Embed Size (px)

Citation preview

OVERVIEW OF THE USE OF

ENVIRONMENTALLY-RELATED

PRODUCT TAXES IN OECD

COUNTRIESNils Axel Braathen,

Principal Administrator, Environment Directorate

Revenues from environmentally related taxes In per cent of GDP, Selected countries, 2012

2

-2

-1

0

1

2

3

4

5

% o

f GD

P

Other

Motor vehicles

Energy

* 2011 figures ** 2010 figure

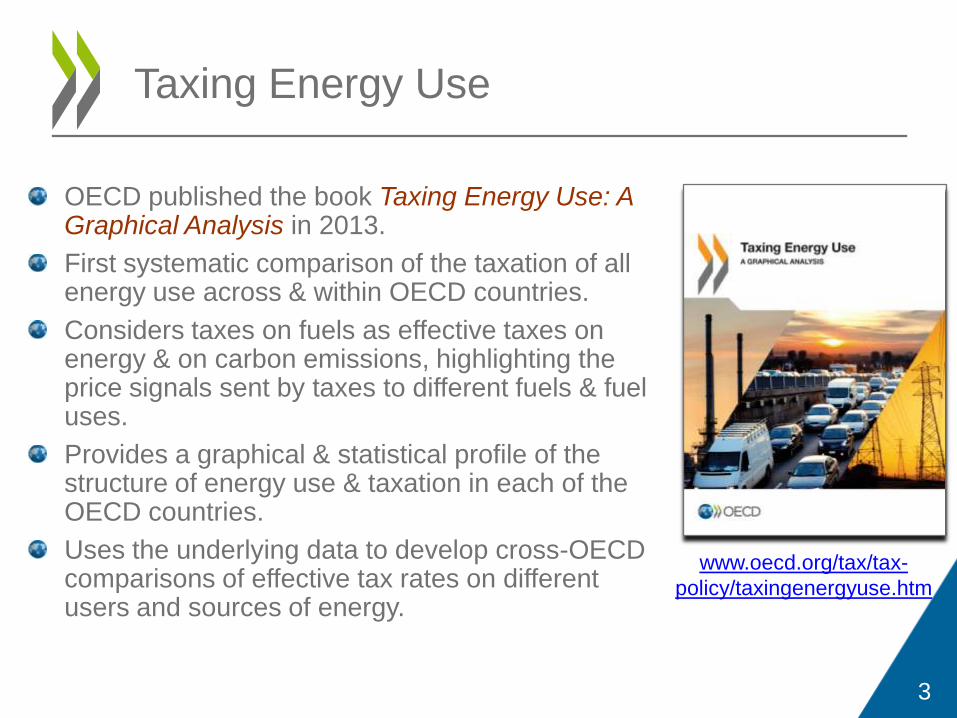

OECD published the book Taxing Energy Use: A Graphical Analysis in 2013.

First systematic comparison of the taxation of all energy use across & within OECD countries.

Considers taxes on fuels as effective taxes on energy & on carbon emissions, highlighting the price signals sent by taxes to different fuels & fuel uses.

Provides a graphical & statistical profile of the structure of energy use & taxation in each of the OECD countries.

Uses the underlying data to develop cross-OECD comparisons of effective tax rates on different users and sources of energy.

3

Taxing Energy Use

www.oecd.org/tax/tax-

policy/taxingenergyuse.htm

4

Taxation of energy in the OECD area:On a carbon content basis

Source: OECD (2013), Taxing Energy Use: A Graphical Analysis.

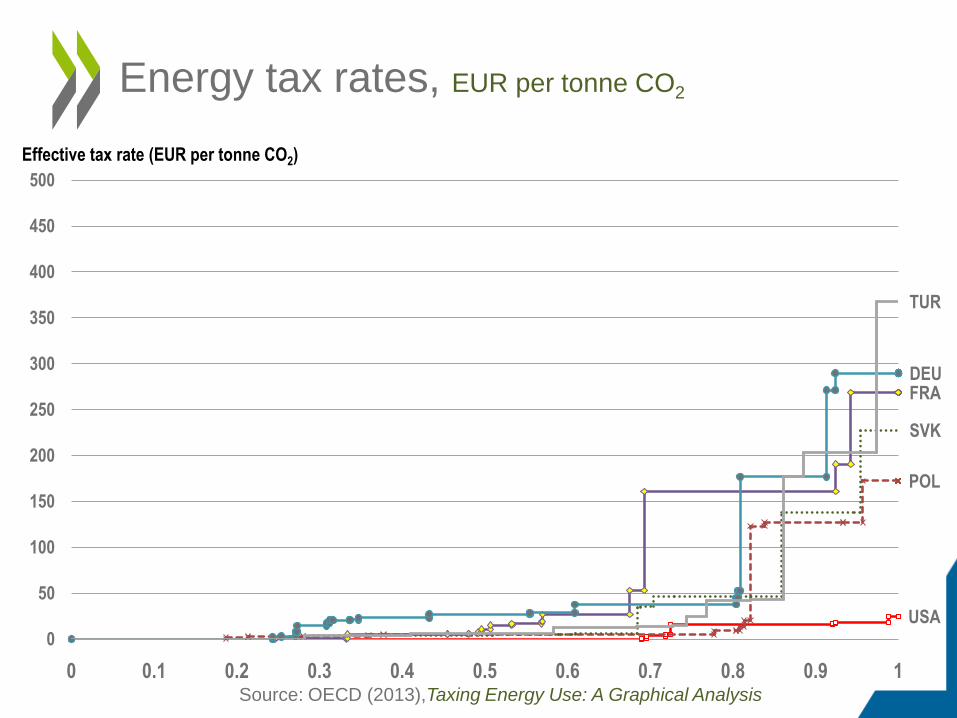

Energy tax rates, EUR per tonne CO2

5

USA

POL

SVK

FRADEU

TUR

0

50

100

150

200

250

300

350

400

450

500

0 0.1 0.2 0.3 0.4 0.5 0.6 0.7 0.8 0.9 1

Effective tax rate (EUR per tonne CO2)

Source: OECD (2013),Taxing Energy Use: A Graphical Analysis

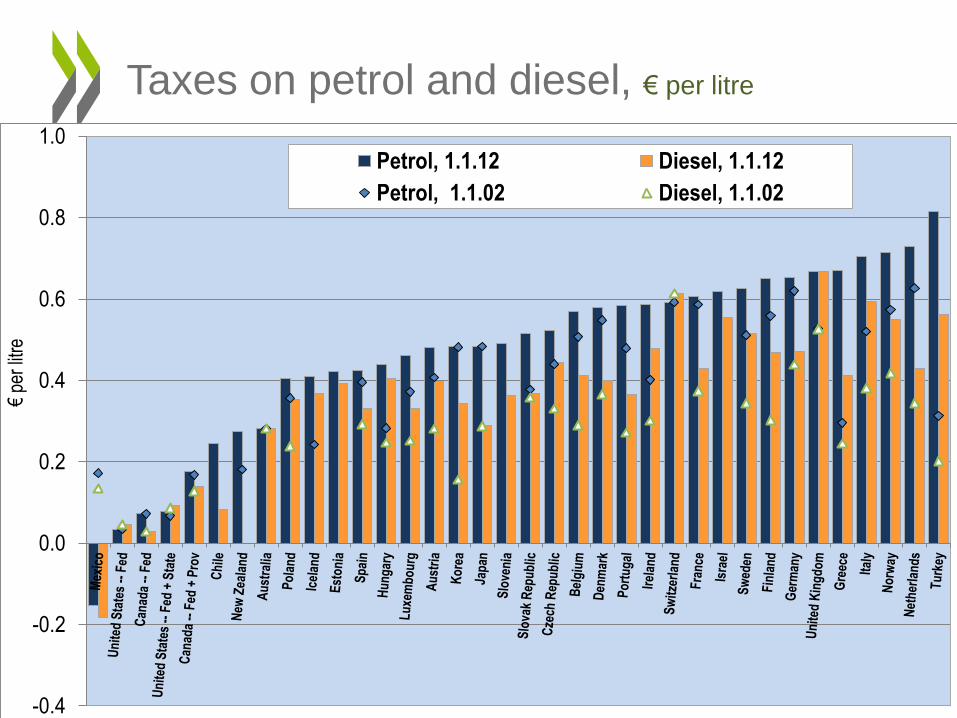

Taxes on petrol and diesel, € per litre

6

-0.4

-0.2

0.0

0.2

0.4

0.6

0.8

1.0

€pe

r lit

re

Petrol, 1.1.12 Diesel, 1.1.12

Petrol, 1.1.02 Diesel, 1.1.02

Taxes on motor vehicles

One-off taxes, linked to the first registration of a motor vehicle;

Recurrent (annual) taxes on the ownership of motor vehicles.

Both types can be differentiated according to various (environmental) criteria:– Expected CO2 emissions;

– Expected emissions of NOx or other pollutants;

– Petrol vs. diesel motor;

– Engine capacity in kW;

– Engine size, in cm³;

– Vehicle weight, etc.

Also fuel taxes and other vehicle-related taxes and charges (e.g. road-use charges) will influence vehicle choices.

7

One-off taxes on motor vehicles

8

0

20

40

60

80

100

120

140

160

EUR

(000

s)

Small Vehicle Medium Vehicle Large Vehicle

Small: 53 kW;

Medium: 132 kW;

Large: 300 kW

All petrol-driven

In addition, Greece has introduced

major motor vehicle taxes.

Tax rates as of 01.01.10

CO2-related motor vehicle taxes

Can be linked directly to expected CO2 emissions, or to the

expected fuel efficiency of the vehicle.

Since a litre of petrol and diesel causes emissions of a fixed

amount of CO2 (2.343 and 2.682 kg respectively), the CO2

emissions are given once the fuel efficiency is known.

Variations between petrol- and diesel-vehicles; depending on

the price of the vehicle; according to vehicle ownership, etc.

Can be part of a bonus–malus system, with subsidies for low-

emission vehicles.

At least 19 OECD countries (+ South Africa) apply some form

of CO2-related differentiation of their motor vehicle taxes.

17 countries apply CO2-related one-off taxes.

9 countries apply CO2-related recurrent taxes. 9

10

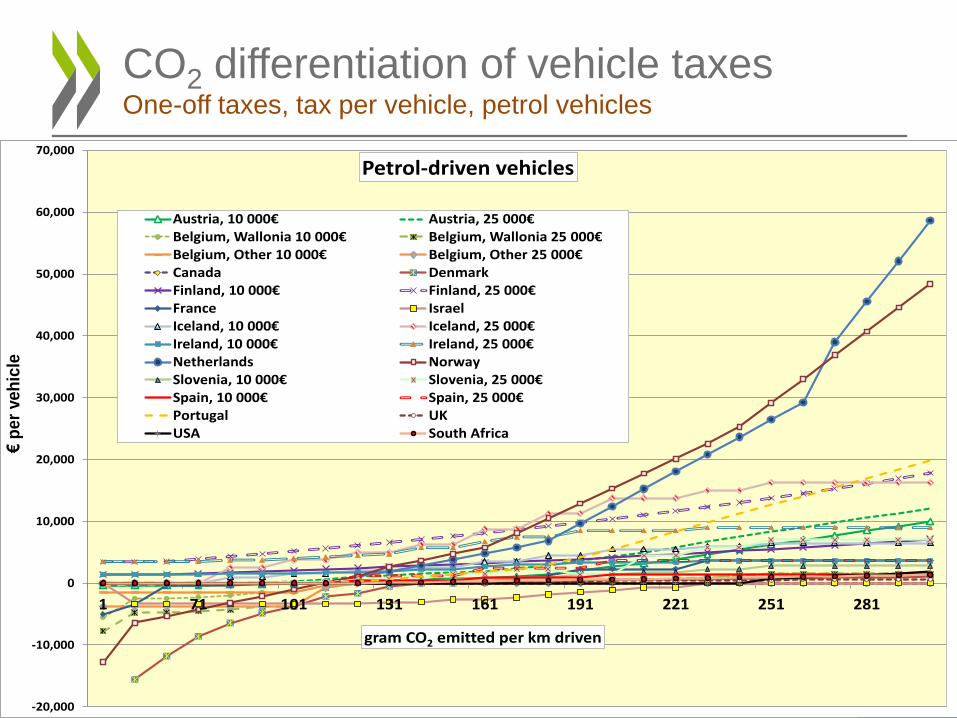

CO2 differentiation of vehicle taxesOne-off taxes, tax per vehicle, petrol vehicles

-20,000

-10,000

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

1 71 101 131 161 191 221 251 281

€p

er

veh

icle

gram CO2 emitted per km driven

Petrol-driven vehicles

Austria, 10 000€ Austria, 25 000€Belgium, Wallonia 10 000€ Belgium, Wallonia 25 000€Belgium, Other 10 000€ Belgium, Other 25 000€Canada DenmarkFinland, 10 000€ Finland, 25 000€France IsraelIceland, 10 000€ Iceland, 25 000€Ireland, 10 000€ Ireland, 25 000€Netherlands NorwaySlovenia, 10 000€ Slovenia, 25 000€Spain, 10 000€ Spain, 25 000€Portugal UKUSA South Africa

11

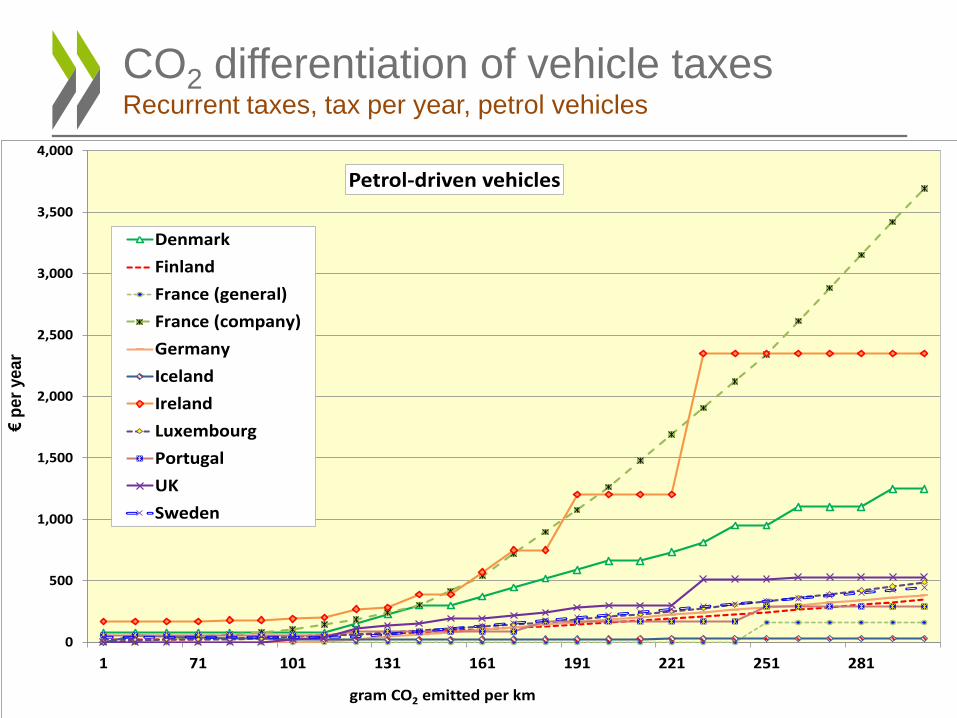

CO2 differentiation of vehicle taxesRecurrent taxes, tax per year, petrol vehicles

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

1 71 101 131 161 191 221 251 281

€p

er

ye

ar

gram CO2 emitted per km

Petrol-driven vehicles

Denmark

Finland

France (general)

France (company)

Germany

Iceland

Ireland

Luxembourg

Portugal

UK

Sweden

Taxes per tonne CO2 emitted over the

vehicles’ lifetime

Once tax rates per vehicle or per year are known, if one

makes a few assumptions, one can calculate the tax rates

per tonne of CO2 that the vehicle will emit over its lifetime.

Assumes that

– Each vehicle is driven 200 000km over its lifespan;

– For recurrent taxes, the lifespan of each vehicle is 15 years;

– Need also to decide on which discount rate to use (if any).

12

13

CO2 differentiation of vehicle taxesTotal taxes per tonne lifetime CO2 emissions, diesel vehicles

-600

-400

-200

0

200

400

600

800

1,000

€pe

r to

nne

CO2

emit

ted

over

the

veh

icle

life

tim

e 100 gram CO2 per km

-600

-400

-200

0

200

400

600

800

1,000

€pe

r to

nne

CO2

emit

ted

over

the

veh

icle

life

tim

e 150 gram CO2 per km

-600

-400

-200

0

200

400

600

800

1,000

€pe

r to

nne

CO2

emit

ted

over

the

veh

icle

life

tim

e 200 gram CO2 per km

-600

-400

-200

0

200

400

600

800

1,000

€pe

r to

nne

CO2

emit

ted

over

the

veh

icle

life

tim

e 250 gram CO2 per km

One-off Recurrent

CO2-related vehicle taxes – Some comments I

Some countries apply tax rates per tonne of CO2emitted that

are very high, especially for high-emission vehicles.

Keep in mind that each tonne emitted will do the same

damage, regardless of whether it is emitted from a vehicle

that causes large or small CO2 emissions per km driven.

The emission reduction incentives that are provided in the

vehicle sector are in some case out of proportion to the

incentives given to other sectors of the economy.

The taxes have contributed to a major reduction in vehicles’

average CO2 emissions – but the shift in demand contributes

to reduce the amount of revenues raised.

14

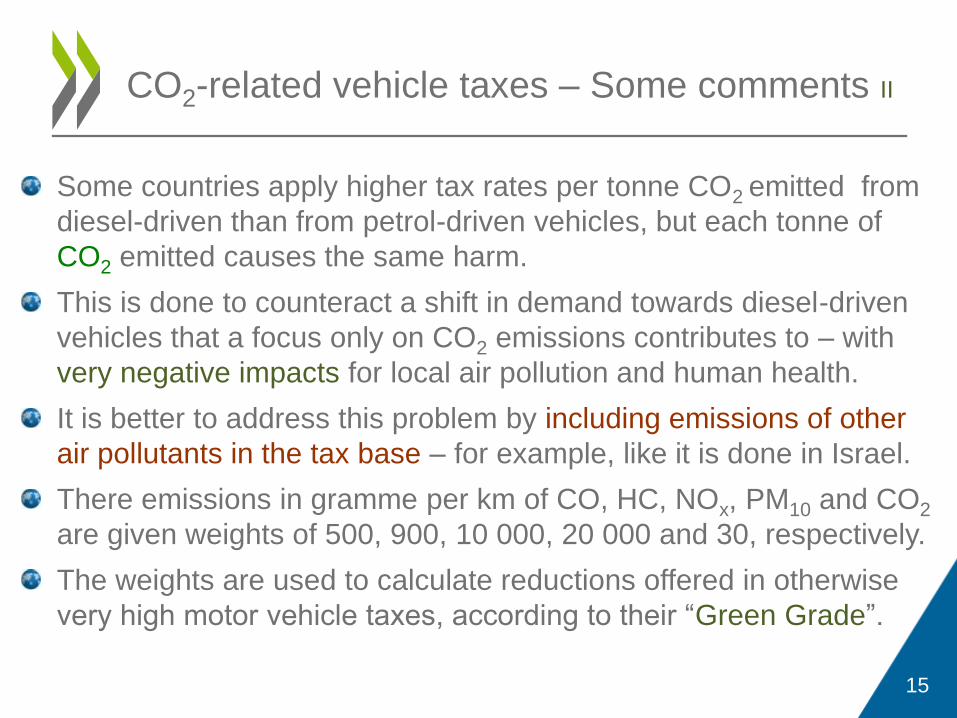

Some countries apply higher tax rates per tonne CO2 emitted from

diesel-driven than from petrol-driven vehicles, but each tonne of

CO2 emitted causes the same harm.

This is done to counteract a shift in demand towards diesel-driven

vehicles that a focus only on CO2 emissions contributes to – with

very negative impacts for local air pollution and human health.

It is better to address this problem by including emissions of other

air pollutants in the tax base – for example, like it is done in Israel.

There emissions in gramme per km of CO, HC, NOx, PM10 and CO2

are given weights of 500, 900, 10 000, 20 000 and 30, respectively.

The weights are used to calculate reductions offered in otherwise

very high motor vehicle taxes, according to their “Green Grade”.

15

CO2-related vehicle taxes – Some comments II

16

Taxes on lubricating oils

0.0

0.1

0.2

0.3

0.4

0.5

0.6

Australia Norway UnitedStates --Alabama

UnitedStates --Florida

Finland France Poland SlovakRepublic

Slovenia

EUR

per

litr

e or

per

kg

Per litre Per kg

17

0

5

10

15

20

25

30

35

Denmark UnitedStates --

SouthCarolina

Iceland Poland Portugal SlovakRepublic

Sweden Switzerland

EUR

per

cel

l/ba

tter

y or

per

kg

Per cell / battery Per kg

Taxes on nickel-cadmium batteries

18

Taxes on vehicle batteries

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

EUR

per

bat

tery

or

per

kg

Per battery Per kg

19

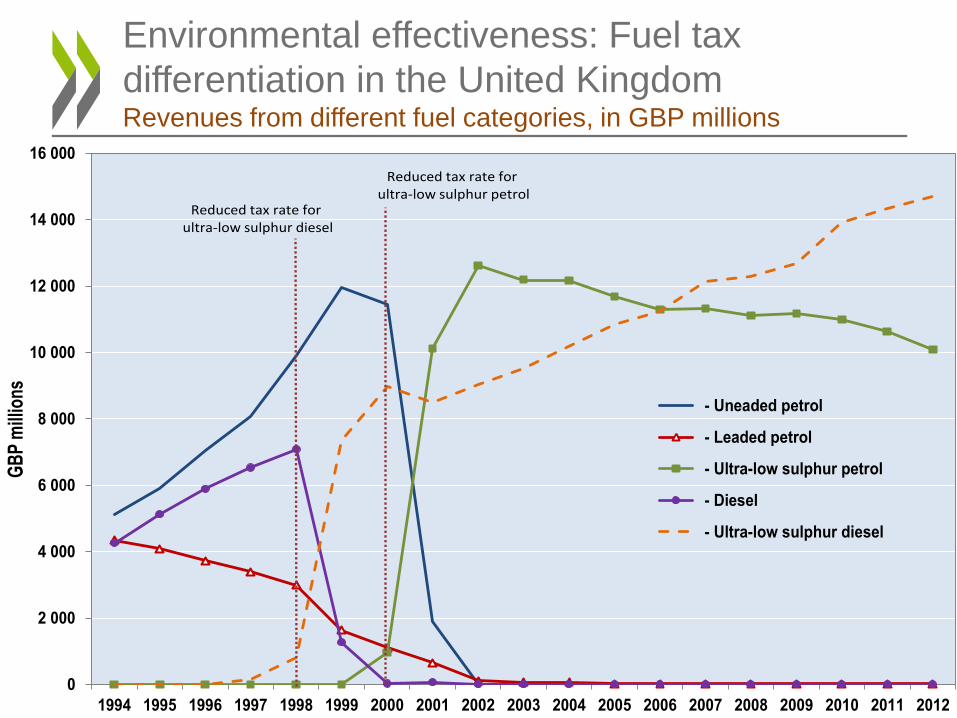

Environmental effectiveness: Fuel tax

differentiation in the United KingdomRevenues from different fuel categories, in GBP millions

0

2 000

4 000

6 000

8 000

10 000

12 000

14 000

16 000

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

GB

P m

illio

ns

- Uneaded petrol

- Leaded petrol

- Ultra-low sulphur petrol

- Diesel

- Ultra-low sulphur diesel

Reduced tax rate for ultra-low sulphur petrol

Reduced tax rate for ultra-low sulphur diesel

20

Environmental effectiveness: Fuel taxes and

fuel use in the transport sector per GDP unit

0.0

0.2

0.4

0.6

0.8

1.0

0

10

20

30

40

50

60

70

80

90

94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10

United States

0.0

0.2

0.4

0.6

0.8

1.0

0

10

20

30

40

50

60

70

80

90

94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10

Turkey

0.0

0.2

0.4

0.6

0.8

1.0

0

10

20

30

40

50

60

70

80

90

94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10

France

0.0

0.2

0.4

0.6

0.8

1.0

0

10

20

30

40

50

60

70

80

90

94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10

Germany

Further information

www.oecd.org/env/policies/database

www.oecd.org/env/taxes

www.oecd.org/env/tools-evaluation/carbon-prices.htm

www.oecd.org/env/taxingenergyuse.htm

21