Embed Size (px)

Citation preview

1

RECENT TRENDS IN THE GLOBAL ECONOMY AND THE NEAR TERM OUTLOOK

Andris Strazds

Adviser

29.04.2015

Global Economy

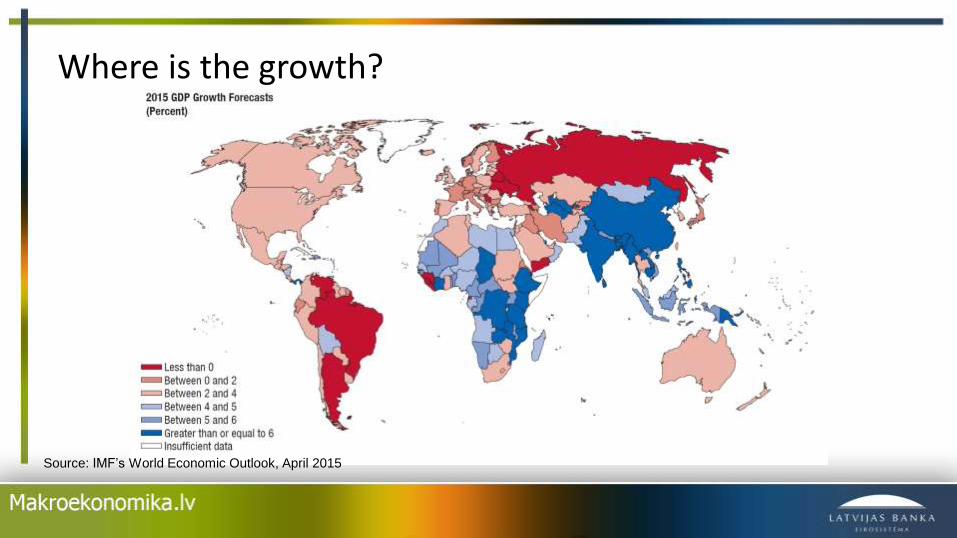

Source: IMF’s World Economic Outlook, April 2015

Where is the growth?

Commodity and oil prices have declined since mid-2014

Source: IMF’s World Economic Outlook, April 2015

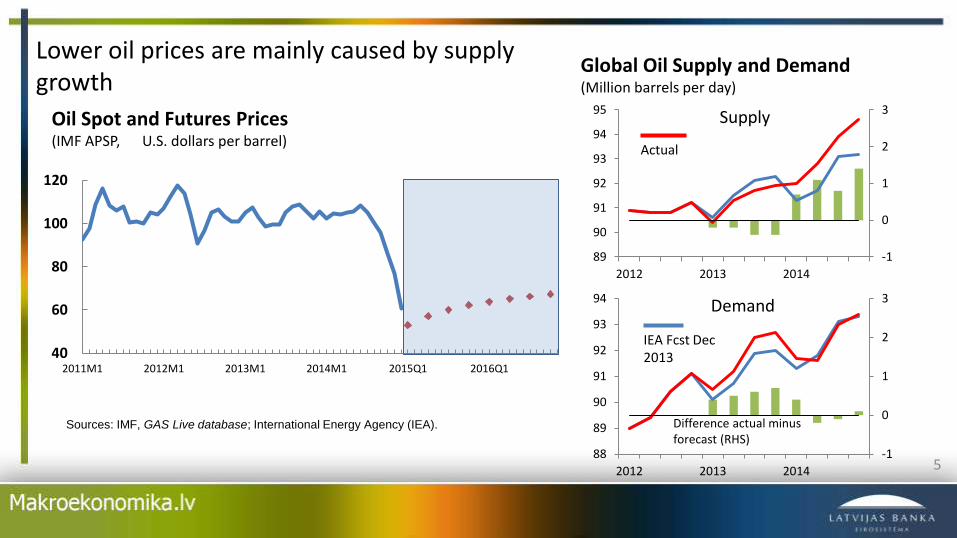

Oil Spot and Futures Prices(IMF APSP, U.S. dollars per barrel)

Lower oil prices are mainly caused by supplygrowth

5

40

60

80

100

120

2011M1 2012M1 2013M1 2014M1 2015Q1 2016Q1

Global Oil Supply and Demand(Million barrels per day)

Sources: IMF, GAS Live database; International Energy Agency (IEA).

-1

0

1

2

3

89

90

91

92

93

94

95

2012 2013 2014

Supply

Actual

-1

0

1

2

3

88

89

90

91

92

93

94

2012 2013 2014

Demand

IEA Fcst Dec 2013

Difference actual minus forecast (RHS)

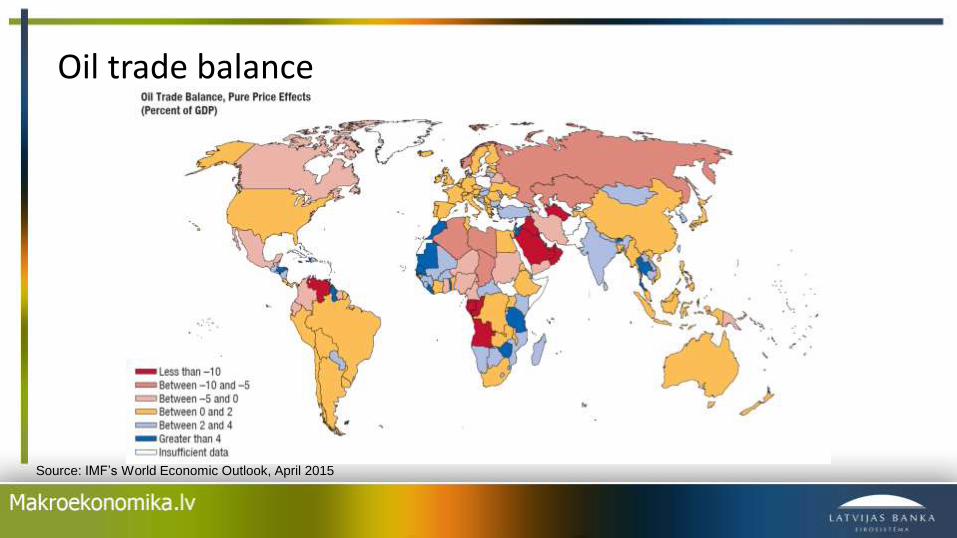

Oil trade balance

Source: IMF’s World Economic Outlook, April 2015

Source: IMF’s World Economic Outlook, April 2015

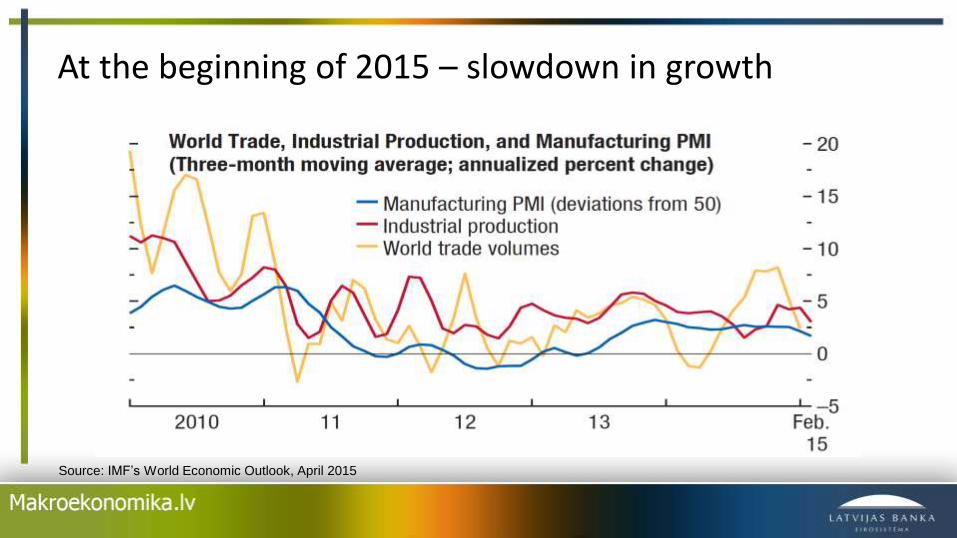

At the beginning of 2015 – slowdown in growth

Source: IMF’s World Economic Outlook, April 2015

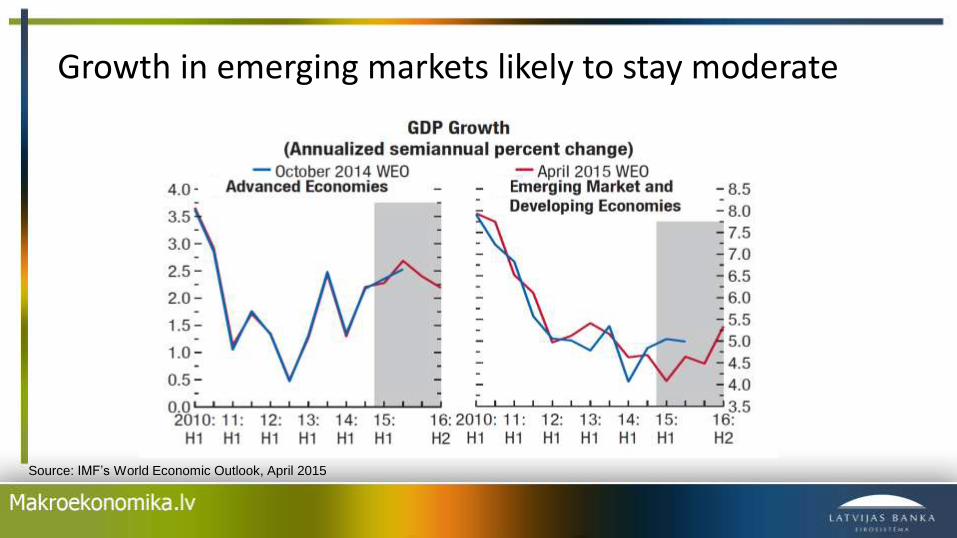

Growth in emerging markets likely to stay moderate

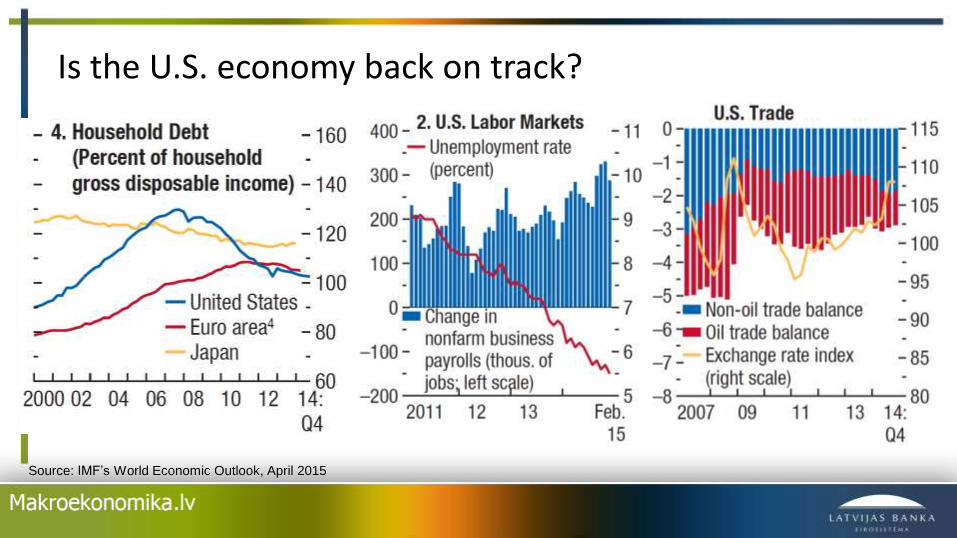

Is the U.S. economy back on track?

Source: IMF’s World Economic Outlook, April 2015

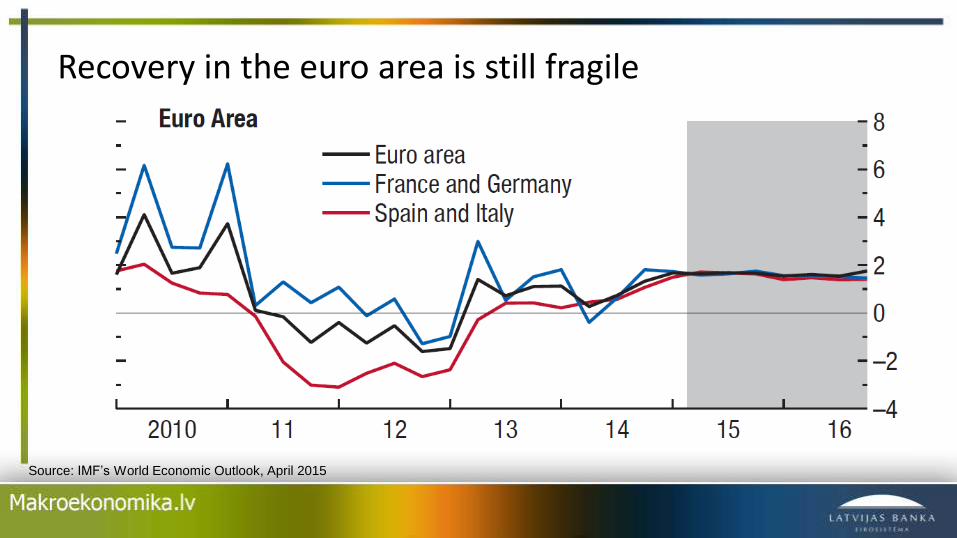

Recovery in the euro area is still fragile

Source: IMF’s World Economic Outlook, April 2015

Source: IMF’s World Economic Outlook, April 2015

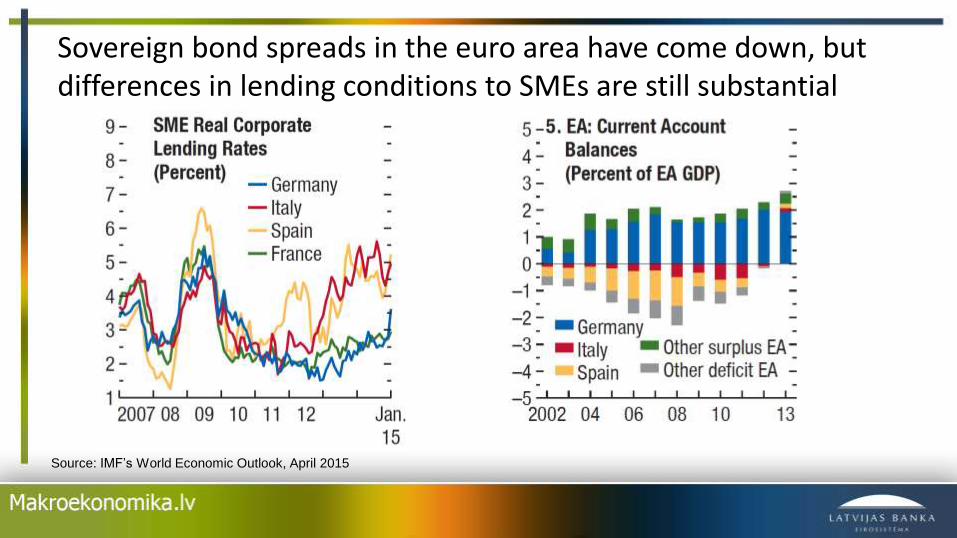

Sovereign bond spreads in the euro area have come down, but differences in lending conditions to SMEs are still substantial

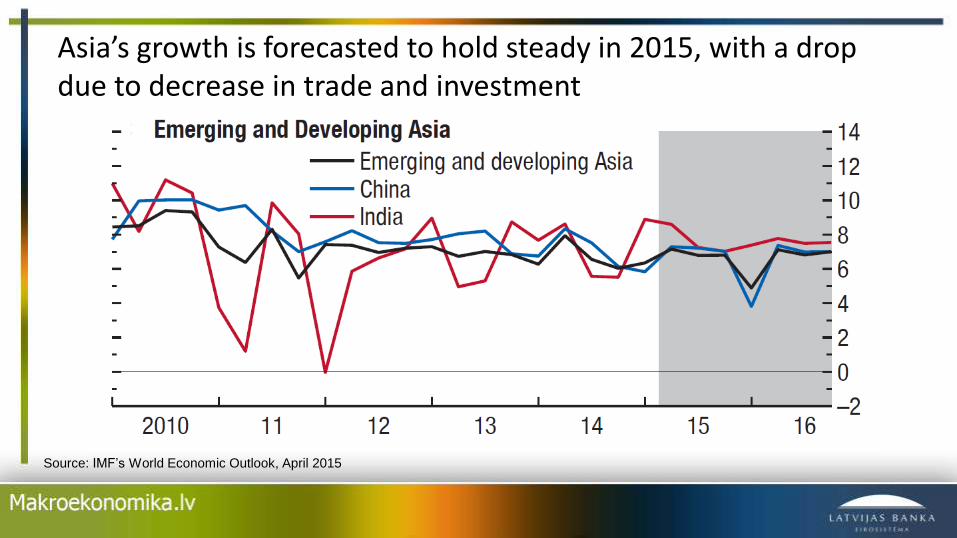

Asia’s growth is forecasted to hold steady in 2015, with a dropdue to decrease in trade and investment

Source: IMF’s World Economic Outlook, April 2015

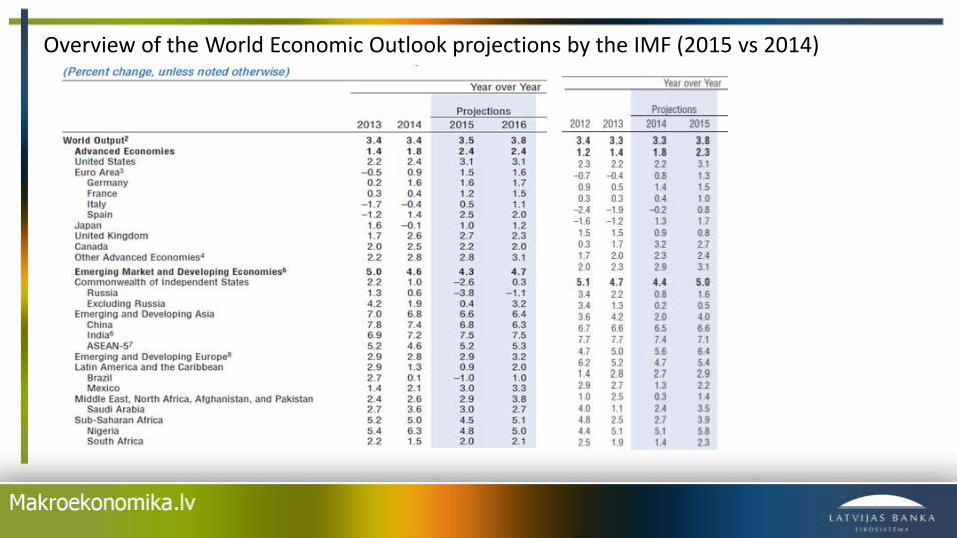

Overview of the World Economic Outlook projections by the IMF (2015 vs 2014)

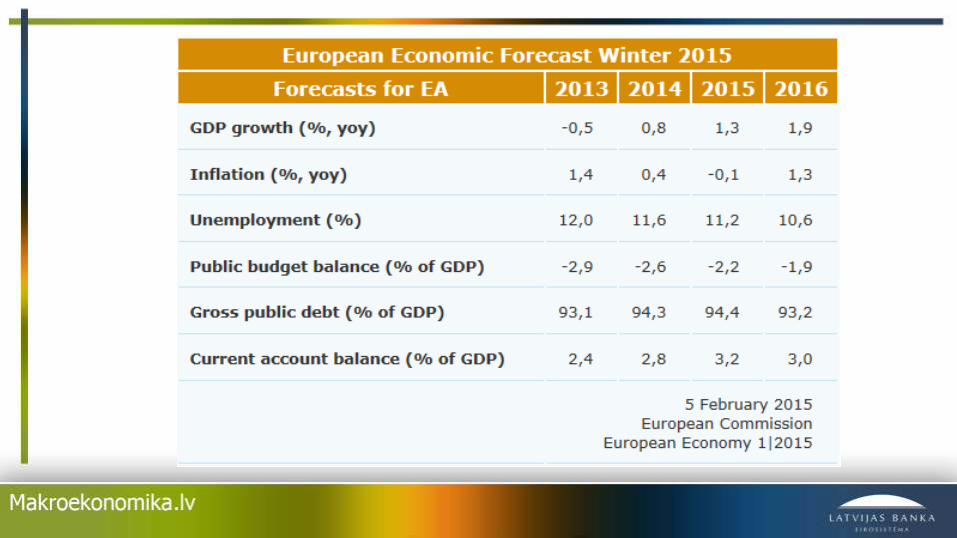

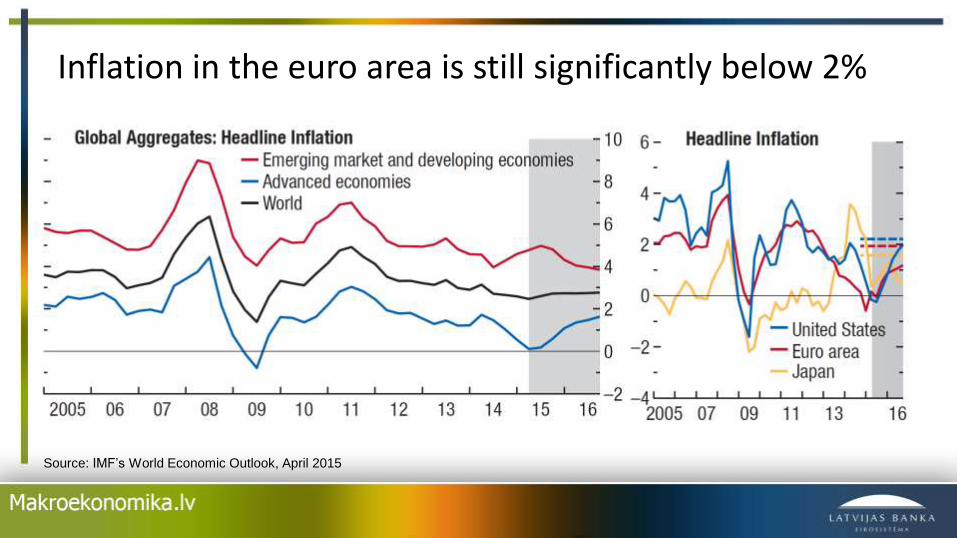

Inflation in the euro area is still significantly below 2%

Source: IMF’s World Economic Outlook, April 2015

16

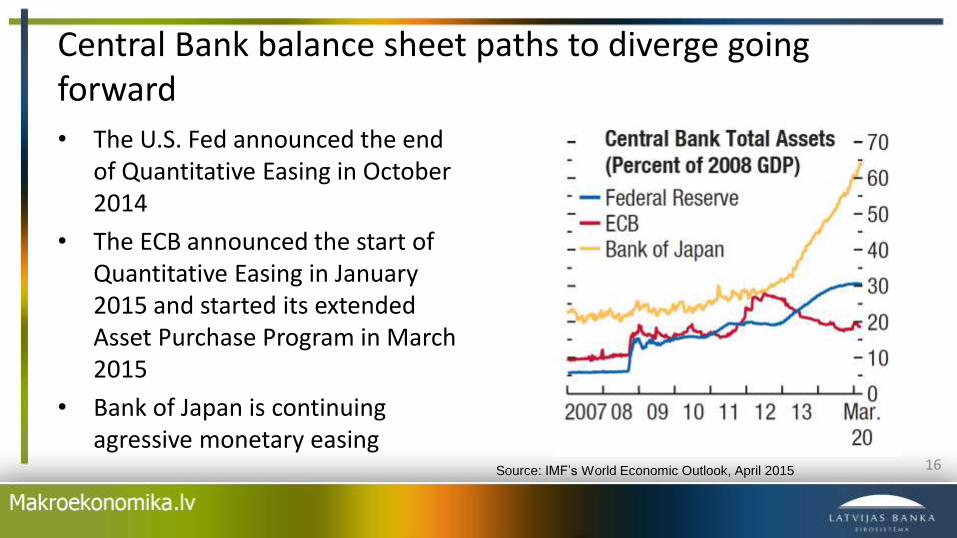

Central Bank balance sheet paths to diverge goingforward

• The U.S. Fed announced the endof Quantitative Easing in October2014

• The ECB announced the start ofQuantitative Easing in January2015 and started its extendedAsset Purchase Program in March2015

• Bank of Japan is continuingagressive monetary easing

Source: IMF’s World Economic Outlook, April 2015

17

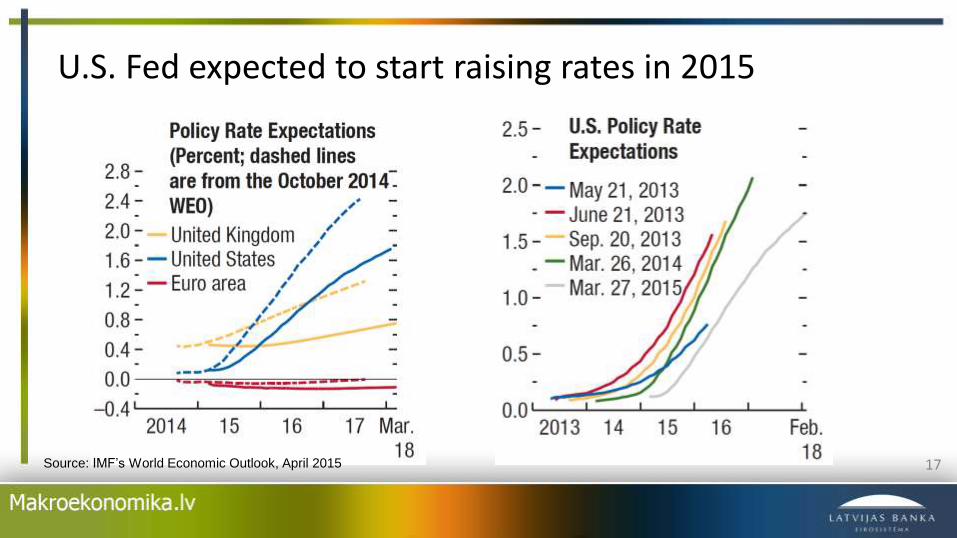

U.S. Fed expected to start raising rates in 2015

Source: IMF’s World Economic Outlook, April 2015

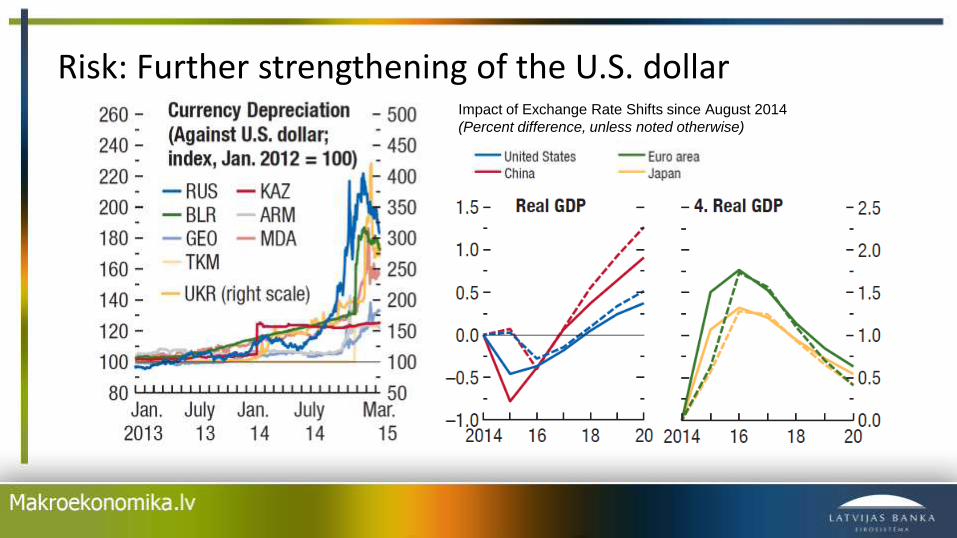

Risk: Further strengthening of the U.S. dollarImpact of Exchange Rate Shifts since August 2014

(Percent difference, unless noted otherwise)

Key near term risks going forward

• Geopolitical risks

• Risks from a financial market correction

• Protracted period of low inflation in the euro area

• Risk of stagnation and lower potential growth in a number ofadvanced economies

• Considerably slower growth in China

Policy recommendations

• Both continued support to demand and supply side policies needed

• Increased public investment in most current account surplus countries(other than China)

• (Continued) structural reforms in the (former) current account deficitcountries

• Macroprudential tools (such as loan-to-value, debt-service-to-incomeratios) to limit credit booms in a number of smaller advanced economies

Policy recommendations: Euro area

• Reestablish confidence in banks and improve financial intermediation inthe euro area

• Cost-effective active labor market policies, measures to lower the opportunity cost of employment, and better-targeted training programs

• Complete the single market in services, including a single digital market

• Make progress with free trade agreements

• More closely integrate energy platforms and policies

Fiscal Outlook

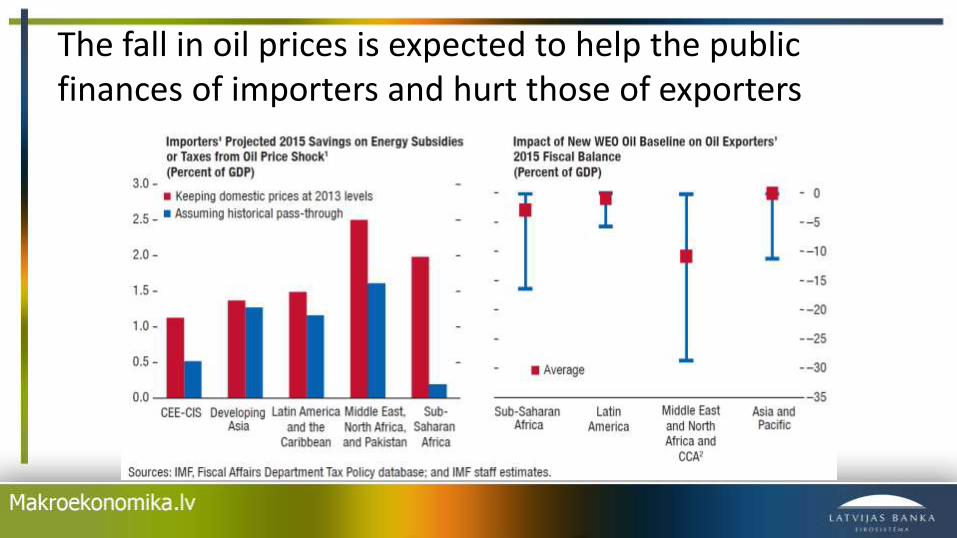

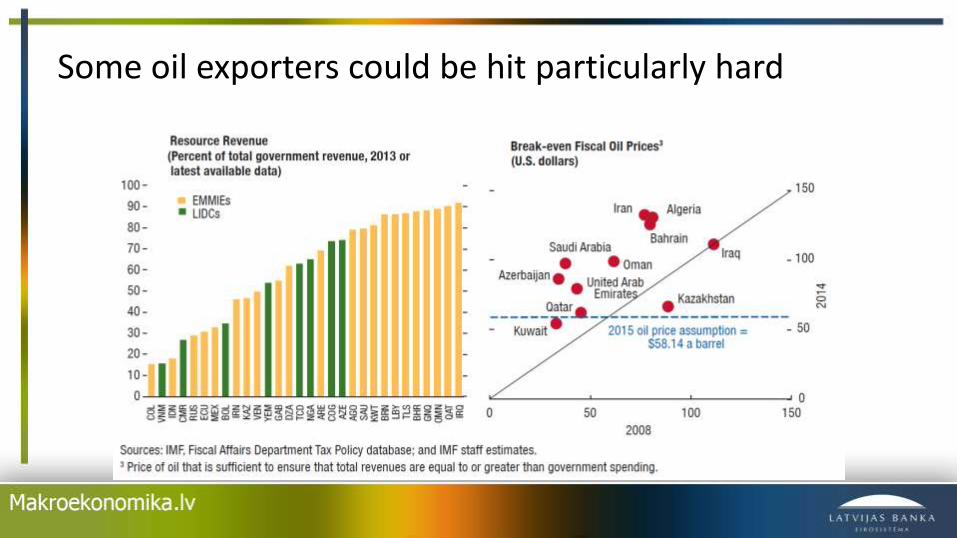

The fall in oil prices is expected to help the public finances of importers and hurt those of exporters

Some oil exporters could be hit particularly hard

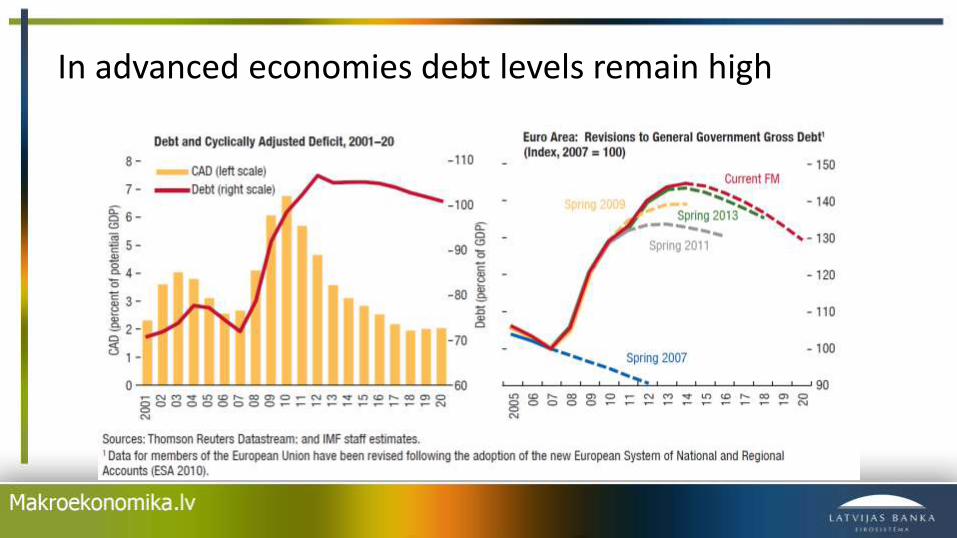

In advanced economies debt levels remain high

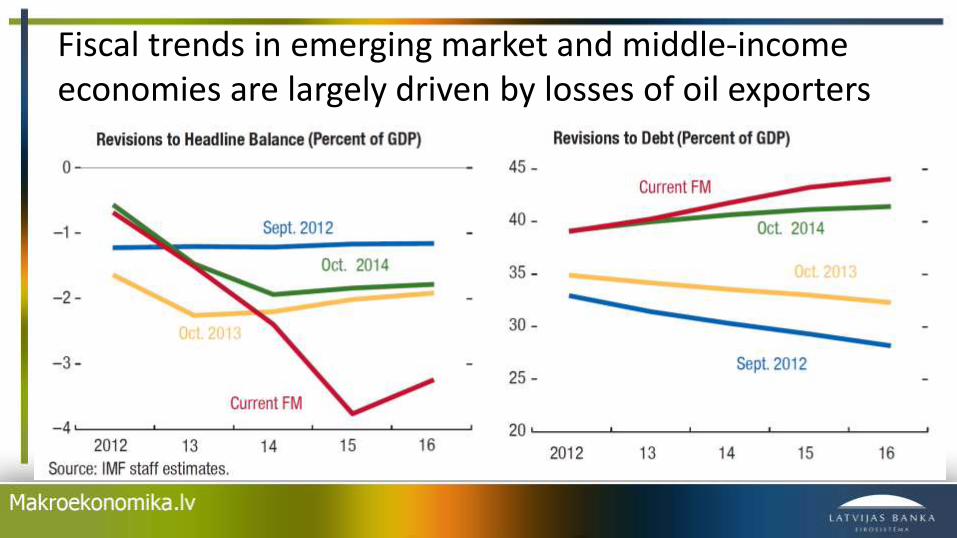

Fiscal trends in emerging market and middle-incomeeconomies are largely driven by losses of oil exporters

Fiscal policy can play a supportive role

Triple solution

• Monetary stimulus

• Structural reforms

• Supported by fiscal policy– Use fiscal policy flexibly to support growth

– Seize the opportunity created by falling oil prices

– Strengthen institutional frameworks for managingfiscal policy

Triple threat

• Low growth

• Low inflation

• High debt

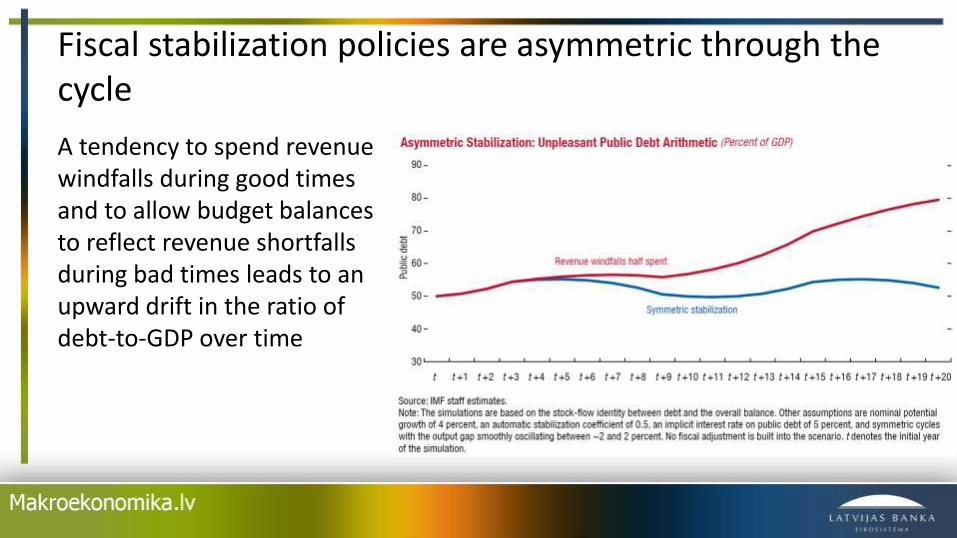

Fiscal stabilization policies are asymmetric through the cycle

A tendency to spend revenue windfalls during good times and to allow budget balances to reflect revenue shortfalls during bad times leads to an upward drift in the ratio of debt-to-GDP over time

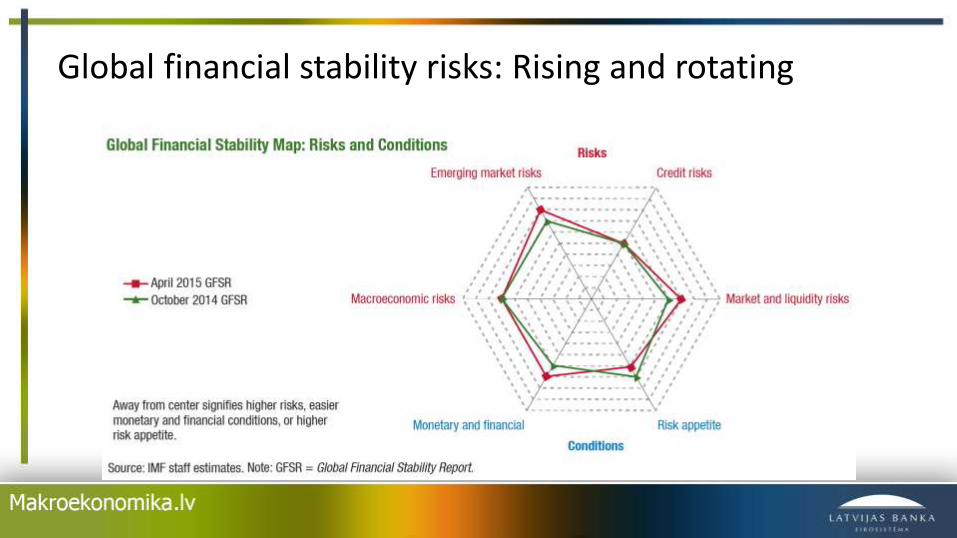

Financial Stability

Global financial stability risks: Rising and rotating

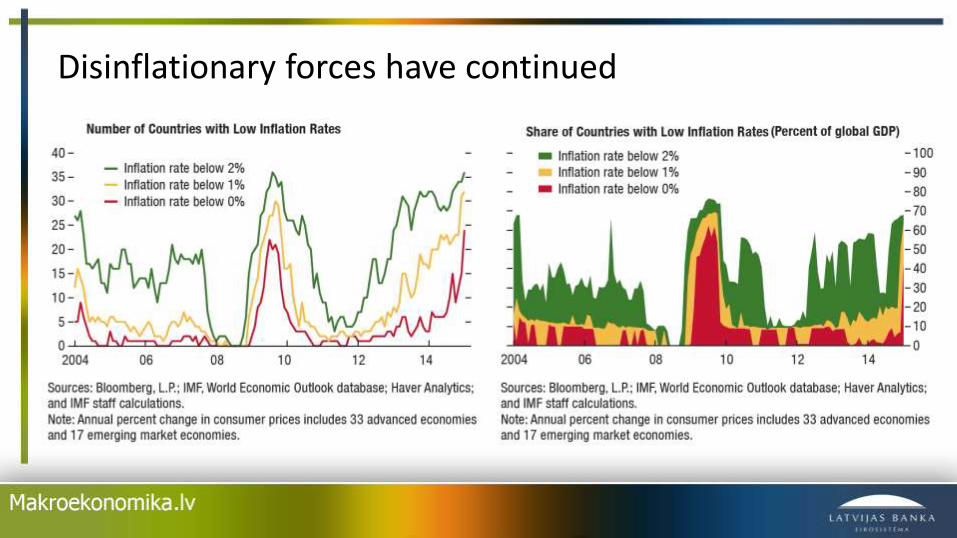

Disinflationary forces have continued

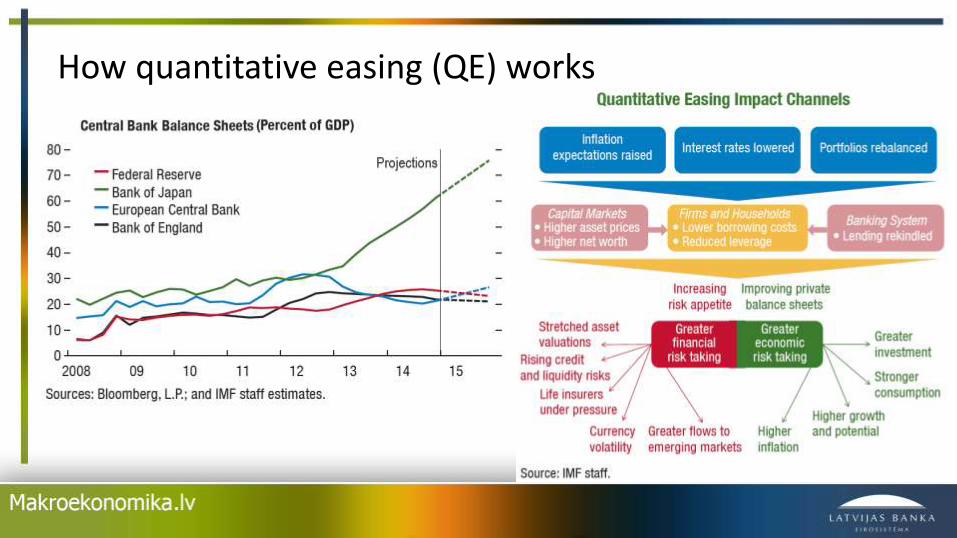

How quantitative easing (QE) works

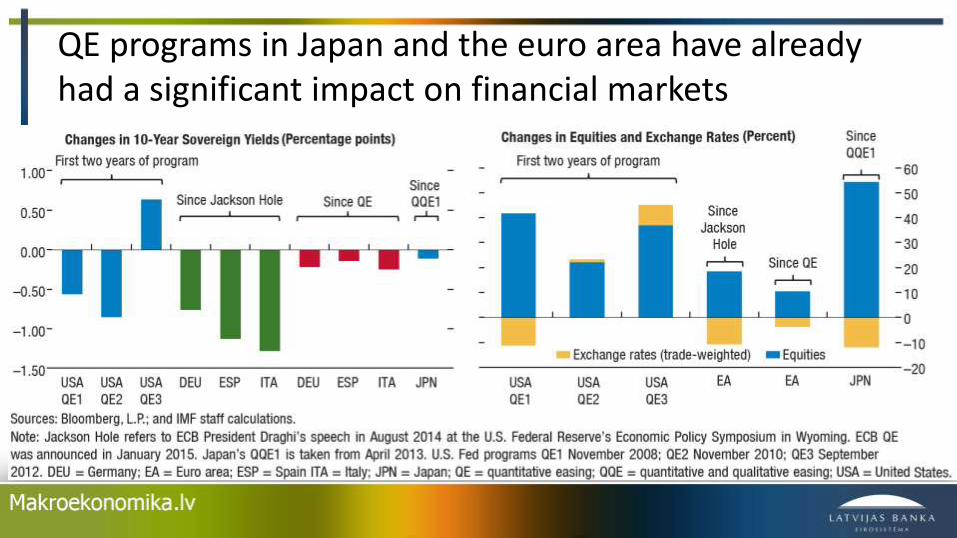

QE programs in Japan and the euro area have already had a significant impact on financial markets

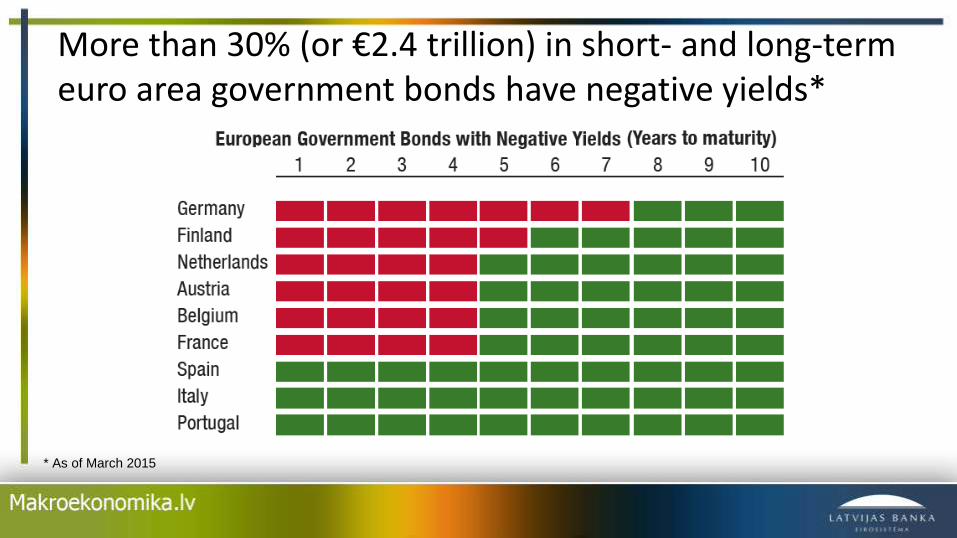

More than 30% (or €2.4 trillion) in short- and long-term euro area government bonds have negative yields*

* As of March 2015

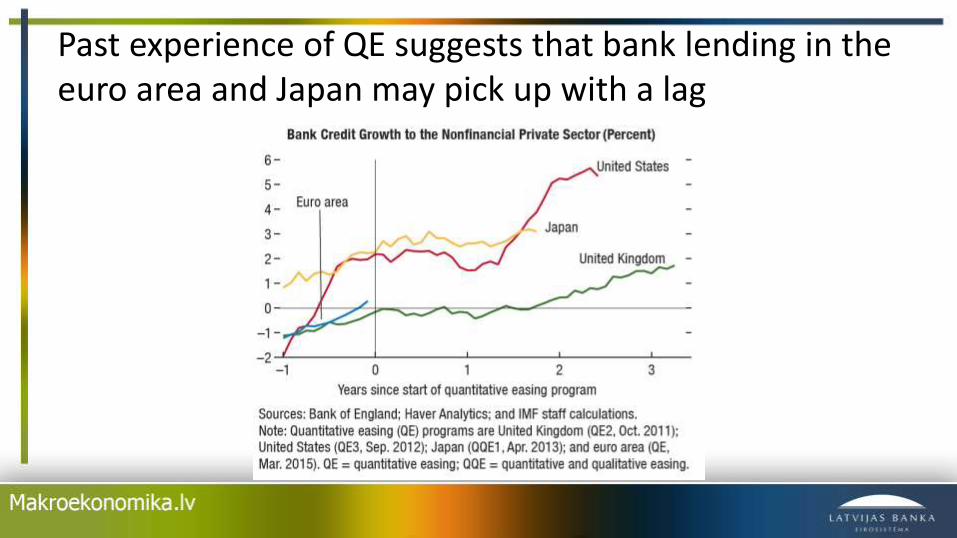

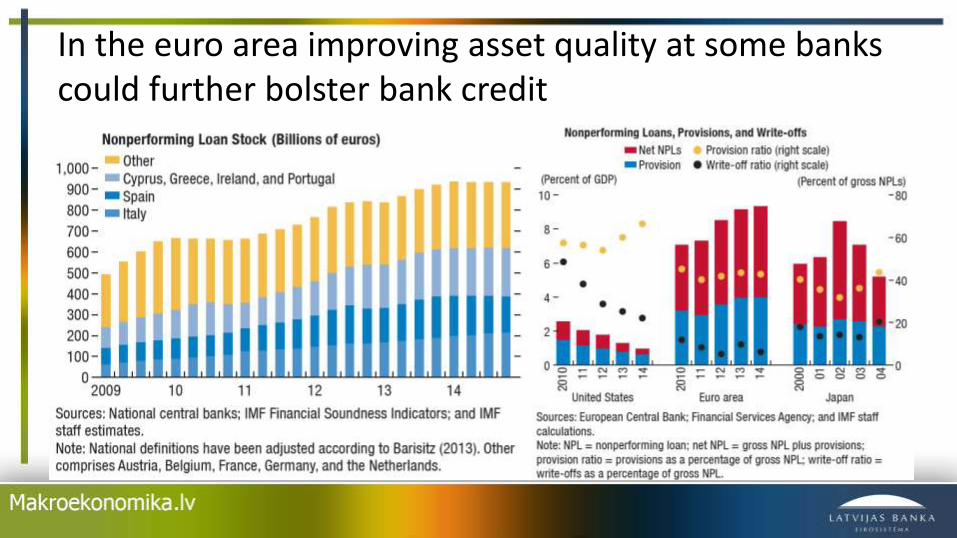

Past experience of QE suggests that bank lending in the euro area and Japan may pick up with a lag

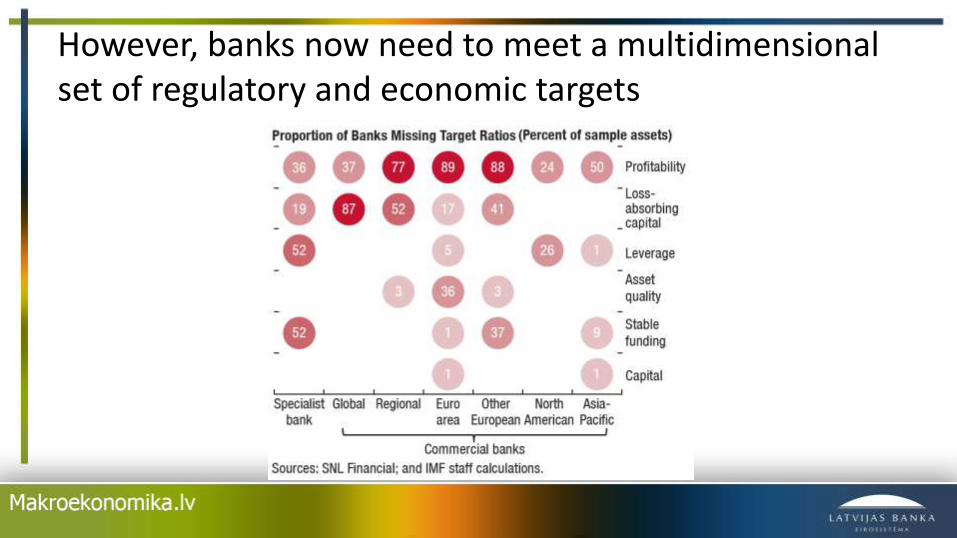

However, banks now need to meet a multidimensional set of regulatory and economic targets

In the euro area improving asset quality at some banks could further bolster bank credit

38

THANK YOU!

Questions and Answers