Embed Size (px)

Citation preview

ALM for Life Insurers, 18–19 Sepetember 2013AllianceBernstein.com

Erik Vynckier Chief Investment Officer—Insurance (EMEA)

Wien/Vienna 28 May 2015

Preparing the Buy-Side to Optimize Collateral4th Annual Collateral Management Forum

ALM for Life Insurers, 18–19 Sepetember 2013AllianceBernstein.com

Agenda

�Asset Allocation + Derivatives Overlay = Collateral

�Cleaning the Credit Support Annex

�Planning Liquidity with Potential Future Exposure

�High Performance Computation

�Operating Model: the Integrated Front-to-Back Office

1

ALM for Life Insurers, 18–19 Sepetember 2013AllianceBernstein.com

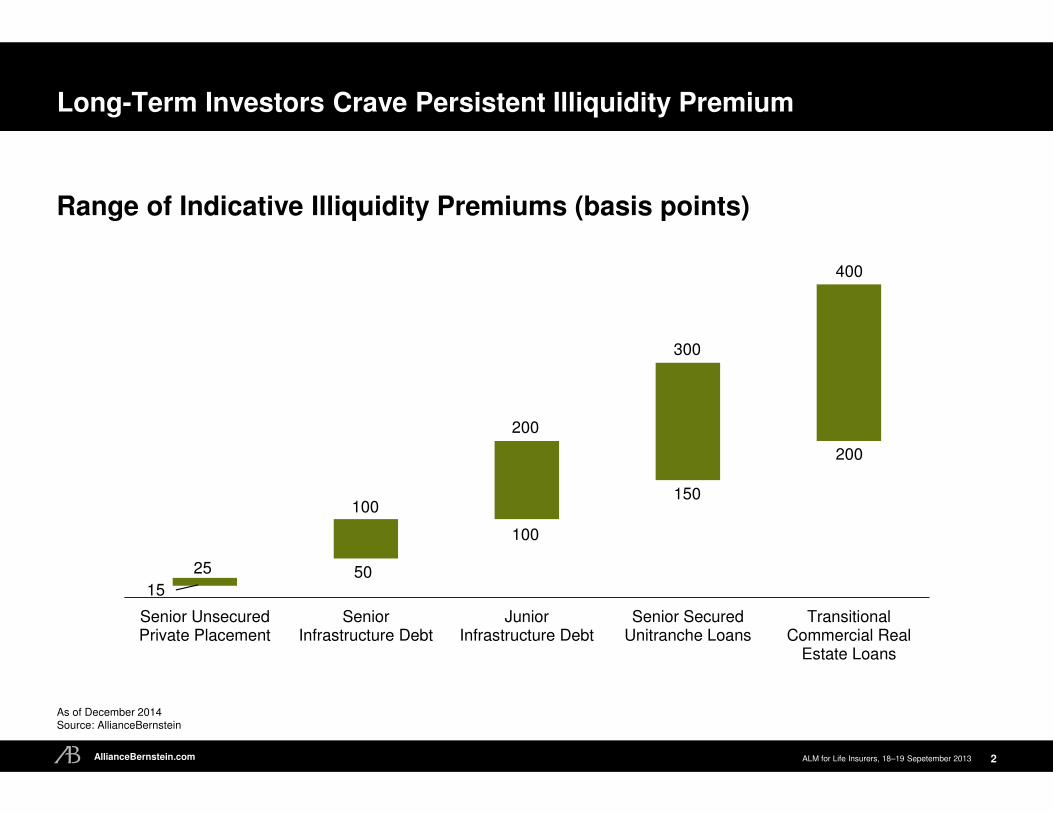

Long-Term Investors Crave Persistent Illiquidity Premium

2

As of December 2014Source: AllianceBernstein

Senior UnsecuredPrivate Placement

SeniorInfrastructure Debt

JuniorInfrastructure Debt

Senior SecuredUnitranche Loans

TransitionalCommercial Real

Estate Loans

15

25

200

100

100

50

300

150

400

200

Range of Indicative Illiquidity Premiums (basis points)

ALM for Life Insurers, 18–19 Sepetember 2013AllianceBernstein.com

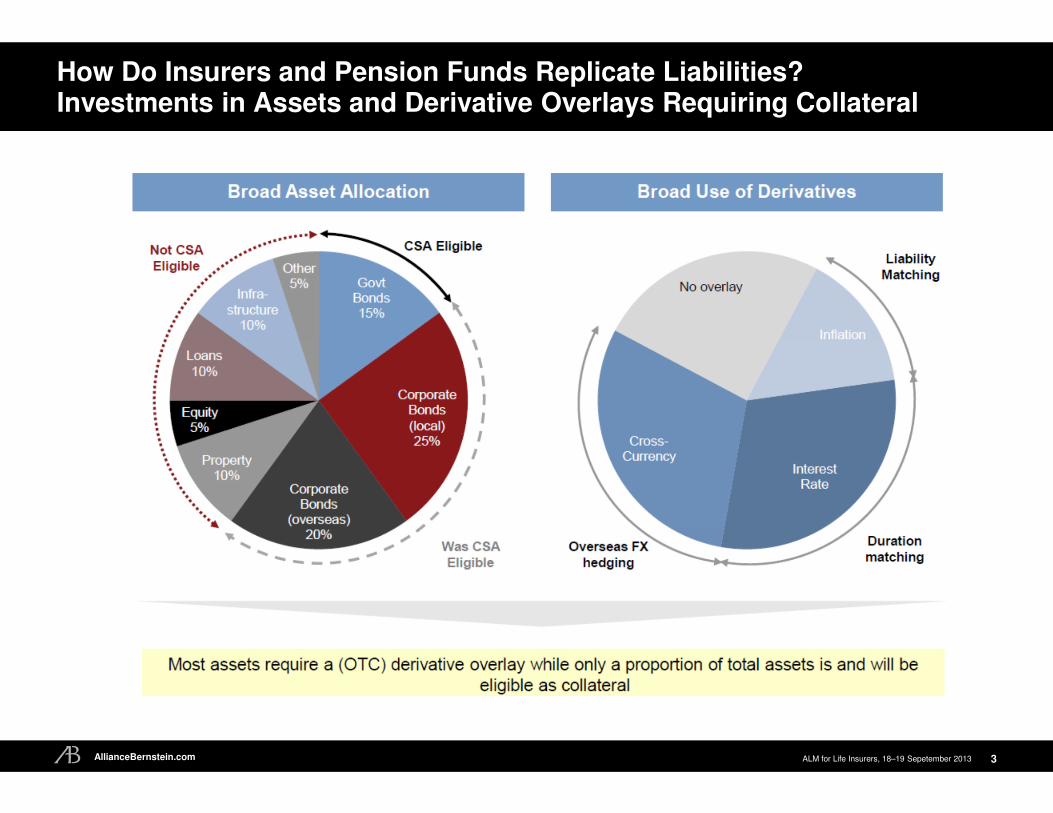

How Do Insurers and Pension Funds Replicate Liabilities?Investments in Assets and Derivative Overlays Requiring Collateral

3

ALM for Life Insurers, 18–19 Sepetember 2013AllianceBernstein.com

Collateral ManagementDerivatives May Constrain Asset Allocation

�Collateral may be tight

�Collateral needs to be funded, and suffers haircuts

�Opportunity cost for having to hold cash for collateral, constrains investment strategy

�Repo markets to generate cash involves extra operations and costs and an agreed legal

framework known as GMRA (global master repurchase agreement)

�Volatile and/or illiquid assets are ruled out as collateral

�Clearing and settlement through a clearing house requires a “clean” cash CSA

�The future of un-cleared derivatives?

�Pension funds benefit from a transition phase where they are not forced to clear their derivative trades

�The future of un-collateralized derivatives?

�Non-financial corporates below certain trading and exposure thresholds

�Heavy capital charges (CVA) borne by counterparty in Basel III impact pricing

4

ALM for Life Insurers, 18–19 Sepetember 2013AllianceBernstein.com

OTC Derivatives Regulatory Overview

5

6

ALM for Life Insurers, 18–19 Sepetember 2013AllianceBernstein.com

Regulations Impacting DerivativesAvalanche of Regulations Effective or in the Making

�Dodd-Frank and European Markets Infrastructure Regulation (EMIR)

�Financial Counterparties which includes insurers, reinsurers and fund structures

�Interest rate derivatives (fixed/floating interest rate swaps, basis swaps, forward rate agreements, overnight index swaps) captured

�New trade, novation, notional increase, maturity extension, (swaptions) physical exercise

�Use of central clearing with initial margin and variation margin

�Trade execution facility

�Reporting to a trade repository

�Check the adoption agenda for clearing

�Financial Transaction Tax could apply multiple times to a single trade (counterparties + laying off risk through inter-broker dealer)

6

ALM for Life Insurers, 18–19 Sepetember 2013AllianceBernstein.com

Reporting Templates for Solvency II Pillar 3: D1 – D6

�D1: line-item reporting of assets held for insurer

�D2: derivatives (trades and open positions)

�D3: comprehensive insurer report

�D4: look-through table (fund-of-funds)

�D5: securities financing

�D6: collateral

7

Trial-runs ahead of regulatory implementation are a must!

ALM for Life Insurers, 18–19 Sepetember 2013AllianceBernstein.com

Agenda

�Asset Allocation + Derivatives Overlay = Collateral

�Cleaning the Credit Support Annex

�Planning Liquidity with Potential Future Exposure

�High Performance Computation

�Operating Model: the Integrated Front-to-Back Office

8

ALM for Life Insurers, 18–19 Sepetember 2013AllianceBernstein.com

Valuation of SwapsCredit Support Annex Impacts Bootstrapping and Discounting

�Present Value of an interest rate swap receiving fixed rate F which trades at fixed rate M:

�Value = DV01 x (F – M) [you receive F where, if you traded today, you would receive M]

�DV01 = Σ day-count fraction (i) x discount factor(i) x notional(i) [i sums all future cash flows]

�Collateral dependent discounting triggers a multi-curve & multi-currency handling of a plain vanilla swap

�Market standard quotation for USD Libor 3M, EUR Euribor 3M, GBP Libor 6M discount with the

domestic overnight rate, USD US Fed Funds—EUR EONIA—GBP SONIA

�Dual-curve bootstrapping of market quotes solves for arbitrage-free forwards of the swap rate –project one yield curve, discount with another yield-curve.

� If CSA is not market standard, discount the projected forwards with a different discount curve, resulting

in a different fair value for the swap!

�Credit-risky collateral requires a credit spread to be applied to the discount curve

�Foreign currency collateral implies cross-currency bootstrapping, incorporating cross-currency basis

�Choice of collateral currency in multi-currency CSA further complicates valuation

� the “cheapest-to-deliver” currency on a forward basis in a rough approximation ignoring

optionality

9

ALM for Life Insurers, 18–19 Sepetember 2013AllianceBernstein.com

Swap PricerSample Trading Screen for a Swap

10

© Thomson Reuters Eikon

ALM for Life Insurers, 18–19 Sepetember 2013AllianceBernstein.com

CSA-dependent Valuation MattersTrading and Balance Sheet, Re-couponing, Novation, Collateral…

�Trading with broker-specific CSA

�Forward pricing or quotation — quoting a cash settlement on maturity is now

standard in the swaptions market: choose your own discounting

�But we still need essential agreement on amount of collateral to post or receive

�Efficiently comparing CSA-dependent broker quotes requires advanced software

�Clean the book of legacy positions with re-couponing or novation to a cash CSA or to a different broker

�Settlement at mark-to-market for re-couponing depends on “dirty” CSA

�Transfer price and top-up payments to novate swaps between brokers, require

pricing against at least two or preferably all three CSAs

�Third-party trade compression services for detecting novation opportunities over

multiple counterparties while maintaining confidentiality (TriOptima)

�Requirement to use Swap trade Execution Facility forthcoming

11

ALM for Life Insurers, 18–19 Sepetember 2013AllianceBernstein.com

Pricers and Tri-party ValuationTools and Investment Operations

�Pricing toolkits and market data

�Derivatives toolkits FiNCAD F3, Quantifi, SciComp, SuperDerivatives, NumeriX,

Murex … with multi-curve discounting

�Market data vendors Bloomberg, Thomson Reuters Eikon, SuperDerivatives…

�Inter-broker dealers seeing significant derivatives flow may be the most reliable market data sources: ICAP, Tullett Prebon, Cantor Fitzgerald …

�Tri-party valuation with escalation for discrepancies – Unless you agree in valuation,

you cannot agree on collateral to post or receive

�Insurer or asset manager

�Counterparty (investment bank)

�Custodian

�Independent valuation services (SuperDerivatives, Bloomberg, mark-it)

12

ALM for Life Insurers, 18–19 Sepetember 2013AllianceBernstein.com

Agenda

�Asset Allocation + Derivatives Overlay = Collateral

�Cleaning the Credit Support Annex

�Planning Liquidity with Potential Future Exposure

�High Performance Computation

�Operating Model: the Integrated Front-to-Back Office

13

ALM for Life Insurers, 18–19 Sepetember 2013AllianceBernstein.com

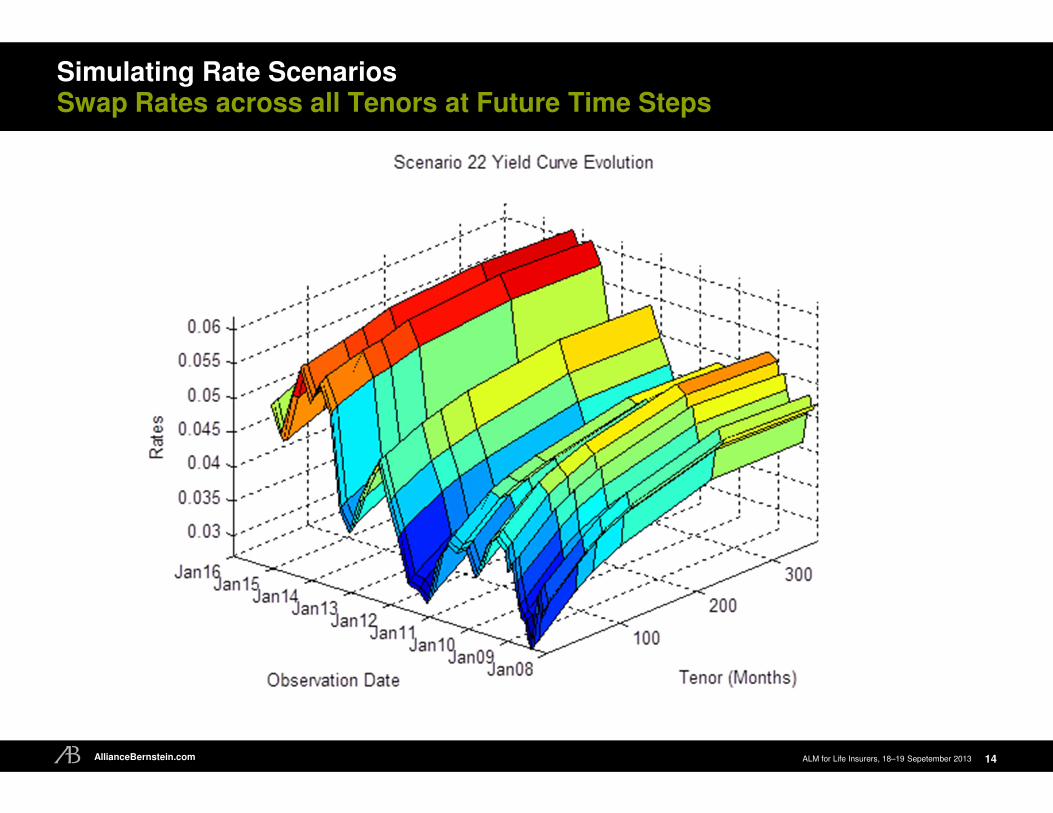

Simulating Rate ScenariosSwap Rates across all Tenors at Future Time Steps

14

ALM for Life Insurers, 18–19 Sepetember 2013AllianceBernstein.com

Mark-to-Market of Each Swap at Every Step for a Scenario

15

ALM for Life Insurers, 18–19 Sepetember 2013AllianceBernstein.com

Mark-to-Market of Entire Swap Portfolio for Each Scenario

16

ALM for Life Insurers, 18–19 Sepetember 2013AllianceBernstein.com

Portfolio Exposure Across Scenarios indicates Potential Liquidity Sink

17

�Potential Future Exposure (PFE)

the maximum expected counterparty exposure or collateral

requirement within a specified high

level of confidence

�Expected Positive Exposure (EPE) the Expected or average Exposure up

to a given future date t.

�Credit Valuation Adjustment (CVA)

the adjustment to the price of a

derivative to take into account counterparty credit risk = Expected

Positive Exposure x Probability of

Default x Loss Given Default

ALM for Life Insurers, 18–19 Sepetember 2013AllianceBernstein.com

Agenda

�Asset Allocation + Derivatives Overlay = Collateral

�Cleaning the Credit Support Annex

�Planning Liquidity with Potential Future Exposure

�High Performance Computation

�Operating Model: the Integrated Front-to-Back Office

18

ALM for Life Insurers, 18–19 Sepetember 2013AllianceBernstein.com

High-Performance Computing – What Are the options?

19

�Multi-core for embarrassingly parallel tasks

�NVIDIA Tesla, Kepler, Maxwell …

�Programming models OpenCL, OpenACC, OpenMP, CUDA

�Data bandwidth considerations, hosting and moving of the data

�Libraries (NAG, NVIDIA, MathWorks) and domain specific languages (SciComp)

�Dataflow Simulation on Field-Programmable Gate Arrays

�Standardised and portable OpenCL

�MaxCompiler high-level programming language for dataflow computing

�Clouds

�On-demand bursting fills punctual requirements

�Outsourced, low capital cost

�Hosting the data in the cloud?

ALM for Life Insurers, 18–19 Sepetember 2013AllianceBernstein.com

NVIDIA GPU Computing: Graphical Processing Units

20

ALM for Life Insurers, 18–19 Sepetember 2013AllianceBernstein.com

VERY MANY Computational Cores on a Chip

21

ALM for Life Insurers, 18–19 Sepetember 2013AllianceBernstein.com

Data-Flow Computation on FPGAPipeline Programming Generates Fresh Simulations @ 300 MHz

22

ALM for Life Insurers, 18–19 Sepetember 2013AllianceBernstein.com

Agenda

�Asset Allocation + Derivatives Overlay = Collateral

�Cleaning the Credit Support Annex

�Planning Liquidity with Potential Future Exposure

�High Performance Computation

�Operating Model: the Integrated Front-to-Back Office

23

ALM for Life Insurers, 18–19 Sepetember 2013AllianceBernstein.com

New Operating Model for Investment Management

24

�Front-office needs to understand collateral and liquidity consequences of its investment

decisions

�Back-office not just an operation task but crucial input into asset allocation, asset-liability management, hedging best practices, reporting and compliance

�Collateral and liquidity management a critical input into overall balance sheet and capital

management of bank, insurer, pension fund

�Product Pricing and Product Development in Banking, Insurance and Pensions require

accurate liquidity pricing and sound collateral practices

�Position monitoring and liquidity analytics need to upgrade so as to accurately report & plan collateral & liquidity

ALM for Life Insurers, 18–19 Sepetember 2013AllianceBernstein.com

Read Up and Connect with Colleagues

25

�Clear Path Analysis study: “Collateral Management for Institutional Investors”

�https://www.clearpathanalysis.com/product/104-cmli-2014/

�International Securities Services: “Collateral Management”

�http://www.iss-mag.com/collateral-management/iss-magazine-discusses-

collateral-management-wi

ALM for Life Insurers, 18–19 Sepetember 2013AllianceBernstein.com

Disclaimer

�This information is issued by AllianceBernstein Limited, 50 Berkeley Street, London W1J 8HA,

a company registered in England under company number 2551144. AllianceBernstein Limited is authorised and regulated in the UK by the Financial Conduct Authority (FCA – Reference

Number 147956). This information is directed at Professional Clients only. It is provided for informational purposes only and is not intended to be an offer or solicitation, or the basis for any

contract to purchase or sell any security, product or other instrument, or for AllianceBernstein to

enter into or arrange any type of transaction as a consequence of any information contained

herein. The views and opinions expressed in this document are based on AllianceBernstein's

internal forecasts and should not be relied upon as an indication of future market performance. Past performance is no guarantee of future returns. This information is not intended for public

use.

�© 2013 AllianceBernstein

26

ALM for Life Insurers, 18–19 Sepetember 2013AllianceBernstein.com

A WORD ABOUT RISK

� Market Risk: The market values of the investments may rise and fall from day to day, so investments may

lose value.

� Interest Rate Risk: Bonds may lose value if interest rates rise or fall—long-duration bonds tend to rise and fall

more than short-duration bonds.

� Credit Risk: A bond’s credit rating reflects the issuer’s ability to make timely payments of interest or capital—

the lower the rating, the higher the risk of default. If the issuer’s financial strength deteriorates, the issuer’s

rating may be lowered and the bond’s value may decline.

� Allocation Risk: Allocating to different types of assets may have a large impact on returns if one of these

asset classes significantly underperforms the others.

� Foreign Risk: Investing in overseas assets may be more volatile because of political, regulatory, market and

economic uncertainties associated with them. These risks are magnified in assets of emerging or developing

markets.

� Currency Risk: currency fluctuations may have a large impact on returns and the value of an investment may

be negatively affected when translated into the currency in which the initial investment was made.

� Capitalization Size Risk (Small/Mid): Holdings in smaller companies are often more volatile than holdings in

larger ones.

� © 2013 AllianceBernstein

27