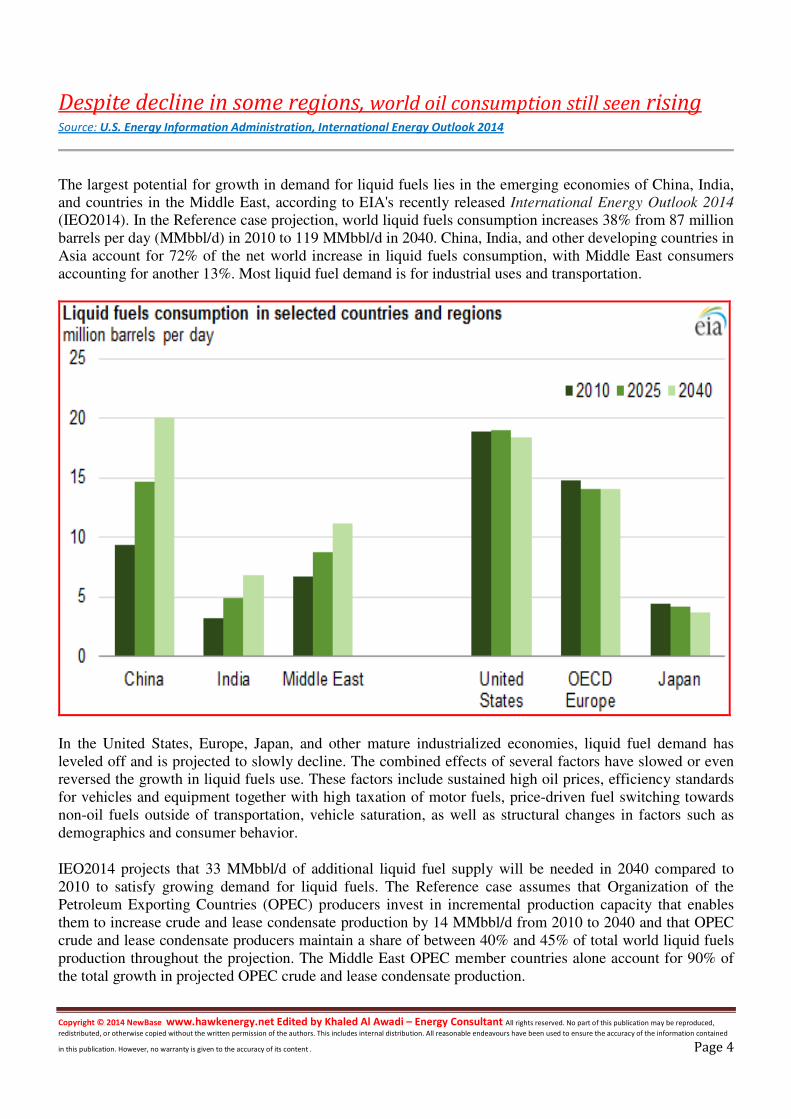

The largest potential for growth in demand for liquid fuels lies in the emerging economies of China, India,

and countries in the Middle East, according to EIA's recently released International Energy Outlook 2014

(IEO2014). In the Reference case projection, world liquid fuels consumption increases 38% from 87 million

barrels per day (MMbbl/d) in 2010 to 119 MMbbl/d in 2040. China, India, and other developing countries in

Asia account for 72% of the net world increase in liquid fuels consumption, with Middle East consumers

accounting for another 13%. Most liquid fuel demand is for industrial uses and transportation.

In the United States, Europe, Japan, and other mature industrialized economies, liquid fuel demand has

leveled off and is projected to slowly decline. The combined effects of several factors have slowed or even

reversed the growth in liquid fuels use. These factors include sustained high oil prices, efficiency standards

for vehicles and equipment together with high taxation of motor fuels, price-driven fuel switching towards

non-oil fuels outside of transportation, vehicle saturation, as well as structural changes in factors such as

demographics and consumer behavior.

IEO2014 projects that 33 MMbbl/d of additional liquid fuel supply will be needed in 2040 compared to

2010 to satisfy growing demand for liquid fuels. The Reference case assumes that Organization of the

Petroleum Exporting Countries (OPEC) producers invest in incremental production capacity that enables

them to increase crude and lease condensate production by 14 MMbbl/d from 2010 to 2040 and that OPEC

crude and lease condensate producers maintain a share of between 40% and 45% of total world liquid fuels

production throughout the projection. The Middle East OPEC member countries alone account for 90% of

the total growth in projected OPEC crude and lease condensate production.

Copyright © 2014 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced,

redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained

in this publication. However, no warranty is given to the accuracy of its content . Page 5

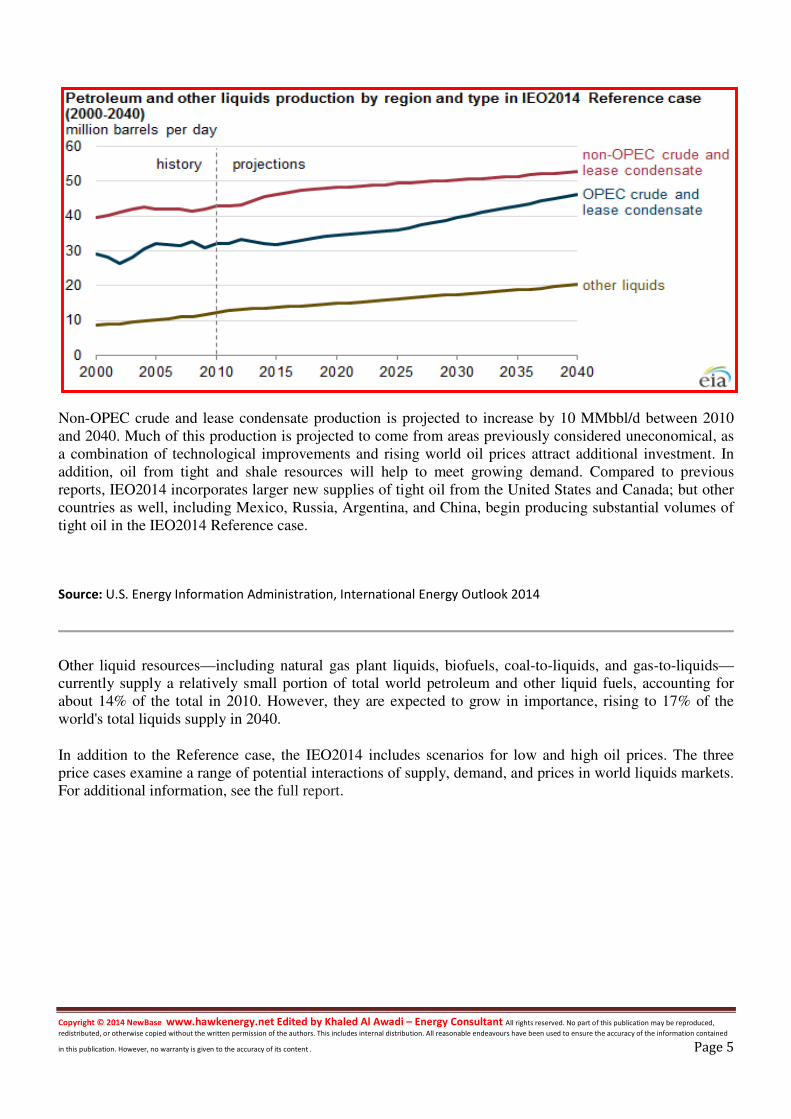

Non-OPEC crude and lease condensate production is projected to increase by 10 MMbbl/d between 2010

and 2040. Much of this production is projected to come from areas previously considered uneconomical, as

a combination of technological improvements and rising world oil prices attract additional investment. In

addition, oil from tight and shale resources will help to meet growing demand. Compared to previous

reports, IEO2014 incorporates larger new supplies of tight oil from the United States and Canada; but other

countries as well, including Mexico, Russia, Argentina, and China, begin producing substantial volumes of

tight oil in the IEO2014 Reference case.

Source: U.S. Energy Information Administration, International Energy Outlook 2014

Other liquid resources—including natural gas plant liquids, biofuels, coal-to-liquids, and gas-to-liquids—

currently supply a relatively small portion of total world petroleum and other liquid fuels, accounting for

about 14% of the total in 2010. However, they are expected to grow in importance, rising to 17% of the

world's total liquids supply in 2040.

In addition to the Reference case, the IEO2014 includes scenarios for low and high oil prices. The three

price cases examine a range of potential interactions of supply, demand, and prices in world liquids markets.

For additional information, see the full report.

Copyright © 2014 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced,

redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained

in this publication. However, no warranty is given to the accuracy of its content . Page 6

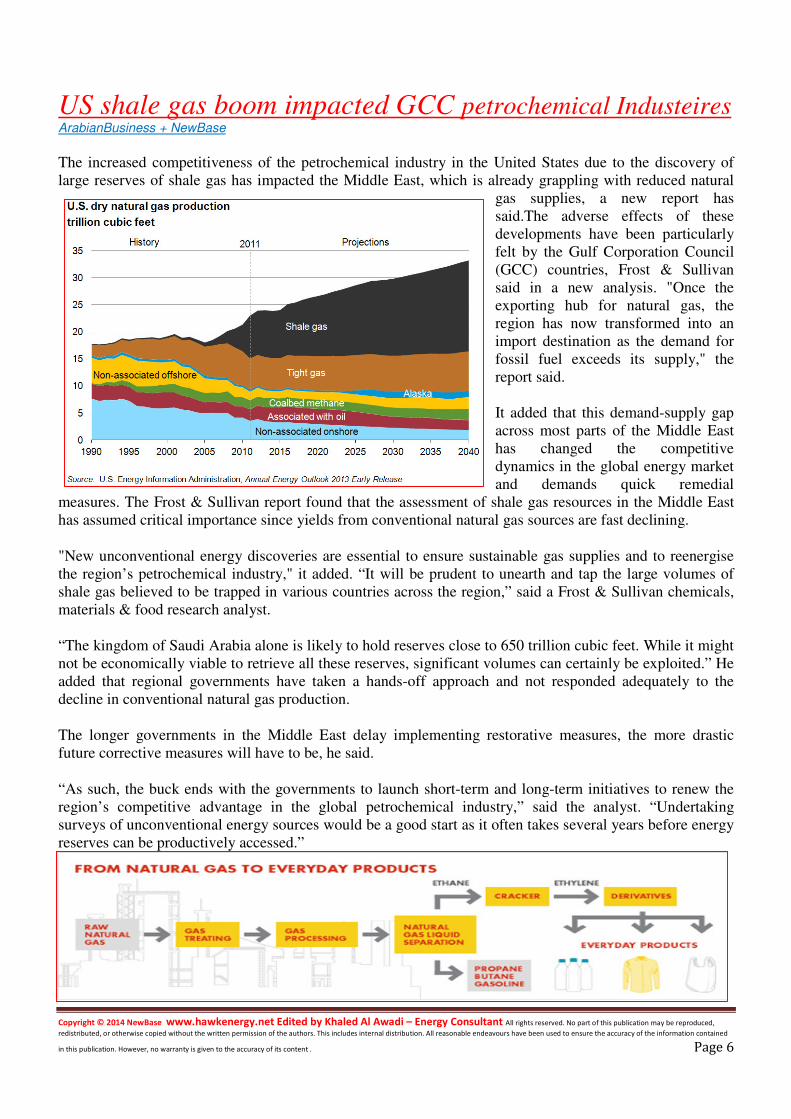

US shale gas boom impacted GCC petrochemical Industeires ArabianBusiness + NewBase

The increased competitiveness of the petrochemical industry in the United States due to the discovery of

large reserves of shale gas has impacted the Middle East, which is already grappling with reduced natural

gas supplies, a new report has

said.The adverse effects of these

developments have been particularly

felt by the Gulf Corporation Council

(GCC) countries, Frost & Sullivan

said in a new analysis. "Once the

exporting hub for natural gas, the

region has now transformed into an

import destination as the demand for

fossil fuel exceeds its supply," the

report said.

It added that this demand-supply gap

across most parts of the Middle East

has changed the competitive

dynamics in the global energy market

and demands quick remedial

measures. The Frost & Sullivan report found that the assessment of shale gas resources in the Middle East

has assumed critical importance since yields from conventional natural gas sources are fast declining.

"New unconventional energy discoveries are essential to ensure sustainable gas supplies and to reenergise

the region’s petrochemical industry," it added. “It will be prudent to unearth and tap the large volumes of

shale gas believed to be trapped in various countries across the region,” said a Frost & Sullivan chemicals,

materials & food research analyst.

“The kingdom of Saudi Arabia alone is likely to hold reserves close to 650 trillion cubic feet. While it might

not be economically viable to retrieve all these reserves, significant volumes can certainly be exploited.” He

added that regional governments have taken a hands-off approach and not responded adequately to the

decline in conventional natural gas production.

The longer governments in the Middle East delay implementing restorative measures, the more drastic

future corrective measures will have to be, he said.

“As such, the buck ends with the governments to launch short-term and long-term initiatives to renew the

region’s competitive advantage in the global petrochemical industry,” said the analyst. “Undertaking

surveys of unconventional energy sources would be a good start as it often takes several years before energy

reserves can be productively accessed.”

Copyright © 2014 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced,

redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained

in this publication. However, no warranty is given to the accuracy of its content . Page 7

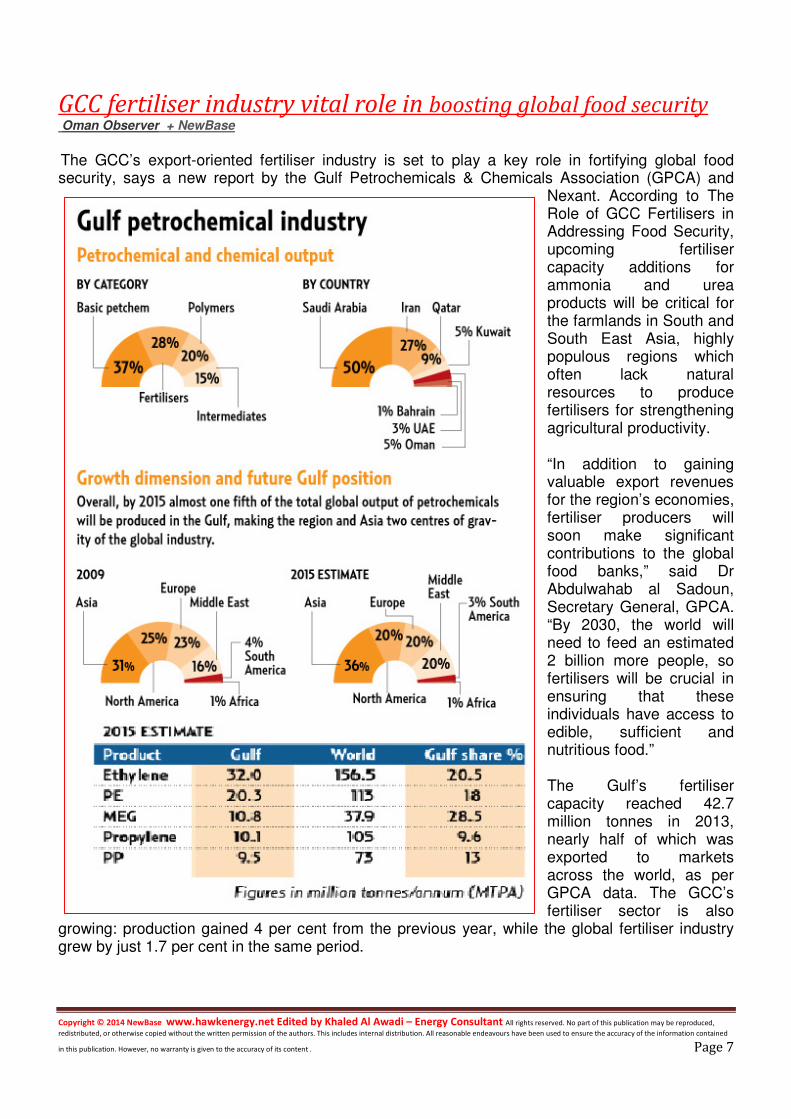

GCC fertiliser industry vital role in boosting global food security Oman Observer + NewBase

The GCC’s export-oriented fertiliser industry is set to play a key role in fortifying global food security, says a new report by the Gulf Petrochemicals & Chemicals Association (GPCA) and

Nexant. According to The Role of GCC Fertilisers in Addressing Food Security, upcoming fertiliser capacity additions for ammonia and urea products will be critical for the farmlands in South and South East Asia, highly populous regions which often lack natural resources to produce fertilisers for strengthening agricultural productivity.

“In addition to gaining valuable export revenues for the region’s economies, fertiliser producers will soon make significant contributions to the global food banks,” said Dr Abdulwahab al Sadoun, Secretary General, GPCA. “By 2030, the world will need to feed an estimated 2 billion more people, so fertilisers will be crucial in ensuring that these individuals have access to edible, sufficient and nutritious food.”

The Gulf’s fertiliser capacity reached 42.7 million tonnes in 2013, nearly half of which was exported to markets across the world, as per GPCA data. The GCC’s fertiliser sector is also

growing: production gained 4 per cent from the previous year, while the global fertiliser industry grew by just 1.7 per cent in the same period.

Copyright © 2014 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced,

redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained

in this publication. However, no warranty is given to the accuracy of its content . Page 8

Fertiliser sector growth has been augmented by the GCC’s vast reserves of natural gas, essential for producing ammonia and urea fertilisers. With relatively low domestic demand, the Gulf’s fertiliser exports are set continue to rise in the long- term. The growth of the GCC fertiliser industry, therefore, has the potential not only to overcome serious food security challenges, but also to raise the region’s profile as a major trade partner and producer of high- value commodities.”

The Role of GCC Fertilisers in Addressing Food Security is an in- depth report that surveys major trends across the agriculture, food,

energy and petrochemical industries. Jointly produced by the GPCA and Nexant, it will be released at GPCA’s Fertilizer Convention from September 16-18 in Dubai.

Copyright © 2014 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced,

redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained

in this publication. However, no warranty is given to the accuracy of its content . Page 9

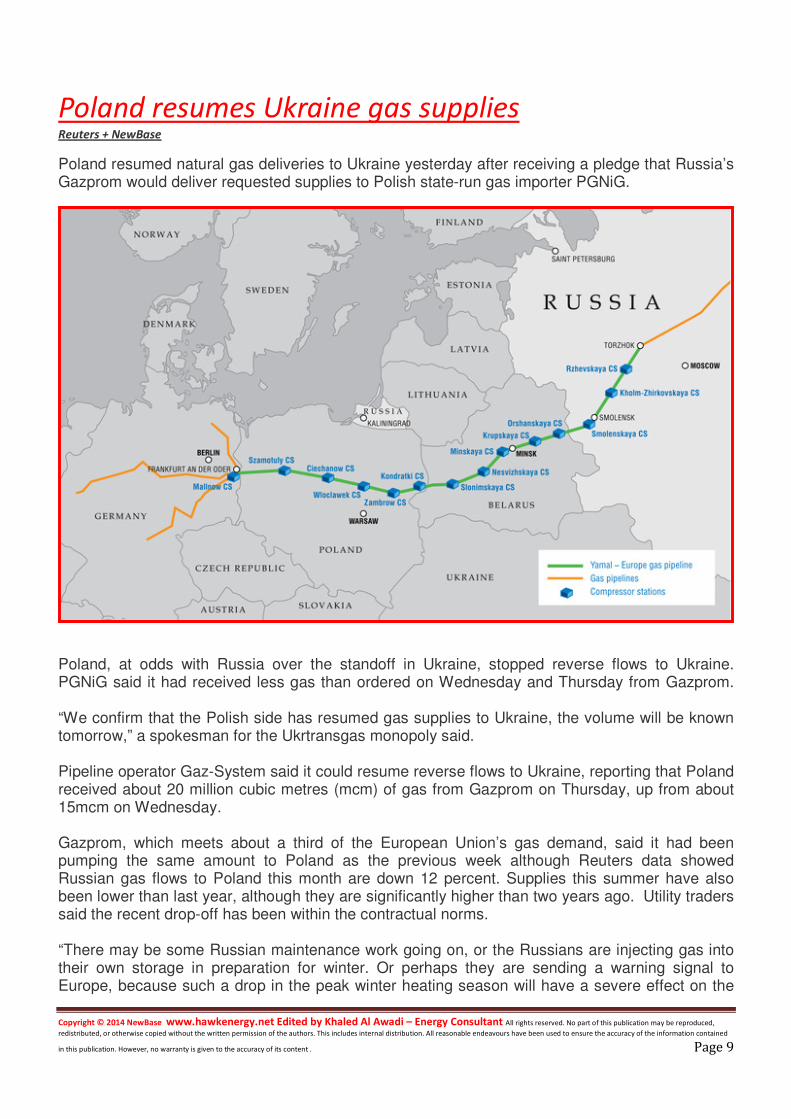

Poland resumes Ukraine gas supplies Reuters + NewBase

Poland resumed natural gas deliveries to Ukraine yesterday after receiving a pledge that Russia’s Gazprom would deliver requested supplies to Polish state-run gas importer PGNiG.

Poland, at odds with Russia over the standoff in Ukraine, stopped reverse flows to Ukraine. PGNiG said it had received less gas than ordered on Wednesday and Thursday from Gazprom. “We confirm that the Polish side has resumed gas supplies to Ukraine, the volume will be known tomorrow,” a spokesman for the Ukrtransgas monopoly said. Pipeline operator Gaz-System said it could resume reverse flows to Ukraine, reporting that Poland received about 20 million cubic metres (mcm) of gas from Gazprom on Thursday, up from about 15mcm on Wednesday. Gazprom, which meets about a third of the European Union’s gas demand, said it had been pumping the same amount to Poland as the previous week although Reuters data showed Russian gas flows to Poland this month are down 12 percent. Supplies this summer have also been lower than last year, although they are significantly higher than two years ago. Utility traders said the recent drop-off has been within the contractual norms. “There may be some Russian maintenance work going on, or the Russians are injecting gas into their own storage in preparation for winter. Or perhaps they are sending a warning signal to Europe, because such a drop in the peak winter heating season will have a severe effect on the

Copyright © 2014 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced,

redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained

in this publication. However, no warranty is given to the accuracy of its content . Page 10

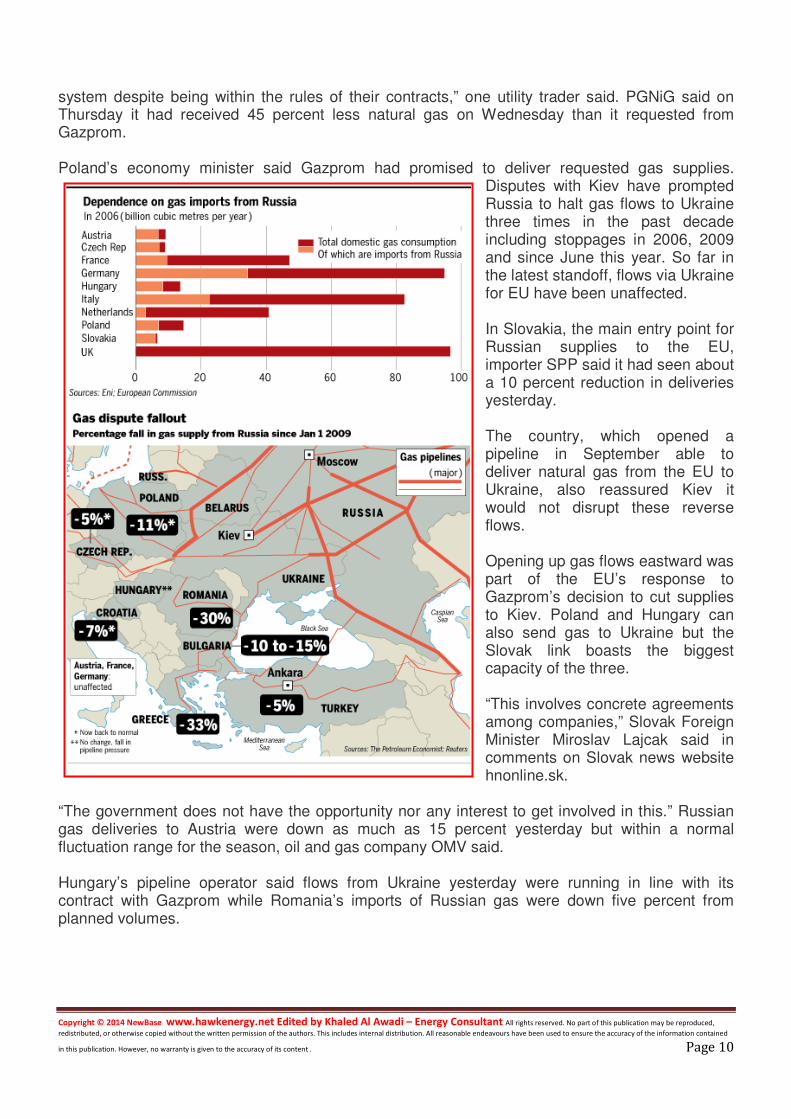

system despite being within the rules of their contracts,” one utility trader said. PGNiG said on Thursday it had received 45 percent less natural gas on Wednesday than it requested from Gazprom. Poland’s economy minister said Gazprom had promised to deliver requested gas supplies.

Disputes with Kiev have prompted Russia to halt gas flows to Ukraine three times in the past decade including stoppages in 2006, 2009 and since June this year. So far in the latest standoff, flows via Ukraine for EU have been unaffected. In Slovakia, the main entry point for Russian supplies to the EU, importer SPP said it had seen about a 10 percent reduction in deliveries yesterday. The country, which opened a pipeline in September able to deliver natural gas from the EU to Ukraine, also reassured Kiev it would not disrupt these reverse flows. Opening up gas flows eastward was part of the EU’s response to Gazprom’s decision to cut supplies to Kiev. Poland and Hungary can also send gas to Ukraine but the Slovak link boasts the biggest capacity of the three. “This involves concrete agreements among companies,” Slovak Foreign Minister Miroslav Lajcak said in comments on Slovak news website hnonline.sk.

“The government does not have the opportunity nor any interest to get involved in this.” Russian gas deliveries to Austria were down as much as 15 percent yesterday but within a normal fluctuation range for the season, oil and gas company OMV said. Hungary’s pipeline operator said flows from Ukraine yesterday were running in line with its contract with Gazprom while Romania’s imports of Russian gas were down five percent from planned volumes.

Copyright © 2014 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced,

redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained

in this publication. However, no warranty is given to the accuracy of its content . Page 11

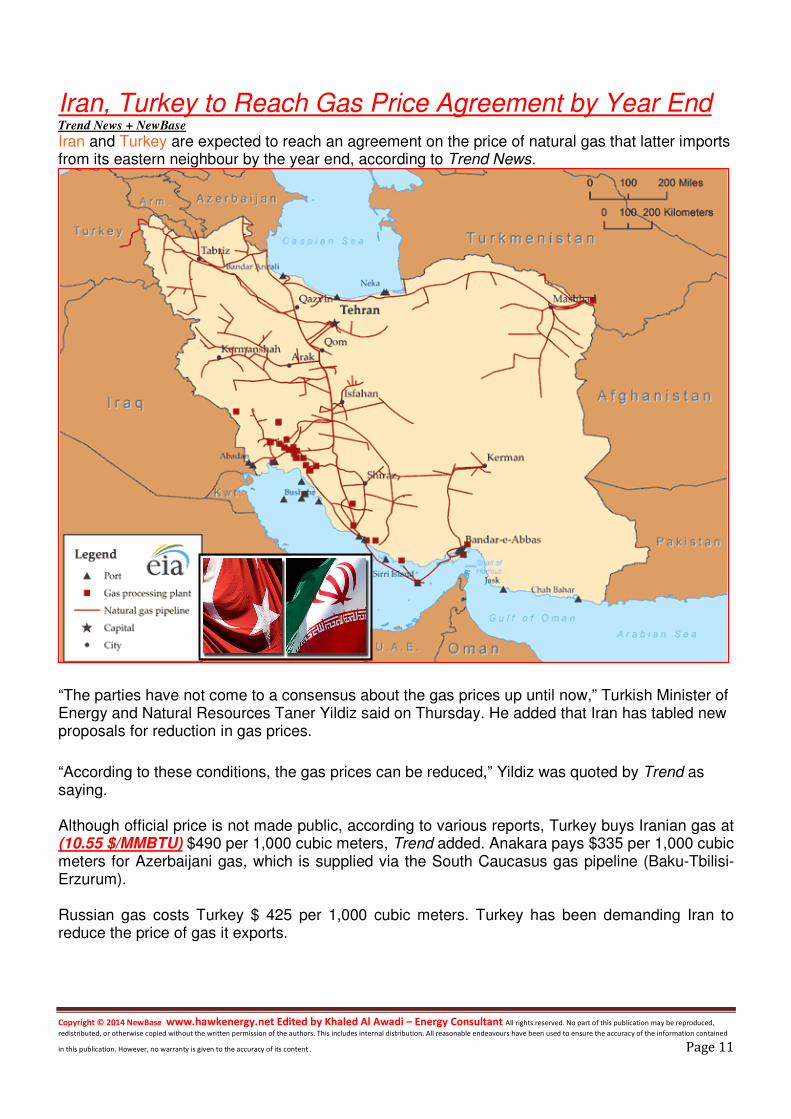

Iran, Turkey to Reach Gas Price Agreement by Year End Trend News + NewBase

Iran and Turkey are expected to reach an agreement on the price of natural gas that latter imports from its eastern neighbour by the year end, according to Trend News.

“The parties have not come to a consensus about the gas prices up until now,” Turkish Minister of Energy and Natural Resources Taner Yildiz said on Thursday. He added that Iran has tabled new proposals for reduction in gas prices.

“According to these conditions, the gas prices can be reduced,” Yildiz was quoted by Trend as saying. Although official price is not made public, according to various reports, Turkey buys Iranian gas at (10.55 $/MMBTU) $490 per 1,000 cubic meters, Trend added. Anakara pays $335 per 1,000 cubic meters for Azerbaijani gas, which is supplied via the South Caucasus gas pipeline (Baku-Tbilisi-Erzurum). Russian gas costs Turkey $ 425 per 1,000 cubic meters. Turkey has been demanding Iran to reduce the price of gas it exports.

Copyright © 2014 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced,

redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained

in this publication. However, no warranty is given to the accuracy of its content . Page 12

Japan’s nuclear ramp up to weigh on Asia oil and gas market

The National + NewBase

The approval in Japan to restart nuclear reactors, the first since the earthquake and tsunami that led to the Fukushima Daiichi nuclear plant disaster in 2011, is another bearish development for oil and gas markets in Asia, the most important market for Middle East producers.

Japan’s Nuclear Regulation Authority, last week gave final approval to restart two reactors at Kyushu Electric Power’s Sendai plant, about 1,360 kilometres south of Tokyo.

The plant’s two reactors had been shut down after the Fukushima disaster, along with 48 others across the country. Now, the Sendai plant is the first to have met the much tougher standards set by the authority, which was set up after the disaster with a strict safety mandate.

The Sendai reactors still must get approvals from city and regional governments before they can resume operations, but they are expected to be clear to start producing electricity again from early next year. Sendai is one of

10 utilities that have applied so far to get safety approval for 20 reactors. The shutdown of Japan’s nuclear power sector has hit the country hard, both economically and environmentally.

According to the International Energy Agency, Japan’s carbon dioxide emissions rose by 70 million tonnes, or 5.8 per cent, in 2012, a rate of growth that had not been seen in two decades, as fossil fuels were burnt to make up for the loss of 90 per cent of the electricity generation that had been coming from nuclear power. About 30 per cent of Japan’s total electricity had been supplied by the nuclear sector before the Fukushima disaster.

Japan’s prime minister, Shinzo Abe, has been making great efforts to soothe public opinion to start getting nuclear capacity back online. The increase in fossil-fuel imports was also a large contributor to Japan’s record trade deficit of ¥6.9 trillion (Dh236 billion) in 2012.

The most expensive and least efficient method of power generation is oil-fired, which accounts for about 15 per cent of Japan’s power generation and will be first to be substituted, says Laszlo Varro, the head of power, coal and natural gas analysis at the IEA.

However, the natural gas market is likely to feel the impact even more, as Japan has relied heavily on LNG for gas-fired generation – which runs more consistently than oil-fired – to fill the power

Copyright © 2014 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced,

redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained

in this publication. However, no warranty is given to the accuracy of its content . Page 13

generation gap left by nuclear. Now, says Mr Varro, “there is a feeling in the gas markets that Japan has turned the corner”. The Japanese nuclear ramp-up comes at a time when a considerable amount of new LNG supply is due on the market.

Australia has seven large LNG programmes at various stages of development, with total investment of more than $200bn, and production from those plants is due to start hitting the Asian market soon, adding to the more than 20 million tonnes a year of LNG Australia already exports from its three big LNG plants.

Australia is set to surpass Qatar as the world’s biggest exporter of LNG, according to Citibank, which forecasts Australia’s exports will climb to 83 million tonnes a year by 2020, compared with 79 million tonnes for Qatar. The market already has been weak, mainly because of lacklustre economic performances in Asia and elsewhere.

LNG prices for delivery to north-east Asia were at US$12.50 per million British thermal units at the end of last week, near to their lowest levels since 2011. The good news for Japan’s nuclear industry is likely to darken the mood further in the LNG market.

Copyright © 2014 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced,

redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained

in this publication. However, no warranty is given to the accuracy of its content . Page 14

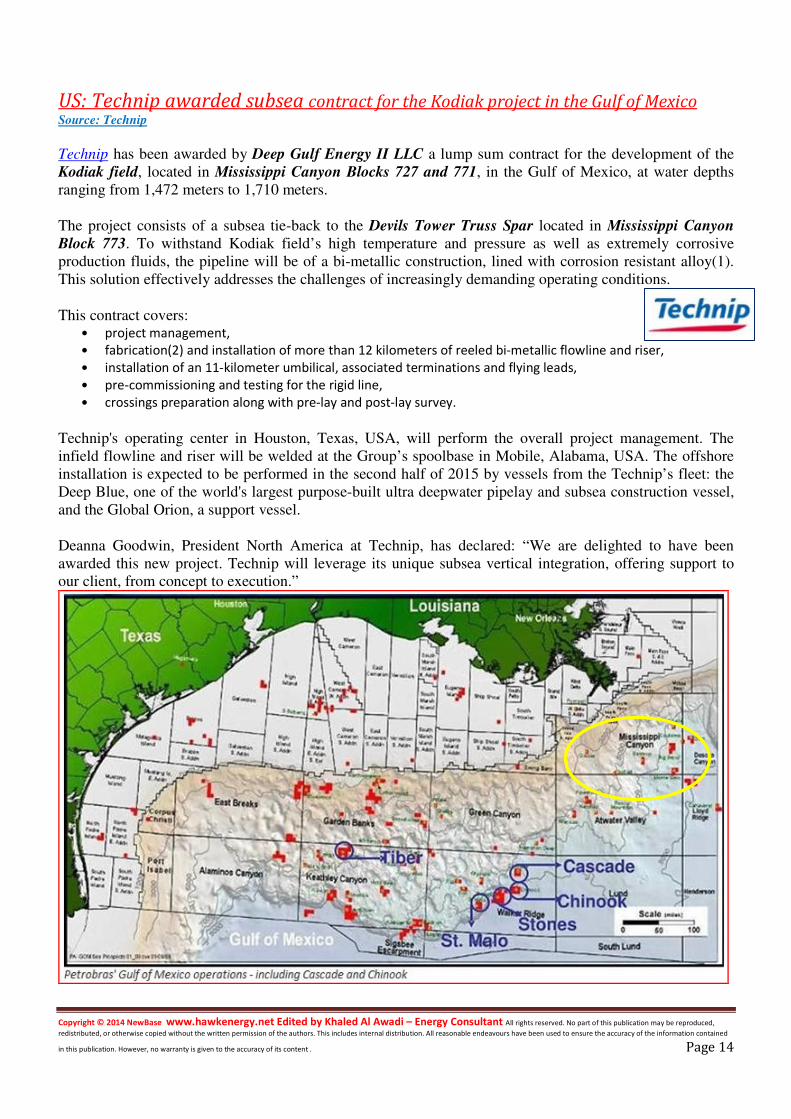

US: Technip awarded subsea contract for the Kodiak project in the Gulf of Mexico Source: Technip

Technip has been awarded by Deep Gulf Energy II LLC a lump sum contract for the development of the

Kodiak field, located in Mississippi Canyon Blocks 727 and 771, in the Gulf of Mexico, at water depths

ranging from 1,472 meters to 1,710 meters.

The project consists of a subsea tie-back to the Devils Tower Truss Spar located in Mississippi Canyon

Block 773. To withstand Kodiak field’s high temperature and pressure as well as extremely corrosive

production fluids, the pipeline will be of a bi-metallic construction, lined with corrosion resistant alloy(1).

This solution effectively addresses the challenges of increasingly demanding operating conditions.

This contract covers: • project management,

• fabrication(2) and installation of more than 12 kilometers of reeled bi-metallic flowline and riser,

• installation of an 11-kilometer umbilical, associated terminations and flying leads,

• pre-commissioning and testing for the rigid line,

• crossings preparation along with pre-lay and post-lay survey.

Technip's operating center in Houston, Texas, USA, will perform the overall project management. The

infield flowline and riser will be welded at the Group’s spoolbase in Mobile, Alabama, USA. The offshore

installation is expected to be performed in the second half of 2015 by vessels from the Technip’s fleet: the

Deep Blue, one of the world's largest purpose-built ultra deepwater pipelay and subsea construction vessel,

and the Global Orion, a support vessel.

Deanna Goodwin, President North America at Technip, has declared: “We are delighted to have been

awarded this new project. Technip will leverage its unique subsea vertical integration, offering support to

our client, from concept to execution.”

Copyright © 2014 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced,

redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained

in this publication. However, no warranty is given to the accuracy of its content . Page 15

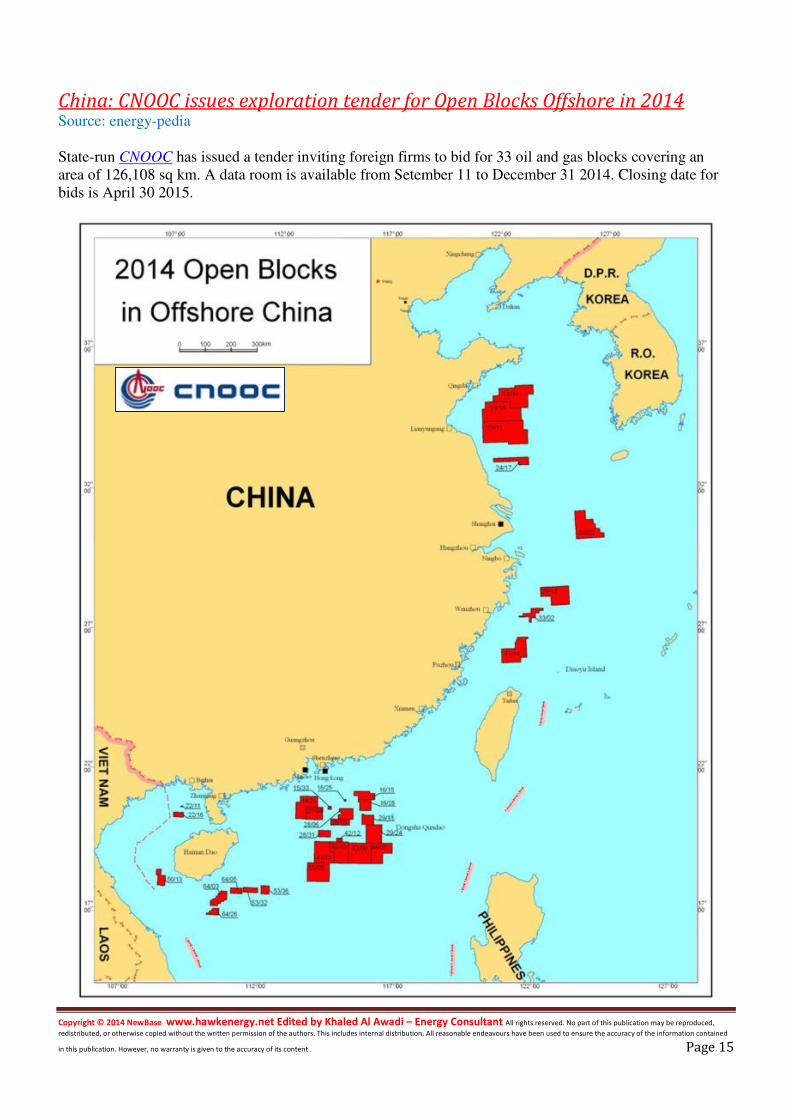

China: CNOOC issues exploration tender for Open Blocks Offshore in 2014 Source: energy-pedia

State-run CNOOC has issued a tender inviting foreign firms to bid for 33 oil and gas blocks covering an

area of 126,108 sq km. A data room is available from Setember 11 to December 31 2014. Closing date for

bids is April 30 2015.

Copyright © 2014 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced,

redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained

in this publication. However, no warranty is given to the accuracy of its content . Page 16

NewBase For discussion or further details on the news below you may contact us on +971504822502 , Dubai , UAE

Your partner in Energy Services

NewBase For discussion or further details on the news below you may contact us on +971504822502 , Dubai , UAE

Your partner in Energy Services

Copyright © 2014 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced,

redistributed, or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained

in this publication. However, no warranty is given to the accuracy of its content . Page 17

Khaled Malallah Al Awadi, Energy Consultant

MSc. & BSc. Mechanical Engineering (HON), USA ASME member since 1995 Emarat member since 1990

Mobile : +97150-4822502 [email protected] [email protected]

Khaled Al Awadi is a UAE National with a total of 24 yearsKhaled Al Awadi is a UAE National with a total of 24 yearsKhaled Al Awadi is a UAE National with a total of 24 yearsKhaled Al Awadi is a UAE National with a total of 24 years of experience in theof experience in theof experience in theof experience in the Oil & Gas sector. Currently working as Oil & Gas sector. Currently working as Oil & Gas sector. Currently working as Oil & Gas sector. Currently working as

Technical Affairs Specialist for Emirates General Petroleum Corp. “Emarat“ with external volTechnical Affairs Specialist for Emirates General Petroleum Corp. “Emarat“ with external volTechnical Affairs Specialist for Emirates General Petroleum Corp. “Emarat“ with external volTechnical Affairs Specialist for Emirates General Petroleum Corp. “Emarat“ with external voluntary Energy consultation for untary Energy consultation for untary Energy consultation for untary Energy consultation for

the GCC area via Hawk Energy Service as a UAE operations base , Most of the experience were spent as the Gas Operations the GCC area via Hawk Energy Service as a UAE operations base , Most of the experience were spent as the Gas Operations the GCC area via Hawk Energy Service as a UAE operations base , Most of the experience were spent as the Gas Operations the GCC area via Hawk Energy Service as a UAE operations base , Most of the experience were spent as the Gas Operations

Manager in Emarat , responsible for Emarat Gas Pipeline Network Facility & gas compressor stationsManager in Emarat , responsible for Emarat Gas Pipeline Network Facility & gas compressor stationsManager in Emarat , responsible for Emarat Gas Pipeline Network Facility & gas compressor stationsManager in Emarat , responsible for Emarat Gas Pipeline Network Facility & gas compressor stations . Through the years , he has developed . Through the years , he has developed . Through the years , he has developed . Through the years , he has developed

great experiences in the designing & constructinggreat experiences in the designing & constructinggreat experiences in the designing & constructinggreat experiences in the designing & constructing of gas pipelines, gas metering & regulating stations and in the engineering of supply of gas pipelines, gas metering & regulating stations and in the engineering of supply of gas pipelines, gas metering & regulating stations and in the engineering of supply of gas pipelines, gas metering & regulating stations and in the engineering of supply

routes. Many years were spent drafting, & compiling gas transportation , operatroutes. Many years were spent drafting, & compiling gas transportation , operatroutes. Many years were spent drafting, & compiling gas transportation , operatroutes. Many years were spent drafting, & compiling gas transportation , operation & maintenance agreements along with many MOUs for ion & maintenance agreements along with many MOUs for ion & maintenance agreements along with many MOUs for ion & maintenance agreements along with many MOUs for

the local authorities. He has become a reference for many of the Oil & Gas Conferences held in the UAE andthe local authorities. He has become a reference for many of the Oil & Gas Conferences held in the UAE andthe local authorities. He has become a reference for many of the Oil & Gas Conferences held in the UAE andthe local authorities. He has become a reference for many of the Oil & Gas Conferences held in the UAE and Energy program broadcasted Energy program broadcasted Energy program broadcasted Energy program broadcasted

internationally , via GCC leading satellite Channels . internationally , via GCC leading satellite Channels . internationally , via GCC leading satellite Channels . internationally , via GCC leading satellite Channels .

NewBase : For discussion or further details on the news above you may contact us on +971504822502 , Dubai , UAE

NewBase 14 September 2014 K. Al Awadi