Embed Size (px)

Citation preview

Superannuationreforms

GarvinJones|Director - Superannuation|29November2016

Disclaimer

HillRogersAdvisoryPtyLtdThematerialcontainedinthispublicationisgeneralcommentaryonlyfordistributiontoclientsofHillRogers.Noneofthematerialis,orshouldberegardedaspersonalorfinancialproductadvice.Accordingly,nopersonshouldrelyonanyofthecontentsofthispublicationwithoutfirstobtainingspecificadvicefromHillRogers.Everyefforthasbeenmadetoensurethatthecontentisaccurate,howeveritisnot intendedtobeacompletedescriptionofthemattersdescribed.HillRogers,itsPrincipalsandagentsacceptnoresponsibilitytoanypersonwhoactsorreliesinanywayonanyofthematerialwithoutfirstobtainingsuchspecificadvice.

TwilightSeminar|SuperannuationReforms|29November2016| 3

Aboutthespeaker

TwilightSeminar|SuperannuationReforms|29November2016| 4

Garvin’s extensive expertise and technical experience in income tax and superannuation makeshim a valuable advisor to his clients, including SMSFs, High Net Worth Individuals and SMEs.

Garvin’s advises clients in

• Tax planning and compliance

• Wealth creation plans

• Retirement planning

• Regulatory compliance

Garvinispassionateabouthelpingpeopletoplanforthetransitionbetweenworkandretirement inawaythatseestheirfinancialgoalsachieved.

GarvinJones- Director,BBus,CA,SMSFSpecialistAdvisor

Services:SuperannuationHighNetWorth IndividualsandProfessionals

t:+61292325111d:+61292200346e:[email protected]:www.hillrogers.com.au

Superannuationreforms- 2016

• Non-concessionalcontributions(non-deductible)

• Concessionalcontributions(deductible)

• Worktest

• 10%test

• $1.6millionmemberaccountbalance

• Questions?

Wherearewe?

TwilightSeminar|SuperannuationReforms|29November2016| 5

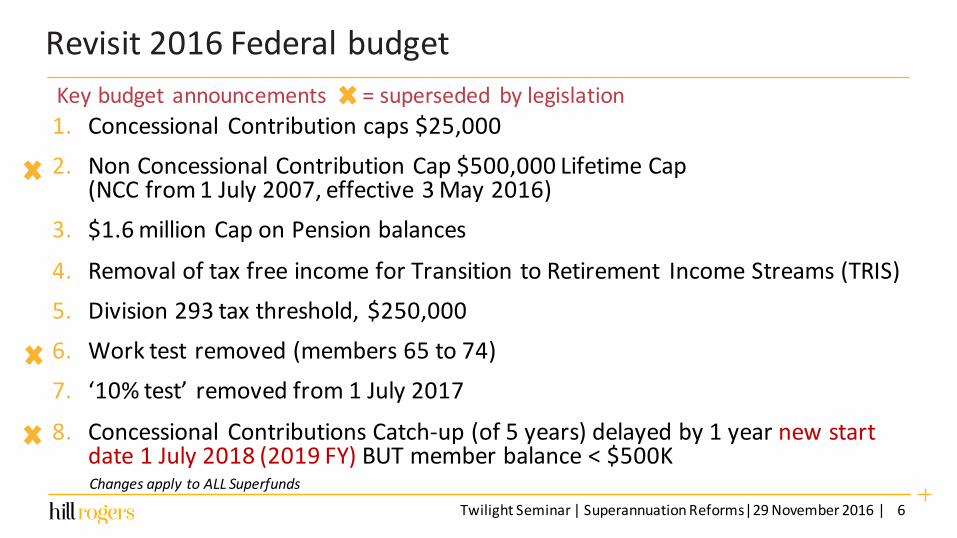

Revisit2016Federalbudget

1. Concessional Contributioncaps$25,0002. NonConcessionalContributionCap$500,000LifetimeCap

(NCCfrom1July2007,effective3May2016)3. $1.6millionCaponPensionbalances

4. RemovaloftaxfreeincomeforTransitiontoRetirement IncomeStreams(TRIS)5. Division293taxthreshold,$250,0006. Worktestremoved(members65to74)7. ‘10%test’removedfrom1July2017

8. Concessional ContributionsCatch-up(of5years)delayedby1yearnew startdate1July2018(2019FY) BUTmemberbalance˂$500KChangesapply toALLSuperfunds

6

Keybudgetannouncements =superseded bylegislation

TwilightSeminar|SuperannuationReforms|29November2016|

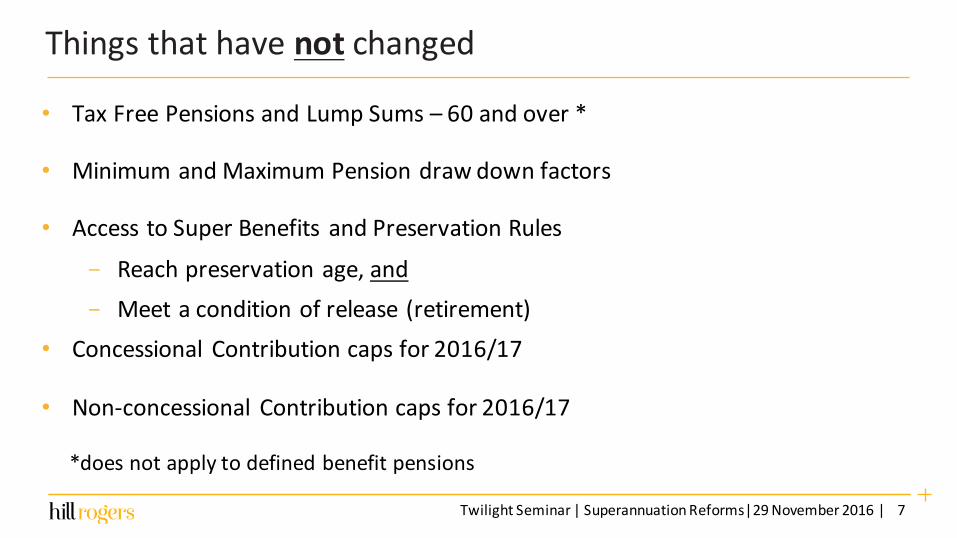

Thingsthathavenot changed

• TaxFreePensionsandLumpSums– 60andover*

• MinimumandMaximumPensiondrawdownfactors

• AccesstoSuperBenefits andPreservationRules

- Reachpreservationage,and- Meetaconditionofrelease(retirement)

• Concessional Contributioncapsfor2016/17

• Non-concessional Contributioncapsfor2016/17

*doesnotapplytodefinedbenefitpensions

TwilightSeminar|SuperannuationReforms|29November2016| 7

Non-concessionalcontributions

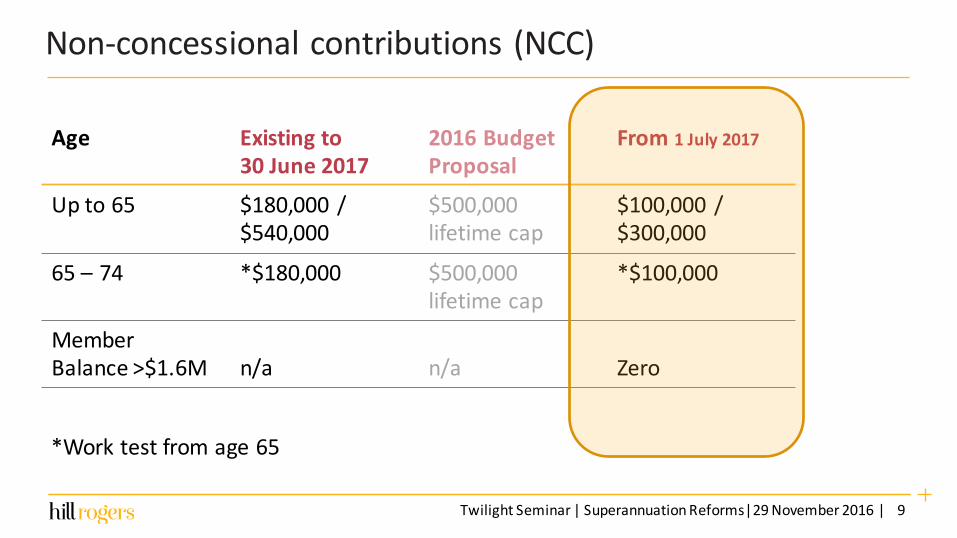

Non-concessionalcontributions(NCC)

9

Age Existingto30June2017

2016BudgetProposal

From1July2017

Up to65 $180,000 /$540,000

$500,000lifetime cap

$100,000/$300,000

65– 74 *$180,000 $500,000lifetimecap

*$100,000

MemberBalance˃ $1.6M n/a n/a Zero

*Worktestfromage65

TwilightSeminar|SuperannuationReforms|29November2016|

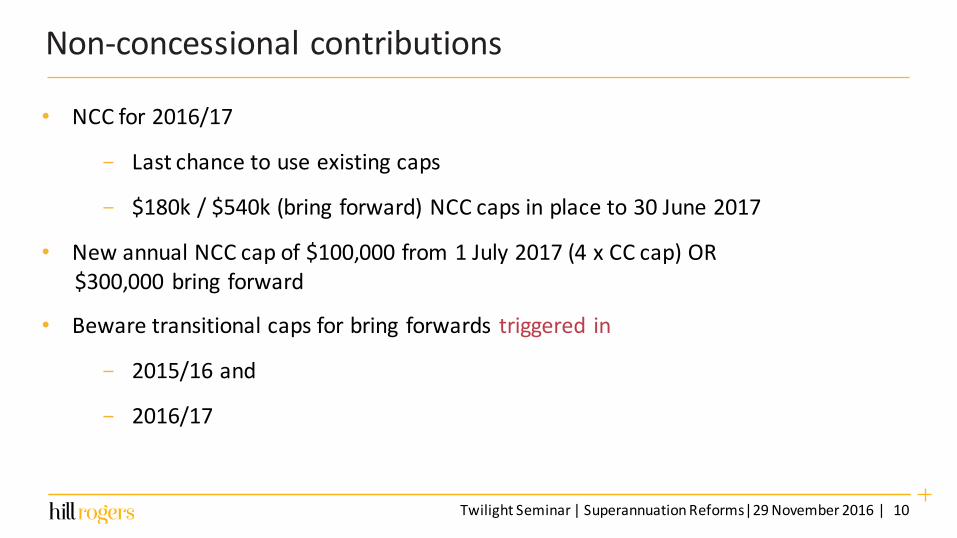

Non-concessionalcontributions

• NCCfor2016/17

- Lastchancetouseexistingcaps

- $180k/$540k(bring forward)NCCcapsinplaceto30June2017

• NewannualNCCcapof$100,000from1July2017(4xCCcap)OR$300,000bring forward

• Bewaretransitionalcapsforbring forwards triggered in

- 2015/16and

- 2016/17

10TwilightSeminar|SuperannuationReforms|29November2016|

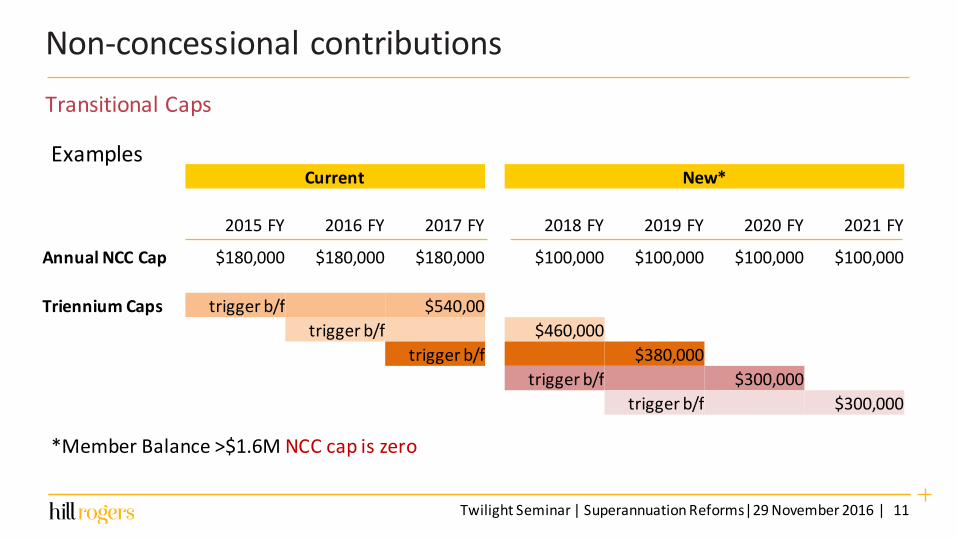

Non-concessionalcontributions

11

Current New*

2015FY 2016FY 2017FY 2018FY 2019FY 2020FY 2021FY

AnnualNCCCap $180,000 $180,000 $180,000 $100,000 $100,000 $100,000 $100,000

TrienniumCaps triggerb/f $540,00triggerb/f $460,000

triggerb/f $380,000triggerb/f $300,000

triggerb/f $300,000

Examples

*MemberBalance˃ $1.6M NCCcapiszero

TransitionalCaps

TwilightSeminar|SuperannuationReforms|29November2016|

Non-concessionalcontributions

• Totalsuperbalanceofmorethan$1.6M?

- Measuredatprevious30June

- Indexedsameas$1.6mtransferbalancecap(CPI,$100kincrements)

- For2017/18,NCCallowedifbalanceon30June2017is$1.6morless

• Ifapproaching$1.6m,bewarebringforwards…

TwilightSeminar|SuperannuationReforms|29November2016| 12

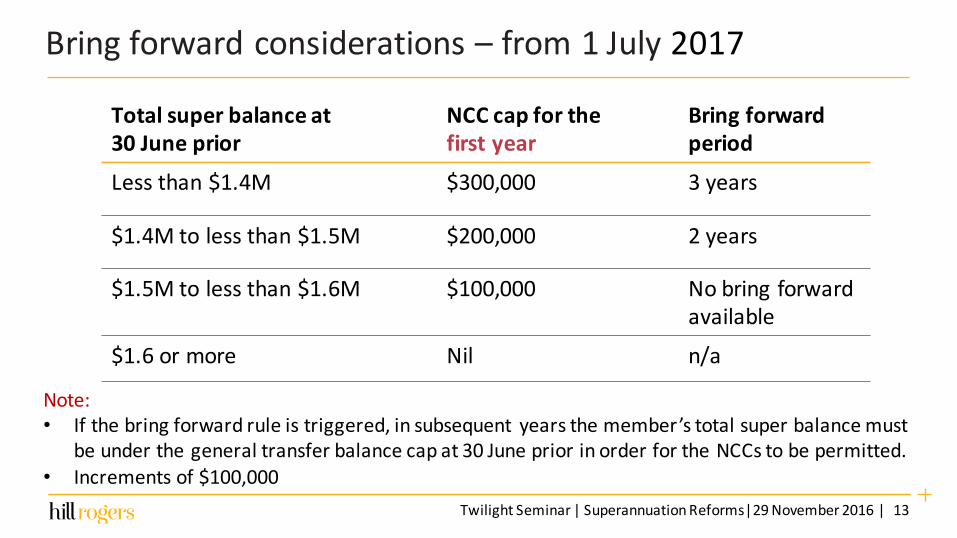

Bringforwardconsiderations– from1July2017

TwilightSeminar|SuperannuationReforms|29November2016| 13

Totalsuperbalanceat30Juneprior

NCCcapforthefirstyear

Bringforwardperiod

Lessthan $1.4M $300,000 3years

$1.4Mtolessthan$1.5M $200,000 2years

$1.5Mtolessthan$1.6M $100,000 Nobring forwardavailable

$1.6ormore Nil n/a

Note:• Ifthebringforwardruleistriggered,insubsequent yearsthemember’stotalsuperbalancemust

beunderthegeneraltransferbalancecapat30JunepriorinorderfortheNCCstobepermitted.• Incrementsof$100,000

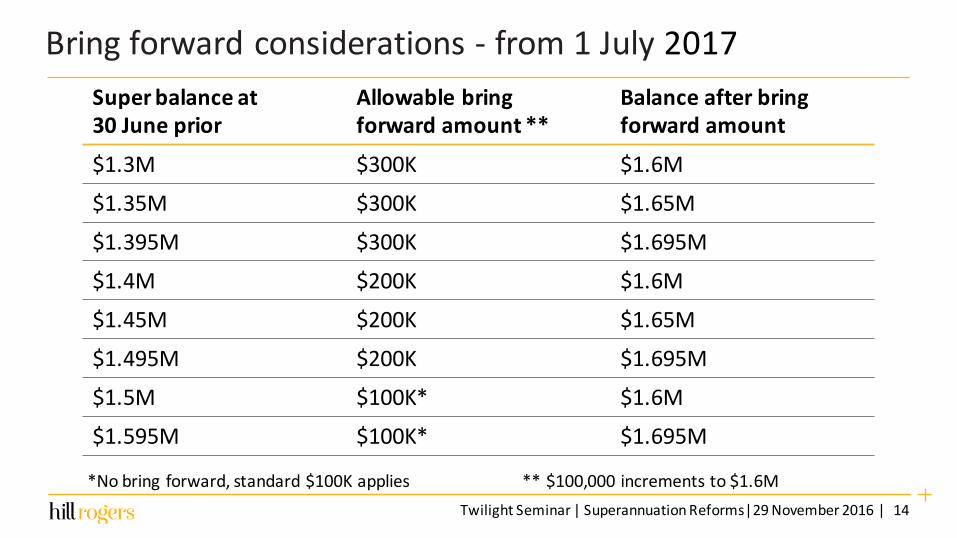

Bringforwardconsiderations- from1July2017

TwilightSeminar|SuperannuationReforms|29November2016| 14

Superbalanceat30Juneprior

Allowablebringforwardamount**

Balanceafterbringforwardamount

$1.3M $300K $1.6M

$1.35M $300K $1.65M

$1.395M $300K $1.695M

$1.4M $200K $1.6M

$1.45M $200K $1.65M

$1.495M $200K $1.695M

$1.5M $100K* $1.6M

$1.595M $100K* $1.695M

*Nobringforward,standard$100Kapplies**$100,000incrementsto$1.6M

Non-concessionalcontributions: items

• Bringforwardsplannedfor2016/2017– lastchance

• In-speciecontributionsalreadyintrain

• Contractedproperty:settlementsumfundedbyNCC

• UKpensiontransfersalreadyintrain

• Futurerecontributions

• LRBAs:dependentonlargeNCCforrepaymentorassetimprovement

Review

TwilightSeminar|SuperannuationReforms|29November2016| 15

Non-concessionalcontributions: items

TwilightSeminar|SuperannuationReforms|29November2016| 16

• Remember:disalloweddeductiblecontributionscount!

• ReimburseSMSFexpensespaidpersonally

• Bewareimprovements tofundassetsfor$0

• Obtainadvicebeforemakingcontributions

• Includeallsuperwhentesting$1.6Mbalance

WatchforinadvertentuseofNCCcap

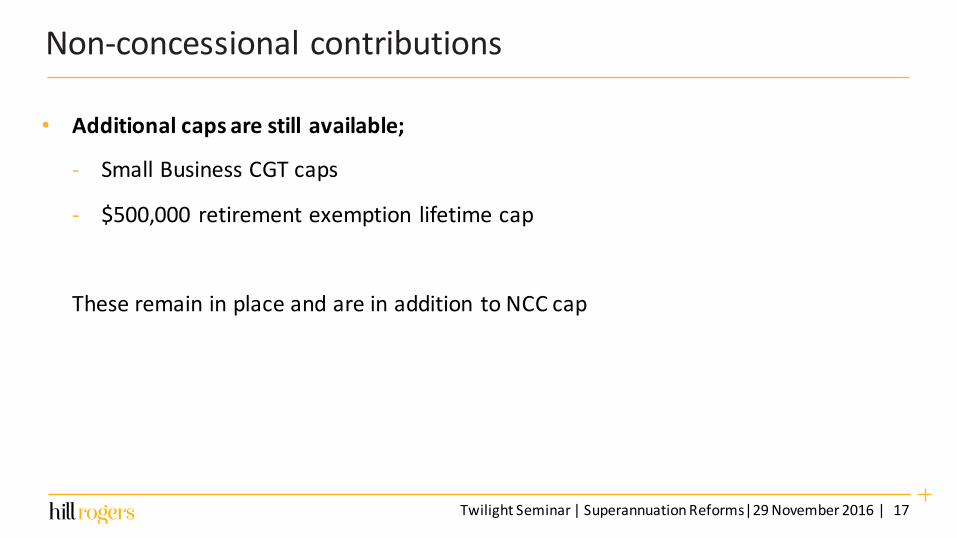

Non-concessionalcontributions

• Additionalcapsarestillavailable;

- SmallBusinessCGTcaps

- $500,000 retirementexemption lifetimecap

Theseremaininplaceandareinaddition toNCCcap

TwilightSeminar|SuperannuationReforms|29November2016| 17

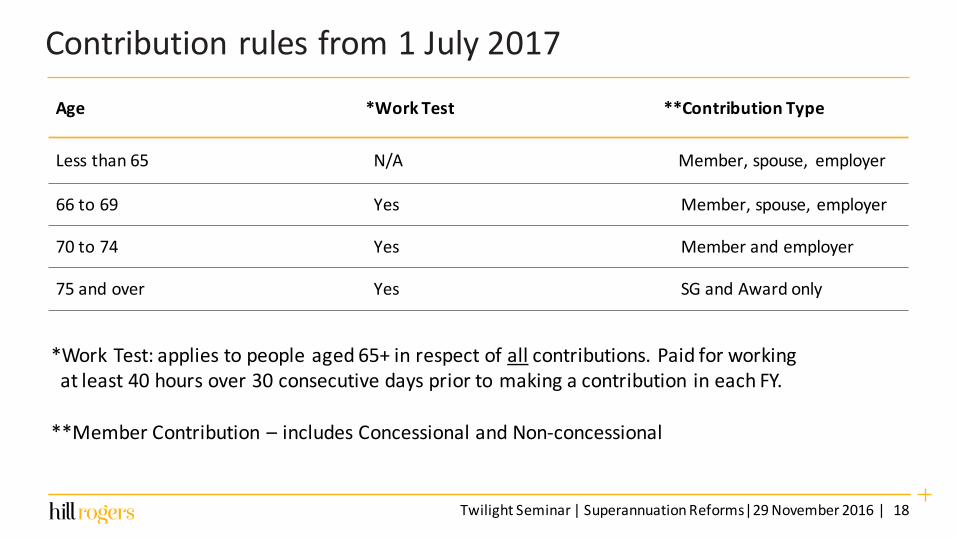

Contributionrulesfrom1July2017

TwilightSeminar|SuperannuationReforms|29November2016| 18

Age *WorkTest **ContributionType

Lessthan65 N/A Member,spouse, employer

66to69 Yes Member,spouse, employer

70to74 Yes Memberandemployer

75andover Yes SGandAwardonly

*WorkTest: appliestopeopleaged65+inrespectofall contributions.Paidforworkingatleast40hoursover30consecutivedayspriortomakingacontribution ineachFY.

**MemberContribution– includesConcessionalandNon-concessional

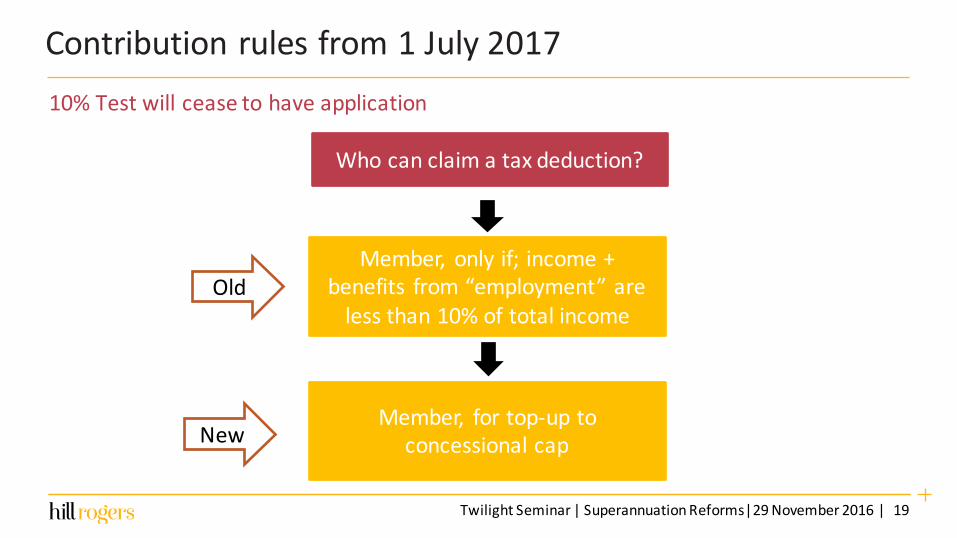

Contributionrulesfrom1July2017

TwilightSeminar|SuperannuationReforms|29November2016| 19

10%Testwillceasetohaveapplication

Whocanclaimataxdeduction?

Member, onlyif;income+benefits from“employment”arelessthan10%oftotalincome

Member, fortop-uptoconcessionalcap

Old

New

• 10%ruletoberemovedfrom1July2017

• Eligibletoclaimadeductionregardlessofemploymentcircumstances*

• Removesneedforsalarysacrificeagreements

• AllowsallindividualstomakeortopupCCtotheCCcap

• Deductionslimitedtoassessableincome

• Taxdeductionelectionprocessremainsunchanged(Sec290-160Notices)

*worktestfromage65

TwilightSeminar|SuperannuationReforms|29November2016| 20

Taxdeductionsforpersonalcontributions

Concessionalcontributions

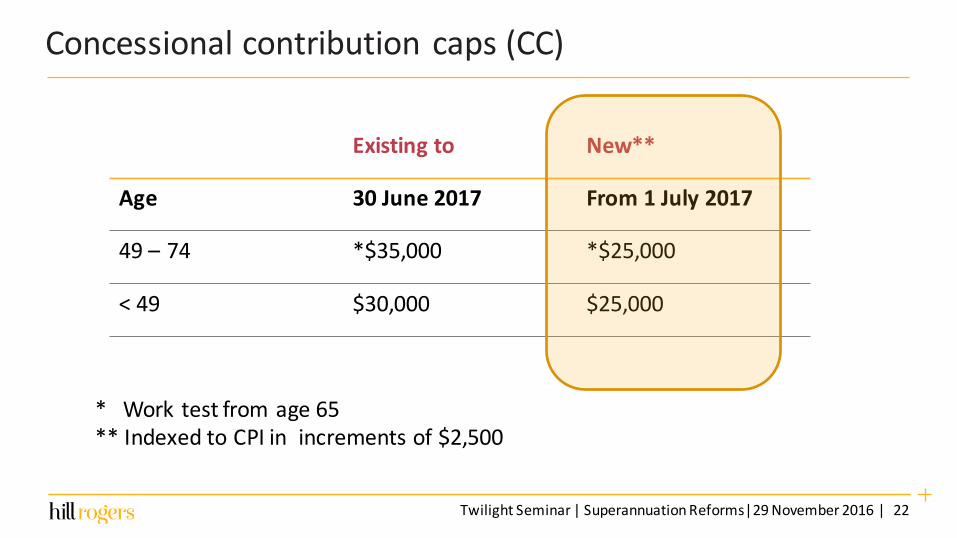

Concessionalcontributioncaps(CC)

TwilightSeminar|SuperannuationReforms|29November2016| 22

Existingto New**

Age 30June 2017 From1July2017

49 – 74 *$35,000 *$25,000

< 49 $30,000 $25,000

*Work testfromage65**IndexedtoCPIinincrementsof$2,500

TwilightSeminar|SuperannuationReforms|29November2016| 23

Allowingcatchupconcessionalcontributions

• Newandbeneficialchangeforclaimingsupercontributions

• Oldrulesto30June2017,‘useitorloseit’

• Newrules‘anaveragingtypearrangement’

• Allowsunusedamountstobecarriedforward

• UnusedportionofCCcapcarriedforwardonarolling5yearperiod

• Effectivefrom1July2018(2019/20firstcatch-upopportunity)

• Notabringforwardentitlement

• “Totalsuperannuationbalance”mustbelessthan$500Kat30Juneprior

• Mustapplyunusedamountsinorderfromtheearliestyeartothemostrecentyear

• Amountsnotusedafter5yearswillexpire

TwilightSeminar|SuperannuationReforms|29November2016| 24

Allowingcatchupconcessionalcontributions

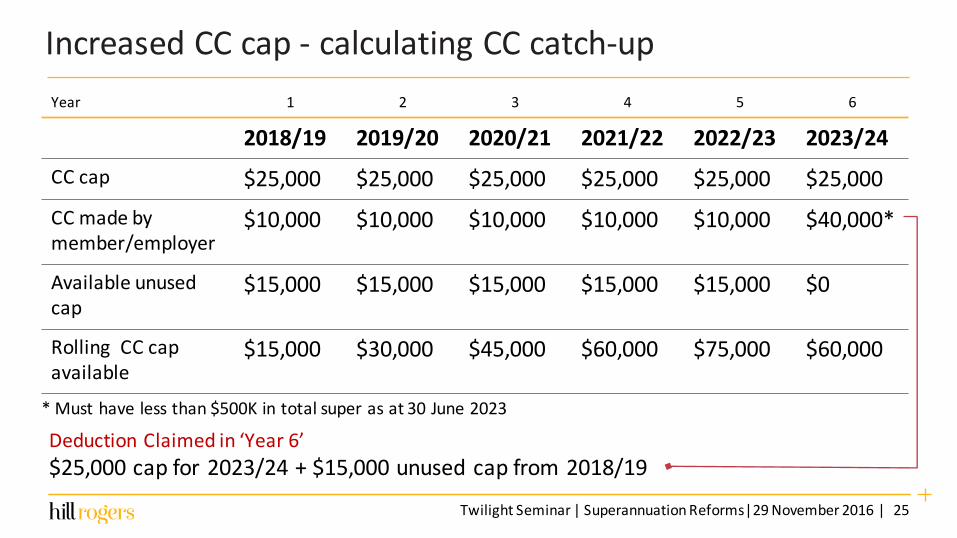

IncreasedCCcap- calculatingCCcatch-up

DeductionClaimedin‘Year6’$25,000capfor2023/24+$15,000unusedcapfrom2018/19

*Musthavelessthan$500Kintotalsuperasat30June2023

TwilightSeminar|SuperannuationReforms|29November2016| 25

Year 1 2 3 4 5 6

2018/19 2019/20 2020/21 2021/22 2022/23 2023/24CCcap $25,000 $25,000 $25,000 $25,000 $25,000 $25,000CCmadebymember/employer

$10,000 $10,000 $10,000 $10,000 $10,000 $40,000*

Availableunusedcap

$15,000 $15,000 $15,000 $15,000 $15,000 $0

RollingCCcapavailable

$15,000 $30,000 $45,000 $60,000 $75,000 $60,000

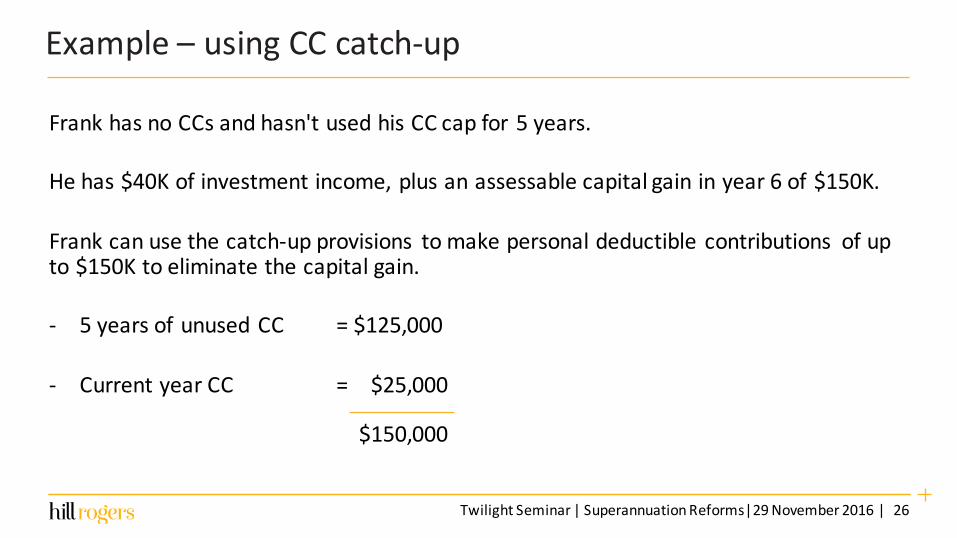

Example– usingCCcatch-up

FrankhasnoCCsandhasn'tusedhisCCcapfor5years.

Hehas$40Kofinvestmentincome,plusanassessablecapitalgaininyear6of$150K.

Frankcanusethecatch-upprovisions tomakepersonaldeductiblecontributions ofupto$150Ktoeliminatethecapitalgain.

- 5yearsofunusedCC =$125,000

- CurrentyearCC =$25,000

$150,000

TwilightSeminar|SuperannuationReforms|29November2016| 26

‘Catchup’unusedconcessionalcontributions

TwilightSeminar|SuperannuationReforms|29November2016| 27

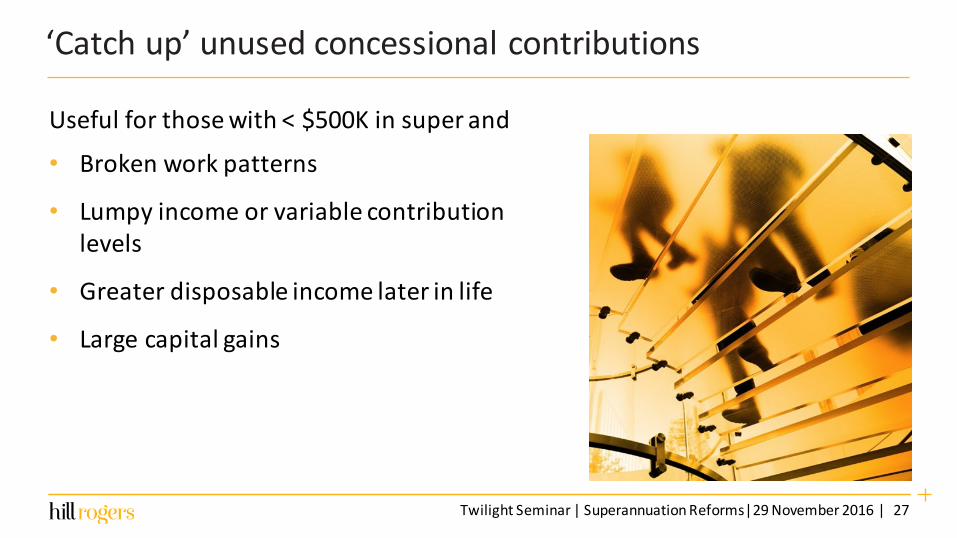

• Brokenworkpatterns

• Lumpyincomeorvariablecontributionlevels

• Greaterdisposableincomelaterinlife

• Largecapitalgains

Usefulforthosewith<$500Kinsuperand

Otherproposedcontributionschanges

TwilightSeminar|SuperannuationReforms|29November2016| 28

Division293Tax

• Additional15%paidonConcessionalContributions

• Effectistotaxconcessionalcontributionsat30%

• Incomethresholdtoreducefrom$300,000to$250,000

Effective1July2017

Pensionchanges

basedonwhatwecurrentlyunderstand

Pensionsandthe$1.6Mcap

• Itsallaboutlimitingthetaxfreeincomeinsidethesuperfund

• Nothingtodowithaccessingtaxfreesuperbymembers

Dispelling theconfusion!

TwilightSeminar|SuperannuationReforms|29November2016| 30

$1.6Mpensioncap:example

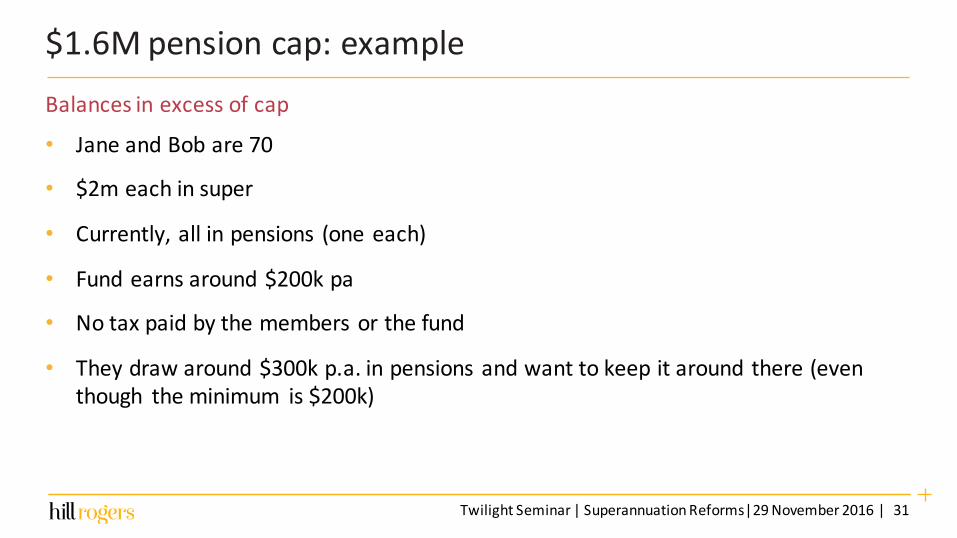

• JaneandBobare70

• $2meachinsuper

• Currently,allinpensions (oneeach)

• Fundearnsaround$200kpa

• Notaxpaidbythemembersorthefund

• Theydrawaround$300kp.a.inpensionsandwanttokeepitaround there(eventhough theminimum is$200k)

Balancesinexcessofcap

TwilightSeminar|SuperannuationReforms|29November2016| 31

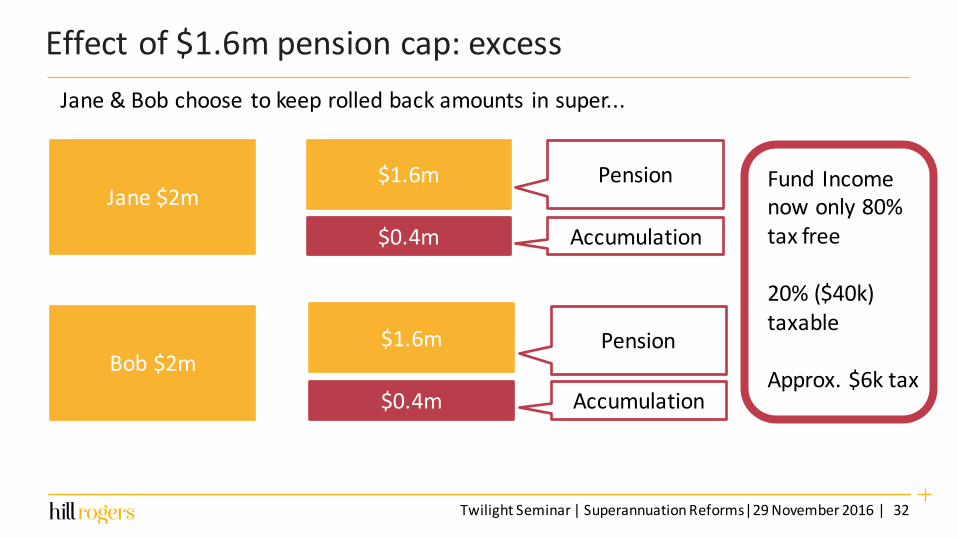

Effectof$1.6mpensioncap:excess

TwilightSeminar|SuperannuationReforms|29November2016| 32

Jane$2m

Bob$2m

$1.6m

$0.4m

Pension

Accumulation

$1.6m

$0.4m Accumulation

Pension

Fund Incomenowonly80%taxfree

20%($40k)taxable

Approx.$6ktax

Jane&Bobchoose tokeeprolledbackamounts insuper...

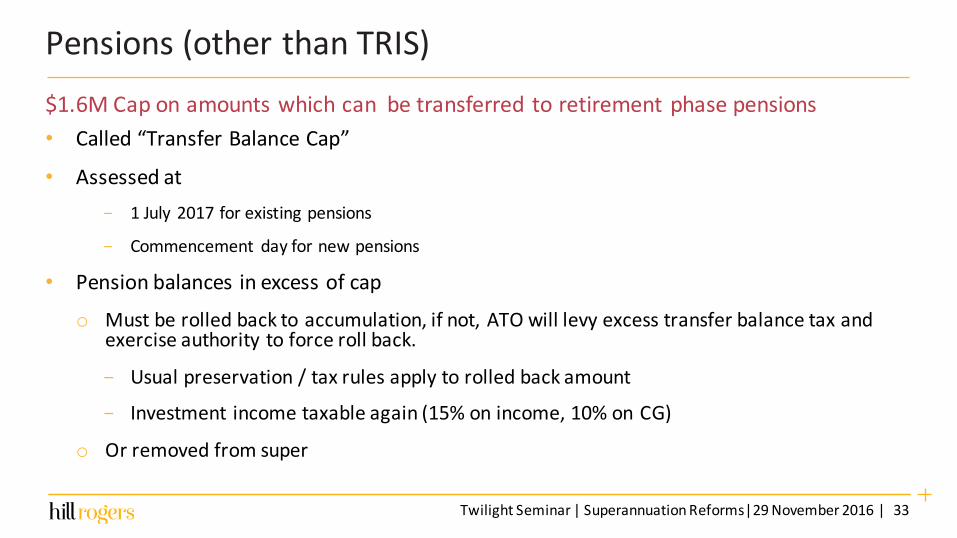

Pensions(otherthanTRIS)

• Called“TransferBalanceCap”

• Assessedat- 1July 2017forexistingpensions

- Commencement dayfornewpensions

• Pensionbalancesinexcessofcap

o Mustberolledbacktoaccumulation,ifnot,ATOwilllevyexcesstransferbalancetaxandexerciseauthoritytoforcerollback.

- Usualpreservation/taxrulesapplytorolledbackamount

- Investment incometaxableagain(15%onincome,10%onCG)

o Orremovedfromsuper

$1.6MCaponamountswhichcanbetransferred toretirementphasepensions

TwilightSeminar|SuperannuationReforms|29November2016| 33

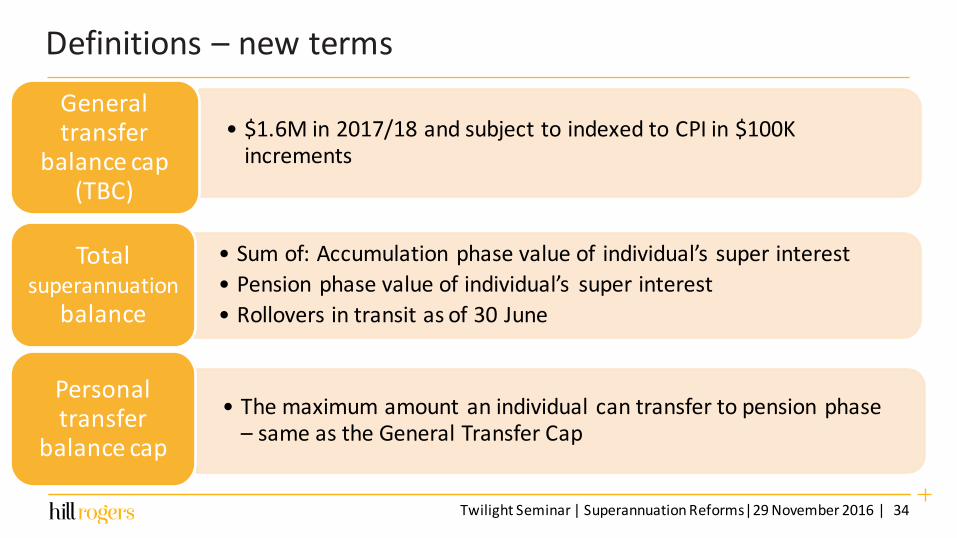

Definitions– newterms

TwilightSeminar|SuperannuationReforms|29November2016| 34

• Sumof:Accumulationphasevalueof individual’s superinterest• Pensionphasevalueofindividual’s superinterest• Rolloversintransitasof30June

Totalsuperannuation

balance

• $1.6Min2017/18andsubjecttoindexedtoCPIin$100Kincrements

Generaltransfer

balancecap(TBC)

• Themaximumamountanindividual cantransfertopensionphase– sameastheGeneralTransferCap

Personaltransfer

balancecap

$1.6mpensioncap

TwilightSeminar|SuperannuationReforms|29November2016| 35

• Earnings(or losses)onpensionbalanceafterassessmentdonotcounttowardscap

• IndexedtoCPI,in$100kincrements

• Proportionatemethodusedtodeterminehowmuch‘capspace’available

• Limitpermember,notperfund, notperaccount

• Trackmovements in/outofpension phasevia“TransferBalanceAccount”(likeabankaccountoraccounting ledger)

Effective1July2017

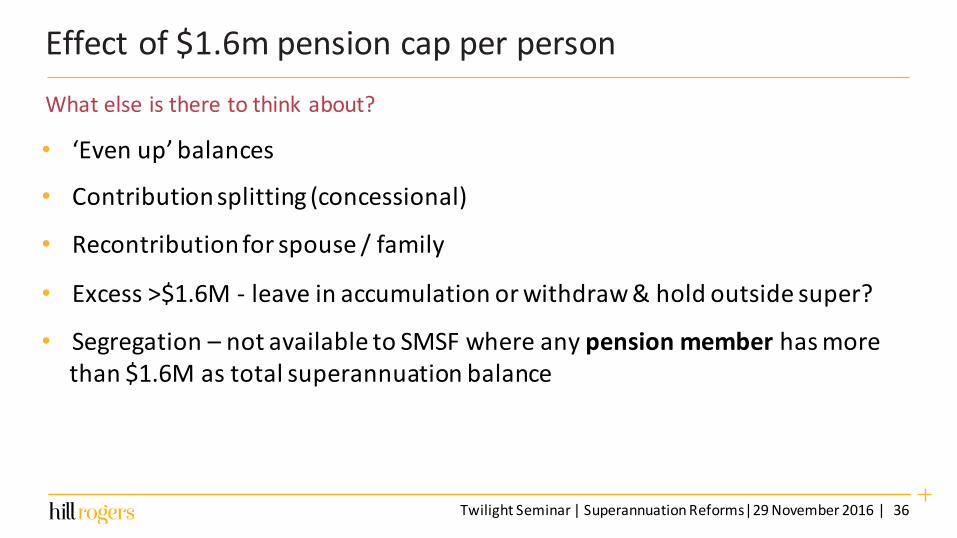

Effectof$1.6mpensioncapperperson

• ‘Evenup’balances

• Contributionsplitting(concessional)

• Recontributionforspouse/family

• Excess>$1.6M- leaveinaccumulationorwithdraw&holdoutsidesuper?

• Segregation– notavailabletoSMSFwhereanypensionmember hasmorethan$1.6Mastotalsuperannuationbalance

TwilightSeminar|SuperannuationReforms|29November2016| 36

Whatelseistheretothinkabout?

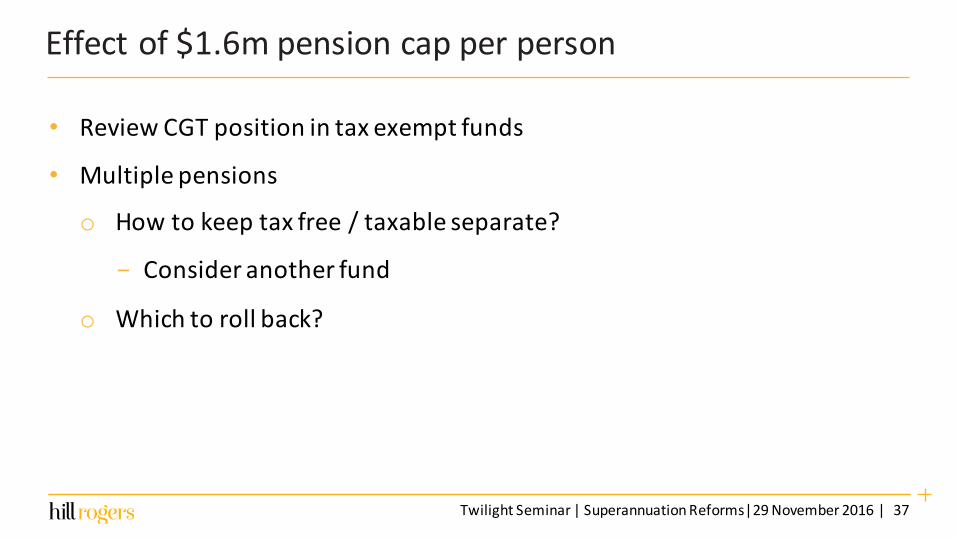

Effectof$1.6mpensioncapperperson

• ReviewCGTpositionintaxexemptfunds

• Multiplepensions

o Howtokeeptaxfree/taxableseparate?

- Consideranotherfund

o Whichtorollback?

TwilightSeminar|SuperannuationReforms|29November2016| 37

TRIS:removaloftaxconcessionsEffective1July2017– newandexistingTRISaccounts

TwilightSeminar|SuperannuationReforms|29November2016| 38

• Notaxexemptionon investmentincomegeneratedfromassetsunderpinning TRISbalance

• $1.6Mpensions capdoesnotapply

• NOCHANGEtotheeligibility rulestocommencetoTRIS

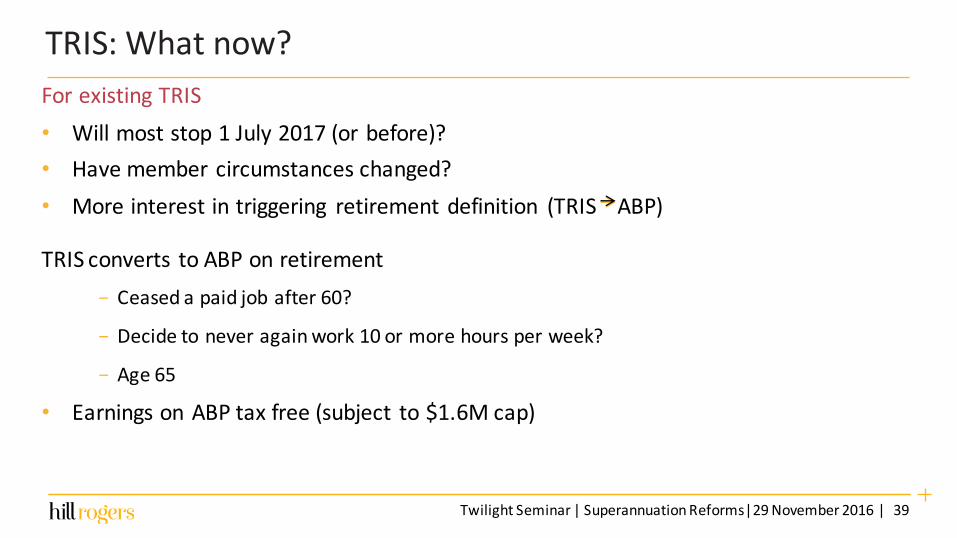

TRIS:Whatnow?

• Willmoststop1July2017(orbefore)?• Havemembercircumstanceschanged?• Moreinterestintriggering retirementdefinition (TRIS ABP)

TRISconverts toABPonretirement- Ceasedapaidjobafter60?

- Decidetoneveragainwork10ormorehoursperweek?

- Age65

• EarningsonABPtaxfree(subject to$1.6Mcap)

ForexistingTRIS

TwilightSeminar|SuperannuationReforms|29November2016| 39

Otherpensions

Definedbenefit&marketlinkedpensionsdealtwithdifferently

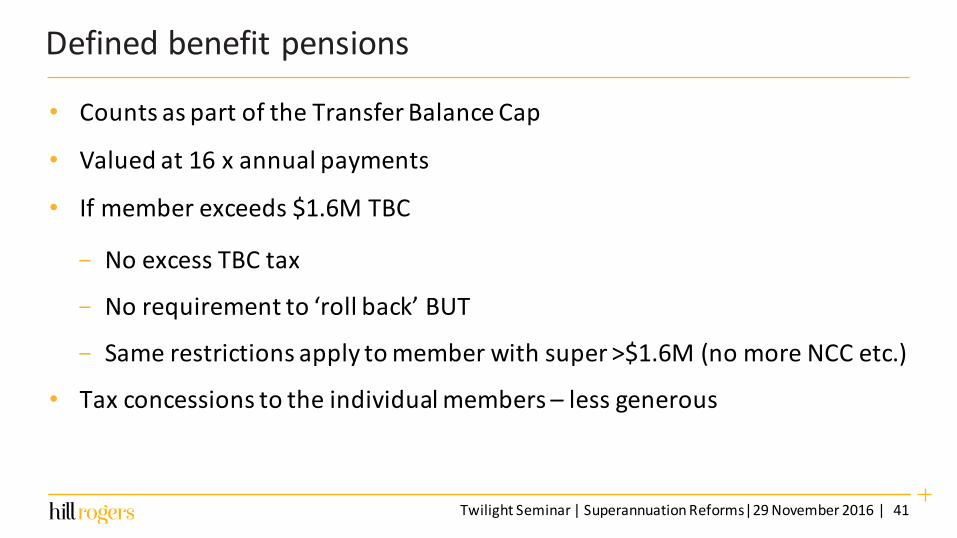

Definedbenefitpensions

• CountsaspartoftheTransferBalanceCap

• Valuedat16xannualpayments

• Ifmemberexceeds$1.6MTBC

- NoexcessTBCtax

- Norequirementto‘rollback’BUT

- Samerestrictionsapplytomemberwithsuper>$1.6M(nomoreNCCetc.)

• Taxconcessionstotheindividualmembers– lessgenerous

TwilightSeminar|SuperannuationReforms|29November2016| 41

Otherissues

Deathandsuper

Otherissues

• Whatwillhappenondeath

- Memberdrawingpensionattimeofdeath?

- Membernotyetinpensionattimeofdeath?

- Insuranceproceeds?

TwilightSeminar|SuperannuationReforms|29November2016| 43

Example– deathandsuper

DavidandJennyage75,eachhasa$2Mpensionbalance.Daviddies-• Undercurrentrules- David’spensionwould reverttoJenny

- Jennynowdrawing2pensions totalling$4M

- Taxfreeincomeinsuper

- Taxfreepensions toJenny

• Butfrom1July2017TBCrulesapply

TwilightSeminar|SuperannuationReforms|29November2016| 44

Example– deathandsuper

• At1July2017- DavidandJennyrestructuretheirpensions leaving$1.6Meachinpension&transferthe

balanceof($400K)outofsuper

- Reversiontospouse(ondeath)

BothhaveexhaustedtheirTBC

• Now1July2020- David’sbalance$800,000

- Jenny’sbalance$1.4M

Daviddies-

TwilightSeminar|SuperannuationReforms|29November2016| 45

Example– deathandsuper

• UndertheTBCrulesJennyhasalreadyusedher$1.6Mcap

TwilightSeminar|SuperannuationReforms|29November2016| 46

Option1

Option2

JennytakesDavid’ssuperinterestof$800,000asadeathbenefit lumpsum,cashedoutofthesuperfund.Alternatively;

Jennycommutes$800,000ofher$1.4MABPretaining itinaccumulationphaseandtakesadeathbenefit incomestreamof$800,000.

IfJennychoosesoption 2,shewouldnotneedtocashanyofDavid’ssuperoutofthesuperfund asadeathbenefit lumpsum.

Otherissues

Capitalgainstax

Capitalgainstax

Currentlaw• Capitalgainsrealisedonthedisposalofassetsthatunderpinpension

accounts(incl.TRIS)areexemptfromtax,eventhosegainsaccruedovermanyyears

Newrules• TRISsandthe$1.6mtransfercapwillconstrainfutureCGTrelief• Assetssoldin2016/17arenotaffectedbythenewrules

TwilightSeminar|SuperannuationReforms|29November2016| 48

CapitalgainstaxConceptually,thereliefisdesignedtoensurethatwhenanassetissoldafter1July2017:• capitalgainsthataccruedpost1Julywillbetaxable/taxexemptinaccordancewiththenew

rules;while

• capitalgainsbuiltupbefore1Julywillgetsomerecognitionthattheywouldhavebeenwhollyorpartlytaxexemptundertheoldrules

Choice- 2pathstoCGTrelief

• onlyappliestoassetsactuallyheldat9November2016(notnewassetsboughtsincethattime)

• “opt in”process,notanautomaticprocess

• The“optin”willbeirrevocable

TwilightSeminar|SuperannuationReforms|29November2016| 49

Takeaways

• NCCcaps

- Lastchancetotakeadvantageof$180,000/$540,000

- Bewaretransitionalcapsforbringforwardsbeyond30June2017

• CCcaps

- Allreducedto$25,000from1July2017

- Catch-upsforunusedCCcapavailablefor5years(balance<$500,000)

- Removalof10%testallowsallindividualstotop-upCC

TwilightSeminar|SuperannuationReforms|29November2016| 50

Takeaways

• TRISpension

- Fund incometaxedasifitwereinaccumulationphase

- Trigger retirementevent?StopTRIS?

• $1.6Mpension cap

- Limitstaxfreeincomeinfund

- Excessrolled– backtoaccumulation

- Allofyoursupercountstowardsthe$1.6Mcap

- Newlaws‘inplace’provideopportunity tomakedecisionsandactbefore1July2017

TwilightSeminar|SuperannuationReforms|29November2016| 51

Questions

t+61292325111f+61292337950www.hillrogers.com.au| [email protected]

Level5,1ChifleySquare,SydneyNSW2000 AustraliaGPOBox7066,SydneyNSW2001

H.R.P.HPtyLimitedpractisingasHillRogers|ABN12003718 518MemberofMorsion KSi,anassociationofglobal independentaccountingfirms.Liability limitedbyaschemeapprovedunderProfessional StandardsLegislation.

Disclaimer:HillRogersAdvisory PtyLtdThe material contained in this publ ication is general commentary only fordistribution to cl ients of Hi ll Roger s. None of the material i s, or shou ld beregarded as persona l or financial product advice. Accordingly , no per sonshould rely onany of the contents of thispublication without f irst obtain ingspecific advice from Hil lRogers. Every effort has been made t oen sure thatthe content is accurate, however it is not intended to be a completedescription of the matter s described. Hil l Roger s, its Pr incipals and agentsaccept no respon sib ility to any per son who actsor re lies in any way on anyof the material without first obtaining such specific advice.

H.R.P.HPtyLimitedpractisingasHillRogers|ABN12003718518MemberofMorison KSi,anassociationofglobal independentaccountingfirms.Liability limitedbyaschemeapprovedunderProfessional StandardsLegislation.