Embed Size (px)

Citation preview

INVESTOR GOVERNANCE

REVISITED:

The risk and reward of democracy in

institutional investment decision-

making

1

SAFA Conference

Colin Habberton

UCT GSB, Cape Town

16 January 2015

2

My thoughts on the

conference…

3

Framing Statement

4

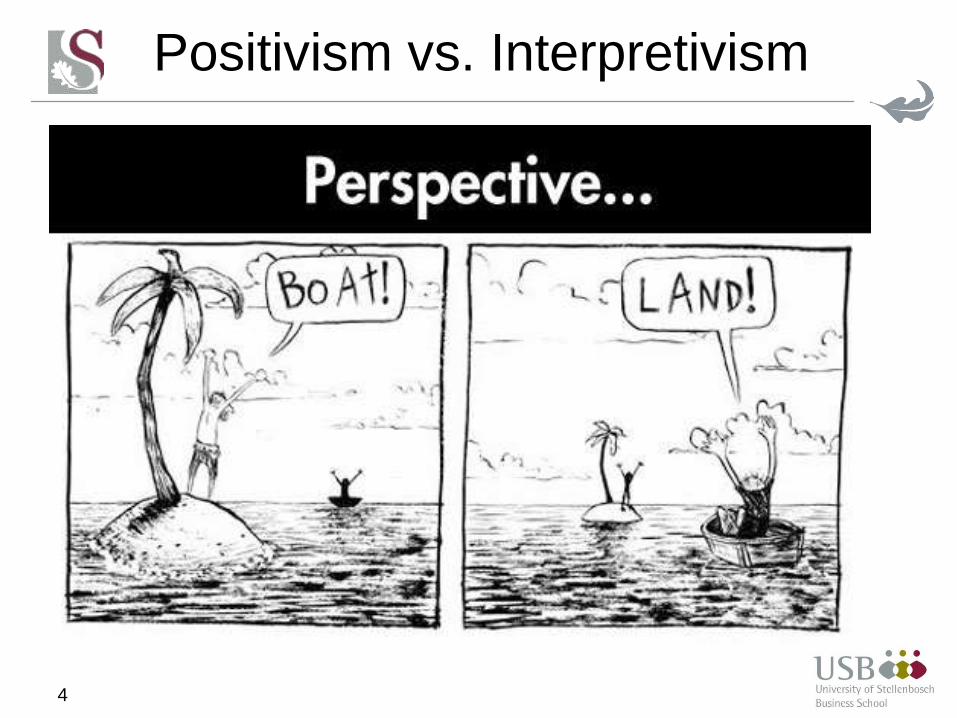

Positivism vs. Interpretivism

5

Democracy

“If liberty and equality, as is thought by

some, are chiefly to be found in democracy,

they will be best attained when all persons

alike share in the government to the

utmost.”

Aristotle

6

Introduction

• The paper investigates whether institutional

investors consider the interests and opinions their

individual capital contributors in their decision-

making.

• Institutional investors dominate the investment

activity within financial markets (Blume & Keim 2012;

OECD, 2014; ASISA, 2013).

• Predominant focus of investing is the risk-adjusted

maximisation of financial return.

• ‘Wicked’ problems – poverty, unemployment,

climate change – exist and ultimately, impact on risk

and return.

• Recent scandals highlight disconnect between

Research context

• The emergence of investment principles known as

Responsible Investing (e.g. UNPRI, CRISA)

• Assessment of the integration of ‘ESG’ criteria into

investment practices is the differentiator.

• ‘Active’ ownership (i.e. participation) is a common

feature of Responsible Investing processes.

• Disclosure and reporting (i.e. transparency) are

also recommended and increasingly required.

• The ‘G’ in particular the notion of stakeholder

governance offers a interesting lens for

investigation.

• South Africa was used as a focus.7

8

Research Questions

• Is good governance applied and practiced by

institutional investors in taking responsibility for

investment decisions on behalf of stakeholder

communities?

• Should individual contributors participate in

decision-making processes, holding institutional

investors as their agents accountable to their

interests?

• Should institutional investors be more proactive in

providing access to information, education and

opportunity to participate in decision-making?

• What are the risks and rewards for a greater

degree of democracy in investment decision-

Research methodology

• The analysis of the existing regulatory and

normative frameworks forms the theoretical

foundation of the paper.

• Secondary literature research refined the

conceptual framework to inform the selection of

population, sample frame for interviews.

• The consequent understanding of the theory and

industry information was integrated into the

design and execution of semi-structured

interviews with industry experts.

9

10

Institutional Investors

• Blume, M. E. & Keim, D. B. 2012. Institutional Investors and

Stock Market Liquidity: Trends and Relationships. SSRN

• Gifford, E.J.M. 2010. Effective Shareholder Engagement: The

Factors that Contribute to Shareholder Salience. Journal of

Business Ethics. 92:79-97..

• David, P., Kochhar, R. & Levitas, E. 1998. The effect of

institutional investors on the level and mix of CEO compensation.

Academy of Management Journal, 41(2):200-208.

• Gillian, L.S. and Starks, L.T. 2002. Institutional Investors,

Corporate Ownership and Corporate Governance. Global

Perspectives: Discussion Paper 2002/9. WIDER: United Nations

University.

• Piotroski, J. D. 2004. The Influence of Analysts, Institutional

Investors, and Insiders on the Incorporation of Market, Industry,

and Firm-Specific Information into Stock Prices. The Accounting

Review, 79(4):1119-1151.

• Victoravich, L. M., Xu, P. & Gan, H. 2013. Institutional ownership

and executive compensation: Evidence from US banks during

Literature

11

Institutional Structure

• Clarke, G.L. 2000. The functional and spatial structure of the

investment management industry. Geoforum, 31(1):71-86.

• Vitali, S, Glattfelder, J.B. & Battiston. 2011. The network of global

corporate control. PLoS ONE. 6(10).

Responsible Investing in South Africa

• IODSA. 2013. CRISA disclosure by institutional investors and

their service providers. Sandton: IODSA

• Van der Ahee, G & Schulschenk, J. 2013. The State of RI in

South Africa:. Climate Change and Sustainability Services: E&Y

Africa.

• Viviers, S., Eccles, N.S., de Jong, D., Bosch, J.K., Smit, E. v.d.M

& Buijs, A. 2008. Responsible investing in South Africa – drivers,

barriers and enablers. Investment Analysts Journal. 69(1):3-16.

• Viviers, S. & Eccles, N.S. 2012. 35 years of SRI research –

General trends over time. SA Journal of Business Management.

43(4):15-31.

• Viviers, S. 2014. Motives, modus operandi and sources of

Literature

Institutional Investor dominance

12

• Over 67% of market capitalisation in the

USA

• Own 73% of the US’s 1000 largest

companies

• 33 OECD countries average is 40%

ownership

(Source: OECD, 2014)

13

• Increasing support for normative

frameworks

• UN Principles for Responsible Investment

(PRI)

• CDP & Integrated Reporting <IR> Initiatives

Growth of Responsible Investing

(Source: UNPRI, 2014)

US$45tn

AuM

1300+

Signatorie

s

Principles for Responsible

Investing

14

(Source: UNPRI, 2014)

15

“All retirement funds, long term insurers, collective

investment scheme (CIS) management companies

are treated as institutional investors…” (SARB, 2013)

• Asset Owners

• Public Sector: GEPF, Transnet, Eskom,

parastatals

• Private Sector: Over 5000 funds registered

FSB

• Asset Managers

• Public Sector: Public Investment Corporation

• Over 200 Retirement Funds & CIS

companies

Institutional Investors in South Africa

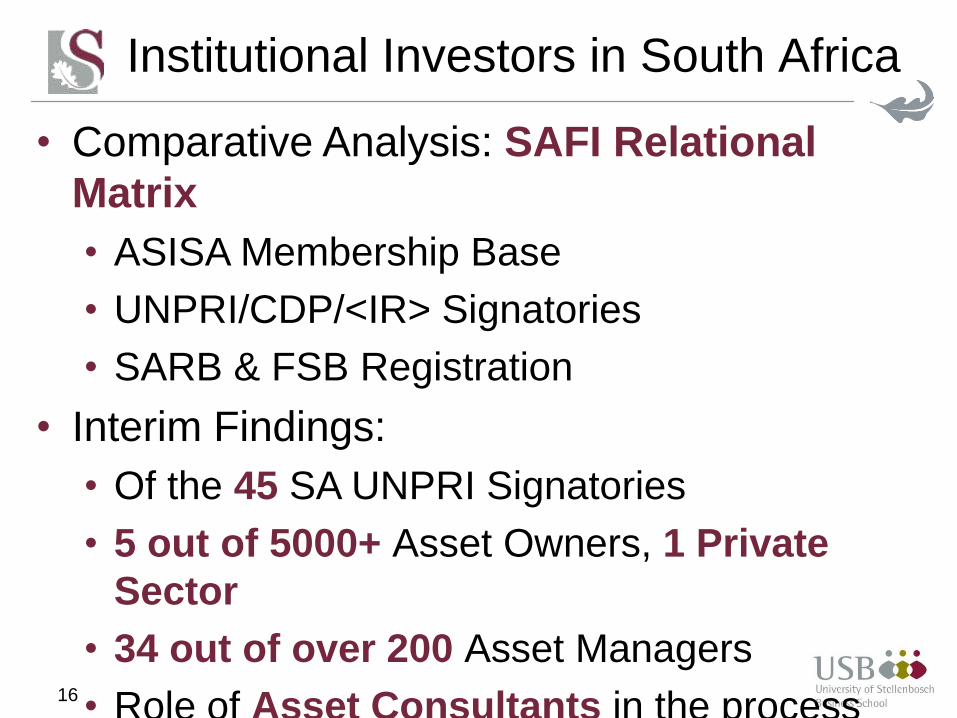

16

• Comparative Analysis: SAFI Relational

Matrix

• ASISA Membership Base

• UNPRI/CDP/<IR> Signatories

• SARB & FSB Registration

• Interim Findings:

• Of the 45 SA UNPRI Signatories

• 5 out of 5000+ Asset Owners, 1 Private

Sector

• 34 out of over 200 Asset Managers

• Role of Asset Consultants in the process

Institutional Investors in South Africa

17

• SA one of the leading countries on the

African continent in terms of

governance (Mo Ibrahim Foundation,

2013)

• King Reports & Institute of Directors SA

• Influencing business and legal practice

• King III – Sustainability & Stakeholders“…characterised by the ethical values of responsibility,

accountability, fairness and transparency...”

“…how a company has, both positively or negatively,

impacted on the economic life of the community in

which it operated…” (IODSA, 2009).

Governance in South Africa

18

Pension Funds: Stakeholder System

(Source: Clarke, 2000)

19

• Role of Professional Investor

• Fiduciary responsibilities as an agent

• Accountability of pension fund trustees

• Skill vs. experience vs. representivity

• Appointed by wide range of

Stakeholders

• Transparency of decision-making

process

• Investor participation & inclusion

• Need for transparency & engagement

• Investor education & responsibility

Observations on Investor Governance

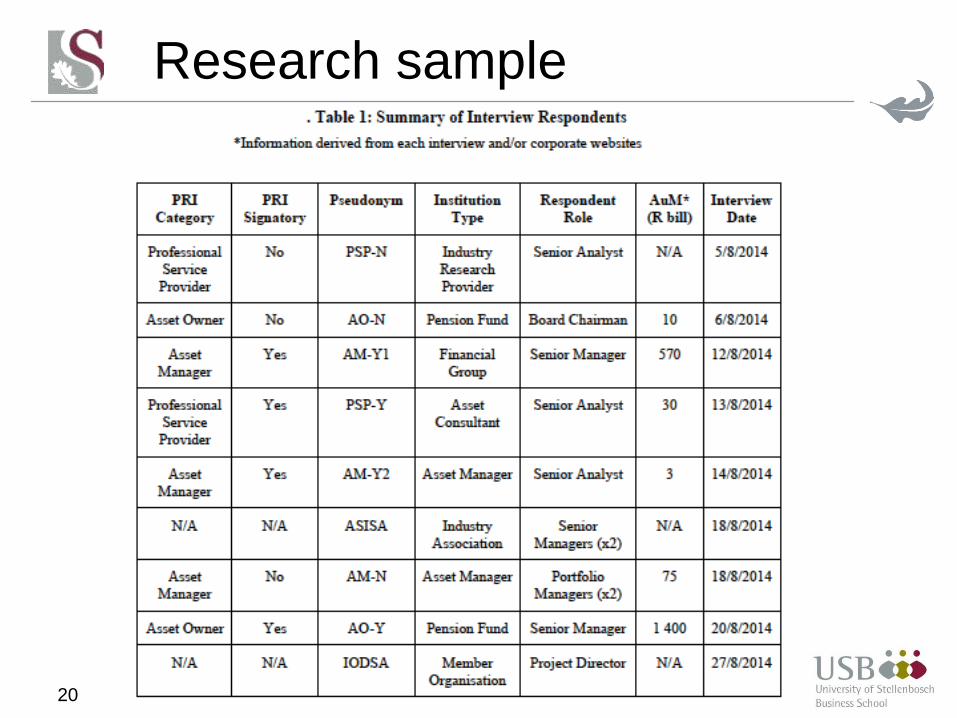

Research sample

20

21

• Institutional PRI/CRISA participation

• Perception of institutional ‘window-dressing’

• Unanimous acceptance of importance of ESG

• Investment decision-making

• Delegation of decision-making to skilled

specialists

• Influence of unregulated asset consultants

• Fee structures heavily geared towards

benchmarks

• Responsibility

• Different perspectives on definition of

responsibility

• Maximisation of return overriding intent

Findings: Institutional Investor

Interviews

22

• Risks

• Resistance to concept by the professionals

• Requires additional resources and time

• Potential disregard for analysis and depth

• Inefficient, chaotic driven by sentiment

• Lack of investor literacy and prudence

• Rewards

• Increase institutional investor accountability

to ownership responsibilities

• Highlight the importance of ESG decision-

making

• Increased demand may enhance choice

Findings: Individual Investor

Participation

23

• Investment industry characterised by profit driven

strategic and systemic constraints.

• Limited access to information, transparency in

investment processes beyond professionals is

apparent.

• Role of asset consultants and their influence

over decision-making is admittedly significant.

(Research?)

• Investment mandates and fee structures are

drivers of professional investor activity (Bogle,

Ellis)

• Institutional investors may be pushed to assume

more responsibility and accountability for their

Conclusions & research opportunities

24

Final Word

INVESTOR GOVERNANCE

REVISITED

25

Colin Habberton

@relatomics