Embed Size (px)

Citation preview

Deutsche Bank

Systematic M&A Arbitrage

April 9, 2016

Deutsche Bank does and seeks to do business with companies covered in its research reports. Thus, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. DISCLOSURES AND ANALYST CERTIFICATIONS ARE LOCATED IN APPENDIX 1. MICA(P) 072/04/2012

Global Quantitative Strategy

Yin Luo, CFA ▪ 212 250 8983 ▪ [email protected]

Managing Director & Global Head of Quantitative Strategy

Deutsche Bank

Yin Luo, CFA ▪ 1.212.250.8983 ▪ [email protected]

#1 Ranked Global Quantitative & Strategy Team

Source: gettyimages.com, Deutsche Bank Quantitative Strategy

research surveys: America #1; Europe #1; Asia #1; Fixed Income quant research #1

The US team is also top ranked in the “Accounting & Tax Policy” and” Portfolio Strategy” sectors

All our research can be accessed at: http://eqindex.db.com/gqs

1

New York

— Javed Jussa

US Head of Quantitative Strategy

— Miguel Alvarez

— Sheng Wang

— Gaurav Rohal, CFA

— Zheyin (George) Zhao

— Allen Wang

— David Elledge

Quant IT

— Sergei Khomiouk

Chile Offshore Support

— Nicolas Magunacelaya

— Joaquin Gonzalez

London

— Spyros Mesomeris, PhD

European Head of Quantitative Strategy

— Christian Davies

— Jacopo Capra

— Shuo (Alison) Qu, PhD

— Paul Ward

— James Osiol

Quant FX/Commodities

— Caio Natividade

— Vivek Anand

Hong Kong

— Khoi LeBinh

Asian Head of Quantitative Strategy

— Vincent Zoonekynd, PhD

— Ada Lau

— Hemant Sambatur

— Jiazi Tang

— Yin Luo, CFA

Global Head of Quantitative Strategy

Deutsche Bank

Yin Luo, CFA ▪ 1.212.250.8983 ▪ [email protected]

04/04/2016 15:40:54 2010 DB Blue template

— Our data set covers 40,000 M&A deals over 25 years of

history. We use merger types and moods to measure

post-announcement drift.

— We provide a model predicting the probability of a merger

going through: the MAS model.

— A multifactor model provides the expected alpha of each

merger: the MAA model.

— We find certainly characteristics of the deal have

significant impact on the duration of the transaction: the

MAD model.

— Combining the MAA, MAS and the expected duration

(MAD model) of a deal, we deliver a systematic M&A

portfolio with an annualized return of 15% and a Sharpe

ratio of 1.6x.

Abstract

2

Performance of the systematic M&A (SMA) strategy

Source: Thompson Reuters, Compustat, IBES, Russell, S&P, Deutsche Bank Quantitative Strategy

0

2

4

6

8

10

12Russell 3000

Naïve M&A strategy

Final M&A portfolio

Deutsche Bank

Yin Luo, CFA ▪ 1.212.250.8983 ▪ [email protected]

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Other Cash only Stock only Cash and stock

Source: Thompson Reuters, Compustat, IBES, Russell, S&P, Deutsche Bank Quantitative Strategy

Thomson Reuters’ Deals M&A database Number of deals of each type Percentage of each type

Percentage of each style Percentage of each mood

3

0

500

1000

1500

2000

2500

Other Cash only Stock only Cash and stock

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Stake purchases Undisclosed dollar value

Disclosed dollar value Self tenders, recaps

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Friendly Neutral Hostile Not appl. Unsolic.

Deutsche Bank

Yin Luo, CFA ▪ 1.212.250.8983 ▪ [email protected]

0.97

0.98

0.99

1.00

1.01

1.02

1.03

1.04

1.05

Deal goes through Deal fails

Post-announcementdrift

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

US Mergers International Mergers

Source: Thompson Reuters, Compustat, IBES, Russell, S&P, Deutsche Bank Quantitative Strategy

Other important deal features Percentage US vs. international Average final control sought

Distribution of deal success/failure by deal age Average profit of successful deals

4

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Percentage of deals going through

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1.0

Pro

po

rtio

n o

f m

erg

ers

go

ing

thro

ugh

Announcement year

Average: 61%

drops 20% during crisis

0.00

0.01

0.02

0.03

0.04

0.05

0.06

0.07

0.08

0.09

0.10

Fre

qu

en

cy

Days until deal is cancelled/closed

Deal closed successfully Deal withdrawn

Pre- and post-announcement drift

0.80

0.85

0.90

0.95

1.00

1.05

1.10

1.15

1.20

1.25

1.30

Deal goes through Deal fails

Pre-announcementdrift

Announcement jump

Deutsche Bank

Yin Luo, CFA ▪ 1.212.250.8983 ▪ [email protected]

0.0 0.1 0.2 0.3 0.4 0.5 0.6 0.7 0.8

Month

Merton's distance to default

Price-to-52 week high

Normalized abnormal volume

Target price implied return

Return on invested capital (ROIC)

Operating earnings yield, trailing 12M, Basic

Recommendation, mean

Earnings yield, FY0

Expected dividend yield

Asset turnover

Skewness, 1Y daily

12M-1M price return

Total return, 12M

Price-to-operating EPS, trailing 12M, Basic

# of days to cover short

Return on net operating assets (RNOA)

Altman's z-score

Price-to-sales, trailing 12M

Earnings yield x IBES 5Y growth

IBES FY1 EPS up/down ratio, 1M

Barry ratio

Factor strength

Fact

or

nam

e

5

Factor strength in predicting merger success (red = dec. blue = inc.)

— A logit model predicts eventual success of deal each month. This is done on the most up-to-date information set

of that month over the point-in-time population of merger targets to avoid any look ahead bias.

— Fully dynamic. Probability reflects both the age of the deal, and its deteriorating or improving fundamental

characteristics.

Dynamic prediction of M&A success: the MAS model

Factor strength evolution over time

Source: Thompson Reuters, Compustat, IBES, Russell, S&P, Deutsche Bank Quantitative Strategy

-1.0

-0.8

-0.6

-0.4

-0.2

0.0

0.2

0.4

0.6

Fact

or

Stre

ngt

h

Calibration year (expanding window)

Month

Merton's distance to default

Price-to-52 week high

Normalized abnormal volume

Target price implied return

Return on invested capital (ROIC)

Operating earnings yield, trailing 12M, Basic

Recommendation, mean

Earnings yield, FY0

Expected dividend yield

Deutsche Bank

Yin Luo, CFA ▪ 1.212.250.8983 ▪ [email protected]

MAS model with M&A type, style and mood

6

The impact of deal type, style and mood on the transaction success probability

Other useful factors

— Factors such as deal type, style, and mood are not included in the MAS model, because these factors may

change over time and are sometimes backfilled, which leads to potential look-ahead bias.

— It is interesting to see that deals with undisclosed value, hostile takeovers, and unsolicited transactions have

much higher failure rates.

Source: Thompson Reuters, Compustat, IBES, Russell, S&P, Deutsche Bank Quantitative Strategy

-5

-4

-3

-2

-1

0

1

Deutsche Bank

Yin Luo, CFA ▪ 1.212.250.8983 ▪ [email protected]

MAS performance

— Bold range of predictions as the model

commonly boasts out-of-sample convictions

ranging from 10% to 90%

— Accurate predictions where the predicted

probability matches the out-of-sample frequency

of success

— Positive alpha as screening out deals likely to fail

improves merger arbitrage performance

7

Estimated vs realized success frequencies Performance for above and below median probability of success

Distribution of MAS predictions

Source: Thompson Reuters, Compustat, IBES, Russell, S&P, Deutsche Bank Quantitative Strategy

0

200

400

600

800

1000

1200

1400

1600

Nu

mb

er

of

dat

a p

oin

ts

Estimated probability of success

y = 0.8809x + 0.1554R² = 0.9493

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

0.90

1.00

0.00 0.20 0.40 0.60 0.80 1.00

Re

aliz

ed

fre

qu

en

cy o

f su

cce

ss

Estimated probability of success

0.96

0.97

0.98

0.99

1

1.01

1.02

1.03

low probability of success high probability of success

Deutsche Bank

Yin Luo, CFA ▪ 1.212.250.8983 ▪ [email protected]

0 0.05 0.1 0.15 0.2 0.25 0.3 0.35 0.4 0.45 0.5

Mood: Hostile

Mood: Not Appl.

month

Type: Cash only

Price-to-52 week high

Return on invested capital (ROIC)

Return on Asset

Valuation spread

80

90

100

110

120

130

140

150

160

170

1 2 3 4 5 6 7 8 9 10 11 12

Exp

ect

ed

re

mai

nin

g d

ura

tio

n in

day

s

Age of deal in months

-0.6

-0.5

-0.4

-0.3

-0.2

-0.1

0.0

0.1

0.2

1 2 3 4 5 6 7 8 9 10 11 12

Z-sc

ore

fac

tor

valu

e

Age of deal in months

Price-to-52 week low YoY change in # of shares outstanding

IBES 5Y EPS growth Price to book ratio

Long-term debt/equity

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

1 2 3 4 5 6 7 8 9 10 11 12

Ave

rage

pro

bab

ility

of

goin

g th

rou

gh

Age of deal in months

Source: Thompson Reuters, Compustat, IBES, Russell, S&P, Deutsche Bank Quantitative Strategy

The impact of age: the deal duration MAD model Probability of success as a function of age Fundamentals deteriorate as the deal ages

Remaining duration as a function of deal age – four-month is the

critical value Factor coefficients for a Cox survival model (red = long; blue = short)

8

Deutsche Bank

Yin Luo, CFA ▪ 1.212.250.8983 ▪ [email protected]

The takeover target universe

9

M&A universe outperforms the market over the long run

Plain vanilla risk arbitrage strategy as our benchmark

— All M&A targets that are in the Russell 3000 universe at the

announcement date

— Close our trade when the deal closes successfully or when is withdrawn,

with a maximum holding period of one year

— Monthly rebalance – a stock enters the M&A universe at the closest month

end after its announcement date

— Long only, no leverage, fully invested

Coverage of the M&A universe

0

50

100

150

200

250

1

10

100

Russell 3000

M&A universe

Source: Thompson Reuters, Compustat, IBES, Russell, S&P, Deutsche Bank Quantitative Strategy

Sharpe ratio

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1.0

Russell 3000 M&A universe

Deutsche Bank

Yin Luo, CFA ▪ 1.212.250.8983 ▪ [email protected] 10

Annualized return

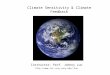

— For M&A transactions involving acquirer’s stocks, a long-only strategy takes significant unnecessary risk. For

the stock deals, risk arbitrageurs would long the target company shares and short the acquire company

stocks. The hedge ratio on the short side is calculated based on the deal structure.

— Similar to the naïve long-only risk arbitrage strategy, we weight each deal by the market cap of the target

companies at every month end. For the stock deals in which the acquire companies are also in the Russell

3000 iIndex, we short the acquirer company using the appropriate hedge ratio. If a stock deal closes

successfully or is withdrawn within a month, both the long and the short positions are closed intra month, on

the same day. Otherwise, the positions are rebalanced at the end of each month.

A naïve long/short risk arbitrage strategy

Sharpe ratio

Source: Thompson Reuters, Compustat, IBES, Russell, S&P, Deutsche Bank Quantitative Strategy

0%

2%

4%

6%

8%

10%

12%

14%

16%

Long only Long/short

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1.0

Long only Long/short

Deutsche Bank

Yin Luo, CFA ▪ 1.212.250.8983 ▪ [email protected]

-80%

-60%

-40%

-20%

0%

20%

40%

60%

80%Rank IC

12 month average

Avg = 7.60%Min = -47%Max = 64%Avg/Std.Dev.= 0.41

0%

2%

4%

6%

8%

10%

12%

14%

16%

1 2 3 4 5 6 7 8 9 10 11 12 M&A

Source: Thompson Reuters, Compustat, IBES, Russell, S&P, TAQ, Deutsche Bank Quantitative Strategy

Multifactor M&A alpha: the MAA model Common quant factors also predict the returns of takeover targets (IC) The MAA model strongly predicts the future return of targets (IC)

Forecasting power as a function of forecasting horizon Investing in deals with strong alpha based on the MAA model

11

0%

1%

2%

3%

4%

5%

6%

7%

0

1

2

3

4

5

6

7

8

9M&A universe

MAS model

MAA model

Deutsche Bank

Yin Luo, CFA ▪ 1.212.250.8983 ▪ [email protected] 12

Average bias statistic: realized future risk / historical volatility

— Equity risk model (i.e., the covariance matrix) is generally estimated based on historical data (returns and factors).

— For takeover target companies, however, the future risk is more of a binary issues – if the deals close on their

original terms, the risk tends to be fairly minimal; on the other hand, if the deals break up, the downside risk is

tremendous.

— Our MAS model predicts deal success probability and can significantly improve deal risk estimation.

— We use the bias statistic to measure the accuracy of our risk prediction. The bias statistic is the ratio of realized risk

and predicted risk. A perfect risk model should have a bias statistic close to 1.0.

Using the MAS model to improve deal risk estimation

The higher the deal success probability, the lower realized risk,

@COR(model scores, bias statistic)

Source: Thompson Reuters, Compustat, IBES, Russell, S&P, Deutsche Bank Quantitative Strategy

0.00

0.50

1.00

1.50

2.00

2.50M&A universe

Russell 3000

-80%

-60%

-40%

-20%

0%

20%

40%

60%

80%

MAS model MAA model

)exp( ,,, tititi pVolNewVol

Deutsche Bank

Yin Luo, CFA ▪ 1.212.250.8983 ▪ [email protected]

Source: Thompson Reuters, Compustat, IBES, Russell, S&P, Deutsche Bank Quantitative Strategy

More sophisticated portfolio construction technique – risk parity

Sharpe ratio Max drawdown

13

— More sophisticated portfolio construction techniques can further improve performance

— Equally weighted MAA: in this portfolio, we simply equally weight all takeover targets ranked in the top

half by the MAA model;

— Inverse volatility: for the same target stocks, we apply the inverse volatility weighting scheme;

— Risk parity – sample covariance matrix: we weight the same target firms, using the risk parity algorithm.

The covariance matrix is based on sample return data.

— Risk parity – MAS matrix: we weight the same target companies, using the risk parity scheme.

However, we adjust the covariance matrix using our MAS model.

— Weighting stocks by inverse volatility helps, while taking into account of correlation (risk parity) further

improves performance. Lastly, our MAS-adjusted covariance matrix boosts return and cuts down risk.

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

Equally weighted MAA

Inverse volatility Risk parity - sample covariance matrix

Risk parity - MAS matrix

-50%

-45%

-40%

-35%

-30%

-25%

-20%

-15%

-10%

-5%

0%

Equally weighted MAA

Inverse volatility Risk parity - sample covariance matrix

Risk parity - MAS matrix

Deutsche Bank

Yin Luo, CFA ▪ 1.212.250.8983 ▪ [email protected]

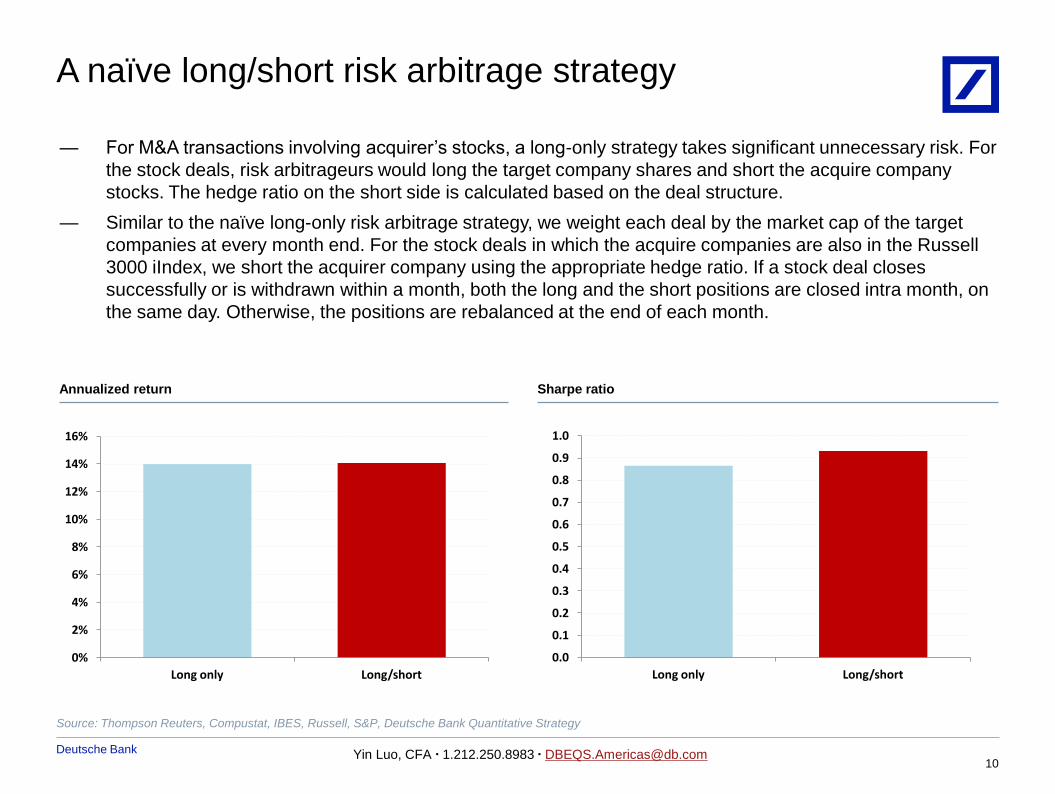

The final systematic M&A (SMA) portfolio

— Start with the universe of targets of all US target

companies in the Russell 3000 index

— Use the MAA model and adjust the expected alpha by

the expected duration from the MAD model for a

duration-adjusted alpha signal

— Use the MAS model to predict the deal success

probability, which is then used to improve our

covariance matrix estimation

— Finally, we apply a mean-variance optimization to

construct our systematic M&A arbitrage (SMA) portfolio

14

Max drawdown

Sharpe ratio

Annualized returns

Source: Thompson Reuters, Compustat, IBES, Russell, S&P, Deutsche Bank Quantitative Strategy

www ''

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

An

nu

aliz

ed

Sh

arp

e

Strategies

0%2%4%6%8%

10%12%14%16%

An

nu

aliz

ed

me

an r

etu

rns

Strategies -70%

-60%

-50%

-40%

-30%

-20%

-10%

0%M

axim

um

dra

wd

ow

n

Strategies

Deutsche Bank

Yin Luo, CFA ▪ 1.212.250.8983 ▪ [email protected]

04/04/2016 15:40:58 2010 DB Blue template

Appendix 1 Important Disclosures Additional Information Available upon Request

DOUBLE CLICK IN

For disclosures pertaining to recommendations or estimates made on securities other than the primary subject of this research, please see the

most recently published company report or visit our global disclosure look-up page on our website at

http://gm.db.com/ger/disclosure/DisclosureDirectory.eqsr

15

Deutsche Bank

Yin Luo, CFA ▪ 1.212.250.8983 ▪ [email protected]

Special Disclosures N/A

Analyst Certification

The views expressed in this report accurately reflect the personal views of the undersigned lead analyst(s). In addition, the

undersigned lead analyst(s) has not and will not receive compensation for providing a specific recommendation or view in this report.

[Yin Luo]

Hypothetical Disclaimer

Backtested, hypothetical or simulated performance results discussed herein have inherent limitations. Unlike an actual performance

record based on trading actual client portfolios, simulated results are achieved by means of the retroactive application of a backtested

model itself designed with the benefit of hindsight. Taking into account historical events the backtesting of performance also differs

from actual account performance because an actual investment strategy may be adjusted any time, for any reason, including a

response to material, economic or market factors. The backtested performance includes hypothetical results that do not reflect the

reinvestment of dividends and other earnings or the deduction of advisory fees, brokerage or other commissions, and any other

expenses that a client would have paid or actually paid. No representation is made that any trading strategy or account will or is likely

to achieve profits or losses similar to those shown. Alternative modeling techniques or assumptions might produce significantly different

results and prove to be more appropriate. Past hypothetical backtest results are neither an indicator nor guarantee of future returns.

Actual results will vary, perhaps materially, from the analysis.

16

Deutsche Bank

Yin Luo, CFA ▪ 1.212.250.8983 ▪ [email protected]

Regulatory Disclosures 1. Important Additional Conflict Disclosures Aside from within this report, important conflict disclosures can also be found at https://gm.db.com/equities under the “Disc losures Lookup” and “Legal” tabs. Investors are strongly encouraged to review this information before investing.

2. Short-Term Trade Ideas Deutsche Bank equity research analysts sometimes have shorter-term trade ideas (known as SOLAR ideas) that are consistent or inconsistent with Deutsche Bank’s existing longer term ratings. These trade ideas can be found at the SOLAR link at http://gm.db.com.

3. Country-Specific Disclosures Australia & New Zealand: This research, and any access to it, is intended only for "wholesale clients" within the meaning of the Australian Corporations Act and New Zealand Financial Advisors Act respectively. EU countries: Disclosures relating to our obligations under MiFiD can be found at http://www.globalmarkets.db.com/riskdisclosures. Japan: Disclosures under the Financial Instruments and Exchange Law: Company name - Deutsche Securities Inc. Registration number - Registered as a financial instruments dealer by the Head of the Kanto Local Finance Bureau (Kinsho) No. 117. Member of associations: JSDA, Type II Financial Instruments Firms Association, The Financial Futures Association of Japan, Japan Investment Advisers Association. Commissions and risks involved in stock transactions - for stock transactions, we charge stock commissions and consumption tax by multiplying the transaction amount by the commission rate agreed with each customer. Stock transactions can lead to losses as a result of share price fluctuations and other factors. Transactions in foreign stocks can lead to additional losses stemming from foreign exchange fluctuations. "Moody's", "Standard & Poor's", and "Fitch" mentioned in this report are not registered credit rating agencies in Japan unless “Japan” or "Nippon" is specifically designated in the name of the entity. Russia: This information, interpretation and opinions submitted herein are not in the context of, and do not constitute, any appraisal or evaluation activity requiring a license in the Russian Federation.

17

Deutsche Bank

Yin Luo, CFA ▪ 1.212.250.8983 ▪ [email protected]

Global Disclaimer The information and opinions in this report were prepared by Deutsche Bank AG or one of its affiliates (collectively "Deutsche Bank"). The information herein is believed to be reliable and has been obtained from public sources believed to be reliable. Deutsche Bank makes no representation as to the accuracy or completeness of such information.

Deutsche Bank may engage in securities transactions, on a proprietary basis or otherwise, in a manner inconsistent with the view taken in this research report. In addition, others within Deutsche Bank, including strategists and sales staff, may take a view that is inconsistent with that taken in this research report.

Opinions, estimates and projections in this report constitute the current judgement of the author as of the date of this report. They do not necessarily reflect the opinions of Deutsche Bank and are subject to change without notice. Deutsche Bank has no obligation to update, modify or amend this report or to otherwise notify a recipient thereof in the event that any opinion, forecast or estimate set forth herein, changes or subsequently becomes inaccurate. Prices and availability of financial instruments are subject to change without notice. This report is provided for informational purposes only. It is not an offer or a solicitation of an offer to buy or sell any financial instruments or to participate in any particular trading strategy. Target prices are inherently imprecise and a product of the analyst judgement.

As a result of Deutsche Bank’s March 2010 acquisition of BHF-Bank AG, a security may be covered by more than one analyst within the Deutsche Bank group. Each of these analysts may use differing methodologies to value the security; as a result, the recommendations may differ and the price targets and estimates of each may vary widely.

In August 2009, Deutsche Bank instituted a new policy whereby analysts may choose not to set or maintain a target price of certain issuers under coverage with a Hold rating. In particular, this will typically occur for "Hold" rated stocks having a market cap smaller than most other companies in its sector or region. We believe that such policy will allow us to make best use of our resources. Please visit our website at http://gm.db.com to determine the target price of any stock.

The financial instruments discussed in this report may not be suitable for all investors and investors must make their own informed investment decisions. Stock transactions can lead to losses as a result of price fluctuations and other factors. If a financial instrument is denominated in a currency other than an investor's currency, a change in exchange rates may adversely affect the investment.

All prices are those current at the end of the previous trading session unless otherwise indicated. Prices are sourced from local exchanges via Reuters, Bloomberg and other vendors. Data is sourced from Deutsche Bank and subject companies.

Past performance is not necessarily indicative of future results. Deutsche Bank may with respect to securities covered by this report, sell to or buy from customers on a principal basis, and consider this report in deciding to trade on a proprietary basis.

Derivative transactions involve numerous risks including, among others, market, counterparty default and illiquidity risk. The appropriateness or otherwise of these products for use by investors is dependent on the investors' own circumstances including their tax position, their regulatory environment and the nature of their other assets and liabilities and as such investors should take expert legal and financial advice before entering into any transaction similar to or inspired by the contents of this publication. Trading in options involves risk and is not suitable for all investors. Prior to buying or selling an option investors must review the "Characteristics and Risks of Standardized Options," at http://www.theocc.com/components/docs/riskstoc.pdf If you are unable to access the website please contact Deutsche Bank AG at +1 (212) 250-7994, for a copy of this important document.

The risk of loss in futures trading, foreign or domestic, can be substantial. As a result of the high degree of leverage obtainable in futures trading, losses may be incurred that are greater than the amount of funds initially deposited.

Unless governing law provides otherwise, all transactions should be executed through the Deutsche Bank entity in the investor's home jurisdiction. In the U.S. this report is approved and/or distributed by Deutsche Bank Securities Inc., a member of the NYSE, the NASD, NFA and SIPC. In Germany this report is approved and/or communicated by Deutsche Bank AG Frankfurt authorized by the BaFin. In the United Kingdom this report is approved and/or communicated by Deutsche Bank AG London, a member of the London Stock Exchange and regulated by the Financial Services Authority for the conduct of investment business in the UK and authorized by the BaFin. This report is distributed in Hong Kong by Deutsche Bank AG, Hong Kong Branch, in Korea by Deutsche Securities Korea Co. This report is distributed in Singapore by Deutsche Bank AG, Singapore Branch or Deutsche Securities Asia Limited, Singapore Branch, and recipients in Singapore of this report are to contact Deutsche Bank AG, Singapore Branch or Deutsche Securities Asia Limited, Singapore Branch in respect of any matters arising from, or in connection with, this report. Where this report is issued or promulgated in Singapore to a person who is not an accredited investor, expert investor or institutional investor (as defined in the applicable Singapore laws and regulations), Deutsche Bank AG, Singapore Branch or Deutsche Securities Asia Limited, Singapore Branch accepts legal responsibility to such person for the contents of this report. In Japan this report is approved and/or distributed by Deutsche Securities Inc. The information contained in this report does not constitute the provision of investment advice. In Australia, retail clients should obtain a copy of a Product Disclosure Statement (PDS) relating to any financial product referred to in this report and consider the PDS before making any decision about whether to acquire the product. Deutsche Bank AG Johannesburg is incorporated in the Federal Republic of Germany (Branch Register Number in South Africa: 1998/003298/10). Additional information relative to securities, other financial products or issuers discussed in this report is available upon request. This report may not be reproduced, distributed or published by any person for any purpose without Deutsche Bank's prior written consent. Please cite source when quoting.

Copyright © 2013 Deutsche Bank AG

18