Embed Size (px)

Citation preview

Week 5Chapter 12

Strategy, Balanced Scorecard, and Strategic Profitability

Analysis1

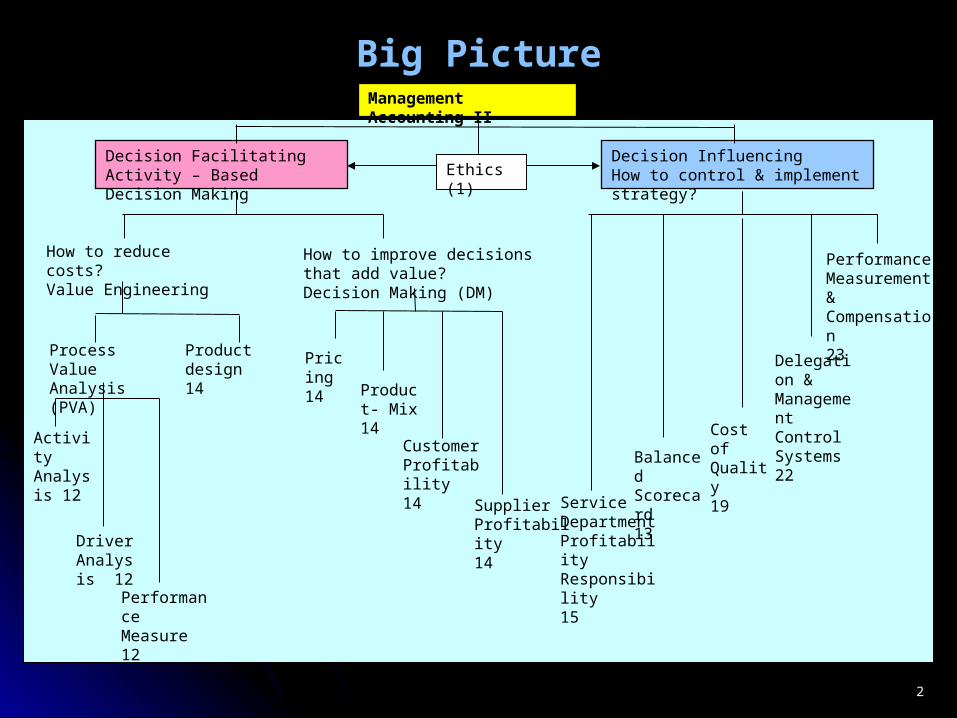

Decision FacilitatingActivity – Based Decision Making

Decision InfluencingHow to control & implement strategy?

Management Accounting II

How to reduce costs?Value Engineering

Driver Analysis 12

Activity Analysis 12

Performance Measure12

How to improve decisions that add value?Decision Making (DM)

ServiceDepartmentProfitabilityResponsibility15

Balanced Scorecard13

Cost of Quality19

Delegation & Management Control Systems 22

Performance Measurement & Compensation23

Ethics (1)

2

Process Value Analysis (PVA)

Pricing14

Product- Mix14

Customer Profitability14

Supplier Profitability14

Product design14

Big Picture

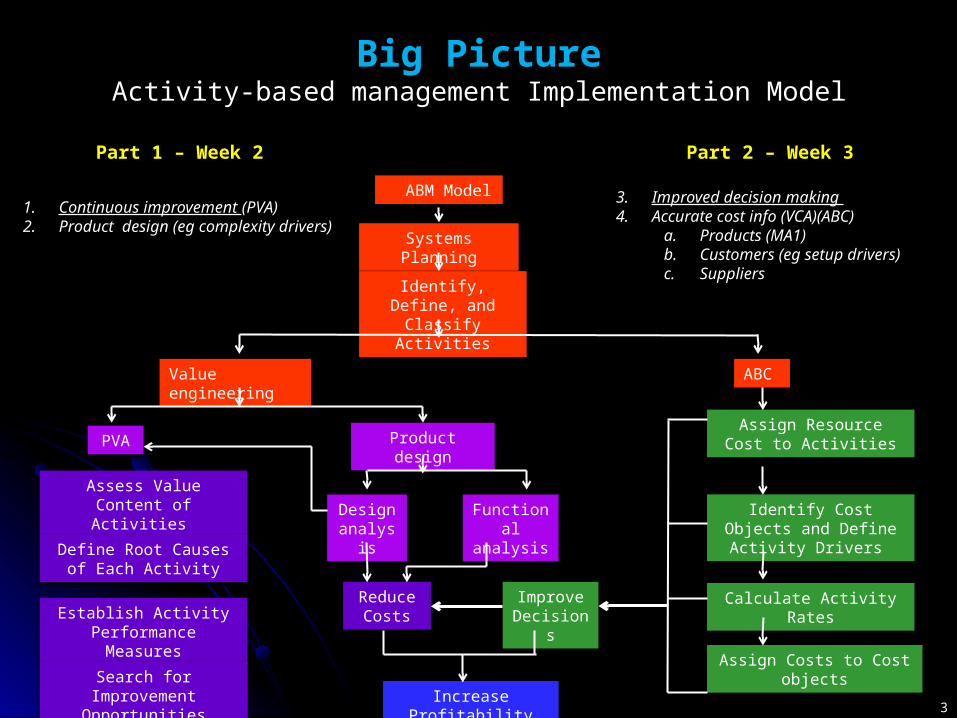

Big PictureActivity-based management Implementation Model

3

ABM Model

Systems Planning

Identify, Define, and Classify Activities

Reduce Costs

Improve Decisions

Increase Profitability

ABC

1. Continuous improvement (PVA) 2. Product design (eg complexity drivers)

3. Improved decision making 4. Accurate cost info (VCA)(ABC)

a. Products (MA1)b. Customers (eg setup drivers)c. Suppliers

PVA

Assess Value Content of Activities

Define Root Causes of Each Activity

Establish Activity Performance Measures

Search for Improvement Opportunities

Part 1 – Week 2 Part 2 – Week 3

Assign Resource Cost to Activities

Identify Cost Objects and Define Activity Drivers

Calculate Activity Rates

Assign Costs to Cost objects

Product design

Value engineering

Design analysis

Functional analysis

Big PictureActivity-Based versus Strategic-Based Responsibility Accounting

4

Responsibility Accounting

Financial-based centers (Cost,

Revenue, Profit, Investment)

Strategy-basedResponsibility accounting system translates the

strategy of the organization into operational objectives and measures

Which one is bottom up/top down?

Activity-based AB system adds a process perspective to the financial perspective of the functional-based

responsibility accounting system.

7

Communication Content, Management Control and the Balanced Scorecard?

Strategy Alignment FWK• Focusing• Competitors• Customers

Systems Thinking• Visualizing• Strategy Map

Measurement• Formalizing• Attributes

Strategic Responsibility Systems

8

• System – role of employees

• Creating alignment with strategy

Visualizing, Formalizing the System (Long term)

• Employee skills, attitude, teamwork

• Customer behavior - satisfaction

Decision making

(Problem Solving)

(Short term)

Outcomes• Empowerment• Learning• Fun place to work

• Low turnoverOutputs• On-time delivery• Less Errors• Fast cycle time• Cheques processed • Customer return• Word of mouth marketing

• What do we have to do today?

• To get what we want tomorrow?

Strategic Responsibility SystemsCreating alignment with non-financial

performance measures

1. Familiarization

2. Learning Objectives

3. Game Objectives

17 Quarters

Highest profit

Diary One-Page summary of learning

Chapter

12 & 23 14 19Accounting Customer Internal

Strategy

Systems Thinking

Measurement

Week 5-8: Learning Objective Summary

10

Week 5: Learning Objective Summary

Strategy Learning objective 1: Recognize which of two generic strategies a company is using

Reengineering Learning objective 2: Understand what comprises reengineering

Balanced Scorecard Learning objective 3: Understand the four perspectives of the balanced scorecard

Evaluating Strategy Learning objective 4: Analyze changes in operating income to evaluate strategy

Engineered & Discretionary Cost Learning objective 5: Distinguish engineered costs from discretionary costs

Managing Unused Capacity Learning objective 6: Identify unused capacity and how to manage it

Balanced ScorecardreengineeringStrategyEngineered &

Discretionary CostManaging Unused

CapacityEvaluating Strategy

1Strategy – How do firms succeed?

11

© Neale O'Connor 2010

Strategy Reengineering Balanced Scorecard Engineered & Discretionary Cost

Managing Unused CapacityEvaluating Strategy

12

Strategy Alignment FWK•Focusing•Competitors•Customers

Strategy Reengineering Balanced Scorecard Engineered & Discretionary Cost

Managing Unused CapacityEvaluating Strategy

13

Why are we doing this? – to help your firm become more successful

What do you mean by success?

Name some successful firms?

Strategy - Every firm has to have a plan that will lead to success?

Measurement - How to we measure progress towards success?

Strategy – How do firms succeed?

Strategy Reengineering Balanced Scorecard Engineered & Discretionary Cost

Managing Unused CapacityEvaluating Strategy

Learning objective 1:Recognize which of two generic strategies a company is using… product differentiation or cost leadership

1

14

Strategy Reengineering Balanced Scorecard Engineered & Discretionary Cost

Managing Unused CapacityEvaluating Strategy

16

How do we implement strategy?

Strategy Formulation

Strategy Execution

SCA

Com

petit

ors

Customer

Customer Internal

Processes Learning &

Growth

Strategy Map-Business Model

Benchmarking , Memory, Learning

Action PlansMKT

OPHRM

Rank Action Date

Initiatives Measure(KPI) Target

Balanced Scorecard

CommunicatingPeople controls-Personnel-Culture

Formulation of actions + targetsAction controls-Behavioral Constraint (Locks)-Preaction Reviews (Budget setting)-Action Accountability (Standard operating procedures)-Redundancy

Formulation of targets + rewardsResults controls-Measure-Targets-Rewards

HRM

MKT

OP

1. Focusing 2. Visualizing 3. Formalizing

MEASUREMENT

3. Formalizing

Cannot manage what you cannot measureAligning (role clarity)Action controls(dos and don’ts)Results controls(incentives)

Strategy Reengineering Balanced Scorecard Engineered & Discretionary Cost

Managing Unused CapacityEvaluating Strategy

17

Basic Business Strategies

1. Product Differentiation – an organization’s ability to offer products or services perceived by its customers to be superior and unique relative to the products or services of its competitors

Leads to brand loyalty and the willingness of customers to pay high prices

Example: A retailer of computers might offer on-site repair service, a feature not offered by other rivals in the local market.

2. Cost Leadership – an organization’s ability to achieve lower costs relative to competitors through productivity and efficiency improvements, elimination of waste, and tight cost control

Leads to lower selling prices

Example: A company might redesign a product so that fewer parts are needed, lowering production costs and the costs of maintaining the product after purchase.

Strategy Reengineering Balanced Scorecard Engineered & Discretionary Cost

Managing Unused CapacityEvaluating Strategy

Which product function offering can we best compete with?

Price range (HK$)

15,000-55,000

5,000-10,000

2,000-4,000

2,000-4000

18

Strategy Reengineering Balanced Scorecard Engineered & Discretionary Cost

Managing Unused CapacityEvaluating Strategy

Basic Business Strategies

3. A focusing strategy happens when a firm selects or emphasizes a market or customer segment in which to compete.

19

Exercise – How do firms succeed?

List some cost leaders/differentiators that you know of

Why do you use a particular service?Save moneyGood quality service

Strategy Reengineering Balanced Scorecard Engineered & Discretionary Cost

Managing Unused CapacityEvaluating Strategy

Commodities Cost leadership business Fast food? It is not because that it is cheap but how a firm competes People go to a product and pay more (differentiation) Different industries

20

Strategy Reengineering Balanced Scorecard Engineered & Discretionary Cost

Managing Unused CapacityEvaluating Strategy

Q. Which phone vendors follow cost leadership and/or product differentiation strategy?

Basic Business Strategies : Example

21

Strategy Reengineering Balanced Scorecard Engineered & Discretionary Cost

Managing Unused CapacityEvaluating Strategy

Q. Which phone vendors follow cost leadership and/or product differentiation strategy?

Basic Business Strategies : Example

22

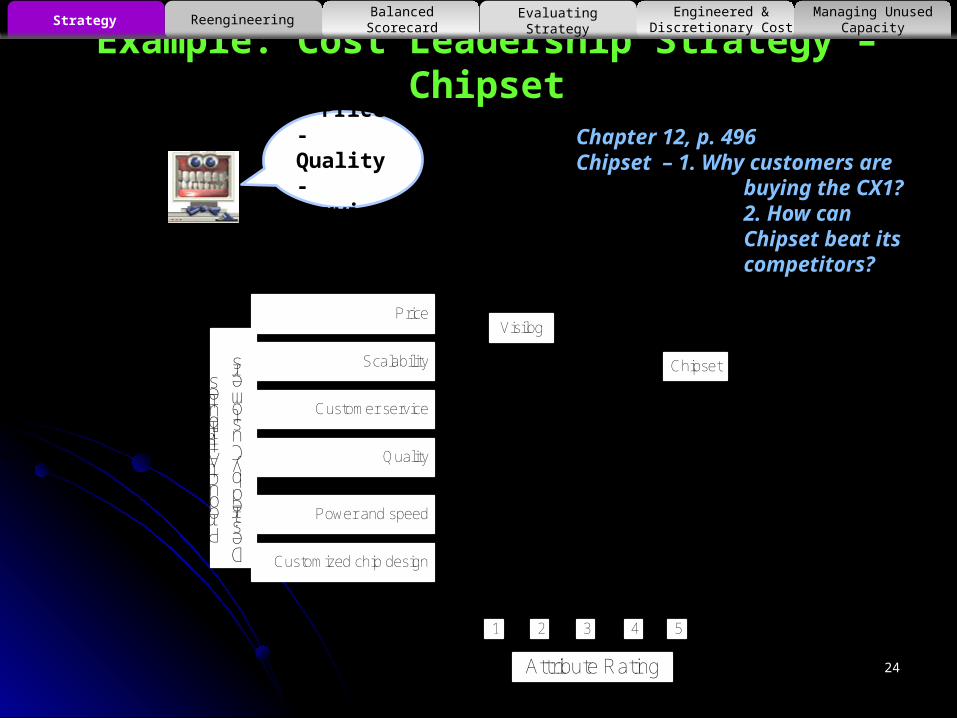

Strategy Alignment FWK•Customer preference map

Strategy Reengineering Balanced Scorecard Engineered & Discretionary Cost

Managing Unused CapacityEvaluating Strategy

Chipset, a integrated-circuits company produces a single specialized product, CX1, a standard, high-performance microchip. It can be used in multiple applications and enjoys a reputation for superior features with flexible design to meet customers’ needs.

23

Strategy Reengineering Balanced Scorecard Engineered & Discretionary Cost

Managing Unused CapacityEvaluating Strategy

Example: Cost Leadership Strategy – Chipset

24

Example: Cost Leadership Strategy – ChipsetChapter 12, p. 496Chipset – 1. Why customers are

buying the CX1? 2. How can Chipset beat its competitors?

Strategy Reengineering Balanced Scorecard Engineered & Discretionary Cost

Managing Unused CapacityEvaluating Strategy

Attribute Rating

1 2

Customized chip design

53 4

Power and speed

Quality

Customer service

Scalability

Price

Product Attributes

Desired by Customers

Chipset

Visilog

- Price- Quality- Service

25

LO1: Understand customer preference maps

LO1: Decide on a cost-leadership strategy(Chipset’s strategy)

LO1: Build internal capabilities to achieve cost leadership

LO3:Strategy implementation- Balanced scorecard

LO4: Evaluating strategy- Measurement

LO5: Management of Capabilities

LO2: Value engineering;Process engineering

- Price- Quality- Service

Strategy Reengineering Balanced Scorecard Engineered & Discretionary Cost

Managing Unused CapacityEvaluating Strategy

Example: Cost Leadership Strategy – Chipset

2What is Reengineering?

27

© Neale O'Connor 2010

Strategy Reengineering Balanced Scorecard Engineered & Discretionary Cost

Managing Unused CapacityEvaluating Strategy

28

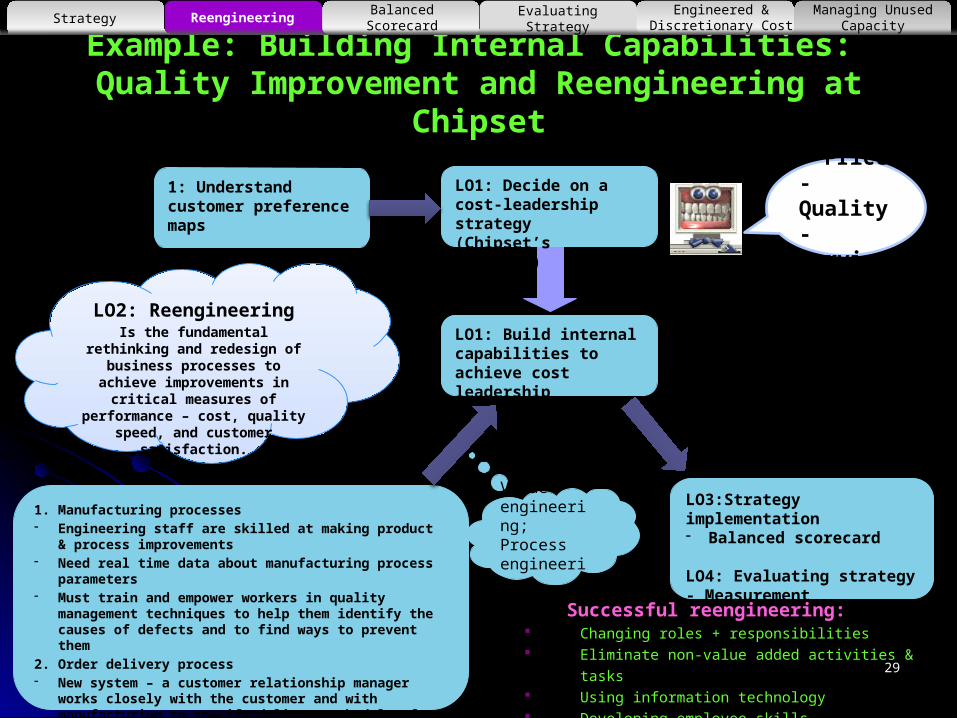

Example: Building Internal Capabilities: Quality Improvement and Reengineering at Chipset

When do we maximize the benefits of reengineering?

When the reengineered process cuts across functional lines.

Successful reengineering: Changing roles + responsibilities Eliminate non-value added activities & tasks Using information technology Developing employee skills Learning objective 2 :

Understand what comprises reengineering… redesigning business processes to improve performance by reducing cost and improving quality

2

Strategy Reengineering Balanced Scorecard Engineered & Discretionary Cost

Managing Unused CapacityEvaluating Strategy

29

1. Manufacturing processes- Engineering staff are skilled at making product & process

improvements- Need real time data about manufacturing process parameters- Must train and empower workers in quality management

techniques to help them identify the causes of defects and to find ways to prevent them

2. Order delivery process- New system – a customer relationship manager works closely

with the customer and with manufacturing to specify delivery schedules for CX1 one month in advance of shipment.

Example: Building Internal Capabilities: Quality Improvement and Reengineering at Chipset

- Price- Quality- Service

LO1: Build internal capabilities to achieve cost leadership

LO3:Strategy implementation- Balanced scorecard

LO4: Evaluating strategy- Measurement

LO1: Decide on a cost-leadership strategy(Chipset’s strategy)

LO2: ReengineeringIs the fundamental rethinking and redesign of business processes to achieve improvements in critical measures of performance – cost,

quality speed, and customer satisfaction.

Strategy Reengineering Balanced Scorecard Engineered & Discretionary Cost

Managing Unused CapacityEvaluating Strategy

Successful reengineering: Changing roles + responsibilities Eliminate non-value added activities & tasks Using information technology Developing employee skills

Value engineering;Process engineering

1: Understand customer preference maps

3What is the Balanced Scorecard?

30

© Neale O'Connor 2010

Strategy Reengineering Balanced Scorecard Engineered & Discretionary Cost

Managing Unused CapacityEvaluating Strategy

What is the Balanced Scorecard?Environment- Government regulations- Securities laws- Financial reporting

Customer- Customer values & needs- Competitor offerings

Learning and Growth– People (Skills, Satisfaction)

- Information system- Organization culture (Norms & Values)

- Highest control over change- Change takes longer = less attention

CustomerProduct/Service attributes,

Relationship, Image- Low control over

change- Change can be fast

= more attention

FinancialRevenue – Costs

- No control

Increasing amount of control over the business model

Increasing amount of attention that is typically given by management

Least attention

Internal Business Process– Innovation, Operations, Customer Service, Regulatory requirements

- Medium control over change- Change can be fast (ie BPR)

© Neale O'Connor 2014

Most attention

31

Strategy Reengineering Balanced Scorecard Engineered & Discretionary Cost

Managing Unused CapacityEvaluating Strategy

Learning objective 3 :Understand the four perspectives of the balanced scorecard…financial, customer, internal business process, learning and growth

3

It is about balancing:

Strategy and operations Measurement of financial and non-financial

indicators Systems thinking – lead and lag indicators

© Neale O'Connor 2014

What is the Balanced Scorecard?

32

Strategy Reengineering Balanced Scorecard Engineered & Discretionary Cost

Managing Unused CapacityEvaluating Strategy

33

SMS GOAL

Strategic objectives

Measures

SystemsThinking

Goal Alignment

On-TimeDecisionMaking

AccurateDecisionMaking

Learning

What is the Balanced Scorecard?

Strategy Reengineering Balanced Scorecard Engineered & Discretionary Cost

Managing Unused CapacityEvaluating Strategy

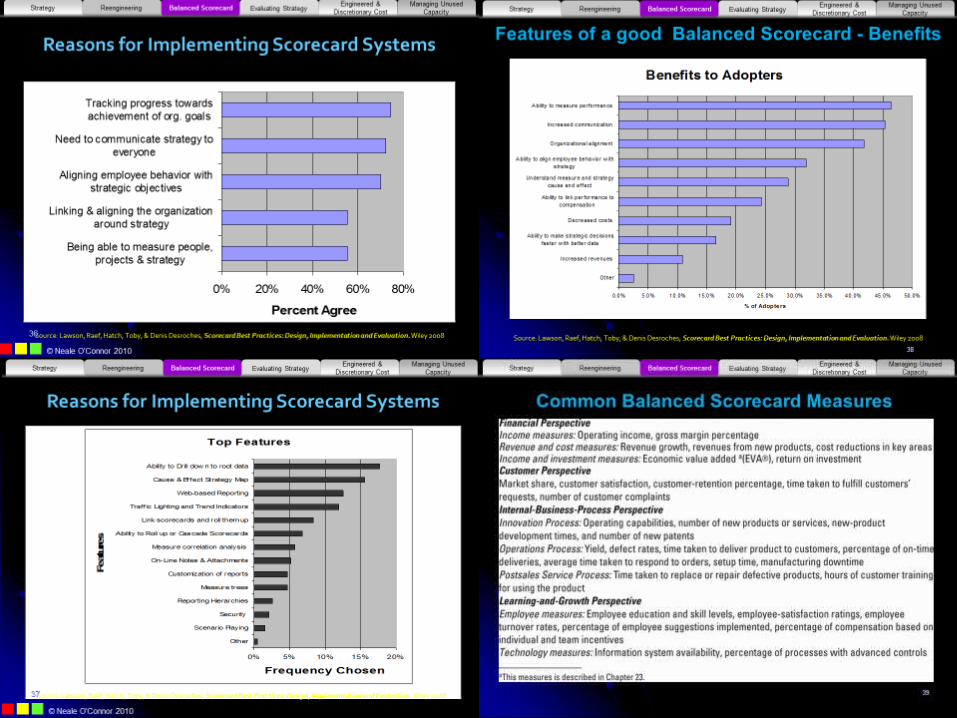

Features of a good Balanced Scorecard - Benefits Linking vision and strategy to employees’ everyday actions

Helps managers to manage the balance between financial and non-financial measures of cause and effect relations in the business system between internal and external perspectives

Setting priorities: This helps organizational participants to understand the priorities – the things that need to be done in order to create the right product or service to deliver value to the customer.

Managing change: The balanced scorecard also helps to manage change by determining the appropriate objectives and performance measures once the SCA and the strategy map of the business has been formulated. This helps organizations to manage change by helping to align participants’ attention, skills and effort towards the processes that matter for delivering value to the customer.

34

Strategy Reengineering Balanced Scorecard Engineered & Discretionary Cost

Managing Unused CapacityEvaluating Strategy

35

40

3.Example: Balanced

scorecard - Chipset (P.501)

Strategy Reengineering Balanced Scorecard Engineered & Discretionary Cost

Managing Unused CapacityEvaluating Strategy

Chipset, a integrated-circuits company produces a single specialized product, CX1, a standard, high-performance microchip. It can be used in multiple applications and enjoys a reputation for superior features with flexible design to meet customers’ needs.

Chipset’s manager implemented the Balance Scorcard approach to further its cost leadership strategy: improve quality and reengineer process.

Customer perspective ( example from CHIPSET INCORP.)

Objectives Measures Initiatives Target perf.

Actual perf.

Increase market share

Market share in market segment

Identify future needs of customers 78% 79.3%

Increase customer satisfaction

No .of new customers

Identify new target-customer segments

1 1

Increase customer satisfaction

Customer-satisfaction ratings

Increase customer focus of sales organization

90% 87%

Strategy Reengineering Balanced Scorecard Engineered & Discretionary Cost

Managing Unused CapacityEvaluating Strategy

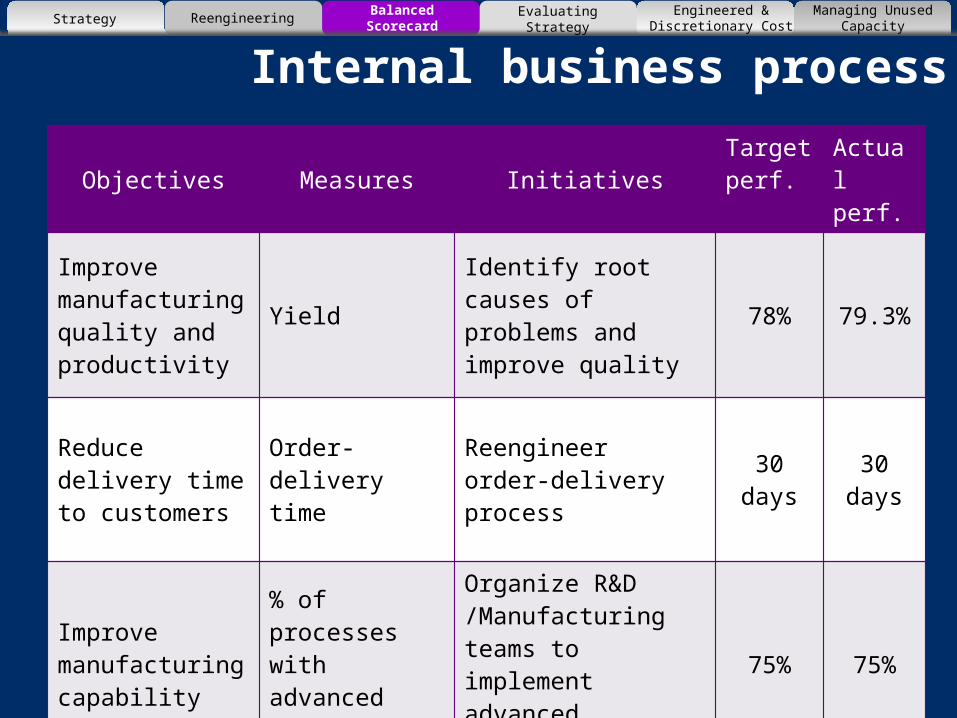

Internal business processObjectives Measures Initiatives Target

perf.Actual perf.

Improve manufacturing quality and productivity

YieldIdentify root causes of problems and improve quality

78% 79.3%

Reduce delivery time to customers

Order-delivery time

Reengineer order-delivery process

30 days

30 days

Improve manufacturing capability

% of processes with advanced controls

Organize R&D /Manufacturing teams to implement advanced controls

75% 75%

Strategy Reengineering Balanced Scorecard Engineered & Discretionary Cost

Managing Unused CapacityEvaluating Strategy

Learning-and-growth perspective

Objectives Measures Initiatives Target perf.

Actual perf.

Empower workforce

% of workers empowered to manage processes

Have supervisors act as coaches rather than decision makers

85% 90%

Align employees & organization goals

Employee-satisfaction ratings

Employees participation and suggestions program to build teamwork

80% 88%

Develop process skills

% of workers trained in process and quality management

Employee training program 90% 92%

Strategy Reengineering Balanced Scorecard Engineered & Discretionary Cost

Managing Unused CapacityEvaluating Strategy

44

Systems Thinking•Visualizing•Strategy Map

Strategy Reengineering Balanced Scorecard Engineered & Discretionary Cost

Managing Unused CapacityEvaluating Strategy

45

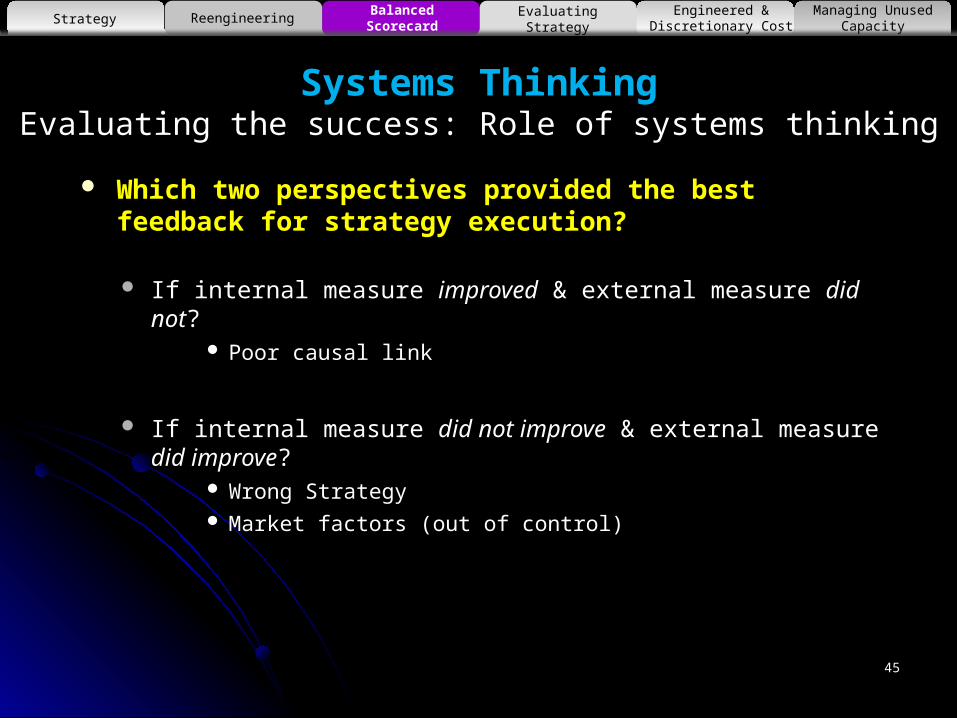

Systems ThinkingEvaluating the success: Role of systems thinking

Which two perspectives provided the best feedback for strategy execution?

If internal measure improved & external measure did not? Poor causal link

If internal measure did not improve & external measure did improve? Wrong Strategy Market factors (out of control)

Strategy Reengineering Balanced Scorecard Engineered & Discretionary Cost

Managing Unused CapacityEvaluating Strategy

46

Systems ThinkingWhat would success look like?

Use strategy map (systems thinking) to link long term success (strategy) to daily operational success

Strategy Reengineering Balanced Scorecard Engineered & Discretionary Cost

Managing Unused CapacityEvaluating Strategy

47

Systems Thinking•Visualizing•Strategy Map•Connecting the Dots

Systems ThinkingStrategy Reengineering Balanced Scorecard Engineered &

Discretionary CostManaging Unused

CapacityEvaluating Strategy

Factors leading to failure of BSCat Philips Lighting

Fishbone diagram

FAILUREUnreliable and

untimely information

No clear link to strategy

Information overload

Strategy Reengineering Balanced Scorecard Engineered & Discretionary Cost

Managing Unused CapacityEvaluating Strategy

49

3. Example: Balanced scorecard - Chipset Strategy Map (P.500)

Strategy Reengineering Balanced Scorecard Engineered & Discretionary Cost

Managing Unused CapacityEvaluating Strategy

50

Systems Thinking

Example: Fast food: map the following process and outcomes T

Shareholder value

Strategy Reengineering Balanced Scorecard Engineered & Discretionary Cost

Managing Unused CapacityEvaluating Strategy

Customer buying behavior

Sustained profitability

Employee satisfaction

Employee-added value

Customer satisfaction

Selection and staffing

51

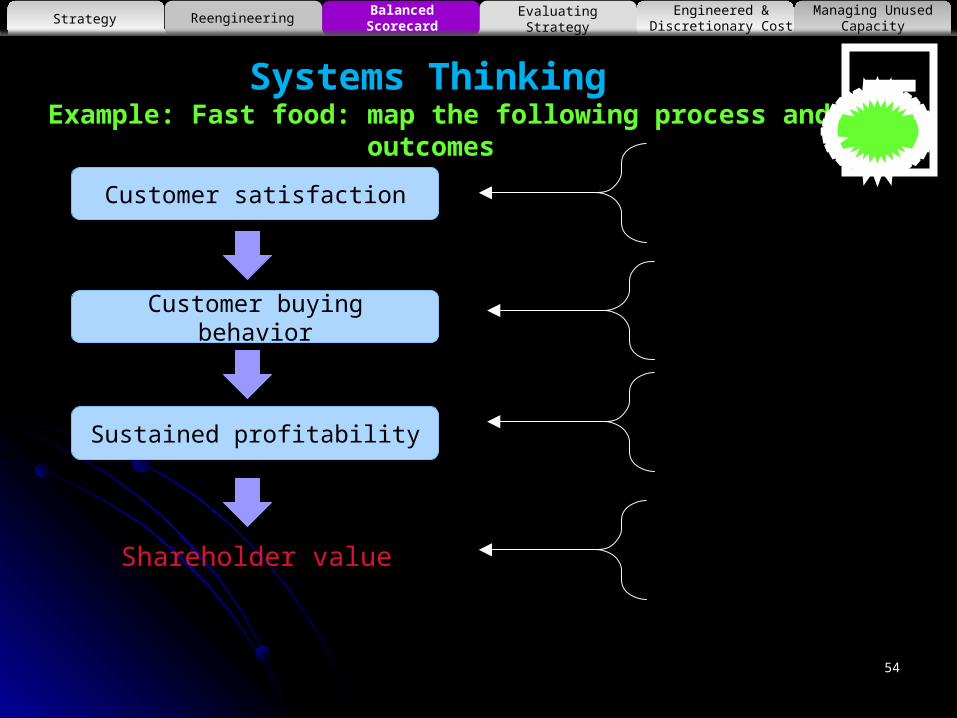

Systems Thinking Example: Fast food: map the following process and outcomes

1.2.3.

1.2.3.

1.2.

TStrategy Reengineering Balanced Scorecard Engineered &

Discretionary CostManaging Unused

CapacityEvaluating Strategy

52

Shareholder value

1.2.3.

1.2.3.

1.2.3.

1.2.3.

TSystems Thinking Example: Fast food: map the following process and outcomes

Strategy Reengineering Balanced Scorecard Engineered & Discretionary Cost

Managing Unused CapacityEvaluating Strategy

53

Systems Thinking Example: Fast food: map the following process and outcomes

Strategy Reengineering Balanced Scorecard Engineered & Discretionary Cost

Managing Unused CapacityEvaluating Strategy

TSelection and staffing

Employee satisfaction

Employee-added value

54

Systems Thinking Example: Fast food: map the following process and outcomes

Strategy Reengineering Balanced Scorecard Engineered & Discretionary Cost

Managing Unused CapacityEvaluating Strategy

TCustomer satisfaction

Customer buying behavior

Sustained profitability

Shareholder value

55

Measurement•Formalizing•Attributes

Strategy Reengineering Balanced Scorecard Engineered & Discretionary Cost

Managing Unused CapacityEvaluating Strategy

Types of Measures / Indicators Key Result Indicators

Customer Satisfaction Profitability/campaign

Performance Indicators % Sales Increase % Campaign Conversion

Key Performance Indicator Availability Delays in delivary Resolution on 1st touch

56

Key Result Indicator

Key Performance

Indicator

Source Key Performance Indicators. D. Pamenter

Strategy Reengineering Balanced Scorecard Engineered & Discretionary Cost

Managing Unused CapacityEvaluating Strategy

57

3.Example: Balanced scorecard - Chipset Strategy Map (P.496)

Strategy Reengineering Balanced Scorecard

Engineered & Discretionary Cost

Managing Unused Capacity

Evaluating Strategy

58

Measurement Example: Which Measures Matter

Strategy Reengineering Balanced Scorecard Engineered & Discretionary Cost

Managing Unused CapacityEvaluating Strategy

Supervision Support Fairness

New hires Education

Work experience

QualityShopping experience

Timeliness

GrowthEarnings

Free cash flow

Each outletOver time

Better than competition

EmpowermentAccountability

FrequencyRetentionReferral

59

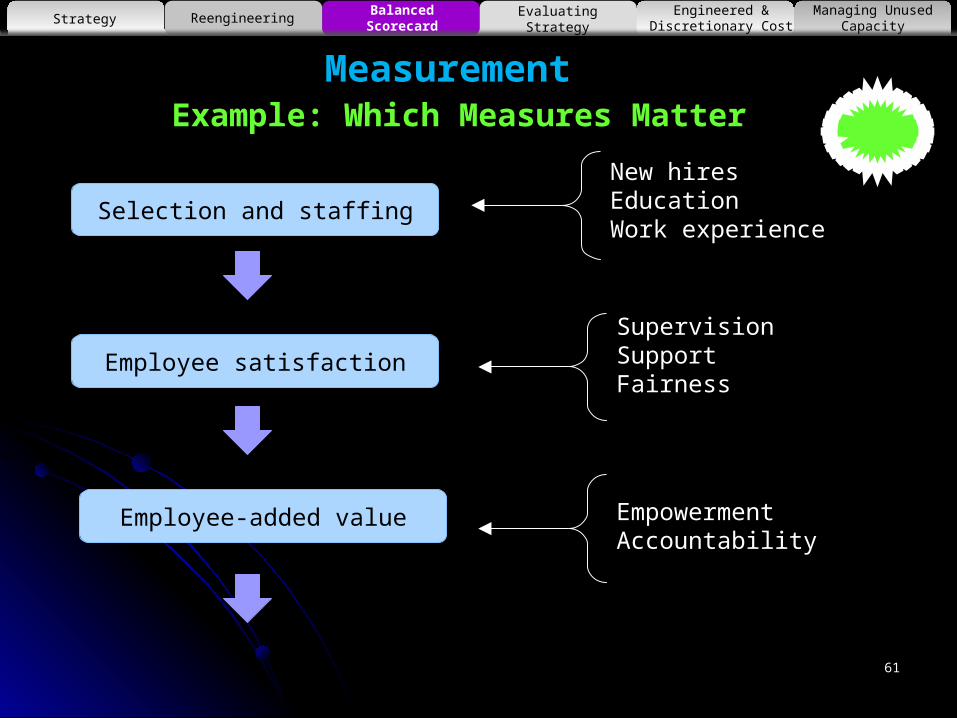

Systems Thinking Example: Fast food: map the following process and outcomes

Strategy Reengineering Balanced Scorecard Engineered & Discretionary Cost

Managing Unused CapacityEvaluating Strategy

TSelection and staffing

Employee satisfaction

Employee-added value

60

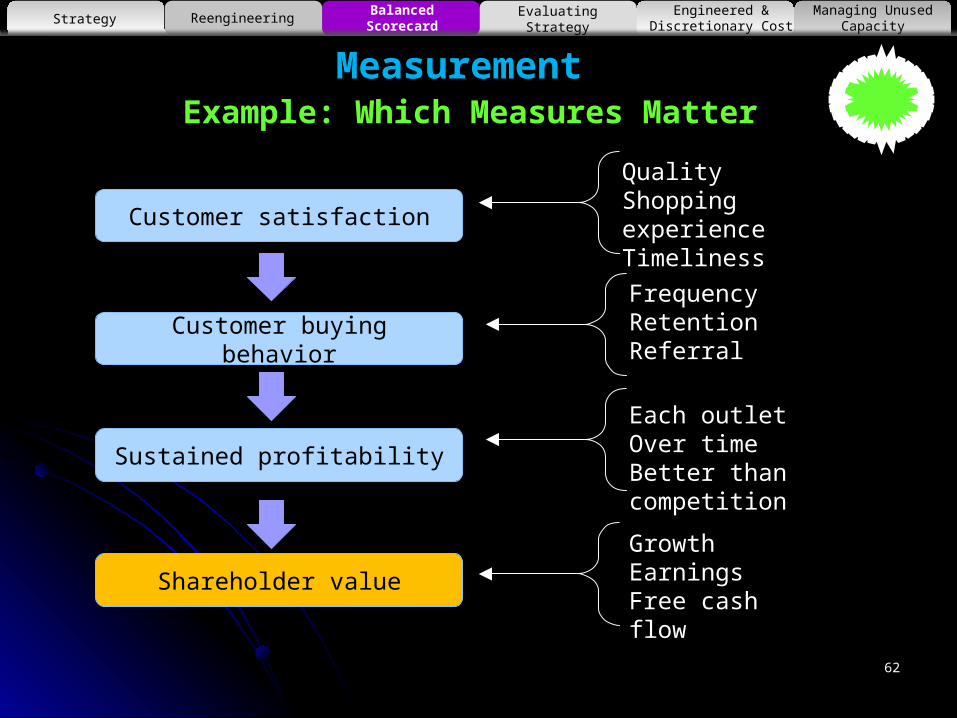

Systems Thinking Example: Fast food: map the following process and outcomes

Strategy Reengineering Balanced Scorecard Engineered & Discretionary Cost

Managing Unused CapacityEvaluating Strategy

TCustomer satisfaction

Customer buying behavior

Sustained profitability

Shareholder value

New hiresEducationWork experience

SupervisionSupportFairness

EmpowermentAccountability

61

Measurement Example: Which Measures Matter

Strategy Reengineering Balanced Scorecard Engineered & Discretionary Cost

Managing Unused CapacityEvaluating Strategy

Selection and staffing

Employee satisfaction

Employee-added value

QualityShopping experienceTimeliness

FrequencyRetentionReferral

Each outletOver timeBetter than competition

GrowthEarningsFree cash flow

Measurement Example: Which Measures Matter

62

Strategy Reengineering Balanced Scorecard Engineered & Discretionary Cost

Managing Unused CapacityEvaluating Strategy

Customer satisfaction

Customer buying behavior

Sustained profitability

Shareholder value

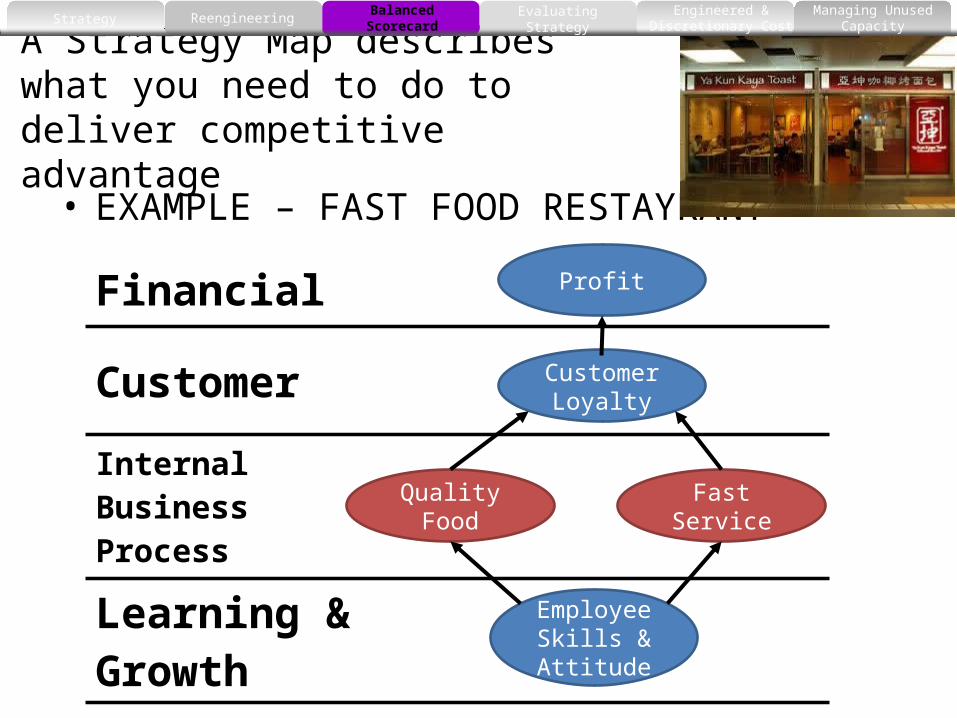

A Strategy Map describes what you need to do to deliver competitive advantage

• EXAMPLE – FAST FOOD RESTAYRANT

Financial

Customer

InternalBusinessProcess

Learning &Growth

Profit

Customer Loyalty

Quality Food

Fast Service

Employee Skills & Attitude

Strategy Reengineering Balanced Scorecard Engineered & Discretionary Cost

Managing Unused CapacityEvaluating Strategy

Class ExerciseStrategic Themes (The “Strategies”!)

1. Drive Sales through fantastic coffee2. Improve loyalty by providing a great

customer experience3. Improve margins by being an efficient

business

Format for a Strategic Theme –Desired “Business” Outcome [by the means to achieve it]

Strategy Reengineering Balanced Scorecard Engineered & Discretionary Cost

Managing Unused CapacityEvaluating Strategy

Financial Results

Our Customers

Our Business Process

Our People

Increase Sales Revenue

Increase Operating Profit

Reduce Operating Costs as a % of Sales

Offer a Great Coffee

Sensation!

Increase CustomerLoyalty – Get the

Customers toCome Back!

Quick, Reliable &Friendly, Service- Don’t Keep Customers Waiting

Serve Customers

Facilities Management

Supply Chain Management

Product Innovation

Standardize the New Coffee Making Process

Modernize the Look of the Coffee Shop –

Refurbish With Glass & Stainless

Buy a High-TechItalian Coffee

Machine

Change from Nescafe Instant to an Expensive

Italian Blend

Move to Purchasing Raw

Materials On-Line

Improve Inventory Management of Our

Raw Materials – Cups, Milk etc

Train Staff to get a Barista Qualification

At www.coffeeshop.com.au

Develop a Customer-Focused

Culture

Train Staff to Order On-Line

Strategy Reengineering Balanced Scorecard Engineered & Discretionary Cost

Managing Unused CapacityEvaluating Strategy

Financial Results

Our Customers

Our Business Process

Our People

Increase Operating Profit

Reduce Operating Costs as a % of Sales

Offer a Great Coffee

Sensation!

Increase CustomerLoyalty – Get the

Customers toCome Back!

Quick, Reliable &Friendly, Service- Don’t Keep Customers Waiting

Serve Customers

Facilities Management

Supply Chain Management

Product Innovation

Standardize the New Coffee Making Process

Modernize the Look of the Coffee Shop –

Refurbish With Glass & Stainless

Buy a High-TechItalian Coffee

Machine

Change from Nescafe Instant to an Expensive

Italian Blend

Move to Purchasing Raw

Materials On-Line

Improve Inventory Management of Our

Raw Materials – Cups, Milk etc

Train Staff to get a Barista Qualification

At www.coffeeshop.com.au

Develop a Customer-Focused

Culture

Train Staff to Order On-Line

Theme 1: Drive Sales Through Fantastic Coffee

Increase Sales Revenue

Strategy Reengineering Balanced Scorecard Engineered & Discretionary Cost

Managing Unused CapacityEvaluating Strategy

Financial Results

Our Customers

Our Business Process

Our People

Increase Operating Profit

Reduce Operating Costs as a % of Sales

Offer a Great Coffee

Sensation!

Increase CustomerLoyalty – Get the

Customers toCome Back!

Quick, Reliable &Friendly, Service- Don’t Keep Customers Waiting

Serve Customers

Facilities Management

Supply Chain Management

Product Innovation

Standardize the New Coffee Making Process

Modernize the Look of the Coffee Shop –

Refurbish With Glass & Stainless

Buy a High-TechItalian Coffee

Machine

Change from Nescafe Instant to an Expensive

Italian Blend

Move to Purchasing Raw

Materials On-Line

Improve Inventory Management of Our

Raw Materials – Cups, Milk etc

Train Staff to get a Barista Qualification

At www.coffeeshop.com.au

Develop a Customer-Focused

Culture

Train Staff to Order On-Line

Theme 2: Improve Loyalty by Providing a Great Customer Experience

Increase Sales Revenue

Strategy Reengineering Balanced Scorecard Engineered & Discretionary Cost

Managing Unused CapacityEvaluating Strategy

Financial Results

Our Customers

Our Business Process

Our People

Increase Operating Profit

Reduce Operating Costs as a % of Sales

Offer a Great Coffee

Sensation!

Increase CustomerLoyalty – Get the

Customers toCome Back!

Quick, Reliable &Friendly, Service- Don’t Keep Customers Waiting

Serve Customers

Facilities Management

Supply Chain Management

Product Innovation

Standardize the New Coffee Making Process

Modernize the Look of the Coffee Shop –

Refurbish With Glass & Stainless

Buy a High-TechItalian Coffee

Machine

Change from Nescafe Instant to an Expensive

Italian Blend

Move to Purchasing Raw

Materials On-Line

Improve Inventory Management of Our

Raw Materials – Cups, Milk etc

Train Staff to get a Barista Qualification

At www.coffeeshop.com.au

Develop a Customer-Focused

Culture

Train Staff to Order On-Line

Theme 3: Improve Margins by Being an Efficient Business

Increase Sales Revenue

Strategy Reengineering Balanced Scorecard Engineered & Discretionary Cost

Managing Unused CapacityEvaluating Strategy

Financial Results

Our Customers

Our Business Process

Our People

Increase Sales Revenue

Increase Operating Profit Reduce

Operating Costs as a % of Sales

Offer a Great Coffee

Sensation!

Increase CustomerLoyalty – Get the

Customers toCome Back!

Quick, Reliable &Friendly, Service- Don’t Keep Customers Waiting

Serve Customers

Facilities Management

Supply Chain Management

Product Innovation

Standardize the New Coffee Making Process

Modernize the Look of the Coffee Shop –

Refurbish With Glass & Stainless

Buy a High-TechItalian Coffee

Machine

Change from Nescafe Instant to an Expensive

Italian Blend

Move to Purchasing Raw

Materials On-Line

Improve Inventory Management of Our

Raw Materials – Cups, Milk etc

Train Staff to get a Barista Qualification

At www.coffeeshop.com.au

Develop a Customer-Focused

Culture

Train Staff to Order On-Line

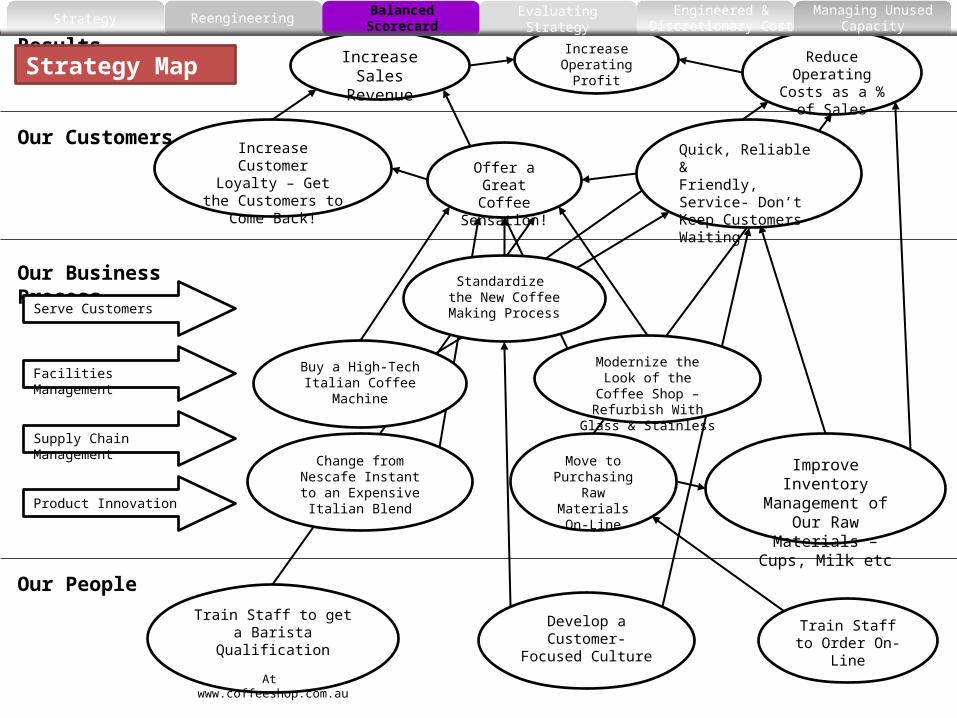

Strategy Map

Strategy Reengineering Balanced Scorecard Engineered & Discretionary Cost

Managing Unused CapacityEvaluating Strategy

Financial Results

Our Customers

Our Business Process

Our People

Increase Sales Revenue

Increase Operating Profit Reduce

Operating Costs as a % of Sales

Offer a Great Coffee

Sensation!

Increase CustomerLoyalty – Get the

Customers toCome Back!

Quick, Reliable &Friendly, Service- Don’t Keep Customers Waiting

Serve Customers

Facilities Management

Supply Chain Management

Product Innovation

Standardize the New Coffee Making Process

Modernize the Look of the Coffee Shop –

Refurbish With Glass & Stainless

Buy a High-TechItalian Coffee

Machine

Change from Nescafe Instant to an Expensive

Italian Blend

Move to Purchasing Raw

Materials On-Line

Improve Inventory Management of Our

Raw Materials – Cups, Milk etc

Train Staff to get a Barista Qualification

At www.coffeeshop.com.au

Develop a Customer-Focused

Culture

Train Staff to Order On-Line

Sales x ProductExpenses/Sales %

Service Quality Index

NOPATNet Operating Profit

After TaxCustomer Satisfaction Survey Result

Sales Repeat Customers/Total Sales %

Non-Conformances to Standardized Coffee

Making Process

Install Italian Coffee Machine (Y/N?)

Cleanliness Index

% Progress Barrista Training

Staff Satisfaction Survey % Staff Trained On-Line Ordering

Number & Type of Stockouts

Refurbishment Project (On Time, On Budget, On

Spec)

% Materials Ordered On-Line

Strategy Reengineering Balanced Scorecard Engineered & Discretionary Cost

Managing Unused CapacityEvaluating Strategy

4Evaluating Strategy

71

© Neale O'Connor 2010

Strategy Reengineering Balanced Scorecard Engineered & Discretionary Cost

Managing Unused CapacityEvaluating Strategy

72

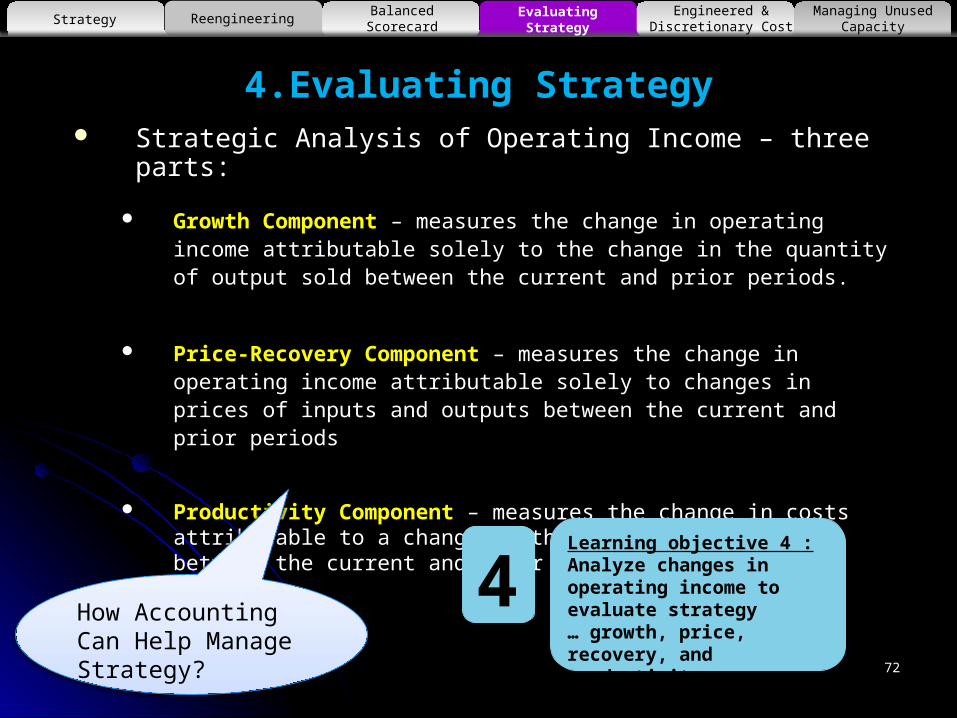

4.Evaluating Strategy Strategic Analysis of Operating Income – three parts:

Growth Component – measures the change in operating income attributable solely to the change in the quantity of output sold between the current and prior periods.

Price-Recovery Component – measures the change in operating income attributable solely to changes in prices of inputs and outputs between the current and prior periods

Productivity Component – measures the change in costs attributable to a change in the quantity of inputs between the current and prior periods

Strategy Reengineering Balanced Scorecard Engineered & Discretionary Cost

Managing Unused CapacityEvaluating Strategy

Learning objective 4 :Analyze changes in operating income to evaluate strategy… growth, price, recovery, and productivity

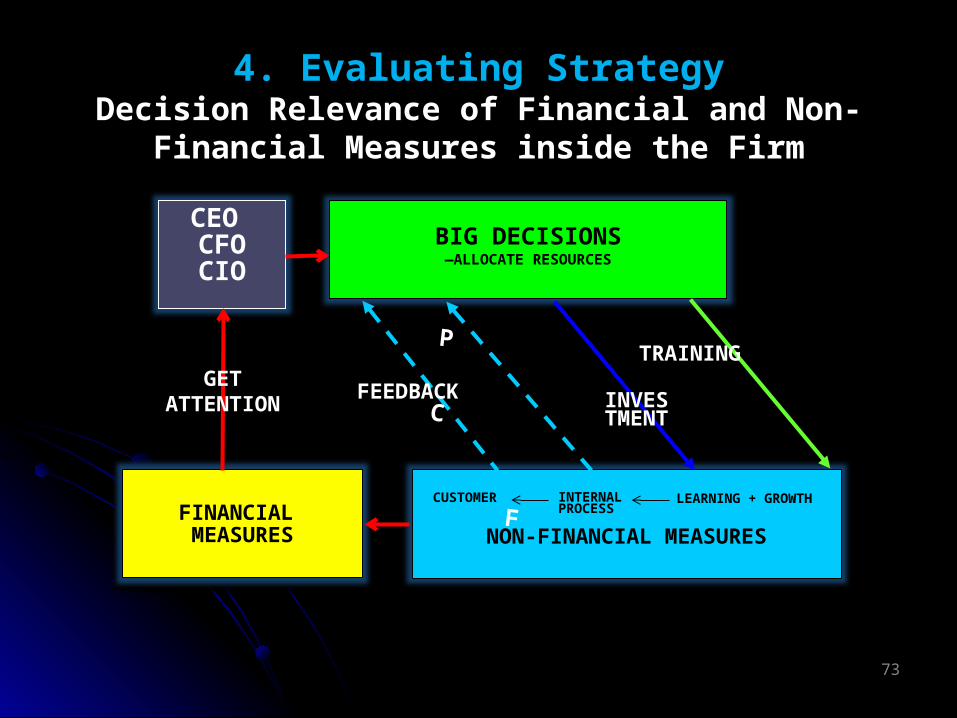

4How Accounting Can Help Manage Strategy?

73

NON-FINANCIAL MEASURES

BIG DECISIONS—ALLOCATE RESOURCES

FEEDBACK

CEO CFOCIO

P C

F

CUSTOMER INTERNAL

PROCESSLEARNING + GROWTH

FINANCIAL MEASURES

TRAININGGET

ATTENTION

4. Evaluating StrategyDecision Relevance of Financial and Non-Financial

Measures inside the Firm

INVESTMENT

74

75

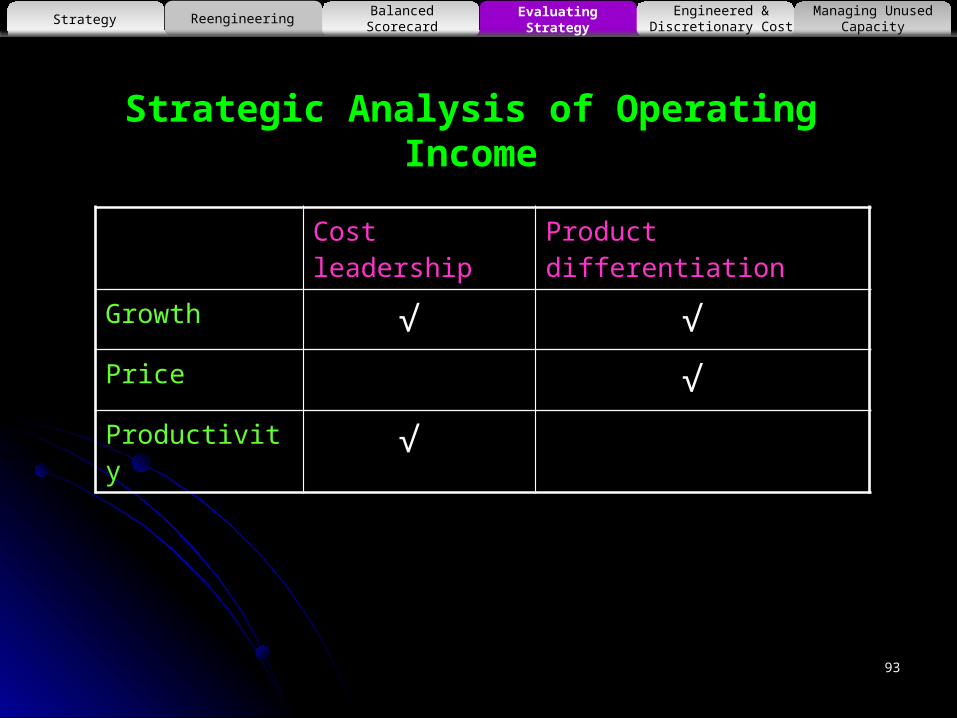

Strategic Analysis of Operating Income

Cost leadership Product differentiation

Growth √ √ Price √ Productivity √

Strategy Reengineering Balanced Scorecard Engineered & Discretionary Cost

Managing Unused CapacityEvaluating Strategy

Other accounting measures to support cost leadership?Manage costs through

Value engineering, Activity based costing, Activity based budgeting

Other measures to support differentiation?Focus on non-financial measures

Lead indicators of long term customer valueMeasures of innovation for long term sustainable differentiation

How Accounting Can Help Manage Strategy?

Example: Strategic Analysis of Operating Income

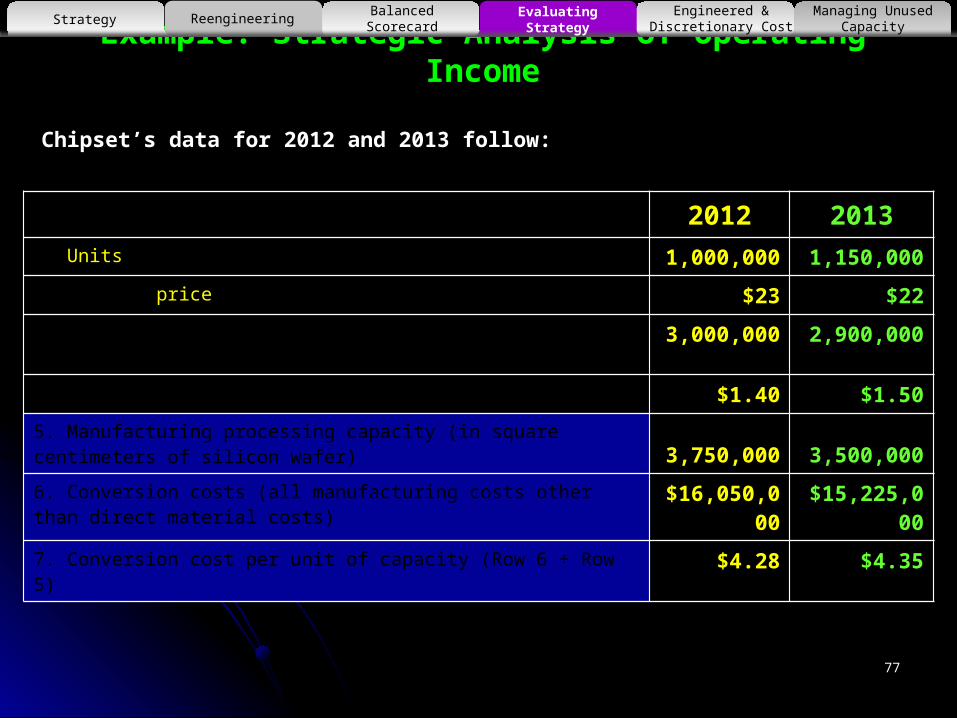

2012 20131. Units of CX1 produced and sold 1,000,000 1,150,0002. Selling price $23 $223. Direct materials (square centimeters of silicon wafers) 3,000,000 2,900,0004. Direct material cost per square centimeter $1.40 $1.505. Manufacturing processing capacity (in square centimeters of silicon wafer) 3,750,000 3,500,0006. Conversion costs (all manufacturing costs other than direct material costs) $16,050,000 $15,225,0007. Conversion cost per unit of capacity (Row 6 ÷ Row 5) $4.28 $4.35

Chipset’s data for 2012 and 2013 follow:

77

Strategy Reengineering Balanced Scorecard Engineered & Discretionary Cost

Managing Unused CapacityEvaluating Strategy

Example: Strategic Analysis of Operating Income

2012 2013

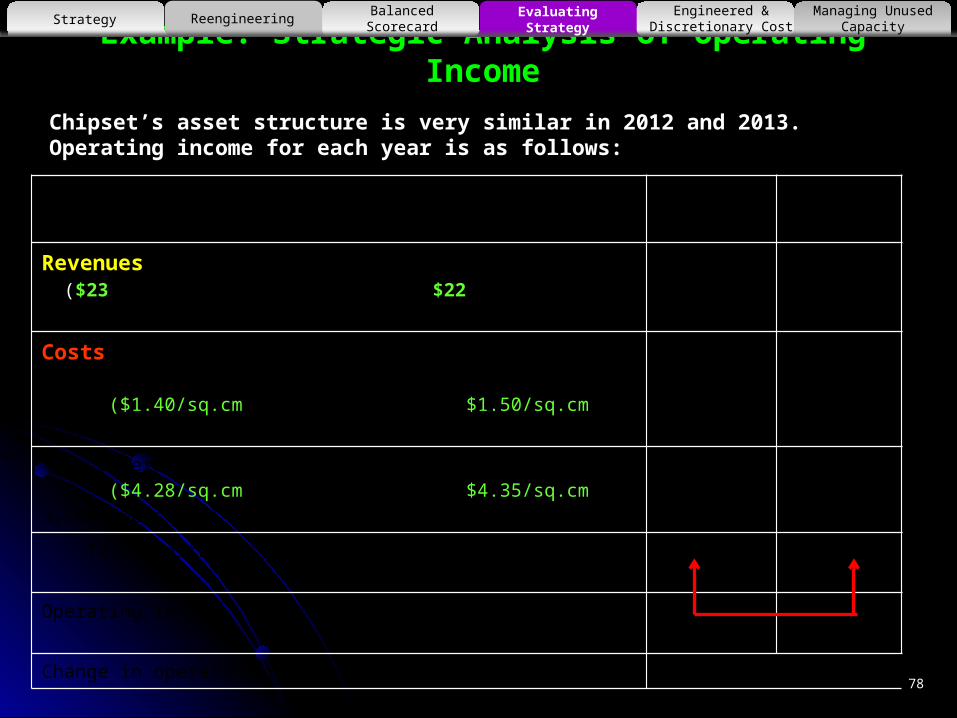

Revenues ($23 per unit x 1,000,000 units; $22per unit x 1,150,000 units) $23,000,000 $25,300,000Costs Direct material costs ($1.40/sq.cm x 3,000,000 sq.cm; $1.50/sq.cm x 2,900,000 sq.cm)

4,200,000 4,350,000 Conversion costs ($4.28/sq.cm x 3,750,000 sq.cm; $4.35/sq.cm x 3,500,000 sq.cm)

16,050,000 15,225,000 Total costs 20,250,000 19,575,000Operating income $2,750,000 $5,725,000Change in operating income $2,975,000 F

Chipset’s asset structure is very similar in 2012 and 2013. Operating income for each year is as follows:

78

Strategy Reengineering Balanced Scorecard Engineered & Discretionary Cost

Managing Unused CapacityEvaluating Strategy

79

Example: Strategic

Analysis of Operating

Income

Basic Data for Growth

80

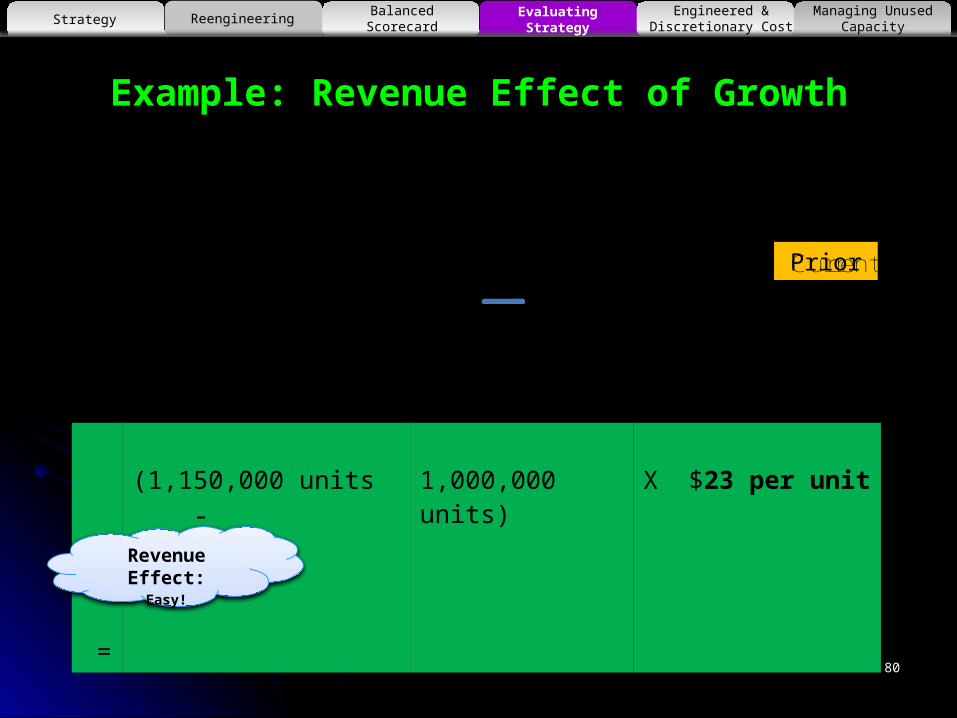

Example: Revenue Effect of Growth

Actual Units of Output Sold in

the Prior Period

Actual Units of Output Sold in the Current Period

XCurrentPeriodSellingPrice

RevenueEffect

OfGrowth

=

=

(1,150,000 units - 1,000,000 units) X $23 per unit

Strategy Reengineering Balanced Scorecard Engineered & Discretionary Cost

Managing Unused CapacityEvaluating Strategy

Revenue Effect:Easy!

Prior

81

Example: Cost Effect of Growth for Variable Costs

Actual Units of Input used to produce

Prior Period Output

Units of Input required to produce Current Output in the Prior Period

XCurrentPeriodInputPrice

CostEffect

OfGrowth

For Variable

Costs

=

Cost effect of growth for direct materials

= (3,000,000 sq.cm. x

1,150,000 units

- 3,000,000 sq.cm.) X $1.40 per sq.cm.

1,000,000 units

= (3,450,000sq.cm. -

3,000,000 sq.cm.) X $1.40 per sq.cm. = $630,000 U

Strategy Reengineering Balanced Scorecard Engineered & Discretionary Cost

Managing Unused CapacityEvaluating Strategy

Cost Effect:Keeping productivity constant – what should DM cost you in the

second period?

Prior

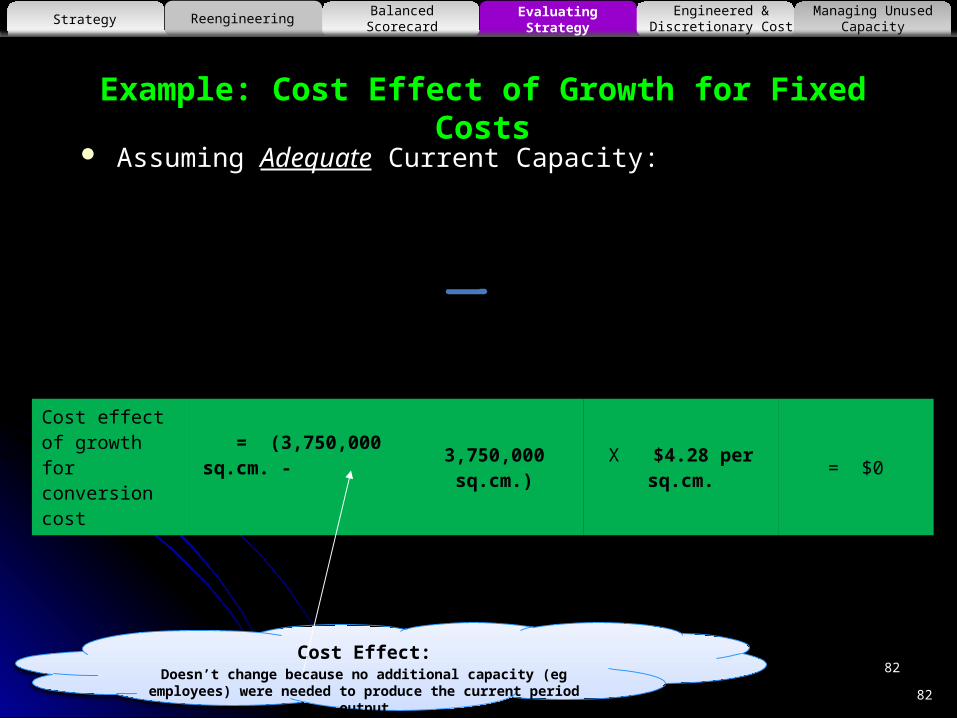

Example: Cost Effect of Growth for Fixed Costs

Assuming Adequate Current Capacity:

Actual Units of Capacity

in the Prior

Period

Actual Units of capacity in Prior Period to Produce Current Period Output

X

Prior Period Price

per unit of

capacity

CostEffect

OfGrowth

For FixedCosts

=

Cost effect of growth for conversion cost

= (3,750,000 sq.cm. - 3,750,000 sq.cm.) X $4.28 per sq.cm. = $0

Strategy Reengineering Balanced Scorecard Engineered & Discretionary Cost

Managing Unused CapacityEvaluating Strategy

82

82Cost Effect:

Doesn’t change because no additional capacity (eg employees) were needed to produce the current period output

83

Example: Cost Effect of Growth for Fixed Costs

Assuming Inadequate Current Capacity:

Actual Units

of Capacity in the Prior

Period

Units of Capacity required to produce Current Period Output in the Prior Period

X

Prior Period Price

per unit of

capacity

CostEffect

OfGrowth

For FixedCosts

=

Strategy Reengineering Balanced Scorecard Engineered & Discretionary Cost

Managing Unused CapacityEvaluating Strategy

Inadequate Capacity Effect:Fixed Costs don’t change because no additional capacity (eg employees) were needed to produce the current period output

84

Example: Strategic

Analysis of Operating

Income

Basic Data for

Price

85

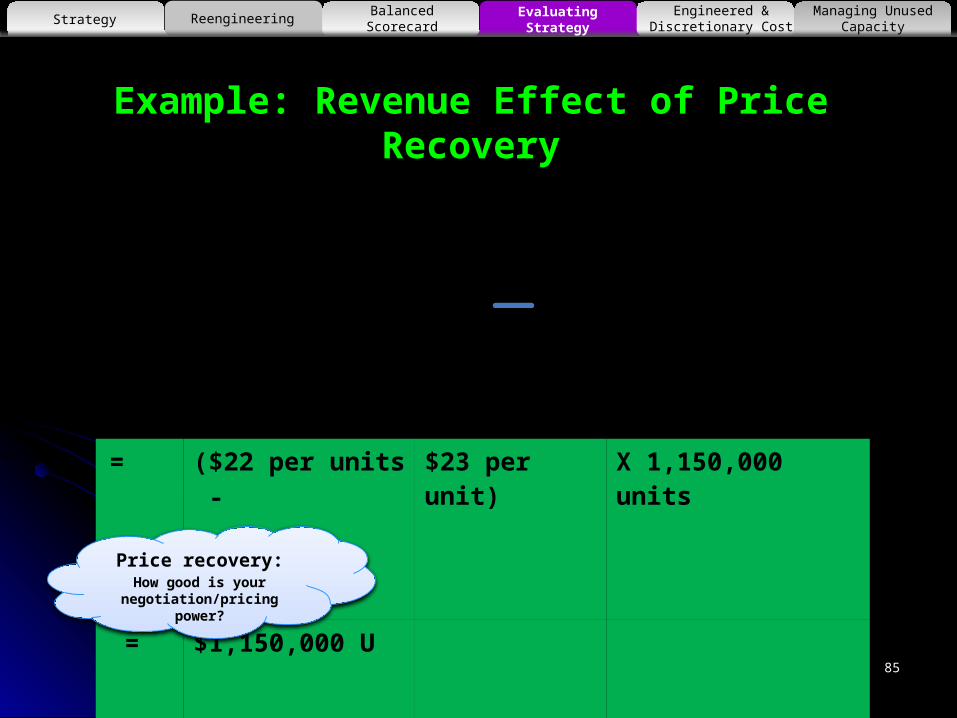

Example: Revenue Effect of Price Recovery

Prior Period Selling Price

Current Period Selling Price X

CurrentPeriod Units Sold

RevenueEffect

OfPrice-

Recovery

=

=

($22 per units - $23 per unit) X 1,150,000 units

=

$1,150,000 U

Strategy Reengineering Balanced Scorecard Engineered & Discretionary Cost

Managing Unused CapacityEvaluating Strategy

Price recovery:How good is your

negotiation/pricing power?

86

Example: Cost Effect of Price Recovery Variable Costs:

Prior Period Input Price

Current Period Input Price X

Units of Input

required to produce Current Period’s Output in the Prior Period

CostEffect

OfPrice-

Recovery for

Variable Costs

=

Cost effect of price recovery for direct materials

= ($1.50 per sq.cm. - $1.40 per sq.cm.) X 3,450,000 sq. = $345,000U

Strategy Reengineering Balanced Scorecard Engineered & Discretionary Cost

Managing Unused CapacityEvaluating Strategy

Price recovery:How good is your negotiation/pricing power?

This is the unit price effect due to increase in unit costs?

87

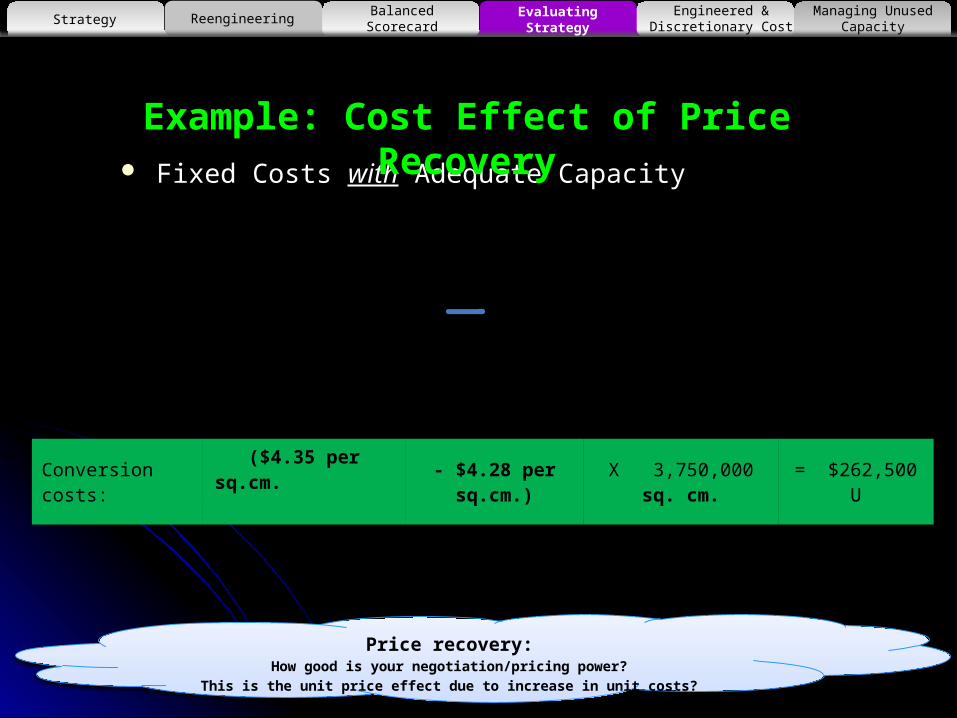

Fixed Costs with Adequate Capacity

Prior Period Price per Unit

of Capacity

Current Period Price per Unit of Capacity

X

Actual Units of Capacity on

Prior Period to Produce Current

Period’s Output

CostEffect

OfPrice-

Recovery for Fixed

Costs

=

Example: Cost Effect of Price Recovery

Conversion costs: ($4.35 per sq.cm.

- $4.28 per sq.cm.)

X 3,750,000 sq. cm. = $262,500 U

Strategy Reengineering Balanced Scorecard Engineered & Discretionary Cost

Managing Unused CapacityEvaluating Strategy

Price recovery:How good is your negotiation/pricing power?

This is the unit price effect due to increase in unit costs?

88

Fixed Costs without Adequate Capacity

Prior Period Price per Unit

of Capacity

Current Period Price per Unit of Capacity

X

Units of Capacity

Required to Produce Current Period’s Output

in the Prior Period

CostEffect

OfPrice-

Recovery for Fixed

Costs

=

Example: Cost Effect of Price Recovery

Strategy Reengineering Balanced Scorecard Engineered & Discretionary Cost

Managing Unused CapacityEvaluating Strategy

89

Example: Strategic

Analysis of Operating

Income

Basic Data for

Producti-vity

90

Example: Cost Effect of Productivity for Variable Costs

Units of Input Required to

Produce Current Period’s Output

in Prior Period

Actual Units of Input used to Produce Current Period Output

X Input Price in Current Period

CostEffect

OfProductivity for Variable

Costs

=

Cost effect of productivity of direct materials

= (2,900,000 sq.cm. - 3,450,000 sq.cm.) X $1.50 per sq.cm.

= 550,000 sq.cm. x $1.50 per sq.cm. = $825,000 F

Strategy Reengineering Balanced Scorecard Engineered & Discretionary Cost

Managing Unused CapacityEvaluating Strategy

Efficiency:How good is your

production process?

91

Example: Cost Effect of Productivity for Fixed Costs With Adequate Capacity

Actual Units of Capacity in Prior

Period to Produce Current Period’s Output

Actual Units of Capacity in Current Period

XPrice Per Unit of

Capacity in Current Period

CostEffect

OfProductivity

for Fixed Costs

=

Conversion costs: (3,500,000 sq.cm. - 3,750,000sq.cm.) X $4.35 per sq.

cm. = $1,087,500 F

Strategy Reengineering Balanced Scorecard Engineered & Discretionary Cost

Managing Unused CapacityEvaluating Strategy

Efficiency:How efficient is your

capacity?

92

Example: Cost Effect of Productivity for Fixed Costs

Without Adequate Capacity

Units of Capacity Required to

Produce Current Period’s Output in

the Prior Period

Actual Units of Capacity in Current Period

XPrice Per Unit of

Capacity in Current Period

CostEffect

OfProductivity

for Fixed Costs

=

Strategy Reengineering Balanced Scorecard Engineered & Discretionary Cost

Managing Unused CapacityEvaluating Strategy

93

Strategic Analysis of Operating Income

Cost leadership Product differentiation

Growth √ √ Price √ Productivity √

Strategy Reengineering Balanced Scorecard Engineered & Discretionary Cost

Managing Unused CapacityEvaluating Strategy

94

Example: Strategic Analysis of Profitability - Chipset

Strategy Reengineering Balanced Scorecard Engineered & Discretionary Cost

Managing Unused CapacityEvaluating Strategy

Strategy Reengineering Balanced Scorecard Engineered & Discretionary Cost

Managing Unused CapacityEvaluating Strategy

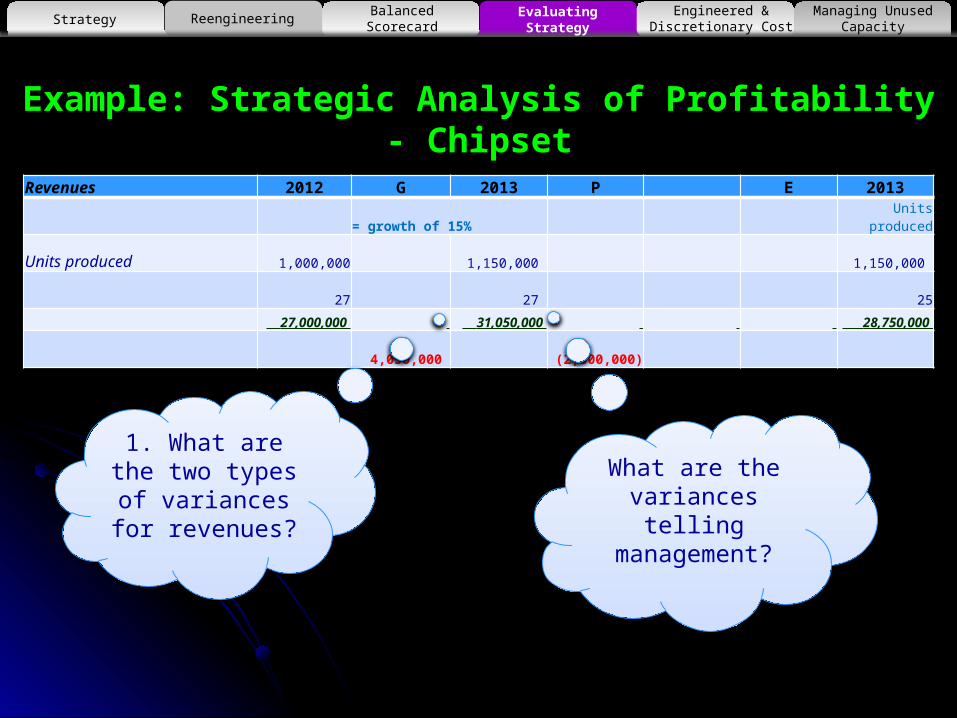

Example: Strategic Analysis of Profitability - Chipset

Revenues 2012 G 2013 P E 2013= growth of 15% Units produced

Units produced 1,000,000 1,150,000 1,150,000 27 27 25

27,000,000 31,050,000 28,750,000 4,050,000 (2,300,000)

1. What are the two types of variances for revenues?

What are the variances telling management?

Strategy Reengineering Balanced Scorecard Engineered & Discretionary Cost

Managing Unused CapacityEvaluating Strategy

Example: Strategic Analysis of Profitability - Chipset

Costs 2012 G 2013 P E 2013 For growth of 15% should have req 3450000 sq cm

Actual

Materials costs 3,000,000 3,450,000 3,450,000 2,900,000

1.40 1.40 1.50 1.50

4,200,000 4,830,000 5,175,000 4,350,000

630,000 345,000 (825,000)

1. What are the two types of variances for

ordinary standard costing analysis?

2. Where does the third variance come

from?

Growth Price Productivity

Strategy Reengineering Balanced Scorecard Engineered & Discretionary Cost

Managing Unused CapacityEvaluating Strategy

Example: Strategic Analysis of Profitability - ChipsetCosts 2012 G 2013 P E 2013

Actual units of capacity in prior period to produce current periods output Fixed Conversion costs 3,750,000 3,750,000 3,750,000 3,500,000

Processing capacity -

4.28 4.28

4.35

4.35 sq cm of silicon wafer 16,050,000 16,050,000 16,312,500 15,225,000

- 262,500 (1,087,500) Actual units of capacity in prior period to produce current periods output

R & D Costs 40 40 40 39 Employees 100,000 100,000 100,000 100,000

4,000,000 4,000,000 4,000,000 3,900,000 - - (100,000)

24,250,000 24,880,000 25,487,500 23,475,000 630,000 607,500 (2,012,500)

Growth Price Productivity

1. What are the two types of variances for

ordinary standard costing analysis?

2. Where does the third variance come

from?

Strategy Reengineering Balanced Scorecard Engineered & Discretionary Cost

Managing Unused CapacityEvaluating Strategy

Example: Strategic Analysis of Profitability - ChipsetRevenues 2012 G 2013 P E 2013

= growth of 15% Units producedUnits produced 1,000,000 1,150,000 1,150,000

27 27 25 27,000,000 31,050,000 28,750,000

4,050,000 (2,300,000)Costs 2012 G 2013 P E 2013

For growth of 15% should have req 3450000 sq cm

Actual

Materials costs 3,000,000 3,450,000 3,450,000 2,900,000

1.40 1.40 1.50 1.50

4,200,000 4,830,000 5,175,000 4,350,000

630,000 345,000 (825,000) Actual units of capacity in prior period to produce current periods output

Fixed Conversion costs 3,750,000 3,750,000 3,750,000 3,500,000

Processing capacity -

4.28 4.28

4.35

4.35 sq cm of silicon wafer 16,050,000 16,050,000 16,312,500 15,225,000

- 262,500 (1,087,500) Actual units of capacity in prior period to produce current periods output

R & D Costs 40 40 40 39 Employees 100,000 100,000 100,000 100,000

4,000,000 4,000,000 4,000,000 3,900,000 - - (100,000)

24,250,000 24,880,000 25,487,500 23,475,000 630,000 607,500 (2,012,500)

Revenues 2012 G 2013 P E 2013= growth of 15% Units produced

Units produced 1,000,000 1,150,000 1,150,000 27 27 25

27,000,000 31,050,000 28,750,000 4,050,000 (2,300,000)

Costs 2012 G 2013 P E 2013 For growth of 15% should have req 3450000 sq cm Actual

Materials costs 3,000,000 3,450,000 3,450,000 2,900,000

1.40 1.40 1.50 1.50

4,200,000 4,830,000 5,175,000 4,350,000

630,000 345,000 (825,000) Actual units of capacity in prior period to produce current periods output

Fixed Conversion costs 3,750,000 3,750,000 3,750,000 3,500,000

Processing capacity -

4.28 4.28

4.35

4.35 sq cm of silicon wafer 16,050,000 16,050,000 16,312,500 15,225,000

- 262,500 (1,087,500) Actual units of capacity in prior period to produce current periods output

R & D Costs 40 40 40 39 Employees 100,000 100,000 100,000 100,000

4,000,000 4,000,000 4,000,000 3,900,000 - - (100,000)

24,250,000 24,880,000 25,487,500 23,475,000 630,000 607,500 (2,012,500)

Strategy Reengineering Balanced Scorecard Engineered & Discretionary Cost

Managing Unused CapacityEvaluating Strategy

Example: Strategic Analysis of Profitability - Chipset

5Analysis of Unused Capacity

100

© Neale O'Connor 2010

Strategy Reengineering Balanced Scorecard Engineered & Discretionary Cost

Managing Unused CapacityEvaluating Strategy

101

5. Analysis of Unused Capacity Two Important Features:

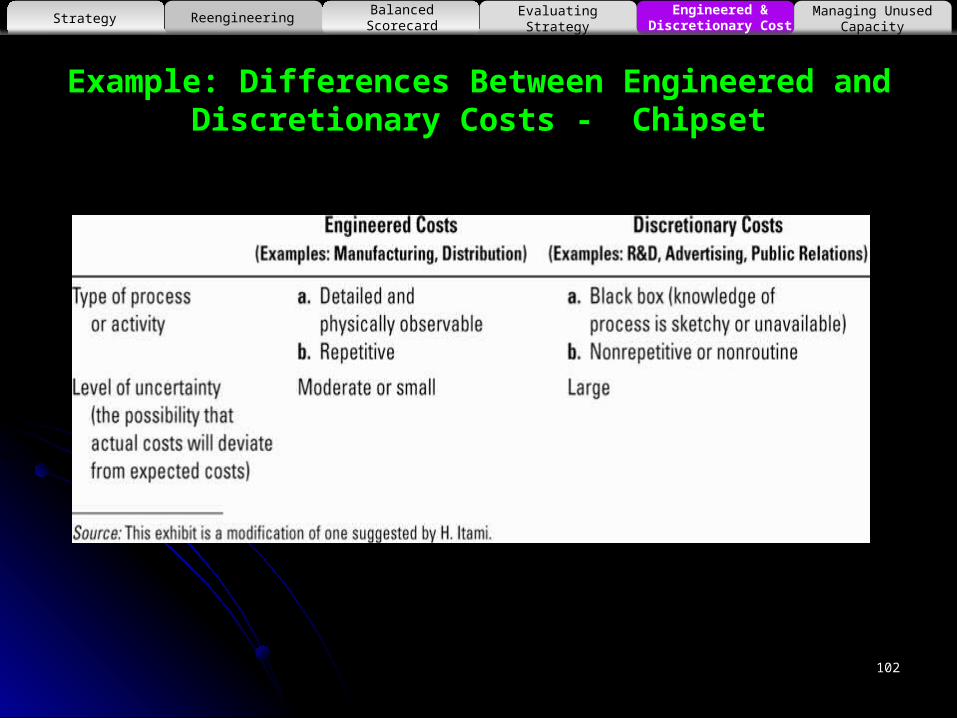

1. Engineered Costs result from a cause-and-effect relationship between the cost driver and the resources used to produce that output

2. Discretionary Costs have two parts:1. They arise from periodic (annual) decisions regarding the maximum

amount to be incurred

2. They have no measurable cause-and-effect relationship between output and resources used

Strategy Reengineering Balanced Scorecard Engineered & Discretionary Cost

Managing Unused CapacityEvaluating Strategy

Learning objective 5 :Distinguish engineered costs… a cause-and-effect relationship exists between output produced and costs incurred

from discretionary costs… no cause-and-effect relationship exists between outputProduced and costs incurred

5

102

Example: Differences Between Engineered and Discretionary Costs - Chipset

Strategy Reengineering Balanced Scorecard Engineered & Discretionary Cost

Managing Unused CapacityEvaluating Strategy

6Managing Unused Capacity

103

© Neale O'Connor 2010

Strategy Reengineering Balanced Scorecard Engineered & Discretionary Cost

Managing Unused CapacityEvaluating Strategy

104

Managing Unused Capacity

Managers can reduce capacity-based fixed costs by measuring and managing unused capacity

Unused Capacity is the amount of productive capacity available over and above the productive capacity employed to meet consumer demand in the current period

Strategy Reengineering Balanced Scorecard Engineered & Discretionary Cost

Managing Unused CapacityEvaluating Strategy

Learning objective 6 :Identify unused capacity… capacity available minus capacity used

and how to manage it…downsize to reduce capacity

6

105

Example: Differences Between Engineered and Discretionary Costs - Chipset

Strategy Reengineering Balanced Scorecard Engineered & Discretionary Cost

Managing Unused CapacityEvaluating Strategy

106

Managing Unused Capacity

Downsizing (Rightsizing) is an integrated approach of configuring

processes, products, and people to match costs to the activities that

need to be performed to operate effectively and efficiently in the present

and future

Strategy Reengineering Balanced Scorecard Engineered & Discretionary Cost

Managing Unused CapacityEvaluating Strategy

107

Summary

Strategy Learning objective 1: Recognize which of two generic strategies a company is using

Reengineering Learning objective 2: Understand what comprises reengineering

Balanced Scorecard Learning objective 3: Understand the four perspectives of the balanced scorecard

Evaluating Strategy Learning objective 4: Analyze changes in operating income to evaluate strategy

Engineered & Discretionary Cost Learning objective 5: Distinguish engineered costs from discretionary costs

Managing Unused Capacity Learning objective 6: Identify unused capacity and how to manage it

Strategy Reengineering Balanced Scorecard Engineered & Discretionary Cost

Managing Unused CapacityEvaluating Strategy

APPENDIX

108

109109

In Practice: Framework for thinking and deciding on strategyStrategic objectives

What is the basis for success?

What is the Sustainable Competitive Advantage (SCA)?

Why? - Direction of effort

How?

Learn how to beat competitors and provide value to customer

Develop consensus as to the priorities and initiatives to undertake in the short term

(next 12 months)

Strategy Reengineering Balanced Scorecard Engineered & Discretionary Cost

Managing Unused CapacityEvaluating Strategy

HOW?

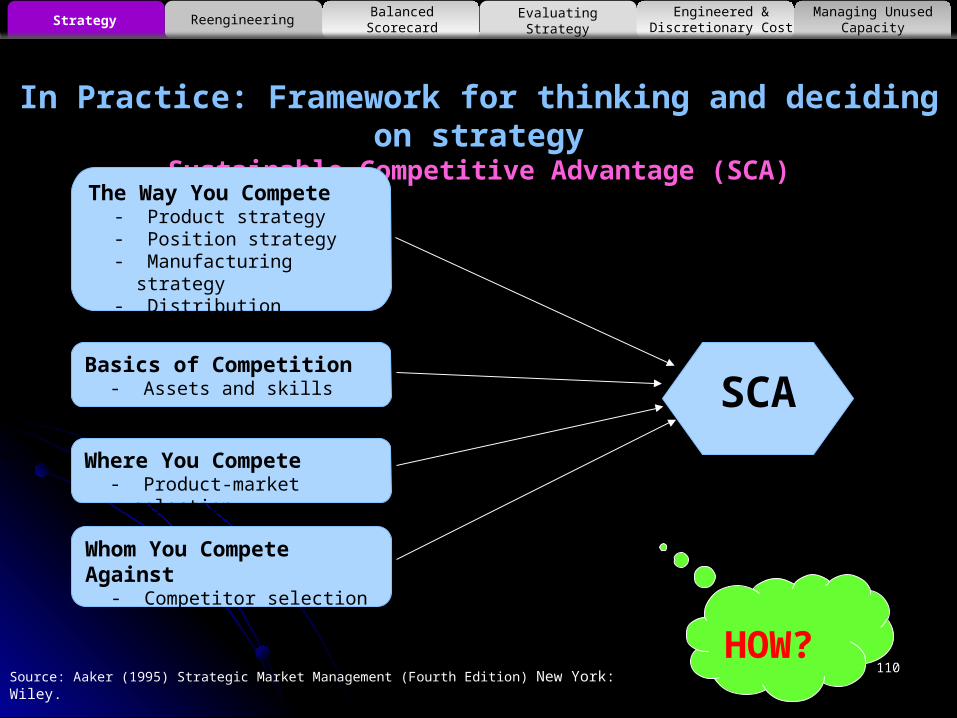

In Practice: Framework for thinking and deciding on strategySustainable Competitive Advantage (SCA)

Source: Aaker (1995) Strategic Market Management (Fourth Edition) New York: Wiley. 110

Strategy Reengineering Balanced Scorecard Engineered & Discretionary Cost

Managing Unused CapacityEvaluating Strategy

SCA

The Way You Compete- Product strategy- Position strategy- Manufacturing strategy- Distribution strategy, etc.

Basics of Competition- Assets and skills

Where You Compete- Product-market selection

Whom You Compete Against- Competitor selection

HOW?

111

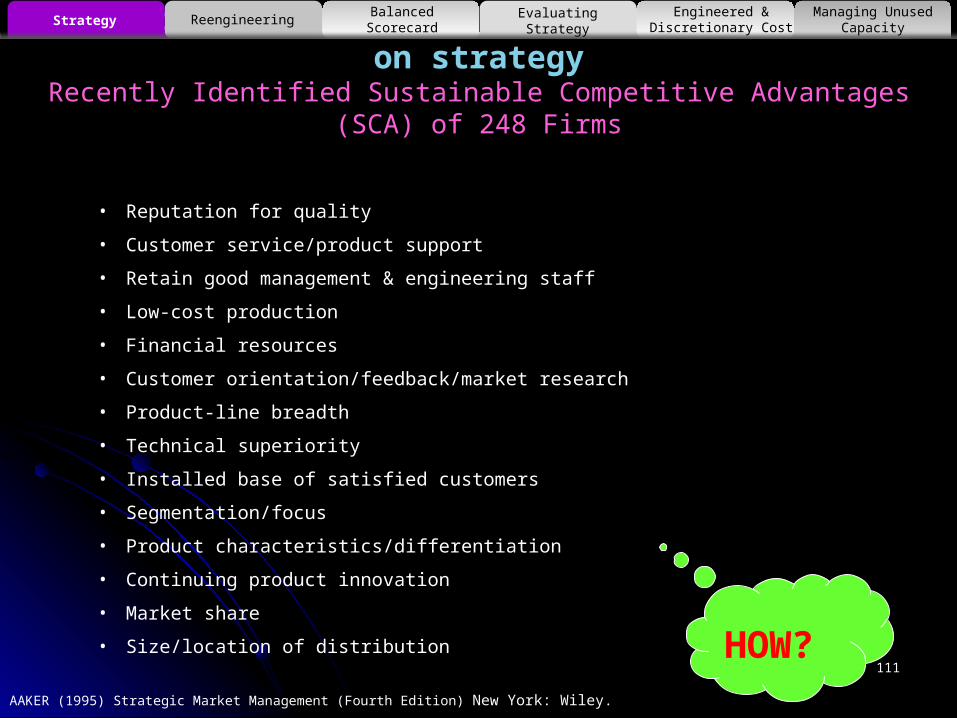

In Practice: Framework for thinking and deciding on strategyRecently Identified Sustainable Competitive Advantages (SCA) of 248 Firms

AAKER (1995) Strategic Market Management (Fourth Edition) New York: Wiley.

• Reputation for quality

• Customer service/product support

• Retain good management & engineering staff

• Low-cost production

• Financial resources

• Customer orientation/feedback/market research

• Product-line breadth

• Technical superiority

• Installed base of satisfied customers

• Segmentation/focus

• Product characteristics/differentiation

• Continuing product innovation

• Market share

• Size/location of distribution

Strategy Reengineering Balanced Scorecard Engineered & Discretionary Cost

Managing Unused CapacityEvaluating Strategy

HOW?

In Practice: Framework for thinking and deciding on strategyYour Sustainable Competitive Advantage

Ability to beat competitors

10 High5Low 0

5

High 10

Valu

e to

Cus

tom

er

Top Five Issues12345

© Neale O’Connor 2005

T

112

Strategy Reengineering Balanced Scorecard Engineered & Discretionary Cost

Managing Unused CapacityEvaluating Strategy

HOW?

© Neale O'Connor 2010

What is the BSC Strategic Objectives Simulation GameSystems Thinking

115

Case Example #2

Xinan JVBalanced Scorecard

SystemAppendix A

Xinan JV - Two Challenges

1. Product development Pharmaceutical Market reform by the Chinese

government, through the State Drug Product Council.

2. Sales manager development Sales force had an “old Chinese way of thinking” (short

term) mindset.

© Neale O'Connor 2010

Case Study

116

Xinan JV - Product development

1. Reduced drug prices Reforms in the Chinese pharmaceutical market, such as the

reduction of drug prices of between 30% to 50% across the board,

2. Increased competition Introduction of tendering in hospitals, which increased the

competition for the supply of drugs. For example, local generic product manufacturers were bidding between 30% and 50% below Xinan JV’s price.

3. Speed up the development of new products This served as a wake-up call for Xinan JV, which had an aging

portfolio of products that were largely protected from competition, and the challenge for the company was to speed up the development of new products.

© Neale O'Connor 2010

Case Study

117

Xinan JV - Sales manager development1. “old Chinese way of thinking” mindset

Fail to develop customer relationships Lack of motivation to develp product knowledge

Faced with these two challenges, Xinan JV set up an action plan that focused on the development and management of its intangible assets. This included the development of new products and the restructuring and development of the skills of its sales managers.

© Neale O'Connor 2010

Case Study

118

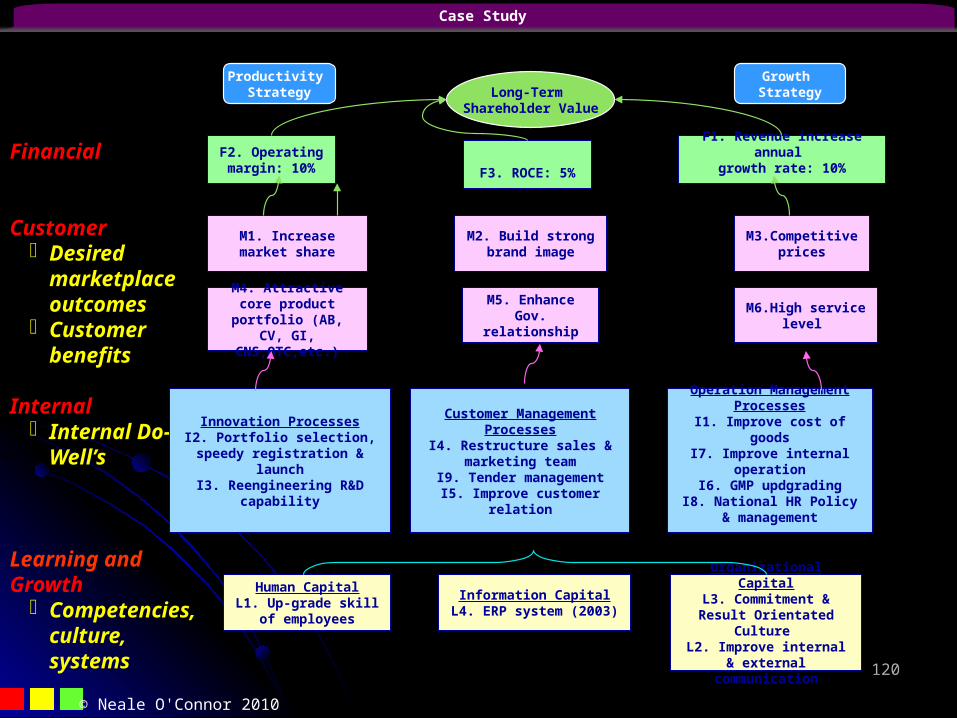

Xinan JV - Balanced Scorecard Implementation (2002)

Objective Strategy - Making medicine accessible – To be a

leader in China branded generic business in 5 years time.

Improve communication and control over strategy and the associated objectives and initiatives

© Neale O'Connor 2010

Case Study

119

Information CapitalL4. ERP system (2003)

Financial

Customer– Desired

marketplace outcomes

– Customer benefits

Internal – Internal Do-

Well’s

Learning and Growth

– Competencies, culture, systems

M2. Build strong brand image

M1. Increase market share

M4. Attractive core product

portfolio (AB, CV, GI, CNS,OTC,etc.)

M5. Enhance Gov.

relationshipM6.High service

level

Operation Management Processes

I1. Improve cost of goods

I7. Improve internal operation

I6. GMP updgradingI8. National HR Policy &

management

Human CapitalL1. Up-grade skill

of employees

M3.Competitive prices

Organizational CapitalL3. Commitment & Result Orientated

Culture L2. Improve internal &

external communication

F3. ROCE: 5%

Customer Management Processes

I4. Restructure sales & marketing team

I9. Tender managementI5. Improve customer

relation

Innovation ProcessesI2. Portfolio selection, speedy registration &

launchI3. Reengineering R&D

capability

F2. Operating margin: 10%

F1. Revenue increase annual

growth rate: 10%

Long-Term Shareholder Value

Productivity Strategy

Growth Strategy

© Neale O'Connor 2010

Case Study

120

Problems in implementing the balanced scorecard

1. Training and participation2. Frequent reviews3. Contingency plans were difficult to show

© Neale O'Connor 2010

Case Study

121

© Neale O'Connor 2010

What is the BSC Strategic Objectives Simulation GameSystems Thinking

122

Case Example #1

CTI Ltd’sIncentive System

Appendix A

Critical factors in CTI’s strategyCTI

Two factors were critical to CTI’s profit growth strategy:Reliance on sales of higher margin products

Cash collection.

Incentive plan change With increasing introduction of new products and growth in sales

– these two factors drove CTI to change the incentive plan to direct management effort towards these objectives.

© Neale O'Connor 2010

Case Study

123

Setting of this study Quotes on the incentive plan

“We want people to be able to see everything. They

should not just be able to make sales, but should be able to motivate people, organize things strategically, putting down their thoughts into paper, think logically, and express themselves in a coherent fashion.”

© Neale O'Connor 2010

Case Study

124

Components of General multiple measure formula

© Neale O'Connor 2010

Bonus compensation formula = (Employees + 1) * (General formula) + (Direct sales formula)

Direct sales formula = Products - 50 cents per old product sold,

1.00 per new product sold.General formula = 5000 + (Points – 60) * 100

Points awarded according to

Objective assessment formula

and Objective (Financial) Measures

(45 points)

Points awarded according to Subjective

assessment and Objective (Non-

Financial) Measures(30 points)

Points awarded according to Subjective assessment and

Subjective measures(25- 35 points)

Sales components-Cash collection (40)a

-Relative branch office costs (5)a

Service level components-Execution of routine maintenance (5)b

-Major incident complaint (10)b

-Customer satisfaction survey (15)b

Management capability components-Regional office daily management (15)-Evaluation by VP – Teamwork, cooperativeness (10)-Evaluation by President and VP sales – proactive, innovative e.g., Making suggestions doing things beyond responsibility and solving difficult problems - Bonus points (10)

Case Study

125

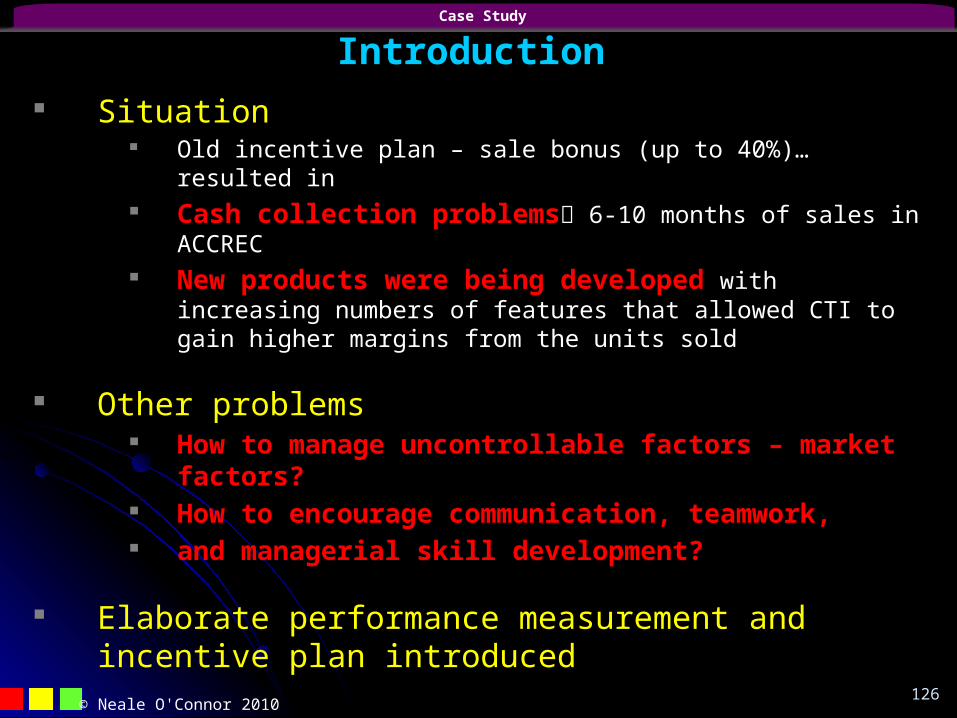

Introduction Situation

Old incentive plan – sale bonus (up to 40%)… resulted in Cash collection problems 6-10 months of sales in ACCREC New products were being developed with increasing numbers of

features that allowed CTI to gain higher margins from the units sold

Other problems How to manage uncontrollable factors – market factors? How to encourage communication, teamwork, and managerial skill development?

Elaborate performance measurement and incentive plan introduced

Case Study

© Neale O'Connor 2010 126