Embed Size (px)

Citation preview

Valuation

The Science

Valuation

• Art– Intangibles that make give the investment

value• Science–Determining the correct number by using

math• Voodoo–Making it fit in your portfolio

• The Art of Valuation (7 M’s)– Market– Management– Momentum– Model– Money– Magic– Match

What’d We Learn Last Time

So Now What?

Now that we understand the company, we need to develop some tangible estimates of the

actual intrinsic value of the business

Where to Start

How do we value an apple tree?

What are our options?

• Main Methods–Discounted Cash

Flow Analysis–Multiples Method• Precedent

Transactions• Trading Comps

• Tons of Others– Liquidation Value–Replacement

Value– LBO Model– Sum of Parts

DCF Model

A DCF values a company based on the Present Value of its Cash Flows and the Present Value

of its Terminal Value.

FREE CASH FLOW SUMMARY

Home depot Lowe’s

NOPLATDepreciation

Gross cash flow

Investment in operating working capitalNet capital expendituresInvestment in capitalized operating leasesInvestments in intangibles and goodwillDecrease (increase) in other operating assetsIncrease (decrease) in accumulated othercomprehensive income

Gross investment

Free cash flow

2001 2002 2003 2001 2002 2003

3,208 756

3,964

834 (3,063)

(775)(113)105

(153)

(3,165)

799

3,981 895

4,876

(194)(2,688)

(430)(164)

31 138

(3,307)

1,569

5,083 1,075

6,157

72 (3,970)

(664)(259)277 172

(4,372)

1,785

5,185 1,193

6,378

(294)(3,399)

(721)(92)58

0

(4,448)

1,930

5,741 1,321

7,062

(318)(3,708)

(780)(99)62

0

(4,843)

2,219

6,342 1,459

7,801

(344)(4,036)

(842)(107)

67

0

(5,261)

2,539

$ Million

LAN-ZWB887-20050620-13749-ZWB

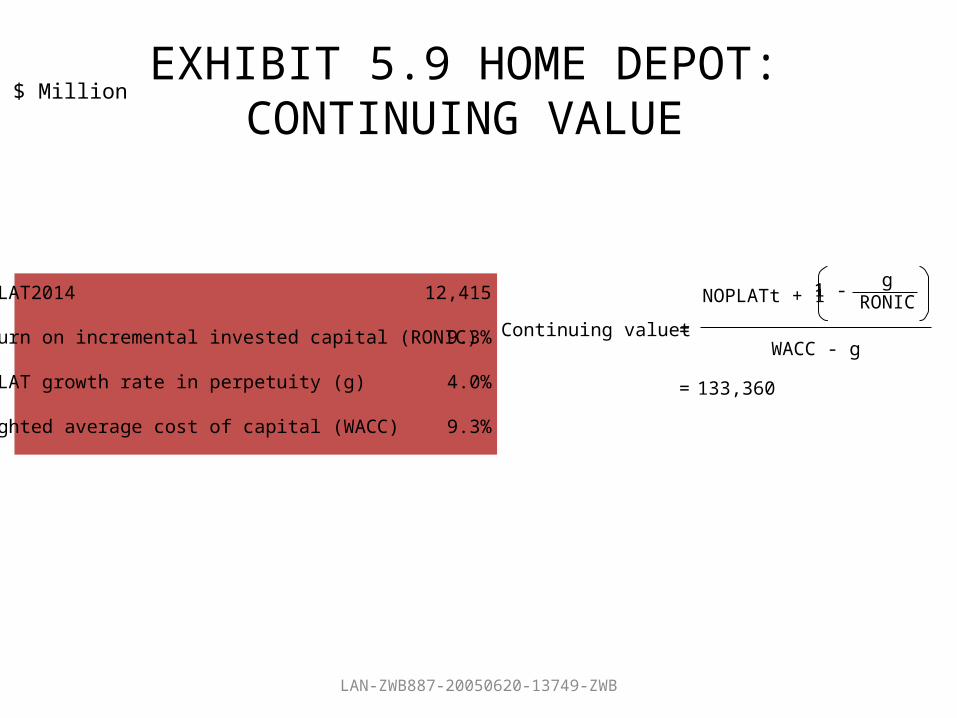

EXHIBIT 5.9 HOME DEPOT: CONTINUING VALUE

$ Million

NOPLAT2014

Return on incremental invested capital (RONIC)

NOPLAT growth rate in perpetuity (g)

Weighted average cost of capital (WACC)

12,415

9.3%

4.0%

9.3%

Continuing valuet =

NOPLATt + 1 1 - gRONIC

WACC - g

= 133,360

ENTERPRISE DCF VALUATION

Year

Free cash flow (FCF)$ Million

Discount factor @ 9.3%

Present value of FCF$ Million

2004200520062007200820092010201120122013Continuing value

1,9302,2192,5392,8933,2833,7114,1804,6915,2465,849

133,360

0.9150.8370.7660.7000.6410.5860.5360.4910.4490.4110.411

Present value of cash flow

Mid-year adjustment factor

Value of operations

Value of excess cash Value of other nonoperating assets

Enterprise value

Number of shares (at fiscal year-end 2003, million)

Estimated share value (Dollars)

1,766 1,857 1,944 2,026 2,104 2,175 2,241 2,301 2,355 2,402

54,757

75,928

1,046

79,384

1,609 84

81,077

2,257

32.41

Value of debt Value of capitalized operating leases

(1,365)(6,554)

73,158Equity value

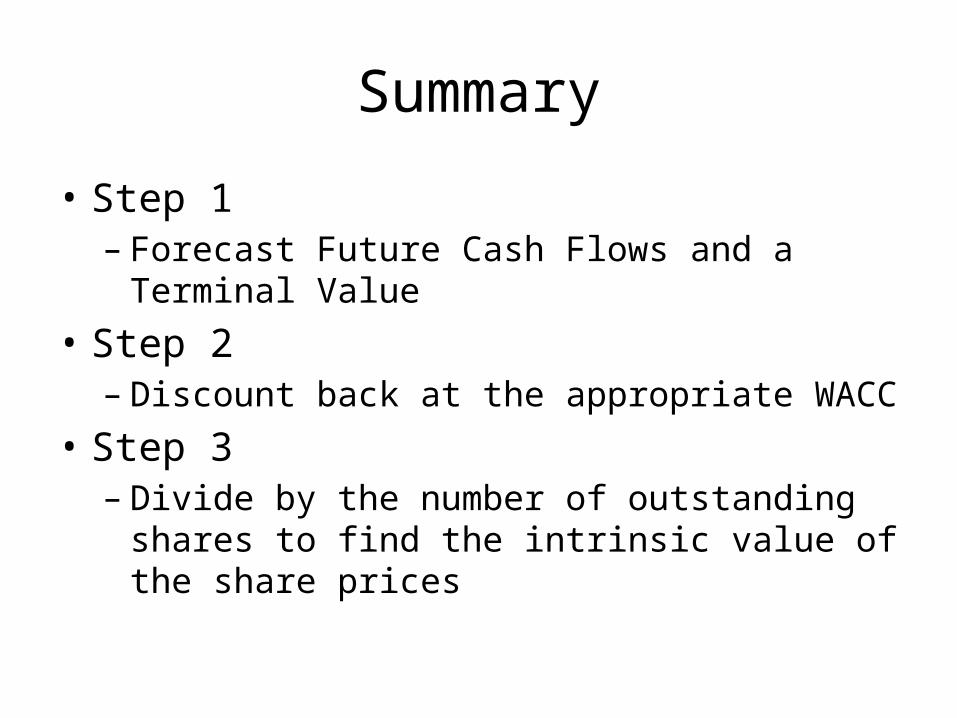

Summary

• Step 1– Forecast Future Cash Flows and a Terminal Value

• Step 2– Discount back at the appropriate WACC

• Step 3– Divide by the number of outstanding shares to

find the intrinsic value of the share prices

Using Market Multiples to Determine Relative Valuation

• Ratios that are commonly used to determine relative valuation:– EV/Revenue– EV/EBITDA– EV/EBIT– P/E (Share Price / Earnings per Share)– P/BV (Share Price / Book Value).

Some other Multiples ….

• Technology (Internet): – EV / Unique Visitors, EV / Pageviews

• Retail / Airlines: – EV / EBITDAR (Earnings Before Interest, Taxes, Depreciation,

Amortization & Rent) • Energy:

– P / MCFE, P / MCFE / D (MCFE = 1 Million Cubic Foot Equivalent, MCFE/D = MCFE per Day), P / NAV (Share Price / Net Asset Value)

• Real Estate Investment Trusts (REITs): – Price / FFO, Price / AFFO (Funds From Operations, Adjusted

Funds From Operations

Market Multiples

Market Multiples

• Determining the Appropriate Multiple– Finding Comparable Firms– Adjustments within the Sample• Growth Rate• Risk• “Quality of Earnings”

LAN-ZWB887-20050624-13827-ZWB

ADJUSTED TO ENTERPRISE VALUE MULTIPLES$ Million

Home Depot Lowe’s

Lowe’sHome Depot Difference

Raw enterprise value multiple

Adjusted enterprise value multiple

8.7

8.9

9.3

9.4

(6.6%)

(5.1%)

3,755

39,075

42,830

1,365

74,250

75,615

Outstanding debt

Market value of equity

Enterprise value

2,762

(1,033)

44,559

6,554

(1,609)

80,560

Capitalized operating leases

Excess cash

Adjusted enterprise value

4,589

154

4,743

8,691

340

9,031

2005 EBITA

Implied interest from leases

Adjusted 2005 EBITA

LAN-ZWB887-20050624-13827-ZWB

COMPARING EBITA AND EBITDA MULTIPLES

Company B

Multiples

Company Boutsourcesmanufacturing toanother company

Enterprise value ($ Million)

Enterprise value/EBITDA

Enterprise value/EBITA

Depreciation

EBITA

150.0

6.0

7.5

(5)

20

100

(35)

(40)

25

Company A

150.0

3.0

7.5

(30)

20

100

(10)

(40)

50

Revenues

Raw materials

Operating costs

EBITDA

Company BCompany A

$ Million

Final Notes

• Everything is: – Personal– Relative

• And the true price of something is only as much as something is willing to pay for it!

The End

The Digital FrontierBusiness Strategies for a Web 2.0 World

IDH3931 (M 7, W 7-8)

![HVS - Art Science of Hotel Valuation in an Economic Downturn[1]](https://img.pdfslide.net/doc/110x75/55cf9ca6550346d033aa908b/hvs-art-science-of-hotel-valuation-in-an-economic-downturn1.jpg)