Embed Size (px)

Citation preview

Unveiling the Potential of

Market Based Mechanism

Implementation in

Indonesia

Thailand and Chile case studies

Dicky Edwin Hindarto

Indonesia JCM Secretariat

What happened in COP 21?

Parties of the UNFCCC pledged to curb its carbonemission, strengthen resilience and joined to takecommon climate action .

Paris Deal includes a temperature limit of “well below 2C” and says there should be “efforts” to limit it to 1.5 C.To do so requires 32 GtCO2e emission to be cut in 2050,and around US$ 40 trillion additional investment totransition to a global low-carbon economy.

To achieve long-term temperature goal or in anotherword reaching net zero-emission after 2050.

Legal obligation on developed countries to continue toprovide climate finance to developing countries.

On mitigation, binds parties to prepare and regularlyupdate climate commitments and developing countriesare encouraged to move towards stricter goals.

The most important paragraphs…

PARIS AGREEMENT (article 2 para 1-2)1.This Agreement, in enhancing the implementation of the

Convention, including its objective, aims to strengthen the globalresponse to threat of climate change, in the context of sustainabledevelopment and efforts to eradicate poverty, including by:

1.Holding the increase in the global average temperature to well below 2O Celciusabove pre industrial levels and to pursue efforts to limit the temperatureincrease to 1.5O Celcius above pre industrial levels, recognizing that this wouldsignificantly reduce the risks and impacts of climate change;

2. Increasing the ability to adapt to the adverse impacts of climate change and fosterclimate resilience and low greenhouse gas emission development, in a mannerthat does not threaten food productions;

3.Making finance flows consistent with a pathway towards low greenhouse gasemissions and climate resilient development.

2.This Agreement will be implemented to reflect equity and theprinciple of common but differentiated responsibilities andrespective capabilities, in the light of different nationalcircumstances.

MBM in Paris Agreement: article 61. Parties recognize that some Parties choose to pursue voluntary cooperation in the

implementation of their nationally determined contributions to allow for higher ambition in their mitigation and adaptation actions and to promote sustainable development and environmental integrity.

2. Parties shall, where engaging on a voluntary basis in cooperative approaches that involve the use of internationally transferred mitigation outcomes towards nationally determined contributions, promote sustainable development and ensure environmental integrity and transparency, including in governance, and shall apply robust accounting to ensure, inter alia, the avoidance of double counting, consistent with guidance adopted by the Conference of the Parties serving as the meeting of the Parties to the Paris Agreement.

3. The use of internationally transferred mitigation outcomes to achieve nationally determined contributions under this Agreement shall be voluntary and authorized by participating Parties.

4. A mechanism to contribute to the mitigation of greenhouse gas emissions and support sustainable development is hereby established under the authority and guidance of the Conference of the Parties serving as the meeting of the Parties to the Paris Agreement for use by Parties on a voluntary basis. It shall be supervised by a body designated by the Conference of the Parties serving as the meeting of the Parties to the Paris Agreement, and shall aim:

1. To promote the mitigation of greenhouse gas emissions while fostering sustainable development;

2. To incentivize and facilitate participation in the mitigation of greenhouse gas emissions by public and private entities authorized by a Party;

3. To contribute to the reduction of emission levels in the host Party, which will benefit from mitigation activities resulting in emission reductions that can also be used by another Party to fulfill its nationally determined contribution; and

4. To deliver an overall mitigation in global emissions.

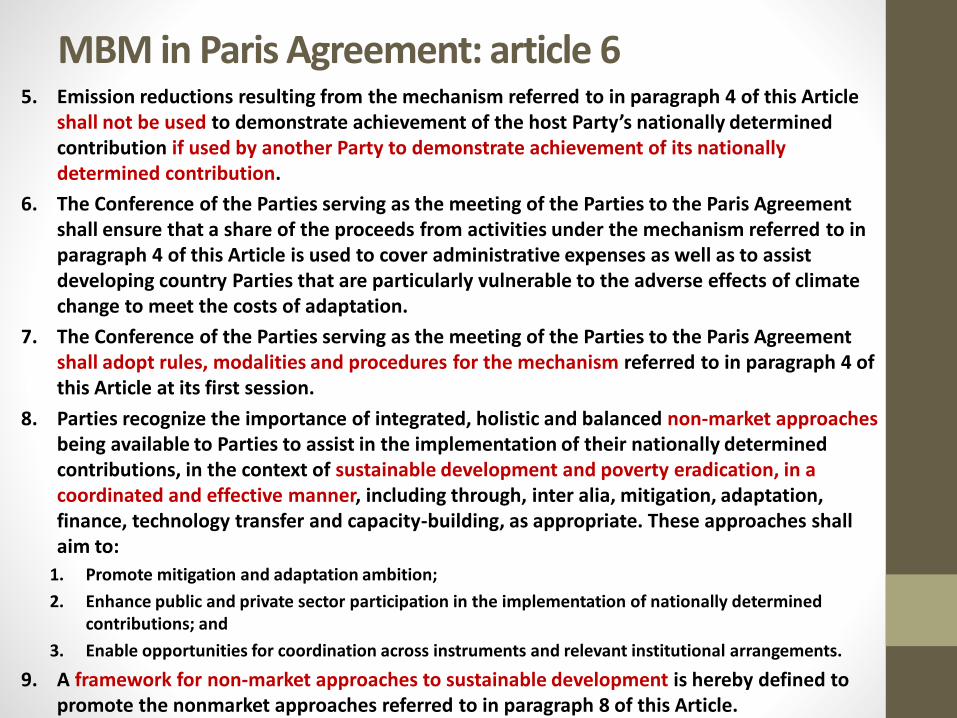

5. Emission reductions resulting from the mechanism referred to in paragraph 4 of this Article shall not be used to demonstrate achievement of the host Party’s nationally determined contribution if used by another Party to demonstrate achievement of its nationally determined contribution.

6. The Conference of the Parties serving as the meeting of the Parties to the Paris Agreement shall ensure that a share of the proceeds from activities under the mechanism referred to in paragraph 4 of this Article is used to cover administrative expenses as well as to assist developing country Parties that are particularly vulnerable to the adverse effects of climate change to meet the costs of adaptation.

7. The Conference of the Parties serving as the meeting of the Parties to the Paris Agreement shall adopt rules, modalities and procedures for the mechanism referred to in paragraph 4 of this Article at its first session.

8. Parties recognize the importance of integrated, holistic and balanced non-market approaches being available to Parties to assist in the implementation of their nationally determined contributions, in the context of sustainable development and poverty eradication, in a coordinated and effective manner, including through, inter alia, mitigation, adaptation, finance, technology transfer and capacity-building, as appropriate. These approaches shall aim to:

1. Promote mitigation and adaptation ambition;

2. Enhance public and private sector participation in the implementation of nationally determined contributions; and

3. Enable opportunities for coordination across instruments and relevant institutional arrangements.

9. A framework for non-market approaches to sustainable development is hereby defined to promote the nonmarket approaches referred to in paragraph 8 of this Article.

MBM in Paris Agreement: article 6

Some thinking of article 6 of Paris Agreement (PA)

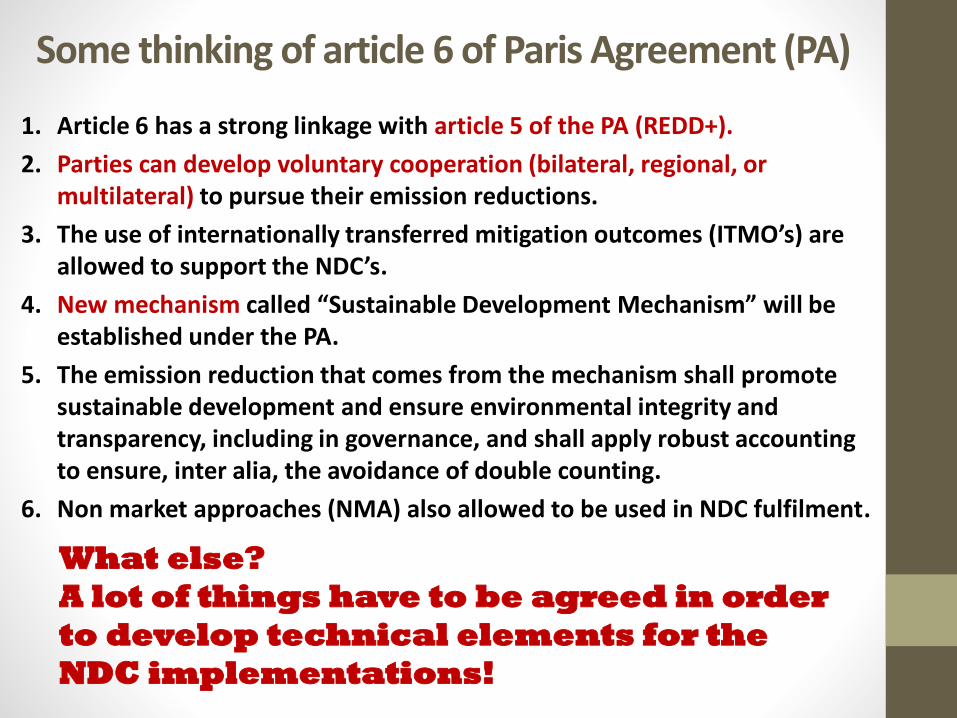

1. Article 6 has a strong linkage with article 5 of the PA (REDD+).

2. Parties can develop voluntary cooperation (bilateral, regional, or multilateral) to pursue their emission reductions.

3. The use of internationally transferred mitigation outcomes (ITMO’s) are allowed to support the NDC’s.

4. New mechanism called “Sustainable Development Mechanism” will be established under the PA.

5. The emission reduction that comes from the mechanism shall promote sustainable development and ensure environmental integrity and transparency, including in governance, and shall apply robust accounting to ensure, inter alia, the avoidance of double counting.

6. Non market approaches (NMA) also allowed to be used in NDC fulfilment.

What else?

A lot of things have to be agreed in order

to develop technical elements for the

NDC implementations!

How to finance climate change mitigation?

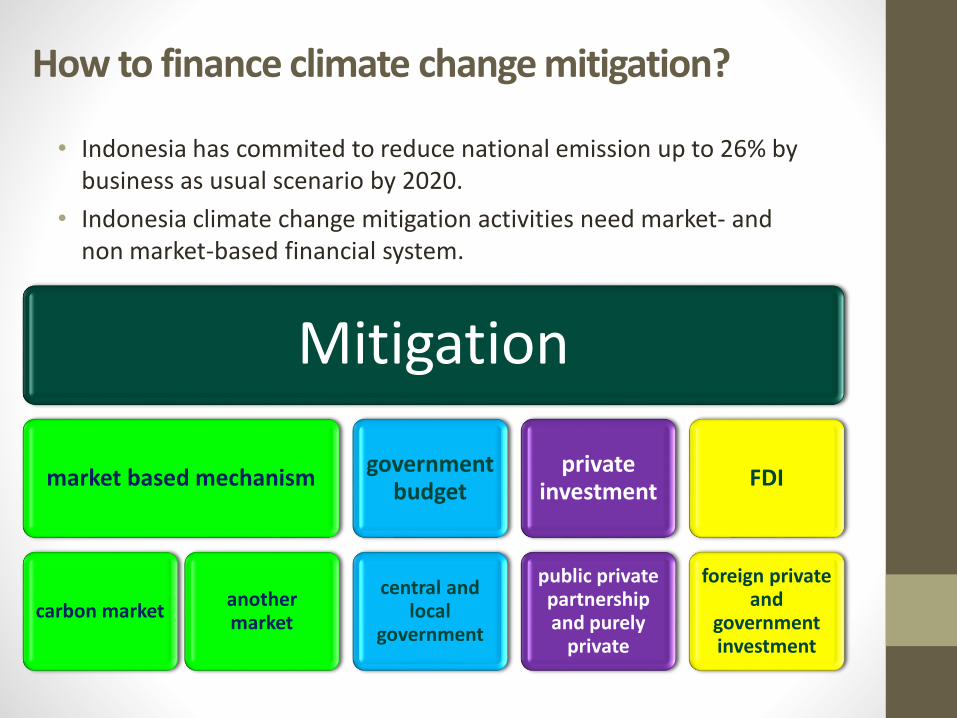

• Indonesia has commited to reduce national emission up to 26% bybusiness as usual scenario by 2020.

• Indonesia climate change mitigation activities need market- andnon market-based financial system.

Mitigation

market based mechanism

carbon market another market

government budget

central and local

government

private investment

public private partnership and purely

private

FDI

foreign private and

government investment

Why we need to put price on emission?

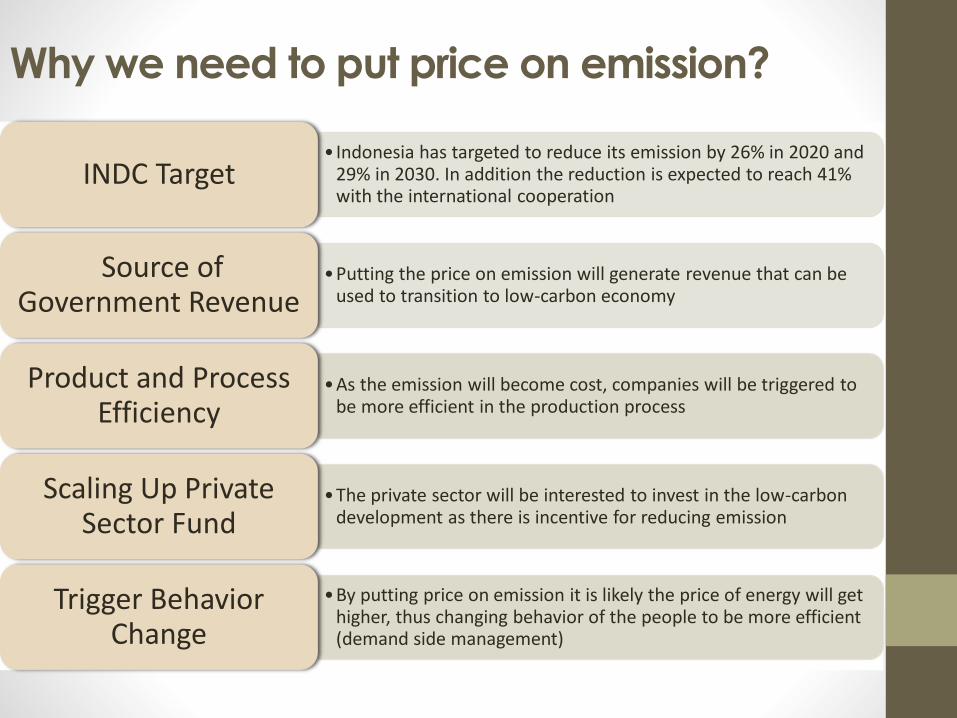

• Indonesia has targeted to reduce its emission by 26% in 2020 and 29% in 2030. In addition the reduction is expected to reach 41% with the international cooperation

INDC Target

•Putting the price on emission will generate revenue that can be used to transition to low-carbon economy

Source of Government Revenue

•As the emission will become cost, companies will be triggered to be more efficient in the production process

Product and Process Efficiency

•The private sector will be interested to invest in the low-carbon development as there is incentive for reducing emission

Scaling Up Private Sector Fund

•By putting price on emission it is likely the price of energy will get higher, thus changing behavior of the people to be more efficient (demand side management)

Trigger Behavior Change

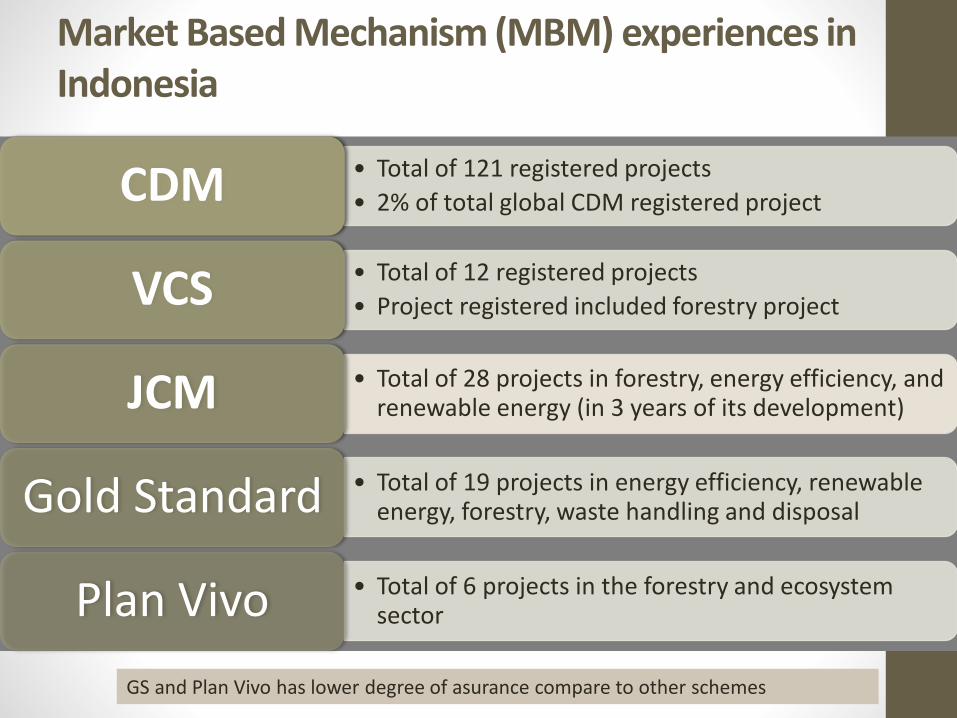

Market Based Mechanism (MBM) experiences in Indonesia

• Total of 121 registered projects

• 2% of total global CDM registered projectCDM

• Total of 12 registered projects

• Project registered included forestry project VCS

• Total of 28 projects in forestry, energy efficiency, and renewable energy (in 3 years of its development)JCM

• Total of 19 projects in energy efficiency, renewable energy, forestry, waste handling and disposalGold Standard

• Total of 6 projects in the forestry and ecosystem sectorPlan Vivo

GS and Plan Vivo has lower degree of asurance compare to other schemes

Other Indonesia’s initiatives in market based mechanism

• Indonesia was one of the first countries who join this initiative in 2010.

• Currently still in the implementation preparation stage.PMR

• Indonesia actively involved in Asia Pacific Carbon Market Roundtable initiated by New Zealand.

• The roundtable is intended to seek the possibilities of regional market based cooperation.APCMR

• The newest international initiatives on market based mechanism dialogue initiated by G7 countries.

• This is a high level dialogue and discussion intended to create common understanding in the MBM implementation.

Carbon Market Platform

• The declaration was made to support the Paris Agreement implementation.

• Support a strong role for carbon markets to enhance the ambition and facilitate the delivery of mitigation under the Paris Agreement.

• Committed to environmental integrity, transparency and the avoidance of double counting when market mechanisms are used

MinistrialDeclaration on Carbon Market

Market based mechanism types

• Clean development Mechanism (CDM)

• Joint Implementation

• Emission Trading Scheme (ETS)

• Crediting scheme (VCS, JCM, plan vivo, CCB)

• Carbon tax

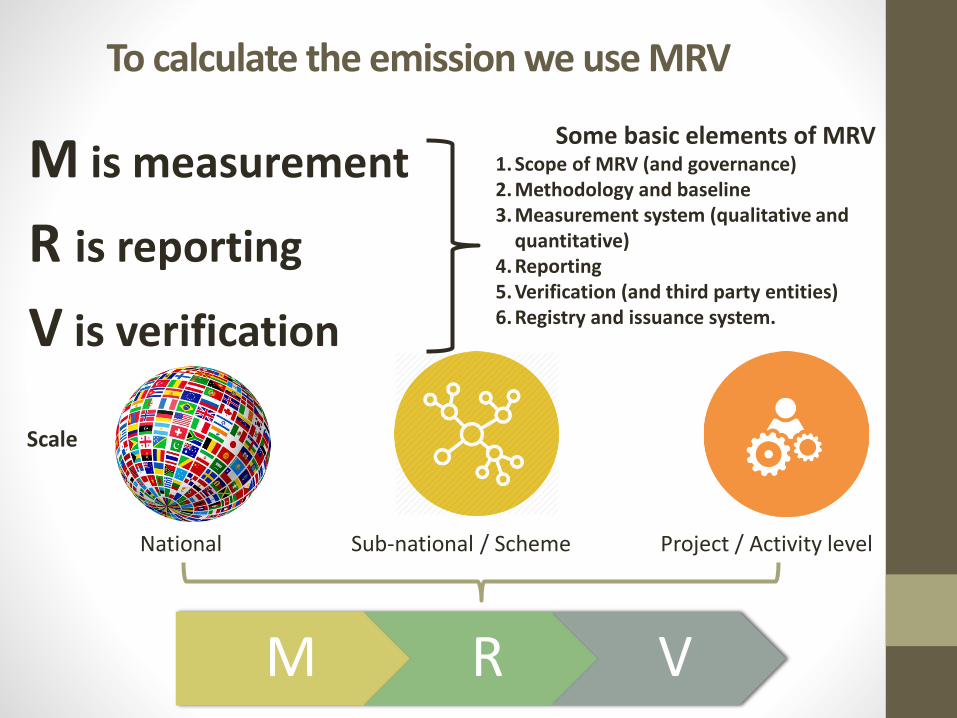

To calculate the emission we use MRV

M is measurement

R is reporting

V is verification

National Sub-national / Scheme Project / Activity level

M R V

Scale

Some basic elements of MRV1. Scope of MRV (and governance)2. Methodology and baseline3. Measurement system (qualitative and

quantitative)4. Reporting5. Verification (and third party entities)6. Registry and issuance system.

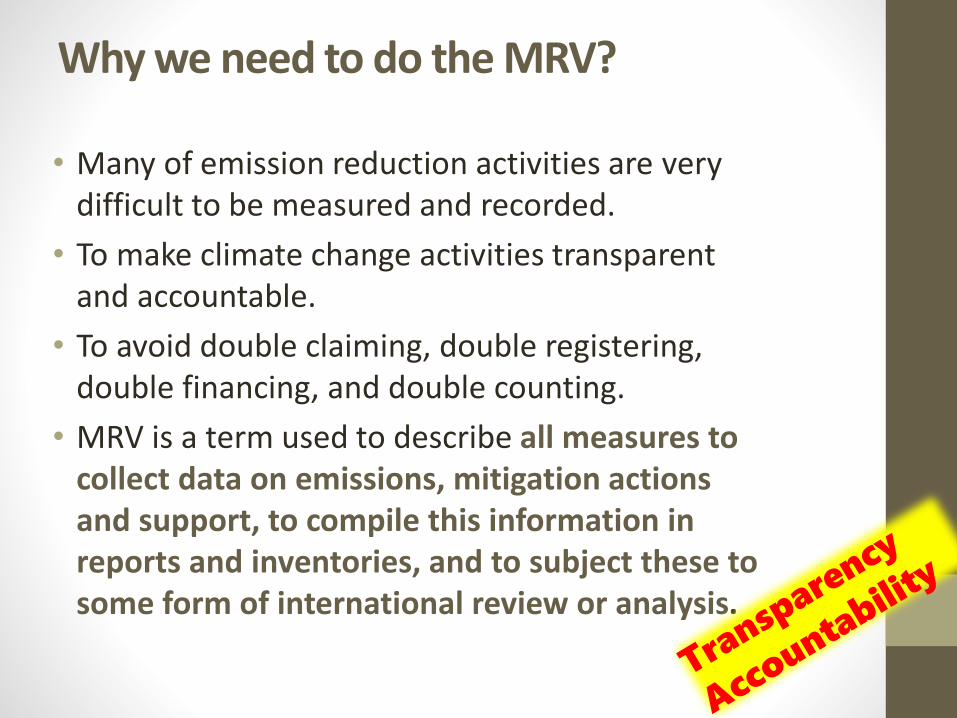

Why we need to do the MRV?

• Many of emission reduction activities are very difficult to be measured and recorded.

• To make climate change activities transparent and accountable.

• To avoid double claiming, double registering, double financing, and double counting.

• MRV is a term used to describe all measures to collect data on emissions, mitigation actions and support, to compile this information in reports and inventories, and to subject these to some form of international review or analysis.

Example: MRV in national level

What is measurement?• GHG emission and removal by sink.• Emission reduction associated with mitigation actions compared to a baseline scenario.• Progress in achieving climate change mitigation and adaptation, achievement of

sustainable development goals and co-benefit.• Support received (finance, technology, and capacity building.• Progress with implementation.

What is report?• Data on GHG emissions and removals by sinks.• Data on emissions reductions associated with mitigation actions compared to a baseline

scenario.• Progress with implementation of the mitigations actions.• Key assumptions and methodologies.• Sustainability objectives, coverage, institutional arrangements, and activities.• Information on constraints and gaps as well support needed and received.

What is verification?• All qualitative and quantitative information reported, in the BUR, on national GHG

emissions and removals, mitigations actions and its effects, together with support needed and received.

• Data maybe verified through national MRV where appropriate.

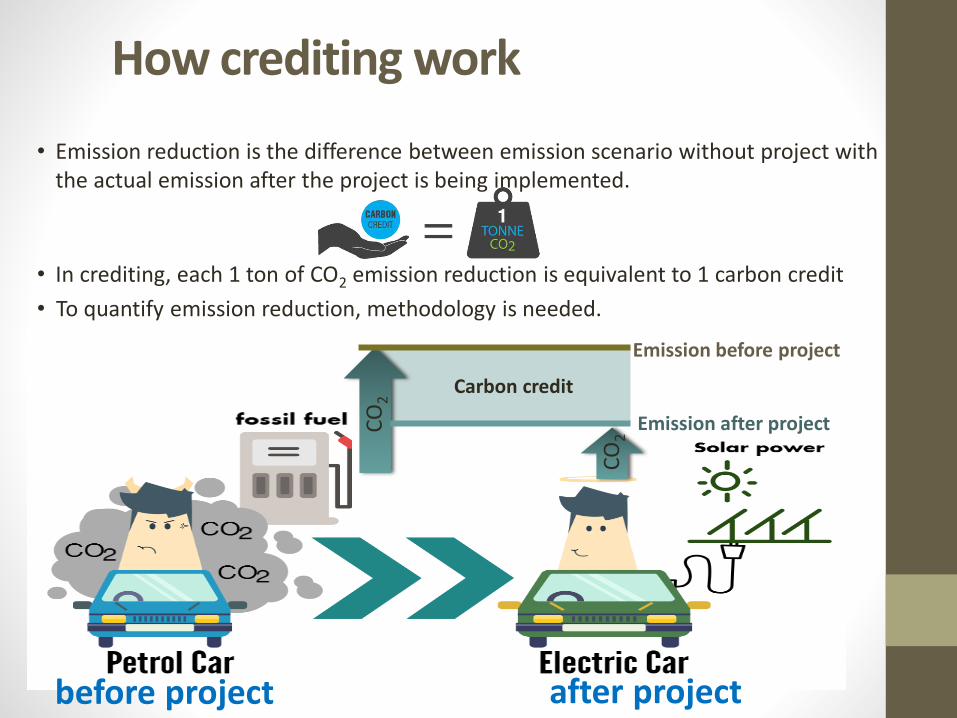

How crediting work

• Emission reduction is the difference between emission scenario without project with the actual emission after the project is being implemented.

• In crediting, each 1 ton of CO2 emission reduction is equivalent to 1 carbon credit

Emission before project

Emission after project

Carbon credit

before project after project

CO

2

CO

2

• To quantify emission reduction, methodology is needed.

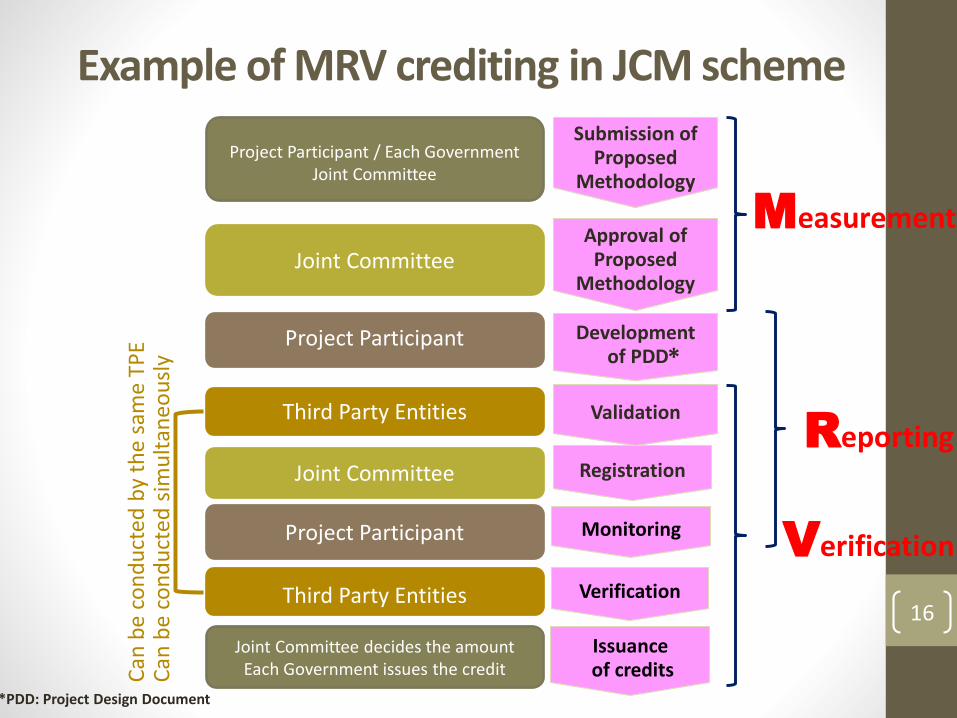

Example of MRV crediting in JCM scheme

*PDD: Project Design Document

Submission of Proposed

Methodology

Approval of Proposed

Methodology

Developmentof PDD

Validation

Registration

Monitoring

Verification

Issuanceof credits

Project Participant / Each GovernmentJoint Committee

Joint Committee

Project Participant

Third Party Entities

Joint Committee

Project Participant

Third Party Entities

Joint Committee decides the amountEach Government issues the creditC

an b

e co

nd

uct

ed b

y th

e sa

me

TPE

Can

be

con

du

cted

sim

ult

aneo

usl

y *

Measurement

Reporting

Verification

16

JCM Indonesia infrastructures development

Guideline:1. Project Design

Document2. Proposed

Methodology3. Third Party Entity4. Validation and

Verification5. Sustainable

Development Implementation Plan and Report (Indonesia’s specific JCM guidelines )

Procedure: Project Cycle Procedure

Rules: 1. Rules of Implementation2. Rules of Procedure for JC

Since JCM establishment in 2013, it has developed several guidelines, procedure, rules, registry system and methodologies

Registry system:We have developed the first climate change mitigation

registry system in Indonesia, and it is expected to connect with the National Registry

Methodologies:10 methodologies of energy efficiencies and

renewable energy have been developed

ISO 1

40

65

base

d

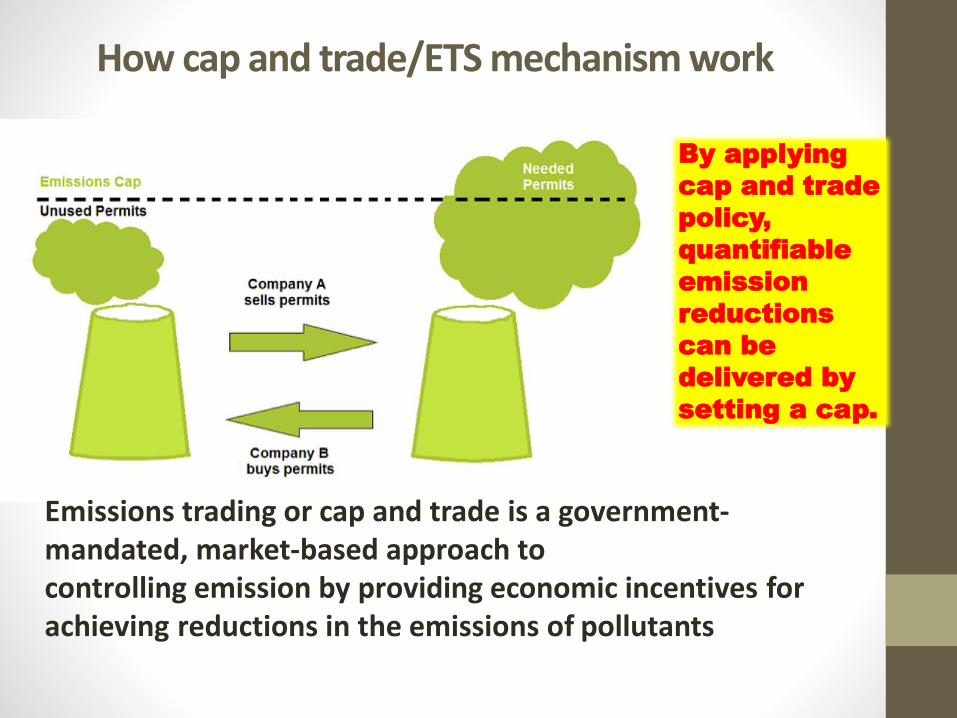

How cap and trade/ETS mechanism work

Emissions trading or cap and trade is a government-mandated, market-based approach to controlling emission by providing economic incentives for achieving reductions in the emissions of pollutants

By applying

cap and trade

policy,

quantifiable

emission

reductions

can be

delivered by

setting a cap.

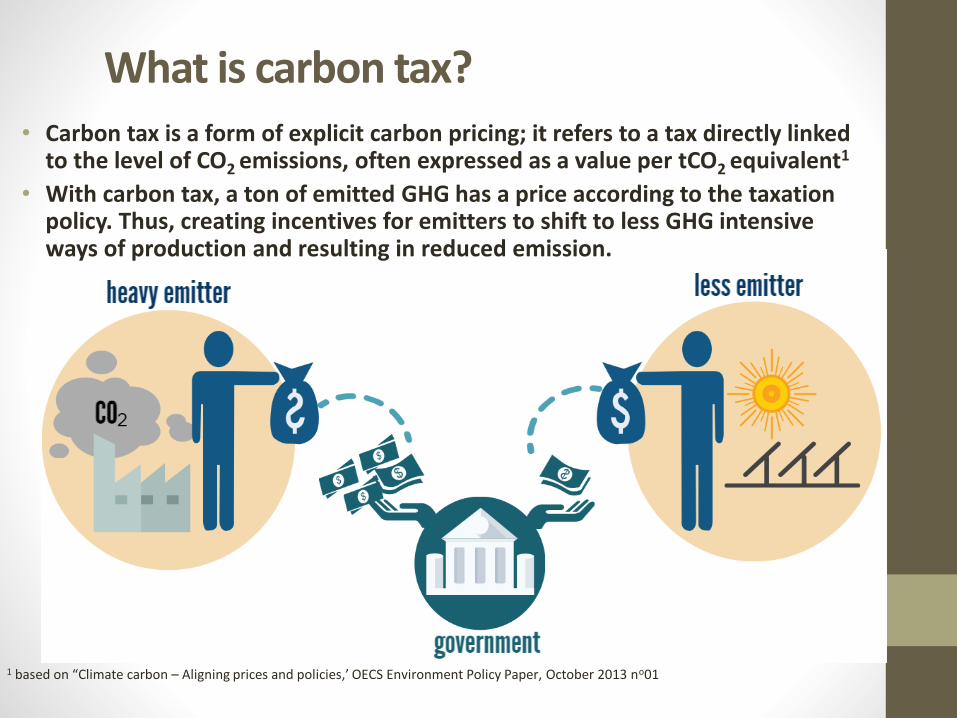

What is carbon tax?• Carbon tax is a form of explicit carbon pricing; it refers to a tax directly linked

to the level of CO2 emissions, often expressed as a value per tCO2 equivalent1

• With carbon tax, a ton of emitted GHG has a price according to the taxation policy. Thus, creating incentives for emitters to shift to less GHG intensive ways of production and resulting in reduced emission.

1 based on “Climate carbon – Aligning prices and policies,’ OECS Environment Policy Paper, October 2013 no01

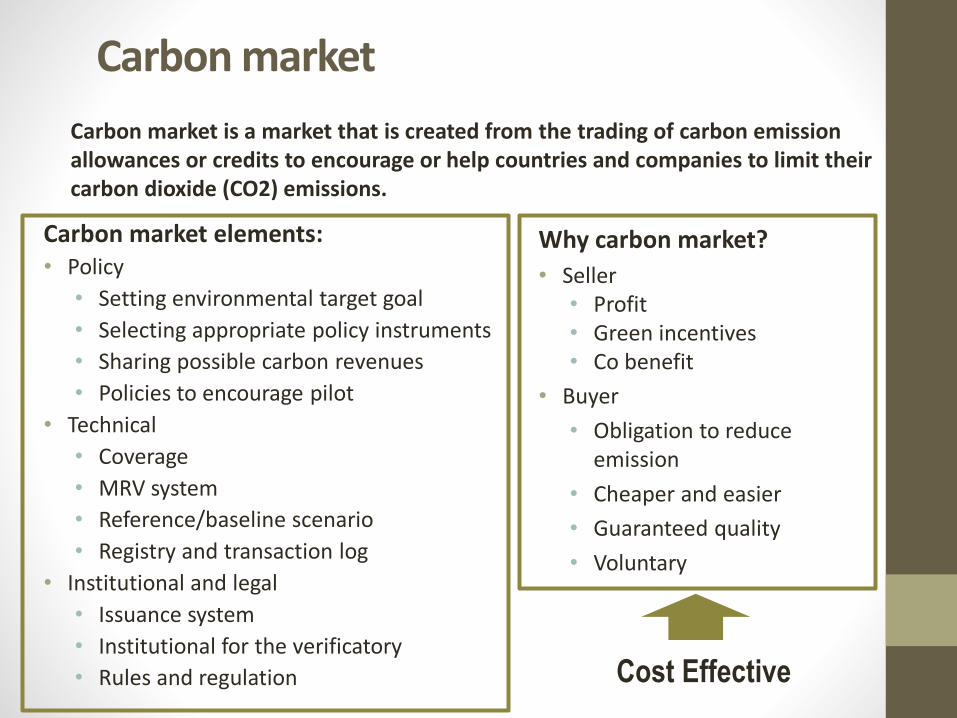

Carbon market

Carbon market elements:• Policy

• Setting environmental target goal

• Selecting appropriate policy instruments

• Sharing possible carbon revenues

• Policies to encourage pilot

• Technical

• Coverage

• MRV system

• Reference/baseline scenario

• Registry and transaction log

• Institutional and legal

• Issuance system

• Institutional for the verificatory

• Rules and regulation

Carbon market is a market that is created from the trading of carbon emission allowances or credits to encourage or help countries and companies to limit their carbon dioxide (CO2) emissions.

Why carbon market?

• Seller• Profit• Green incentives• Co benefit

• Buyer

• Obligation to reduce emission

• Cheaper and easier

• Guaranteed quality

• Voluntary

Cost Effective

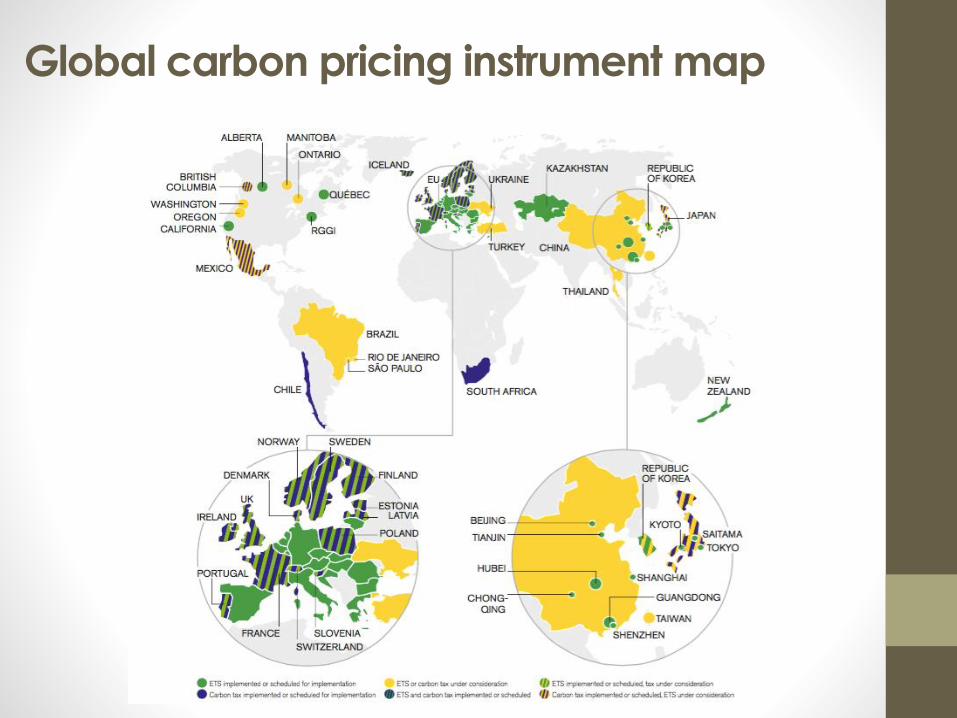

Global carbon pricing instrument map

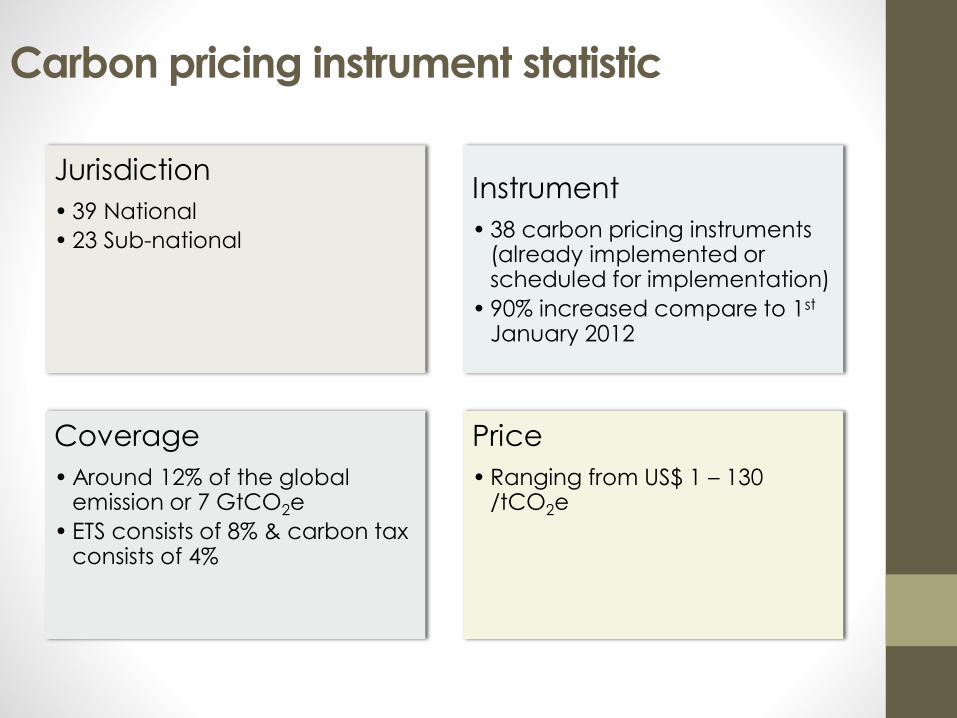

Carbon pricing instrument statistic

Jurisdiction

• 39 National

• 23 Sub-national

Instrument

• 38 carbon pricing instruments (already implemented or scheduled for implementation)

• 90% increased compare to 1st

January 2012

Coverage

• Around 12% of the global emission or 7 GtCO2e

• ETS consists of 8% & carbon tax consists of 4%

Price

• Ranging from US$ 1 – 130 /tCO2e

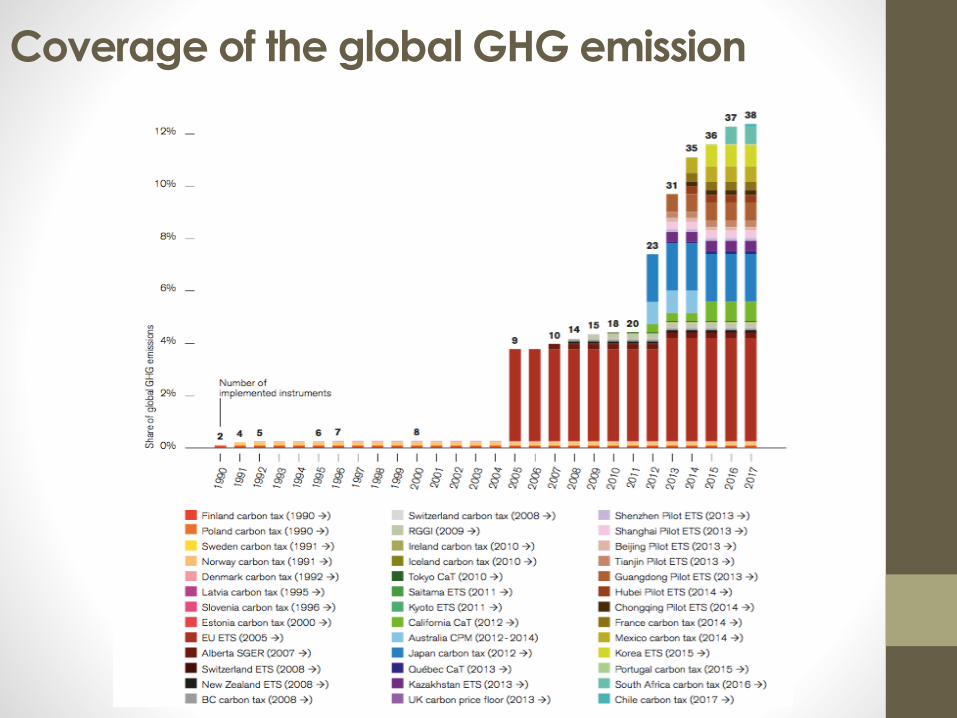

Coverage of the global GHG emission

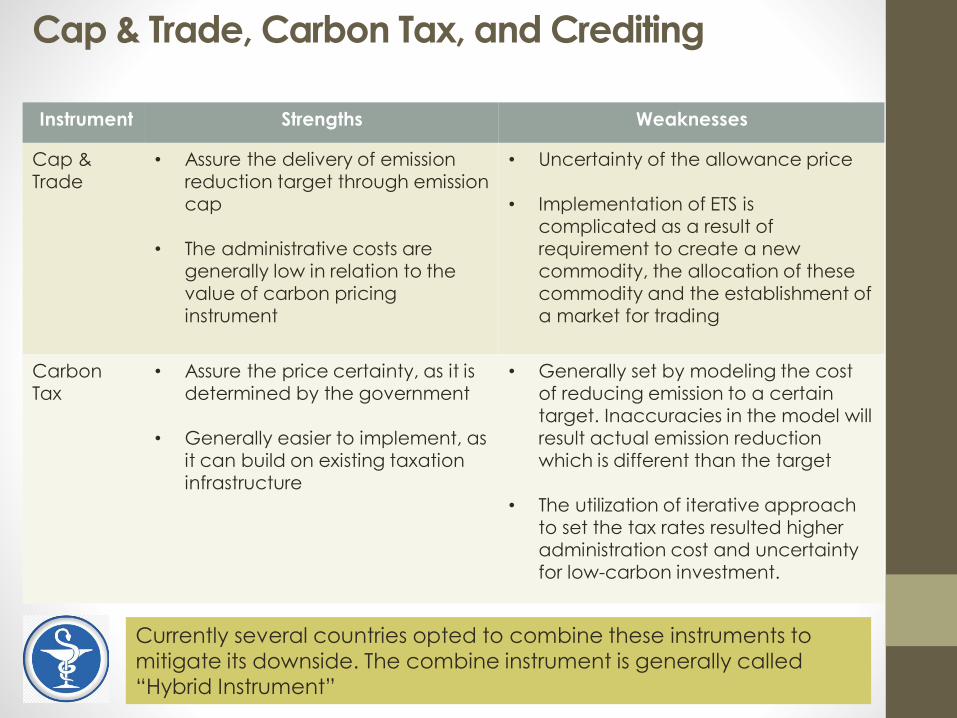

Instrument Strengths Weaknesses

Cap &

Trade

• Assure the delivery of emission

reduction target through emission

cap

• The administrative costs are

generally low in relation to the

value of carbon pricing

instrument

• Uncertainty of the allowance price

• Implementation of ETS is

complicated as a result of

requirement to create a new

commodity, the allocation of these

commodity and the establishment of

a market for trading

Carbon

Tax

• Assure the price certainty, as it is

determined by the government

• Generally easier to implement, as

it can build on existing taxation

infrastructure

• Generally set by modeling the cost

of reducing emission to a certain

target. Inaccuracies in the model will

result actual emission reduction

which is different than the target

• The utilization of iterative approach

to set the tax rates resulted higher

administration cost and uncertainty

for low-carbon investment.

Currently several countries opted to combine these instruments to

mitigate its downside. The combine instrument is generally called

“Hybrid Instrument”

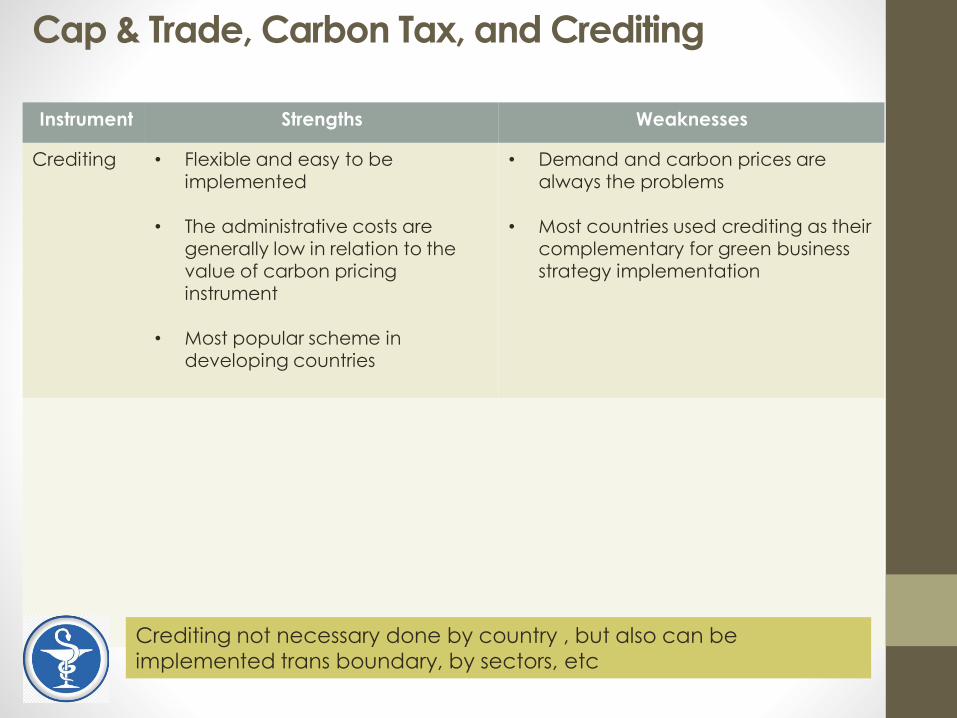

Cap & Trade, Carbon Tax, and Crediting

Cap & Trade, Carbon Tax, and Crediting

Instrument Strengths Weaknesses

Crediting • Flexible and easy to be

implemented

• The administrative costs are

generally low in relation to the

value of carbon pricing

instrument

• Most popular scheme in

developing countries

• Demand and carbon prices are

always the problems

• Most countries used crediting as their

complementary for green business

strategy implementation

Crediting not necessary done by country , but also can be

implemented trans boundary, by sectors, etc

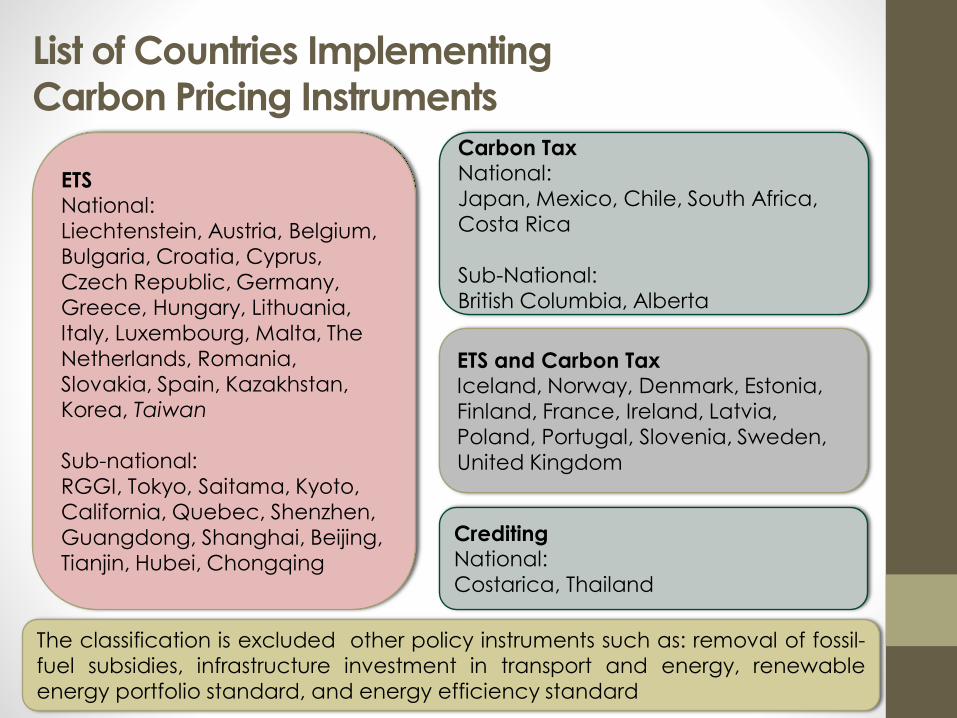

List of Countries Implementing

Carbon Pricing InstrumentsCarbon Tax National:

Japan, Mexico, Chile, South Africa,

Costa Rica

Sub-National:

British Columbia, Alberta

ETSNational:

Liechtenstein, Austria, Belgium,

Bulgaria, Croatia, Cyprus,

Czech Republic, Germany,

Greece, Hungary, Lithuania,

Italy, Luxembourg, Malta, The

Netherlands, Romania,

Slovakia, Spain, Kazakhstan,

Korea, Taiwan

Sub-national:

RGGI, Tokyo, Saitama, Kyoto,

California, Quebec, Shenzhen,

Guangdong, Shanghai, Beijing,

Tianjin, Hubei, Chongqing

ETS and Carbon TaxIceland, Norway, Denmark, Estonia,

Finland, France, Ireland, Latvia,

Poland, Portugal, Slovenia, Sweden,

United Kingdom

The classification is excluded other policy instruments such as: removal of fossil-

fuel subsidies, infrastructure investment in transport and energy, renewable

energy portfolio standard, and energy efficiency standard

Crediting National:

Costarica, Thailand

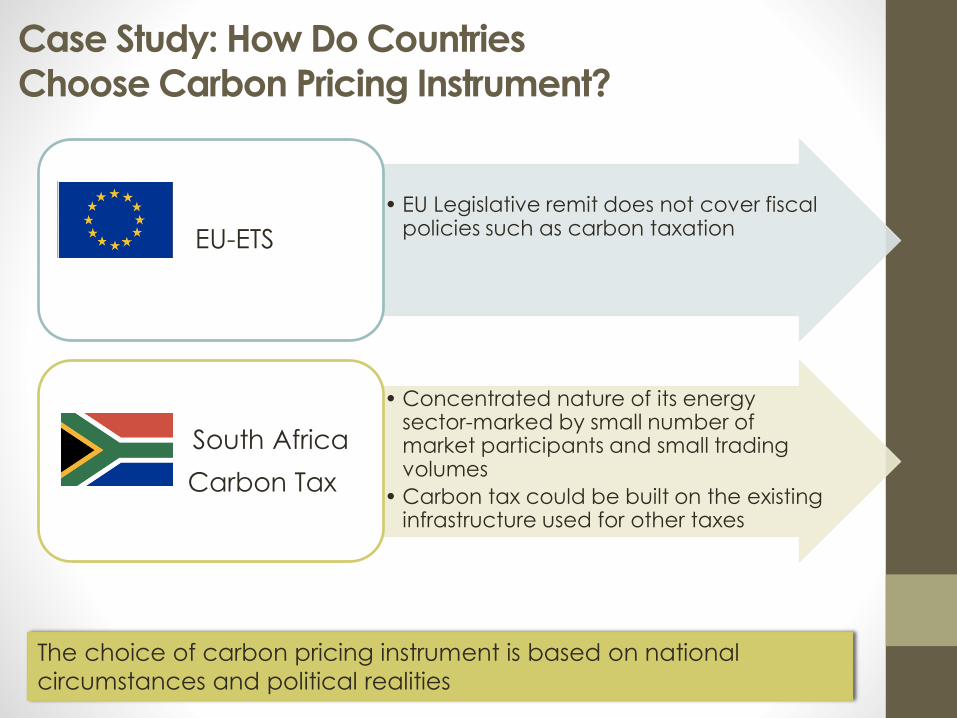

Case Study: How Do Countries

Choose Carbon Pricing Instrument?

• EU Legislative remit does not cover fiscal policies such as carbon taxation

EU-ETS

• Concentrated nature of its energy sector-marked by small number of market participants and small trading volumes

• Carbon tax could be built on the existing infrastructure used for other taxes

South Africa

Carbon Tax

The choice of carbon pricing instrument is based on national

circumstances and political realities

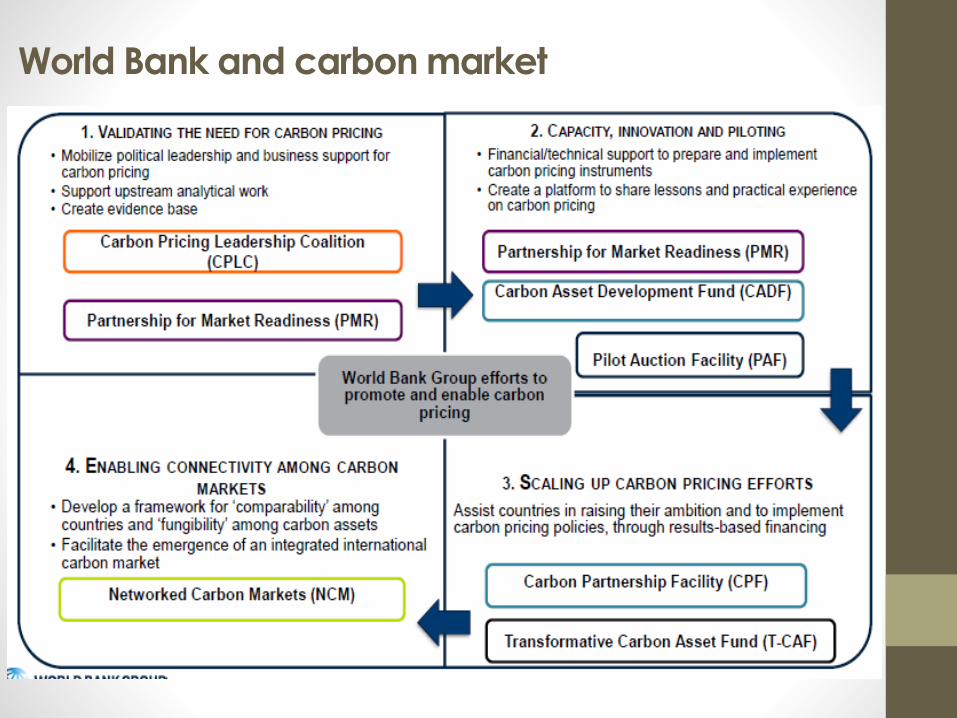

World Bank and carbon market

Partnership for Market Readiness

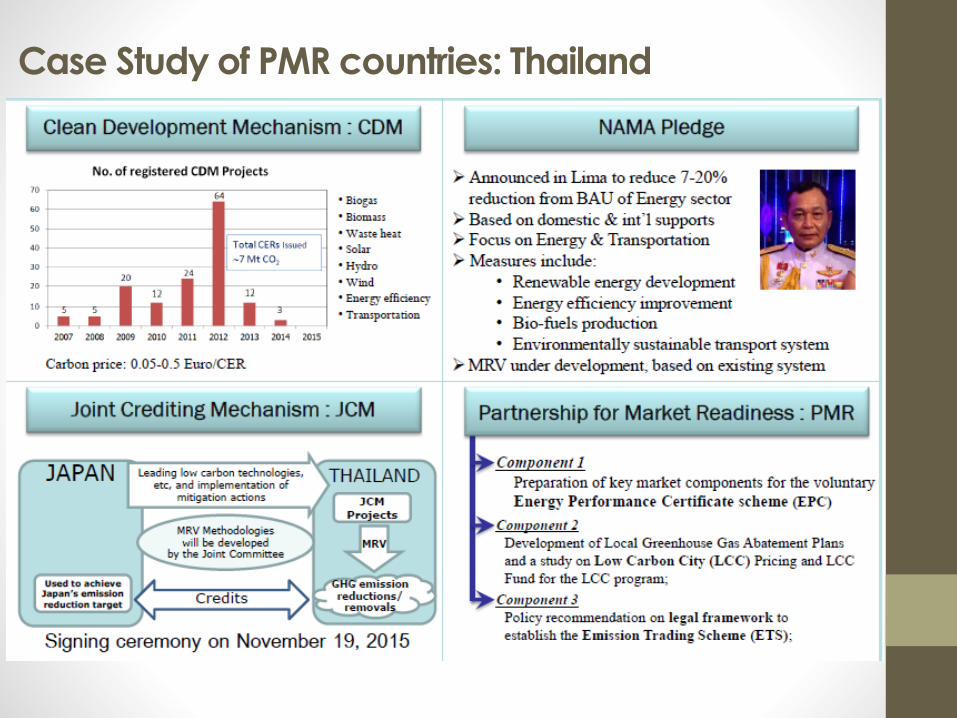

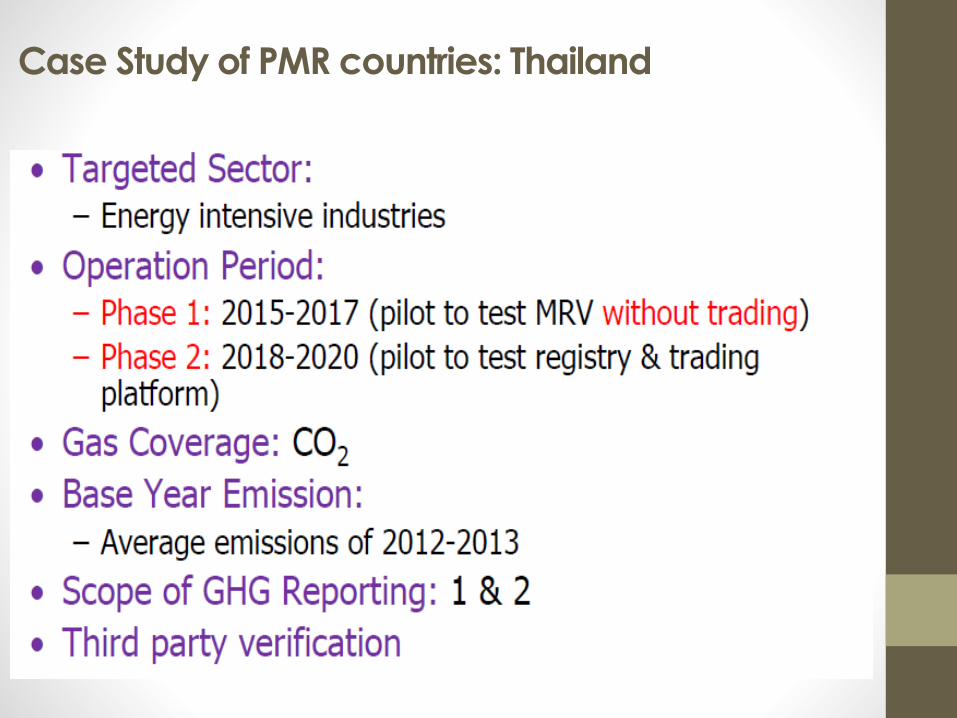

Case Study of PMR countries: Thailand

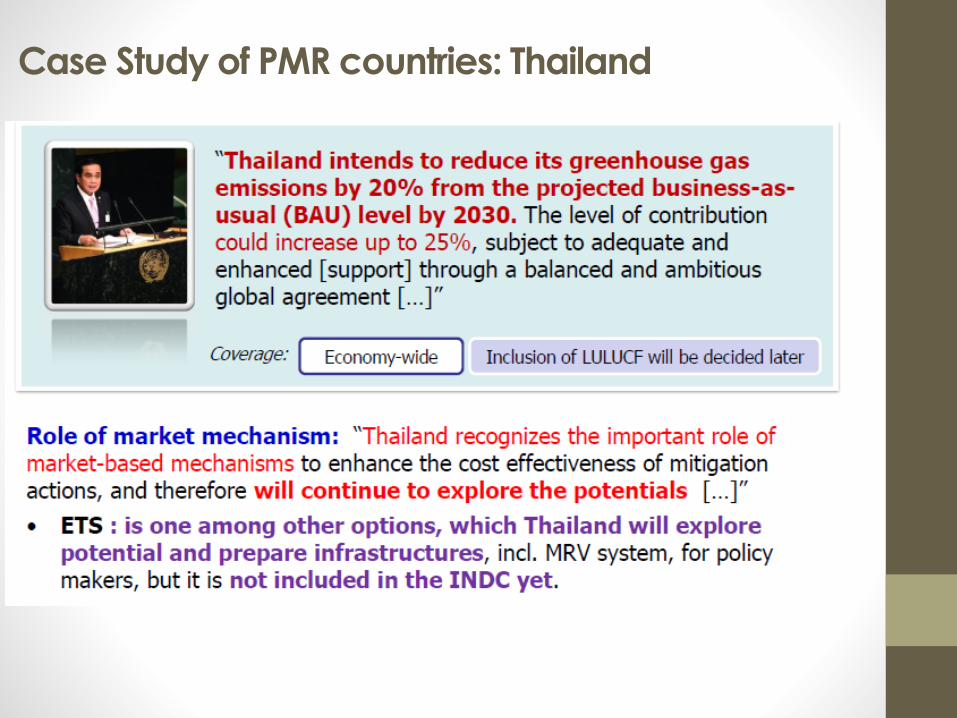

Case Study of PMR countries: Thailand

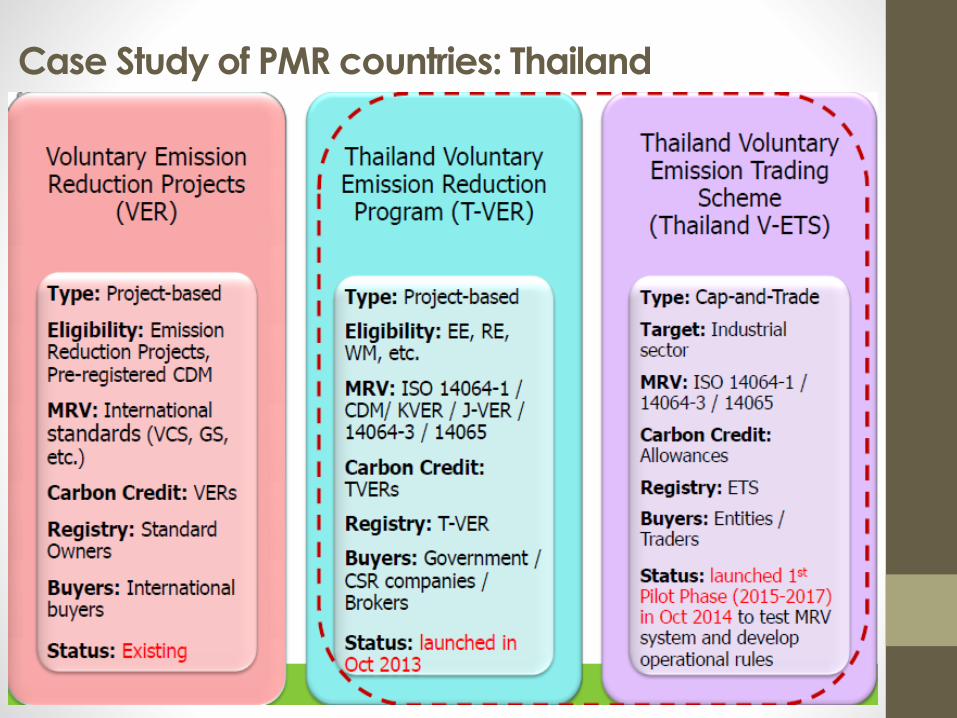

Case Study of PMR countries: Thailand

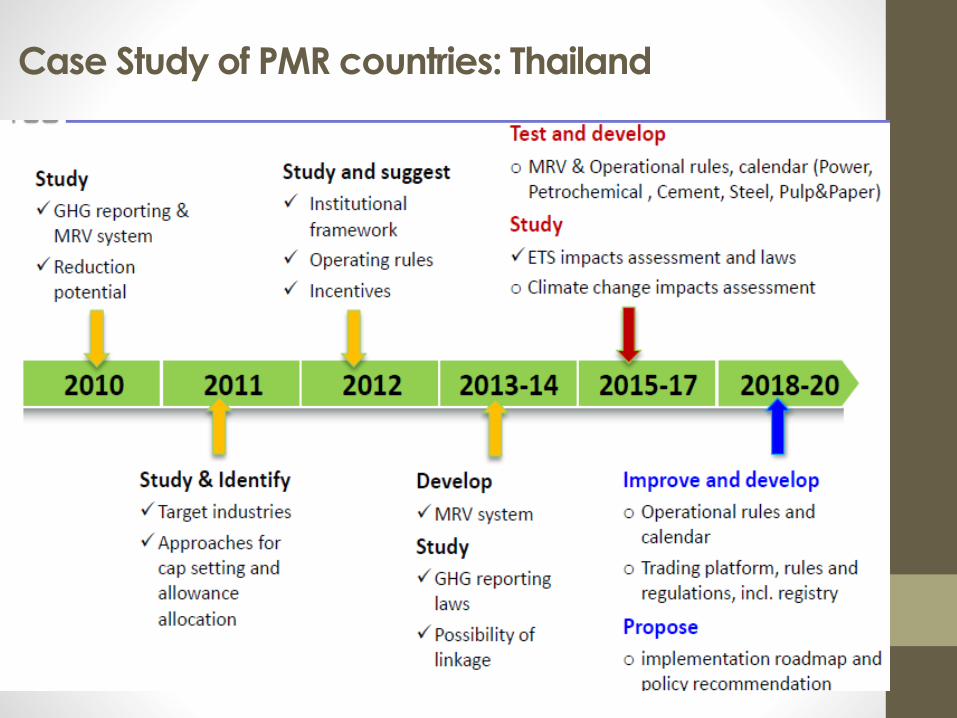

Case Study of PMR countries: Thailand

Case Study of PMR countries: Thailand

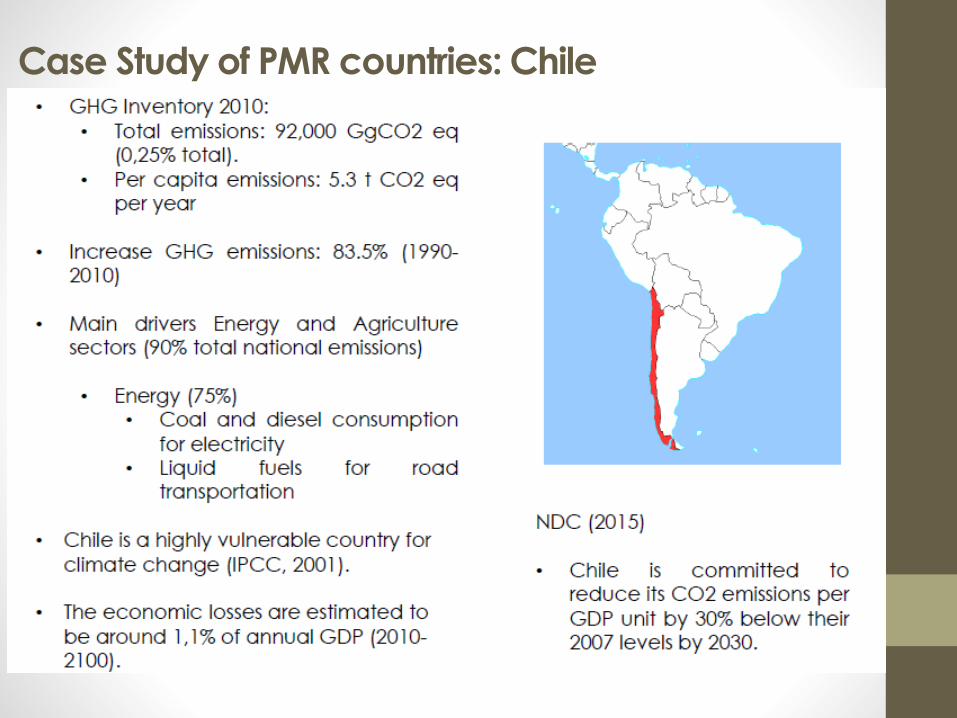

Case Study of PMR countries: Chile

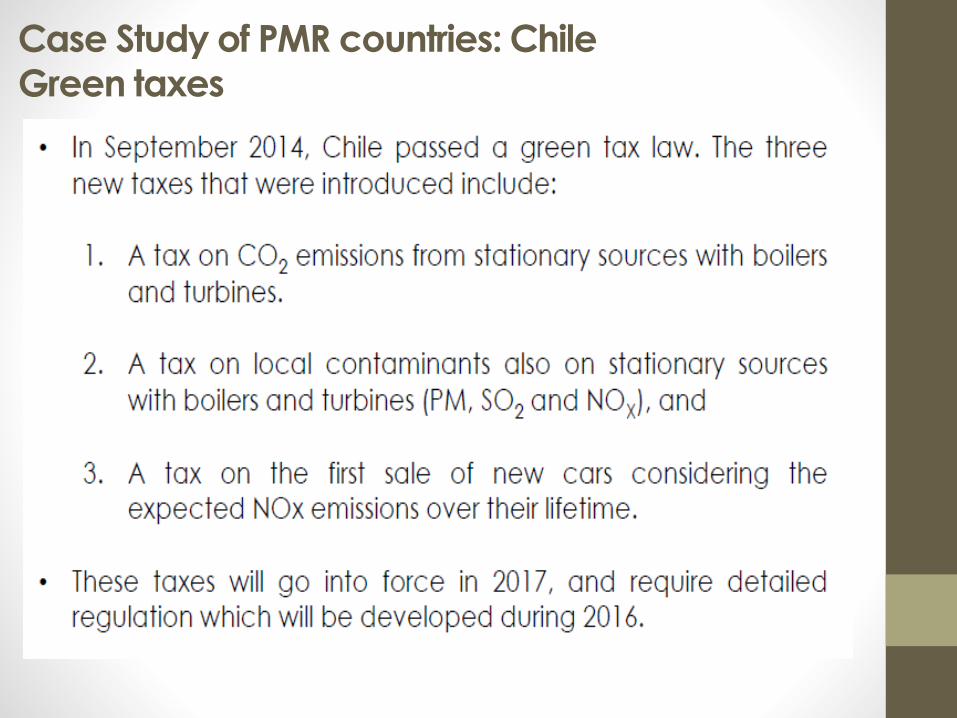

Case Study of PMR countries: Chile

Green taxes

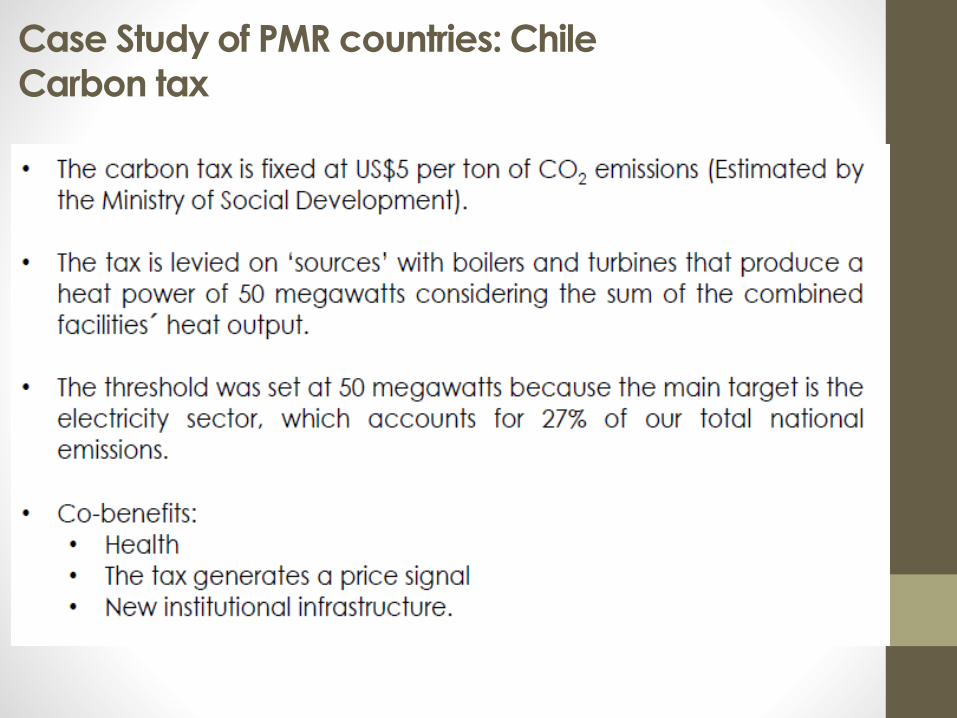

Case Study of PMR countries: Chile

Carbon tax

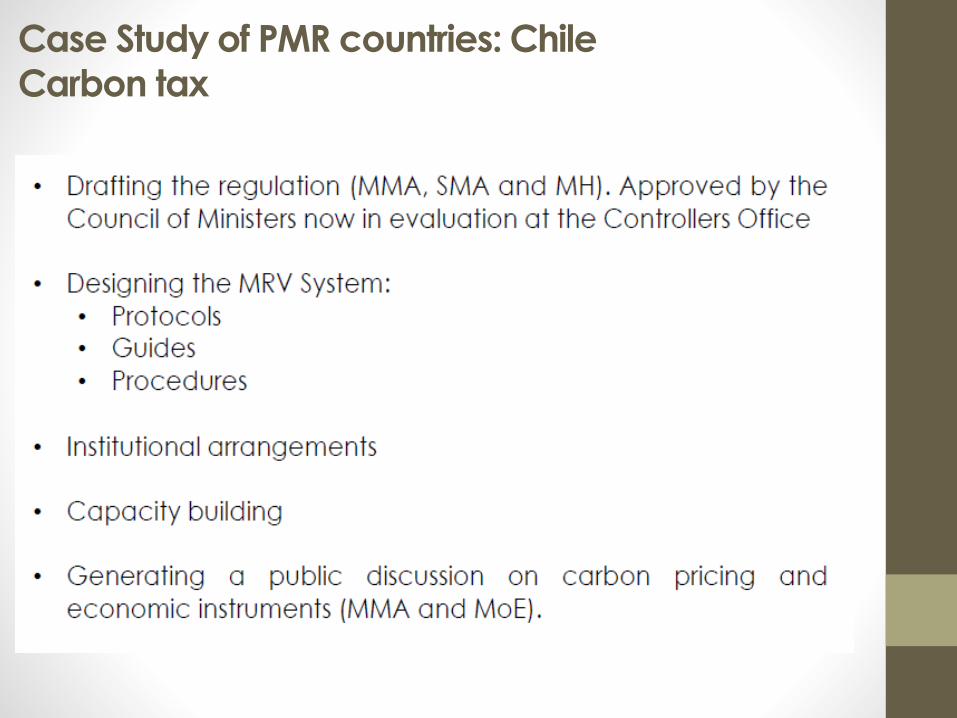

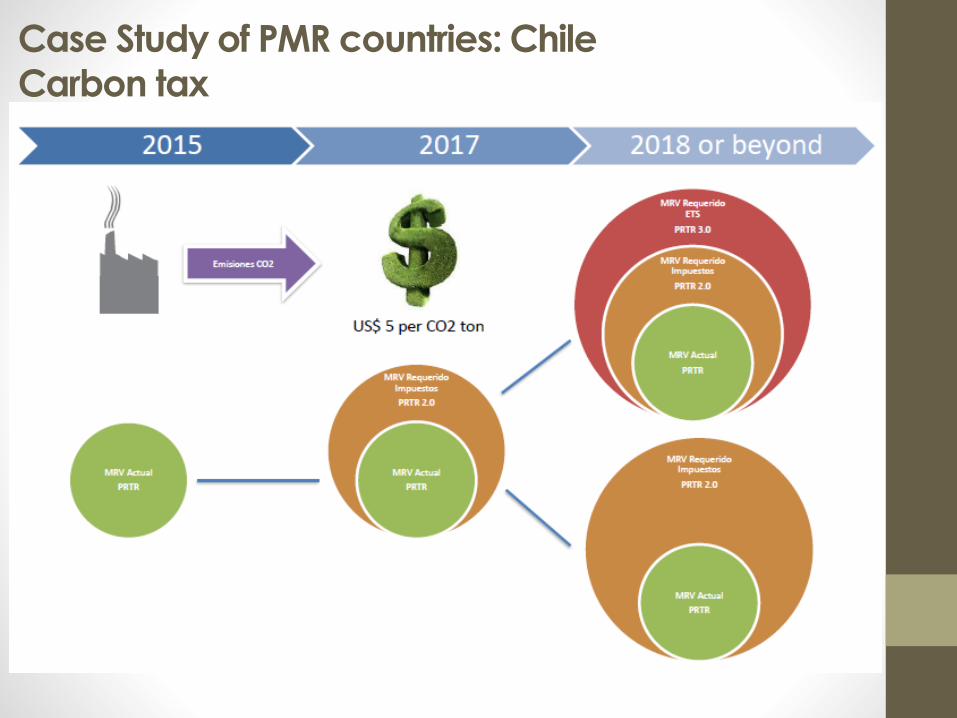

Case Study of PMR countries: Chile

Carbon tax

Case Study of PMR countries: Chile

Carbon tax

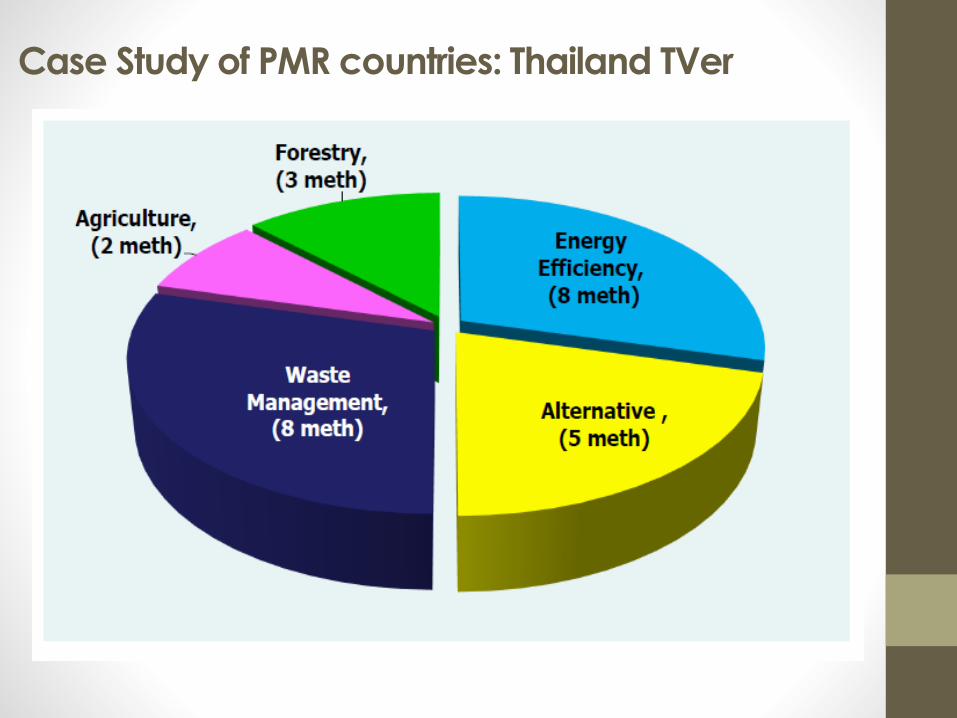

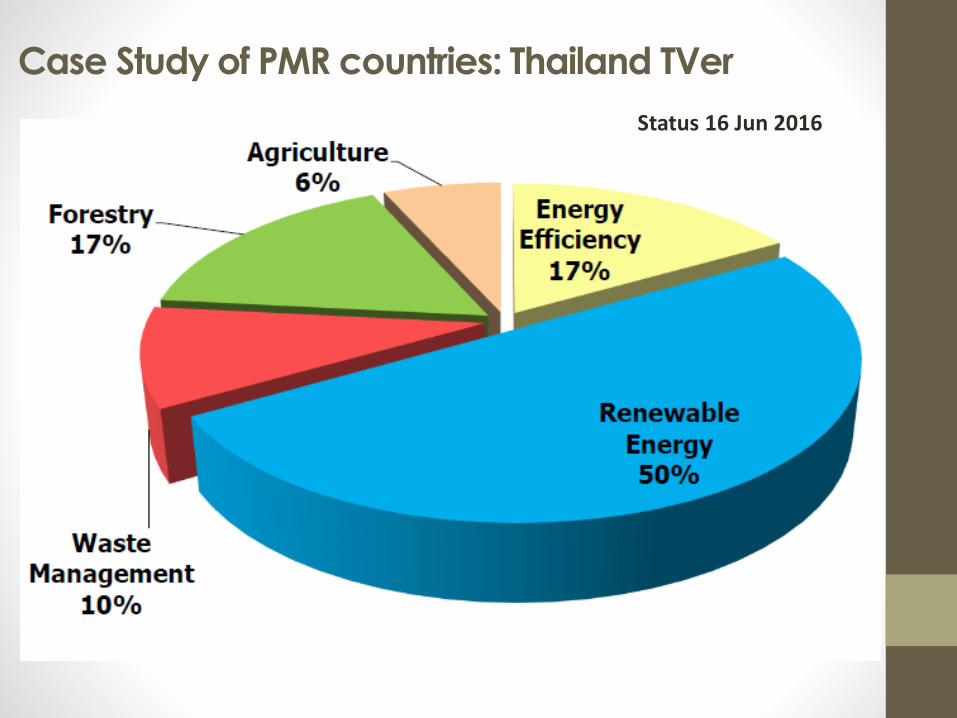

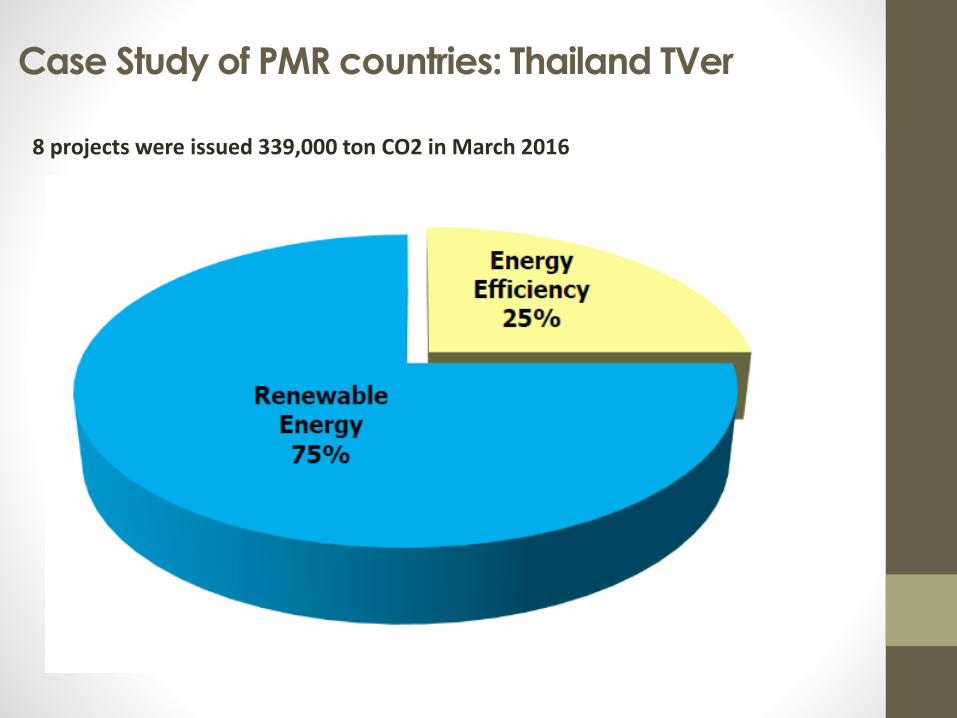

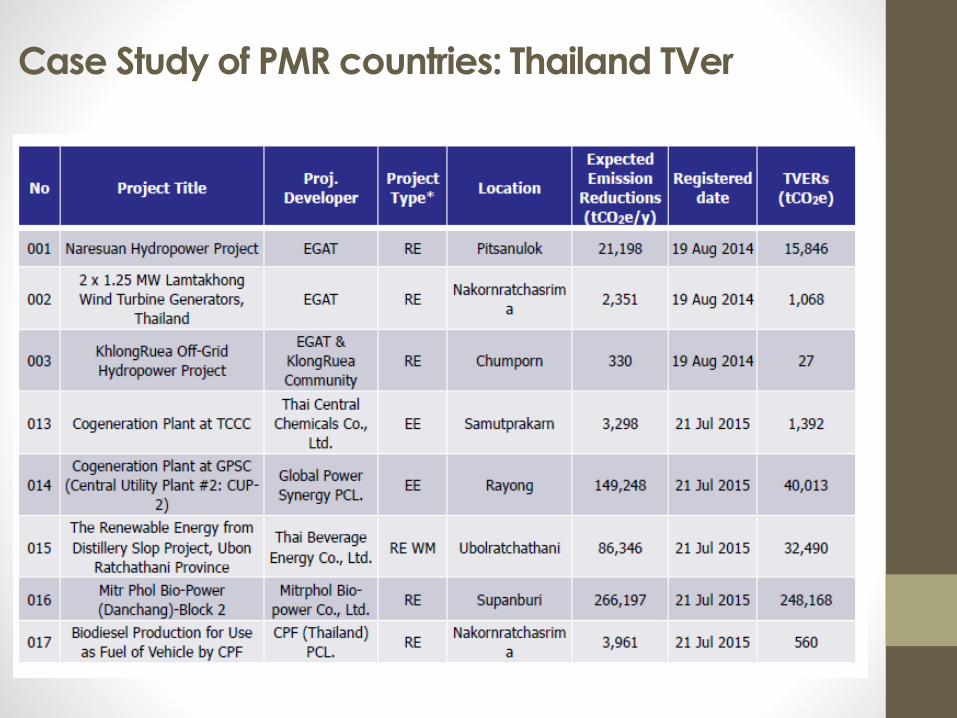

Case Study of PMR countries: Thailand TVer

Case Study of PMR countries: Thailand TVer

Case Study of PMR countries: Thailand TVer

Status 16 Jun 2016

Case Study of PMR countries: Thailand TVer

8 projects were issued 339,000 ton CO2 in March 2016

Case Study of PMR countries: Thailand TVer

Conclusion• Market based mechanism implementation is “a must do”

action if we want to reduce emission in an effective and cost efficient way.

• Country may choose their preferences of the market based mechanism scheme that can be implemented in their region.

• Carbon tax is the most feasible to implement in Indonesia as it does not require complicated infrastructure

• The implementation of the taxes, however have to be done gradually to increase the reception from all sectors

• It is required to provide assistance for the energy intensive industry as it will be hit the hardest by the implementation of carbon tax

• Crediting scheme can be the second choice to be implemented.

• Indonesia can start the crediting scheme by implementing domestic scheme.

• The biggest challenge for crediting is to create the demand.

References

1. Atika, Ratu Keni, MRV in MBM presentation 2016

2. Chile delegation presentation at APCMR Meeting Santiago, 2016

3. Setiawati, Rini, Carbon Tax presentation, 2016

4. Thailand delegation presentation at APCMR Meeting Santiago, 2016

5. World Bank PMR Annual Report 2015

![Higgs Mechanism at Finite Chemical Potential with Type-II ...€¦ · Higgs Mechanism at Finite Chemical Potential with Type-II Nambu-Goldstone Boson Based on arXiv:1102.4145v2 [hep-ph]](https://img.pdfslide.net/doc/110x75/5ec11d8f7d70e4118c52cb65/higgs-mechanism-at-finite-chemical-potential-with-type-ii-higgs-mechanism-at.jpg)