Embed Size (px)

Citation preview

________________________________________________

PERSONAL FINANCIAL PLAN

FOR

JAMES, JILL AND JANE.

(PLAN DATED 2008)

________________________________________________

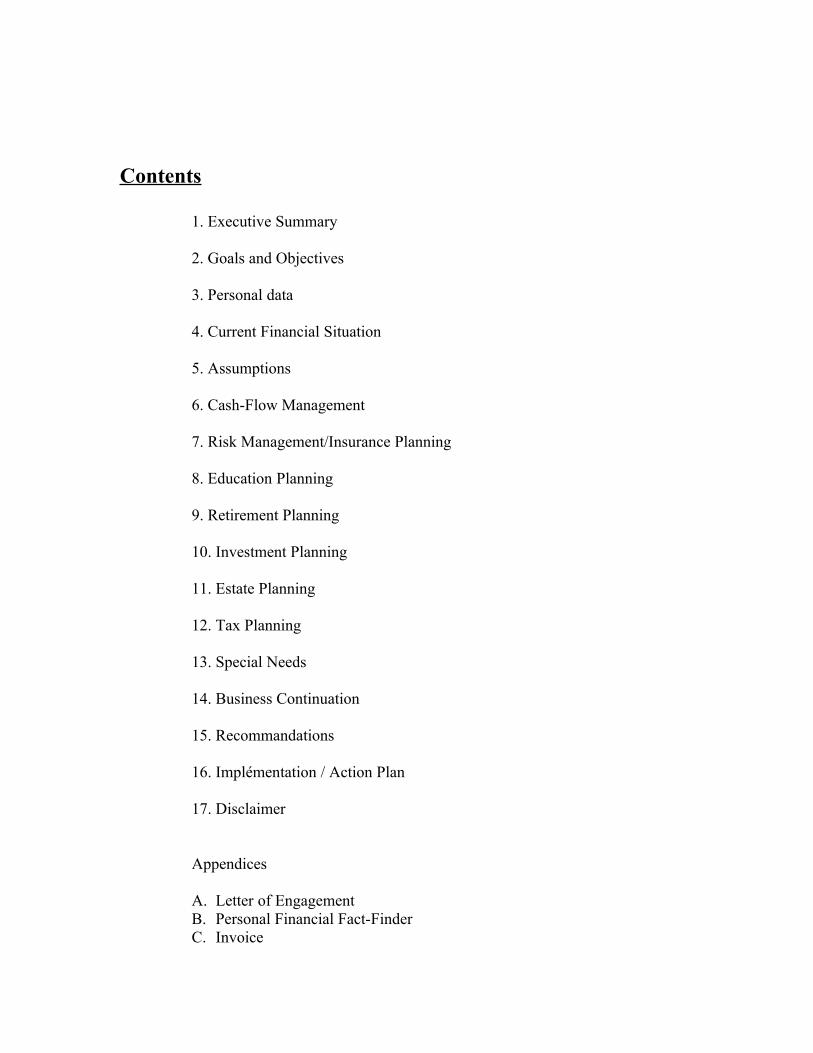

Contents

1. Executive Summary

2. Goals and Objectives

3. Personal data

4. Current Financial Situation

5. Assumptions

6. Cash-Flow Management

7. Risk Management/Insurance Planning

8. Education Planning

9. Retirement Planning 10. Investment Planning

11. Estate Planning

12. Tax Planning

13. Special Needs

14. Business Continuation

15. Recommandations

16. Implémentation / Action Plan

17. Disclaimer

Appendices

A. Letter of EngagementB. Personal Financial Fact-FinderC. Invoice

1. EXECUTIVE SUMMARY

1.1 Cash Flow Management

Your cash flow management for the next 12 months has been revised, without any significant change in lifestyle. Based on our recommendations, your annual surplus has been increased from a mere RM30 to RM40,278. After accounting for extra premium of RM15,500 payable for additional insurances, the surplus is scaled down to RM24,778. However, this does not mean that the entire extra insurance premium of RM15,500 is treated as an expense. Main bulk of this premium forms the investment element in the insurance policies that can be reaped at later years and therefore form part of the investment portfolio.

Your desire to grow your networth by 15% compounded every year is possible with our recommendations in this plan. In fact, the growth will be from RM380K to RM3.3m within the 15 years, giving a compounded growth of 15.5%.

1.2 Risk management/Insurance

Your family’s personal insurance programme is now complete. The additional RM15,500 premium for the additional insurances will give you and your family full protection and at the same time give a long term projected return rate of 8% until your age 50. This will also form part of your retirement wealth accumulation plan.

For husband :

Coverage Old (RM) Additional (RM)Natural death & disability 100,000 1,500,000Accidental death & disability 100,000 1,500,000Critical Illness 0 400,000Medical 0 Up to 300,000

lifetime limitWaiver of premiums on disability and critical illness

No Yes

For Jill :

Coverage Old (RM) Additonal (RM)Natural death & disability 100,000 630,000Accidental death & disability 100,000 630,000Critical Illness 50,000 350,000Medical 0 Up to 300,000

lifetime limitWaiver of premiums on disability and critical illness

No Yes

For Jane :

Coverage Old (RM) New (RM)Natural death & disability 0 300,000Accidental death & disability 0 300,000Critical Illness 0 200,000Medical 0 Up 150,000

lifetime limit Waiver of premiums on disability and critical illness

0 Yes

1.3 Retirement Planning

Based on your assumptions, your required retirement income is RM161,880 in future ringgit at age 50 and based on principal liquidation basis, the lump sum needed is RM4.2m. However, all your funding sources can only accumulate to a total RM3.3m. We recommend that your retirement income be scaled down to RM RM107,355 in future ringgit at age 50 in order to achieve both the retirement and education lump sum required at age 50.

1.4 Investment Planning

Your current asset portfolio only derive return rate of 5.6% which is too low for your moderate risk appetite. In order to achieve the required wealth accumulation targets, we recommend the return rate be increased to 8.0% via asset restructuring including a leveraging effect to be taken place.

1.5 Estate Planning

Your wish to ensure that all assets be passed on securely can be done easily by writing wills, by both you and your wife, and placing them in trusts. We are able to provide you with the will-writing and trust creation services.

1.6 Tax Planning

Your desire to maximize tax saving has been looked into and we recommend an insurance programme where it support the major reliefs allowed. Other reliefs are coincidentals.

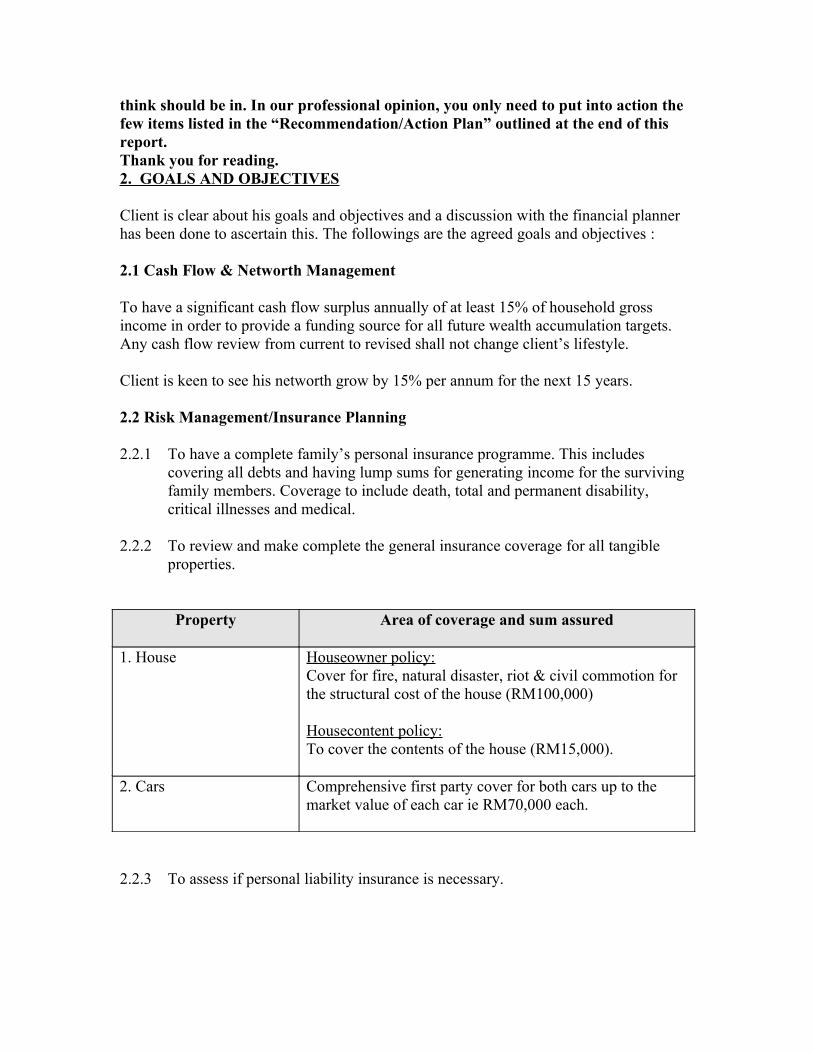

In summary, your personal financial planning is relatively well-planned by your goodself and we certainly are glad that you have in place most of the things that we

think should be in. In our professional opinion, you only need to put into action the few items listed in the “Recommendation/Action Plan” outlined at the end of this report.Thank you for reading.2. GOALS AND OBJECTIVES

Client is clear about his goals and objectives and a discussion with the financial planner has been done to ascertain this. The followings are the agreed goals and objectives : 2.1 Cash Flow & Networth Management

To have a significant cash flow surplus annually of at least 15% of household gross income in order to provide a funding source for all future wealth accumulation targets. Any cash flow review from current to revised shall not change client’s lifestyle.

Client is keen to see his networth grow by 15% per annum for the next 15 years.

2.2 Risk Management/Insurance Planning

2.2.1 To have a complete family’s personal insurance programme. This includes covering all debts and having lump sums for generating income for the surviving family members. Coverage to include death, total and permanent disability, critical illnesses and medical.

2.2.2 To review and make complete the general insurance coverage for all tangible properties.

Property Area of coverage and sum assured

1. House Houseowner policy:Cover for fire, natural disaster, riot & civil commotion for the structural cost of the house (RM100,000)

Housecontent policy:To cover the contents of the house (RM15,000).

2. Cars Comprehensive first party cover for both cars up to the market value of each car ie RM70,000 each.

2.2.3 To assess if personal liability insurance is necessary.

2.3 Retirement Planning

2.3.1. To retire at James’ age 50 with future value ringgit retirement income of RM161,880 per annum.

2.3.2 To have a retirement home in Cameron Highlands in the form of a country home with rental and land lease of RM800 per month.

2.4 Investment Planning

To have an asset portfolio that will grow at a rate that support the realization of the wealth accumulation goals for financial freedom (retirement) and education for child.

2.5 Estate Planning

To have wills written for both husband and wife and to have a trust set up for the child.

2.6 Tax Planning

To optimize tax avoidance or savings under the Malaysian tax system. Client is keen on using up all personal tax reliefs and rebates and to have good income reallocation planning.

3. PERSONAL DATA

Client, James is a training consultant married to Jill , a lawyer and they have a 1-year old daughter named Jean.

The followings are their personal details:

Area James Jill Jean

Birth date 3 Aug 1970 30 Oct 1973 26 March 2004

Sex Male Female Female

Marital status Married Married Single

Address 23 Jalan 13/2Petaling Jaya

Same Same

Tel 03-73573488 Same Same

Occupation Training consultant Lawyer Nil

Employer XYZ Training Consultancy

Peter & Jill Nil

Income from employment

RM120,000 per annum

RM65,000 per annum

NA

Business Nil Nil NilPosition in business

Nil Nil Nil

Income from business

Nil Nil Nil

4. CURRENT FINANCIAL SITUATION

4.1 Cash Flow Statement – Current

The income and expenses of the client for the past 12 months are as follows:

Cash Flow Statement – Current Incoming RM Outgoing RM

James net salary 90,705 Car loan instalments 25,068 Jill net salary 60,537 House loan instalments 10,644 Interest Saving A/C 240 Car maintenance 4,800 Interest Saving FD 4,800 House maintenance 2,340 Credit Card payments 24,000 Eating out 30,000 Groceries 6,000 Travel 24,000 Utilities 4,800 Life insurance 3,000 Miscellaneous 21,600 Total 156,282 Total 156,252 Surplus 30

On a yearly basis, client has a very small surplus of RM 30 only which hardly can be used for commencing funding instruments to achieve their goals and objectives.

Networth Statement – Current Assets RM Liabilities RM

Liquid assets : Mortgage loan 92,795 Pure cash - Car loans 78,712 Saving account 12,000 Credit Cards 18,000 Current account - Fixed Deposits 120,000 Unit Trusts 5,000

Sub-total 137,000 Non-liquid assets : Equities 6,500 Properties 142,000 EPF 280,000 Club memberships 2,000 Cars 140,000 Life insurance cash value 2,000

Sub-total 572,500 TOTAL 709,500 TOTAL 189,507

NETWORTH 519,993

The financial ratios of the above cash flow are :

a) Liquidity ratio = Cash/Monthly expenses = 132,000 / (156,252/12) = 10 months

(Comment: More than meet the benchmark band of 3 – 6 months of expenses. Unless the Fixed Deposits are for long term hold as part of the Asset Portfolio, liquidity ratio is high)

b) Liquid Assets to Net Worth = 137,000 / 519,993 = 0.26 = 26%

(Comment: Lower liquidity – may be a bit tight or less flexible in converting or restructuring assets in case of an immediate investment opportunity)

c) Solvency ratio = Net Worth/Total Assets = 519,993 / 709,500 = 0.73 = 73%

(Comment: Relatively high solvency. Financial stability is ranked as strong)

d) Debt to Asset ratio = Total Debts/Total Assets = 189,507 / 709,500 = 0.27 = 27%

(Comment: Gearing at 27% at client’s age is considered low; need to be higher if risk profile permits)

e) Saving ratio = Annual Saving/Gross Income = 30 / 185,000 = 0.02 %

(Comment: Extremely low compared to the national saving rate of about 30%. However, in this calculation, savings in insurance policies, car and housing loan repayments on principals are excluded. If included, the cash values of such payments will add to the ratio.)

4.2 Risk Management/Insurance Planning

The current personal insurance programme is as follows:

Person Plan type Premium p.a. Plan breakdown Remarks

Husband 1999 WL 1,200 WL - 100K No riders. Traditional policy.

Wife 2003 1,800 Death/TPD – 100K Investment-linked

Investment-linked WL

Critical Illness - 50K policy.

Daughter No policy

The current property insurance programme is as follows:

Property Area of coverage and sum assured

Apartment in Subang Jaya Houseowner : RM 100,000Householder : nil

Cars Two Proton Perdanas : RM 70,000 eachOn comprehensive first party cover.

There is currently no personal liability insurance programme.

4.3 Retirement Planning

There is currently no clear plan on retirement. Other than the EPF that the client has been contributing, there is no other plan on retirement.

Client has been taking the past approach of retiring when they have enough money. Even the benchmark of “enough” is not clear until discussion has taken place with the financial planner.

4.4 Investment Planning

The following table lists out the portfolio of investment-grade assets currently owned and the portfolio return rate :

Asset Amount RM('000) Return Rate Weightage = Amount/Total x Return Rate

Saving Account 12.0 0.02 0.000FD 120.0 0.04 0.008Equities 6.5 0.12 0.001Property 142.0 0.08 0.020Life insurance 2.0 0.05 0.000Unit Trust 5.0 0.12 0.001EPF 280.0 0.05 0.025Club m/ship 2.0 0.01 0.000 - 0.00 0.000Total: 569.5 Portfolio return: 0.056

Based on the portfolio rate of return of 5.6%, the overall risk profile is considered conservative. Even taking out EPF as a compulsory saving element, the portfolio rate of return without EPF is only 6.2%. At age 35, client can take more risk for long term investment instruments and based on the risk profile questionnaire completed, can take a portfolio return rate of 8%.

4.5 Estate Planning

There is no arrangement of any nature including will and trust done, other than the nominations done for

• EPF• All the insurance policies

4.6 Tax Planning

Max amount deductible

Amount used up(RM)

Balance to be used (RM)

Area of relief :

EPF/life insurance premiums

5,000 per adult 5,000 for husband and 1,800 for wife

3,200 for wife

Medical/education insurances

3,000 per adult Nil 3,000 for both husband and wife

Parents’ medical 5,000 per adult 0 5,000 per adult

Child/ren 1,000 per child 1,000 under husband

Nil

Annuity 1,000 per adult 0 1,000 per adult

Books/magazines 500 per adult 0 500 per adultEducational fees 2,000 per adult 0 2,000 per adult

Area of rebates:

Computer purchase

Zakat/Fitrah

Rebate of 400

Full rebate

0

NA

400

NA

The other facts and data were collected in the “Personal Financial Fact-Finder” form as attached in the Appendices.5. ASSUMPTIONS

BASE CASE :

James’ income increases at the rate of 8 % per annum until age 50. There is unlikely to be a change in job at the moment. Even if there is, this assumption still holds.

Income from wife will be increasing at a rate of 2% per annum.

Rate of inflation at 4 % per annum based on government official rate on Consumer Price Index. Lifestyle inflation taken at 7% per annum on a basket goods taken at upper middle income lifestyle.

Fixed deposit rate at long term 4% p.a. nominal rate.

Equities investment rate of return at 12% p.a. on long term basis.

Property investment rate of return at 12 % p.a. covering both capital gain and rental yield.

Investment-linked equities funds at rate of return of 11% p.a.

Investment-linked bond funds at rate of return of 7 % p.a.

Venture capital fund rate of return at 50 % p.a.

The market value of client’s own house is RM142,000 and value increasing at 4 % per annum

The retirement home in Cameron Highlands will be on rental basis and therefore the current apartment home shall be treated as an investment grade asset to be liquidated at age 50.

Cars decrease in value at the rate of 10% p.a.

The tax bracket of JHDN for personal income and business income will remain at today’s rate.

Pre-retirement investment portfolio rate of return = 8% Post-retirement investment portfolio rate of return = 6%

6. CASH FLOW MANAGEMENT

The current cash flow surplus is very low at RM30 per annum. Based on no change or very minimal change in lifestyle of the client, we have studied and done an analysis.

In recommending changes, we have kept in mind some basic principles:

• Lifestyle of the client need to be maintained as original as possible unless the client is willing to sacrifice today for a better tomorrow.

• Any reshuffling of assets including paying off debts or loans must leave behind enough liquid assets that caters to the 3-6 months’ of emergency buffer fund.

• Repayment of loans must take into considerations what client wants to do with his liquid assets like FD and saving account balances in the near future, for example, in case there is a very good investment opportunity where the rate of return is higher than the borrowing cost of the loans to be redeemed. In this scenario, client has no such near term investment opportunity.

Our analysis and recommendations:

1. Credit Card : The couple keeps quite a high balance and repays only 10% per month. Keeping a constant balance of about RM18,000 attracting 18% per annum interest rate is rather high in holding cost. In another word, upon receiving the credit card monthly statement, client pays 10% or RM2,000 of the RM20,000 outstanding balance and the new balance is RM18,000. From the balance sheet, we note that the couple saves quite an amount at RM12,000 in saving accounts and RM120,000 in fixed deposits in the banks. But this saving account and FD is only getting 2% and 4% rate of return per annum respectively. It will be better off to clear all the credit card balances by transferring RM10,000 from this saving account and RM 8,000 from FD into the credit card account. This will save them RM270 per month in interest. Therefore the monthly repayment of all expenses charged to the card without interest will be RM2,000 less RM270 = RM 1,730 per month.

2. Travel : To spend RM 24,000 per annum on travel is relatively high which is RM6,000 per pax per trip. The financial planner has to probe into the reasons so as to determine if this is a preferred lifestyle. If it is not, it is recommended that the couple travel to less expensive places but meeting the same leisure objectives. They may want to reserve the more expensive destinations for future travel when their finances are much stronger and also when they have more time to travel to such far away destinations. It will be good if the couple can reduce the annual travel expense down to RM 16,000. For RM4,000 per trip per pax, client can actually go to a number of good destinations around the world.

3. Eating out : To spend RM 30,000 per annum or RM 2,500 per month eating out is unusually high. Again, if this is the preferred lifestyle, this has to be respected. If the

couple is frequenting the same few restaurants or chain of restaurants, maybe they should get some customer loyalty cards where discounts are available. Otherwise, they have to be convinced that cutting down the expenses by eating the same food in cheaper places will be a good idea although the ambience will be different. If discount loyalty cards can save 15%, that will be RM4,500 saved.

4. Car repayments : The interest rate on car loans is based on flat rates. At 8.5 % per annum, this means paying an additional 59.5% of the original car prices after a 7-year period. After credit card which has borrowing cost of nominal rate of 18% per annum, these car loans have a converted monthly rest rate of 14.4%. Again, if the fixed deposits in the bank sitting at 4% rate of return has no special usage in the near term, we will recommend the clients to use part of it to pay off completely the balance of the car loans of RM 78,712.

5. Miscellaneous expenses : At RM 21,600 per annum, the amount looks high for small ticket items. It is recommended that the couple keeps track of the little items that they spend so that this amount is managed downwards. A lot of small and low cost items are purchased without realizing that there is no economy of scale, usually duplicated and inefficiencies occurred. By keeping track such purchases in a ledger, we can study the pattern and avoid wastages by probably 10% of the total amount down to RM19,440.

6. Refinance the housing loan : The interest rate for the current loan is at BLR + 2% whereas the current rate is BLR + 0.5%. A number of banks are also offering free switch over i.e. no transfer cost such as legal fees, etc. Over the next 15 years for a loan of RM92,795 which is the current housing loan redemption value, the saving of 1.5 % can come to RM79 per month or RM948 per annum. The new repayment is RM782 per month compared to the previous monthly payment of 887 per month.

(Calculations on the new housing loan repayments :

n = 15 x 12 = 180 monthsi = 6.5 / 12 = 0.5417 %

FV = 0PV = 92,795Mode = endFind PMT which is RM 808 per month)

7. EPF Account II used to reduce/redeem housing loan : Since 30% of the balance in the client’s EPF come to RM84,000, this can be used to reduce the outstanding loan of their apartment. This option is not recommended at the moment as client has indicated to use this portion to possibly upgrade their home in the future. However, one point to remember is that if the rate of return in EPF is lower than housing loan rate, then it will be a good move. On the discipline perspective, it is better to keep the EPF money intact as fund in EPF has its own clear objective of providing for retirement.

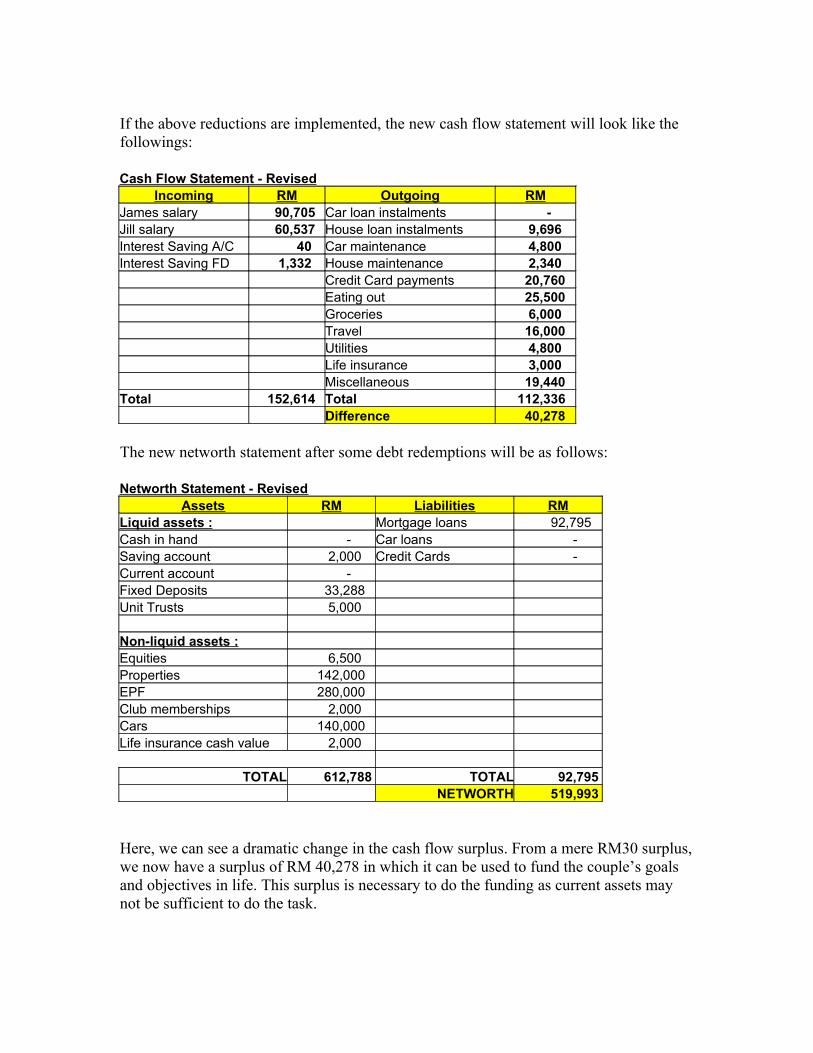

If the above reductions are implemented, the new cash flow statement will look like the followings:

Cash Flow Statement - RevisedIncoming RM Outgoing RM

James salary 90,705 Car loan instalments - Jill salary 60,537 House loan instalments 9,696 Interest Saving A/C 40 Car maintenance 4,800 Interest Saving FD 1,332 House maintenance 2,340 Credit Card payments 20,760 Eating out 25,500 Groceries 6,000 Travel 16,000 Utilities 4,800 Life insurance 3,000 Miscellaneous 19,440 Total 152,614 Total 112,336 Difference 40,278

The new networth statement after some debt redemptions will be as follows:

Networth Statement - RevisedAssets RM Liabilities RM

Liquid assets : Mortgage loans 92,795 Cash in hand - Car loans - Saving account 2,000 Credit Cards - Current account - Fixed Deposits 33,288 Unit Trusts 5,000 Non-liquid assets : Equities 6,500 Properties 142,000 EPF 280,000 Club memberships 2,000 Cars 140,000 Life insurance cash value 2,000

TOTAL 612,788 TOTAL 92,795

NETWORTH 519,993

Here, we can see a dramatic change in the cash flow surplus. From a mere RM30 surplus, we now have a surplus of RM 40,278 in which it can be used to fund the couple’s goals and objectives in life. This surplus is necessary to do the funding as current assets may not be sufficient to do the task.

Although substantial amount of FD has been transferred out to pay the credit card and car loans, the client is assured that with the healthy surplus of RM 40,278, this reduction in liquid assets will be replenish in 2.5 years’ time. And the wonderful thing is that the client will have RM 40,278 on year 3 onwards for many years compared to RM30 earlier!

After using part of the surplus for a full insurance programme under Section 7, the cash flow statement has to be revised again as follows:

Cash Flow Statement - Revised (after insurance programme)Incoming RM Outgoing RM

James salary 90,705 Car loan instalments - Jill salary 60,537 House loan instalments 9,696 Interest Saving A/C 40 Car maintenance 4,800 Interest Saving FD 1,332 House maintenance 2,340 Credit Card payments 20,760 Eating out 25,500 Groceries 6,000 Travel 16,000 Utilities 4,800 Life insurance 18,500 Miscellaneous 19,440 Total 152,614 Total 127,836 Difference 24,778

7. RISK MANAGEMENT/INSURANCE

7.1 Personal Insurance

Client is keen to upgrade his and his family’s insurance programme so as to meet the goal and objectives as outlined in Section 2 above. Based on the normal guideline of premium budget of 10-15% of their gross income for a complete personal insurance programme, it is recommended that client set aside RM18,500 as the annual premium budget for the entire family’s insurance programme. Currently, client spends RM3,000 per annum.

Calculations for client’s sum assured :

a) Death & Total and Permanent Disability

For husband, based on principal liquidated basis :

FV = 0N = 24 years (until the child becomes an independent adult at age 25)I = 4 % (risk free rate equal bank FD rate, inflation not factored in)PMT = 112,336 per annum (based on cash flow revised before complete insurance programme)Mode = BGNFind PV = 1,712,783

With the new networth statement, the debts of the husband shall be only on outstanding housing loan of RM92,975.

Husband RMTotal basic sum assured needed 1,712,783Add : Debt (house loan) 92,975Less : Current insurance (100,000)Less : Networth of family on investment assets only ie S/A, FD, Equities, Unit Trust, husband’ EPF.

(206,788)

Additonal insurance required 1,498,970 or rounded to 1.5m

For wife, the need of wife will be arbitrary as if something were to happen to her, husband will continue working and supporting the remaining family. Therefore, sum assured of half of husband’s amount ie 850K should suffice.

Wife RMTotal basic sum assured needed 850,000Add : Debt NilLess : Current insurance (100,000)Less : Wife’s EPF. (120,000)

Additonal insurance required 630,000

For the child, death cover will not be an important need as the financial loss to the parents will be minimal. However, disability cover is needed and it is recommended that disability income of RM12,000 per year be given. To generate this income perpetually, a basic sum assured of 12,000 / 4% (risk free rate) = RM300,000 is recommended.

For tax reliefs purposes, recommended that both parents buy an investment-linked education policy on the child with minimum RM3,000 premium per annum.

b) Critical Illness & Medical

The amount will be based on the most expensive immediate critical illness treatment ie liver transplant at RM400,000 for both father and mother. For the child, due to the cost of premium, half of the amount or RM200,000 is recommended.

For medical, for father and mother, an annual limit of RM300,000 is recommended. The child to be covered up to RM150,000 annual limit.

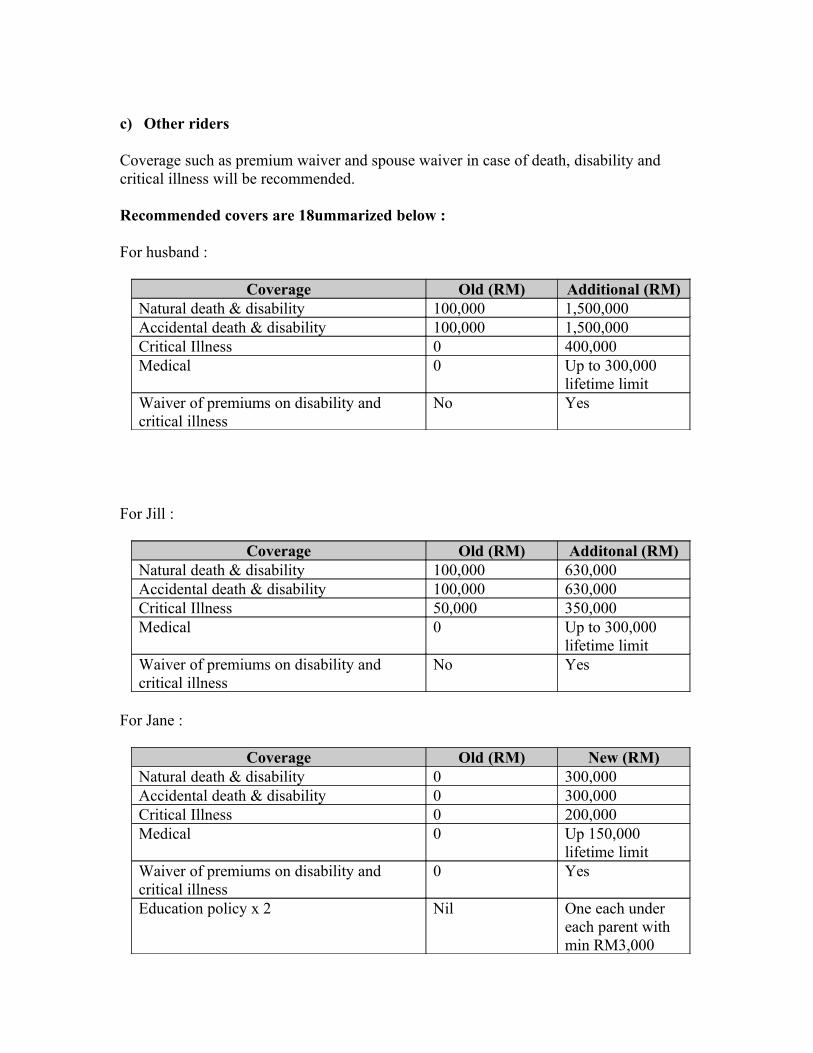

c) Other riders

Coverage such as premium waiver and spouse waiver in case of death, disability and critical illness will be recommended.

Recommended covers are 18ummarized below :

For husband :

Coverage Old (RM) Additional (RM)Natural death & disability 100,000 1,500,000Accidental death & disability 100,000 1,500,000Critical Illness 0 400,000Medical 0 Up to 300,000

lifetime limitWaiver of premiums on disability and critical illness

No Yes

For Jill :

Coverage Old (RM) Additonal (RM)Natural death & disability 100,000 630,000Accidental death & disability 100,000 630,000Critical Illness 50,000 350,000Medical 0 Up to 300,000

lifetime limitWaiver of premiums on disability and critical illness

No Yes

For Jane :

Coverage Old (RM) New (RM)Natural death & disability 0 300,000Accidental death & disability 0 300,000Critical Illness 0 200,000Medical 0 Up 150,000

lifetime limit Waiver of premiums on disability and critical illness

0 Yes

Education policy x 2 Nil One each under each parent with min RM3,000

annual premium.Note : The basis for getting a basic sum assured for the child is not on calculation but rather on a projected amount necessary should the child get into a disability. The child has no income to protect therefore the methods used for adults are not applicable to children

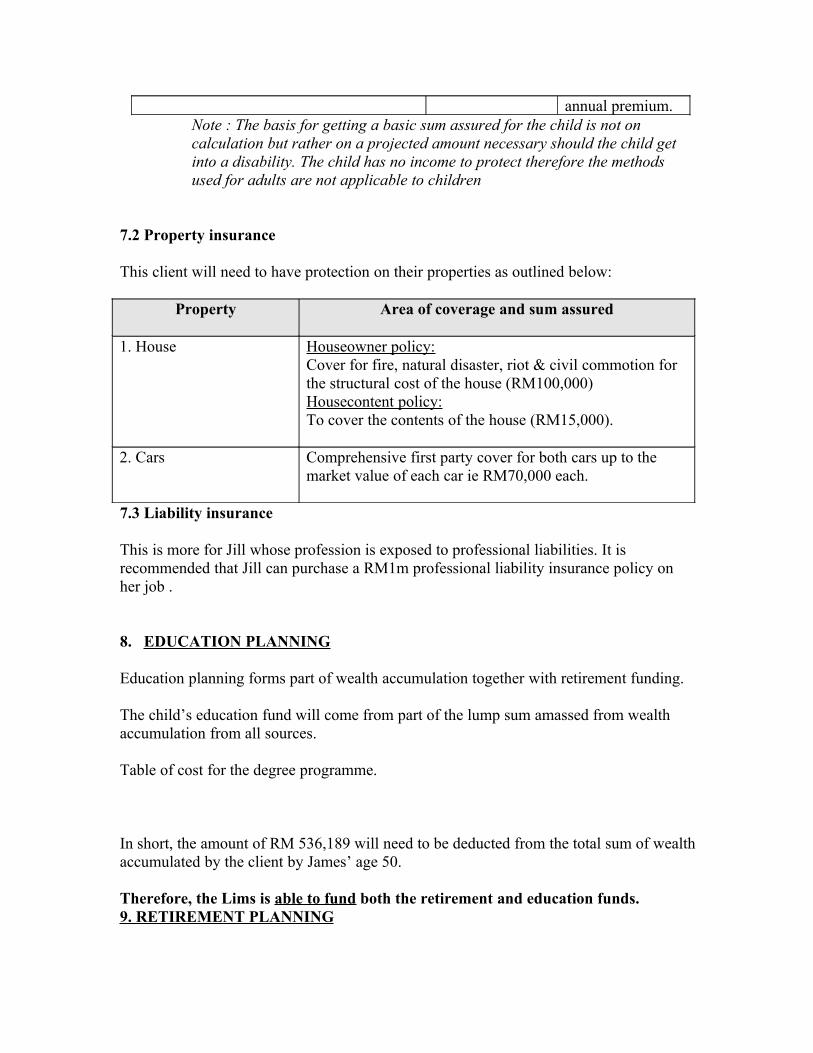

7.2 Property insurance

This client will need to have protection on their properties as outlined below:

Property Area of coverage and sum assured

1. House Houseowner policy:Cover for fire, natural disaster, riot & civil commotion for the structural cost of the house (RM100,000) Housecontent policy:To cover the contents of the house (RM15,000).

2. Cars Comprehensive first party cover for both cars up to the market value of each car ie RM70,000 each.

7.3 Liability insurance

This is more for Jill whose profession is exposed to professional liabilities. It is recommended that Jill can purchase a RM1m professional liability insurance policy on her job .

8. EDUCATION PLANNING

Education planning forms part of wealth accumulation together with retirement funding.

The child’s education fund will come from part of the lump sum amassed from wealth accumulation from all sources.

Table of cost for the degree programme.

In short, the amount of RM 536,189 will need to be deducted from the total sum of wealth accumulated by the client by James’ age 50.

Therefore, the Lims is able to fund both the retirement and education funds.9. RETIREMENT PLANNING

9.1 Financial Independence by age 50

Retirement Income needed :

i) Retirement income projection by TRR method:

Working out the last drawn income by both James and Jill.

For James, using financial calculator,

n = 15 (James has 15 years to go before the target retirement age of 50)i = 8 % (this is the rate of growth of James’s salary per annum)PV = - 120,000 (this is the annual salary for the beginning of the period in calculation)Find FV = 380,660.

Using the same calculation we find Jill’s income 15 years from now and both incomes are tabulated as follows:

Person Years to retirement

Rate of growth in

income

Present annual income (RM)

Future annual income in 15th

year from now (RM)

TRR method at 50 % rate –projected retirement

income

James 15 8 % 120,000 380,660 190,330

Jill 15 2 % 65,000 87,481 43,741

TOTAL : 234,071

The TRR method simply takes a certain percentage of the last drawn salary immediately prior to retirement in which is 50% in this case. Based on the observation that the size of client’s household income is relatively large, 50 % amount is taken. The total projected retirement income need by the couple is RM 234,071 per annum or RM 19,506 per month in future ringgit.

ii) Retirement income projection by Expense Method:

From fact-finding discussion held with client, we list out all the expenses that they projected they will incur when they retire. The amount of each expense is benchmarked at today’s price. The future pricing is found by taking inflation into consideration at 4 % per annum. All the figures are tabulated in the following table:

Retirement Income - Projection by Expense Method

Items needed when retired Today's annual cost Inflation rate Cost at age 50Food 6,000 2% 8,075 Clothing 3,600 1% 4,179 Cars maintenance 4,800 4% 8,645 House rental 9,600 4% 17,289 Personal maintenance 3,600 4% 6,483 Car purchase sinking fund 10,000 5% 20,789 Medical 4,800 8% 15,226 Groceries 6,000 4% 10,806 Travel 24,000 5% 49,894 Utilities 4,800 1% 5,573 Life insurance 4,800 1% 5,573 Entertainment 6,000 3% 9,348 Total 88,000 161,880

Here, we find that the retirement income projected is lower than the TRR method. The Expense Method is the more accurate method but relies quite heavily on the rate of inflation. The TRR method has the advantage of pegging to the level of lifestyle immediately prior to retirement, hence the change in lifestyle is minimal.

Finding the lump sum for retirement :

To find the lump sum to generate this projected retirement income is sufficient, we first select the annual retirement income calculated from the Expense Method at RM 161,880 which is the lower figure among the two retirement incomes calculated above.

Then we work into two scenarios on the length of time this income is needed.

Scenario 1 : The principal intact scheme.The RM 161,880 annual retirement income is to be needed perpetually i.e. indefinitely. Here, based on the inflation-adjusted discount rate i I , we calculate the lump sum needed for such inflation-adjusted income generation.

Assumptions : Rate of inflation, I = 4 %Post-retirement rate of return in fixed income instruments, r = 6 %

Lump sum needed = 161,880 / (6% - 4%) = 8.1 m

The client needs RM 8.1 m to have this retirement income perpetually without liquidating any of the principal amount. The amount looks very high. In lay man terms, this is the “deluxe scheme”. The second scenario will be the “economy scheme”.

Scenario 2 : Principal liquidation scheme.

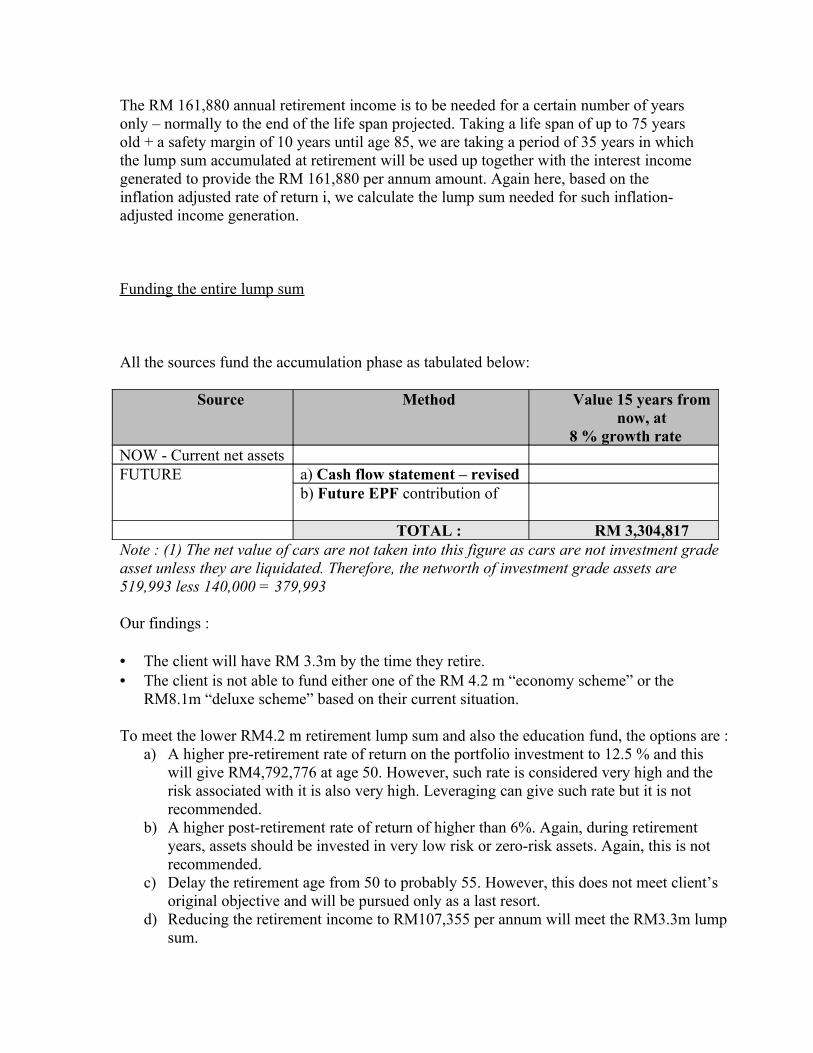

The RM 161,880 annual retirement income is to be needed for a certain number of years only – normally to the end of the life span projected. Taking a life span of up to 75 years old + a safety margin of 10 years until age 85, we are taking a period of 35 years in which the lump sum accumulated at retirement will be used up together with the interest income generated to provide the RM 161,880 per annum amount. Again here, based on the inflation adjusted rate of return i, we calculate the lump sum needed for such inflation-adjusted income generation.

Funding the entire lump sum

All the sources fund the accumulation phase as tabulated below:

Source Method Value 15 years fromnow, at

8 % growth rateNOW - Current net assetsFUTURE a) Cash flow statement – revised

b) Future EPF contribution of

TOTAL : RM 3,304,817Note : (1) The net value of cars are not taken into this figure as cars are not investment grade asset unless they are liquidated. Therefore, the networth of investment grade assets are 519,993 less 140,000 = 379,993

Our findings :

• The client will have RM 3.3m by the time they retire.• The client is not able to fund either one of the RM 4.2 m “economy scheme” or the

RM8.1m “deluxe scheme” based on their current situation.

To meet the lower RM4.2 m retirement lump sum and also the education fund, the options are :a) A higher pre-retirement rate of return on the portfolio investment to 12.5 % and this

will give RM4,792,776 at age 50. However, such rate is considered very high and the risk associated with it is also very high. Leveraging can give such rate but it is not recommended.

b) A higher post-retirement rate of return of higher than 6%. Again, during retirement years, assets should be invested in very low risk or zero-risk assets. Again, this is not recommended.

c) Delay the retirement age from 50 to probably 55. However, this does not meet client’s original objective and will be pursued only as a last resort.

d) Reducing the retirement income to RM107,355 per annum will meet the RM3.3m lump sum.

We recommend the option (d) as this is easiest to adapt.

9.2 Retirement Home in Cameron Highlands

The retirement home will be on rental basis as desired by the client. There will not be any capital expenditure but only cash flow outlays.

10. INVESTMENT PLANNING

To meet the desired retirement lump sum at age 50, the portfolio investment rate of return used above is 8% for pre-retirement. However, based on the current portfolio as per Section 4, the portfolio return rate is only 5.6%.

The portfolio needs to be restructured to the followings :

Asset Amount RM('000) Return Rate Weightage-Amount/Total x Return Rate

Saving Account 2.0 0.020 0.000FD 60.0 0.044 0.005Equities 16.5 0.120 0.003Property (home) 142.0 0.080 0.020Life insurance 2.0 0.050 0.000Unit Trust 89.4 0.120 0.019EPF 225.6 0.050 0.020Club m/ship 2.0 0.010 0.000Property B 30.0 0.251 0.013Total: 569.5 Portfolio return: 0.080

The recommendations are :

Based on the risk profile questionnaire, client has a moderate risk appetite. Client need not have a large cash in saving account and FD. Therefore, we recommend a reduction of cash in FD by half from 120K to 60K. 30K will be channeled to unit trust and another 30K to purchase another property.

The property B to be purchased has a market value of RM300K. With a downpayment of 30K, balance 270K will be from a bank’s housing loan. Assuming over the long term, property B gives a return rate of 8% per annum covering both capital gain and rental yield. Over one year, the return is 300K x 8% = 24K. However, the borrowing cost is at BLR + 0.1% or 6.1% (BLR currently is 6%) therefore incurring 270K x 6.1% = 16.47K interest. Net return is 24K – 16.47K = 7.53K. Over the original investment money of 30K, this is 25.1% return.

10K from saving account to be channeled to direct equities, leaving 62K in both saving and FD which is equal to 5.8 months of emergency buffer fund.

Transfer EPF Account 2 which constitutes 30% of the 280K or 168K. Less 100K (50K per person as the EPF is over the couple) then 20% of it over 4 quarters, the amount of RM54,400 can be invested into EPF approved unit trust.

This restructured portfolio will give an 8 % return in order to meet the accumulation goals of the client. However, such restructuring must meet the risk profile of the clients in which we have matched. If it does not, the financial planner will need to discuss again with the client again if they can arrive to some acceptable conclusions which include but not limited to, making some changes to their goals and objectives.

11. ESTATE PLANNING

Since there is no estate duty in Malaysia, the need for estate planning centers more on will writing, trust creation and estate distribution. A will is recommended to be written to instruct the trustees to distribute all wealth to the beneficiaries as per the wishes of the client should he be demised.

To ensure assets go to the right person(s), it is recommended that all nominations must be properly done for all insurance policies, EPF and mutual funds.

12. TAX PLANNING

12.1 Tax reliefs & rebates

Client is keen to maximize whatever reliefs and rebates he has so that he can pay minimum taxes.

12.2 Income reallocations

By placing investment incomes under the spouse with the lower income tax bracket, less tax are paid. It is recommended that the Property B and shares with dividends be purchased under the wife’s name.

Parking equities shareholdings under the wife allow dividends declared to be given to wife and she can apply for tax refunds for the difference between the corporate tax rate (28% currently) applied at source and her tax bracket which is well below 28% under Income Tax Act Section 110.

Max amount deductible

Amount used up(RM)

Balance to be used (RM)

Area of relief :

EPF/life insurance premiums

5,000 per adult 5,000 for husband and 1,800 for wife

3,200 for wife

Medical/education insurances

3,000 per adult Nil 3,000 for both husband and wife

Parents’ medical 5,000 per adult 0 5,000 per adult

Child/ren 1,000 per child 1,000 under husband

Nil

Annuity 1,000 per adult 0 1,000 per adult

Books/magazines 500 per adult 0 500 per adultEducational fees 2,000 per adult 0 2,000 per adult

Area of rebates:

Computer purchase

Zakat/Fitrah

Rebate of 400

Full rebate

0

NA

400

NA

Our tax recommendations : With the new insurance programme taken up, the RM5,000 insurance

premium/EPF tax relief for wife will be taken up. As part of the same insurance programme, sign up 2 investment-linked

education policies on the same child but applied separately by father and mother. On separate assessment, both will enjoy the RM3,000 education/medical insurance premiums.

To advise their elderly parents to keep all receipts of medical treatments in order to seek tax relief on this item in which currently are not used at all.

Both James and Jill are recommended to purchase an IRD- approved annuity each for annual contribution of RM 1,000 per person as to fully utilize the tax relief under this area. (currently the product is withdrawn until further notice)

If the couple is attending any work-related courses on their own expenses such as training programmes or legal-related courses, they are advised to submit their course fees receipts for tax relief on this area of up to RM 2,000 per annum.

The couple is also recommended to keep any receipts for the purchase of a home computer or accessories as to claim tax rebate of RM 400 every 5 years.

For books purchased in approved bookstores like MPH, the couple is recommended to keep receipts for books purchased for tax relief.

The child relief shall always be placed under James as he is facing a much higher income tax bracket.

13. SPECIAL NEEDS

None at the moment.

14. BUSINESS CONTINUATION

None at the moment.

15. RECOMMENDATION

15.1 Cash Flow Management

Credit Card :. Transfer RM10,000 from saving account and RM 8,000 from FD into the credit card account to clear the entire RM18,000 outstanding.

Travel : Travel to less expensive places but meeting the same leisure objectives. Reserve the more expensive destinations for future travel when finances are much stronger and also when there is more time to travel to such far away destinations

Eating out : Get some customer loyalty cards where discounts are available. different. If discount loyalty cards can save 15%, that will be RM4,500 saved.

Car repayments : To use part of FD to pay off completely the balance of the car loans of RM 78,712.

Miscellaneous expenses : To keep track of the little items spent so that this amount is managed downwards. Use a ledger for 2 months.

Refinance the housing loan : Refinance to a new housing loan at the margin equal the previous redemption sum and with lower rate.

15.2 Risk Management / Insurance

To set aside 10% of annual household income or RM18,500 (inclusive of the current RM3,000 annual premiums) for the insurance specialists to design a full comprehensive package for the entire family.

15.3 Retirement Planning

To review the retirement income amount downwards to RM107,355 per annum future ringgit although the retiring age can be retained at age 50. To have further discussion with financial planner on this.

15.4 Investment Planning

To restructure the asset portfolio so that the portfolio return be enhanced from 5.6% to 8.0% in order to attain the necessary targets for wealth accumulation in retirement planning and education planning. Financial planner will assist in the process.15.5 Estate Planning

To get a will writer or a lawyer to write wills for client and wife. As child is still a minor, a trust should be created and the wills be placed in a public trustee. At the same, do ensure that all nominations for

• Employees Provident Fund• All insurance policies• Unit Trust Funds

be done or updated .

15.6 Tax Planning

To make full use of the tax reliefs and rebates, the main action recommended is a comprehensive insurance programme.

16. IMPLEMENTATION/PLAN OF ACTION

What Who to do it DeadlineTo redeem credit card and car loans Husband 31 June 05

To apply for a discount loyalty card for restaurants

Husband 31 May 05

To refinance housing loan to a new loan with lower interest rate

Financial Planner 31 May 05

To keep a ledger on miscellaneous spendings for 2 months

Wife 1 June 05

To prepare and complete a comprehensive insurance programme for the entire family

Financial Planner 31 May 05

To review retirement planning goals and objectives

Financial Planner + Couple 31 July 05

To restructure the current asset portfolio from 5.6% to 8.0%

Financial Planner 31 May 05

To get a will written and nominations for others.

Financial Planner 31 May 05

To ensure new insurance programme supports more tax reliefs

Financial Planner 28 Feb 06

16. DISCLAIMER

All recommendations in this plan are made on a reasonable basis relative to your current situation. While every effort has been made to ensure the success of the plan, we, our employees, agents or sub agents are not liable and/or responsible for, or guarantee in the following:

The performance of the investments made as a result of our recommendations. Although reliable performance benchmarks were used, past performance of the investment does not guarantee future returns. Performance benchmarks serve only as a guide:

The success of your plan should you modify, omit and/or deviate from our recommendations;

The consequences of any negligence of other professionals who are involved in helping us implement ;

The consequences of any change in the required assumptions made in the plan;

APPENDICES

A. Letter of Engagement

B. Personal Financial Fact-Finder

C. Invoice