Embed Size (px)

Citation preview

All

right

s re

serv

ed

May 12, 2015ASSOCHAM, National Seminar on TDS

TDS - CONTRACTORS, COMMISSION, RENT, ROYALTY/ FTSTDS - CONTRACTORS, COMMISSION, RENT, ROYALTY/ FTS

All

right

s re

serv

ed

CONTENTS…

BRIEF PROVISIONSBRIEF PROVISIONS

AMENDMENTS BY FINANCE ACT 2012AMENDMENTS BY FINANCE ACT 2012

ISSUESISSUES

TDS-SNAPSHOTTDS-SNAPSHOT

All

right

s re

serv

ed

TDS

SNAPSHOT

All

right

s re

serv

ed

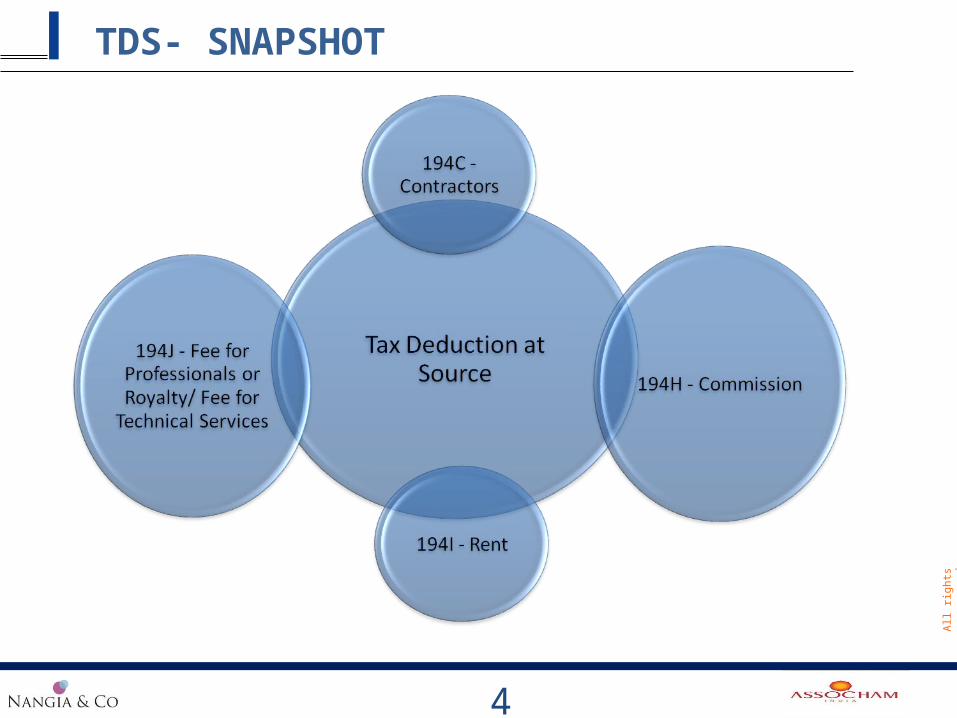

TDS- SNAPSHOT

4

All

right

s re

serv

ed

TDS-SNAPSHOT (Contd..)Section 194C 194H 194I 194J

Applicability Contracts and Sub-Contracts

Commission Rent Professional Services, Technical Services, Director Fees, Royalty or non-compete fees.

Payee Resident

Threshold Limit

Rs. 30,000 or in aggregate Rs. 75,000 p.a.

In aggregate Rs. 5,000 p.a.

In aggregate Rs. 1,80,000 p.a.

In aggregate Rs. 30,000 p.a.

Time of Deduction

Time of Payment or Credit , whichever is earlier

TDS Rate 1% - Individual & HUF Payee2% - Others Payee

10% 2% - P&M10% - L&B, F&F

10% (under each category)

5

Tax not be deducted on service tax if it is shown separately in the invoice /agreement/contract - CBDT Circular 01/2014

All

right

s re

serv

ed

BRIEF PROVISIONS

All

right

s re

serv

ed

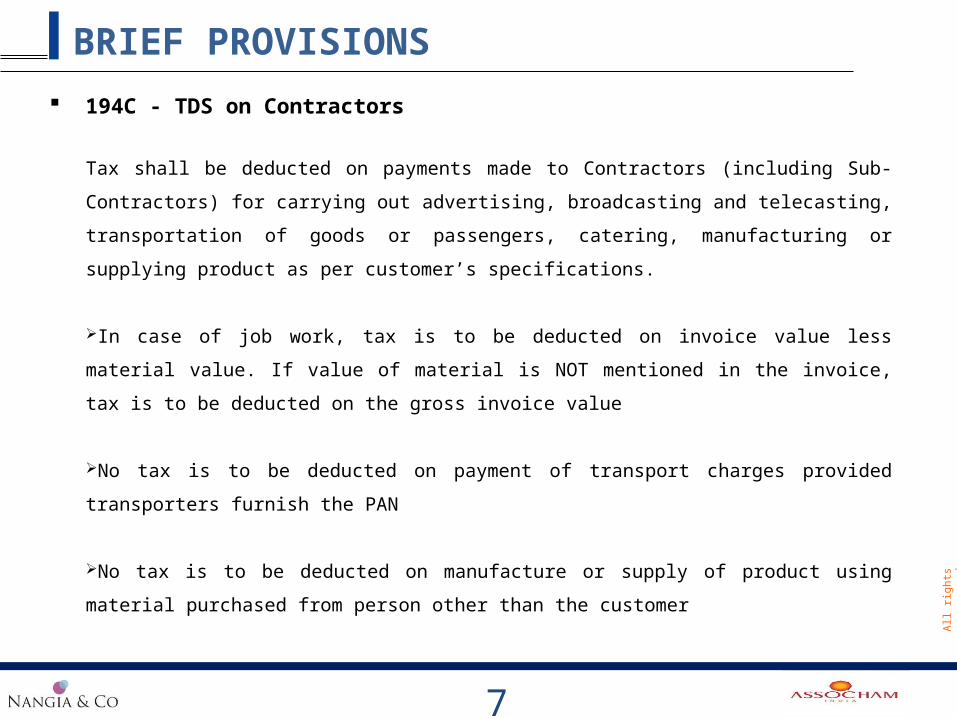

BRIEF PROVISIONS 194C - TDS on Contractors

Tax shall be deducted on payments made to Contractors (including Sub-Contractors) for carrying out

advertising, broadcasting and telecasting, transportation of goods or passengers, catering, manufacturing

or supplying product as per customer’s specifications.

In case of job work, tax is to be deducted on invoice value less material value. If value of material is NOT

mentioned in the invoice, tax is to be deducted on the gross invoice value

No tax is to be deducted on payment of transport charges provided transporters furnish the PAN

No tax is to be deducted on manufacture or supply of product using material purchased from person

other than the customer

7

All

right

s re

serv

ed

BRIEF PROVISIONS (Contd..) 194H - TDS on Commission or Brokerage

Commission includes any payment received by a person acting on behalf of any other person for services

rendered (not covered by professional services)

No tax is to be deducted on certain payments (viz - guarantee commission, credit card or debit card

transaction etc.) made to the banks - Notification no. 56/2012 [F. NO. 275/53/2012-IT(B)], dated 31-12-

2012

Commission retained by agent constitutes constructive payment by principal, accordingly, liable for tax

deduction - [Circular No. 619, dated 04-12-1991]

Payments of Gateway Charges are in the nature of bank charges, not liable for tax deduction - Jet

Airways (India) Ltd. (Mum) (ITAT)

8

All

right

s re

serv

ed

BRIEF PROVISIONS (Contd..) 194I - TDS on Rent

Rent means any payment for the use of land, building, plant, machinery, equipment, F&F

In case of co-ownership, threshold limit of Rs. 1,80,000 shall apply to each co-owner. Senior Manager,

SBI (All.) (HC)

Tax is to be deducted in case of non-refundable deposit as it is in the nature of advance rent [Circular

No. 718, dated 22-08-1995] & Reebok India Co. (Del) (HC)

Hotel Accommodation - Payment made to hotels for accommodation on “Regular Basis” amounts to

Rent. Whereas if the payment is made under a “rate contract”, the payment is not rent - [Circular No.

05, dated 30-07-2002]

9

All

right

s re

serv

ed

BRIEF PROVISIONS (Contd..) 194I - TDS on Rent

Landing and parking charges paid by assessee - airlines to Airport Authority of India were rent Japan

Airlines Co. Ltd. (Delhi) (HC)

Taxi Hiring - Where owner of the vehicle has full control through the driver, it amounts to hiring of taxi

for a specific job warranting tax deduction under section 194C. However, where the hirer has full

control over the vehicle, tax shall be deducted under section 194I [SKIL Infrastructure Ltd (ITAT

Mumbai)]

C&F Agents - Where certain other services are also rendered by C&F agent viz-inventory

management, packing, follow-up, collection etc.; payment is not predominantly for the use of the land

or building, such payment is not liable for tax deduction under section 194I - [Eli Lilly & Co. (India) (P)

Ltd. (Del) (ITAT]

10

All

right

s re

serv

ed

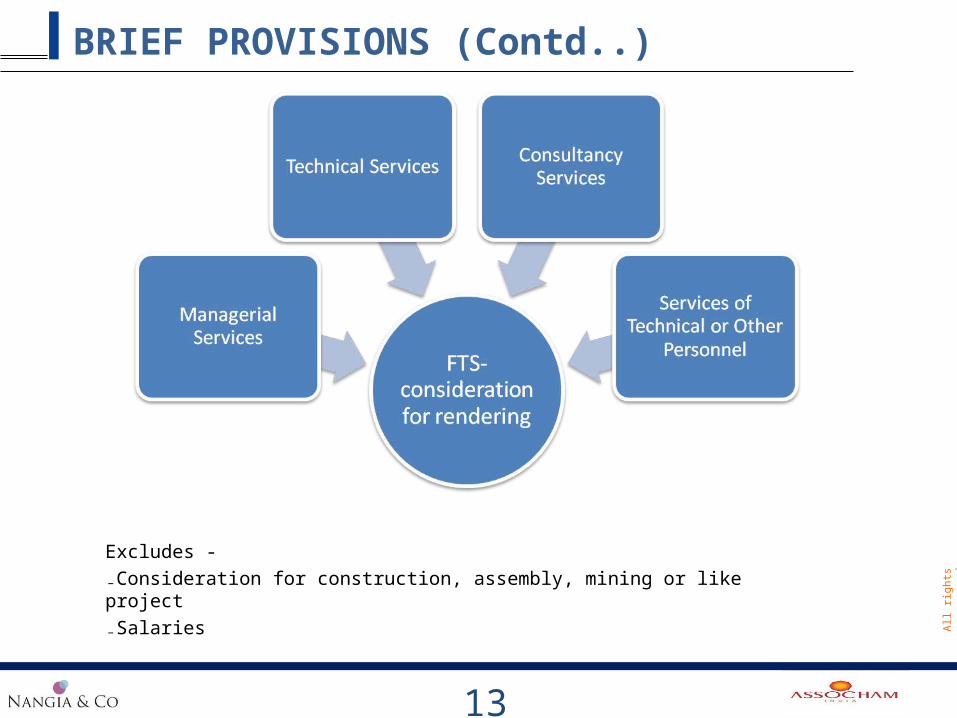

BRIEF PROVISIONS (Contd..) 194J - TDS on Fee for Professional or Technical Services, Royalty etc.

Professional Services - means services rendered by a person in the course of carrying on legal,

medical, engineering or architectural profession or the profession of accountancy or technical

consultancy etc. or such other profession as is notified by the Board for the purposes of section 44AA

or of this section [Explanation 1 to Section 194J]

Fee for Technical Services - consideration (including any lump sum consideration) for the rendering of

any managerial, technical or consultancy services (including the provision of services of technical or

other personnel but does not include consideration for any construction, assembly, mining or like

project undertaken by the recipient, or consideration which would be income of the recipient

chargeable under the head “Salaries”. [Explanation 2 to Section 9(1)(vii)]

11

All

right

s re

serv

ed

BRIEF PROVISIONS (Contd..) Royalty - "Royalty" means consideration (including any lump sum consideration but excluding any

consideration which would be the income of the recipient chargeable under the head "Capital gains") for—

i. the transfer of all or any rights (including the granting of a licence) in respect of a patent, invention,

model, design, secret formula or process or trade mark or similar property ;

ii. the imparting of any information concerning the working of, or the use of, a patent, invention, model,

design, secret formula or process or trade mark or similar property ;

iii. the use of any patent, invention, model, design, secret formula or process or trade mark or similar

property

iv. the imparting of any information concerning technical, industrial, commercial or scientific knowledge,

experience or skill;

v. the use or right to use any industrial, commercial or scientific equipment but not including the amounts

referred to in section 44BB;

vi. the transfer of all or any rights (including the granting of a licence) in respect of any copyright, literary,

artistic or scientific work including films or video tapes for use in connection with television or tapes for

use in connection with radio broadcasting, but not including consideration for the sale, distribution or

exhibition of cinematographic films; or

vii. rendering of any services in connection with the activities referred to above.

12

All

right

s re

serv

ed

BRIEF PROVISIONS (Contd..)

13

Excludes -₋Consideration for construction, assembly, mining or like project₋Salaries

All

right

s re

serv

ed

BRIEF PROVISIONS (Contd..) Managerial Services –

A manager is a person who deals with administration of the business. He controls the policies or scrutinises

the effectiveness of the policies [(Panalfa Autoelektrik Ltd.) (Del) (HC)]

"Management" includes the act of managing by direction, or regulation or superintendence. Thus,

managerial service essentially involves controlling, directing or administering the business." [R. Dalmia

(SC)]

14

All

right

s re

serv

ed

BRIEF PROVISIONS (Contd..) Technical Services –

Services are of technical nature when special skills or knowledge related to a technical field are required for

the provision of such services.

Use of technology in service not indicative of technical nature

Technical services involve special skills or knowledge relating to a technical field, involving or concerning

applied and industrial science [Panalfa Autoelektrik Ltd. (Del) (HC)]

The expression fees for technical services as appearing in section 194J, would have reference to only

technical service involving human intervention [Bharti Cellular Ltd. (Del) (HC)]

15

All

right

s re

serv

ed

BRIEF PROVISIONS (Contd..) Consultancy Services –

Services constituting the provision of advice by someone, such as professional, who has special

qualifications

Consulting services involve giving professional advice or consultation by a person on any field, involving

special qualification that allow him to do so [Panalfa Autoelektrik Ltd. (Del) (HC)]

16

All

right

s re

serv

ed

AMENDMENTS BY THE FINANCE ACT 2012

All

right

s re

serv

ed

Amendments by THE Finance Act, 2012 Amendments to the definition of Royalty –

Explanation 4 - For the removal of doubts, it is hereby clarified that the transfer of all or any rights in

respect of any right, property or information includes and has always included transfer of all or any right for

use or right to use a computer software (including granting of a licence) irrespective of the medium through

which such right is transferred (Ericsson AB) (Del)(HC) overruled?

Explanation 5 - For the removal of doubts, it is hereby clarified that the royalty includes and has always

included consideration in respect of any right, property or information, whether or not—

a) the possession or control of such right, property or information is with the payer;

b) such right, property or information is used directly by the payer;

c) the location of such right, property or information is in India.

(Asia Satellite Telecommunications) (Del) (HC) overruled?

• Explanation 6 - For the removal of doubts, it is hereby clarified that the expression "process" includes and

shall be deemed to have always included transmission by satellite (including up-linking, amplification,

conversion for down-linking of any signal), cable, optic fibre or by any other similar technology, whether or

not such process is secret (Asia Satellite Telecommunications) (Del) (HC) overruled?

18

All

right

s re

serv

ed

Notification no. 21/2012 dated 13 June 2012 No multilevel TDS on software purchase

Tax shall not be deducted while payment by a person (‘buyer’) of a software from any resident

(‘seller’), if -

The software is transferred by the seller without any modification;

Tax was deducted (u/s 194J/ 195) by the seller at the time of initial purchase; and

The buyer obtains a declaration from the seller that the tax was deducted along with PAN of

the seller

19

Benefit restricted to Resident sellers / distributors only

All

right

s re

serv

ed

ISSUES

All

right

s re

serv

ed

ISSUES Discount – Can it be classified as Commission?

Product Discount Schemes - Products were sold directly to distributors/ stockists. They

are not acting on behalf of the manufacturer; no services were offered by the

manufacturer. Most of the credit was given by way of gift items to the distributors/

stockists, hence, does not constitute “commission”- Intervet India Pvt. Ltd. (Bombay High

Court)

Discount on Purchase of Stamp Papers - Discount is given on purchase of stamp papers

in bulk i.e. Cash Discount. The transaction is on principal to principal basis and is of sale -

Ahmedabad Stamp Vendors Association (SC)

Discount offered by Laboratories - Discount offered by laboratories to franchises who are

acting as collection centers is not “commission” - SRL Ranbaxy Ltd. (Delhi) (ITAT)

21

All

right

s re

serv

ed

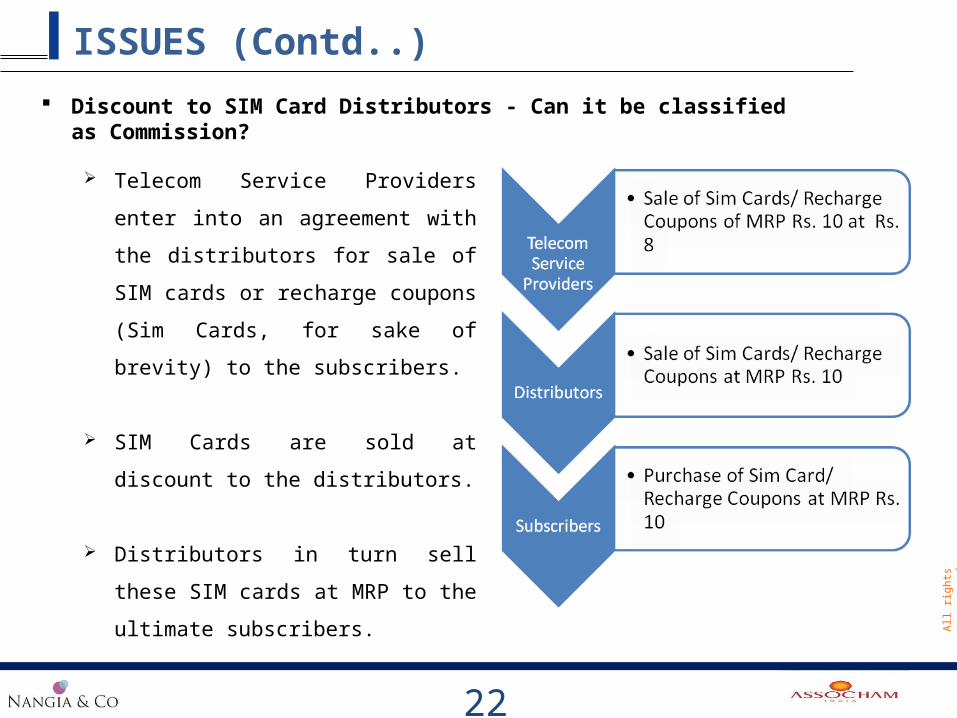

ISSUES (Contd..)

Telecom Service Providers enter into an

agreement with the distributors for sale

of SIM cards or recharge coupons (Sim

Cards, for sake of brevity) to the

subscribers.

SIM Cards are sold at discount to the

distributors.

Distributors in turn sell these SIM cards at

MRP to the ultimate subscribers.

22

Discount to SIM Card Distributors - Can it be classified as Commission?

All

right

s re

serv

ed

ISSUES (Contd..)

23

Idea Cellular(325 ITR 148)

Vodafone Essar(332 ITR 255)

Bharti Cellular(354 ITR 507)

Bharti Airtel & Others(TS-722-HC-2014)

High Court Delhi Kerala Calcutta Karnataka

Date of Judgment February 19, 2010 August 17, 2010 May 19, 2011 August 14, 2014

Whether Discount

given is “Commission”

Yes Yes Yes No

Basis of Comparison

Cases

The discounts/ incentives given by distributors to wholesalers/ retailers are “Commission” [Jay Shree Enterprises (Del) (ITAT)] – April 2015 –

Ideal Cellular relied upon

All

right

s re

serv

ed

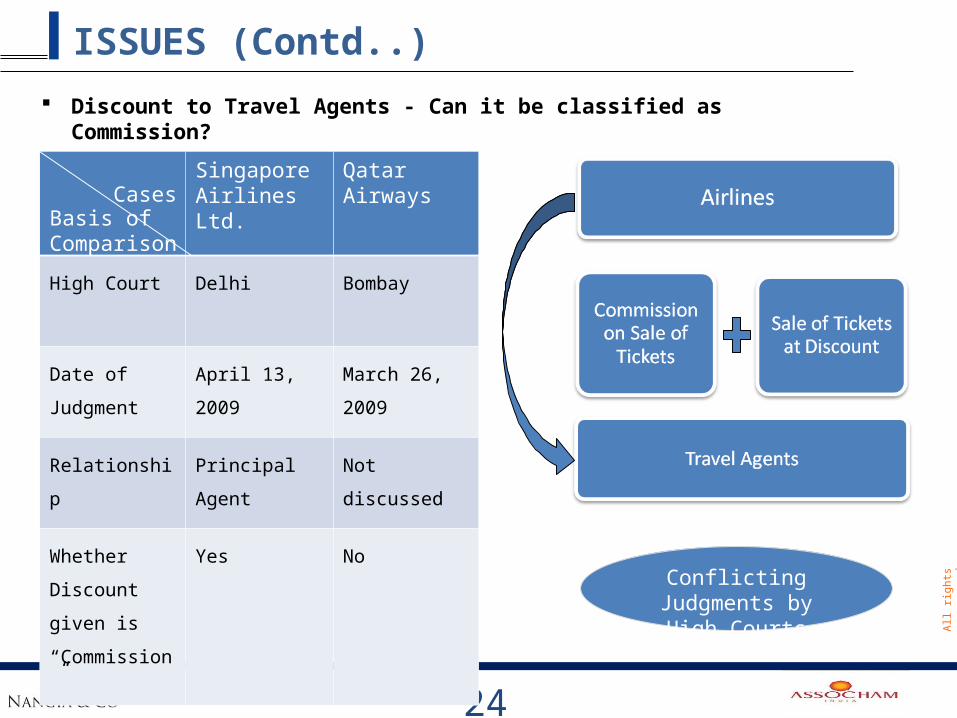

ISSUES (Contd..)

24

Singapore Airlines Ltd.

Qatar Airways

High Court Delhi Bombay

Date of

Judgment

April 13, 2009 March 26, 2009

Relationship Principal Agent Not discussed

Whether

Discount given is

“Commission”

Yes No

Basis of Comparison

Cases

Discount to Travel Agents - Can it be classified as Commission?

Conflicting Judgments by High Courts

All

right

s re

serv

ed

ISSUES Contract for putting up a hoarding – 194C or 194I?

It is in the nature of advertising contract and hence covered by section 194C

If a person takes a particular space on rent and thereafter sub lets the same fully or in

part for putting up a hoarding – Section 194I applies

25

Circular: No. 715, dated 08-08-1995 and Roshan Publicity (Mum)(ITAT)

All

right

s re

serv

ed

ISSUES(Contd..) Cost Sharing Arrangement – FTS?

Background-

₋ F Co. is a foreign company engaged in shipping business

₋ It has three agents in India – A1, A2, A3 who would book cargo

and act as clearing agents

₋ All were connected through a communication system

connected to a mainframe and other computer services in

each country of operation

₋ Cost of the system was shared among all the parties

Held by High Court

₋ Consideration received is not “Fee for Technical Services”:-

1. No profit element is involved, it is merely a cost sharing

arrangement.

2. The system is an automated software based system

which do not require F. Co. to render any technical

service.

26

AP Moller Mosek A/S (ITA 1456...2509/2013)

(Bom) (HC) - April 29, 2015)

All

right

s re

serv

ed

BRIEF PROVISIONS (Contd..) Interconnect/ port/ access/ toll services provided by telephone service provider – FTS?

Service provided by telecom service provider for services of interconnect/ port/ access/ toll would not fall

within the purview of payments as provided for under section 194J, so as to be liable for TDS

The expression fees for technical services as appearing in section 194J, would have reference to only

technical service involving human element [(Bharti Cellular Ltd) (Del.) (HC)]

Collection of fee for use of standard facility of mobile telephone provided to all those willing to pay for it

does not amount to the fee having been received for technical services and hence is not subject to

withholding under section 194J [(Skycell Communications Ltd.) (Mad.) (HC)]

27

Impact of amendment in the definition of “Royalty” (“Process” clarified) by the Finance Act, 2012?

All

right

s re

serv

ed

BRIEF PROVISIONS (Contd..) Payment for online Advertising –Whether qualify for FTS?

Payment for online advertisement are not taxable as Fees for Technical Services [(Right Florists) (Kol.)

(ITAT)]

Payment for online advertisement cannot be taxable even as Royalty [(Pinstorm Technologies) (Mum)

(ITAT); and (Yahoo India) (Mum) (ITAT)]

28

Impact of amendment in the definition of “Royalty” by the Finance Act, 2012?

All

right

s re

serv

ed

BRIEF PROVISIONS (Contd..) Sales Commission –Whether qualify for FTS?

TDS under section 194J would not get attracted on payments made to any person appointed for onward

transmission of the goods to the market on a commission basis [(Piramal Healthcare Ltd.) (Mum) (ITAT)]

29

Depends upon the nature/ character of services rendered [(Panalfa Autoelekrtik) (Del) (HC)]

All

right

s re

serv

ed

Concluding Remarks

Non compliance with withholding provisions results into harsh consequences (including penalty and disallowances of payments)

Increasing complexity coupled with divergent interpretation by judiciary requires close monitoring on withholding payments

Considering the consequences of non-compliance, utmost important to adopt conservative view

30

All

right

s re

serv

ed

NEW DELHISuite 4A, Plaza M 6, Jasola, New Delhi 110025, India‐ ‐ ‐

Tel: +91 (11) 4737 1000, Fax: +91 (11) 4737 1010, Email: [email protected]

MUMBAI11th Floor, B Wing, Peninsula Business Park, Ganpatrao Kadam Marg,

Lower Parel, Mumbai–400 013, IndiaPh: +91-22-6173 7000 Fax: +91-22-6173 7060, Email: [email protected]

DEHRADUN3rd Floor, NCR Plaza, New Cantt. Road, Dehradun–248 001, India

Ph: +91-135-274 7081, +91-135-274 7082 Fax: +91-135-2747080, Email: [email protected]

SINGAPORENangia & Co (Singapore) Pte Ltd., 24 Raffles Place, #25-04A Clifford Centre, Singapore 048621