Embed Size (px)

Citation preview

“Study of Trend of FII

investment and its impact on

Sensex”

MAJOR RESEACH PROJECT FOR

SESSION 2013-15

For Partial Fulfillment of the Requirement for the

Degree of

MBA (International Business

SUBMITTED TO

SUBMITTED BY

1

Dr. Vidya Telang Piyush

Kumar Patidar

MBA

(International

Business)

ACKNOWLEDGEMENT

I am using this opportunity to express my deep gratitude to

everyone who supported me throughout my Major Research Project on

the Topic “Study of Trend of FII investment and its impact on Sensex”.

I am thankful for to all for aspiring guidance, valuable thoughts and

friendly advice during the project work. I am sincerely grateful to them for

sharing their truthful and illuminating views on a number of issues related

to the project.

I express my warm thanks to my project Mentor Dr. Vidya Telang

for their valuable support and special guidance during the project work.

I would also like to thank my Friends and all the people who

provided me with the facilities being required and conductive conditions

for my MBA project.

Piyush Kumar

Patidar

2

DECLARATION

I Piyush Kumar Patidar studying in MBA (IB) 4th semester declares that i

have done a project on “Study of Trend of FII investment and its impact

on Sensex”. As required by the university rules, I state that the work

presented in this thesis is original in nature and to the best my

knowledge, has not been submitted so far to any other university.

Whenever references have been made to the work of others, it is

clearly indicated in the sources of information in references.

3

Piyush Kumar Patidar

4

CERTIFICATE

This is to certify that the Major Research Project on topic

“Study of Trend of FII investment and its impact on Sensex” which is

being submitted by Piyush Kumar Patidar of MBA [International

Business] branch in the partial fulfilment of this course curriculum has

satisfactorily completed under my supervision and guidance. This is

original work done by him. I approve this project for further evaluation.

Guided by-

Student’s name-

Dr. Vidya Telang

Piyush Kumar Patidar

5

Contents

Chapter 1 - Introduction …page no. 7

Chapter 2 - Review of Literature …page no. 12

Chapter 3 - Research Methodology …page no. 17

Chapter 4 - Data Analysis and Interpretation …page no. 22

Chapter 5 – Conclusion …page no. 32

References …page no. 33

6

Chapter 1

7

Introduction

Capital is considered to be very important growth in any economy. In case of

developing country like India Domestic capital is not sufficient to fulfill the

requirement of economy. In that case foreign capital plays a very important role.

Foreign Capital comes in two forms Foreign Direct Investment (FDI) and Foreign

Institutional Investment (FII). FDI is considered as a more stable form of foreign

capital as compared to FII. But, FII inflows and outflows directly create impact on

stock market. Hence FIIs have emerged as movers and shakers of Indian Stock

Market. This Research Project examines the trend and pattern of FII flow in India

and also examines the relationship between FII and Sensex.

Institutional Investor is any investor or investment fund that is from or registered in a

country outside of the one in which it is currently investing. Institutional investors

include hedge funds, insurance companies, pension funds and mutual funds. The

growing Indian market had attracted the foreign investors, which are called Foreign

Institutional Investors (FII) to Indian equity market, and in this paper, we are trying a

simple attempt to explain the impact and extent of foreign institutional investors in

Indian stock market. Role of FII has increased and changed the face of Indian Stock

Market. It has brought both qualitative and quantitative change. It had also increased

the breadth and depth of market. Although the Foreign institutional investors (FIIs),

whose investments are often called 'hot money' because they can be pulled out at

any time, have been blamed for large and concerted withdrawals of capital from the

country at the time of recent financial crisis, they have emerged as important players

in the Indian capital market. With over 20 million shareholders, India has the third

largest investor base in the world after the USA and Japan.

Over 9,000 companies are listed on the stock exchanges, which are serviced by

approximately 7,500 stockbrokers. The Indian capital market is significant in terms of

the degree of development, volume of trading and its tremendous growth potential.

The Foreign Institutional Investors (FIIs) have emerged as remarkable players in the

Indian stock market and their growing contribution adds as an important feature of

8

the development of stock markets in India. As a result, the Indian Stock Markets

have reached new heights and became more volatile making the researches work in

this dimension of establishing the link between FIIs and Stock Market volatility.

Hence, it’s an interesting topic to ascertain the role of FIIs in Indian Stock Market.

After the launch of the reforms, foreign institutional investors (FIIs) from September

14, 1992, with suitable restrictions, were permitted to invest in all securities traded

on the primary and secondary markets, including shares, debentures and warrants

issued by companies which were listed or were to be listed on the Stock Exchanges

in India and in schemes floated by domestic mutual funds. A positive contribution of

the FIIs has been their role in improving the stock market infrastructure and the SEBI

assured its contribution towards its development.

Hence, in this age of transnational capitalism, a significant amount of capital is

flowing from developed world to emerging economies. Positive fundamentals

combined with fast growing markets have made India an attractive destination for

foreign institutional investors (FIIs). Although the Foreign institutional investors

(FIIs), whose investments are often called 'hot money' because they can be pulled

out at anytime, have been blamed for large and concerted withdrawals of capital

from the country at the time of recent financial crisis, they have emerged as

important players in the Indian capital market.

Form 2nd June 2014 the new foreign portfolio investor (FPI) regulations, which

replace the two-decade old foreign institutional investors (FII) regime, in the Indian

market has got operational now. From now on, new overseas investors wanting to

enter the Indian market will be registered under the FPI Regulations.

ROUTE OF FIIS INVESTMENT:

FIIs have two route of making investment in Indian capital market:

1. On its own behalf.

2. On behalf of sub account (Sub-account means any person residents outside India,

on whose behalf investments are proposed to be made in India by a FII investor

9

and who is registered as a sub-account under SEBI. For each sub-account a

separate registration is granted. The sub-account should fall into the categories,

namely: a Broad Based Fund or Portfolio incorporated or established outside India;

a Proprietary Fund; a Foreign Corporate (A foreign corporate means a body

corporate incorporated outside India which has listed securities on any stock

exchange outside India with an asset base of not less than $ 2 billion US dollars

and had an average net profit of not less than fifty million US dollars during the

three financial years preceding the date of the application.) or an Foreign individual;

(A Foreign Individual has a net worth of not less than $ 50 million, holds the

passport of a foreign country for 5 years, hold a certificate of good standing from a

bank and client of the concern FII for last 3 years. The NRIs shall not be eligible for

opening a subaccount) or a University Fund, Endowment, Foundation, Charitable

Trust or Charitable society (Securities and Exchange Board of India (Foreign

Institutional Investors) Regulations, 1995).

INVESTMENTS PATTERN OF FIIS IN INDIAN STOCK MARKET:

(i) A FII could invest in the primary and secondary markets including shares,

debentures and warrants of the companies unlisted, listed or to be listed on a

recognized stock exchange in India. These could also invest in units of mutual

fund whether listed or unlisted; dated government securities; listed

derivatives; commercial paper and security receipts.

(ii) Total investments in equity, convertible debentures (CDs) and tradable

warrants on its own account or on behalf of sub-account shall not be less than

70% of the aggregate of total investment by the FIIs. A foreign corporate or

individual shall not be eligible to invest through the 100% debt route.

(iii) FIIs can’t invest in security receipts on behalf of its sub-account. FIIs could

invest or transact in the Indian securities market only on the basis of taking

and giving delivery of securities purchased or sold. They could enter into

short selling transaction as specified by SEBI. RBI shall grant permission to

10

make transactions in government securities like commercial paper (CP) and

T-Bill.

(iv) FII investment in equity shares of a company on behalf of its sub-accounts

shall not exceed 10% of the total issued capital provided further that foreign

corporate or individuals, each of such sub-account shall not more than 5% of

the issued capital.

(v) FII could lend or borrow securities on behalf of sub account. No FII could

issue or deal in off-shore derivative instruments, directly or indirectly, unless

such off-shore derivative instruments are issued only to persons who are

regulated by an appropriate foreign regulatory authority and know your

customer (KYC) norms have been fulfilled. No sub-account shall issue off-

shore derivative instruments. Off-shore derivative instruments are issued by

FIIs against securities held by it that are listed or proposed to be listed on any

recognized stock exchange in India.

(vi) FIIs shall disclose information regarding the terms of and parties to off-shore

derivative instruments such as Participatory Notes (PNs), Equity Linked Notes

or any other such instruments enter into by it or its subaccount units or

affiliates relating to any securities listed or proposed to be listed in Indian

Stock Exchange.(Securities and Exchange Board of India (Foreign

Institutional Investors) Regulations, 1995).

11

Chapter 2

12

Review of Literature

Kulwantraj N. Bindu (2004), in his research paper titled ‘A study on the

determinants of foreign Institutional Investments in India and the role of risk,

inflation and return’ had conducted an intensive study to find out the

determinants responsible for the flow of FIIs and their degree of impact. With

the help of monthly data they found out that FII inflow depends on stock

market returns, inflation rates (both domestic and foreign), and ex-ante risk. In

terms of magnitude, the impact of stock market returns and the ex-ante risk

turned out to be the major determinants of FII inflow. The study has not found

any causative link running from FII inflow to stock returns.

Raj Chaitanya (2003),

In his research work titled ‘Foreign Institutional Investments’ discussed in

length about the FIIs and their impact on the Indian economy. Analyzing daily

flow data, he concludes that the stock market performance has been the sole

driver of FII flows, though monthly data in the pre-Asian crisis period suggests

some reverse causality.

Krishna Reddy Chittedi (2009) In his research work titled ‘ Volatility of Indian

Stock Market and FIIs’ analyzed the performance of SENSEX v/s. FIIs and

some of the most talked about movements of the SENSEX, starting with the

secondary market summary of each year. Foreign investments in BSE reveal

that the liquidity as well as volatility was highly influenced by the FII flows. FIIs

are significant factor in determining the liquidity and volatility in the stock

prices. With thorough analysis regarding the stock market in last 2 years, it

was concluded that stock market touched its peak at 21000 but then crashed

badly.

Rao (1999), in their study of foreign institutional investments and Indian stock

market found that the net FII investments influence the stock prices in India.

13

Chakrabarti and Vimal (2001), Concluded in their study that in the pre-Asian

crisis period any change in FII was found to have a positive impact on the

equity returns, whereas in the post- Asian crisis the reverse relationship was

noticed. FII’s were a major portion of investments and their roles in

determining the movement of share price and indices is considerably high.

The movement of indices in India depends only on the trade done in limited

number of stocks. Thus, when the FII’s frequently buy and sell stocks, it leads

to volatility of the market.

Gordon and Gupta (2002), on the portfolio flows in India and the influence of

domestic fundamental factors, it was found that there exists a strong impact of

the domestic fundamentals on the investment flows into India. They used the

data from September 1992 till October 2001 and applied regression model

and unit root test. It was concluded that the portfolio flows to India are small,

compared to other emerging markets and also less volatile. The combination

of domestic, regional and global variables are important in the determination

of the portfolio flows into India.

Kumar (2002), on the role of institutional investors (including the FIIs) in

Indian equity market, concluded that FIIs and Indian mutual funds combined

together are the most powerful and influential force in driving the Indian

market.

Mukherjee (2002), examined the various probable determinants of FII and

concluded

(1) Foreign investment flows to the Indian markets tend to be caused by

return in the domestic equity market;

(2) Returns in the Indian equity market is an important factor that has an

impact on FII flows;

14

(3) whereas FII sale and FII net inflow are significantly affected by the

performance of the Indian equity market, FII purchase show no such affect to

this market performance;

(4) FII investors do not probably use Indian equity market for the purpose of

diversification of their investment;

(5) Returns from the exchange rate variation and the fundamentals of the

economy may have an impact on FII decisions, but such influences do not

Prove to be strong enough.

Batra, A (2004), In his research work has analyzed the trading behaviour of

FIIs and their impact of trading biases upon stock market volatility. It was

found that there is a strong evidence for the fact that FIIs on daily basis have

been positive investors and trend chasers at the aggregate level. But there

seem to exist no evidence of positive feedback trading on monthly basis. The

research work also indicates that the foreign investors have a tendency to

herd together in their trading activity in India. The trading behavior/biases of

the FIIs do not appear to have a destabilizing impact on the equity market.

Dhwani Mehta (2009), in her research work titled ‘A Study: FII Flows in India’

the Indian stock markets have been experiencing humungous amount of FII

flows. This has affected small investors thinking that markets are rigged. For

the good news to Indian investors it has been established that out of all the

factors, it is basically the performance of Indian stock markets vis-à-vis other

emerging and developed markets that probably may cause returns and not

the other way round.

Mohan, T.T. (2005), concludes that the crossover funds in the emerging

markets form only a very small component of global portfolios and hence they

are somewhat a bit less vulnerable to fluctuations to stock returns arising from

changes in fundamental and economic conditions in emerging markets.

15

Rai, K. and N. Bhanumurthy (2004), Examined the role of return, risk and

inflation as determinants of foreign institutional investors in the context of

India. They found that FII inflow depends on stock market returns, inflation

rates (both domestic and foreign) and ex-ante risk. In terms of magnitude, the

impact of market returns and the ex-ante risk turned out to be the major

determinants of FII inflow. They have also found that there is any causative

link running from FII inflow to stock returns. And in the last, they have

suggested that the stabilizing the stock market volatility and minimizing the

ex-ante risk would help to attract more FII, an inflow of which have a positive

impact on the real economy.

Narayan Sethi (2007), Globalization, Capital Flows and Growth in India:

Capital flow is of importance, when the magnitude of those flows is steady

and stable. The international capital flow like direct and portfolio flows has

great contribution to impact the economic behavior of the countries in a

positive way.

Bhupender Singh (2005), in his research work titled ‘Inter-Relation between

FII, Inflation and Exchange Rate’ discussed about as to how the financial

sector of an economy plays a vital role in attracting the Foreign Institutional

Investment inflows. The study tries to examine the extent of effect of

significant macroeconomic variables; inflation and exchange rate on the flows

of Foreign Institutional Investment in India. He has tried to analyze the inter-

relation between Foreign Institutional Investment, Exchange Rate and

Inflation. Given the large volume of these flows and their impact on domestic

financial markets; understanding the major determinants of these flows

becomes imperative as the economy has now moved towards full capital

account convertibility.

Pal, P. (2004), found that FIIs are the major players in the Indian stock market

and their impact on the domestic market is increasing. Trading activities of

16

FIIs and the domestic stock market turnover indicates that FII’s are becoming

more important at the margin as an increasingly higher share of stock market

turnover is accounted for by FII trading in India.

17

Chapter 3

18

Research Methodology

Objectives of Study

To study the trends and patterns of foreign capital flow into India in the form

of FIIs.

To find relation between FIIs & Sensex.

To examine whether FIIs have any influence on SENSEX.

19

Research design

The research has been carried out by collection of secondary data with the use

of primarily the internet via website of SEBI and BSE; the data of FIIs Net

Investment have collected from the report of SEBI whereas the Sensex data

have collected from the archives of the BSE. Sensex consist of 30 component

stocks representing large, well-established and financially sound blue chip

companies across the key sectors .No primary data has been used here like face

to face interviews or telephonic interviews, questionnaires etc.

RESEARCH TYPE

Analytical research - In analytical research, the researcher has to use facts

or information already available, and analyze these to make a critical

evaluation of the material. The analytical research usually concerns itself with

cause-effect relationships. While analytical research attempts to

establish why it is that way or how it came to be.

Exploratory research - Exploratory research helps determine the best

research design, data collection method and selection of subject. Research is

quite informal, relying on secondary research. Results of exploratory research

provide significant insight in given situation.

Descriptive research - Descriptive research are a means of discovering

new meaning, describing what exists, determining the frequency with which

something occurs, and categorizing information. Also deals with everything

that can be counted and studied, which has an impact of the lives of the

people it deals with. It is description of the state of affairs as it exists at

present. The main characteristic of this method is that the researcher has no

control over the variables; we can only report what has happened or what is

happening.

20

Research Approach

Data type - Secondary Data

Secondary data are those that have already been collected by others. These

are usually available in journals, periodicals, dailies, research, publications,

official records etc.

Data collection - Secondary Data is collected through published sources like

Government publication, reports on projects, research papers of educational

Institutions, organizations and various government official websites. In this

research data is collected from official website of BSE and SEBI. Last 10 year

data is being used for research.

Tools Used for Research

Trend analysis: is done with Graphical presentation and table analysis, ratio of

equity and debts is calculated also absolute change & absolute percentage

change is being calculated for the better understanding and analysis of trend. All

the graphical n tabulation is done with the help of MS-Excel.

Correlation analysis:

Relationship between FII and Sensex is calculated with the help of MS- Excel for

two different data type in which first data table includes the value of year 2008-09

and in second analysis value of 2008-09 is excluded for the accuracy of result.

The correlation coefficient (a value between -1 and +1) tells you how strongly two

variables are related to each other.

A correlation coefficient of +1 indicates a perfect positive correlation. As

variable X increases, variable Y increases.

A correlation coefficient of -1 indicates a perfect negative correlation. As

variable X increases, variable Z decreases.

21

A correlation coefficient near 0 indicates no correlation.

Regression Analysis

Regression analysis is a statistical tool for the investigation of relationships between

variables. Usually, the investigator seeks to ascertain the causal effect of one

variable upon another—the effect of a price increase upon demand, for example, or

the effect of changes in the money supply upon the inflation rate. To explore such

issues, the investigator assembles data on the underlying variables of interest and

employs regression to estimate the quantitative effect of the causal variables upon

the variable that they influence. The investigator also typically assesses the

“statistical significance” of the estimated relationships, that is, the degree of

confidence that the true relationship is close to the estimated relationship.

In this research project impact of FII is on the Sensex is done on the yearly data of

last 10 years. In which FII is independent variable and Sensex is dependent

variable. Regression is calculated with the help of MS-Excel.

22

Chapter - 4

23

Data Analysis and Interpretation

Table 1 -The following data of investment of FII is for the period of 12 years in

form of equity and debts.

FPI Investments - Financial Year

INR crores

Financial Year Equity Debt Total

2004-05 44,123 1,759 45,881

2005-06 48,801 -7,334 41,467

2006-07 25,236 5,605 30,840

2007-08 53,404 12,775 66,179

2008-09 -47,706 1,895 -45,811

2009-10 1,10,221 32,438 1,42,658

2010-11 1,10,121 36,317 1,46,438

2011-12 43,738 49,988 93,726

2012-13 1,40,033 28,334 1,68,367

2013-14 79,709 -28,060 51,649

2014-15 ** 9,602 -9,185 418

Total 6,17,282 1,24,532 7,41,812

Year Equity Debt Ratio2003-04 39,960 5,805 6.88:1

2004-05 44,123 1,759 25.08:1

2005-06 48,801 -7,334 -6.65:1

2006-07 25,236 5,605 4.5:1

2007-08 53,404 12,775 4.18:1

2008-09 -47,706 1,895 25.17:1

2009-10 1,10,221 32,438 3.4:1

2010-11 1,10,121 36,317 3.03:1

2011-12 43,738 49,988 0.87:1

2012-13 1,40,033 28,334 4.94:1

2013-14 79,709 -28,060 -2.84:1

2014-15 9,602 -9,185 -1.05:1

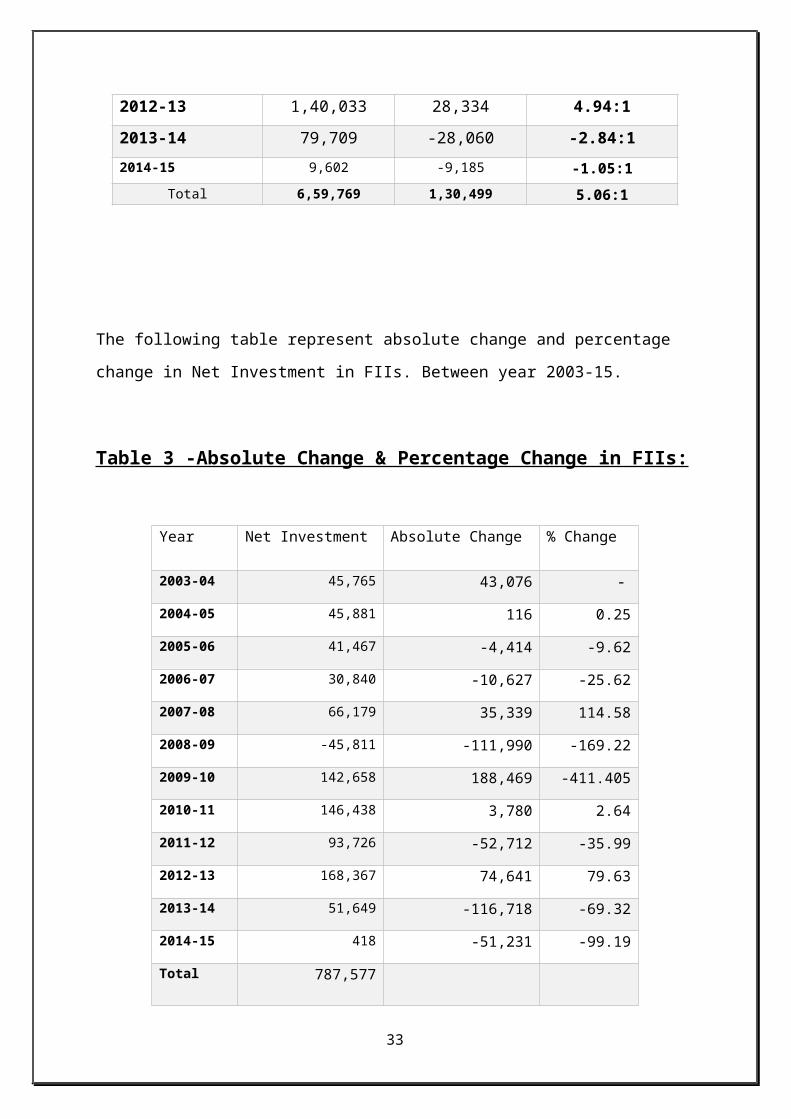

Total 6,59,769 1,30,499 5.06:1

24

Table 2- Showing Equity – Debt Ratio.

The following table represent absolute change and percentage change in Net

Investment in FIIs. Between year 2003-15.

Table 3 -Absolute Change & Percentage Change in FIIs:

25

Year Net Investment Absolute Change % Change

2003-04 45,765 43,076 -

2004-05 45,881 116 0.25

2005-06 41,467 -4,414 -9.62

2006-07 30,840 -10,627 -25.62

2007-08 66,179 35,339 114.58

2008-09 -45,811 -111,990 -169.22

2009-10 142,658 188,469 -411.405

2010-11 146,438 3,780 2.64

2011-12 93,726 -52,712 -35.99

2012-13 168,367 74,641 79.63

2013-14 51,649 -116,718 -69.32

2014-15 418 -51,231 -99.19

Total 787,577

Graph 1 -Net Investment of FII

2004-05

2005-06

2006-07

2007-08

2008-09

2009-10

2010-11

2011-12

2012-13

2013-14

2014-15 **

Total

-200,000

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

1,600,000

FPI Investments - Financial Year INR crores Total

FPI Investments - Financial Year INR crores Debt

FPI Investments - Financial Year INR crores Equity

Graph 2 - Trend Line for FIIs

2004-05

2005-06

2006-07

2007-08

2008-09

2009-10

2010-11

2011-12

2012-13

2013-14

2014-15 **

-100000

-50000

0

50000

100000

150000

200000

YearFIILinear (FII)

26

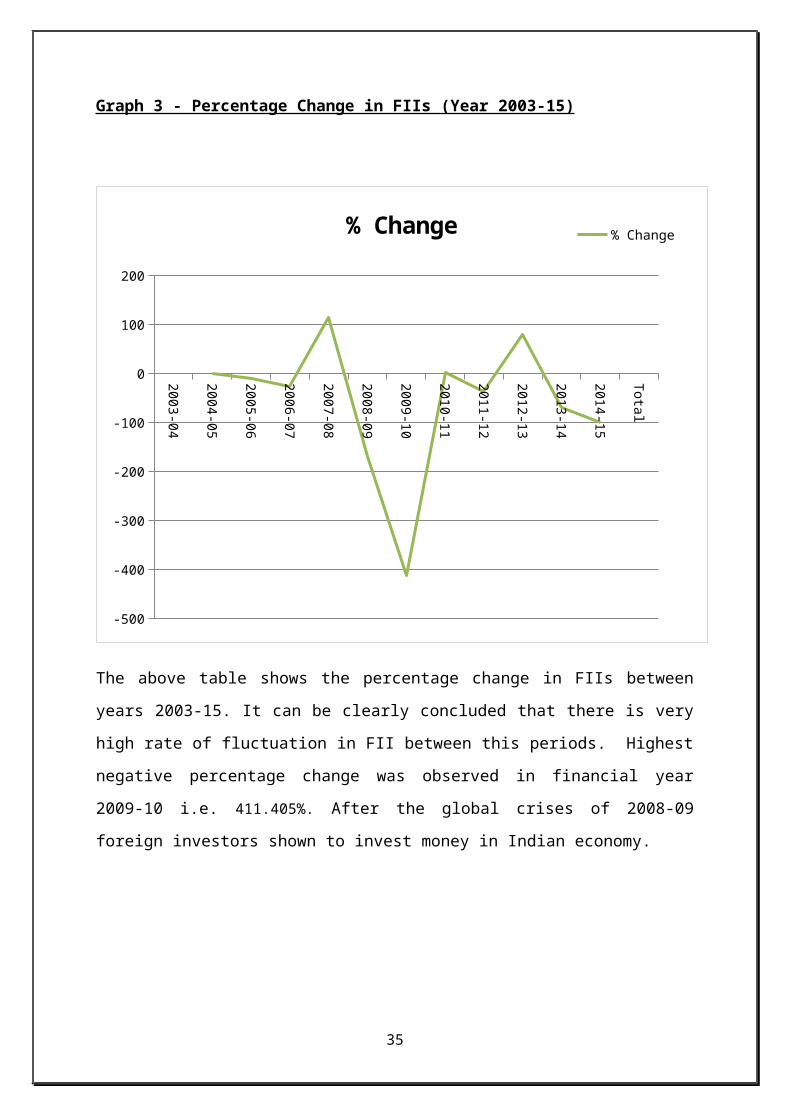

Graph 3 - Percentage Change in FIIs (Year 2003-15)

2003-04

2004-05

2005-06

2006-07

2007-08

2008-09

2009-10

2010-11

2011-12

2012-13

2013-14

2014-15

Total

-500

-400

-300

-200

-100

0

100

200

% Change% Change

The above table shows the percentage change in FIIs between years 2003-15. It

can be clearly concluded that there is very high rate of fluctuation in FII between this

periods. Highest negative percentage change was observed in financial year 2009-

10 i.e. 411.405%. After the global crises of 2008-09 foreign investors shown to invest

money in Indian economy.

27

Trend Analysis

Table 1 reveals that investors are investing more in equity as compare to debts. So

following point can be concluded by analyzing above data,

2005-06, investment in Equity were 48801 crores which is more compare to

previous year but net invest which was 41467 crores which is less than

previous year due to withdraw of 7334 crores from debts.

2006-07, Net Investment was also low compare to previous year i.e. 30840 cr.

2007-08, more than 50% of growth is observed in net investment i.e. 66179 cr.

But 2008-09, net inflow of foreign capital in form of FIIs was negative, previous

researcher joined this Incidence with Global Economic Crises in this period,

recession in UK and bursting of Real State Bubble in USA.

2009-10, starting year of UPA -2, highest ever net investment is observed in

FIIs i.e. 142658 cr.

2010-11, highest investment in equities observed and which is considered one

of the great years for investors with partial growth in net investment i. e.

146438.

2011-12, highest investment in debts 49988 cr. but decrease in net investment

of 136836 cr.

2012-13, Investment in equity touched new millstone with 140033 cr. As well as

in net investment i.e. 168367 cr.

2013-14, net investment was decreased approx. to 1/3 of previous year’s i.e.

51649 cr.

2014-15, new hope is arising as NDA first time come in power with full

majority. Trying to provide good environment to foreign investors which is good

sign for shareholders as well as Indian Economy.

Trend of FII investment is positive.

28

Relation between FIIs and Sensex

Table 4

Year FII Sensex

2003-04 45,765 6602.69

2004-05 45,881 9397.93

2005-06 41,467 13786.91

2006-07 30,840 20286.99

2007-08 66,179 9647.31

2008-09 -45,811 17464.81

2009-10 142,658 20509.09

2010-11 146,438 15454.92

2011-12 93,726 19426.71

2012-13 168,367 21170.68

2013-14 51,649 27499.42

Correlation

Column 1 Column 2

Column1 1 0.205

Column2 0.205 1

This table shows that FII and Sensex has weak positive correlation.

Correlation coefficient: 0.205

29

By excluding values of Year 2008-09

Table 5

Year FII Sensex

2003-04 45,765 5590.6

2004-05 45,881 6492.82

2005-06 41,467 11279.96

2006-07 30,840 13072.1

2007-08 66,179 15644.44

2009-10 142,658 17527.77

2010-11 146,438 19445.22

2011-12 93,726 17404.2

2012-13 168,367 18835.77

2013-14 51,649 27499.42

Correlation

Column 1 Column 2

Column1 1 0.436

Column2 0.436 1

This table shows that FII and Sensex are positively correlated.

Correlation coefficient: 0.436

30

Correlation Analysis:

Correlations have been applied on the above data set. Table 3 shows

investment and Sensex point of 2008-2009. Table 4 has excluded that value

due to Global economic crisis between this period.

Therefore the correlation from table 3 is less i.e. 0.205 and that of table 4 is

0.436. And these both values show positive correlation between FII and

Sensex.

Regression Analysis -1

From table: 3 including value of year 2008-09

Multiple R 0.205

R square 0.042

Intercept 15006.44

FII 0.020

P- Value 0.00079

Regression Analysis -2

From table: 4 excluding value of year 2008-09

Multiple R 0.43

R square 0.190

Intercept 10650.5

FII 0.055

P- Value 0.025

31

Interpretation:

There is a positive relation between FII and Sensex. Including the data of 2008-

09 we can say that if one unit of FII increase 0.02 change in Sensex.

There is comparatively more positively relation between FII and Sensex.

Excluding the data of 2008-09 we can say that if one unit of FII increase 0.055

change in the Sensex.

From table 3 we can conclude that Sensex is 20% dependent on FIIs.

From table 4 we can conclude that Sensex is 43% dependent on FIIs.

32

Chapter- 5

33

Conclusion:

From the above study, it can be concluded that FIIs has significant impact on

Sensex. The correlation coefficient between FII and Sensex for both analyses

is positively correlated. From table-4 correlation coefficient is 0.205 and from

table-5 coefficients is 0.436 in which values FIIs and Sensex is excluded.

Trends of FII is positive as per the trend analysis i.e. Foreign investors are

looking forward to invest in India. NDA come up in the power with full majority

in General Election (Loksabha Election) – 2014. Providing stable govt. which is

good for the investors as well as economy.

When regression analysis is done on the same data sets. Than we can

conclude that from table 4, Sensex is 20% dependent on FIIs and from table 5,

Sensex is 43% dependent which is more than double increment in result.

No doubt inflow of foreign capital brings foreign currency ($) into the country

which contributes towards increase in wealth of shareholder but large portion of

capital in stock market comes through domestic route. Thus it is important for

the country to encourage the investment with in the country along with the

foreign investment because FII look for income if the economy grows they

entered into the stock market of the concerned economy but exit from the

market in the same speed as they entered. Also global and domestic activities

are responsible for change in the FII investment pattern.

34

References

1) A. Kulwantraj N. Bindu (2004).” The determinants of foreign Institutional

Investments in India and the role of risk, inflation and return”, Indian Economic

Review, Vol. 32, Issue 2, pages 217-229

2) Mayur Shah (2013) “Flows of FIIs and Indian Stock Market’’

http://www.cpi.edu.in/

3) Gordon, J. and Gupta, P. (2003). “Portfolio Flows into India: Do Domestic

Fundamentals Matter?” IMF Working Paper, Number WP/03/02 .

4) Chakrabarti, R. (2001). “FII Flows to India: Nature and Causes”, Money and

Finance, Vol. 2, No. 7.

5) Mukherjee (2002) “Taking Stock of Foreign Institutional Investors.”

Economic and Political Weekly. June 11, 2005.

<www.rbi.ord.in>, www.sebi.gov.in

6) Pal, P. (2004),” Foreign Institutional Investment in India”, Research on

Indian Stock Volatility. Vol. 12. Publisher: Emerald Group Publishing Limited.

7) Aggarwal, R., Klapper, L. & Wysocki, P. D. (2005). “Portfolio preferences

of foreign institutional investors”, Journal of Banking and Finance, Vol. 29, No.

12, pp. 2919-2946.

8) Batra, A (2004) “Foreign Institutional Investors: An Introduction”, Icfai,

University Press, pages-107-111.

9) Rai, K. and N. Bhanumurthy (2004) “Role of return, risk and inflation as

determinants of foreign institutional investors in India”, Journal of Institutional

Investors. Vol. 17. Publisher: Emerald Group Publishing Limited.

35

9) Bhupender Singh (2005), “Inter-Relation between FII, Inflation and

Exchange Rate”, Journal of Institutional Investors. Vol. 17. Publisher: Emerald

Group Publishing Limited.

10) Krishna Reddy Chittedi (2009). “Volatility of Indian Stock Market and

FIIs”, Journal: European Business Review. Vol. 15, pages 22-34

11) Kumar (2002), “Pasricha, J.S. and Umesh C. Singh. “Foreign Institutional

Investors and Stock Market Volatility.” The Indian Journal of Commerce. Vol.54,

No.3, July-September, 2002.

12) Narayan Sethi (2007),”Globalization, Capital Flows and Growth in India”,

Journal of ICFAI, Vol: 25. Publisher: MCB UP Ltd.

13) Dhwani Mehta (2009), “A Study: FII Flows in India, Research on “Indian

Stock Volatility”. Vol. 14. Publisher: Emerald Group Publishing Limited.

14) SEBI, BSE and MoneyControl.com

15) Aswini A. and Mayank Kumar (2013), “Impact of FII on Stock Market in

India” Global Journal of Finance and Management. ISSN 0975-6477 Volume 6,

Number 8 (2014), pp. 765-770.

16) Mr. Sarvanakrishanan V (2011), “Trend Analysis of FII investment of India

of Monthly flow during January 2006- October 2011” vol. ,1 no. 6, June, ISSN

2277 3622.

36