Embed Size (px)

Citation preview

Latham & Watkins operates worldwide as a limited liability partnership organized under the laws of the State of Delaware (USA) with affiliated limited liability partnerships conducting the practice in the United Kingdom,

France, Italy and Singapore and as affiliated partnerships conducting the practice in Hong Kong and Japan. The Law Office of Salman M. Al-Sudairi is Latham & Watkins’ associated office in the Kingdom of Saudi Arabia. In

Qatar, Latham & Watkins LLP is licensed by the Qatar Financial Centre Authority. © Copyright 2014 Latham & Watkins. All Rights Reserved.

Barbarians at the Gate:

Shareholder Activism and Hostile Takeovers What’s a Board to Do?

Cary Hyden, Partner, Latham & Watkins, ModeratorJim Katzman, Managing Director, Goldman Sachs, Panelist

Paul Tosetti, Partner, Latham & Watkins, PanelistDaniel Katcher, Partner, Frank │Wilkinson │Brimmer │Katcher, Panelist

Arthur B. Crozier, Chairman, Innisfree M&A, Panelist

Thursday, December 4, 2014

• Increase in amount of hostile takeover activity and

shareholder activism

• Increasing level of success

• Shareholder strategies for hostile takeovers and

activism

• What’s a board to do?

2

Overview

Latham & Watkins operates worldwide as a limited liability partnership organized under the laws of the State of Delaware (USA) with affiliated limited liability partnerships conducting the practice in the United Kingdom,

France, Italy and Singapore and as affiliated partnerships conducting the practice in Hong Kong and Japan. The Law Office of Salman M. Al-Sudairi is Latham & Watkins’ associated office in the Kingdom of Saudi Arabia. In

Qatar, Latham & Watkins LLP is licensed by the Qatar Financial Centre Authority. © Copyright 2014 Latham & Watkins. All Rights Reserved.

Increase in Amount of Hostile Takeover Activity and Shareholder Activism

3

“Mr. Icahn was more accurately heralded

as a corporate raider in the 1980s.

Through the miracle of public relations,

he is now called a shareholder activist.”

4

Changing Times

Source: Al Lewis, Carl Icahn: A Student of Stupidity, The Wall Street Journal (January 26, 2014),

http://online.wsj.com/articles/SB10001424052702303947904579339041047857338

“It was not long ago the activist moniker

had a distinctly negative connotation.

That view of shareholder activists . . .

is not necessarily the current view.”

- SEC Chair Mary Joe White, December 3, 2013

“A visit from an activist shareholder is now a possibility for any publicly

traded company.” – The Economist

5

Changing Times

Sources: John Carney, Welcome to the Golden Age of Activist Investors, CNBC (August 14, 2013), http://www.cnbc.com/id/100963166

Stephen Foley, Shareholder Activism: Battle for the Boardroom, Financial Times (April 23, 2014), http://www.ft.com/cms/s/2/a555abec-be32-11e3-961f-00144feabdc0.html

David Gelles, Hostile Takeover Bids for Big Firms Across Industries Make a Comeback, The New York Times (June 12, 2014),

http://dealbook.nytimes.com/2014/06/12/hostile-takeover-bids-for-big-firms-across-industries-make-a-comeback/?_r=0/

Anything You Can Do, Icahn Do Better, The Economist (February 15, 2014), http://www.economist.com/news/business/21596556-pressure-companies-activist-shareholders-continues-grow-anything-you-can-do

“This much is clear: we're living in the golden age of activist

investors.” – CNBC

“More hedge funds today are styling themselves as activists and they

are notching up significant victories.” – Financial Times

“But the takeover effort . . . pointed to a change on Wall Street today:

Hostile deal making is back.” – The New York Times

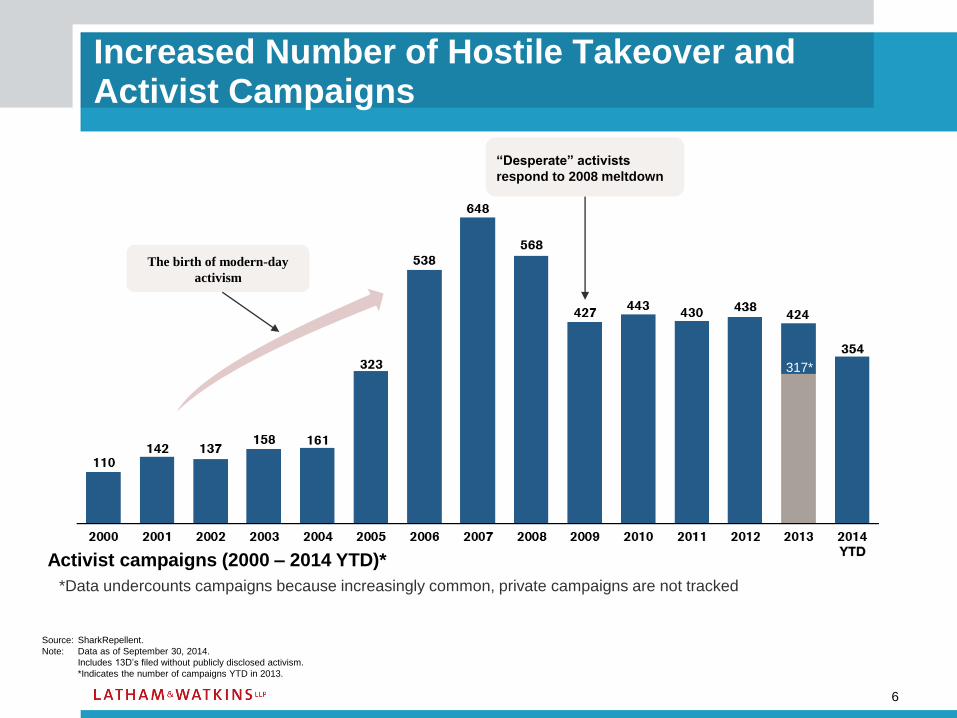

Increased Number of Hostile Takeover and Activist Campaigns

6

Source: SharkRepellent.

Note: Data as of September 30, 2014.

Includes 13D’s filed without publicly disclosed activism.

*Indicates the number of campaigns YTD in 2013.

“Desperate” activists

respond to 2008 meltdown

The birth of modern-day

activism

317*

*Data undercounts campaigns because increasingly common, private campaigns are not tracked

Activist campaigns (2000 – 2014 YTD)*

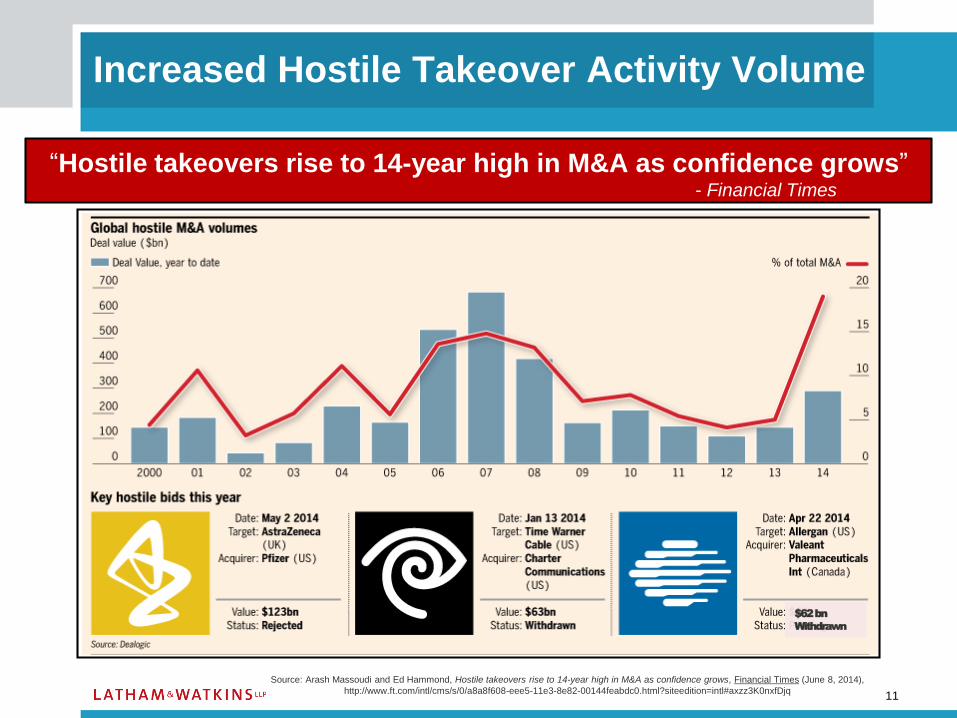

• Only a few hostile takeovers occurred over the past few years, but 25 unsolicited

takeover attempts, with a combined value of around $290 billion, have been

made this year (as of August 2014)

• Sharp increase is due largely to an improving economy, greater availability to

capital and increased pressure against implementing corporate defenses against

take-overs

• Recent changes in corporate governance have also made it easier for companies

to make hostile bids, including decreases in the use of poison pills and staggered

board terms, and increases in the concentrations of company stock in the hands of

a small number of institutional investors

7

Recent Increase in Number of Hostile Takeover Campaigns Specifically

“‘This should be the easiest time on earth to win a hostile,’ said one

senior banker who declined to be named . . .”

- The New York Times

“The Allergan offer [ ] has the potential to upend how the takeover market works,

unleashing a powerful new force in the pairing of hedge funds and corporations . . .”

- The New York Times

Sources: Arash Massoudi and Ed Hammond, Hostile takeovers rise to 14-year high in M&A as confidence grows, Financial Times (June 8, 2014),; http://www.ft.com/intl/cms/s/0/a8a8f608-eee5-11e3-8e82-

00144feabdc0.html?siteedition=intl#axzz3K0nxfDjq; David Gelles, Hostile Takeover Bids for Big Firms Across industries Make a Comeback, The New York Times (June 12, 2014),

http://dealbook.nytimes.com/2014/06/12/hostile-takeover-bids-for-big-firms-across-industries-make-a-comeback/?_r=0; Steven Davidoff Soloman, Allergan Bid Charts New Territory in Takeovers, The New York Times (April

22, 2014), http://dealbook.nytimes.com/2014/04/22/allergan-bid-charts-new-territory-in-takeovers/; Hostile takeovers return, Financier Worldwide (August 2014), http://www.financierworldwide.com/hostile-takeovers-return/.

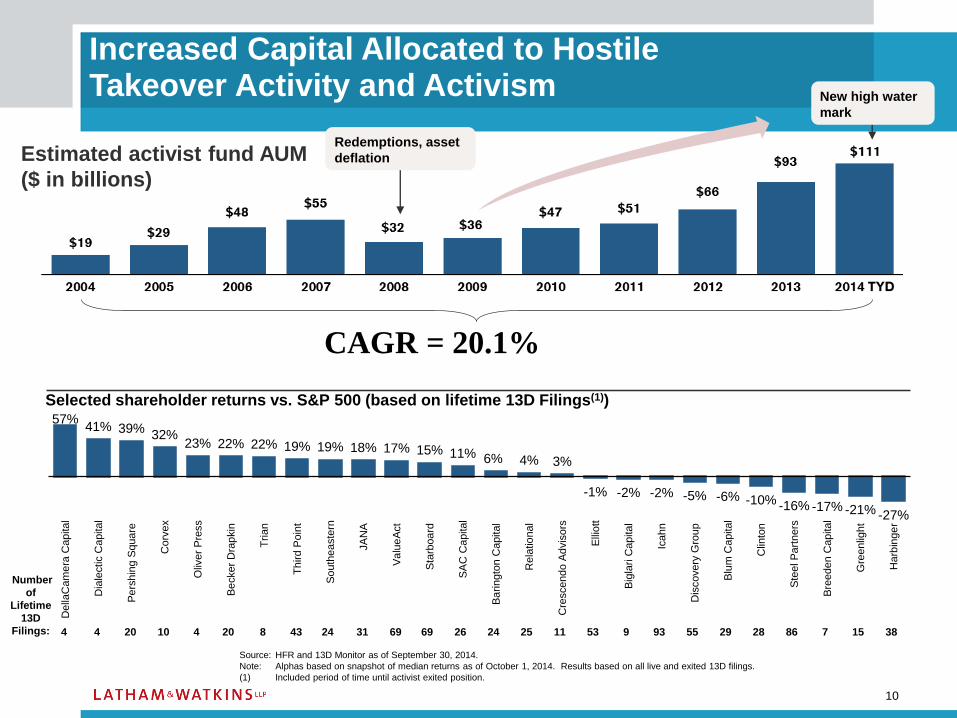

Increased Capital Allocated to Hostile Takeover Activity and Activism

More than 400 funds worldwide focus on activism as a strategy to

pursue hostile takeovers and/or other agenda

More than 150 activist funds emerged in last 2 years

8

Increased Capital Allocated to Hostile Takeover Activity and Activism

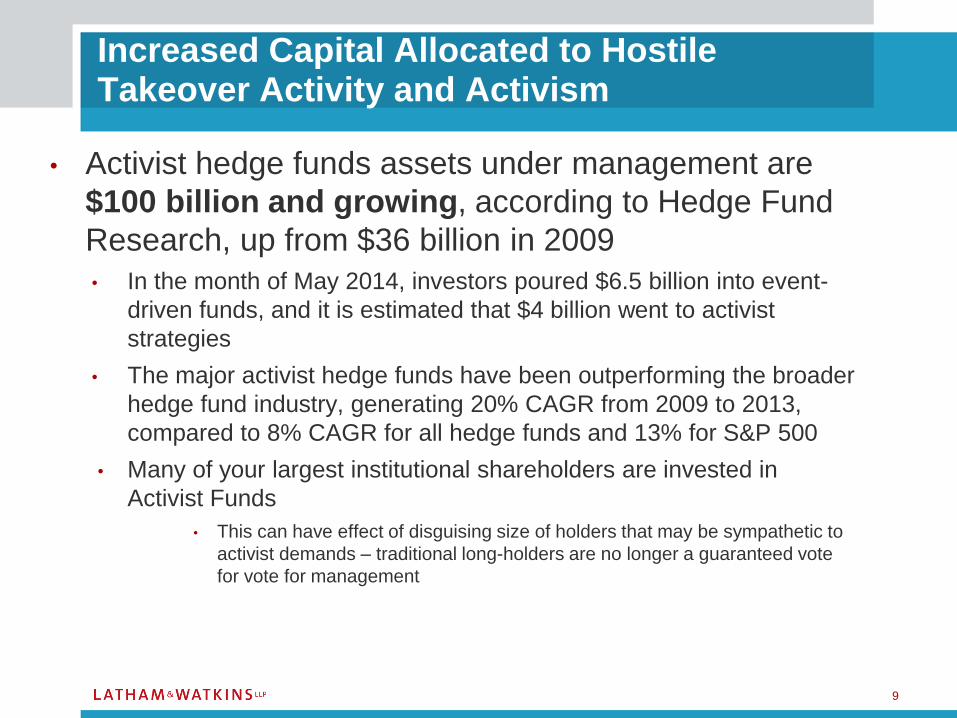

• Activist hedge funds assets under management are

$100 billion and growing, according to Hedge Fund

Research, up from $36 billion in 2009

• In the month of May 2014, investors poured $6.5 billion into event-

driven funds, and it is estimated that $4 billion went to activist

strategies

• The major activist hedge funds have been outperforming the broader

hedge fund industry, generating 20% CAGR from 2009 to 2013,

compared to 8% CAGR for all hedge funds and 13% for S&P 500

• Many of your largest institutional shareholders are invested in

Activist Funds

• This can have effect of disguising size of holders that may be sympathetic to

activist demands – traditional long-holders are no longer a guaranteed vote

for vote for management

9

10

Source: HFR and 13D Monitor as of September 30, 2014.

Note: Alphas based on snapshot of median returns as of October 1, 2014. Results based on all live and exited 13D filings.

(1) Included period of time until activist exited position.

4 4 20 10 4 20 8 43 24 31 69 69 26 24 25 11 53 9 93 55 29 28 86 7 15 38

Selected shareholder returns vs. S&P 500 (based on lifetime 13D Filings(1))

Redemptions, asset

deflation

New high water

mark

CAGR = 20.1%…because activism has created alpha

Increased Capital Allocated to Hostile Takeover Activity and Activism

57%41% 39%

32%23% 22% 22% 19% 19% 18% 17% 15% 11% 6% 4% 3%

-1% -2% -2% -5% -6% -10% -16% -17% -21% -27%

Della

Cam

era

Capital

Dia

lectic C

apital

Pe

rshin

g S

quare

Corv

ex

Oliv

er

Pre

ss

Be

cker

Dra

pkin

Tria

n

Th

ird P

oin

t

So

uth

easte

rn

JA

NA

Va

lue

Act

Sta

rboa

rd

SA

C C

apital

Ba

rin

gto

n C

apital

Rela

tio

nal

Cre

scendo A

dvis

ors

Elli

ott

Big

lari C

apital

Icahn

Dis

covery

Gro

up

Blu

m C

apital

Clin

ton

Ste

el P

art

ners

Bre

eden C

apital

Gre

enlig

ht

Harb

inge

r

Estimated activist fund AUM

($ in billions)

Number

of

Lifetime

13D

Filings:

Increased Hostile Takeover Activity Volume

“Hostile takeovers rise to 14-year high in M&A as confidence grows”- Financial Times

11

Source: Arash Massoudi and Ed Hammond, Hostile takeovers rise to 14-year high in M&A as confidence grows, Financial Times (June 8, 2014),

http://www.ft.com/intl/cms/s/0/a8a8f608-eee5-11e3-8e82-00144feabdc0.html?siteedition=intl#axzz3K0nxfDjq

$62 bn

Withdrawn

Latham & Watkins operates worldwide as a limited liability partnership organized under the laws of the State of Delaware (USA) with affiliated limited liability partnerships conducting the practice in the United Kingdom,

France, Italy and Singapore and as affiliated partnerships conducting the practice in Hong Kong and Japan. The Law Office of Salman M. Al-Sudairi is Latham & Watkins’ associated office in the Kingdom of Saudi Arabia. In

Qatar, Latham & Watkins LLP is licensed by the Qatar Financial Centre Authority. © Copyright 2014 Latham & Watkins. All Rights Reserved.

Increasing Level of Success

12

13

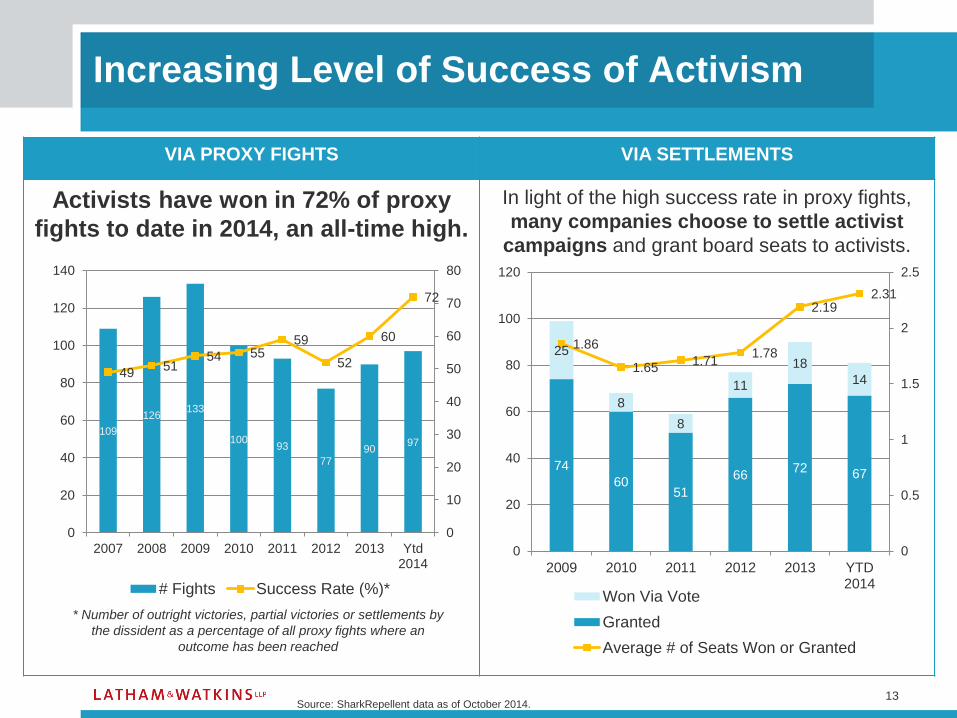

Increasing Level of Success of Activism

VIA PROXY FIGHTS VIA SETTLEMENTS

Activists have won in 72% of proxy

fights to date in 2014, an all-time high.

In light of the high success rate in proxy fights,

many companies choose to settle activist

campaigns and grant board seats to activists.

109

126133

10093

7790

97

4951

54 5559

52

60

72

0

10

20

30

40

50

60

70

80

0

20

40

60

80

100

120

140

2007 2008 2009 2010 2011 2012 2013 Ytd2014

# Fights Success Rate (%)*

* Number of outright victories, partial victories or settlements by

the dissident as a percentage of all proxy fights where an

outcome has been reached

74

6051

6672 67

25

8

8

11

18

14

1.86

1.651.71

1.78

2.192.31

0

0.5

1

1.5

2

2.5

0

20

40

60

80

100

120

2009 2010 2011 2012 2013 YTD2014

Won Via Vote

Granted

Average # of Seats Won or Granted

Source: SharkRepellent data as of October 2014.

Increasing Pressure to Settle with Activists

• Large cap targets require the support of “vanilla” investors

• Mainstream investors are often quiescent unless and until they

are offered a free option (e.g., a premium offer, an activist

alternative plan, etc.)

• To many institutions, activism appears to create alpha

uncorrelated to the market• Mainstream investors have been willing to support activists with successful

track records

• Mainstream investors volunteering their views to activists behind the scenes

• “Taking the high road” and avoiding personal attacks, “poison

pen” letters• Invoking corporate governance “best practices” in their campaigns

• Positioning campaigns as promoting long-term value vs. short-term financial

engineering

• Running more impressive director slates

14

“As Activist Investors Gain Strength, Boards Surrender to Demands.”

- The New York Times

Source: Steven Davidoff Soloman, As Activist Investors Gain Strength, Boards Surrender to Demands, The New York Times (October 14, 2014),

http://dealbook.nytimes.com/2014/10/14/as-activist-shareholders-gain-strength-boards-surrender-to-demands/

Successful Hostile Takeover Attempts Still Remain Elusive

• Require a commitment of

resources, and failed bids have

large sunk costs

• Require a willingness to

engage in a war with a

reluctant target

• In growing economy, targets

have confidence to reject bids

and remain independent

• In growing economy, there are

other bidders available

15

Sources: Arash Massoudi and Ed Hammond, Hostile takeovers rise to 14-year high in M&A as confidence grows, Financial Times (June 8,

2014),; http://www.ft.com/intl/cms/s/0/a8a8f608-eee5-11e3-8e82-00144feabdc0.html?siteedition=intl#axzz3K0nxfDjq; David Gelles, Hostile

Takeover Bids for Big Firms Across industries Make a Comeback, The New York Times (June 12, 2014),

http://dealbook.nytimes.com/2014/06/12/hostile-takeover-bids-for-big-firms-across-industries-make-a-comeback/?_r=0

But hostile tactics are evolving (e.g., activists and hostile bidders

joining forces), increasing the pressures on targeted companies

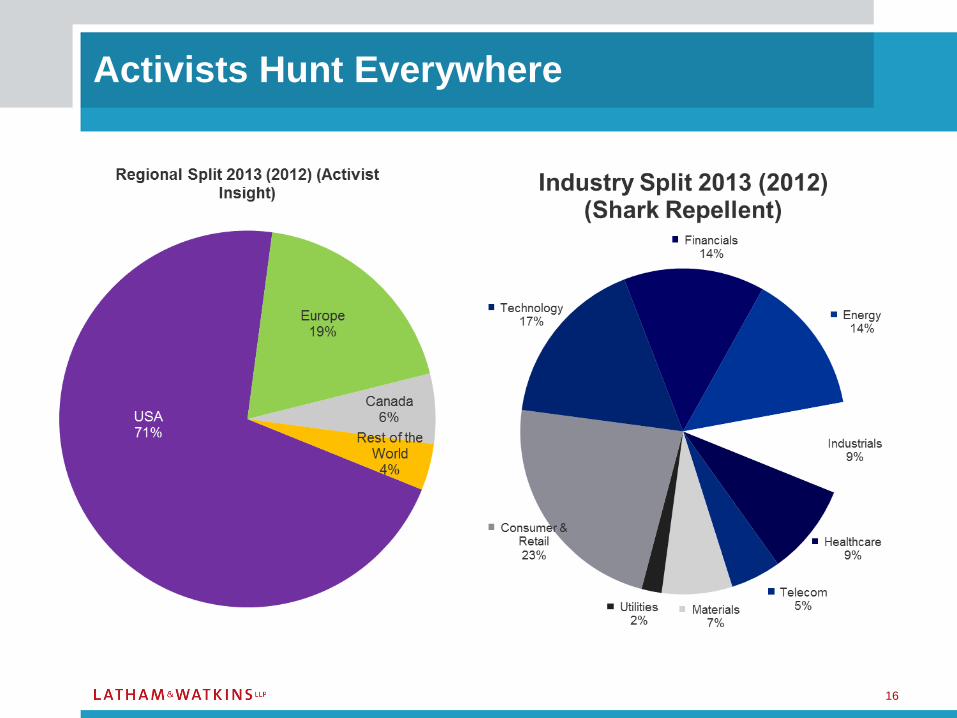

Activists Hunt Everywhere

16

Latham & Watkins operates worldwide as a limited liability partnership organized under the laws of the State of Delaware (USA) with affiliated limited liability partnerships conducting the practice in the United Kingdom,

France, Italy and Singapore and as affiliated partnerships conducting the practice in Hong Kong and Japan. The Law Office of Salman M. Al-Sudairi is Latham & Watkins’ associated office in the Kingdom of Saudi Arabia. In

Qatar, Latham & Watkins LLP is licensed by the Qatar Financial Centre Authority. © Copyright 2014 Latham & Watkins. All Rights Reserved.

Shareholder Strategies for Hostile Takeovers and

Activism

17

Activists’ Two Different Types of Threats

Abusive Takeover Tactics

• Tender offer at inadequate price

• Creeping accumulations or aggressive block purchases

• Partial tender offers

• Public “bear hug” to put company “in play”

Stockholder Activism

• Disproportionate governance role relative to ownership

• Ill-advised or untimely extraordinary corporate transactions

• Leveraged recap or other capital restructuring

• Sale or spin of business segments

• Sale of the entire company

18

Activists’ Specific Demands and Platforms

19

DEMANDS

M&A Activism Sale of company

Sell or spin-off divisions

Hold up transactions for sweeteners

Balance Sheet Activism Share buybacks, special dividends

Operational Activism Replace management

Rationalize cost structure

Governance Activism Replace directors

Push for governance “best practices”

PLATFORMS COMPANY ACTIVIST

Change board (most common)

Stock buyback/special dividend

Spin-off or sell division

Sale of company

Operational/change management

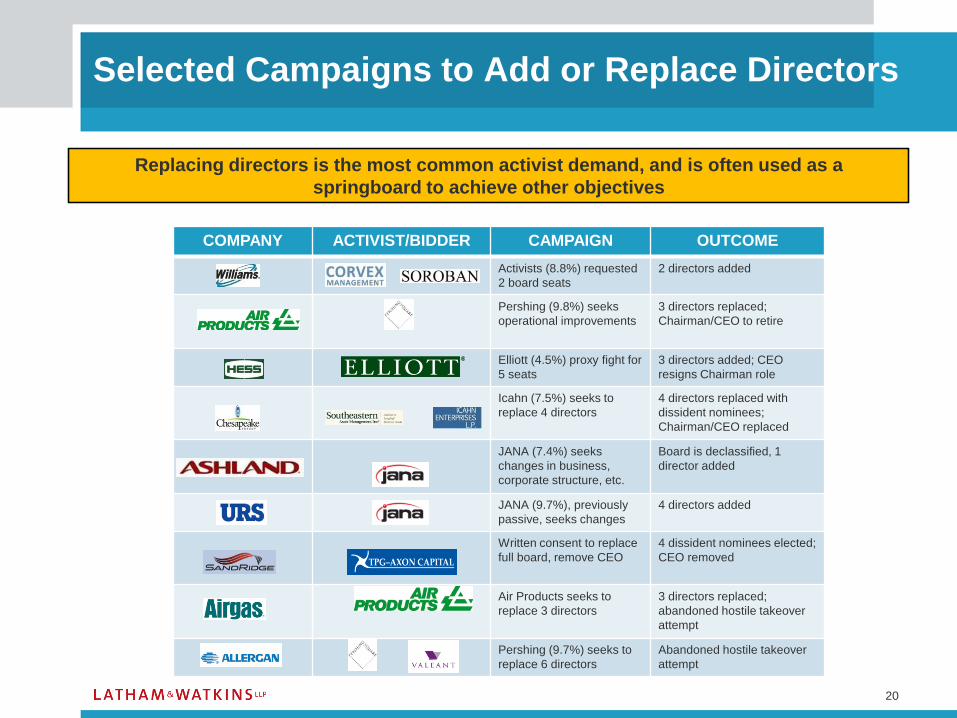

COMPANY ACTIVIST/BIDDER CAMPAIGN OUTCOME

Activists (8.8%) requested

2 board seats

2 directors added

Pershing (9.8%) seeks

operational improvements

3 directors replaced;

Chairman/CEO to retire

Elliott (4.5%) proxy fight for

5 seats

3 directors added; CEO

resigns Chairman role

Icahn (7.5%) seeks to

replace 4 directors

4 directors replaced with

dissident nominees;

Chairman/CEO replaced

JANA (7.4%) seeks

changes in business,

corporate structure, etc.

Board is declassified, 1

director added

JANA (9.7%), previously

passive, seeks changes

4 directors added

Written consent to replace

full board, remove CEO

4 dissident nominees elected;

CEO removed

Air Products seeks to

replace 3 directors

3 directors replaced;

abandoned hostile takeover

attempt

Pershing (9.7%) seeks to

replace 6 directors

Abandoned hostile takeover

attempt

20

Selected Campaigns to Add or Replace Directors

Replacing directors is the most common activist demand, and is often used as a

springboard to achieve other objectives

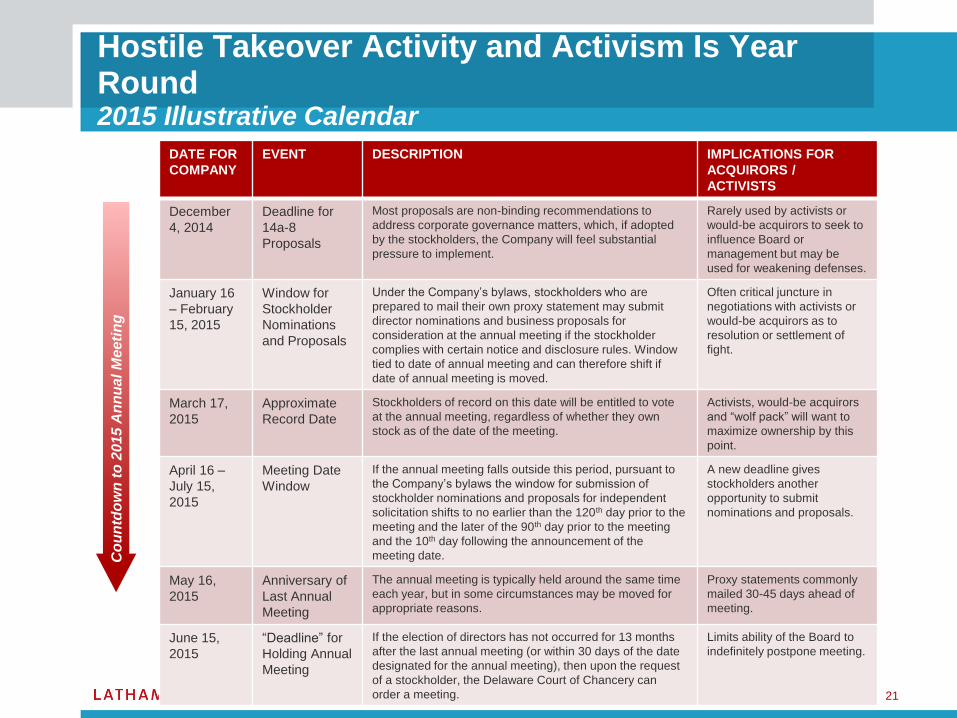

Hostile Takeover Activity and Activism Is Year Round2015 Illustrative Calendar

21

DATE FOR

COMPANY

EVENT DESCRIPTION IMPLICATIONS FOR

ACQUIRORS /

ACTIVISTS

December

4, 2014

Deadline for

14a-8

Proposals

Most proposals are non-binding recommendations to

address corporate governance matters, which, if adopted

by the stockholders, the Company will feel substantial

pressure to implement.

Rarely used by activists or

would-be acquirors to seek to

influence Board or

management but may be

used for weakening defenses.

January 16

– February

15, 2015

Window for

Stockholder

Nominations

and Proposals

Under the Company’s bylaws, stockholders who are

prepared to mail their own proxy statement may submit

director nominations and business proposals for

consideration at the annual meeting if the stockholder

complies with certain notice and disclosure rules. Window

tied to date of annual meeting and can therefore shift if

date of annual meeting is moved.

Often critical juncture in

negotiations with activists or

would-be acquirors as to

resolution or settlement of

fight.

March 17,

2015

Approximate

Record Date

Stockholders of record on this date will be entitled to vote

at the annual meeting, regardless of whether they own

stock as of the date of the meeting.

Activists, would-be acquirors

and “wolf pack” will want to

maximize ownership by this

point.

April 16 –

July 15,

2015

Meeting Date

Window

If the annual meeting falls outside this period, pursuant to

the Company’s bylaws the window for submission of

stockholder nominations and proposals for independent

solicitation shifts to no earlier than the 120th day prior to the

meeting and the later of the 90th day prior to the meeting

and the 10th day following the announcement of the

meeting date.

A new deadline gives

stockholders another

opportunity to submit

nominations and proposals.

May 16,

2015

Anniversary of

Last Annual

Meeting

The annual meeting is typically held around the same time

each year, but in some circumstances may be moved for

appropriate reasons.

Proxy statements commonly

mailed 30-45 days ahead of

meeting.

June 15,

2015

“Deadline” for

Holding Annual

Meeting

If the election of directors has not occurred for 13 months

after the last annual meeting (or within 30 days of the date

designated for the annual meeting), then upon the request

of a stockholder, the Delaware Court of Chancery can

order a meeting.

Limits ability of the Board to

indefinitely postpone meeting.

Co

un

tdo

wn

to

201

5 A

nn

ual M

eeti

ng

22

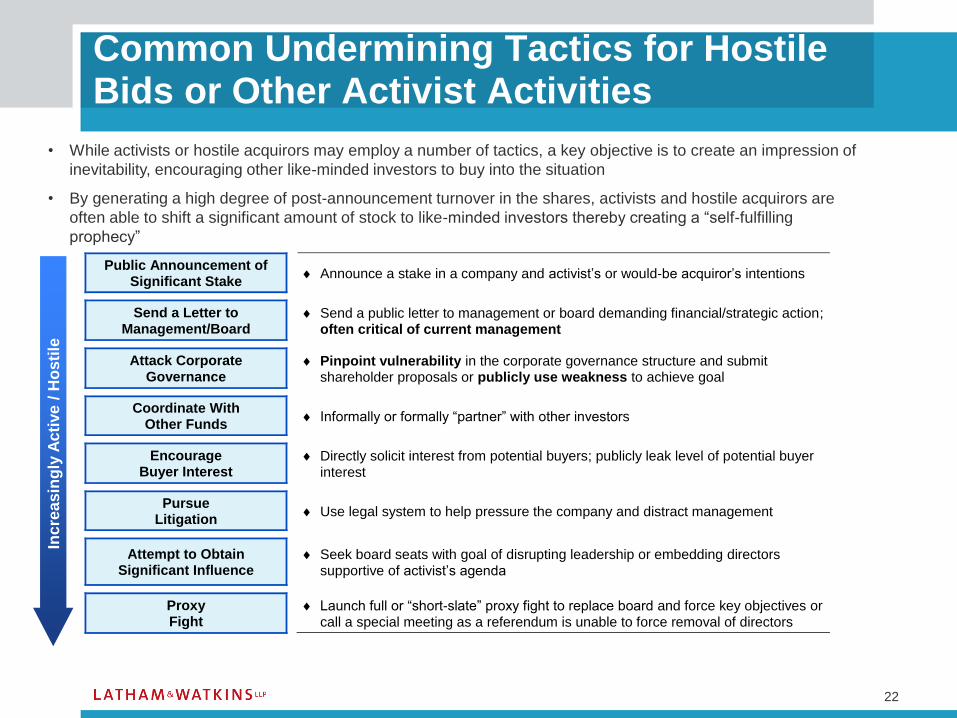

Common Undermining Tactics for Hostile Bids or Other Activist Activities

• While activists or hostile acquirors may employ a number of tactics, a key objective is to create an impression of

inevitability, encouraging other like-minded investors to buy into the situation

• By generating a high degree of post-announcement turnover in the shares, activists and hostile acquirors are

often able to shift a significant amount of stock to like-minded investors thereby creating a “self-fulfilling

prophecy”

Public Announcement of Significant Stake

Announce a stake in a company and activist’s or would-be acquiror’s intentions

Send a Letter to

Management/Board

Send a public letter to management or board demanding financial/strategic action; often critical of current management

Attack Corporate

Governance

Pinpoint vulnerability in the corporate governance structure and submit shareholder proposals or publicly use weakness to achieve goal

Coordinate With

Other Funds Informally or formally “partner” with other investors

Encourage

Buyer Interest

Directly solicit interest from potential buyers; publicly leak level of potential buyer interest

Pursue

Litigation Use legal system to help pressure the company and distract management

Attempt to Obtain

Significant Influence

Seek board seats with goal of disrupting leadership or embedding directors supportive of activist’s agenda

Proxy Fight

Launch full or “short-slate” proxy fight to replace board and force key objectives or call a special meeting as a referendum is unable to force removal of directors

Inc

rea

sin

gly

Ac

tive

/ H

os

tile

Latham & Watkins operates worldwide as a limited liability partnership organized under the laws of the State of Delaware (USA) with affiliated limited liability partnerships conducting the practice in the United Kingdom,

France, Italy and Singapore and as affiliated partnerships conducting the practice in Hong Kong and Japan. The Law Office of Salman M. Al-Sudairi is Latham & Watkins’ associated office in the Kingdom of Saudi Arabia. In

Qatar, Latham & Watkins LLP is licensed by the Qatar Financial Centre Authority. © Copyright 2014 Latham & Watkins. All Rights Reserved.

What’s a Board To Do?

23

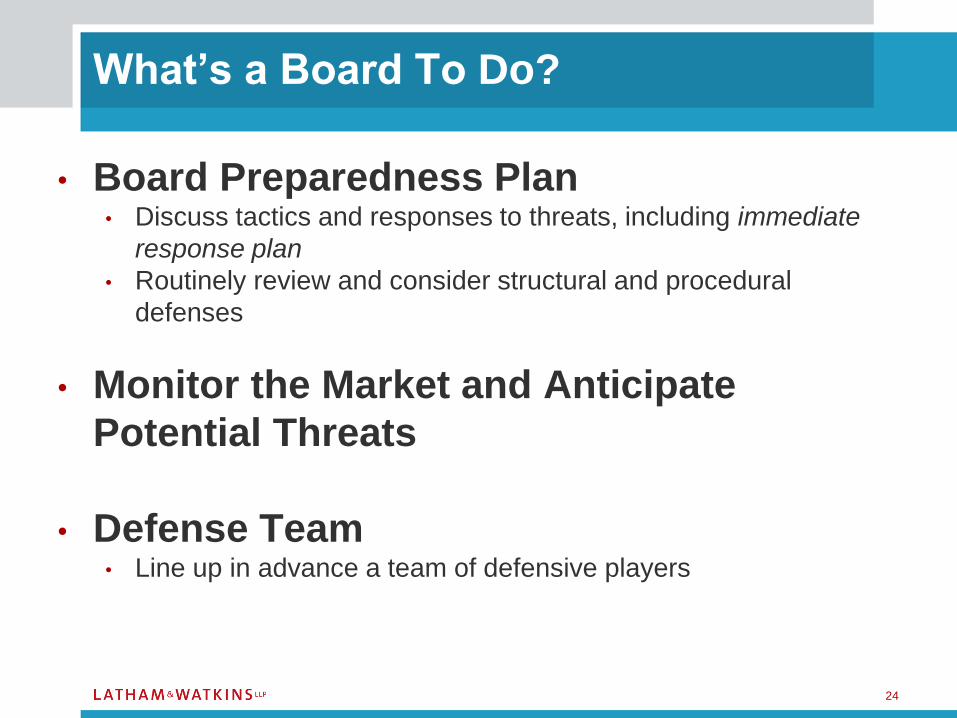

What’s a Board To Do?

24

• Board Preparedness Plan• Discuss tactics and responses to threats, including immediate

response plan

• Routinely review and consider structural and procedural

defenses

• Monitor the Market and Anticipate

Potential Threats

• Defense Team• Line up in advance a team of defensive players

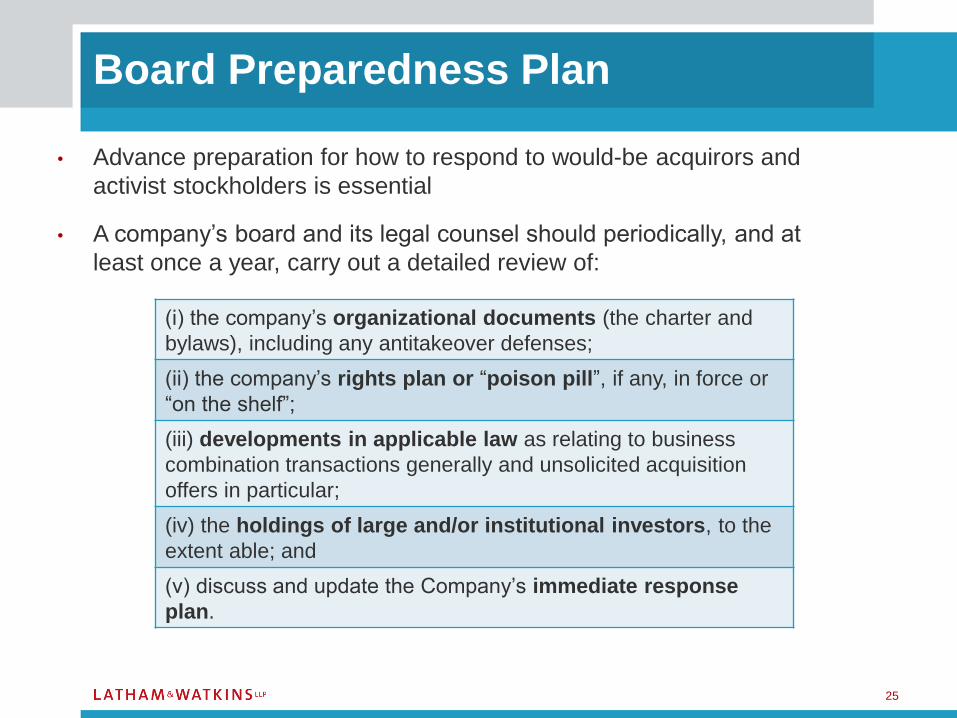

Board Preparedness Plan

25

• Advance preparation for how to respond to would-be acquirors and

activist stockholders is essential

• A company’s board and its legal counsel should periodically, and at

least once a year, carry out a detailed review of:

(i) the company’s organizational documents (the charter and

bylaws), including any antitakeover defenses;

(ii) the company’s rights plan or “poison pill”, if any, in force or

“on the shelf”;

(iii) developments in applicable law as relating to business

combination transactions generally and unsolicited acquisition

offers in particular;

(iv) the holdings of large and/or institutional investors, to the

extent able; and

(v) discuss and update the Company’s immediate response

plan.

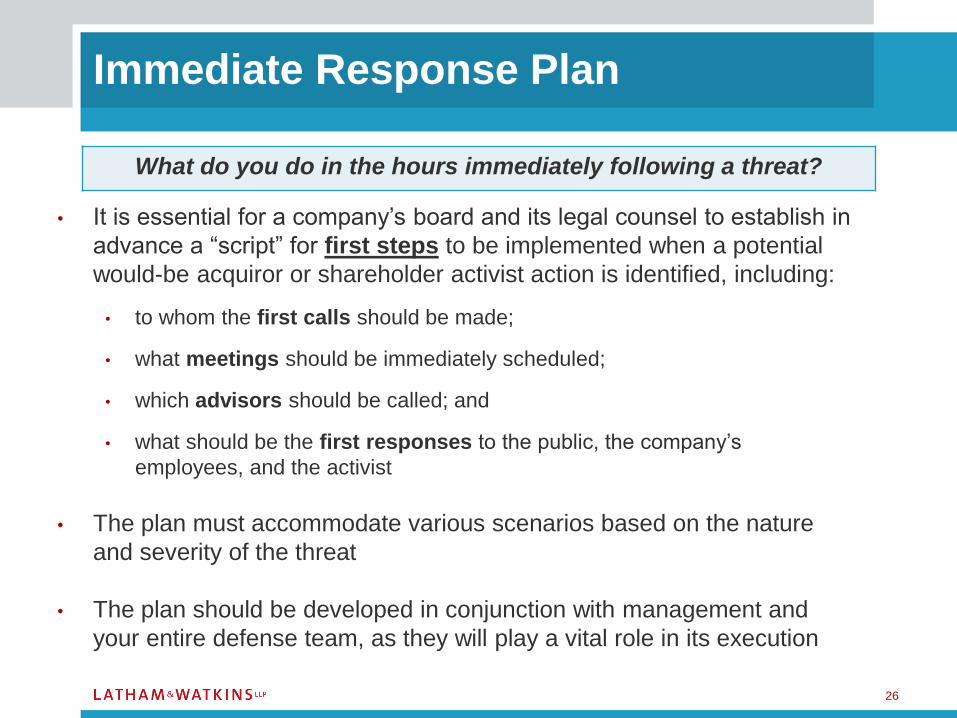

Immediate Response Plan

26

• It is essential for a company’s board and its legal counsel to establish in

advance a “script” for first steps to be implemented when a potential

would-be acquiror or shareholder activist action is identified, including:

• to whom the first calls should be made;

• what meetings should be immediately scheduled;

• which advisors should be called; and

• what should be the first responses to the public, the company’s

employees, and the activist

• The plan must accommodate various scenarios based on the nature

and severity of the threat

• The plan should be developed in conjunction with management and

your entire defense team, as they will play a vital role in its execution

What do you do in the hours immediately following a threat?

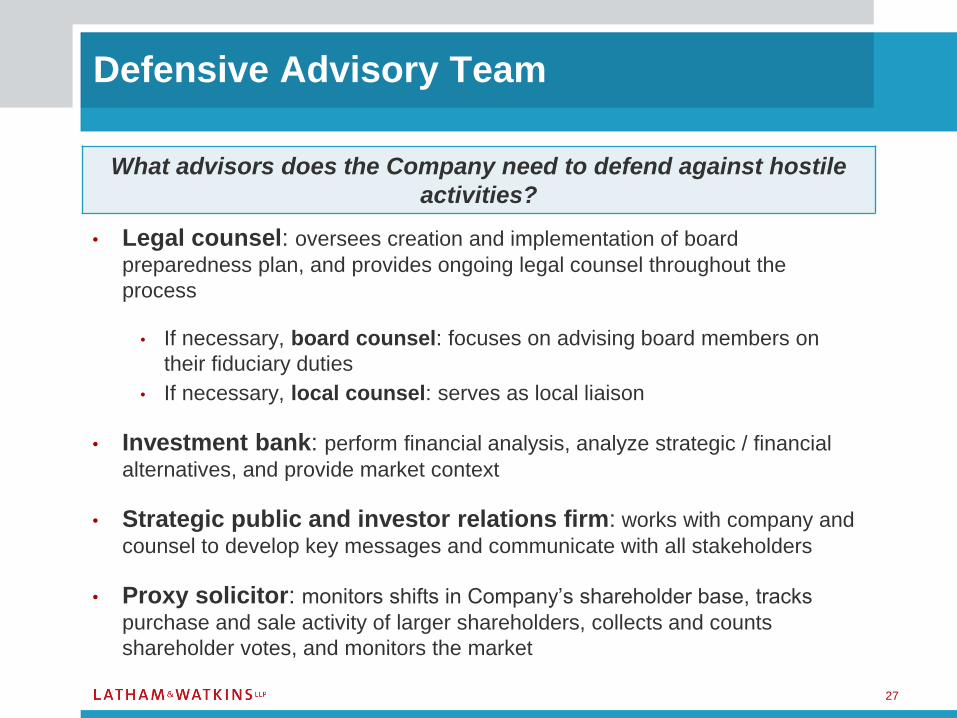

• Legal counsel: oversees creation and implementation of board

preparedness plan, and provides ongoing legal counsel throughout the

process

• If necessary, board counsel: focuses on advising board members on

their fiduciary duties

• If necessary, local counsel: serves as local liaison

• Investment bank: perform financial analysis, analyze strategic / financial

alternatives, and provide market context

• Strategic public and investor relations firm: works with company and

counsel to develop key messages and communicate with all stakeholders

• Proxy solicitor: monitors shifts in Company’s shareholder base, tracks

purchase and sale activity of larger shareholders, collects and counts

shareholder votes, and monitors the market

27

Defensive Advisory Team

What advisors does the Company need to defend against hostile

activities?

28

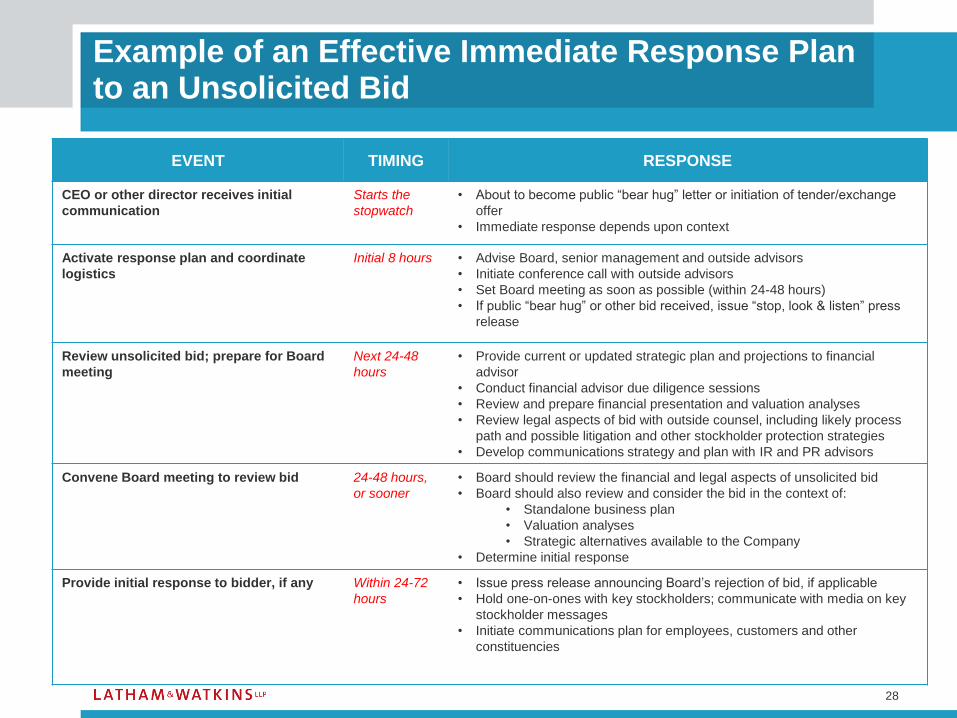

Example of an Effective Immediate Response Plan to an Unsolicited Bid

EVENT TIMING RESPONSE

CEO or other director receives initial

communication

Starts the

stopwatch

• About to become public “bear hug” letter or initiation of tender/exchange

offer

• Immediate response depends upon context

Activate response plan and coordinate

logistics

Initial 8 hours • Advise Board, senior management and outside advisors

• Initiate conference call with outside advisors

• Set Board meeting as soon as possible (within 24-48 hours)

• If public “bear hug” or other bid received, issue “stop, look & listen” press

release

Review unsolicited bid; prepare for Board

meeting

Next 24-48

hours

• Provide current or updated strategic plan and projections to financial

advisor

• Conduct financial advisor due diligence sessions

• Review and prepare financial presentation and valuation analyses

• Review legal aspects of bid with outside counsel, including likely process

path and possible litigation and other stockholder protection strategies

• Develop communications strategy and plan with IR and PR advisors

Convene Board meeting to review bid 24-48 hours,

or sooner

• Board should review the financial and legal aspects of unsolicited bid

• Board should also review and consider the bid in the context of:

• Standalone business plan

• Valuation analyses

• Strategic alternatives available to the Company

• Determine initial response

Provide initial response to bidder, if any Within 24-72

hours

• Issue press release announcing Board’s rejection of bid, if applicable

• Hold one-on-ones with key stockholders; communicate with media on key

stockholder messages

• Initiate communications plan for employees, customers and other

constituencies

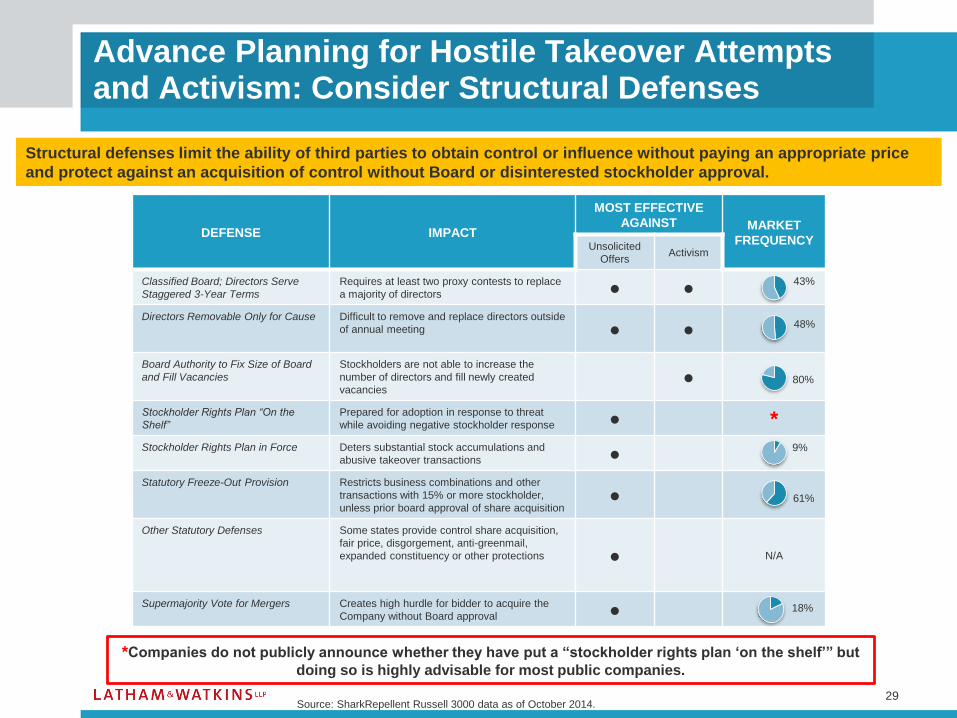

Advance Planning for Hostile Takeover Attempts and Activism: Consider Structural Defenses

DEFENSE IMPACT

MOST EFFECTIVE

AGAINST MARKET

FREQUENCYUnsolicited

OffersActivism

Classified Board; Directors Serve

Staggered 3-Year Terms

Requires at least two proxy contests to replace

a majority of directors ● ●

Directors Removable Only for Cause Difficult to remove and replace directors outside

of annual meeting ● ●

Board Authority to Fix Size of Board

and Fill Vacancies

Stockholders are not able to increase the

number of directors and fill newly created

vacancies●

Stockholder Rights Plan “On the

Shelf”

Prepared for adoption in response to threat

while avoiding negative stockholder response ● *Stockholder Rights Plan in Force Deters substantial stock accumulations and

abusive takeover transactions ●

Statutory Freeze-Out Provision Restricts business combinations and other

transactions with 15% or more stockholder,

unless prior board approval of share acquisition●

Other Statutory Defenses Some states provide control share acquisition,

fair price, disgorgement, anti-greenmail,

expanded constituency or other protections ● N/A

Supermajority Vote for Mergers Creates high hurdle for bidder to acquire the

Company without Board approval ●

Source: SharkRepellent Russell 3000 data as of October 2014.

Structural defenses limit the ability of third parties to obtain control or influence without paying an appropriate price

and protect against an acquisition of control without Board or disinterested stockholder approval.

43%

61%

48%

9%

80%

18%

29

*Companies do not publicly announce whether they have put a “stockholder rights plan ‘on the shelf’” but

doing so is highly advisable for most public companies.

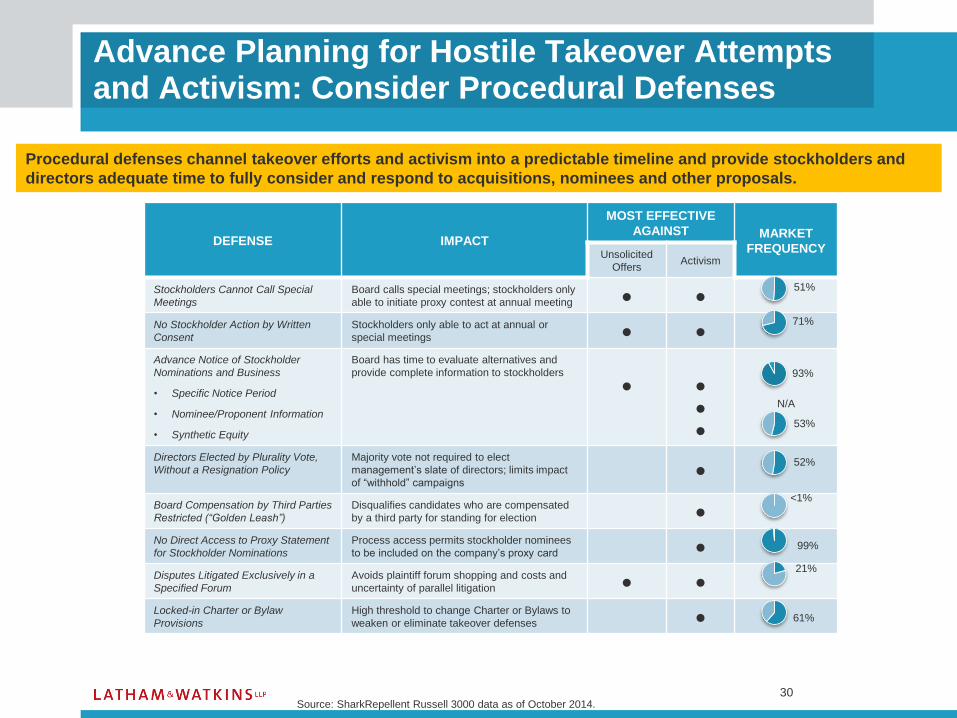

Advance Planning for Hostile Takeover Attemptsand Activism: Consider Procedural Defenses

DEFENSE IMPACT

MOST EFFECTIVE

AGAINST MARKET

FREQUENCYUnsolicited

OffersActivism

Stockholders Cannot Call Special

Meetings

Board calls special meetings; stockholders only

able to initiate proxy contest at annual meeting ● ●

No Stockholder Action by Written

Consent

Stockholders only able to act at annual or

special meetings ● ●

Advance Notice of Stockholder

Nominations and Business

• Specific Notice Period

• Nominee/Proponent Information

• Synthetic Equity

Board has time to evaluate alternatives and

provide complete information to stockholders

● ●

●

●

N/A

Directors Elected by Plurality Vote,

Without a Resignation Policy

Majority vote not required to elect

management’s slate of directors; limits impact

of “withhold” campaigns●

Board Compensation by Third Parties

Restricted (“Golden Leash”)

Disqualifies candidates who are compensated

by a third party for standing for election ●

No Direct Access to Proxy Statement

for Stockholder Nominations

Process access permits stockholder nominees

to be included on the company’s proxy card ●

Disputes Litigated Exclusively in a

Specified Forum

Avoids plaintiff forum shopping and costs and

uncertainty of parallel litigation ● ●

Locked-in Charter or Bylaw

Provisions

High threshold to change Charter or Bylaws to

weaken or eliminate takeover defenses ●

Source: SharkRepellent Russell 3000 data as of October 2014.

71%

93%

99%

21%

<1%

61%

51%

Procedural defenses channel takeover efforts and activism into a predictable timeline and provide stockholders and

directors adequate time to fully consider and respond to acquisitions, nominees and other proposals.

52%

53%

30

• Proxy advisory firms, including Institutional Shareholder Services (“ISS”)

and Glass Lewis & Co., LLC, issue guidance to institutional investors on

how to vote on proxy matters and helps institutional investors execute

their votes

• ISS is the largest such proxy advisory firm, with a 61% market share• ISS helps over 1,700 clients execute nearly 7 million ballots representing 2.7 trillion shares

31

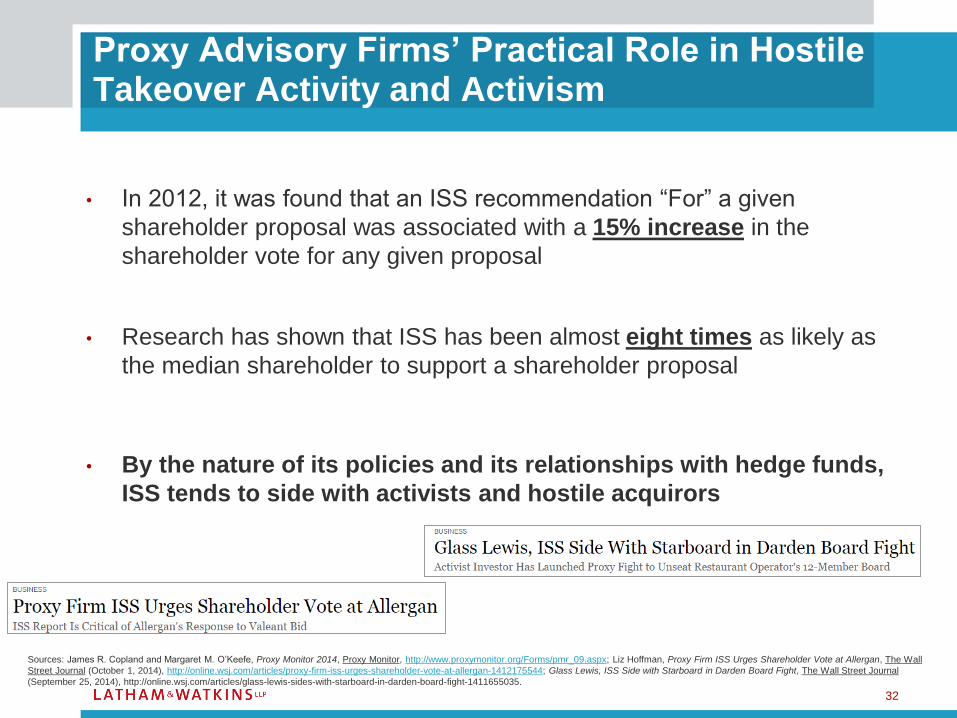

Proxy Advisory Firms’ Practical Role in Hostile Takeover Activity and Activism

Sources: James R. Copland and Margaret M. O’Keefe, Proxy Monitor 2014, Proxy Monitor, http://www.proxymonitor.org/Forms/pmr_09.aspx; Liz Hoffman, Proxy Firm ISS Urges Shareholder Vote at Allergan, The Wall

Street Journal (October 1, 2014), http://online.wsj.com/articles/proxy-firm-iss-urges-hareholder-vote-at-allergan-1412175544; Glass Lewis, ISS Side with Starboard in Darden Board Fight, The Wall Street Journal

(September 25, 2014), http://online.wsj.com/articles/glass-lewis-sides-with-starboard-in-darden-board-fight-1411655035.

• In 2012, it was found that an ISS recommendation “For” a given

shareholder proposal was associated with a 15% increase in the

shareholder vote for any given proposal

• Research has shown that ISS has been almost eight times as likely as

the median shareholder to support a shareholder proposal

• By the nature of its policies and its relationships with hedge funds,

ISS tends to side with activists and hostile acquirors

32

Proxy Advisory Firms’ Practical Role in Hostile Takeover Activity and Activism

Sources: James R. Copland and Margaret M. O’Keefe, Proxy Monitor 2014, Proxy Monitor, http://www.proxymonitor.org/Forms/pmr_09.aspx; Liz Hoffman, Proxy Firm ISS Urges Shareholder Vote at Allergan, The Wall

Street Journal (October 1, 2014), http://online.wsj.com/articles/proxy-firm-iss-urges-shareholder-vote-at-allergan-1412175544; Glass Lewis, ISS Side with Starboard in Darden Board Fight, The Wall Street Journal

(September 25, 2014), http://online.wsj.com/articles/glass-lewis-sides-with-starboard-in-darden-board-fight-1411655035.

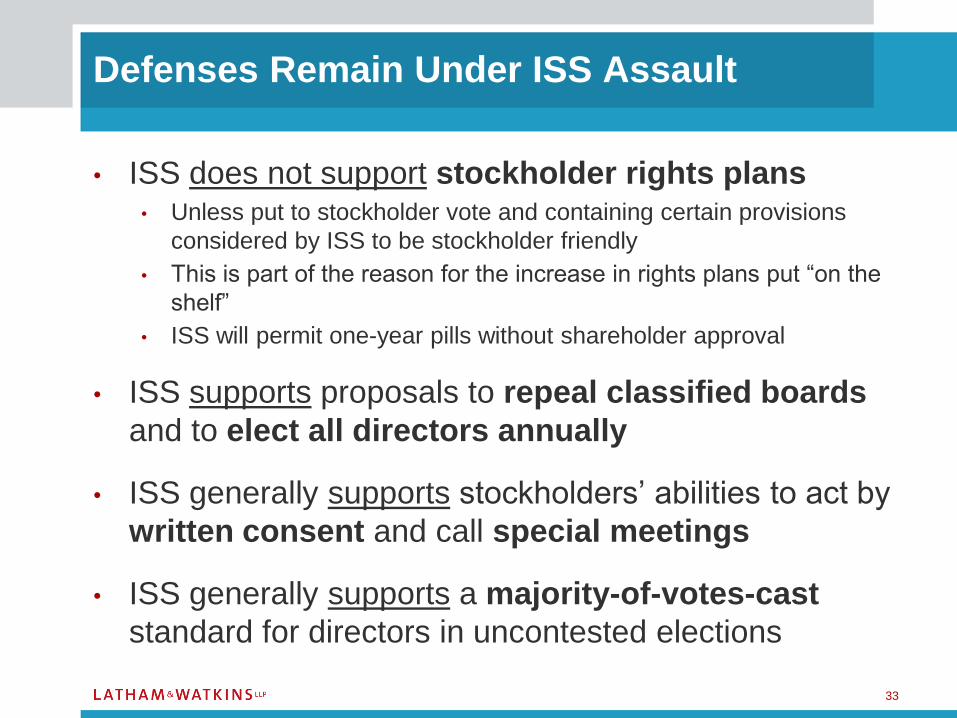

• ISS does not support stockholder rights plans• Unless put to stockholder vote and containing certain provisions

considered by ISS to be stockholder friendly

• This is part of the reason for the increase in rights plans put “on the

shelf”

• ISS will permit one-year pills without shareholder approval

• ISS supports proposals to repeal classified boards

and to elect all directors annually

• ISS generally supports stockholders’ abilities to act by

written consent and call special meetings

• ISS generally supports a majority-of-votes-cast

standard for directors in uncontested elections

33

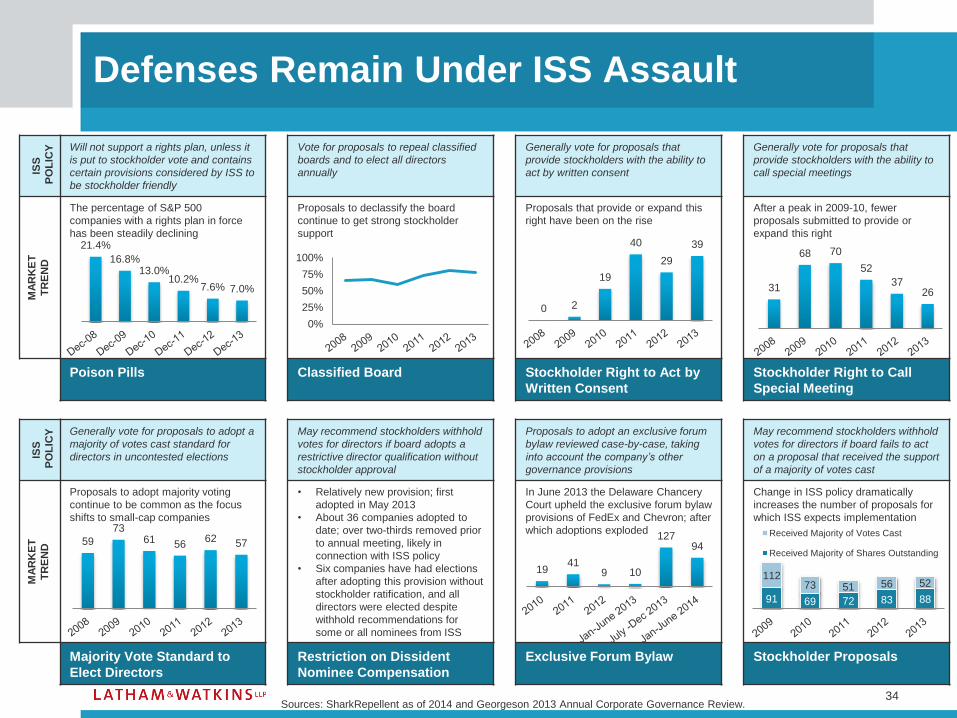

Defenses Remain Under ISS Assault

34

Defenses Remain Under ISS AssaultIS

S

PO

LIC

Y Will not support a rights plan, unless it

is put to stockholder vote and contains

certain provisions considered by ISS to

be stockholder friendly

Vote for proposals to repeal classified

boards and to elect all directors

annually

Generally vote for proposals that

provide stockholders with the ability to

act by written consent

Generally vote for proposals that

provide stockholders with the ability to

call special meetings

MA

RK

ET

TR

EN

D

The percentage of S&P 500

companies with a rights plan in force

has been steadily declining

Proposals to declassify the board

continue to get strong stockholder

support

Proposals that provide or expand this

right have been on the rise

After a peak in 2009-10, fewer

proposals submitted to provide or

expand this right

Poison Pills Classified Board Stockholder Right to Act by

Written Consent

Stockholder Right to Call

Special Meeting

ISS

PO

LIC

Y Generally vote for proposals to adopt a

majority of votes cast standard for

directors in uncontested elections

May recommend stockholders withhold

votes for directors if board adopts a

restrictive director qualification without

stockholder approval

Proposals to adopt an exclusive forum

bylaw reviewed case-by-case, taking

into account the company’s other

governance provisions

May recommend stockholders withhold

votes for directors if board fails to act

on a proposal that received the support

of a majority of votes cast

MA

RK

ET

TR

EN

D

Proposals to adopt majority voting

continue to be common as the focus

shifts to small-cap companies

• Relatively new provision; first

adopted in May 2013

• About 36 companies adopted to

date; over two-thirds removed prior

to annual meeting, likely in

connection with ISS policy

• Six companies have had elections

after adopting this provision without

stockholder ratification, and all

directors were elected despite

withhold recommendations for

some or all nominees from ISS

In June 2013 the Delaware Chancery

Court upheld the exclusive forum bylaw

provisions of FedEx and Chevron; after

which adoptions exploded

Change in ISS policy dramatically

increases the number of proposals for

which ISS expects implementation

Majority Vote Standard to

Elect Directors

Restriction on Dissident

Nominee Compensation

Exclusive Forum Bylaw Stockholder Proposals

Sources: SharkRepellent as of 2014 and Georgeson 2013 Annual Corporate Governance Review.

0 2

19

40

29

39

0%

25%

50%

75%

100%

1941

9 10

1279459

7361 56

62 57

21.4%

16.8%13.0%

10.2%7.6% 7.0% 31

68 70

52

3726

91 69 72 83 88

11273 51 56 52

Received Majority of Votes Cast

Received Majority of Shares Outstanding

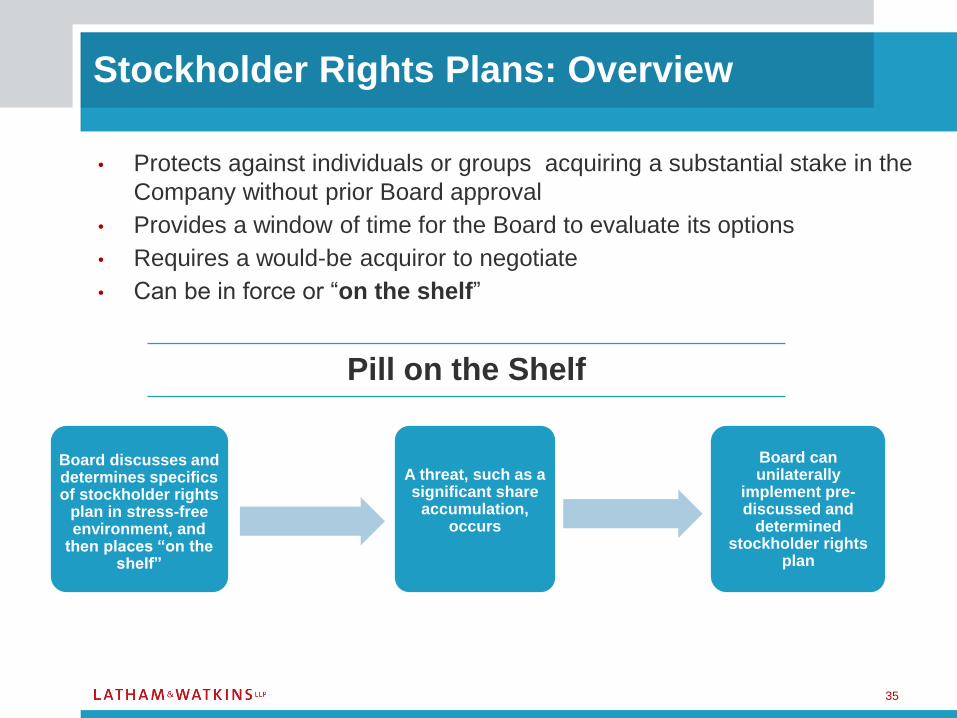

• Protects against individuals or groups acquiring a substantial stake in the

Company without prior Board approval

• Provides a window of time for the Board to evaluate its options

• Requires a would-be acquiror to negotiate

• Can be in force or “on the shelf”

35

Stockholder Rights Plans: Overview

A threat, such as a significant share

accumulation, occurs

Board discusses and determines specifics of stockholder rights

plan in stress-free environment, and

then places “on the shelf”

Board can unilaterally

implement pre-discussed and

determined stockholder rights

plan

Pill on the Shelf

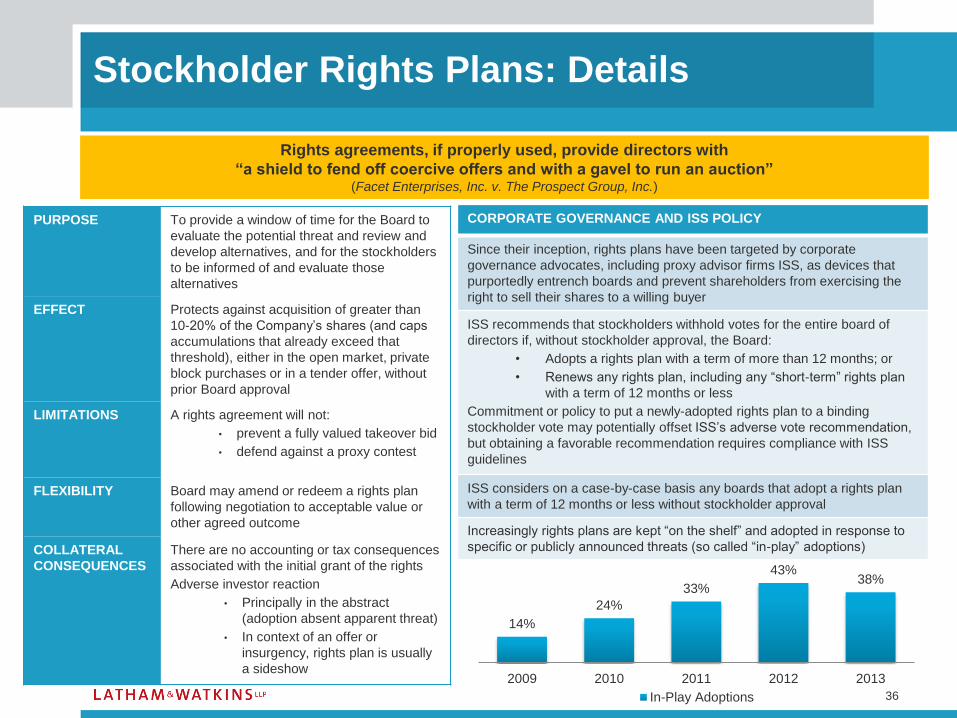

Stockholder Rights Plans: Details

PURPOSE To provide a window of time for the Board to

evaluate the potential threat and review and

develop alternatives, and for the stockholders

to be informed of and evaluate those

alternatives

EFFECT Protects against acquisition of greater than

10-20% of the Company’s shares (and caps

accumulations that already exceed that

threshold), either in the open market, private

block purchases or in a tender offer, without

prior Board approval

LIMITATIONS A rights agreement will not:

• prevent a fully valued takeover bid

• defend against a proxy contest

FLEXIBILITY Board may amend or redeem a rights plan

following negotiation to acceptable value or

other agreed outcome

COLLATERAL

CONSEQUENCES

There are no accounting or tax consequences

associated with the initial grant of the rights

Adverse investor reaction

• Principally in the abstract

(adoption absent apparent threat)

• In context of an offer or

insurgency, rights plan is usually

a sideshow

CORPORATE GOVERNANCE AND ISS POLICY

Since their inception, rights plans have been targeted by corporate

governance advocates, including proxy advisor firms ISS, as devices that

purportedly entrench boards and prevent shareholders from exercising the

right to sell their shares to a willing buyer

ISS recommends that stockholders withhold votes for the entire board of

directors if, without stockholder approval, the Board:

• Adopts a rights plan with a term of more than 12 months; or

• Renews any rights plan, including any “short-term” rights plan

with a term of 12 months or less

Commitment or policy to put a newly-adopted rights plan to a binding

stockholder vote may potentially offset ISS’s adverse vote recommendation,

but obtaining a favorable recommendation requires compliance with ISS

guidelines

ISS considers on a case-by-case basis any boards that adopt a rights plan

with a term of 12 months or less without stockholder approval

Increasingly rights plans are kept “on the shelf” and adopted in response to

specific or publicly announced threats (so called “in-play” adoptions)

36

Rights agreements, if properly used, provide directors with

“a shield to fend off coercive offers and with a gavel to run an auction”(Facet Enterprises, Inc. v. The Prospect Group, Inc.)

14%

24%

33%

43%38%

2009 2010 2011 2012 2013

In-Play Adoptions

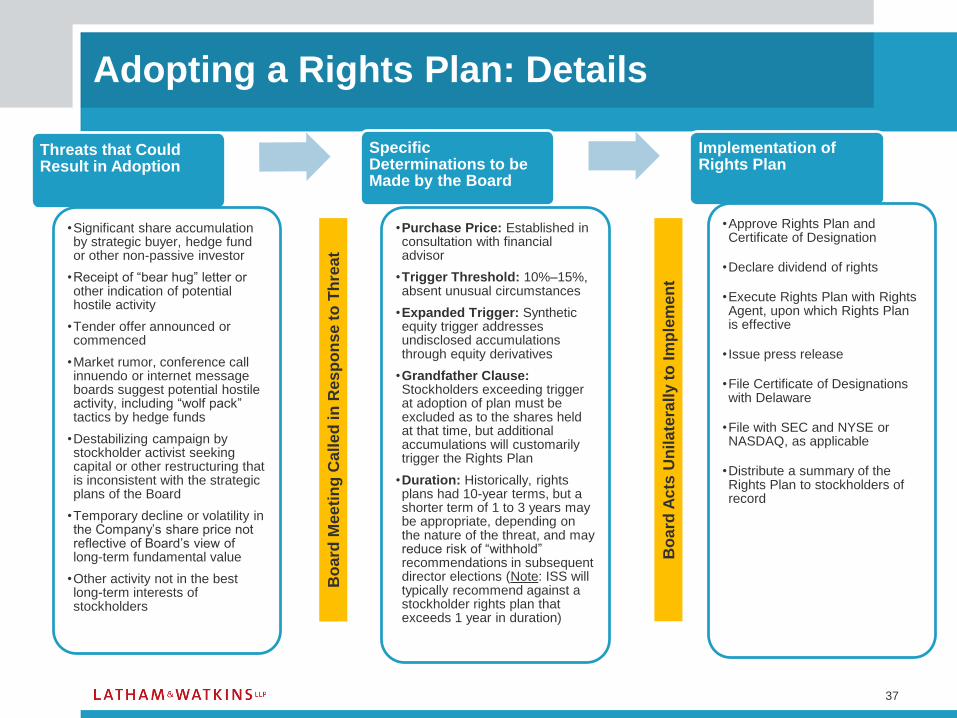

Threats that Could Result in Adoption

•Significant share accumulation by strategic buyer, hedge fund or other non-passive investor

•Receipt of “bear hug” letter or other indication of potential hostile activity

•Tender offer announced or commenced

•Market rumor, conference call innuendo or internet message boards suggest potential hostile activity, including “wolf pack” tactics by hedge funds

•Destabilizing campaign by stockholder activist seeking capital or other restructuring that is inconsistent with the strategic plans of the Board

•Temporary decline or volatility in the Company’s share price not reflective of Board’s view of long-term fundamental value

•Other activity not in the best long-term interests of stockholders

Specific Determinations to be Made by the Board

•Purchase Price: Established in consultation with financial advisor

•Trigger Threshold: 10%–15%, absent unusual circumstances

•Expanded Trigger: Synthetic equity trigger addresses undisclosed accumulations through equity derivatives

•Grandfather Clause:Stockholders exceeding trigger at adoption of plan must be excluded as to the shares held at that time, but additional accumulations will customarily trigger the Rights Plan

•Duration: Historically, rights plans had 10-year terms, but a shorter term of 1 to 3 years may be appropriate, depending on the nature of the threat, and may reduce risk of “withhold” recommendations in subsequent director elections (Note: ISS will typically recommend against a stockholder rights plan that exceeds 1 year in duration)

Implementation of Rights Plan

•Approve Rights Plan and Certificate of Designation

•Declare dividend of rights

•Execute Rights Plan with Rights Agent, upon which Rights Plan is effective

• Issue press release

•File Certificate of Designations with Delaware

•File with SEC and NYSE or NASDAQ, as applicable

•Distribute a summary of the Rights Plan to stockholders of record

Adopting a Rights Plan: Details

37

Bo

ard

Mee

tin

g C

all

ed

in

Res

po

nse

to

Th

rea

t

Bo

ard

Ac

ts U

nil

ate

rall

y t

o I

mp

lem

en

t

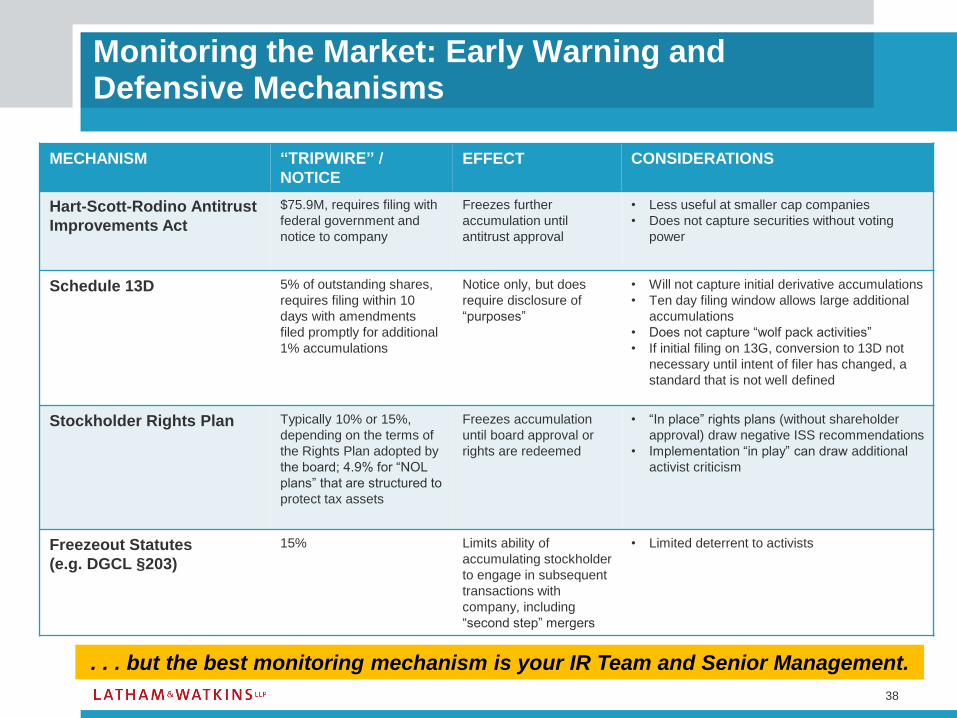

Monitoring the Market: Early Warning and Defensive Mechanisms

MECHANISM “TRIPWIRE” /

NOTICE

EFFECT CONSIDERATIONS

Hart-Scott-Rodino Antitrust

Improvements Act

$75.9M, requires filing with

federal government and

notice to company

Freezes further

accumulation until

antitrust approval

• Less useful at smaller cap companies

• Does not capture securities without voting

power

Schedule 13D 5% of outstanding shares,

requires filing within 10

days with amendments

filed promptly for additional

1% accumulations

Notice only, but does

require disclosure of

“purposes”

• Will not capture initial derivative accumulations

• Ten day filing window allows large additional

accumulations

• Does not capture “wolf pack activities”

• If initial filing on 13G, conversion to 13D not

necessary until intent of filer has changed, a

standard that is not well defined

Stockholder Rights Plan Typically 10% or 15%,

depending on the terms of

the Rights Plan adopted by

the board; 4.9% for “NOL

plans” that are structured to

protect tax assets

Freezes accumulation

until board approval or

rights are redeemed

• “In place” rights plans (without shareholder

approval) draw negative ISS recommendations

• Implementation “in play” can draw additional

activist criticism

Freezeout Statutes

(e.g. DGCL §203)

15% Limits ability of

accumulating stockholder

to engage in subsequent

transactions with

company, including

“second step” mergers

• Limited deterrent to activists

38

. . . but the best monitoring mechanism is your IR Team and Senior Management.

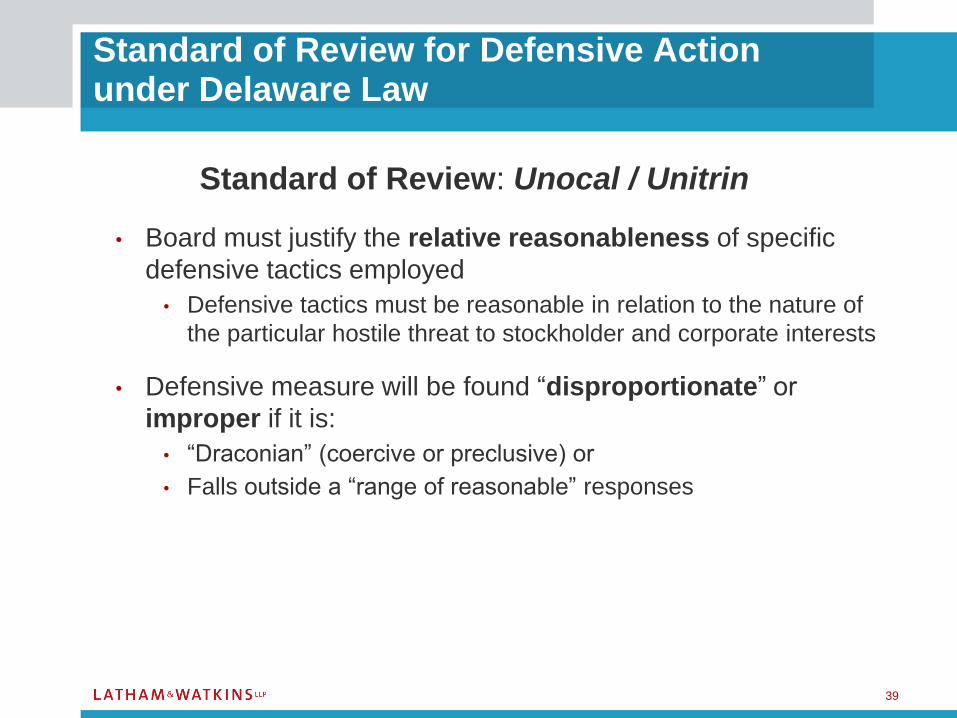

Standard of Review: Unocal / Unitrin

• Board must justify the relative reasonableness of specific

defensive tactics employed

• Defensive tactics must be reasonable in relation to the nature of

the particular hostile threat to stockholder and corporate interests

• Defensive measure will be found “disproportionate” or

improper if it is:

• “Draconian” (coercive or preclusive) or

• Falls outside a “range of reasonable” responses

39

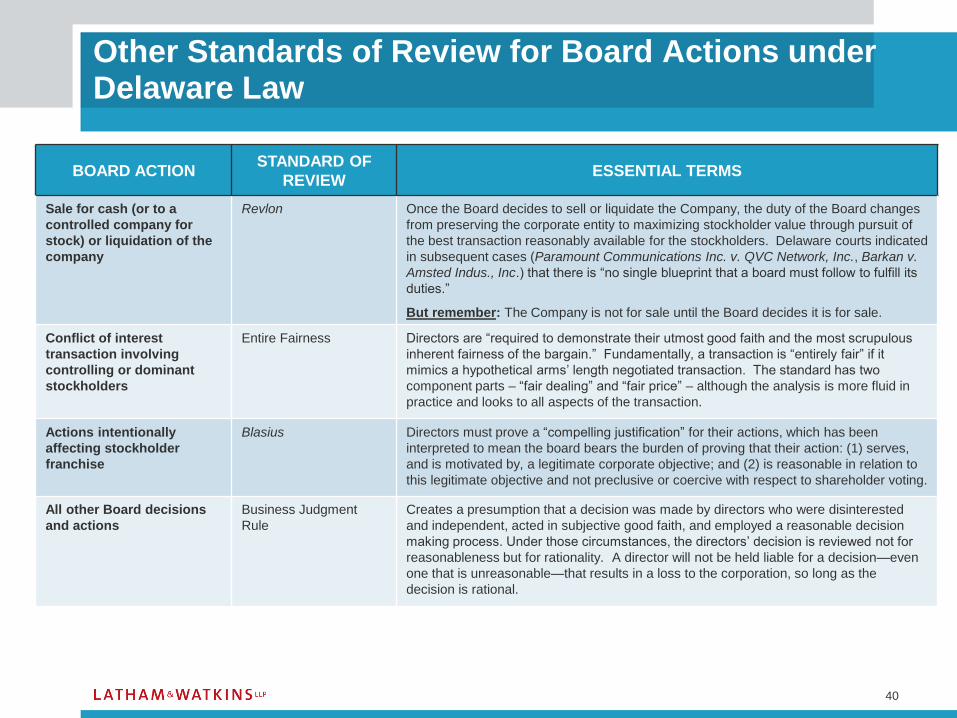

Standard of Review for Defensive Action under Delaware Law

Other Standards of Review for Board Actions under Delaware Law

BOARD ACTIONSTANDARD OF

REVIEWESSENTIAL TERMS

Sale for cash (or to a

controlled company for

stock) or liquidation of the

company

Revlon Once the Board decides to sell or liquidate the Company, the duty of the Board changes

from preserving the corporate entity to maximizing stockholder value through pursuit of

the best transaction reasonably available for the stockholders. Delaware courts indicated

in subsequent cases (Paramount Communications Inc. v. QVC Network, Inc., Barkan v.

Amsted Indus., Inc.) that there is “no single blueprint that a board must follow to fulfill its

duties.”

But remember: The Company is not for sale until the Board decides it is for sale.

Conflict of interest

transaction involving

controlling or dominant

stockholders

Entire Fairness Directors are “required to demonstrate their utmost good faith and the most scrupulous

inherent fairness of the bargain.” Fundamentally, a transaction is “entirely fair” if it

mimics a hypothetical arms’ length negotiated transaction. The standard has two

component parts – “fair dealing” and “fair price” – although the analysis is more fluid in

practice and looks to all aspects of the transaction.

Actions intentionally

affecting stockholder

franchise

Blasius Directors must prove a “compelling justification” for their actions, which has been

interpreted to mean the board bears the burden of proving that their action: (1) serves,

and is motivated by, a legitimate corporate objective; and (2) is reasonable in relation to

this legitimate objective and not preclusive or coercive with respect to shareholder voting.

All other Board decisions

and actions

Business Judgment

Rule

Creates a presumption that a decision was made by directors who were disinterested

and independent, acted in subjective good faith, and employed a reasonable decision

making process. Under those circumstances, the directors’ decision is reviewed not for

reasonableness but for rationality. A director will not be held liable for a decision—even

one that is unreasonable—that results in a loss to the corporation, so long as the

decision is rational.

40

41

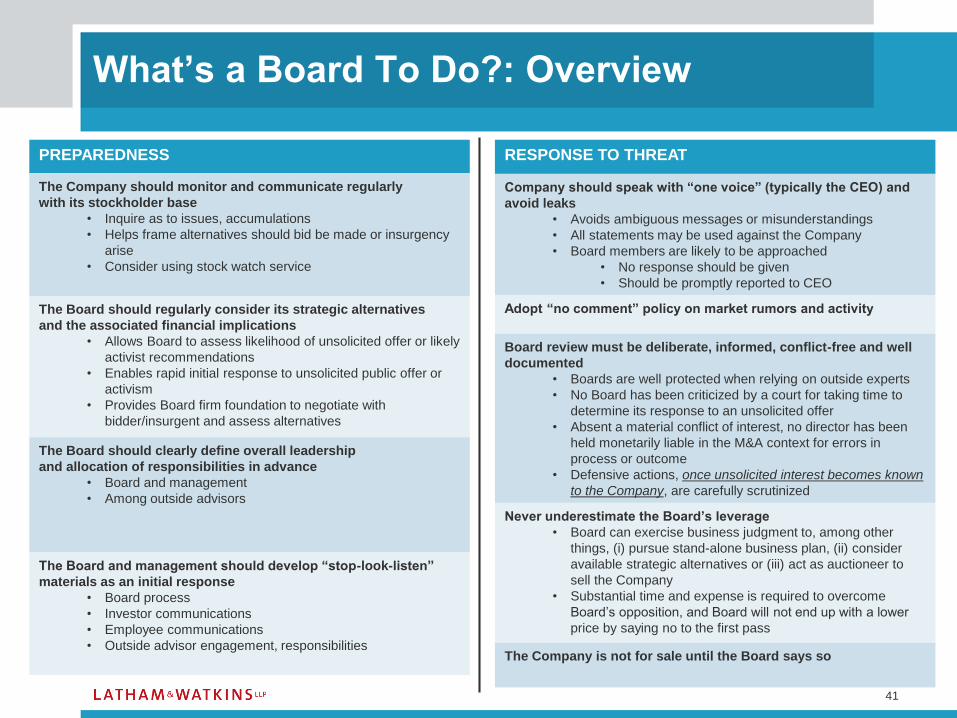

What’s a Board To Do?: Overview

PREPAREDNESS

The Company should monitor and communicate regularly

with its stockholder base

• Inquire as to issues, accumulations

• Helps frame alternatives should bid be made or insurgency

arise

• Consider using stock watch service

The Board should regularly consider its strategic alternatives

and the associated financial implications

• Allows Board to assess likelihood of unsolicited offer or likely

activist recommendations

• Enables rapid initial response to unsolicited public offer or

activism

• Provides Board firm foundation to negotiate with

bidder/insurgent and assess alternatives

The Board should clearly define overall leadership

and allocation of responsibilities in advance

• Board and management

• Among outside advisors

The Board and management should develop “stop-look-listen”

materials as an initial response

• Board process

• Investor communications

• Employee communications

• Outside advisor engagement, responsibilities

RESPONSE TO THREAT

Company should speak with “one voice” (typically the CEO) and

avoid leaks

• Avoids ambiguous messages or misunderstandings

• All statements may be used against the Company

• Board members are likely to be approached

• No response should be given

• Should be promptly reported to CEO

Adopt “no comment” policy on market rumors and activity

Board review must be deliberate, informed, conflict-free and well

documented

• Boards are well protected when relying on outside experts

• No Board has been criticized by a court for taking time to

determine its response to an unsolicited offer

• Absent a material conflict of interest, no director has been

held monetarily liable in the M&A context for errors in

process or outcome

• Defensive actions, once unsolicited interest becomes known

to the Company, are carefully scrutinized

Never underestimate the Board’s leverage

• Board can exercise business judgment to, among other

things, (i) pursue stand-alone business plan, (ii) consider

available strategic alternatives or (iii) act as auctioneer to

sell the Company

• Substantial time and expense is required to overcome

Board’s opposition, and Board will not end up with a lower

price by saying no to the first pass

The Company is not for sale until the Board says so

Latham & Watkins operates worldwide as a limited liability partnership organized under the laws of the State of Delaware (USA) with affiliated limited liability partnerships conducting the practice in the United Kingdom,

France, Italy and Singapore and as affiliated partnerships conducting the practice in Hong Kong and Japan. The Law Office of Salman M. Al-Sudairi is Latham & Watkins’ associated office in the Kingdom of Saudi Arabia. In

Qatar, Latham & Watkins LLP is licensed by the Qatar Financial Centre Authority. © Copyright 2014 Latham & Watkins. All Rights Reserved.

Questions?

42

Latham & Watkins operates worldwide as a limited liability partnership organized under the laws of the State of Delaware (USA) with affiliated limited liability partnerships conducting the practice in the United Kingdom,

France, Italy and Singapore and as affiliated partnerships conducting the practice in Hong Kong and Japan. The Law Office of Salman M. Al-Sudairi is Latham & Watkins’ associated office in the Kingdom of Saudi Arabia. In

Qatar, Latham & Watkins LLP is licensed by the Qatar Financial Centre Authority. © Copyright 2014 Latham & Watkins. All Rights Reserved.

Thank You!

43

Cary Hyden

Partner, Latham & Watkins LLP

(714) 755-8254