Embed Size (px)

Citation preview

Markets Insight Opportunities in Water Technologies October 2015 Samrat P. Karnik Managing Director

Macro Review

Introduction and Executive Summary This water sector review focuses on the opportunities within the water technologies / solutions sectors

The key themes developed in the following pages are as follows:

- Price of water will be an enabler: Price will continue to migrate towards true cost of delivery and help investment

- All water sub-sectors are not equal: Demand dynamics, customer pain points, mode of delivery, etc. carry greater weight

- Industrial and AG markets preferred longer term: Expect better growth, absorption of new technologies and profit margins

- Fundamentals are strong: EBITDA margins are at record levels and revenue growth returning to long-term averages

- Performance drives value creation: Strong correlation to sub-sector growth, margins and long-term value creation

- Innovation expected to be robust: Focus will be on water reuse, desalination, “smart water” and nutrient recovery

- Institutional capital will play a role: While VCs have severely dialed back investment activity, dedicated water PE funds and individuals with interest in water will continue to play a role with firms such as Excellere Partners posting big successes

- M&A to play a key role in corporate growth: Development of new technologies by emerging companies, the need to expand geographic footprints and/or expand product /solution portfolios to offer comprehensive solutions to customers, and the need to consolidate fragmented subsectors will be key drivers for M&A activity

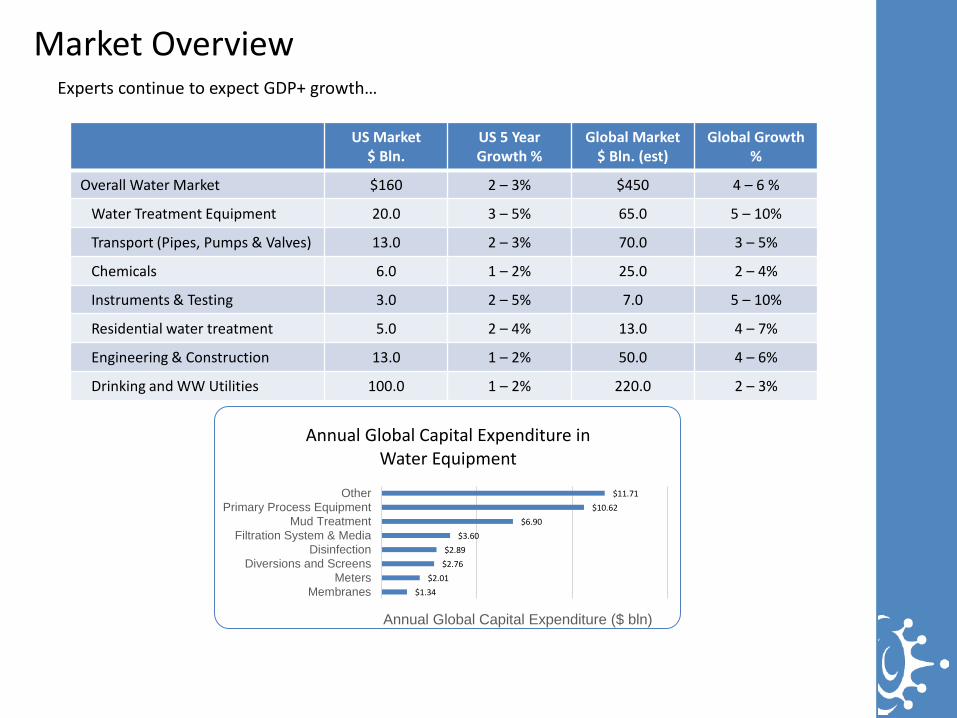

Market Overview Experts continue to expect GDP+ growth…

US Market $ Bln.

US 5 Year Growth %

Global Market $ Bln. (est)

Global Growth %

Overall Water Market $160 2 – 3% $450 4 – 6 %

Water Treatment Equipment 20.0 3 – 5% 65.0 5 – 10%

Transport (Pipes, Pumps & Valves) 13.0 2 – 3% 70.0 3 – 5%

Chemicals 6.0 1 – 2% 25.0 2 – 4%

Instruments & Testing 3.0 2 – 5% 7.0 5 – 10%

Residential water treatment 5.0 2 – 4% 13.0 4 – 7%

Engineering & Construction 13.0 1 – 2% 50.0 4 – 6%

Drinking and WW Utilities 100.0 1 – 2% 220.0 2 – 3%

$1.34 $2.01

$2.76 $2.89

$3.60 $6.90

$10.62 $11.71

MembranesMeters

Diversions and ScreensDisinfection

Filtration System & MediaMud Treatment

Primary Process EquipmentOther

Annual Global Capital Expenditure ($ bln)

Annual Global Capital Expenditure in Water Equipment

Four Key Demand Drivers for Technology

3.0x

to 4

.0x

Incr

ease

In W

ater

Tech

nolo

gy /

Sol

utio

ns

Mar

ket?

2013 2030

It is conceivable that the c. $150 billion global market for water technologies and solutions could grow at over 5.0% CAGR over the next couple of decades given baseline volume growth of 3.0% supplemented by gradual transition to market price, regulation, and stress on efficiency to reduce energy and O&M costs.

$150 Bln. Est. Mrkt. for Water

Technology

Investment “Heat Map” for Technology Companies

Engineering Transport & Storage Treatment Test, Monitoring &

Control

Design

Engineer

Build

Own

Operate

Transport

Storage

Pumps

Valves

Screens

Pipes

Absorbents

Tanks

Harvesting

Drinking Water

Waste water

Applied Water

Primary

Membranes

UV & Ozone

Chemicals

RO / Barrier

Desalination

Recovery

Oil & Gas

Industrial

Bld. / HVAC

Irrigation

Bio-mimicry

Field Sampling

Online

Laboratory

Automation / Control

Asset Inspection

Remote Monitoring

SaaS

Growth companies

Legend On Investment Types

In-line; mature companies

Flat or at risk segments

High growth / emerging

Key Non-Municipal Growth End-Markets

Agriculture Marine – Ballast H20 Power Generation Produced Water

Water to oil ratio (WOR) expected to increase from 2.5x to 5.0x on the back of unconventional production

Equipment portion expected to grow from $0.7 Bln to $2.9 Bln. by 2025, as part of a $10 billion market

More legislation on water use and treatment expected (Prop 6 in TX)

Largely a logistics business opportunity

Given water is the biggest cost component, technologies that reduce water costs should benefit

However, strong near-term headwinds

~ 40% of water consumption for industrial applications in OECD countries is for energy generation (it is the second largest user after ag)

In contrast, in developing countries, only 8.0% is used in power production

Sets the stage for large demand growth

Regulation driven: Significant focus on curtailing use and improving the quality of returned water

Increased regulations with three rules being proposed by the EPA

70% to 80% use Gravity feeding highly

inefficient resulting in excess water, fertilizer use, and lower crop yield

In Asia, only 4% land is micro- or drip- irrigated vs. nearly 40% in the US and 14% on a global basis

Immense opportunity as farms convert

Countries like India showing success

Focus on curtailing use and pollutants

However, some products have been commoditized

Opportunity created by regulation to protect marine life

If fully put into effect, potential $34B dollar opportunity from 2010 to 2020 (over 57,000 vessels) to convert all ships

Proposed IMO requires ships to treat ballast water before returning it to the ocean

Sector Performance

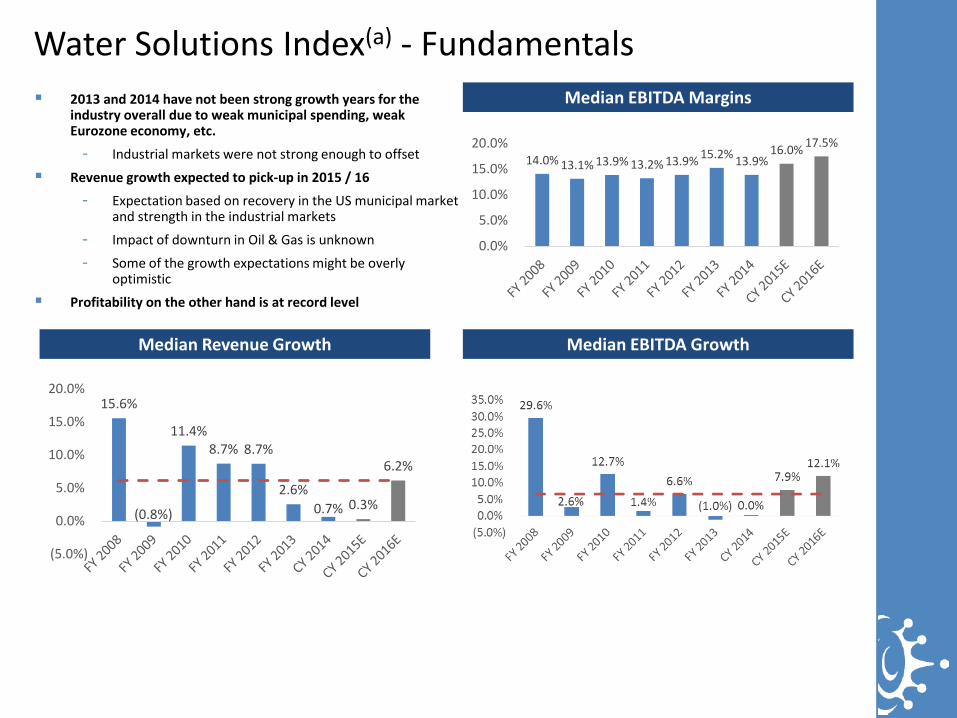

Water Solutions Index(a) - Fundamentals

2013 and 2014 have not been strong growth years for the industry overall due to weak municipal spending, weak Eurozone economy, etc.

- Industrial markets were not strong enough to offset

Revenue growth expected to pick-up in 2015 / 16

- Expectation based on recovery in the US municipal market and strength in the industrial markets

- Impact of downturn in Oil & Gas is unknown

- Some of the growth expectations might be overly optimistic

Profitability on the other hand is at record level

Median EBITDA Margins

Median EBITDA Growth Median Revenue Growth

14.0% 13.1% 13.9% 13.2% 13.9% 15.2% 13.9% 16.0% 17.5%

0.0%

5.0%

10.0%

15.0%

20.0%

15.6%

(0.8%)

11.4% 8.7% 8.7%

2.6% 0.7% 0.3%

6.2%

(5.0%)

0.0%

5.0%

10.0%

15.0%

20.0%

Water Solutions Index – Valuation Performance

The S&P Global Water Index has by and large kept pace with the industrial and S&P 500 benchmarks - Municipal spending issues in North America and

Europe have negatively impacted sales growth Valuation on both revenue and EBITDA basis are either at

or above pre-recession levels - This is in part due to general market bullishness seen in

2013 and 2014; and - In part due to a persistent sense of optimism in the

investor community about the growth potential of the water sector (despite near term earnings issues)

3 Year Water Index Performance

Median EV/EBITDA Median EV / Revenue

Water Technology Valuation Continuum

While the graphic provides a directional sense, company specific factors such as size, IP, end-markets, growth expectations, profitability, management, etc. are overriding factors

LOW < ----- Technology Differentiation, Cost of Failure, ROI and Expected Growth --- > HIGH

Tank

s

5 x

10 x

15 x Pi

pes

Prim

ary

Equi

p.

Pum

ps Au

tom

atio

n

Test

/ In

stru

men

ts

Desa

linat

ion

Mem

bran

es /

RO

Disin

fect

ion

Valv

es

Chem

ical

s

EV /

EBIT

DA

Smar

t Wat

er

Investment Activity

Desalination and Brackish Water

Intensification of Treatment

Resource and Nutrient Recovery

Reduced Chemical Use

Smart Water

Water for Unconventional

Oil & Gas

New Business Models and Partnerships

Extensive focus on reducing energy consumption of the process, which is the largest cost Two traditional technologies (evaporation and RO) reaching theoretical maximum Expect innovations from inside and outside the industry, and use of renewable energy

Urban density will require plants to handle greater flow rates with ever smaller footprints

Large market opportunities in densely packed Asian cities where growth is the strongest

One of the best options to reduce compliance costs and increase asset ROIs Recovery of nutrients and / or gas are the two areas most advanced New delivery / service models similar to the solid waste or power industry emerging

For both compliance and cost purposes Primarily for municipal and in applied water Focus mainly in OECD countries

Enabling technology to manage demand, reduce energy consumption, increase supply, curtail O&M costs, prevent system failures and reduce asset intensity

Investment and adoption necessary to improve ROI and prevent system failure Most likely to fundamentally alter how water infrastructure is managed

Regulatory mandates on contaminants and level of use to drive treatment and re-use Companies focused on applying desalination for brackish water and / or water reuse

New models evolving that help reduce use, lower capital costs, and manage risks Areas where new business models are most likely are in (i) nutrient recovery, (ii) energy

recovery, (iii) monitoring / remote data collection, and (iv) risk mitigation / management

Key Focus Areas for Innovation in Water

CY 2014 witnessed modest water sector M&A activity with eight transactions for roughly $600 million in enterprise value

Some of the notable transactions were:

- Kurita Water’s acquisition of B.K. Giulini’s Performance Products business for c. $300 million:

- The acquisition enables Kurita to strengthen its overseas business platform mainly in Europe - Kurita expects to generate synergy, with its technologies and products and those of the acquired business

- LG Chem’s acquisition of NanoH2O for $200 million:

- Accelerates the delivery of innovative and energy-efficient membrane technologies to the desalination industry by benefiting from LG Chem’s distribution and capital resources

- Strengthens LG Chem’s IP for desalination and RO membranes

10 Year Water Solutions M&A Activity (excludes Water Utilities)

$566

$1,497

$25

$8,989

$51 $398 $268

$1,554

$12,702

$7,434

$4,455

0

2

4

6

8

10

12

14

$0

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

$14,000

Deal

Vol

ume

Mill

ions

Source: CleanTech Group

Water Sector M&A Activity

NanoH2O (VC) U.S. Water Service (PE)

• Date: March 14, 2014

• Transaction Value: $200 million; estimated at over 10.0x actual revenue

• Buyer Description: LG Chem is a diversified chemical company

• Seller Description: NanoH20 provides advanced reverse osmosis (RO) membranes that lower the cost of desalination

• Rationale

• Strengthened LG Chem’s IP for desalination and RO membranes

• Provides LG an immediately strengthened position in the high-growth desalination market through ownership of a leading, emerging technology company

• Provided a c. 2.0x return on total invested VC capital; not the greatest in the land of venture capital investments by a far stretch, but a rare example of a successful exit for a VC investment in the water sector

• Date: January 27, 2015

• Transaction Value: $190 million

• Buyer description: Allete is an American utility and energy company

• Seller description: US Water Service provides integrated water management for industrial processes / applications

• Under Excellere’s ownership, the company had grown c. 3.5x in revenues and c. 4.0x in EBITDA through seven acquisitions and 20% year-on-year organic growth

• Rationale:

• Allete wanted to diversity into unregulated businesses to increase shareholder returns

• Viewed US Water Services as a service centric, stable cash flow, growth platform; and

• Cultural fit with management and financial wherewithal to allow management to continue to grow the business

Private Capital (VC and PE) Success Stories

Appendix

Client Clearwater OptiRTC JWC Environmental

Marsh McBirney Trojan Technologies

Buyer Type Strategic Financial Financial Strategic Strategic

Business Provides non-chemical water

treatment system for cooling water that prevents scale and

biofilm

Opti integrates sensors, forecasts, and environmental

information to actively control

water and environmental infrastructure

Specializes in design and supply of

wastewater solids reduction equipment

Provides flow and level water monitoring instruments

Leading provider of UV disinfection

systems for water treatment

Process Type Broad Auction; Distressed Sale

Capital Raise

Buy-side Transaction Targeted Auction Targeted Auction

Headwaters’ Water Technology Transaction Experience

Samrat P. Karnik, Managing Director Mr. Karnik has extensive middle-market corporate finance advisory experience across the full spectrum of advisory assignments such as mergers & acquisitions, private financing of debt and growth equity, joint ventures and strategic alternatives assessments. He has completed over 25 M&A, LBO, shareholder defense and general corporate advisory mandates for entrepreneur-owned, private and public companies. He joined HeadwatersMB in 2014 with a focus on working with industrial technology companies, in particular those in instrumentation & sensors, automation & advanced manufacturing technologies, energy efficiency and environmental technology sectors where he has considerable legacy experience.

Prior to joining HeadwatersMB, Mr. Karnik was a senior banker in the M&A and Industrial groups of both Duff & Phelps and Houlihan Lokey where he was responsible for covering and providing investment banking advisory services to companies in the Industrial and Environmental Technologies sectors. Prior to Houlihan Lokey, he was an Associate at The Nassau Group, and began his investment banking career at Berenson Minella & Co. a premier M&A and restructuring advisory firm.

Mr. Karnik’s significant clients have included companies such as Babcock & Wilcox, CIRCOR, Crest Ultrasonic, Flow International, Mitsui & Co., Robbins & Myers, Standex Corporation, and Trojan Technologies and sponsors such as ACAS, Carlyle Group, and Littlejohn among other public and private corporations and private equity firms. In addition, his extensive work with entrepreneur led and family-owned companies has established a robust appreciation for understanding, anticipating and handling issues that need to be navigated successfully to lead these companies through their milestone transactions.

Mr. Karnik graduated from New York University’s Leonard N. Stern School of Business where he was on the Dean’s Honors List and Beta Gamma Sigma Honor Society. Mr. Karnik is also a co-founder and Chief Strategy Officer for Dreambox Emergence Benefit, LLC, a social enterprise focused on deploying 3D printing / additive manufacturing technologies for the benefit of rural, underdeveloped communities.