Embed Size (px)

Citation preview

SUCCESSION SOLVEDBrad Bueermann, CEO, FP Transitions

Ted Parker, GM of Advisor Lending, Live Oak Bank

PRESENTED BY

Succession is a constant topic in the industry.

Yet few founder/owners have created workable succession plans.

Attrition is the most common outcome. Why?

FP Transitions has written the book and created more than 375 Succession Plans.

SUCCESSION TALK

WHY WE NEED A SUCCESSION SOLUTION (NOT TALK)!

Succession discussion is often misguided.

Discussion focuses on the End not the Continuation.

PARADIGM SHOULD BE SUSTAINABILITY.

Robo advisors vs. wealth firms is not your greatest threat.

Danger is the perception of wealth management firms as ephemeral.

WHY SUSTAINABILITY?

Wealth management is NOT a hamburger stand!

Planning needs extends beyond longevity of the founding owners career.

Implied covenant is that firm will be around to execute clients’ long term plan.

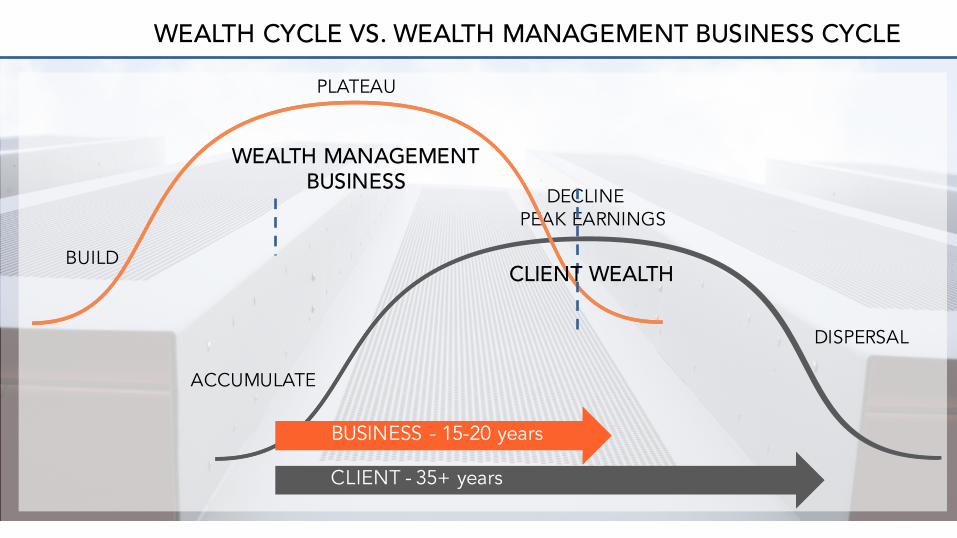

WEALTH CYCLE VS. WEALTH MANAGEMENT BUSINESS CYCLE

ACCUMULATE

PEAK EARNINGS

DISPERSAL

BUILD

DECLINE

PLATEAU

WEALTH MANAGEMENTBUSINESS

CLIENT WEALTH

BUSINESS - 15-20 years

CLIENT - 35+ years

SUSTAINABILITY IS ALSO TIED TO RETENTION

Lack of an equity path for junior advisors makes retaining top talent difficult if not impossible.

Lack of young talent in the firm exacerbates problem with client wealth cycle.

Need younger advisors to connect with beneficiaries of current wealth clients.

ROADBLOCKS TO CREATING VIABLE PLANSWHY ISN’T SUSTAINABLE PLANNING WORKING?

ROADBLOCK 1 : LATE START

Start planning way too late.

When the firm is beginning or nearing decline rather than while it is strong and robust.

Succession is perceived as the “END,” rather than a “sustainability” plan and a long- term growth plan.

ROADBLOCKS TO CREATING VIABLE PLANS

Common compensation systems derived from wirehouse models

Over weights bonuses & commissions, thereby sharing “profit” with non-owners

Result: Firms lack profits and are therefore NOT “investable” enterprises

Sustainable firms must have profits

ROADBLOCK 2 : UNBALANCED COMPENSATION SYSTEMS

ROADBLOCK 3 : G2 HAS NO MONEY TO INVEST

Employees and Junior Advisors derive their income from wages and bonuses from the business and seldom have substantial savings

ROADBLOCKS TO CREATING VIABLE PLANS

SOLUTION:

RE-ENGINEER A SUSTAINABLE FIRM

CREATING THE SUSTAINABLE FIRM

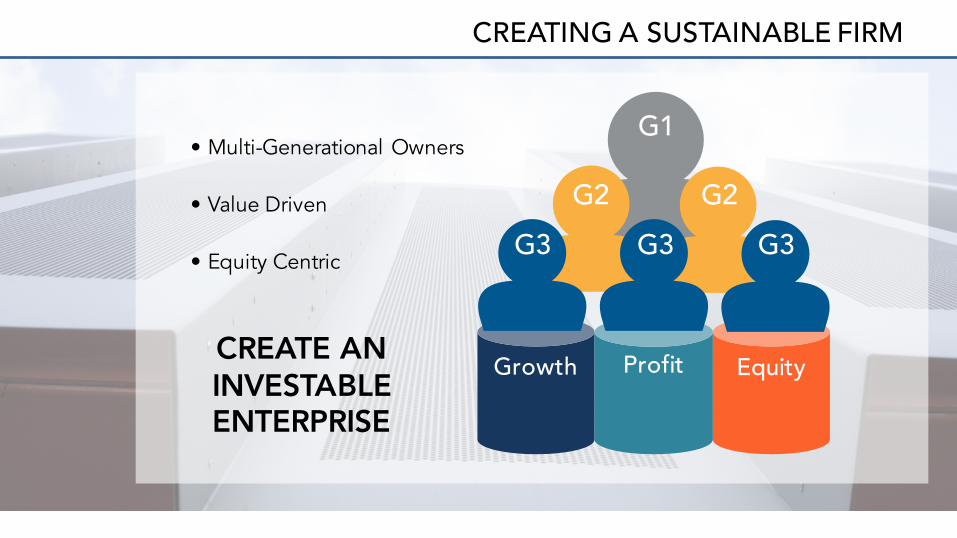

CREATING A SUSTAINABLE FIRM

• Multi-Generational Owners

• Value Driven

• Equity Centric

CREATE AN INVESTABLE ENTERPRISE

Growth Profit Equity

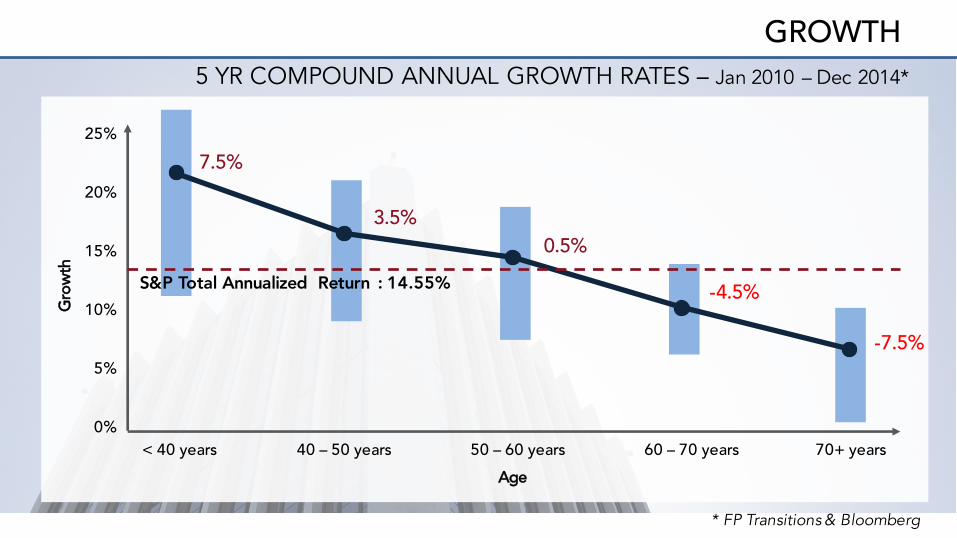

G1

G2 G2G3G3G3

Grow

th

20%

0%

Age

15%

5%

10%

25%

< 40 years 40 – 50 years 50 – 60 years 60 – 70 years 70+ years

5 YR COMPOUND ANNUAL GROWTH RATES – Jan 2010 – Dec 2014*

GROWTH

S&P Total Annualized Return : 14.55%

-7.5%

-4.5%

0.5%3.5%

7.5%

* FP Transitions & Bloomberg

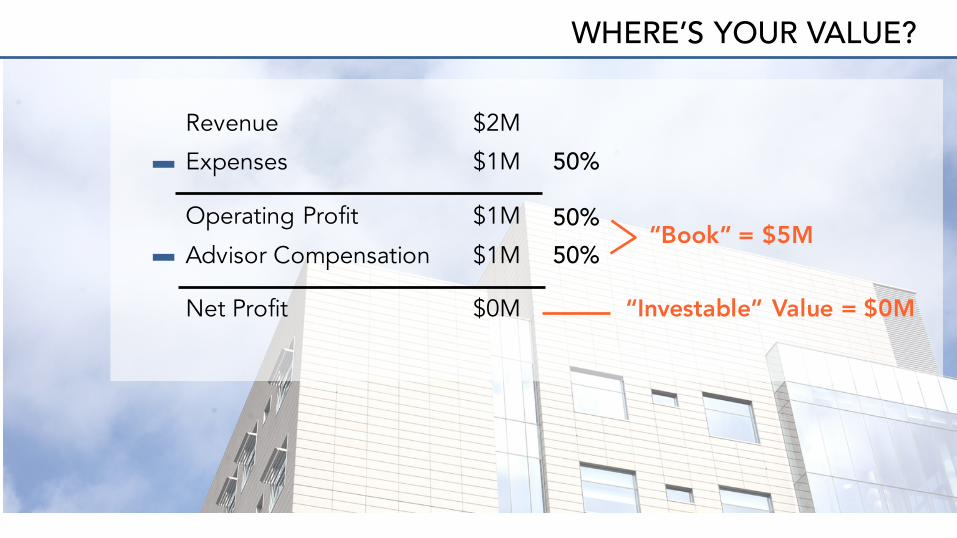

WHERE’S YOUR VALUE?

Revenue $2M

Expenses $1M

Operating Profit $1M

Advisor Compensation $1M

Net Profit $0M

50%

50%

50%“Book” = $5M

“Investable” Value = $0M

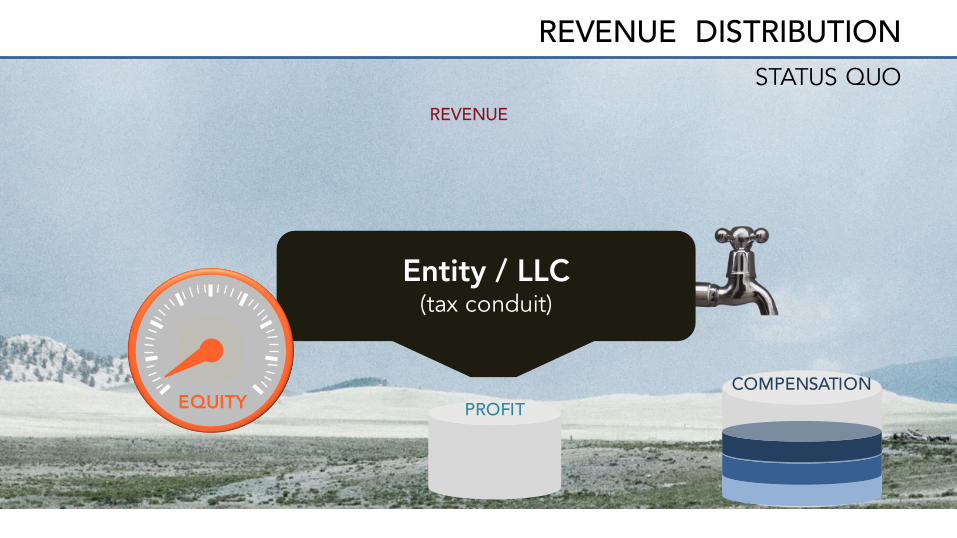

REVENUE DISTRIBUTIONSTATUS QUO

Entity / LLC(tax conduit)

EQUITY

REVENUE

COMPENSATIONPROFIT

GROWTH

Entity / LLC(tax conduit)

EQUITY

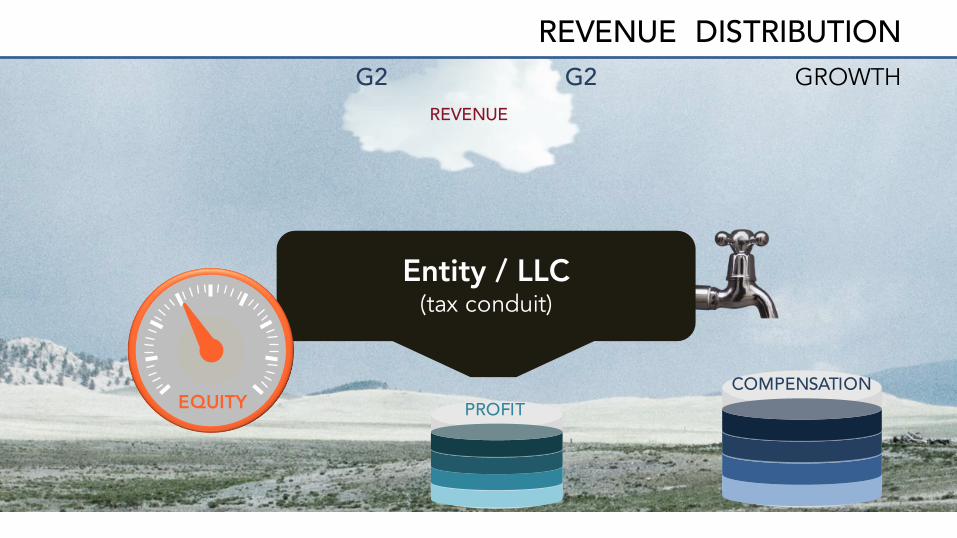

REVENUE DISTRIBUTION

REVENUE

COMPENSATIONPROFIT

GROWTH

Entity / LLC(tax conduit)

G2 G2

EQUITYCOMPENSATION

PROFIT

REVENUE

REVENUE DISTRIBUTION

RE-FOCUS CASH FLOW

PROFIT

INVESTMENT IN THE ENTERPRISE

OWNERSHIP CULTURE

Profit and firm value growth incentivizes & facilitates equity investment

HOW IT WORKS

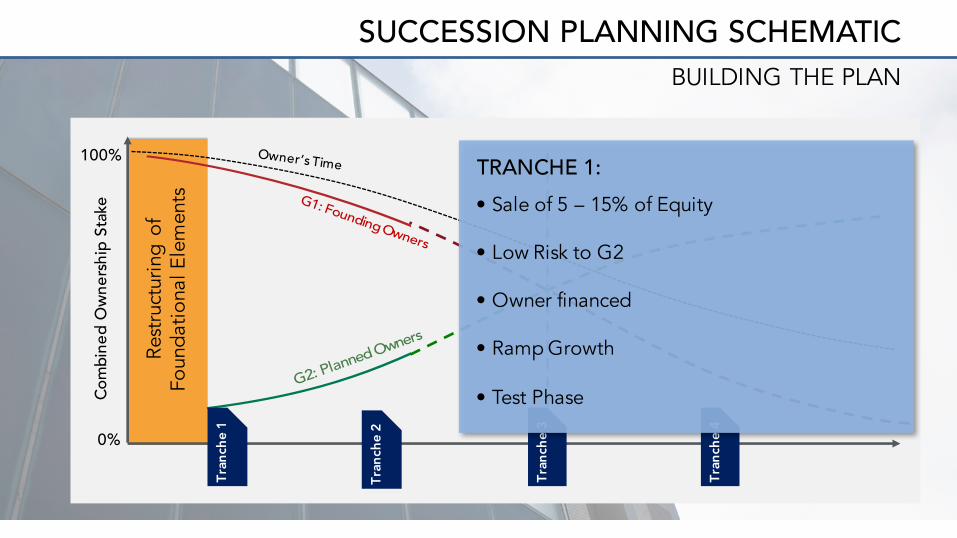

Pathway to equity ownership is accomplished in steps.

CREATING THE SUSTAINABLE FIRM

Plan matches investment to profit share.

Low ownership percentages initiates the ownership experience.

Staged future investments increase G2’s ownership in line with career and life plans of G1 owners.

Plan matches owner goals with G2’s ambitions.

SUCCESSION PLANNING SCHEMATIC

Com

bine

d O

wner

ship

Sta

ke

100%

0%

Tran

che

2

Tran

che

1

Tran

che

3

BUILDING THE PLAN

Tran

che

4

TRANCHE 1:• Sale of 5 – 15% of Equity

• Low Risk to G2

• Owner financed

• Ramp Growth

• Test Phase

Rest

ruct

urin

g of

Foun

datio

nal E

lem

ents

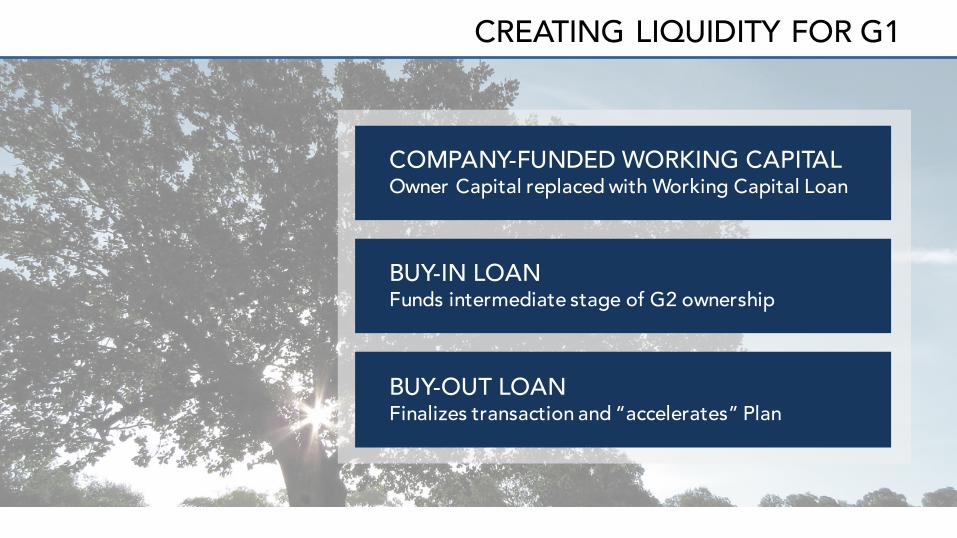

CREATING LIQUIDITY FOR G1

COMPANY-FUNDED WORKING CAPITALOwner Capital replaced with Working Capital Loan

BUY-IN LOAN Funds intermediate stage of G2 ownership

BUY-OUT LOAN Finalizes transaction and “accelerates” Plan

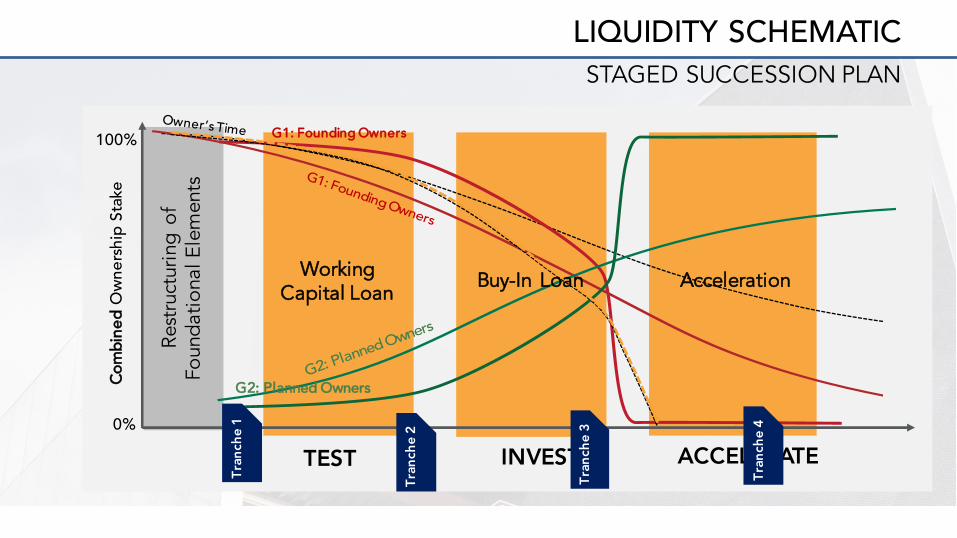

LIQUIDITY SCHEMATICSTAGED SUCCESSION PLAN

Com

bine

d O

wner

ship

Sta

ke100%

0%

G2: Planned Owners

Acceleration

G1: Founding Owners

TEST INVEST ACCELERATE

Tran

che

2

Tran

che

1

Tran

che

3

Tran

che

4

Rest

ruct

urin

g of

Foun

datio

nal E

lem

ents

Working Capital Loan

Buy-In Loan

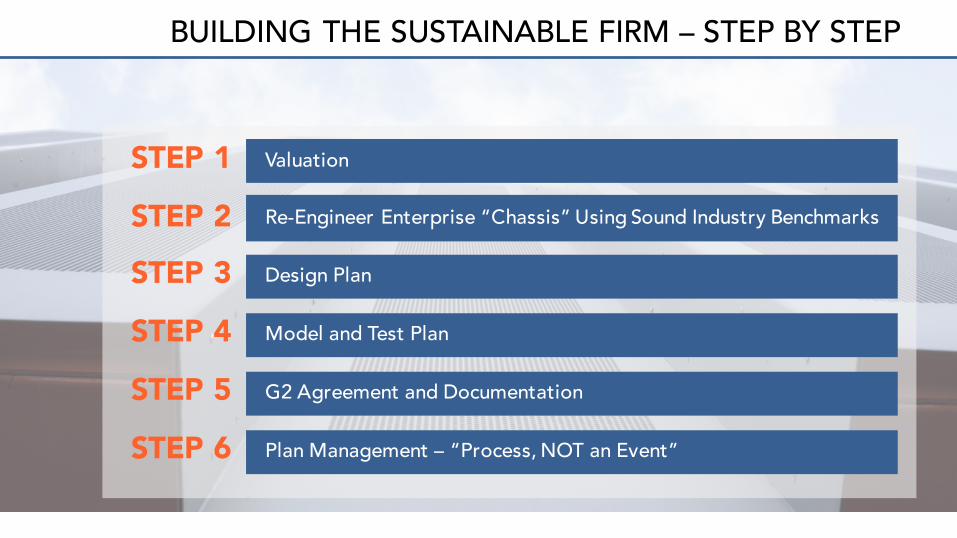

BUILDING THE SUSTAINABLE FIRM – STEP BY STEP

STEP 1

STEP 2

STEP 3

STEP 4

STEP 5

STEP 6

Valuation

Re-Engineer Enterprise “Chassis” Using Sound Industry Benchmarks

Design Plan

Model and Test Plan

G2 Agreement and Documentation

Plan Management – “Process, NOT an Event”

BRINGING THE PIECES TOGETHER

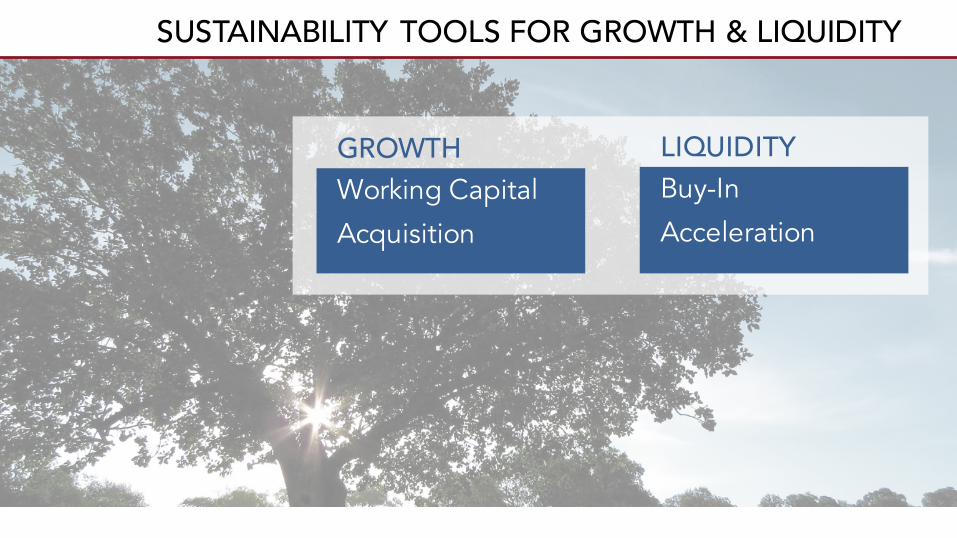

SUSTAINABILITY TOOLS FOR GROWTH & LIQUIDITY

GROWTHWorking Capital

Acquisition

LIQUIDITYBuy-In

Acceleration

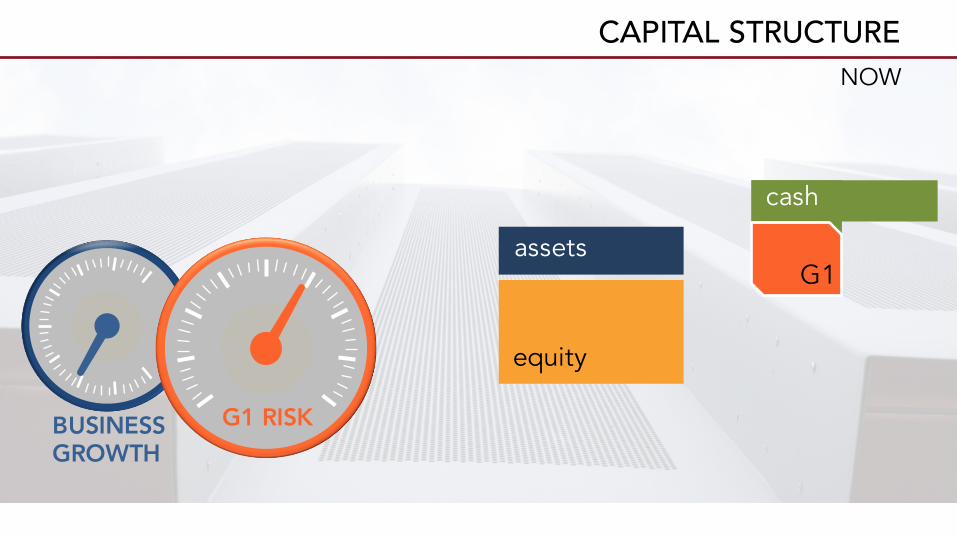

GROWTH VS. RISKWHY CAPITAL STRUCTURE MATTERS

CAPITAL STRUCTURENOW

assets

equity

G1 RISKBUSINESSGROWTH

cashcash

G1

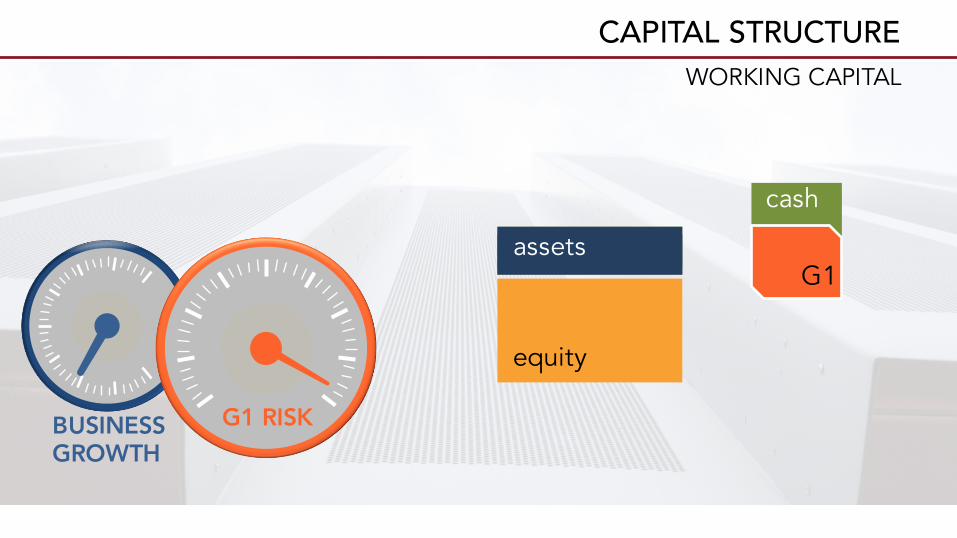

CAPITAL STRUCTUREWORKING CAPITAL

equity

cash

G1

G1 RISKBUSINESSGROWTH

cashworking cap loanassets

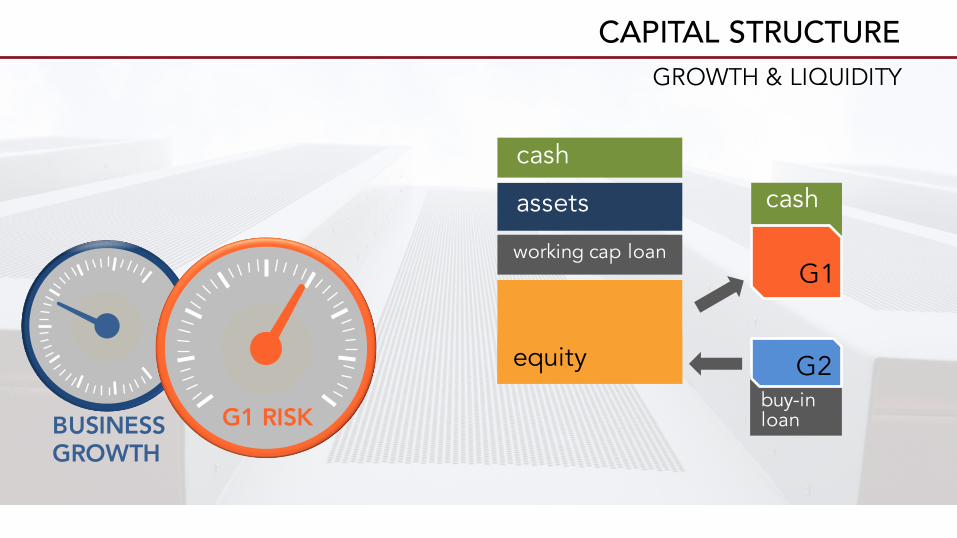

CAPITAL STRUCTUREGROWTH & LIQUIDITY

equity

cash

G1working cap loan

assets

cash

G1 RISKBUSINESSGROWTH

buy-in loan

G2

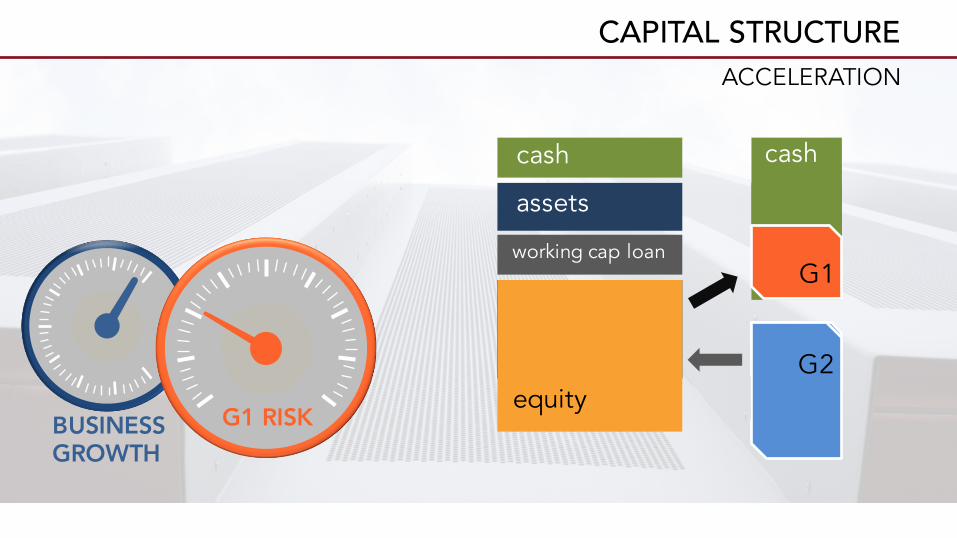

CAPITAL STRUCTUREACCELERATION

cash

G1working cap loan

assets

cash

G1 RISKBUSINESSGROWTH

acceleration loan

equity buy-in

G2

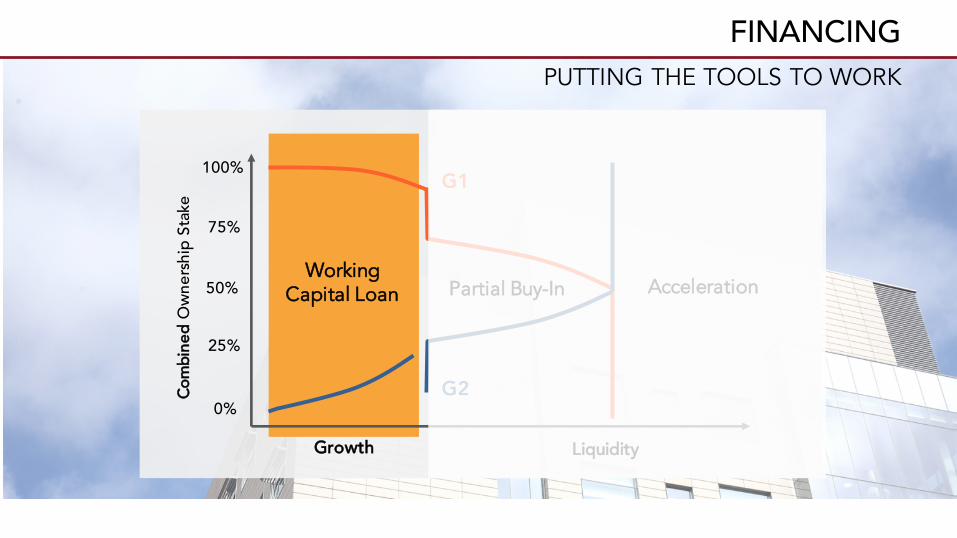

FINANCING

Working Capital Loan

Com

bine

dO

wner

ship

Sta

ke100%

0%

25%

75%

50%

LiquidityGrowth

Partial Buy-In Acceleration

G1

G2

PUTTING THE TOOLS TO WORK

WORKING CAPITAL FOR GROWTH

1ST STEP TO SUSTAINABILITY

Creates an attractive investable asset

Propels growth & “de-risks” G1

Preserves distribution capacity to G2

Enables firm responsiveness to acquisitions

ACQUISITION LOAN FOR GROWTH

Pursue concurrent external growth (M&A)

Encourage strategic collaboration between G1 & G2

Balance … likely pushes out timeline for G1 exit

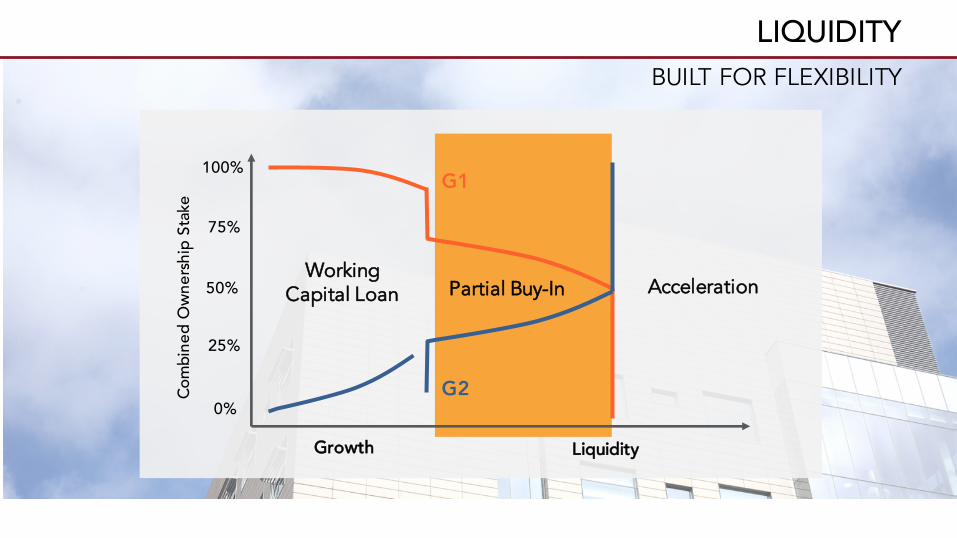

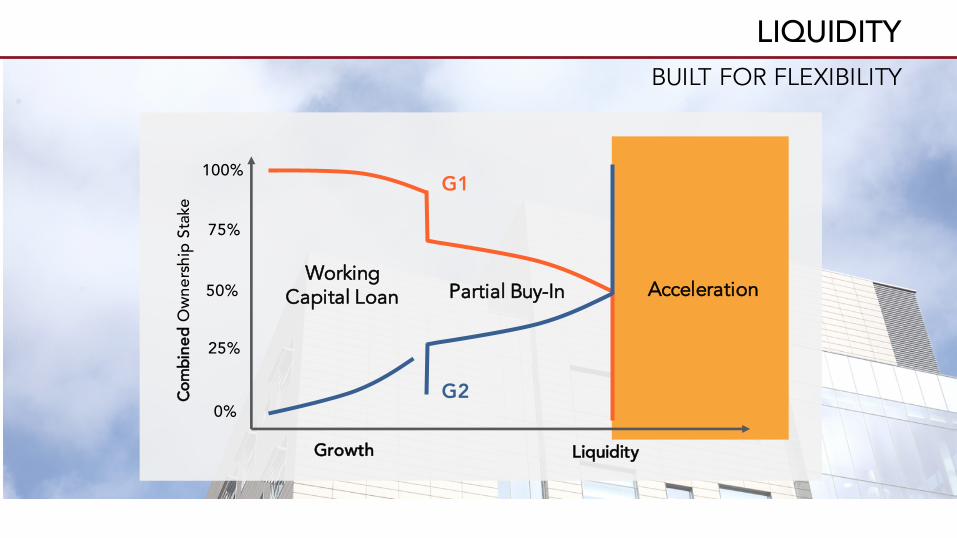

LIQUIDITY

Working Capital Loan

Com

bine

d O

wner

ship

Sta

ke100%

0%

25%

75%

50%

Growth

G1

G2

Liquidity

AccelerationPartial Buy-In

BUILT FOR FLEXIBILITY

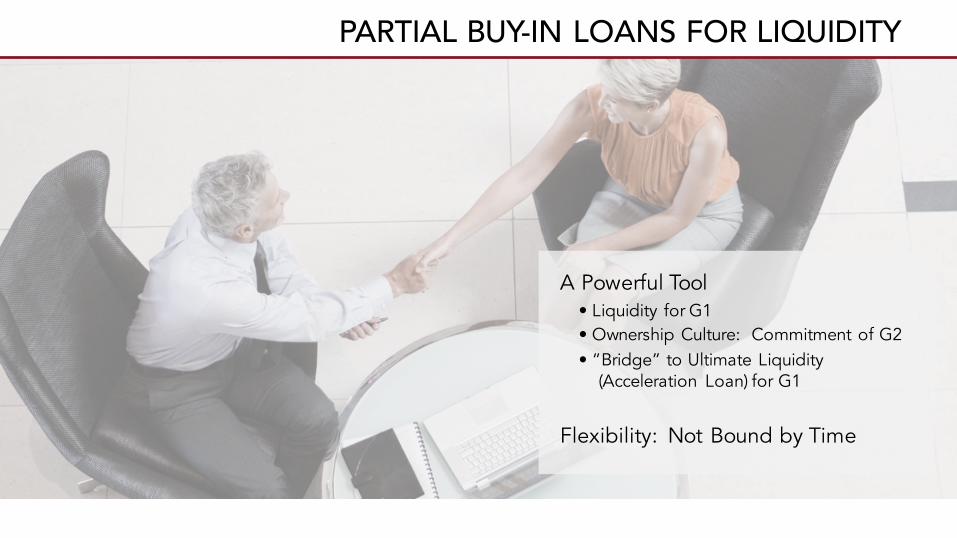

PARTIAL BUY-IN LOANS FOR LIQUIDITY

A Powerful Tool• Liquidity for G1• Ownership Culture: Commitment of G2• “Bridge” to Ultimate Liquidity

(Acceleration Loan) for G1

Flexibility: Not Bound by Time

PARTIAL BUY-IN LOANS FOR LIQUIDITY

Up to 3 Tranches and 40% ownership

1st Tranche : A testing phase

2nd & 3rd Tranches : Steps towards partnership

Underwriting process concurrent for G2 & the Firm

• G2 : 50% DTI

• Firm : “Light” underwriting to hypothetical loan at 60% LTV

BUILT FOR FLEXIBILITY

LIQUIDITY

Working Capital Loan

Com

bine

dO

wner

ship

Sta

ke100%

0%

25%

75%

50%

Growth

G1

G2

Liquidity

AccelerationPartial Buy-In

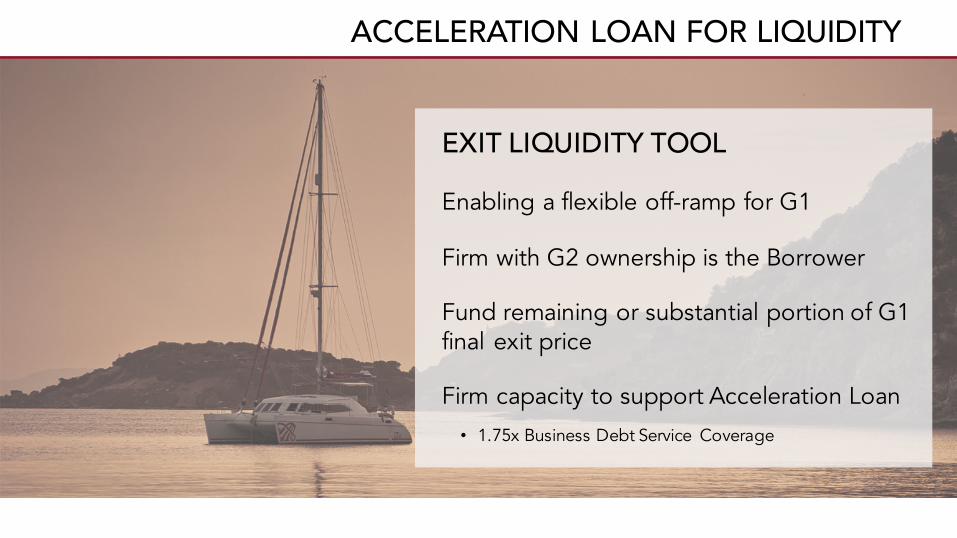

ACCELERATION LOAN FOR LIQUIDITY

EXIT LIQUIDITY TOOL

Enabling a flexible off-ramp for G1

Firm with G2 ownership is the Borrower

Fund remaining or substantial portion of G1 final exit price

Firm capacity to support Acceleration Loan

• 1.75x Business Debt Service Coverage

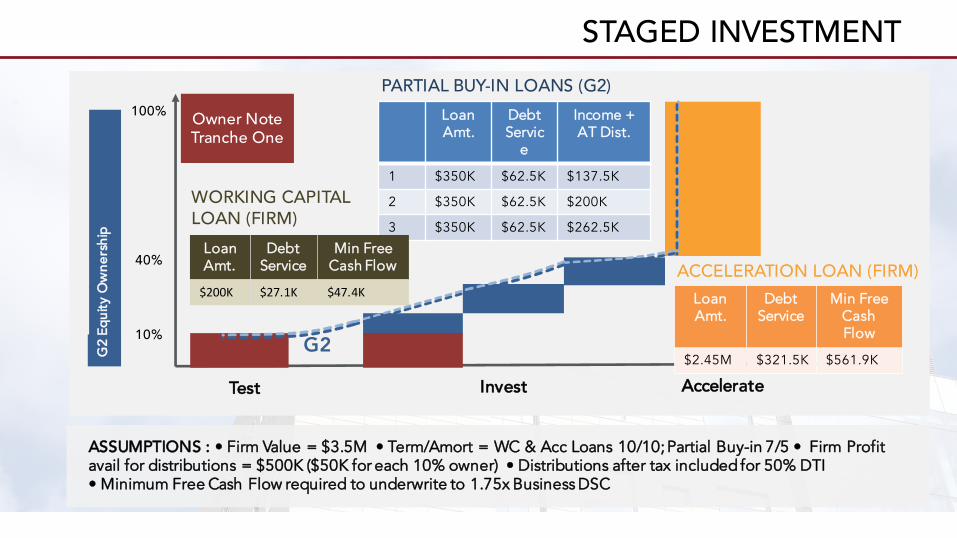

STAGED INVESTMENT

100%

40%

10%

Test

G2

Invest Accelerate

ASSUMPTIONS : • Firm Value = $3.5M • Term/Amort = WC & Acc Loans 10/10; Partial Buy-in 7/5 • Firm Profit avail for distributions = $500K ($50K for each 10% owner) • Distributions after tax included for 50% DTI • Minimum Free Cash Flow required to underwrite to 1.75x Business DSC

Owner NoteTranche One

LoanAmt.

Debt Servic

e

Income + AT Dist.

1 $350K $62.5K $137.5K

2 $350K $62.5K $200K

3 $350K $62.5K $262.5K

PARTIAL BUY-IN LOANS (G2)

LoanAmt.

Debt Service

Min Free Cash Flow

$200K $27.1K $47.4K

WORKING CAPITAL LOAN (FIRM)

LoanAmt.

Debt Service

Min Free Cash Flow

$2.45M $321.5K $561.9K

ACCELERATION LOAN (FIRM)

G2 Eq

uity O

wner

ship

THANK YOU

for more informationfptransitions.com

800.934.3303liveoakbank.com