Embed Size (px)

Citation preview

McKinsey Health Systems Institute 1

The Future of Medicare!Implications of the Affordable Care Act and our Fiscal Imperatives !

Bob Kocher, MD Director of the McKinsey Center on U.S. Health Reform and Non Resident Senior Fellow, Brookings InstitutionApril 28, 2011!

McKinsey Health Systems Institute 2

Summary !

The fundamental issue in U.S. health care for next decade will be cost and affordability

Ultimately, budget pressures will force policies that achieve slower Medicare and Medicaid cost growth

The Affordable Care Act has accelerated an environment for change in the health system

McKinsey Health Systems Institute 3

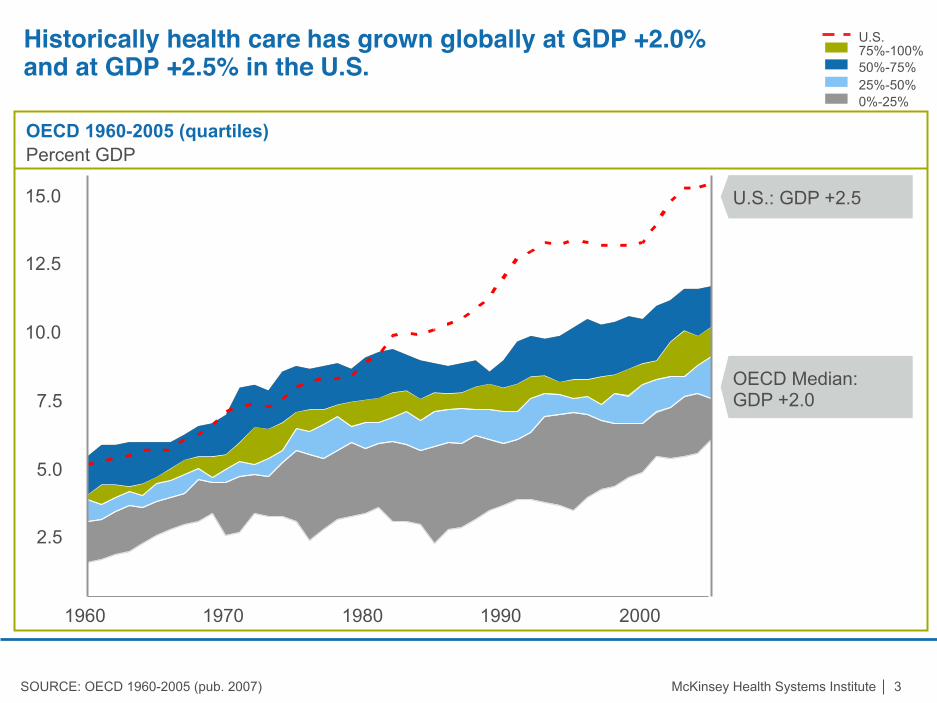

Historically health care has grown globally at GDP +2.0% and at GDP +2.5% in the U.S.!

75%-100% 50%-75% 25%-50% 0%-25%

U.S.

OECD 1960-2005 (quartiles) Percent GDP

2.5

5.0

7.5

10.0

12.5

15.0

1960 1970 1980 1990 2000

SOURCE: OECD 1960-2005 (pub. 2007)

U.S.: GDP +2.5

OECD Median: GDP +2.0

McKinsey Health Systems Institute 4

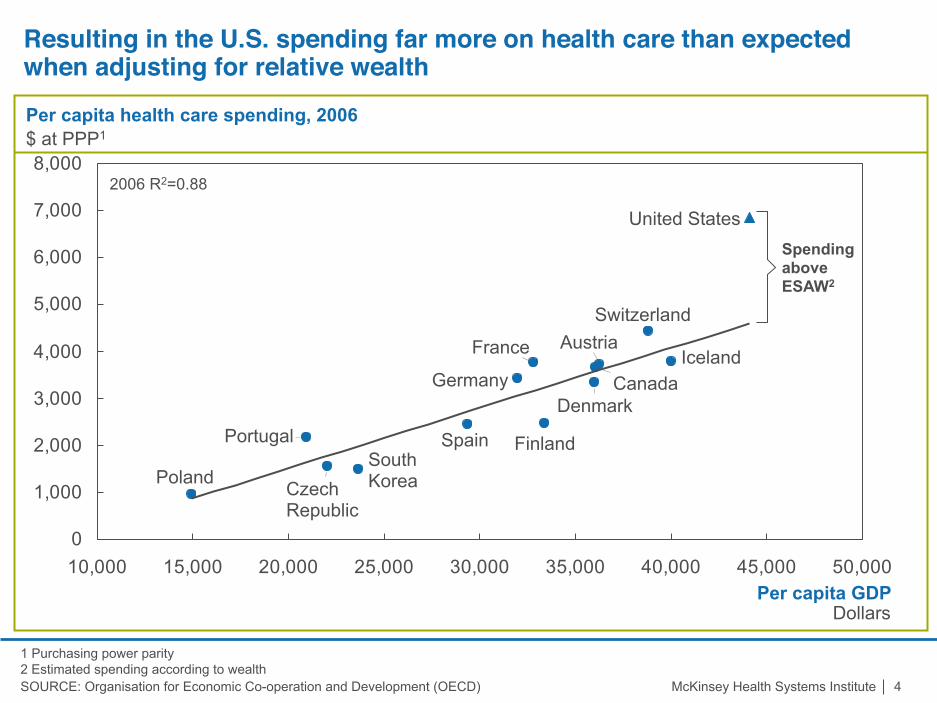

Resulting in the U.S. spending far more on health care than expected when adjusting for relative wealth!

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

10,000 15,000 20,000 25,000 30,000 35,000 40,000 45,000 50,000

South Korea Poland

Portugal Spain

Switzerland

United States

Austria

Canada

Czech Republic

Denmark

Finland

France

Germany Iceland

Per capita GDP Dollars

2006 R2=0.88

Spending above ESAW2

Per capita health care spending, 2006 $ at PPP1

1 Purchasing power parity 2 Estimated spending according to wealth SOURCE: Organisation for Economic Co-operation and Development (OECD)

McKinsey Health Systems Institute 5

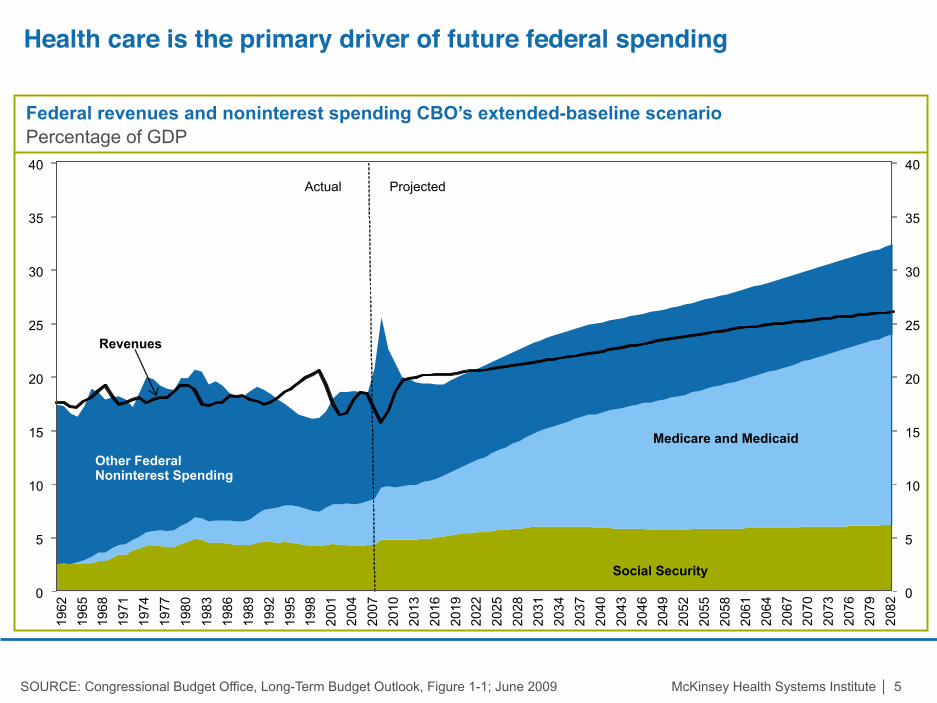

Health care is the primary driver of future federal spending!

SOURCE: Congressional Budget Office, Long-Term Budget Outlook, Figure 1-1; June 2009

Federal revenues and noninterest spending CBO’s extended-baseline scenario Percentage of GDP

0

5

10

15

20

25

30

35

40

0

5

10

15

20

25

30

35

40

1962

19

65

1968

19

71

1974

19

77

1980

19

83

1986

19

89

1992

19

95

1998

20

01

2004

20

07

2010

20

13

2016

20

19

2022

20

25

2028

20

31

2034

20

37

2040

20

43

2046

20

49

2052

20

55

2058

20

61

2064

20

67

2070

20

73

2076

20

79

2082

Revenues

Social Security

Medicare and Medicaid

Other Federal Noninterest Spending

Actual Projected

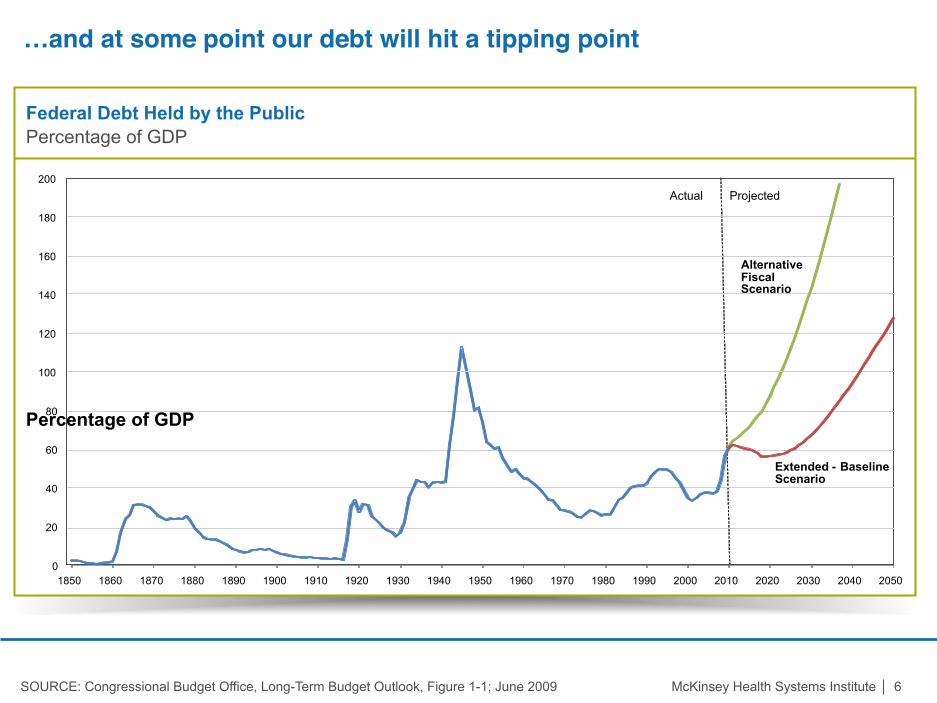

McKinsey Health Systems Institute 6

…and at some point our debt will hit a tipping point !

Federal Debt Held by the Public Percentage of GDP

SOURCE: Congressional Budget Office, Long-Term Budget Outlook, Figure 1-1; June 2009

0

20

40

60

80

100

120

140

160

180

200

1850 1860 1870 1880 1890 1900 1910 1920 1930 1940 1950 1960 1970 1980 1990 2000 2010 2020 2030 2040 2050

Percentage of GDP

Alternative Fiscal Scenario

Extended - Baseline Scenario

Actual Projected

McKinsey Health Systems Institute 7

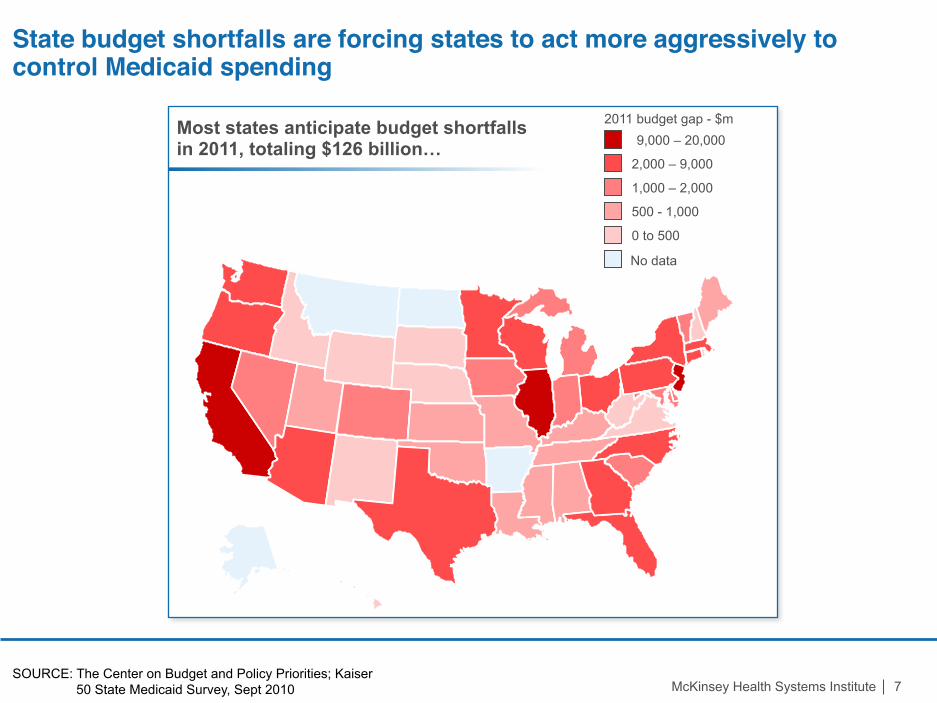

State budget shortfalls are forcing states to act more aggressively to control Medicaid spending!

SOURCE: The Center on Budget and Policy Priorities; Kaiser 50 State Medicaid Survey, Sept 2010

Most states anticipate budget shortfalls in 2011, totaling $126 billion… 9,000 – 20,000

No data

2,000 – 9,000

1,000 – 2,000

500 - 1,000

0 to 500

2011 budget gap - $m

McKinsey Health Systems Institute 8

Summary !

The fundamental issue in U.S. health care for next decade will be cost and affordability

Ultimately, budget pressures will force policies that achieve slower Medicare and Medicaid cost growth

The Affordable Care Act has accelerated an environment for change in the health system

McKinsey Health Systems Institute 9

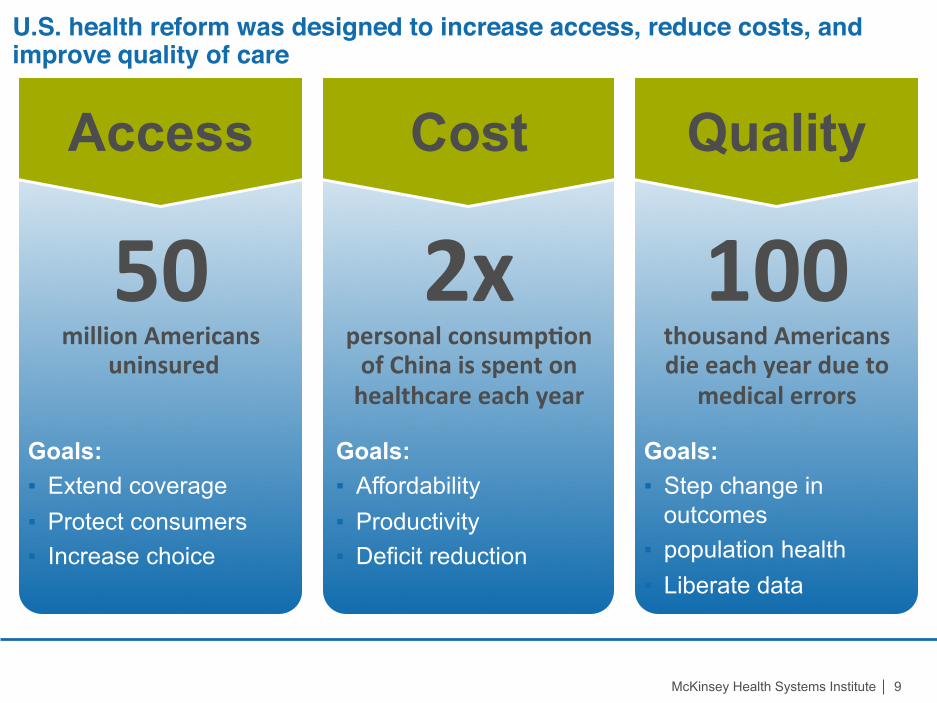

U.S. health reform was designed to increase access, reduce costs, and improve quality of care!

50 million Americans

uninsured

Access

Goals: ▪ Extend coverage ▪ Protect consumers ▪ Increase choice

2x personal consump4on of China is spent on healthcare each year

Cost

Goals: ▪ Affordability ▪ Productivity ▪ Deficit reduction

100 thousand Americans die each year due to

medical errors

Quality

Goals: ▪ Step change in

outcomes ▪ population health ▪ Liberate data

McKinsey Health Systems Institute 10

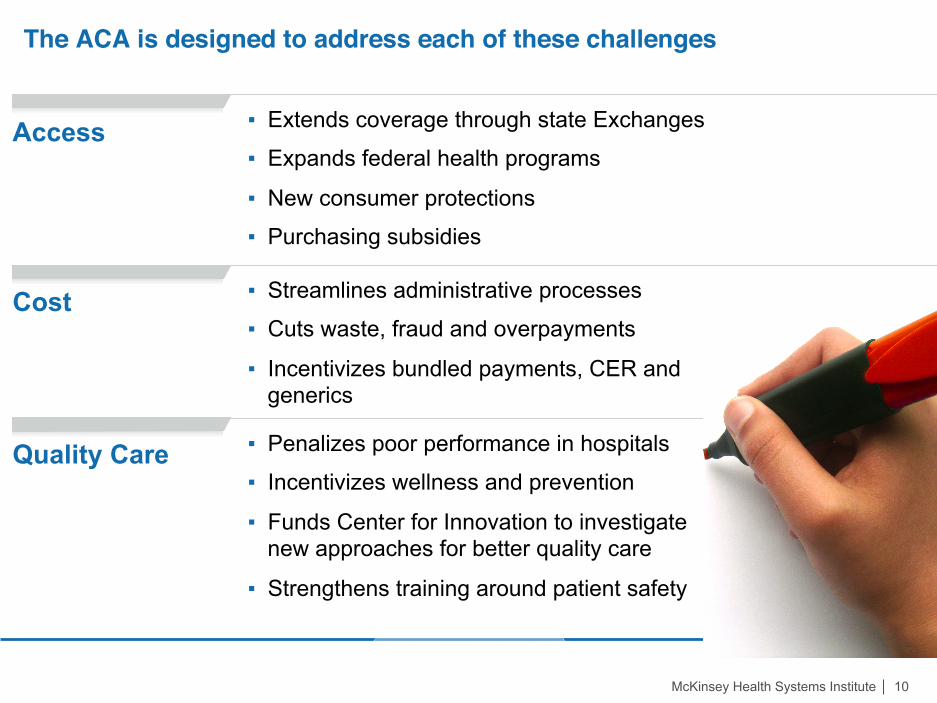

The ACA is designed to address each of these challenges!

Access ▪ Extends coverage through state Exchanges

▪ Expands federal health programs

▪ New consumer protections

▪ Purchasing subsidies

▪ Penalizes poor performance in hospitals

▪ Incentivizes wellness and prevention

▪ Funds Center for Innovation to investigate new approaches for better quality care

▪ Strengthens training around patient safety

Quality Care

Cost ▪ Streamlines administrative processes

▪ Cuts waste, fraud and overpayments

▪ Incentivizes bundled payments, CER and generics

McKinsey Health Systems Institute 11

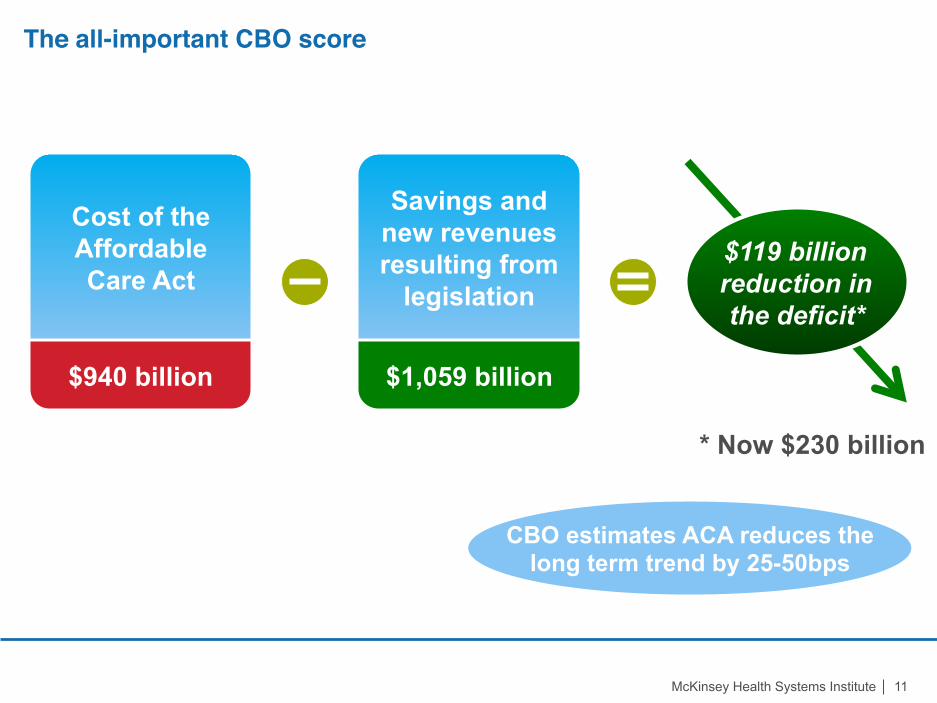

The all-important CBO score!

Cost of the Affordable Care Act

$940 billion

Savings and new revenues resulting from

legislation

$1,059 billion

$119 billion reduction in the deficit*

* Now $230 billion

CBO estimates ACA reduces the long term trend by 25-50bps

McKinsey Health Systems Institute 12

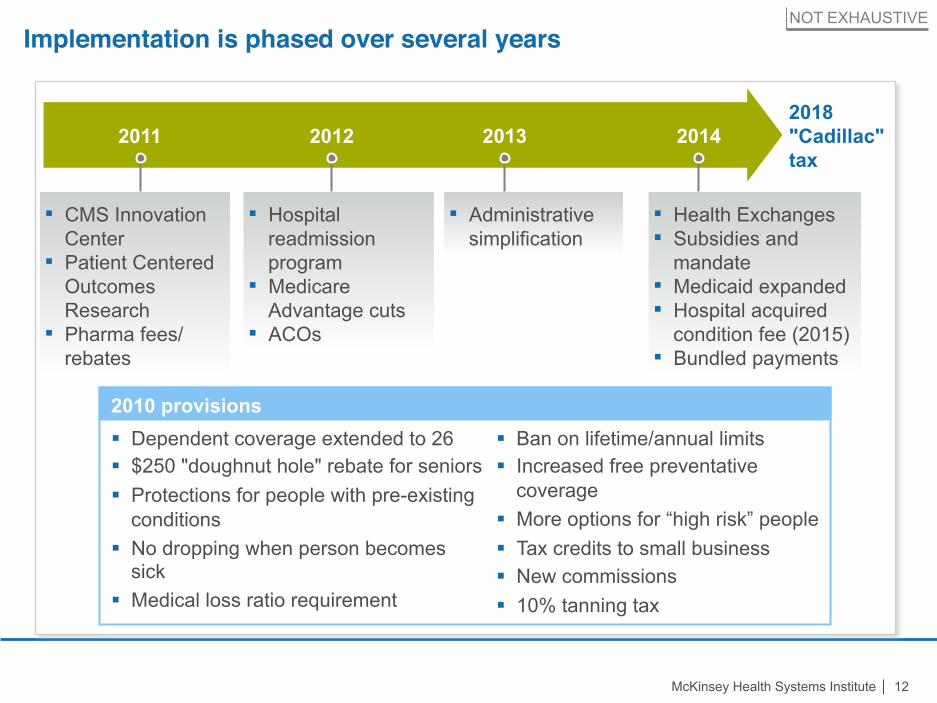

Implementation is phased over several years!NOT EXHAUSTIVE

▪ Hospital readmission program

▪ Medicare Advantage cuts

▪ ACOs

▪ Administrative simplification

▪ CMS Innovation Center

▪ Patient Centered Outcomes Research

▪ Pharma fees/rebates

▪ Health Exchanges ▪ Subsidies and

mandate ▪ Medicaid expanded ▪ Hospital acquired

condition fee (2015) ▪ Bundled payments

2011 2012 2013 2014 2018 "Cadillac" tax

§ Dependent coverage extended to 26 § $250 "doughnut hole" rebate for seniors § Protections for people with pre-existing

conditions § No dropping when person becomes

sick § Medical loss ratio requirement

§ Ban on lifetime/annual limits § Increased free preventative

coverage § More options for “high risk” people § Tax credits to small business § New commissions § 10% tanning tax

2010 provisions

McKinsey Health Systems Institute 13

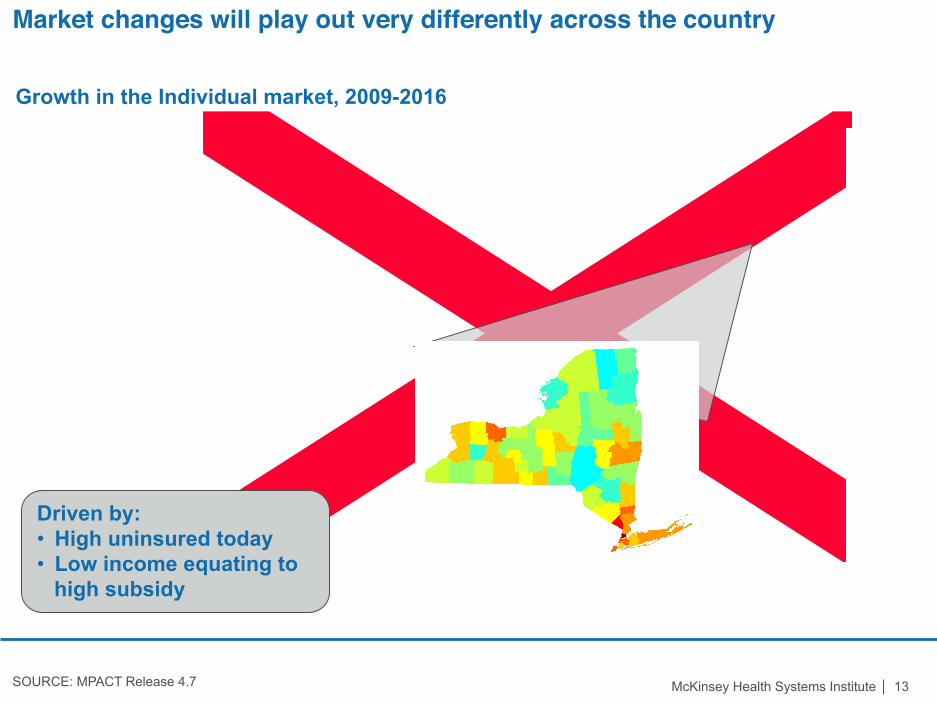

Market changes will play out very differently across the country!

SOURCE: MPACT Release 4.7

Growth in the Individual market, 2009-2016

Driven by: • High uninsured today • Low income equating to

high subsidy

McKinsey Health Systems Institute 14

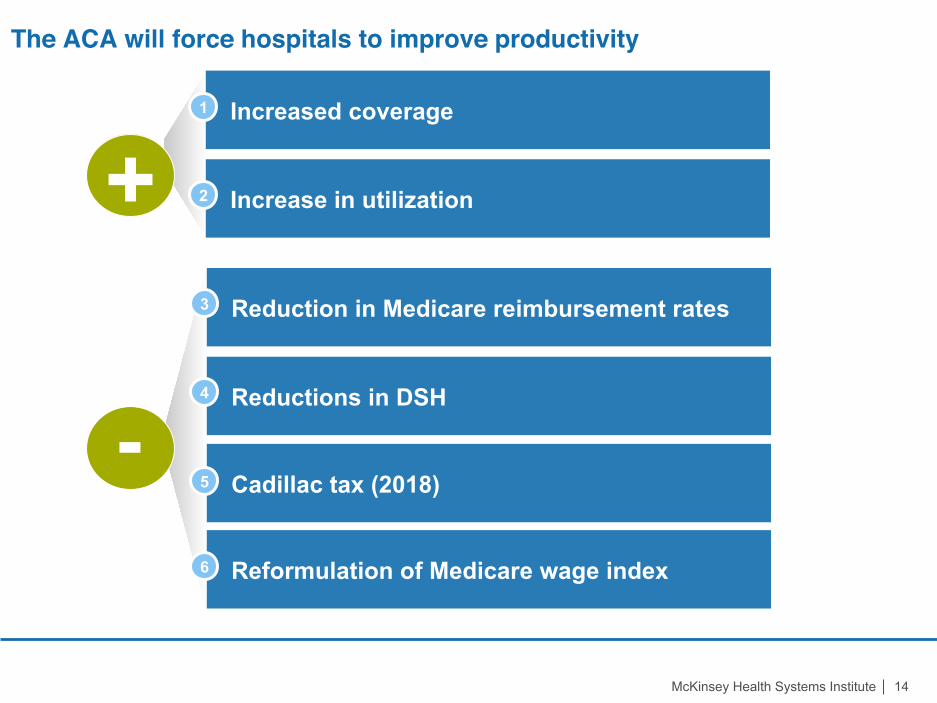

Increased coverage 1

Increase in utilization 2

Cadillac tax (2018) 5

Reductions in DSH 4

Reduction in Medicare reimbursement rates 3

Reformulation of Medicare wage index 6

The ACA will force hospitals to improve productivity!

+

-

McKinsey Health Systems Institute 15

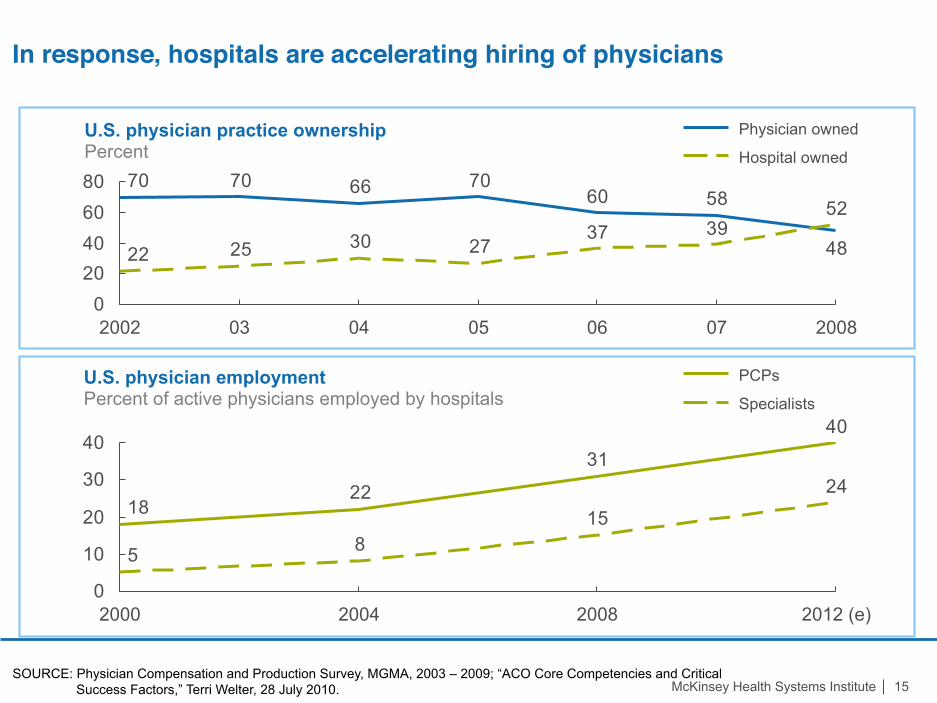

48

586070667070

523937

27302522

020406080

2002

U.S. physician practice ownership Percent

2008 06 05 07 04 03

Hospital owned

Physician owned

SOURCE: Physician Compensation and Production Survey, MGMA, 2003 – 2009; “ACO Core Competencies and Critical Success Factors,” Terri Welter, 28 July 2010.

40

31

2218

24

1585

0

10

20

30

40

2012 (e) 2008 2004 2000

U.S. physician employment Percent of active physicians employed by hospitals

PCPs

Specialists

In response, hospitals are accelerating hiring of physicians!

McKinsey Health Systems Institute 16

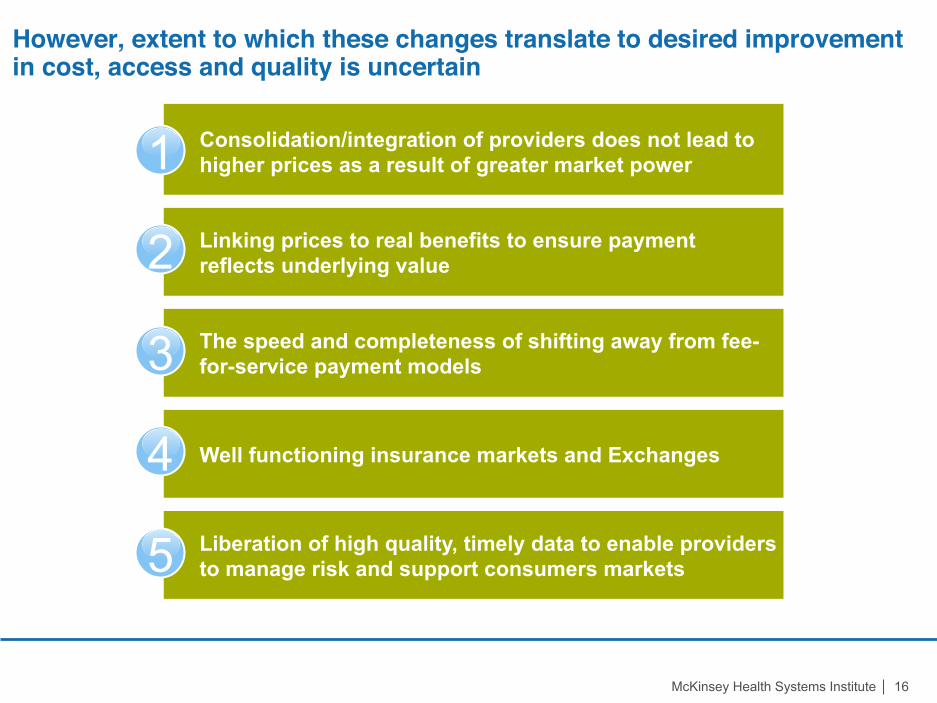

However, extent to which these changes translate to desired improvement in cost, access and quality is uncertain!

Consolidation/integration of providers does not lead to higher prices as a result of greater market power 1 Linking prices to real benefits to ensure payment reflects underlying value 2

The speed and completeness of shifting away from fee-for-service payment models 3

Well functioning insurance markets and Exchanges 4

Liberation of high quality, timely data to enable providers to manage risk and support consumers markets 5

McKinsey Health Systems Institute 17

Summary !

The fundamental issue in U.S. health care for next decade will be cost and affordability

Ultimately, budget pressures will force policies that achieve slower Medicare and Medicaid cost growth

The Affordable Care Act has accelerated an environment for change in the health system

McKinsey Health Systems Institute 18

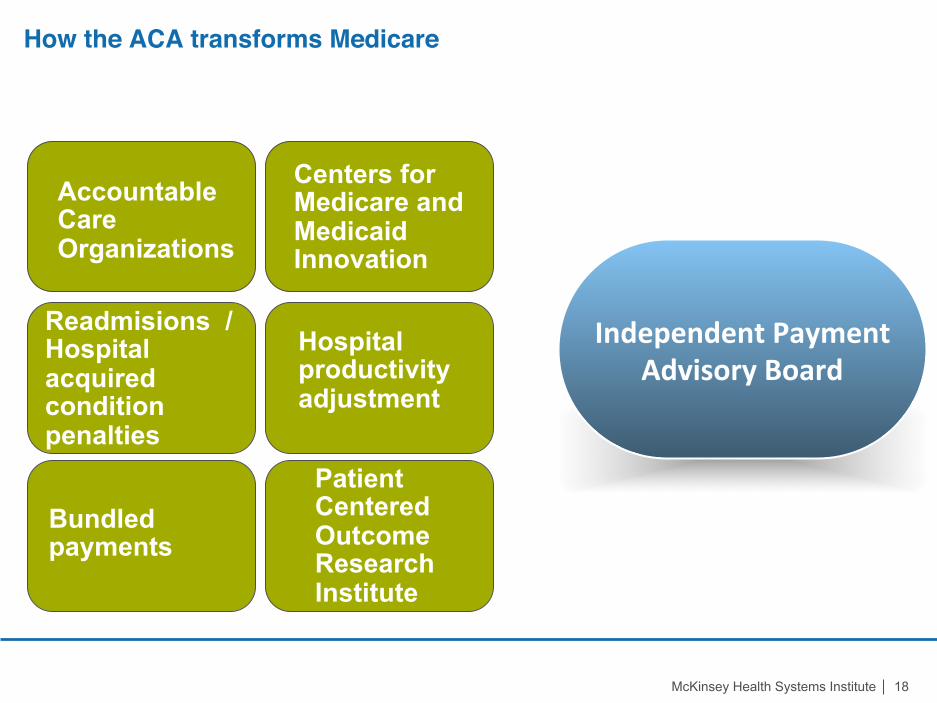

Patient Centered Outcome Research Institute

Centers for Medicare and Medicaid Innovation

Readmisions / Hospital acquired condition penalties

Hospital productivity adjustment

Bundled payments

Accountable Care Organizations

How the ACA transforms Medicare !

Independent Payment Advisory Board

McKinsey Health Systems Institute 19

Thank you!

Questions