Embed Size (px)

Citation preview

NAVIGATING HEALTH CARE REFORM

Michael P. James, JD, MBA, CSSGB

Phone: (517) 377-0823 (313) 237-7300

Email: [email protected]

www.linkedin.com/in/MichaelJamesLaw

© 2014 Fraser Trebilcock Davis & Dunlap, P.C.

Guidance for Small Businesses and Individuals

Why is Health Care Reform So Complicated?

Does health care reform apply to my business? What is it going to cost me? Do I have to provide health insurance to my

employees? Are there penalties? Will the changes ever stop? It’s just too confusing… Am I missing something….? Who can I turn to for help?

Be Prepared for Health Care Reform

Health Insurance Marketplace/Exchange Overview Are You a Large or Small Employer? Secret Cash Bonus for Small Employers. Develop a Strategy. HCR Checkup for Your Business. Develop a Compliance Program.

The Patient Protection & Affordable Care Act (ACA)

Became law in March 2010. Supreme Court upholds constitutionality of ACA

June 2012. ACA creates:

Individual Health Insurance Mandate; Employer Responsibility Requirements; and Small Business Health Care Affordability Tax Credits.

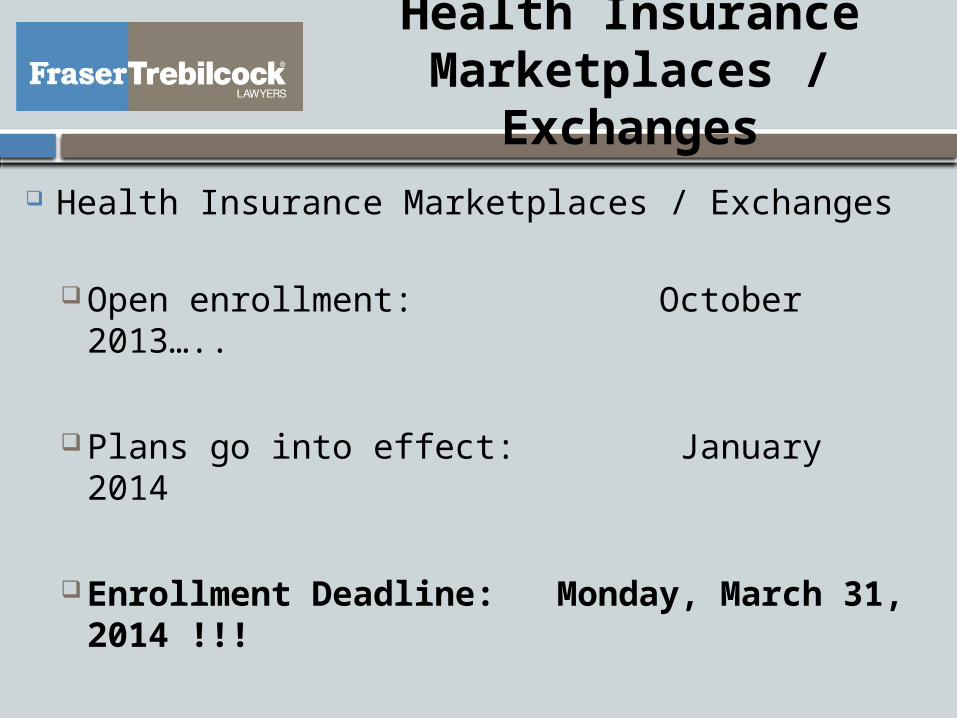

Health Insurance Marketplaces / Exchanges

Health Insurance Marketplaces / Exchanges

Open enrollment: October 2013…..

Plans go into effect: January 2014

Enrollment Deadline: Monday, March 31, 2014 !!!

Platinum

88-92% AV

Gold

78-82% AV

Silver

68-72% AV

Bronze

58-62% AV

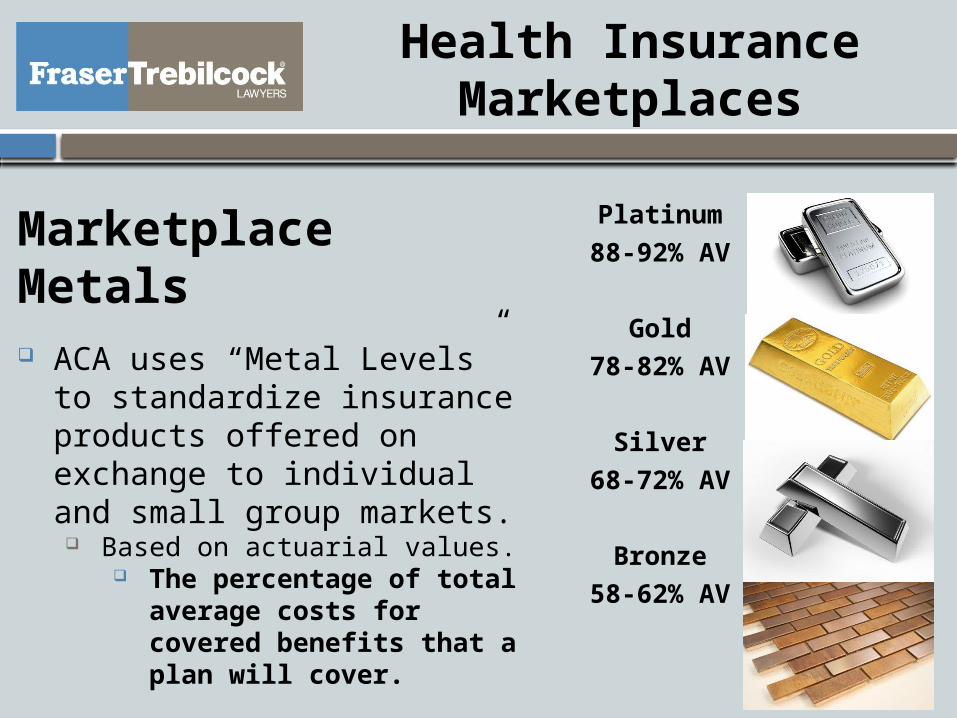

Marketplace Metals ACA uses “Metal Levels” to

standardize insurance products offered on exchange to individual and small group markets.

Based on actuarial values. The percentage of total average

costs for covered benefits that a plan will cover.

Health Insurance Marketplaces

Essential Health Benefits

1) Ambulatory Patient Services2) Emergency Services3) Hospitalization4) Maternity and Newborn Care5) Mental Health & Substance Use Disorder Services; Behavioral

Health Treatment6) Prescription Drugs7) Rehabilitative and Habilitative Services and Devices8) Laboratory Services9) Preventative Wellness Services and Chronic Disease

Management10) Pediatric Services, Including Oral and Vision Care

Health Insurance Marketplaces

Health Insurance Marketplaces

How Does it Work? - What You See

Health Insurance Marketplaces

How Does it Work? - What You See

Health Insurance Marketplaces

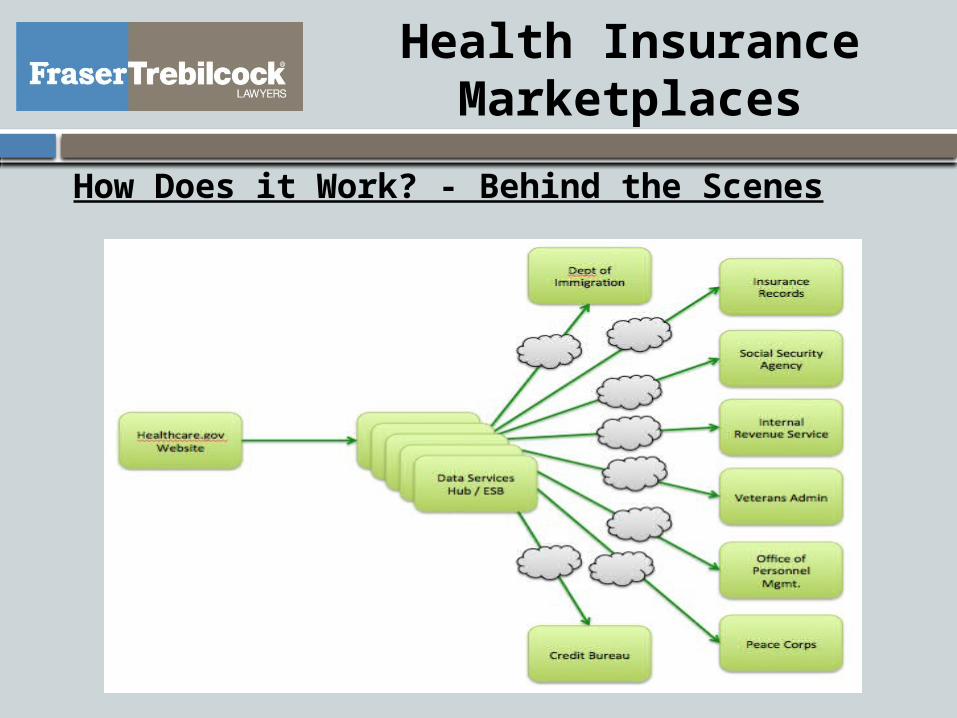

How Does it Work? - Behind the Scenes

Health Insurance Marketplaces

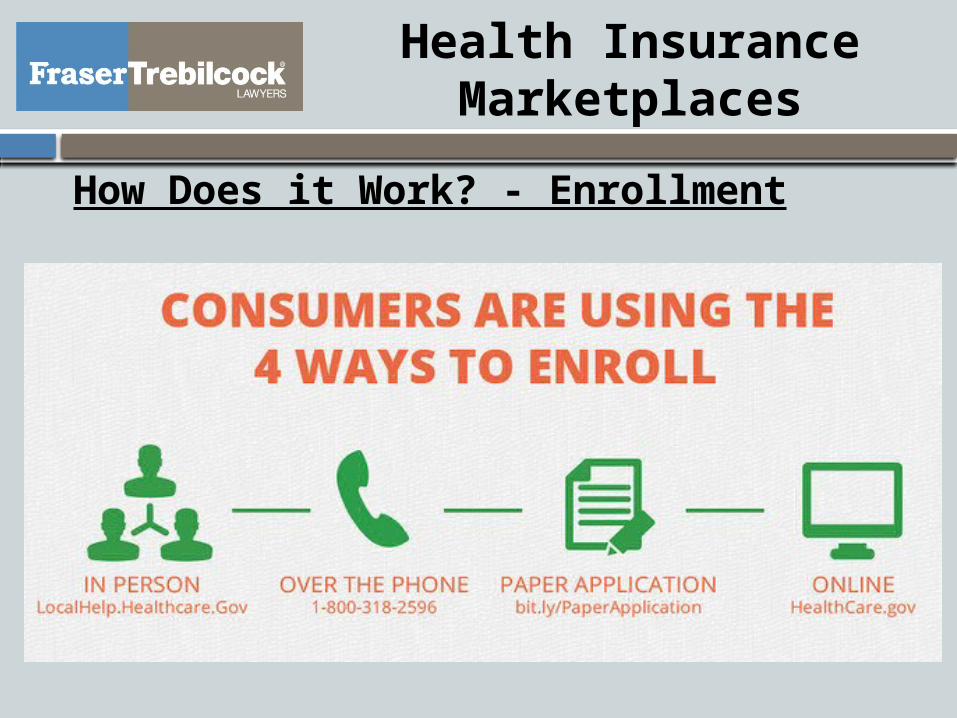

How Does it Work? - Enrollment

Health Insurance Marketplaces

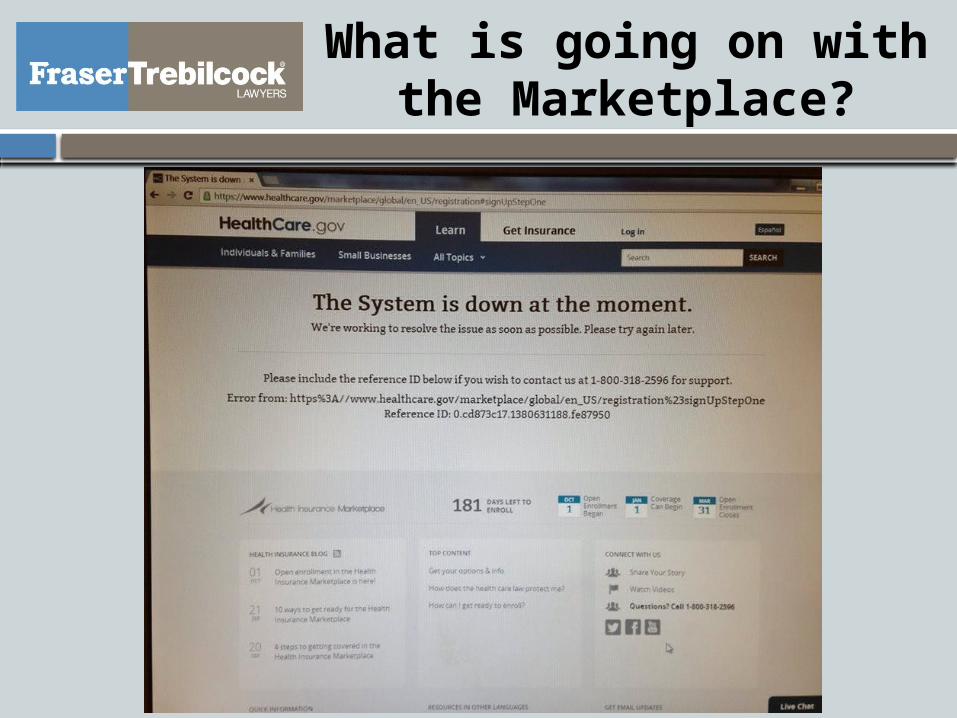

What is going on with the Marketplace?

ACA Individual Health Insurance Mandate

The individual health insurance mandate requires nearly all Americans to purchase and maintain health insurance. Qualified coverage evidenced through tax returns.

ACA Individual Health Insurance Mandate

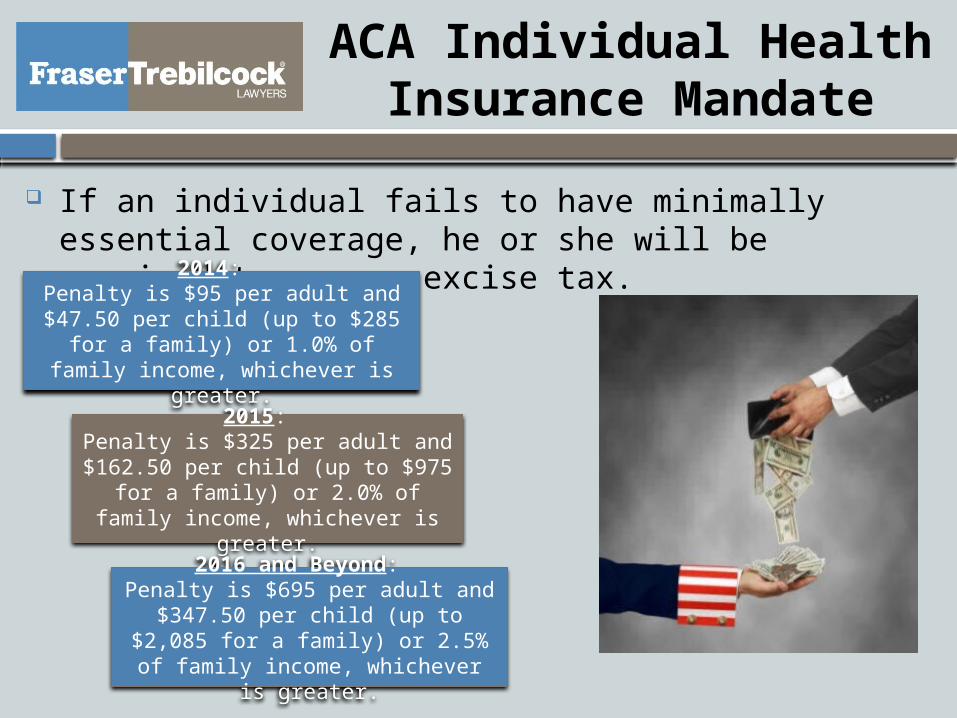

If an individual fails to have minimally essential coverage, he or she will be required to pay an excise tax.

2014: Penalty is $95 per adult and

$47.50 per child (up to $285 for a family) or 1.0% of family income,

whichever is greater.

2015: Penalty is $325 per adult and

$162.50 per child (up to $975 for a family) or 2.0% of family

income, whichever is greater.

2016 and Beyond: Penalty is $695 per adult and

$347.50 per child (up to $2,085 for a family) or 2.5% of family income,

whichever is greater.

Are You a Largeor Small Employer?

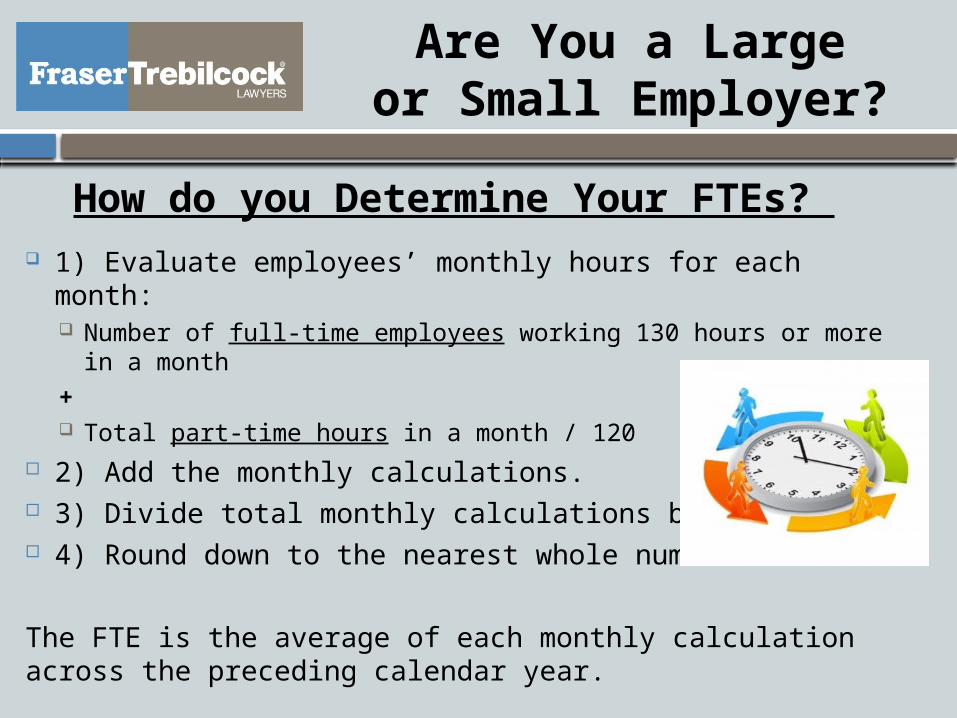

How do you Determine Your FTEs? 1) Evaluate employees’ monthly hours for each month:

Number of full-time employees working 130 hours or more in a month

+ Total part-time hours in a month / 120

2) Add the monthly calculations. 3) Divide total monthly calculations by 12. 4) Round down to the nearest whole number.

The FTE is the average of each monthly calculation across the preceding calendar year.

Employees? Seasonal Employees? Independent Contractors? Owner of Business? Family Members of Business Owner? Employees of Other Businesses You Own?

Are You a Largeor Small Employer?

Which Employees Count Toward FTEs?

Are You a Largeor Small Employer?

Seasonal Employees Redefined A “Seasonal Employee” is an employee in a position for which the

customary annual employment is 6 months or less. The seasonal period should begin around the same part of the year each year.

Seasonal employment may be extended under certain circumstances.

Bona Fide Volunteers Government entities and 501(c) organizations with tax-exempt

volunteers do not need to count the hours of service provided by bona fide volunteers when determining their status as a large or small employer under the ACA.

ACA Employer Responsibility

Under 50 FTEs There is no insurance

requirement. Employers do not have to

offer insurance. However, if health insurance

offered, must meet Essential Health Benefits and metals.

Small Business Health Option Programs

Small Business Health Option Programs (SHOP)

Open to all small businesses in 2014. Must have 50 FTEs or less.

In 2014, employer chooses one insurance product for all employees. In 2015, employer picks the metal level, employees choose the

insurance product. In 2016, SHOP expands to businesses with up to 100 FTEs. In 2017+, States have option to expand SHOP eligibility to large

groups.

Secret Cash Bonus for Small Employers

Small Business Health Care Tax Credits

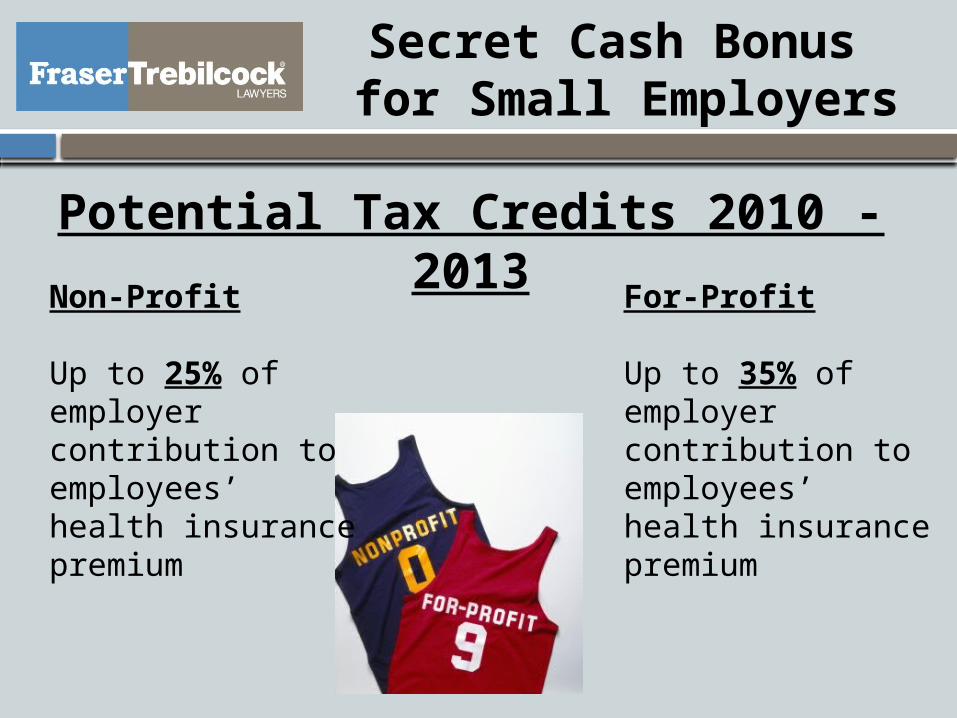

Secret Cash Bonus for Small Employers

Potential Tax Credits 2010 - 2013

For-Profit

Up to 35% of employer contribution to employees’ health insurance premium

Non-Profit

Up to 25% of employer contribution to employees’ health insurance premium

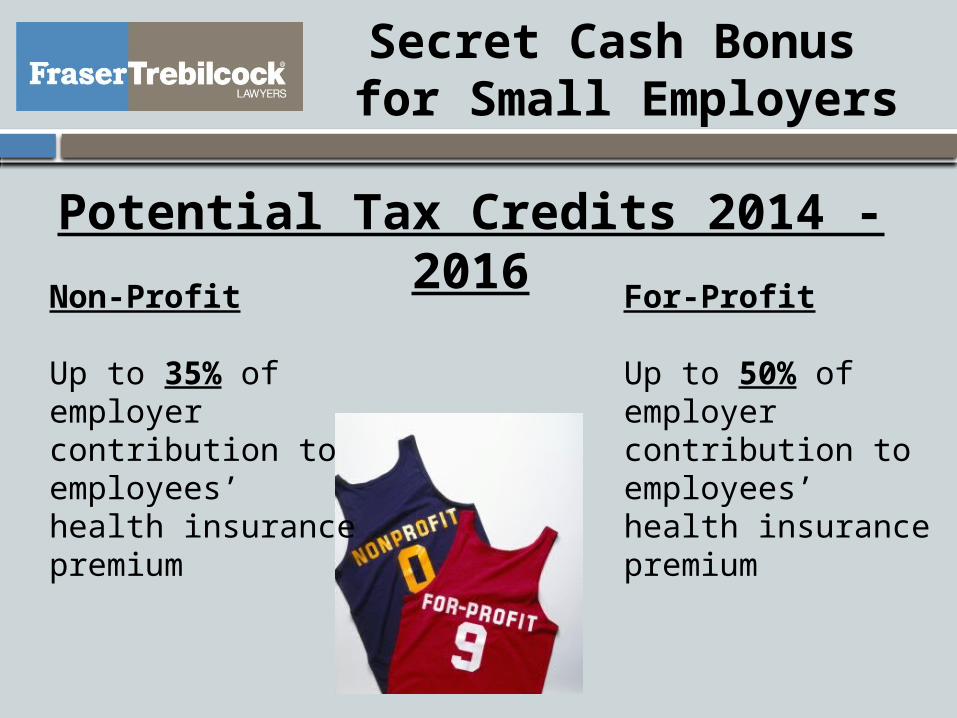

Secret Cash Bonus for Small Employers

Potential Tax Credits 2014 - 2016

For-Profit

Up to 50% of employer contribution to employees’ health insurance premium

Non-Profit

Up to 35% of employer contribution to employees’ health insurance premium

Secret Cash Bonus for Small Employers

Requirements

< 25 Employees

Average Employee Wages< $50,000

Employer must contribute at least 50% of premium cost

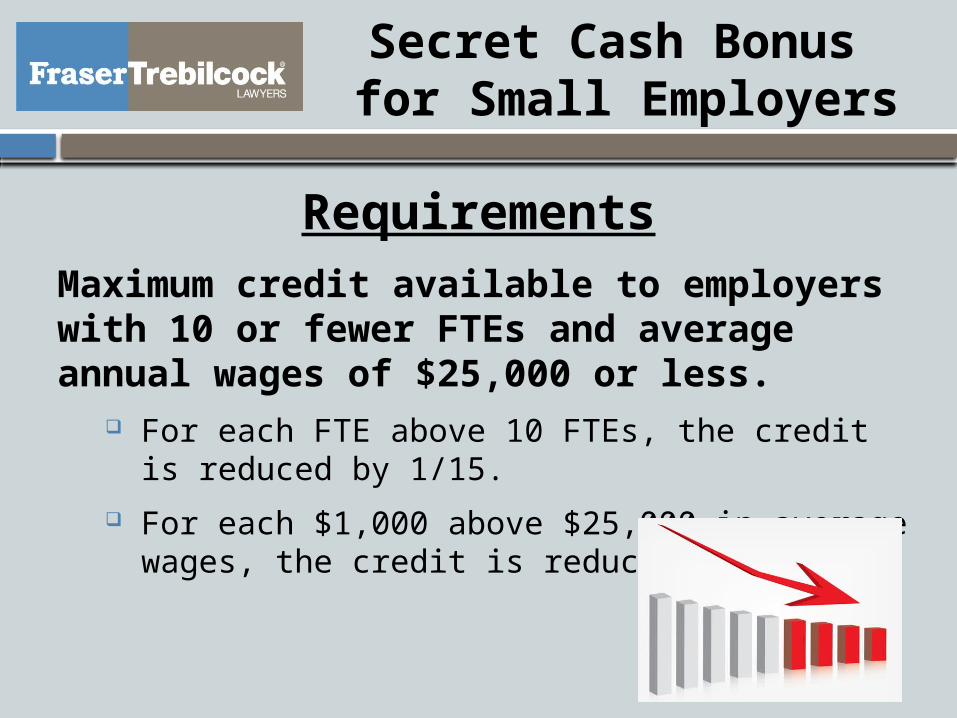

Secret Cash Bonus for Small Employers

RequirementsMaximum credit available to employers with 10 or fewer FTEs and average annual wages of $25,000 or less.

For each FTE above 10 FTEs, the credit is reduced by 1/15.

For each $1,000 above $25,000 in average wages, the credit is reduced by 1/25.

Secret Cash Bonus for Small Employers

Which Employees Count? Seasonal Workers Leased Employees Owner of Business Family Members of Business Owner

Secret Cash Bonus for Small Employers

Members of a controlled or an affiliated service group may be treated as a single employer for tax credit purposes.

Which Employees Count?

Secret Cash Bonus for Small Employers

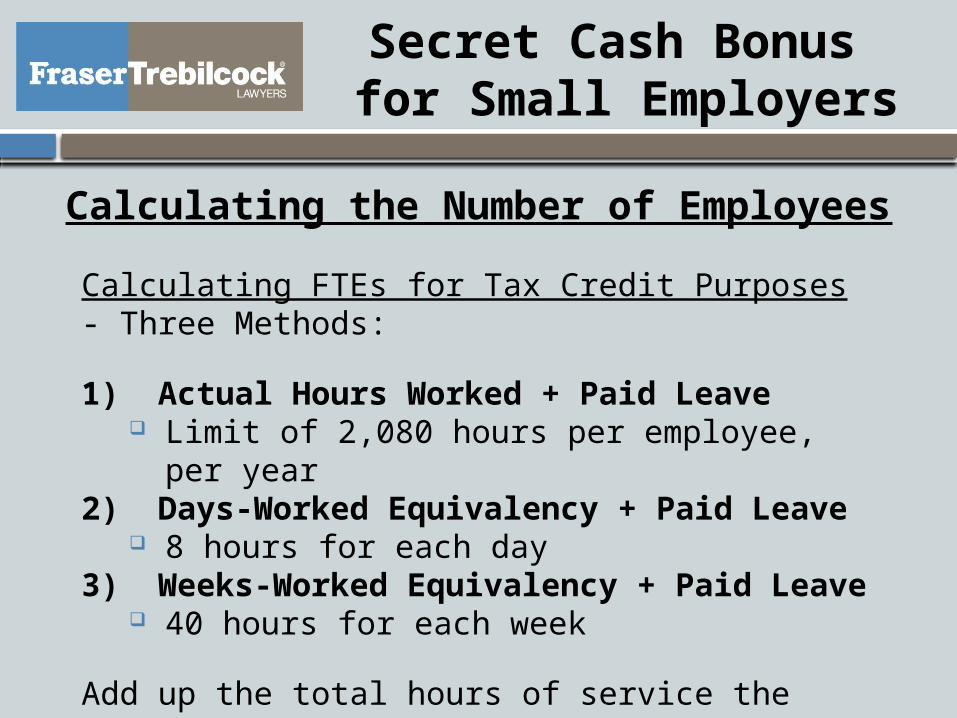

Calculating the Number of Employees

Calculating FTEs for Tax Credit Purposes - Three Methods:

1) Actual Hours Worked + Paid Leave Limit of 2,080 hours per employee, per year

2) Days-Worked Equivalency + Paid Leave 8 hours for each day

3) Weeks-Worked Equivalency + Paid Leave 40 hours for each week

Add up the total hours of service the employer pays wages to employees and divide by 2,080. Round down.

Secret Cash Bonus for Small Employers

Calculating Average Employee Wages1) Add up the total wages paid by employer during the tax year.

2) Divide total wages by the number of FTEs for the year.

3) Round down the result to the nearest $1,000.

The employer’s average wages are $24,000 ($245,786 / 10 = $24,578.60, rounded down to the nearest $1,000).

Example: In 2013, an employer pays a total of $245,786 in wages and has 10 FTEs.

Secret Cash Bonus for Small Employers

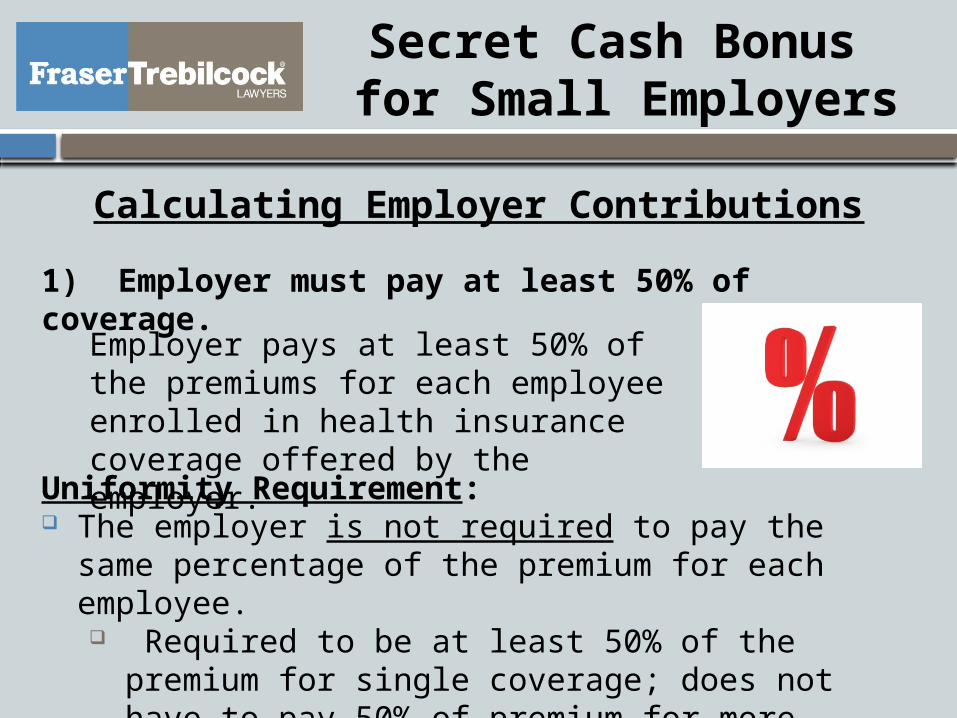

Calculating Employer Contributions1) Employer must pay at least 50% of coverage.

Employer pays at least 50% of the premiums for each employee enrolled in health insurance coverage offered by the employer.

Uniformity Requirement: The employer is not required to pay the same percentage of the

premium for each employee. Required to be at least 50% of the premium for single

coverage; does not have to pay 50% of premium for more expensive coverage options.

Secret Cash Bonus for Small Employers

Calculating Employer ContributionsUniformity Requirement Example:

Employer has 9 employees: 6 enrolled in single coverage. 3 enrolled in family coverage.

Premium Single: $ 8,000Premium Family: $14,000

Employer pays $4,000 per employee:• 50% of the premium for

single coverage for each employee enrolled in single or family coverage.

• Employer has satisfied uniformity requirement.

Secret Cash Bonus for Small Employers

Calculating Employer Contributions2) Payments must be made under a qualified arrangement.

Only premiums paid to a health insurance issuer. Major medical plan, dental, vision, etc.

Each plan must meet requirements.

Payments that do not count: Portion paid by employees; Premium payments under a salary reduction

arrangement; Employer contributions to HRAs, FSAs, and HSAs.

Secret Cash Bonus for Small Employers

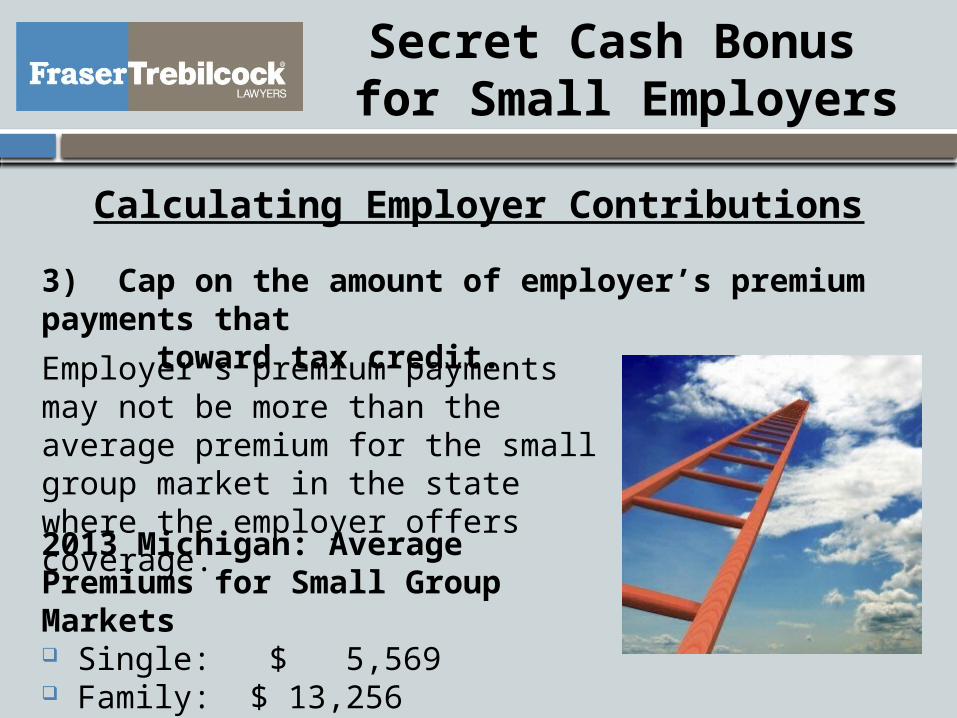

Calculating Employer Contributions3) Cap on the amount of employer’s premium payments that toward tax credit.

Employer’s premium payments may not be more than the average premium for the small group market in the state where the employer offers coverage.

2013 Michigan: Average Premiums for Small Group Markets Single: $ 5,569 Family: $ 13,256

Secret Cash Bonus for Small Employers

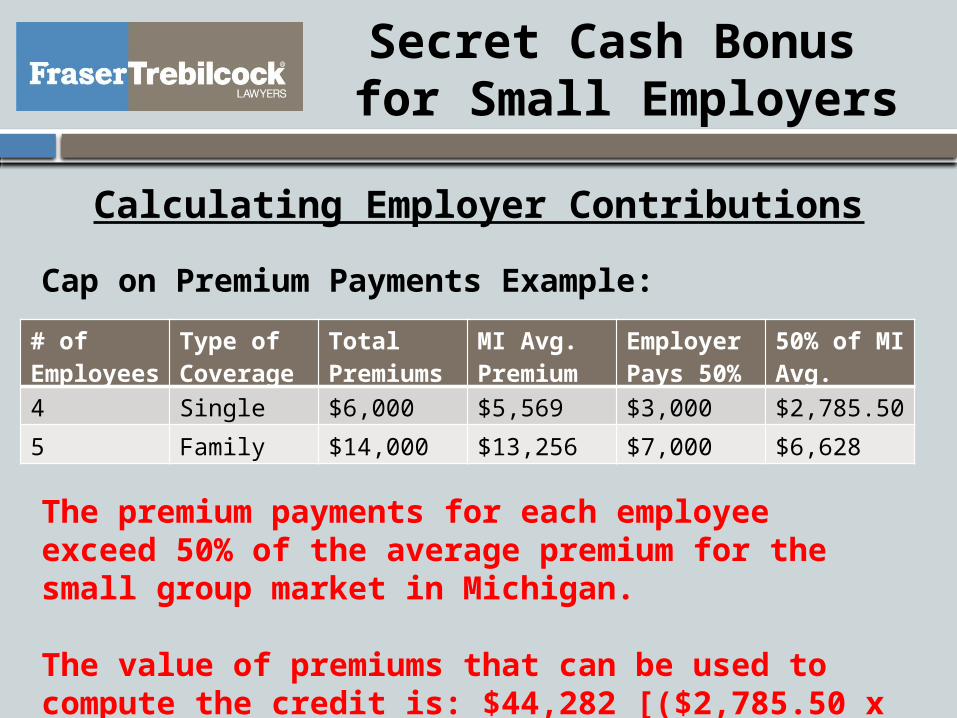

Calculating Employer ContributionsCap on Premium Payments Example:

# of Employees

Type of Coverage

Total Premiums

MI Avg. Premium

Employer Pays 50%

50% of MI Avg.

4 Single $6,000 $5,569 $3,000 $2,785.50

5 Family $14,000 $13,256 $7,000 $6,628

The premium payments for each employee exceed 50% of the average premium for the small group market in Michigan.

The value of premiums that can be used to compute the credit is: $44,282 [($2,785.50 x 4) + ($6,828 x 5)].

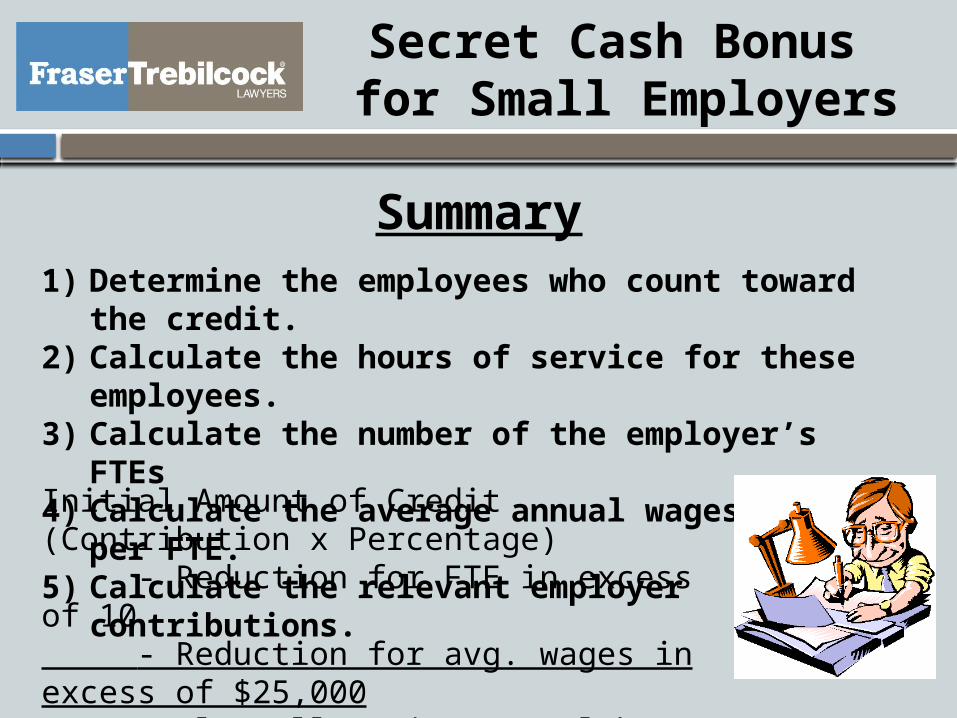

Summary1) Determine the employees who count toward the credit.2) Calculate the hours of service for these employees.3) Calculate the number of the employer’s FTEs4) Calculate the average annual wages paid per FTE.5) Calculate the relevant employer contributions.

Initial Amount of Credit (Contribution x Percentage) - Reduction for FTE in excess of 10 - Reduction for avg. wages in excess of $25,000 Total Small Business Health Care Tax Credit

Secret Cash Bonus for Small Employers

Secret Cash Bonus for Small Employers

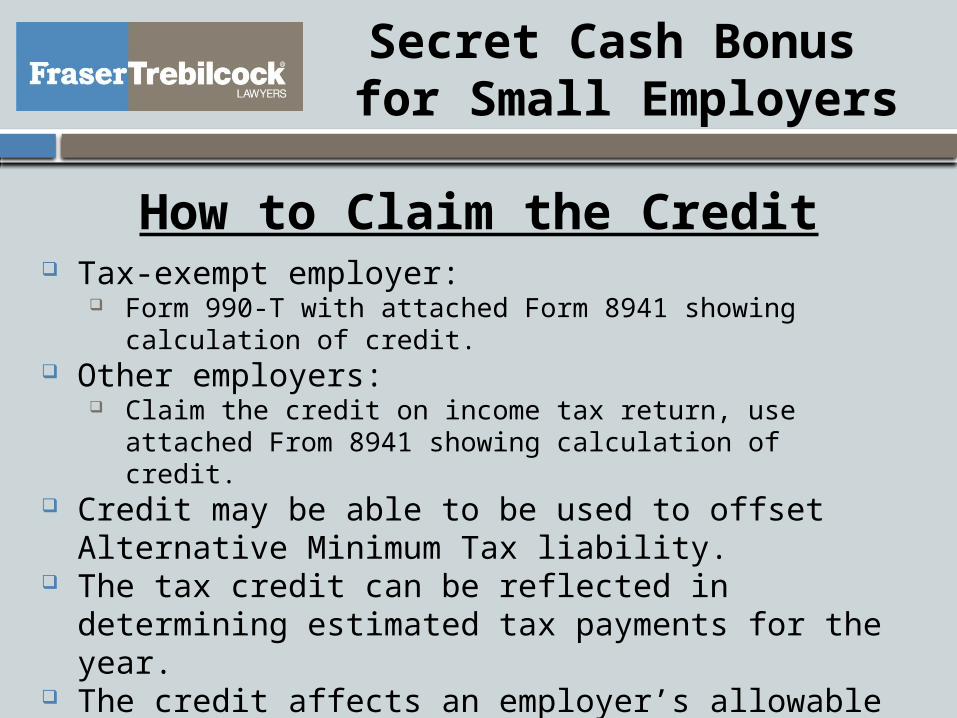

How to Claim the Credit Tax-exempt employer:

Form 990-T with attached Form 8941 showing calculation of credit. Other employers:

Claim the credit on income tax return, use attached From 8941 showing calculation of credit.

Credit may be able to be used to offset Alternative Minimum Tax liability.

The tax credit can be reflected in determining estimated tax payments for the year.

The credit affects an employer’s allowable deduction for health insurance premiums; deduction is reduced by amount of credit.

Credit does not affect employer’s employment tax payments.

What Strategy Worksfor Your Business?

Provide

Health Insura

nce

Send Employees to Exchan

ge

Make Your Employees Love You

Involve employees in decision-making process? Communicate with your employees:

If providing coverage? Providing coverage despite not being required to do so. Culture of business; potential advantage over competitors.

If not providing coverage? Cost to business; other forms of assistance. Be prepared to assist employees with federal exchange.

Make Your Employees Love You

Health Insurance Marketplace Notice An employer is required to provide notice of the availability of

the Exchange, informing employees that: 1) the existence of the Marketplace; 2) that employees may be eligible for a subsidy under the

Marketplace if the employer’s share of the aggregate cost of benefits is less than 60%; and

3) that if the employee purchases a policy through the Marketplace, he or she will lose the contribution to any health benefits offered by the employer.

Notice must be provided to each employee at the time of hiring.

For existing employees, the notice must be given no later than October 1, 2013.

Health Care ReformCheckup for Your Business

Is your business compliant with all the current health care regulations?

Many regulations went into effect in 2012 and 2013. Have you made the necessary adjustments?

Develop a Compliance Plan

Fraser Trebilcock Davis & Dunlap, P.C.124 W. Allegan Street, Suite 1000Lansing, Michigan 48933www.fraserlawfirm.comPhone: (517) 482-5800Fax: (517) 482-0887

Fraser Trebilcock Davis & Dunlap, P.C.One Woodward Avenue, Suite 1550Detroit, Michigan 48226www.fraserlawfirm.comPhone: (313) 237-7300Fax: (313) 961-1651

Michael P. James, JD, MBA, CSSGB

Phone: (517) 377-0823 (313) 237-7300

Email: [email protected]

www.linkedin.com/in/MichaelJamesLaw

© 2014 Fraser Trebilcock Davis & Dunlap, P.C.

Fraser Trebilcock Health Care Reform

www.mihealthcarelaws.com