Embed Size (px)

Citation preview

Managerial Economics

What is Managerial Economics ?

Economics: The branch of knowledge concerned with the production, consumption, and transfer of wealth.

It is the study of to use scarce resources that have alternate uses to satisfy desires that are unlimited and of varying importance. The manager is a person who direct resources to realize an explicit goal. The managerial Economics: The study of how to direct scarce resources within the way that majority efficiently achieves a managerial goal

Different types of economy : Capitalist

Capitalist Economy: A system of economics based on the private ownership of capital and production inputs, and on the production of goods and services for profit. No government involved in the economic decisions. Example : United States of America In economics, the invisible hand is a metaphor used by Adam Smith to describe unintended social benefits resulting from individual actions in his book "An Inquiry into the Nature and Causes of the Wealth of Nations"

Smith’s Invisible Hand "Every individual necessarily labors to render the annual revenue of the society as great as he can. He generally neither intends to promote the public interest, nor knows how much he is promoting it . He intends only his own gain, and he is in this, as in many other cases, led by an invisible hand to promote an end which was no part of his intention. Nor is it always the worse for society that it was no part of his intention. By pursuing his own interest he frequently promotes that of the society more effectually than when he really intends to promote it. I have never known much good done by those who affected to trade for the public good."

Different types of economy : Socialist

Socialist economy : a system is based on some form of social ownership of the means of production, which mean direct public ownership, where the government answer the questions of What to produce ? How to produce and For Whom to produce?

Example : North Korea

Different types of economy : Mixed

Mixed Economy : A system in which both the private enterprise and public sector coexist. All modern economies are mixed where the means of production are shared between the private and public sectors. Also called dual economy.

Example : India

Economic CostCost : is payment of labor or estimated price

and Opportunity cost is the benefit of resources

that we gave up. For example a man opt a job offer in a city away from his home town for better salary gave up the opportunity of staying home, which is the opportunity cost in this case

Cost & Profit

Profit is the difference between the amount earned and the amount spent for any commodity

Economic profit = Total Revenue – Total Economic cost

The economic cost composed of the sum of all opportunity costs

Economic cost = Explicit costs + Implicit costsExplicit cost : Direct Monetary payments/costImplicit Cost : Non Monetary opportunity costs,

like the technology used by the manufacturerIe Economic profit = Total Revenue – (Explicit

costs + Implicit costs)Economic profit = Accounting Profit – Implicit

costsWhere Accounting Profit = Total Revenue –

Explicit costs

Cost

Marginal cost : marginal cost is the change in the total cost when the quantity produced has an increment by unit.

Incremental cost : Incremental cost is the change in total cost when the quantity produced has changed in terms of bulk

Economic Variables : Demand

Demand : defines a consumer's desire and willingness to pay a price for a specific good or service when all other factors are constant

The law of demand : states that, other things remaining same, the quantity demanded of a good increases when its price falls and vice versa

Economic Variables : Demand

Exceptions to the law of demand

Inferior Goods : The goods consumed by the people even if the price raises

Example : Hike in Ticket rates

Veblen Goods : Veblen good’s demand also increases with the raise in price. Veblen goods are types of Luxury goods, expressing conspicuous consumption and high status seeking

Example : a Rolls-Royce

The Demand Curve

The Demand curve is diminishing in nature

Price

Quantity

Demand

Factors influencing Demand

Price of goods or servicesPrices of related goodsIncome of the consumersTaste of the consumersExpected raise in the priceNumber of consumers

Factors influencing Demand

The variation of Demand curve w.r.t PRICE The change in price moves along with the curve

Price

Quantity

DemandP1

P2

q1 q2

Factors influencing Demand The variation of curve w.r.t Taste and other

factors (excluding price of the goods) A decrease in quantity demanded results a leftward shift ( Demand 2) and an increase results a rightward shift (Demand 3) of the curve

Price

Quantity

Demand 1Demand 2

Demand 3

Complimentary and Substitute

Complimentary Goods Whenever price of a good decreases as per the law of demand it’s demand will increase. Complimentary goods are those whose demand increases with the increase in demand of the former. Example : Tea and Sugar Whenever the demand of Tea increases, demand of sugar also increases. Here Sugar is the complimentary good of Tea.

Complimentary and Substitute

Substitute Goods Whenever the price of a good increases as per the law of demand it’s demand will decrease. Substitute good’s demand will decrease with increase in price of the former

Example : Tea and Coffee Whenever the price of Tea increases, it’s demand will decreases. Here Coffee act as a substitute of Tea and it’s demand decreases

Economic Variables : Supply

Supply : refers to the amount of goods that producers and firms are willing to sell at a given price when all other factors being held constant.

Law of Supply: The law of supply states that the quantity supplied of good rises when the price of good rises, considering all other factors constant

The Supply Curve

The Supply curve is incrementing in nature

Price

Quantity

Supply

Factors influencing Supply

Price of goods or servicesPrice of production inputsPrice of substitute goodsAdvance in production technologyExpected raise in the priceNumber of sellers

Factors influencing Supply

Price of goods or servicesPrice of production inputsPrice of substitute goodsAdvance in production technologyExpected raise in the priceNumber of sellers

Factors influencing Supply

The variation of Supply curve w.r.t PRICE The change in price moves along with the curve

Price

Quantity

Supp

ly

P1

P2

q2 q1

Factors influencing Supply

The variation of Supply curve other than price

Supp

ly d

ecre

ases

Supp

ly in

crea

ses

Price

Quantity

Market Equilibrium

A market attain equilibrium when, QUANTITY DEMANDED = QUANTITY SUPPLIED

Price

Quantity

DemandSu

pply

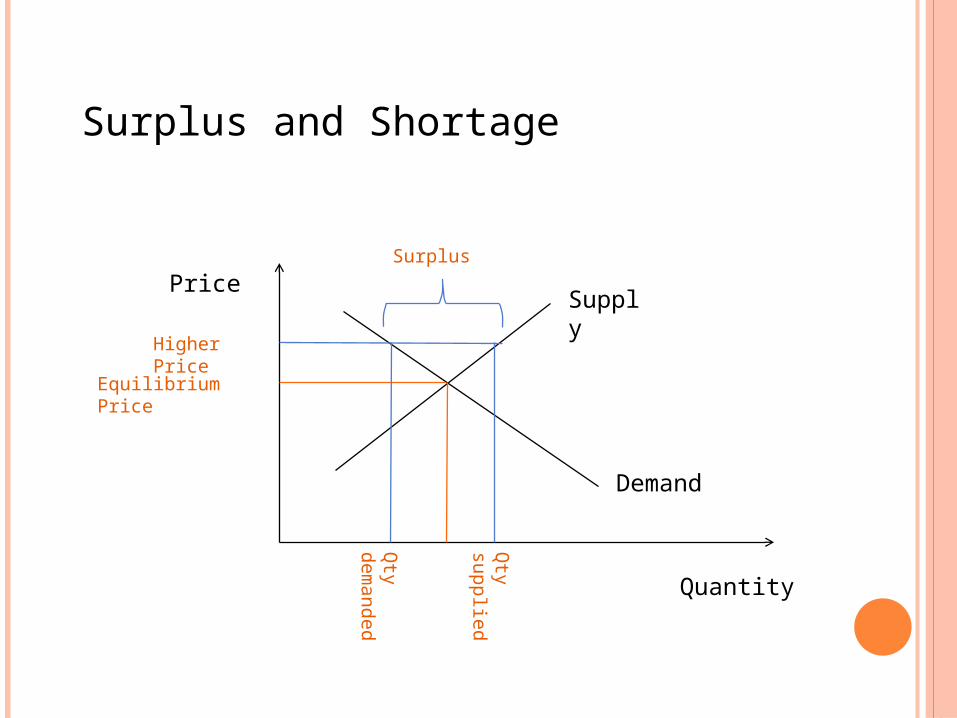

Surplus and Shortage

Surplus : It is the condition that arises when price of the commodity is greater than market equilibrium price. This leads to increase in quantity supplied than the quantity demanded. This excess supply of quantity is called Surplus

Shortage : It is the condition that arises when price of the commodity is less than market equilibrium price. This leads to a hype in demand. This scarcity of commodity than the actual demand is called Shortage

Surplus and Shortage

Price

Quantity

Equilibrium Price

Higher Price

Supply

Demand

Qty

dem

an

ded

Qty

sup

plie

d

Surplus

Surplus and Shortage

Price

Quantity

Equilibrium Price

Lower Price

Supply

Demand

Qty

sup

plie

d

Qty

dem

an

ded

Shortage

Variation in price and quantity when supply and demand changes simultaneously

SupplyNo Change Increases Decreases

No Change Price no changeQty no change

Price decreasesQty increases

Price increasesQty decreases

Increases Price increasesQty increases

Price can’t sayQty increases

Price increasesQty can’t say

Decreases Price decreasesQty decreases

Price decreasesQty can’t say

Price can’t sayQty decreases

Demand

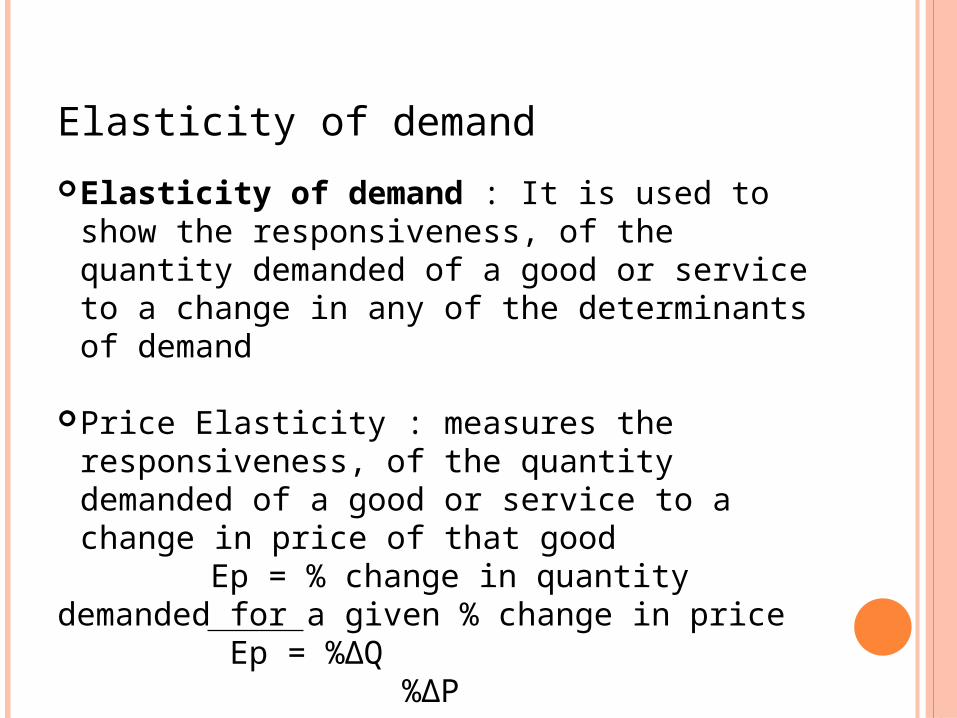

Elasticity of demand

Elasticity of demand : It is used to show the responsiveness, of the quantity demanded of a good or service to a change in any of the determinants of demand

Price Elasticity : measures the responsiveness, of the quantity demanded of a good or service to a change in price of that good

Ep = % change in quantity demanded for a given % change in price Ep = %ΔQ %ΔP

Elasticity of demand

Elasticity of demand : It is used to show the responsiveness, of the quantity demanded of a good or service to a change in any of the determinants of demand

Price Elasticity : measures the responsiveness, of the quantity demanded of a good or service to a change in price of that good

Ep = % change in quantity demanded for a given % change in price, since Q and P are inversely related the value of Ep will be -ve Ep = %ΔQ %ΔP

Elasticity of demand

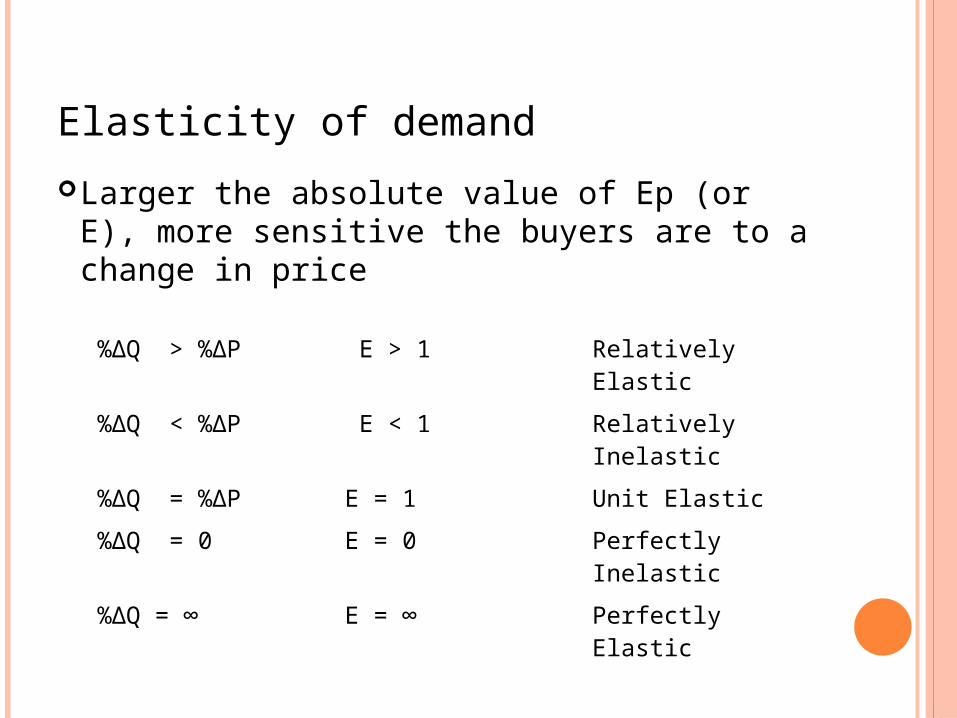

Larger the absolute value of Ep (or E), more sensitive the buyers are to a change in price

%ΔQ > %ΔP E > 1 Relatively Elastic

%ΔQ < %ΔP E < 1 Relatively Inelastic

%ΔQ = %ΔP E = 1 Unit Elastic

%ΔQ = 0 E = 0 Perfectly Inelastic

%ΔQ = ∞ E = ∞ Perfectly Elastic

Elasticity of demand

Price

Quantity

Price

Quantity

Perfectly Elastic Perfectly Inelastic

Elasticity of demand

Price

Quantity

Price

Quantity

Relatively less elastic

5

4

10075

Unit Elastic

10090

Elastic curves are more flatter and Inelastic curves are more steeper

Price Elasticity and total revenue

Price

Quantity

5

75

Tota

l re

ven

ue

Total Revenue = Price x Quantity Here ; Total Revenue = 5 x 75

Price Elasticity and total revenue

Price Elastic Unitary Inelastic

Increases Total Revenue Decreases

No change Total Revenue Increases

Decreases Total Revenue Increases

No change Total Revenue Decreases